STUDY MATERIAL FOR BBA FINANCIAL SERVICES SEMESTER - …

40

STUDY MATERIAL FOR BBA FINANCIAL SERVICES SEMESTER - IV, ACADEMIC YEAR 2020-21 Page 1 of 40 UNIT CONTENT PAGE Nr I CONCEPT OF FINANCIAL SERVICES 02 II FUND BASED FINANCIAL SERVICES 10 III MEANING OF MUTUAL FUNDS 14 IV FACTORING 20 V MERCHANT BANKING 34

Transcript of STUDY MATERIAL FOR BBA FINANCIAL SERVICES SEMESTER - …

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 1 of 40

UNIT CONTENT PAGE Nr

I CONCEPT OF FINANCIAL SERVICES 02

II FUND BASED FINANCIAL SERVICES 10

III MEANING OF MUTUAL FUNDS 14

IV FACTORING 20

V MERCHANT BANKING 34

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 2 of 40

UNIT - I Concept of Financial services:

Financial services are intermediary services in financial market place.Financial Services are provided by the banks and financial institution in financial system. It is a process by which funds are mobilised from a large number of savers and made available to all those who are in need. It is defined as all activities, benefits and satisfactions connected with sale of money, that offers to users and customers financial related value. Objectives of financial services are

Maintain the public’s confidence in the financial system; Facilitate the deterrence of financial crimes; Supervise financial services licensees in accordance with legislation, regulations and

codes; Ensure periodic evaluation of the legislative and regulatory framework in accordance

with developments in the financial services sector; Promote best practices, mutual assistance and exchange of information by maintaining

contact and forging relations with foreign regulatory authorities, international associations of regulatory authority bodies or groups relevant to its functions;

Facilitate the development of the financial services sector. Functions of financial system

Financial system works as an effective conduit for optimum allocation of financial resources inan economy.

It helps in establishing a link between the savers and the investors. Financial system allows ‘asset-liability transformation’. Banks create claims (liabilities)

against themselves when they accept deposits from customers but also create assets when they provide loans to clients.

Economic resources (i.e., funds) are transferred from one party to another through financialsystem.

The financial system ensures the efficient functioning of the payment mechanism in aneconomy. All transactions between the buyers and sellers of goods and services are effectedsmoothly because of financial system.

Financial system helps in risk transformation by diversification, as in case of mutual funds.

Financial system enhances liquidity of financial claims. Financial system helps price discovery of financial assets resulting from the interaction

ofbuyers and sellers. For example, the prices of securities are determined by demand and supplyforces in the capital market.

Financial system helps reducing the cost of transactions.

Financial markets play a significant role in economic growth through their role of allocation capital, monitoring managers, mobilizing of savings and promoting technological changes among others. Economists had held the view that the development of the financial sector is a crucial element for stimulating economic growth. Financial development can be defined as the ability of a financial sector acquire effectively information, enforce contracts, facilitate transactions and create incentives for the emergence of particular types of financial contracts, markets and intermediaries, and all should be at a low cost. Financial development occurs when financial instruments, markets and intermediaries ameliorate through the basis of information, enforcement and transaction costs, and therefore better provide financial services.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 3 of 40

The financial functions or services may influence saving and investment decisions of an economy through capital accumulation and technological innovation and hence economic growth. Capital accumulation can either be modelled through capital externalities or capital goods produced using constant returns to scale but without the use of any reproducible factors to generate steady-state per capita growth. Through capital accumulation, the functions performed by the financial system affect the steady growth rate thereby influencing the rate of capital formation. The financial system affects capital accumulation either by altering the savings rate or by reallocating savings among different capital producing levels. Through technological innovation, the focus is on the invention of new production processes and goods. Characteristics of Financial Services

Financial services are Intangible Financial services are customer oriented The production and delivery of a service are simultaneous functions therefor are

inseparable They are perishable in nature and cannot be stored They are dynamic in nature as a financial service varies with the changing requirements

of the customer and the socio-economic environment. - must be dynamic socio economic changes, disposable income

They are proactive in nature and help to visualize the expectations of the market. Financial Services Market

Financial Markets are the institutional arrangements by which savings generated in the economy are channelized into avenues of investment by industry, business and the government. It is a market for the creation and exchange of financial assets.

Functions of Financial Market 1. Mobilization of savings and channelizing them into the most productive uses:

Facilitates transfer of savings from the savers to the investors. Financial markets help people to invest their savings in various financial instruments and

earn income and capital appreciation. Facilitate mobilization of savings of people and their channelization into the most

productive uses. 2.Facilitate Price Discovery:

Price of anything depends upon the demand and supply factors. Demand and supply of financial assets and securities in financial markets help in

deciding the prices of various financial securities; where business firms represent the demand and the households represent the supply

3.Provide liquidity to financial assets:

Financial markets provide liquidity to financial instruments by providing a ready market for the sale and purchase of financial assets.

Whenever the investors want, they can invest their savings into long term investments and whenever they want, they can sell the investments/ instruments and convert them into cash.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 4 of 40

4.Reduce the cost of transactions:

By providing valuable information to buyers and sellers of financial assets, it helps to saves time, effort and money that would have been spent by them to find each other.

Also investors can buy/sell securities through brokers who charge a nominal commission for their services. These way financial markets facilitate transactions at a very low cost.

Problems of Financial Services Sector

Financial industry challenges are largely generational. The late 1800s were marked by notorious gangs that plundered banks throughout the American Wild West. The 1900s witnessed women struggling to enter the male-dominated banking industry. And now? Well, now we have digital banking. The long-held promise of digital technology to transform financial institutions has not been broken. It just hasn’t been fully kept. The digitization of the financial industry was supposed to solve problems. And it has. It has also created some new ones in the process. Challenges Facing the Financial Services Industry

We will also see how the global financial sector is doubling down on technology to find the solutions it needs not only to survive, but to thrive in the era of digital finance.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 5 of 40

1. Cybercrime in Finance

Reports of data breaches by financial services companies:

Data breaches involving financial service firms increased by 480% from 2017 to 2018. With each attack costing financial institutions millions, innovative solutions are needed if we are to avoid a repeat of the lawless days of the Wild West.

Whatever cybercrime solutions emerge to protect financial services, blockchain technology must be the foundation Period.

As more and more institutions adopt distributed ledger technology (DLT), blockchain will become the de facto solution to keeping financial data secure while at rest. Integrating DLT with existing financial infrastructures poses some serious obstacles that must be overcome. 2. Regulatory Compliance in Finance:

The ever-changing regulatory environment poses a constant challenge for financial institutions of all types.

Regtech is an emerging industry that can help ease the burden of compliance. By using the latest FinTech technologies to address regulatory compliance, RegTechstartups are bridging the gap between regulators and the financial service industry.

Automated reporting, automated audits, and process streamlining are only a few of the benefits offered by RegTech applications. 3. Big Data Use in Finance

Big data provides both opportunities and obstacles for financial service providers. Tapping into social media, consumer databases, and even news feeds can help banks better serve their customers, while better protecting their own interests.

But sorting through torrents of unstructured data for useful information is no small undertaking. It requires powerful data analytics technology if institutions are to reap a benefit.

Fortunately, data analytics solutions are emerging with the potential to transform asset management, trading, risk management, and other financial services.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 6 of 40

4. AI Use in Finance Industry experts believe that AI will transform nearly every aspect of the financial

service industry. Automated wealth management, customer verification, and open banking all provide opportunities for AI solution providers.

But that’s all been said before. So why should we expect AI to keep that promise now?

