Students: Pol Parcerisas-Kuhnlein, Daniel Shear, Andrew...

36

November 30 th , 2018 Students: Pol Parcerisas-Kuhnlein, Daniel Shear, Andrew Weeks

Transcript of Students: Pol Parcerisas-Kuhnlein, Daniel Shear, Andrew...

November 30th, 2018

Students: Pol Parcerisas-Kuhnlein, Daniel Shear, Andrew Weeks

Core business restructuring complete 1 Inflection in same store sales growth has started

What you need to believe

Long Macy’s! Value opportunity, $50.8 Jan-20 TP (42% IRR)

Growth initiatives create multiple ways to win 2 ~30% ’20E EPS beat + SOTP crystallization

Underappreciated downside protection via RE 3 Real estate value equals ~1.0x enterprise value

Value stock with compelling fan of returns

$0

$10

$20

$30

$40

$50

$60

$70

$80

2007 2009 2011 2013 2015 2017 2019

Downside: $30.5

Base: $50.8

Upside: $60.2

Financial Summary Key Shareholders

Executive Team

FY18 Consensus

Vanguard 10.6%

BlackRock 7.3%

SunAmerica 5.7%

Jeffrey Gennette CEO

Paula Price CFO

Robert Harrison COO

Revenue Growth -2.0%

EBITDA Margin 11.4%

EPS 7.2%

Share price

Last Close $33.30

Target Price $50.80

Upside/Downside 53%

52w High $41.99

52w Low $19.33

Short Interest % of Float 13.6%

Market Cap $10,396

Debt $5,534

(-) Cash $736

TEV $15,194

Strong underlying consumer, weak Macy’s?

Source: University of Michigan and Capital IQ

Consumer sentiment not translating into Macy’s value

0

10

20

30

40

50

60

70

80

50

60

70

80

90

100

110

2008 2010 2012 2014 2016 2018

Consumer Sentiment (LHS) Macy's Share Price (RHS)

Index $ Share price

E-Commerce is taking share… …and capturing all the growth

Source: Kleiner Perkings Internet Report 2018

Industry view already priced into stock

Beaten up retail stocks anticipate massive Ecommerce disruption

Physical retail still grows despite under-performance in Tier 2-3 malls

$bn Market value Δ Dividends

Share Repurch. Total

66 54 68 188

16 9 19 45

6 3 8 17

6 2 5 13

Total 94 68 99 262

757 - 1 758

Omnichannel has delivered ~$260bn of value to shareholders since 2009

Fwd P/E: ’09 vs. ’18 (x)

15.5x to 20.8x

12.7x to 14.3x

13.2x to 8.3x

8.5x to 13.8x

37.5x to 67.3x

12.5x to 15.8x

Source: Kleiner Perkings Internet Report 2018, CapIQ

Underestimated value of omnichannel

Negative sentiment does not impede retail from delivering value

Growth is back! Plan to right-size portfolio and close 100 stores is 85% complete

Number of full-line Macy’s Stores

Comparable sales growth (YoY) …that generate SSS growth again for Macy’s

Portfolio rationalization has left the highest quality stores…

(1) (1)

Note: (1) Adjusted for one-off effect (un-adjusted SSS Q1 ’18 4.2% and Q2 ’18 0.5%) Source: Company filings

Core business restructuring complete 1

Refocused portfolio will make Macy’s great again

784 761 730 728 729

666 668 665 664 653 652 652 652

2014 2015 1Q 2016

2Q 2016

3Q 2016

4Q 2016

1Q 2017

2Q 2017

3Q 2017

4Q 2017

1Q 2018

2Q 2018

3Q 2018

1.4%

(2.5%)

(5.6%)

(2.0%) (2.7%) (2.1%)

(4.6%) (2.5%)

(3.6%)

1.4% 1.7% 2.9% 3.3%

2014 2015 1Q 2016

2Q 2016

3Q 2016

4Q 2016

1Q 2017

2Q 2017

3Q 2017

4Q 2017

1Q 2018

2Q 2018

3Q 2018

Localize content

100 store trial of local brands and merchandizing

Align employee incentives

Expand store concept Take over competition

First ever incentive plan for 130k store associates

Store managers to run business as own

Incentives based on whole store performance

Encouraging cooperation and positive environment NYC

(peacock coats) Dallas

(denim)

Rollout of first 120 Backstage locations

Entering attractive off-price market

Full offering store increases basket size and shopping frequency

TJ Maxx opportunity Sales sq. ft

+41%

Single channel competitors are closing down

Bon-Ton 252 stores

Sears 142 stores

Less local competition

60% overlap with Sears (5 miles)