Powerful advances in deep learning technology are paving the way for AI. In fact, if you have been alerted by your bank of suspicious activity on your account, you have likely already benefited from AI.

The challenge that financial services face is learning how to benefit from the power of AI, without being victimized by it. In R&D labs across the world, that question is being pondered at this very moment.

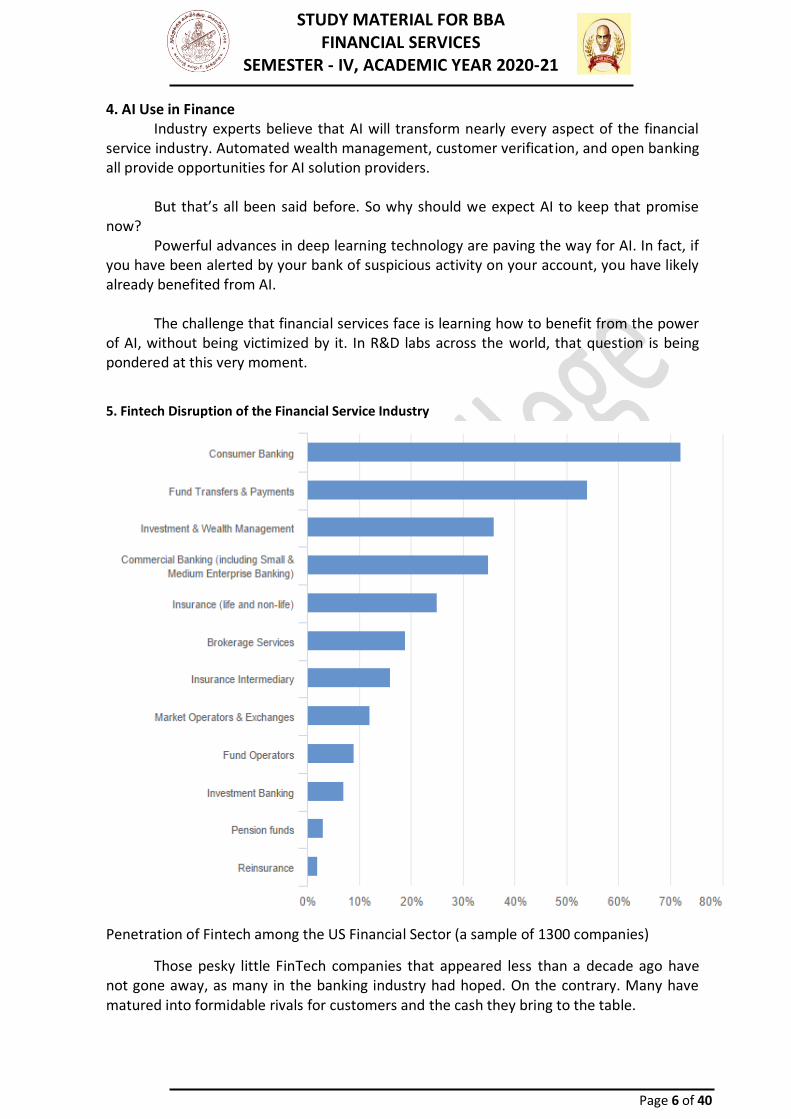

5. Fintech Disruption of the Financial Service Industry

Penetration of Fintech among the US Financial Sector (a sample of 1300 companies)

Those pesky little FinTech companies that appeared less than a decade ago have not gone away, as many in the banking industry had hoped. On the contrary. Many have matured into formidable rivals for customers and the cash they bring to the table.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 7 of 40

6. Customer Retention in the Financial Services Industry Competition for financial service clients has never been fiercer. While brand loyalty

may not be dead, it is definitely on life support.

What matters to most customers in 2019 is greater personalization, more automated services, and easier access to services. Institutions that can deliver all three will capture their share of the market.

Key to not losing the battle is recognizing that customers are less concerned with brand familiarity than getting the services they want. Providing customers those services is key to client retention. 7. Employee Retention in the Financial Service Industry

Today’s financial service companies not only find it difficult to attract customers, but they are also finding it difficult to attract employees.

A lack of qualified talent to fill new IT roles, and a millennial workforce that shuns long-term employment, are leading factors in finding good help.

Institutions that want to attract and retain a qualified workforce must change their philosophy. No longer is it enough to offer good pay and benefits; workers now expect employers to nurture a culture that is accommodating to the values and lifestyles of the employee.

Change is necessary if stable and qualified workforces are to be achieved. But don’t expect it to come easy. 8. Blockchain Integration in Finance

Blockchain is a key component in the battle against cybercrime. But data security is not the only application for blockchains in the financial sector.

Far from it, cases across the globe are already proving the value of blockchain in a wide variety of banking and investment applications. From solving challenges faced by investment banks to helping customers make safer payment transactions, the list is growing daily.

Having said that, industry-wide adoption of blockchain is unlikely to occur until we reach a tipping point in the maturity of the technology. When that will happen is anyone’s guess. 9. Customer Experience in the Financial Services Industry

cx isn’t just a buzzword, it is one of the most important issues facing firms in the financial services industry.

Banking customers, today, expect banking to be mobile, with a la carte services, and they don’t care if the bank is a FinTech no one ever heard of. Changing old-age traditions will take time and money, but mostly open mindedness.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 8 of 40

10. Crossing the Digital Divide in Financial Services Marketing Success in the era of digital banking means more than having a mobile app. It

means digitizing your entire brand. How do you do that? You shift your advertising campaigns from conventional ad media to digital channels. Which is another way of saying you reach your target audience where they are today, rather than where they were yesterday.

Of course, social media exposure is necessary, but you need more than a Facebook ad. You must tap big data and AI to help locate potential customers, and to deliver customized offers in real time. Growth of financial services in India

The present growth rate of financial sector in India is about 8.5% p.a. An increase in growth rate is equivalent to growth of our economy. Over the past few years, there have been reforms in monetary policies, economicpolicies, opening up of financial markets, development of other financial sectors etc. In present times, a wide variety of financial products and services are offered to consumers to keep them satisfied. The Reserve Bank of India has also played a major role to help in growth of financial sector of India.

The diversified financial sector of India comprises of banks, mutual funds,insurance companies,pension funds etc. Do you know that the banking sector in India holds more than 60% of the total financial assets of the country. Atpresent, India is without any doubts one of the world’s most vibrant capital market.Let’s take a look at growth of some of the financial sectors of India one by one. Growth of the banking sector

Being one of the most extensive,the entire Indian banking system has a total asset value of approximately US$ 270 billion with total deposits being around US$ 220 billion. The banking system in India is continuously advancing and transformingitself. The current development of Core banking,Internet banking etc. has made banking operations easy and customer friendly. Growth of the Capital Market in India The capital markets in India have also witnessed changes.Some of them are-

1. Stock exchanges facing privatisation. 2. Removal of ill-used forward trading mechanism 3. In order to serve different investors in different locations,the introduction of

InfoTech systems in National Stock Exchange. 4. The increase in the ratio of transaction with deposit system and share ratio.

Growth in the Insurance sector in India

1. The market potential in India is immense. But it is untapped. So now in order to utilise thisopportunity, both foreign and Indian private players are providing tailor made products with opening of the market.

2. Because of huge competition and entry of new players, the insurance sector has also witnessed innovations like innovative insurance based products, services and value etc.

3. Many foreign companies like New York Life,Aviva,Standard Life have also entered this sector.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 9 of 40

4. Now a days,the insurance companies are engaged in aggressive marketing,selling and distribution techniques because of the extreme competition that they face from each other.