Less comp. = SSS recovery

(3.0%)

(2.0%)

(1.0%)

0.0%

1.0%

2.0%

3.0% Closings

Core business restructuring complete 1

Reinvigorating the legacy portfolio

Source: Company filings

$141

$300

$424

Macy's (standalone)

Backstage T.J. Maxx

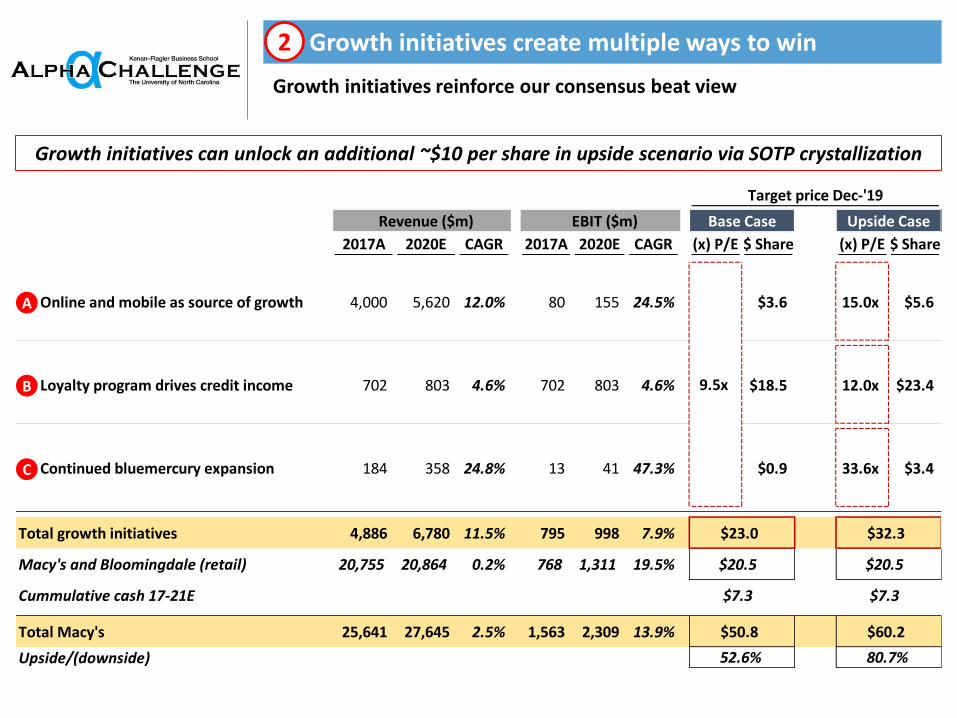

Growth initiatives create multiple ways to win 2

Growth initiatives reinforce our consensus beat view

Target price Dec-'19

Revenue ($m) EBIT ($m) Base Case Upside Case

2017A 2020E CAGR 2017A 2020E CAGR (x) P/E $ Share (x) P/E $ Share

Online and mobile as source of growth 4,000 5,620 12.0% 80 155 24.5% $3.6 15.0x $5.6

Loyalty program drives credit income 702 803 4.6% 702 803 4.6% $18.5 12.0x $23.4

Continued bluemercury expansion 184 358 24.8% 13 41 47.3% $0.9 33.6x $3.4

Total growth initiatives 4,886 6,780 11.5% 795 998 7.9% $23.0 $32.3

Macy's and Bloomingdale (retail) 20,755 20,864 0.2% 768 1,311 19.5% $20.5 $20.5

Cummulative cash 17-21E $7.3 $7.3

Total Macy's 25,641 27,645 2.5% 1,563 2,309 13.9% $50.8 $60.2

Upside/(downside) 52.6% 80.7%

9.5x

A

B

C

Growth initiatives can unlock an additional ~$10 per share in upside scenario via SOTP crystallization

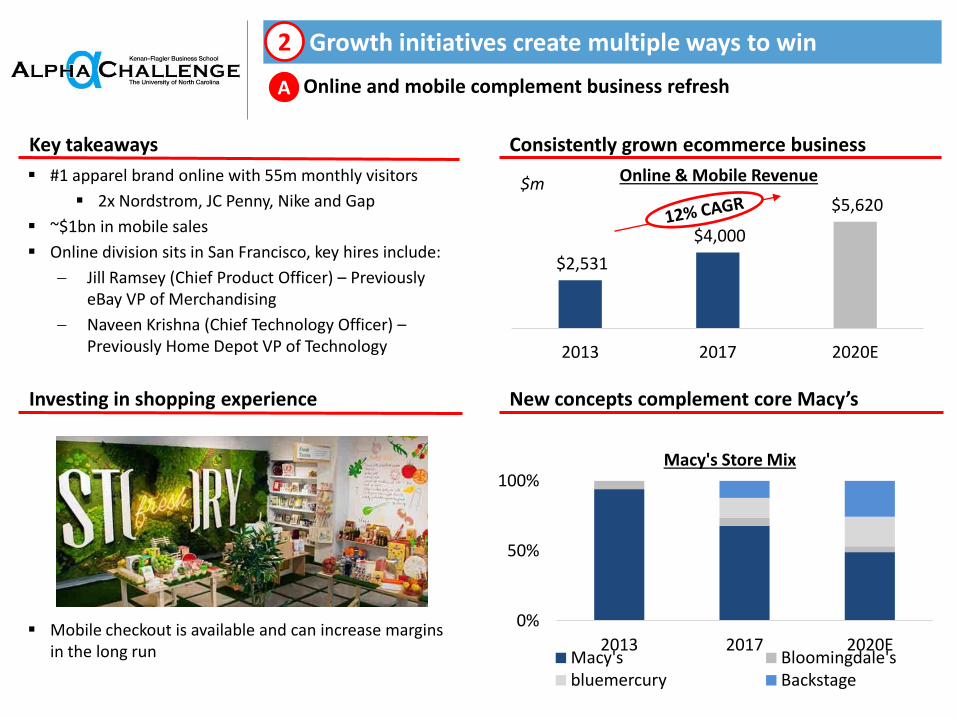

#1 apparel brand online with 55m monthly visitors

2x Nordstrom, JC Penny, Nike and Gap

~$1bn in mobile sales

Online division sits in San Francisco, key hires include:

Jill Ramsey (Chief Product Officer) – Previously eBay VP of Merchandising

Naveen Krishna (Chief Technology Officer) – Previously Home Depot VP of Technology

$2,531

$4,000

$5,620

2013 2017 2020E

Online & Mobile Revenue $m

0%

50%

100%

2013 2017 2020E

Macy's Store Mix

Macy's Bloomingdale's bluemercury Backstage

2 Growth initiatives create multiple ways to win

Online and mobile complement business refresh A

Consistently grown ecommerce business Key takeaways

Investing in shopping experience New concepts complement core Macy’s

Mobile checkout is available and can increase margins in the long run

Deal made with Citigroup in 2005. Income sharing agreement but Citi takes on all credit risk ~45% of Macy’s Sales are on Macy’s credit cards – reduces card transaction costs ~$700m business with ~100% cash EBIT margins Next phase of Card business is integrating rewards and promotions, creating stickier user base and

increasing card penetration

2 Growth initiatives create multiple ways to win

Loyalty integration with cards business B

Old Rewards Model New Rewards Model

Proprietary credit card business beneficial to Macys in multiple ways

Low Medium High Power Total

Avg Spend '17A ($) 122 246 600 2,077 407

Avg Spend '20E ($) 107 265 637 2,204 408

CAGR '17-'20 (4.1%) 2.5% 2.0% 2.0% 0.1%

# of customers '17A (m) 24.5 23.3 7.9 5.5 61.3

# of customers '20E (m) 27.3 24.7 8.1 5.5 65.7

CAGR '17-'20 3.7% 2.0% 1.0% 0.0% 2.4%

Total Macy's Sales '17A ($m) 2,993 5,736 4,738 11,472 24,939

Total Macy's Sales '20E ($m) 2,937 6,555 5,181 12,174 26,847

CAGR '17-'20 (0.6%) 4.6% 3.0% 2.0% 2.5%

% done via Macy's card '17A - 25.0% 40.0% 71.4% 46.2%

% done via Macy's card '20E - 28.8% 43.8% 74.1% 49.1%

Macy's Sales on Card '17A ($m) - 1,434 1,895 8,192 11,522

Macy's Sales on Card '20E ($m) - 1,885 2,267 9,021 13,173

CAGR '17-'20 n.m. 9.5% 6.1% 3.3% 4.6%

Credit take rate

Merchandise take reduction 2.5% 2.5% 2.5% 2.5% 2.5%

Other (orig. fee, portfolio perf.) 3.6% 3.6% 3.6% 3.6% 3.6%

Total take rate 6.1% 6.1% 6.1% 6.1% 6.1%

Credit income '17A - 87 115 499 702

Credit income '21E - 115 138 550 803

CAGR '17-'20 n.m. 9.5% 6.1% 3.3% 4.6%

EBIT margin 100.0% 100.0% 100.0% 100.0% 100.0%

~70% of credit

income

Macy’s customer base is very sticky: ~6m power users spend $2k p.a. and comprise 70% of credit income