5. The credit for the development of this sector also goes to the active part of the regulatory body –Insurance Regulatory and Development Authority.

Growth of the Venture Capital market in India

1. In spite of the hindrances by the external setup, the venture capital sector in India is a very active financial sector.

2. In India,currently,there are around 2 international and 34 national venture capital funds registered by SEBI.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 10 of 40

UNIT - II FUND BASED FINANCIAL SERVICES

It refers to services that are used to acquire assets or funds for a customer. Following are some of the examples of financial services:

Leasing, credit card services, factoring, portfolio management, financial consultancy services, Underwriting, discounting and rediscounting of bills, Depository services, housing finance, Hire purchases, Mutual Fund management. Non- Fund Based Financial Services

This would help them to increase their revenue while optimizing the use of funds and would help to spread their risk over variety of activities. The non-fund based financial services of the public sector banks include loan syndication, consultancy and advisory services, capital issue management etc. The public sector banks have been marketing all the non-fund based financial services either directly by starting merchant banking division or by indirectly floating their subsidiary companies or both. Leasing

A “lease” is defined as a contract between a lessor and a lessee for the hire of a specific asset for a specific period on payment of specified rentals. FORMS OF LEASE FINANCING

Broadly speaking lease financing can take six different forms. They are as follows: We shall now briefly discuss the characteristic features of these doof lease financing. 1. Sale and Lease Back

Under this method, a company owning an asset sells it to another party and leases it back. Thus, the seller gives up the title to the asset hu retains its use. The main advantage of this kind of arrangement to the company that sells and then leases back is that it receives cash from the sale of the asset, which could be reinvested in the business while still making economic use of the asset during the lease period. This method of leasing is mostly found in real estate financing.

The structure of this arrangement is analogous to a mortgage on the asset taken out by the lessee. Rather than making a series of payments that amortized the lessor's acquisition costs and provide the lessor with a required return. By entering into this type of arrangement, the lessee firm can free the capital originally invested in the equipment. 2. Direct Leasing

In contrast with the sale and lease back arrangement under direct leasing the company acquires the right to use the property that it did not previously own. Direct leasing may be arranged either through the manufacturer or the financial institutions. Independent leasing companies or financial institutions usually enter into the business of acquiring assets like machinery etc. for their clients who are in need of certain assets for their business purpose. Once the leasing company owns the property, a direct lease is arranged under usual terms and conditions. It may be categorised into two based on the number of parties involved namely,

Bipartite Lease, and

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 11 of 40

Tripartite Lease. In bipartite lease, only two parties are involved namely, equipment supplier, and

lessor & lessee. It acts like an operating lease with upgradation, improvement of the equipment etc. Whereas tripartite lease involves three different parties namely, the equipment supplier, the lessor, and the lessee. Most of the equipment lease transactions to under this category. This form of lease has recourse to the supplier case of default by the lessee, either to buy back the equipment from the lessor on default or providing a guarantee on behalf of lessee. 3. Operating Leasing

Operating lease may be defined as "any lease other than a finance Under operating lease, the lessor maintains and services leased equipment. Here, the term of the lease contract may be less the economic life of the asset. Therefore, the cost of the equipmentWould not be fully amortised, and the lessor would subsequently lend the asset to other users.

In this method, the lease facility is provided on a period to period basis. In this type of leasing, no long-term obligation is Imposed either on the lessor or on the lessee and the agreement is cancellable at the option of either the owner or the user of the asset after giving a certain stipulated notice. This type of lease may be written off on a month-to-month basis without any specified expiration period. This, operating leases allow lessees to combat technological obsolescence that may affect computers and other equipment’s.

The lessor usually provides the operating know-how, supplies the related services and undertakes the responsibility of insuring and training the equipment. This kind of operating lease is known as “wet lease”Sometimes, the lessee bears the cost of insuring and obtaining the leased equipment. In such case it is called "Dry Lease"In our country, operating leases are not very popular. 4. Service Leasing

Service leasing provides for the maintenance of the equipment and performances of all routine servicing and repairs. The lessor generally meets these expenses and cost of this maintenance is built into the lease payments. In contrast to this, non-maintenance lease places the burden of maintenance and repairs on the lessee. 5. Financial Leasing

Operating lease, as we all know is a cancellable contract i.e.cancellable at the option of either party. Financial leasing, on the other hand, is a non-cancellable contract. Non-cancellability implies that the lessee is legally obliged to make all the lease payments regardless of whether he continues to use the asset or not. He should pay off the entire contract amount before he cancels the contract.

Financial lease transfers a substantial part of the risks and rewards associated with ownership from the lessor to the lessee. Here the lessor enters the transaction as a financier and buys the equipment from the supplier for the use of lessee. In practice, the lessee will usually write the identification for the equipment and liaise with the seller to ensure that is supplied meets those specifications. However, the lessee does note the owner. The primary rental period is designed to correspond he working life of the asset. At

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 12 of 40

the end of the lease period, the lessee has the option to contract for a second period for a nominal rent, or return the asset to the le e asset to the lessor or sell the asset as the lessor's agent. The regulations glasses preclude there being any intention in the leasing agreement that the lessee should at any time become the owner of the asset.

As far as repairs and servicing are concerned, in a financial lease, the lessor is separate from the suppler of the asset. Though the leasing company becomes the true owner of the asset, its real interest is in providing the finance. The leasing agreement will invariably make the responsible for maintaining and repairing the equipment, Characteristics of a Financial Lease The following are the characteristics of a financial lease:

The lessee selects the equipment The lessor is the legal owner and the lessee has no restroom to purchase the

assetat the time the lease is signed The lessee has the right to use the assets provided rentals are paid A non-cancellable primary period during which rentals should amortized capital cost

of asset and give the lessor his profit k essential. The lessee bears the burden of obsolescence. Generally industrial and commercial customers are involved, The lessee is responsible for maintenance and repair. The lessee is responsible for suitability and condition. Options on the expiry period do not include an option to purchase In India, leases are generally structured like financial lease only.

6. Leveraged Leasing

In leveraged leasing, the lessee contracts to make periodic payments during the lease period and in return, he is entitled to the use of the asset over that period of time. The lessor owns property but acquires it partly by contributing his own funds and partly by taking loans from the financial institutions. The financial institutions usually provide loan against the mortgage on the asset as well as by the assignment of the lease and lease payments. Thus, the lessor is the owner as well as the borrower. This method is similar to our popular instalment purchase system

Besides the above, there are arrangements such as the "Sales-aid Lease" involving a tie-up between a manufacturer and a lessor for mu benefit. In case of sales-aid lease, the lessor gains by way of commission and/or credit from the manufacturer. A "Cross-border Lease transcends national boundaries, and a "Big-ticket Lease" is one w very large transaction value. Features of Lease Contract: The important features of lease contract are as follows:

1. The lease finance is a contract. 2. The parties to contract are lessor and lessee. 3. Equipment are bought by lessor at the request of lessee. 4. The lease contract specifies the period of contract. 5. The lessee uses these equipment’s. 6. The lessee, in consideration, pays the lease rentals to the lessor.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 13 of 40

7. The lessor is the owner of the assets and is entitled to the benefit of depreciation and other allied benefits e.g., under sections 32A and 32B of the Income-tax Act.

8. The lessee claims the rentals as expenses chargeable to his income. Hire Purchase: Hire purchase means a transaction where goods are purchased and sold on the terms that:

i. Payment will be made in instalments, ii. The possession of the goods is given to the buyer immediately,

iii. The property (ownership) in the goods remains with the vendor till the last instalment is paid,

iv. The seller can repossess the goods in case of default in payment of any instalment, and

v. Each instalment is treated as hire charges till the last instalment is paid. Features of Hire Purchase: The main features of a hire purchase agreement are as below:

1. The payment is to be made by the hirer (buyer) to the hiree, usually the vendor, in instalments over a specified period of time.