2 Growth initiatives create multiple ways to win

Loyalty integration with cards business B

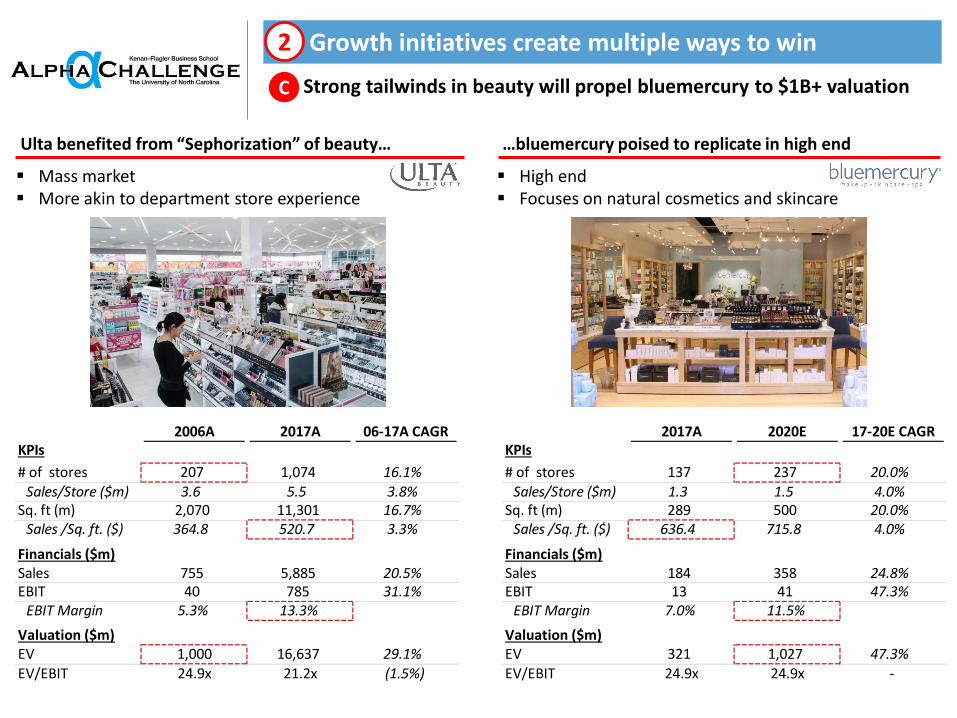

High end Focuses on natural cosmetics and skincare

Mass market More akin to department store experience

Ulta benefited from “Sephorization” of beauty… …bluemercury poised to replicate in high end

2 Growth initiatives create multiple ways to win

Strong tailwinds in beauty will propel bluemercury to $1B+ valuation C

2006A 2017A 06-17A CAGRKPIs

# of stores 207 1,074 16.1%

Sales/Store ($m) 3.6 5.5 3.8%Sq. ft (m) 2,070 11,301 16.7%

Sales /Sq. ft. ($) 364.8 520.7 3.3%

Financials ($m)Sales 755 5,885 20.5%EBIT 40 785 31.1%

EBIT Margin 5.3% 13.3%

Valuation ($m)EV 1,000 16,637 29.1%EV/EBIT 24.9x 21.2x (1.5%)

T.J. Maxx

2017A 2020E 17-20E CAGRKPIs

# of stores 137 237 20.0%

Sales/Store ($m) 1.3 1.5 4.0%Sq. ft (m) 289 500 20.0%

Sales /Sq. ft. ($) 636.4 715.8 4.0%

Financials ($m)Sales 184 358 24.8%EBIT 13 41 47.3%

EBIT Margin 7.0% 11.5%

Valuation ($m)EV 321 1,027 47.3%EV/EBIT 24.9x 24.9x -

20.7

14.2 15.2

StarboardValue '16 RE '18E Ent. Value

The value in Macy’s RE portfolio in $bn

(x) LFY Net PPE

2.72x 2.12x 2.28x

(x) LFY Gross PPE

1.60x 1.25x 1.35x

(x) LFY Gross PP

2.58x 2.00x 2.15x

Our view Value: $166 sq. ft. $128 sq. ft Net rent: $10 sq. ft $10 sq. ft

Cap rate: 6.0% 8.0%

2016

The Starboard Value story

Campaigned to unlock value via a RE JV and a partial sale and lease back

Starboard Value entered at ~$36/sh but exited after one year due to lack of short term catalyst