2. The possession of the goods is transferred to the buyer immediately. 3. The property in the goods remains with the vendor (hiree) till the last instalment

is paid. The ownership passes to the buyer (hirer) when he pays all instalments. 4. The Hire or the vendor can repossess the goods in case of default and treat the

amount received by way of instalments as hire charged for that period. 5. The instalments in hire purchase include interest as well as repayments of

principal. 6. Usually, the hire charges interest on flat rate.

Guidelines for Hire Purchase

Must be in writing and signed by both the parties It must contain description of goods Price of Hire Purchase The date of commencement of agreement The number of instalments, amount & due date.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 14 of 40

UNIT - III MEANING OF MUTUAL FUNDS

A mutual fund is a corporation, which receive funds from investors and deploy the same in equities, long-term bonds and money market etc.

It represents pooled savings of numerous investors invested by professional fund managers in diversified portfolio to obtain maximum return on the investments made with minimum risk to the investors. Thus the fund collected is deployed in diversified portfolio. They have in their pool professional investment analysts who try to maximise the return on behalf of investors keeping in mind the likely risk involved in the whole exercise.

Hence a mutual fund is the most suitable form of investment for the common

person because it offers an opportunity to invest in a diversified, and professionally managed portfolio at a relatively low cost. So anybody with an investible surplus of a few thousand rupees can invest in mutual funds. Each mutual fund scheme has a defined investment objective and strategy. Investors can select fund, which they found suitable to the objective and invest so as to reap a maximum benefit out of it. TYPES OF MUTUAL FUNDS Mutual funds can be broadly classified into two categories such as:

On the basis of Operation and Execution. On the basis of Investment Objectives of Investors. We shall now detail them briefly.

1.On the basis of Operation and Execution On the basis of operation and execution of mutual funds, it can be classified into two namely,

Open-end Funds, and Closed-end Funds.

1.Open-end Funds:

Open-end fund is a mutual fund, which continuously issue new shares or units to meet the demand of the investors.At the same time, it redeems shares for those who want to sell. Hence, there is no limit on the number of shares that can be issued. In fact, the number of shares outstanding keeps changing due to the continuous influx and exit of investors. On account of the constant changes in the aggregate portfolio value and the number of shares, the Net Asset Value keeps changing The purchase and sale prices for redeeming or selling shares are set at or around the net asset value. 2.Close-end Funds:

Closed-end fund is a scheme of an investment company in which a fixed number of shares are issued. The funds so mobilised are invested in a variety of vehicles including shares and debentures, to achieve the stated objective. Capital appreciation for a Growth Fund or current income for an Income Fund can be cited as examples for this type of mutual fund. After the issue, investors may buy shares of the fund from the secondary market. The value of these shares depends on the Net Asset Value of the fund, as well as supply and demand or the fund's shares. Examples are Master Share and India Ratna.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 15 of 40

2.On the basis of Investment Objectives of Investors Based on the investment objectives of investors, mutual funds can be classified into

five types. They are: 1. Share Fund:

Share funds are normally invested in shares. They e hot invested in fixed income earning securities like bonds etc. Such funds can again be classified into four types as shown below: 1) Aggress Aggressive Growth Funds:

This type of funds is willing and ready to assume greater risk with an idea of getting huge profit on the investment made. Current income is not at all considered here. So such funds are invested only in securities, which are subject to frequent pricefluctuations. 2) Growth Funds:

These funds are also ready to assume risk but at a limited level. The basic objective of this type of fund is to get reasonable long-term capital appreciation. Hence, they invest their funds only in companies, which have sound capital structure. 3) Current Income Funds:

In this type, funds are invested only in securities, which have a greater scope to get high current income. Hence, such funds maintain the portfolio, which has permanent income 4) Growth and Income Funds:

This type of funds combines the merits of growth funds and income funds. They maintain their portfolio i such a manner to get fixed dividend as well as capital appreciation 2.Dualpurpose funds:

These funds have twin objectives namely (i) Current income, and (ii) Capital appreciation. They issue their sha in two types such as Capital Shares and Income Shares. Those invest in income shares will receive only a share of net profit of the fundwhereas those who invest in capital funds get only capital appreciation and they will receive no dividend. Here the unit holders will be assumed of only minimum dividend. 3. Balanced Fund:

Balanced fund is a mutual fund whose objective is to eam a mix of periodic income and capital appreciation for its investors.The General Insurance Corporation (GIC) Balanced Fund and Centurion Prudence Fund are examples of this type of fund. 4. Money Market Fund (MMF):

Money market fund is a mutual fund, which invests in money market securities like Treasury Bills and Commercial Paper. In India, the Guidelines for setting up Money Market Mutual Funds Are spelt out by the Reserve Bank of India (RBI) in April 1992. Even then the response was indifferent owing to certain rigidities in the scheme. Consequently, in November 1995, the RBI introduced the following relaxations:

1. The private sector has been permitted to set up MMFS. Before this relaxation, only scheduled commercial banks and public financial institutions were allowed to set up mutual funds.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 16 of 40

2. There will be no ceiling as regards the size of MMFS. 3. Limits on investments in individual instruments by the funds have been removed

except in the case of commercial paper.

In April 1996, the RBI further announced that MMFS might i5sue units to corporate too. RBI will provide liquidity support to those funds,which are dedicated to Government Securities. In a period of rising short-term interest rates, money market funds av become an attractive investment alternative and could even the ff disintermediation from yield savings deposits with banks. 5. Specialised Funds:

Specialised fund is a mutual fund, which focuses on a particular industry or on companies in a specific geographical region. For instance, a mutual fund may be promoted to cater to investors interested in Chemical Industry, or in companies located in a rapidly developing country. Some funds may concentrate on a particular type of security such as Convertible Debentures. In February 1994, Canbank Mutual Fund floated a unique fund called, Canexpo invest mainly in export-oriented businesses. Similarly, ICICI Power, another mutual fund will focus on the infrastructure sector including power and telecom.

Besides the above, there is another mutual fund which has been recently introduced viz., Off Shore Mutual Funds. Such funds received their predetermined corpus fund in foreign currency and bring them to India for portfolio investment. For e.g., UTI's off shore funds, India Fund, India Growth Fund etc. ADVANTAGES TO AN INVESTOR IN MUTUAL FUND Mutual Funds offer numerous benefits to investors, which are as below:

1. Since the shares/units of mutual fund are traded on stock exchange, they are encashable on any day. So it offers liquidity to its units.

2. The worries of investment complexities are taken care of by mutual fund. Individual investor need not bother about it.

3. Different tax benefits are available to investors in mutual funds. 4. Since the total funds available to mutual fund are substantially greater than

available to a particular investor, the mutual funds can judicially deploy the huge fund to a grater extent for the sake of the individual investor.

5. Because of different regulations of SEBI, the RBI and Government on mutual funds, the funds are in safe hands.

6. The continuous return from investment in mutual fund is automatically reinvested on behalf of investors.

7. It induces saving habit. DISADVANTAGES OF MUTUAL FUNDS Mutual funds suffer from various risks. They are as follows: 1. Market Risk:

Market risk arises out of fluctuations in the market value of securities. It may lead to a loss of principal. The market value of shares, debentures etc. fluctuates due to various factors such as demand for and supply of securities, quantum of money supply, economic policy, political conditions etc. So it cannot be avoided in its entirety. Howeverit can be minimised by diversifying among a variety of securities rather than investing in one or two

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 17 of 40

securities. This is because, when one stock is adversely affected another stock may do well or less affected. That is why mutual funds invest their money in many companies. 2. Interest Rate Risk:

The value of a fixed income security like debentures, bonds etc. depends upon the rates of interest prevailing in the market. If the interest rates rise, the value of the security will fall and vice versa. This risk also cannot be avoided. 3. Inflation Risk:

The return on investments does not change proportionately with the change in consumer prices. It is what is called inflation risk. This risk also cannot be avoided. However, it can be managed by investing a portion of its fund in equity shares, which always provide for higher return as compared to debt instruments. 4. Business Risk:

Business risk is associated with the financial soundness, proper management etc of the business. If any business is poorly managed, it denotes that it is not financially sound. Such companies value of securities will fall automatically in the market. This kind of risk also can be avoided by diversifying the portfolio of mutual funds. 5. Credit Risk:

Sometimes the issuer of fixed income security fails to pay interest or principal when it becomes due Such risk is called as credit risk. Normally, this kind of risk arises due to the mismanagement, dissolution etc. of the company. In order to avoid this kind of risk, mutual funds should get the ratings of reliable credit rating agency. The companies with high rating only should be selected for investments 6. Political Risk:

Political risk refers to the change in the market value of a security due to political events like war, change in law, change in Government etc. This risk cannot be avoided. However, diversification to a certain extent will help to minimise it. 7. Liquidity Risk:

Liquidity risk is associated with the marketability of the securities. Mutual funds have different schemes each one has its own time for exiting the market. So, mutual funds cannot enter and exit the market as they like, which affects the marketability of their investmentsThis risk cannot be avoided 8. Timing Risk:

Each investment is to be properly timed Wrong timing of buying and selling the securities will naturally lead to a loss should be avoided. Otherwise, iaats very purpose will be defeated. Expertsin mutual funds schemes should study the market situation and find out whether climate in the market is suitable for purchase/sale and decide accordingly. Benefits of mutual funds 1.Simplicity: Mutual Funds Are Easy to Understand

Because of their simplicity, mutual funds require no experience or knowledge of economics, financial statements, or financial markets to be a successful investor.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 18 of 40

For beginners, here is a simple definition of Mutual Funds. A mutual fund is an investment security type that enables investors to pool their money together into one professionally managed investment. Mutual funds can invest in stocks, bonds, cash and/or other assets. These underlying security types, called holdings combine to form one mutual fund, also called a portfolio1 .

For a simple definition, mutual funds can be considered baskets of investments.

Each basket holds dozens or hundreds of security types, such as stocks or bonds. Therefore, when an investor buys a mutual fund, they are buying a basket of investment securities. Simple!

Yes, there are many things to know about mutual funds but compared to the broad

world of financial products, mutual funds are quite easy to use and understand. 2. Accessibility: Mutual Funds Are Easy to Buy

Mutual funds are offered at brokerage firms, discount brokers online, mutual fund companies, banks, and insurance companies. Even beginning investors can easily open an account at a no-load mutual fund company, such as Vanguard Investments, and open an account within minutes2 . 3. Diversification: Mutual Funds Have Broad Market Exposure

One mutual fund can invest in dozens, hundreds, or even thousands of different investment securities, making it possible to achieve diversification by investing in just one fund. However, it is smart to diversify into several different mutual funds. 4. Variety: Mutual Funds Come in Many Different Categories and Types

As you grow your portfolio of mutual funds, you will want to diversify into various mutual fund categories and types. You can invest in mutual funds that cover the main asset classes (stocks, bonds, cash) and various sub-categories or you can even venture into specialized areas, such as sector funds or precious metals funds. 5. Affordability: Mutual Funds Have Low Minimums

Most mutual funds have minimum initial investment requirements of $3,000 or less. In many cases, if the investor initiates a systematic investment program, the initial investment may be much lower. Some minimums can be as low as $100. Subsequent investments may be lower than $100. If you invest through a 401(k) plan or other employer-sponsored retirement plan, there is no minimum to get started1 . 6.Low Expense: Mutual Funds Can Cost Less to Manage Than Other Portfolio Types

Costs as a percentage of assets in the portfolio may be lower for an actively-managed mutual fund when compared to an actively-managed portfolio of individual securities. When you add up transaction costs, annual fees paid to a brokerage firm, and the cost for research tools or investment advice, mutual funds are often less expensive than the typical portfolio of stocks. 7. Professional Management: Mutual Funds Have a Team of Professionals Researching and Analyzing Investments So You Don't Have To!

Perhaps the greatest benefit of mutual funds is that investors can save countless hours of time, energy and frustration involved with the research and analysis required to

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 19 of 40

find quality investments to hold in a portfolio. That's not to speak of the skill, desire and patience required to do a job well in any professional pursuit. Mutual funds enable investors to do more of the things in life they enjoy rather than spending time and energy on investment matters1 . 8. Flexibility: Mutual Funds Have Several Uses and Applications

All of the above benefits of mutual funds overlap into simplicity and flexibility. You can invest in just one fund or invest in a wide variety. Automatic deposit, systematic withdrawal, 401(k) plans, annuity sub-accounts, dividends, short-term savings, long-term savings, and nearly limitless investment strategies make mutual funds the best overall investment type for both beginners and advanced investors. Regulations of Mutual Fund

For a mutual fund, the AMC set up should consist of 50% independent directors, a separate board of trustees’ company with 50% independent trustees and independent custodians so that some distance can be managed between fund managers, custodians, and trustees.

As AMC manages the funds and trustees hold the custody of all the assets. A balance must be maintained between them so that both can keep a check on each other.

SEBI takes care of the Sponsor, financial soundness of the fund and probity of the business while granting permission.

Mutual funds must adhere to the principles of advertisement. In the case of an open-ended scheme and closed-ended scheme, the minimum of

50 crores and 20 crores corpus is required as per the guidelines of SEBI. A mutual fund should invest the money raised for these savings schemes within 9

months. By this, the funds do not get invested in bullish markets and suffering from poor

NAV also reduces. The maximum amount that a mutual fund can invest in the money market is 25% in

the first 6 months after closing the funds and 15%of the corpus after six months so that short-term liquidity requirements can be met.

SEBI checks mutual funds every year in order to make it in compliance with the regulations and guidelines.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 20 of 40

UNIT - IV FACTORING

MEANING AND DEFINITION OF FACTORING Factoring is a specialised activity whereby a firm converts its receivables into cash

by selling them to a factoring organisation. The factor assumes the risk of collection and in the event of non-payment by the customers/ debtors bears the risk of bad debt losses. It is also termed as "Invoice Factoring” as factoring covers only those receivables, which are not supported by negotiable instruments namely, bills. In case of receivables backed by bills, the firm resorts to the practice of bill discounting bankers. with its banker. With the factoring of receivables, the client dispenses away the credit department and the debtors of the firm become the debtors of the factor.

MECHANICS OF FACTORING

The factoring arrangement starts when the seller (client) concludes an agreement with the factor, wherein the limits, charges and other terms and conditions are mutually agreed upon. Then the client will pass on all credit sales to the factor. When the customer places the order and the client delivers the goods along with invoices to the customer, the client sells the customer’s account to the factor and also informs the customer that payment has to be made to the factor. A copy of the invoice is also sent to the factor. The factor purchases the invoices and makes prepayment, generally up to 80% of the invoice amount. The factor sends monthly statement showing outstanding balance to the customer, copy of which are also sent to the client. The factor also carries follow-up if the customer does not pay by the due date. Once the customer makes payment to the factor, the balance amount due to the client is paid by the factor.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 21 of 40

The factoring process is explained in Fig. 11.2.

TYPES OF FACTORING: Factoring can be classified into many types. This section covers various forms of factoring 1. Recourse Factoring

Under recourse factoring, the factor purchases the receivables on the condition that any loss arising out of irrecoverable receivables will be borne by the client. In other words, the factor has recourse to the cli if the receivables purchased turn out to be irrecoverable. Thus, type of factoring if any debt is not paid by the debtor on maturity, the factor can recover his dues from the seller (client) and the debt is reassigned back to the seller (client). Factoring agencies usually begin with this kind of facility and only after some stabilisation is reached, they convert their venture into full-service factoring which is of without recourse type. 2.Non-Recourse or Full Factoring

This is the most comprehensive and classical form of factoring. As the name implies, in this type of factoring, the factor has no recourse to the client if the receivables are not recovered in. the client gets total credit protection. Under this factoring, all the components of service viz., short-term finance, administration of sales ledger and credit protection are available to the client. It includes all types of facilities including credit protection. The factor buys all approved debts without recourse to the client and even if payment of a debt is not forthcoming, he bears the loss himself

In full factoring, the factor takes the responsibility for all aspects of this part of the

firm's business. By this arrangement the factor relieves the client from the administrative burden of looking after receivables and purchases the debt without recourse and thereby shoulders the risk payment may not be made. As the factor is assuming the credit risk, Lakes the responsibility for credit control, assesses the credit risk a decides what amount of credit will be allowed to individual customers establishing credit intelligence for this purpose. Thus it is considered high risk factors Thus the factor has to closely examine the

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 22 of 40

financial viability of each debtor of his client before entering into such an agreement It also takes over administration of a client's sales ledger, chases debtor and evaluates credit risks. Recourse Factoring and Non-Recourse Factoring:

The recourse factoring and non-recourse factoring differ only respect i.e. who bears the risk of loss in the event of risk of default or delayed collection. In recourse factoring, it is the client who carries the credit risk of the debts sold to the factor. On the other hand, in a non- recourse factoring, the client sells the debts on the condition that in the risk of default or delayed collection, factor has to bear the loss and financial burden cannot be shifted to the client. 3. Maturity Factoring

Under this type of factoring arrangement, the factor does not make any advance or prepayment. The factor pays the client either on a guaranteed payment date or on the date of collection from the customer. This is opposed to "Advance Factoring" where the factor makes prepayment of around 80% of the invoice value to the client. Here he provides only administrative services. In this type of factoring, factor normally performs the following services:

1. Monitoring and maintaining the sales ledger, 2. Issuing and despatching invoices, and 3. Collecting debts on due date.

The factor relieves the client from the following activities:

1. Sending out invoices, 2. Keeping a record of the amount owing to it by the customers 3. Making sure that the customers pay the client by the date and should payment

be not received, and 4. Reminding them or even in some cases taking action to recover the debt. This is

non-credit aspect of the service.

Thus, factor frees the client from maintaining an accounting section Due to economies of scale the factor offers this service very efficiently and quite possibly more cheaply than the client could achieve. Management can devote most of its time for more important tasks. Resides there could be substantial savings from speedy collection of debts. Hence, small and medium-sized companies are able to enjoy professionalism in the management of their debts far beyond that which they might otherwise achieve from their own resources. 4. Invoice Discounting

Strictly speaking, this is not a form of factoring because it does not carry the service elements of factoring. Under this arrangement, the factor provides a pre-payment to the client against the purchase of accounts receivable and collects interest (service charges) for the period extending from the date of collection. The client carries out the sales ledger administration and collection. This service provides the seller (client) with cash in exchange for receivables. In this factoring, the debtor customer) is not aware that the seller (client) is availing any factoring facility and hence this is also called "Confidential Discounting" Here, the utilisation of factoring service is not disclosed to the customer unless or until there is a breach of agreement on the part of the client or where the factor feels that he is at a risk

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 23 of 40

5. Credit Insurance In credit insurance, the factor takes over responsibility for the company's debts and

so removes any risk of loss for the company. The company ends up with just one debt owing to it as the factor buys the debts from it, paying the company when the customers pay the debts The factor is able to take on the risks of the debts because through his specialist knowledge and experience, he can assess the risks better the company. The factor will also set a limit to customers' credit and a not take on any debts he considers to be bad ones.

6. Finance Provision or Advance Factoring

Using this arrangement, the factor will agree to buy the debts of the company, and at the same time will advance up to 80% of their value to the company - the remainder (minus interest) being paid when the debts are collected. In this way the company is able to improve its cash position immediately.

7. Export Factoring

This is designed to help reduce the risks of overseas trading and to ensure that the supplier receives payment for his goods quickly. Usually the factor not only pays the supplier when the goods are shipped, being paid in turn by the purchaser eventually, but also deals with export duties, Local tariffs and so on-being able to use his expert knowledge of the local markets and conditions to help the exporting company considerably.

8. Disclosed and Undisclosed Factoring

In the case of disclosed factoring, the name of the factor is disclosed to the customer by indicating the same in the invoice sent by the supplier (client) to the customer. The client directs the customers to make payment to the factor. The risk of default in payment rests with the supplier and hence it is a form of recourse factoring Sometimes this kind of factoring is done as non-recourse in part by specifying the limit with which factor should act on non-recourse basis

In the case of undisclosed factoring, the name of the factor is disclosed to the client.

The maintenance of sales ledger is done by the tractor but all dealings with customers as to collection of debt are done in the seller (client). However, the control of credit sales by sales administration and management of credit risk is provided by the factor.

9. Bank Participation

Factoring In this method, bank creates floating charge on the amount payable by a factor for client's receivables. Then based on that, the bank gives loan to the client. Besides, it provides a chance to get double finance also to the client.

10. Supplier Guarantee Factoring This type of factoring arises when the client acts as an intermediary between the

supplier and the customer.The factor guarantees the supplier against the invoices raised by supplier on the client. Then client writes receivables on the customer and assigns the same to factor itself. This helps the client to get full profit without any financial problem. 11. Cross-border Factoring or International Factoring

There are four parties in each transaction in a cross-border factoring. They are - an exporter, an export factor, an import factor and an importer. In a cross-border factoring, the exporter enters into an agreement with the export factor in his country and assigns him

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 24 of 40

export receivables as and when they arise. Here payments for factored debts are made in a similar manner as in the case of domestic factoring. The export factor enters into an agreement with the factor in the country in which the import factor resides and enters into a contract with him assigning him the tasks of credit checking, sales ledgering and collection, for payment of a stipulated fee. Features of Factoring: The features of factoring have been explained below:

1. It is very costly. 2. In factoring there are three parties: The seller, the debtor and the factor. 3. It helps to generate an immediate inflow of cash. 4. Here the full liability of debtor has been assumed by the factor. 5. Factor has the right to take any legal action required to recover the debts.

Functions of Factor: A factor performs a number of functions for his client. These functions are: 1. Maintenance of Sales Ledger:

A factor maintains sales ledger for his client firm. An invoice is sent by the client to the customer, a copy of which is marked to the factor. The client need not maintain individual sales ledgers for his customers.

On the basis of the sales ledger, the factor reports to the client about the current

status of his receivables, as also receipt of payments from the customers and as part of a package, may generate other useful information. With the help of these reports, the client firm can review its credit and collection policies more effectively.

2. Collection of Accounts Receivables:

Under factoring arrangement, a factor undertakes the responsibility of collecting the receivables for his client. Thus, the client firm is relieved of the rigours of collecting debts and is thereby enabled to concentrate on improving the purchase, production, marketing and other managerial aspects of the business.

With the help of trained manpower backed by infrastructural facilities a factor

systematically undertakes follow up measure and makes timely demand in the debtors to pay amounts. Normally, debtors are more responsive to demands or reminders from a factor as they would not like to go down in the esteem of credit institution as a factor.

3. Credit Control and Credit Protection:

Another useful service rendered by a factor is credit control and protection. As a factor maintains extensive information records (generally computerized) about the financial standing and credit rating of individual customers and their track record of payments, he is able to advise its client on whether to extend credit to a buyer or not and if it is to be extended the amount of the credit and the period there-for.

Further, the factor establishes credit limits for individual customers indicating the

extent to which he is prepared to accept the client’s receivables on such customers without

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 25 of 40

recourse to the client. This specialised service of a factor assists clients to handle a far greater volume of business with confidence than would have been possible otherwise.

In addition, factor provides credit protection to his client by purchasing without

recourse to him every debt of approved customers (within the stipulated credit limit) and assumes the risk of default in payment by customers only in case of customers’ financial inability to pay. 4. Advisory Functions:

At times, factors render certain advisory services to their clients. Thus, as a credit specialist a factor undertakes comprehensive studies of economic conditions and trends and thus is in a position to advise its clients of impending developments in their respective industries.

Many factors employ individuals with extensive manufacturing experience who can even advise on work load analysis, machinery replacement programmes and other technical aspects of a client’s business.

Factors also help their clients in choosing suitable sales agents/seasoned personnel

because of their close relationship with various individuals and non-factored organizations. Thus, as a financial system combining all the related services, factoring offers a

distinct solution to the problems posed by working capital tied in trade debts. RBI's Guidelines on Factoring

To govern the conduct of factoring business by banking companies the RBI amended the Banking companies Act 1949 and issued the Guidelines in 1990 to enable the banking companies to undertake factoring business in India. The guidelines issued by it are as below:

1. At present, banks shall not involve directly in factoring business 2. They may invest in shares of other factoring companies within the specified limit

with the prior permission of the RBI. They shall not act as promoters of such companies. With the prior approval of the RBI banks may set up separate subsidiaries to invest in factoring companies

3. A factoring subsidiary or joint venture factoring company may undertake factoring business and such other activities as are incidental thereto.

4. Investment of a bank in the shares of factoring companies (inclusive of its subsidiary carrying on factoring business) shall not in the aggregate exceed 10% of the paid up capital and reserves of the bank.

5. Any application to be made to the RBI for setting up of the subsidiaries of the joint venture factoring companies in India shall require prior clearance of the Reserve Bank of India.

6. Banks, which are setting up subsidiaries of investing in joint venture factoring companies for the purpose of carrying on factoring business should furnish such information in such form and at sunset time as the RBI may require from time to time.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 26 of 40

Forfeiting The terms forfeiting is originated from an old French word ‘forfait’, which means to

surrender ones right on something to someone else. In international trade, forfeiting may be defined as the purchasing of an exporter’s receivables at a discount price by paying cash. By buying these receivables, the forfeiter frees the exporter from credit and the risk of not receiving the payment from the importer. Role of Forfeiting in International Trade

The exporter and importer negotiate according to the proposed export sales contract. Then the exporter approaches the forfeiter to ascertain the terms of forfeiting. After collecting the details about the importer, and other necessary documents, forfeiter estimates riskinvolved in it and then quotes the discount rate.

The exporter then quotes a contract price to the overseas buyer by loading the

discount rate and commitment fee on the sales price of the goods to be exported and sign a contract with the forfeiter. Export takes place against documents guaranteed by the importer’s bank and discounts the bill with the forfeiter and presents the same to the importer for payment on due date. Documentary Requirements

In case of Indian exporters availing forfeiting facility, the forfeiting transaction is to be reflected in the following documents associated with an export transaction in the manner suggested below: Invoice:

Forfeiting discount, commitment fees, etc. needs not be shown separately instead, these could be built into the FOB price, stated on the invoice. Shipping Bill and GR form:

Details of the forfeiting costs are to be included along with the other details, such FOB price, commission insurance, normally included in the "Analysis of Export Value "on the shipping bill. The claim for duty drawback, if any is to be certified only with reference to the FOB value of the exports stated on the shipping bill. Forfeiting The forfeiting typically involves the following cost elements:

1. Commitment fee, payable by the exporter to the forfeiter ‘for latter’s’ commitment to execute a specific forfeiting transaction at a firm discount rate within a specified time.

2. Discount fee, interest payable by the exporter for the entire period of credit involved and deducted by the forfeiter from the amount paid to the exporter against the availed promissory notes or bills of exchange.

Benefits to Exporter 100 per cent financing:

Without recourse and not occupying exporter's credit line, That is to say once the exporter obtains the financed fund, he will be exempted from the responsibility to repay the debt.

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 27 of 40

Improved cash flow: Receivables become current cash inflow and it is beneficial to the exporters to

improve financial status and liquidation ability so as to heighten further the funds raising capability.

Reduced administration cost:

By using forfeiting, the exporter will spare from the management of the receivables. The relative costs, as a result, are reduced greatly.

Advance tax refund:

Through forfeiting the exporter can make the verification of export and get tax refund in advance just after financing.

Risk reduction:

Forfeiting business enables the exporter to transfer various risk resulted from deferred payments, such as interest rate risk, currency risk, credit risk, and political risk to the forfeiting bank.

Increased trade opportunity:

With forfeiting, the export is able to grant credit to his buyers freely, and thus, be more competitive in the market. Benefits to Banks Forfeiting provides the banks following benefits:

Banks can offer a novel product range to clients, which enable the client to gain 100% finance, as against 8085% in case of other discounting products.

Bank gain fee-based income Lower credit administration and credit follow up

Features of Forfeiting

Credit is extended to the importer for a period of between 180 days and seven years.

The minimum bill size is normally $250,000, although $500,000 is preferred. The payment is normally receivable in any major convertible currency. A letter of credit or a guarantee is made by a bank, usually in the importer's country. The contract can be for either goods or services.

At its simplest, the receivables should be evidenced by a promissory note, a bill of exchange, a deferred-payment letter of credit, or a letter of forfaiting. Venture Capital MEANING AND DEFINITION OF VENTURE CAPITAL

Venture capital is a form of equity financing specially designed for funding high risk and high reward projects. It plays an important role in financing hi-technology projects and helps to convert research and development into commercial production.

In a narrow sense, the concept of venture capital may be referred to "Investment in young firms, which lack funds". However, in a broader sense. it refers to "The contribution of share capital for the formulation and setting up of small firms that are specialising in

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 28 of 40

new ideas/new technologies". It gives a firm not only funds but also provides skill needed to establish the firm, designs its marketing strategy and organises and manages it

Venture capital is a long-term risk capital for financing high technology projects that involve risk but at the same time has strong potential for growth Generally venture capitalists accumulate their resources in the early years of the project so as to assist the new entrepreneurs As soon as the project develops and starts reaping profits, they sell away their equity shares at high premium.

The Organisation for Economic Co-operation and Development has formulated an

elaborate definition, which covers almost the entire features of venture capital. The definition formulated by it is as follows

"Capital provided by firms who invest alongside management in young companies

that are not quoted on the stock market objective is high return from the investment. Value is created by young in partnership with the venture capitalist's mon and professional expertise".

Thus, a venture capital company may be defined as "A finance institution, which

joins an enterprise as a co-promoter in a project and shares the risks and rewards of the enterprise". FEATURES OF VENTURE CAPITAL The features of venture capital are listed down below:

1. Venture capital is normally contributed in the form of equity capital. However it may also be given in the form of long-term loan or debt capital.

2. It is a high-risk venture. However, it also enjoys high growth potentials 3. Venture capital is provided only for setting up of new firms with new ideas or

new technologies. The enterprise, which are engaged in trading, booking, financial services, agency, liaison work or research and development are not considered for investment by venture capitalists:

4. Venture capitalist joins an enterprise as a co-promoter in projects He shares the risks and rewards of the enterprise.

5. Venture capitalist continuously involve in business in which he makes investment It has a long-term orientation

6. As soon as the venture has reached the full potential the venture capitalist disinvests his holdings. Hence it is obvious that the basic objective of investment is capital appreciation at the time of disinvestment and not profit

7. Venture capitalists provide not only money but also an input skill needed to set up the firm, design its marketing strategy organise and manage it

8. Normally, venture capitalists make investment in small medium firms. 9. The gestation period is long. The benefit or profit from the true capital

investment will start accruing only after an average period of 4 to 5 years 10. It is a long-term investment and the returns are in the form of capital gains 11. It is an active form of investment with a higher degree of involvement in the

management of a venture

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 29 of 40

FORMS OF VENTURE CAPITAL Normally, venture capital is required for the various stages of development of a business such as -

1. Development of Idea, 2. Implementation of the Idea, 3. Commercial Production, and 4. Establishment Stage,

During the first stage i.e. "Development of Idea" the risk associated ab the business

is very high. This stage involves two steps such as 1 Conceiving an Idea, and 2. Converting the Idea so conceived into a business proposition. At this stage, investigation is made deeply which takes normally a year or more. So, the finance required at this stage is called seed finance

The second stage is "Implementation of the Idea Phase". In this stage, the firm is

set up to manufacture a product and so the finance provided by the venture capitalists at this stage is known as start-up capital. The capital introduced up to the second stage is used for manufacturing the products as well as for further business development,

The third stage is going for “Commercial Production” of the product for which firm

was actually set up. During this stage, the firm faces E teething problems. In this stage, it may not be able to get adequate funds. So, the finance is provided additionally to develop the marketing infrastructure for the firm

The fourth stage is the "Establishment Stage" in which the firm is established in the

market and expected to expand at a rapid pace In stage, it needs finance for its growth and expansion so that it can enjoy economies of large scale Here establishment finance is sought from the venture capital fund.

The extent of risk associated with a business decreases gradually in subsequent

stage of development of the business whereas its need e increases gradually when it passes through its every subsequent stages of development. PHASES IN VENTURE CAPITAL FINANCING The venture capital, which the venture capitalists finance passes through different stages such as:

1. Raising of Funds and Exploring Business Plans. 2. Investing in Firms. 3. Leaving Successful Firms. 4. Returning the Capital to Investors

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 30 of 40

The pictorial representation of its phases is given in Fig. 13.1 below.

1.Raising of Funds and Exploring Business plans

Raising of funds and exploring business plans are usually carried on simultaneously. These are ongoing processes. In other words, these are never ending processes. Venture capitalists normally raise funds from general investors who do not know for which purpose their money will be invested. At the same time, he explores the business plans that have growth potential. Normally, out of hundred proposals only one or two will be capable of selection for investment. Hence, venture capitalists should be very careful and analyse the proposal in various angles, and choose the best for their investment.

2. Investing in Firms

The second phase in venture capital financing is making investment in a new firm. Normally, newly created firms concentrate on only one product because they are in the initial stage. Venture capitalist aims at developing such start up business into a stable company. They monitor its operation continuously; take part in strategic decision-making of its Board. They also contribute their business experience, knowledge and decision-making skills for the successful development of a new business.

3. Leaving the Successful Firms

The third stage is exiting the firm. After the company stabilises, the venture capitalists withdraw their money from the company for returning the money to the investors. There are two objectives to withdraw money at this stage. One is this is the stage at which the venture capitalists reap profit due to the capital appreciation. The other one is, the money can be invested in another risky venture. Otherwise, it will be with the company

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 31 of 40

in which no more capital appreciation can be expected than gained already. That is why, once the company developed the venture capitalists withdraw their money from the company and look for another new venture having growth potential. Hence the cycle continues. FUNCTIONS OF VENTURE CAPITAL The key functions of venture capital are as follows: 1.Provides Finance as well as Skills

Venture capital provides finance as well as skills to new firms and new ventures of existing firms. It provides funds not only in the initial stages but also throughout the life of a business concern. Venture capitalist fills the gap in the owner's funds in relation to the quantum of equity required to support the successful launching of a new business or the optimum scale of operations of an existing business. It acts as a trigger in launching new business and is catalyst in stimulating existing firms to achieve optimum performance.

2. Widens the Industrial Base

Venture capital finances hi-tech projects and thereby it widens the industrial base of high-tech industries and promotes the growth of technology

3. Helps in Professionalising the Firms

Venture capitalist assists the entrepreneurs to locate, interview and employ outstanding people to professionalise the firm SEBI REGULATIONS ON VENTURE CAPITAL FUND 1.Meaning of Venture Capital Fund

A venture capital fund means a fund established in the form of or a company including a body corporate and registered under the regulations, which has a dedicated pool of capital, rose in a man specified in the regulations, and invests in venture capital undertaking in accordance with the regulations. 2. Grant of Registration Certificate 1) Application for Grant of Certificate

Any company or trust or body corporate proposing to carry on any activity as a venture capital fund must apply in Form A to SEBI along with non-refundable application of Rs. 25,000 for grant of a certificate of carrying out venture capital activity in India. Registration fee for grant of certificate is Rs. 500.000 2) Eligibility Criteria for Registration For the purpose of grant of certificate by SEBI, the following conditions must be satisfied: A. Where the Application is made by a Company

1. 1.The main object of the company as per its Memorandum of Association must be the carrying on of the activity of venture capital fund

2. Its Memorandum and Articles of Association prohibit it from making an invitation to the public to subscribe to its securities

3. Its directors or its principal officer or employee must be a fit and proper person to act as director or principal officer or employee of the company

STUDY MATERIAL FOR BBA FINANCIAL SERVICES

SEMESTER - IV, ACADEMIC YEAR 2020-21

Page 32 of 40

B. Where the Application is made by a Trust 1. The Trust Deed is in the form of a deed and has been duly registered under the

provisions of the Indian Registration Act 1908 2. The main object of the trust is to carry on the activity of a venture capital fund 3. Its directors or its principal officer or employee must be a fit and proper person

to act as director or principal officer or employee of the company 3) Furnishing of Information

SEBImay require the applicant to furnish such further information as it considers necessary for enabling it to process the application An cation, which is not complete in all respects, shall be rejected by SEBI

4) Procedure for Grant of Certificate

SEBI is satisfied that the applicant is eligible for grant of silicate, it shall send intimation to the applicant of its eligibility. On receipt of intimation, the applicant must pay to SEBI registration fee of R 500,000. On the receipt of such fees, SEBI shall grant a certificate of registration in Form B. 5) Conditions as to Certificate The certificate granted shall be subject to the following conditions:

1. The venture capital fund shall abide by the provisions of the SEBI Act and these regulations

2. The venture capital fund shall not carry on any other activity other than that of a venture capital fund.

3. The venture capital fund shall inform SEBI in writing of any information or details previously submitted to SEBI, which have changed after grant of the certificate.