~1.0x EV

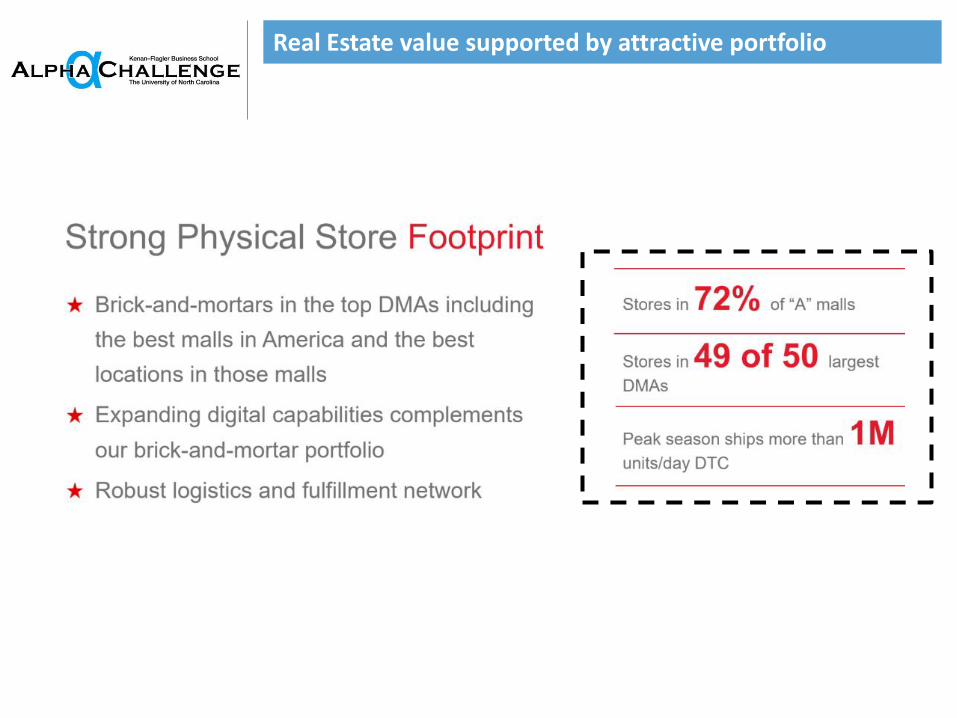

Some stores are in prime real estate locations

>$1bn of RE sale gains over L2Y

We view RE as downside protection

Talented inhouse RE team

Actively working on RE crystallization

3 Underappreciated downside protection via RE

Macy’s real estate value provides a margin of safety

Source: Multiples based of previous FY PP&E

in $bn

Value sq. ft. $1,830 $213 $95 $70 $128

Net rent sq. ft. $76 $17 $9 $7 $10

Cap rate 4.2% 8.0% 9.6% 10.0% 8.0%

+Δ 10Y T RE Val. Spread 6.0% 100bps 8.0% 100bps

Cap rate back-test

Google Chelsea Market acq. ($2.4bn

Mar-18) $2,016 sq. ft.

Locations: Downtown: 21% Tier A Mall: 51%

Lower Tier Mall: 28%

3 Underappreciated downside protection via RE

Herald Square alone worth ~26% of EV

4.0

1.1

6.9

2.2

14.2 15.2

4.8

10.4

Herald Square Bloomingdale's (owned &

ground leased)

Owned mall Ground leased RE Value Enterprise Value

Net debt Market Cap.

Cincinnati Business Courier, Apr-16 NY Post, Nov-16

3 Underappreciated downside protection via RE

Top talent proactively implementing real estate strategy

Consensus overly pessimistic

Market estimates limited turnaround

Historicals Consensus Base Case Deltas vs. consensus

FYE: 31-Jan, $m 2016 2017 2018 2019 2020 2018 2019 2020 2018 2019 2020Online Sales 3,556 4,000 4,000 4,000 4,000 4,480 5,018 5,620 480 1,018 1,620

% growth 12.0% 12.5% - - - 12.0% 12.0% 12.0% 12.0% 12.0% 12.0%% of total 13.4% 15.6% 15.9% 15.8% 15.8% 17.2% 18.8% 20.3% 1.3% 3.0% 4.6%

Retail Sales 22,352 20,939 20,394 20,527 20,605 20,802 20,931 21,222 408 404 617% growth (6.5%) (6.3%) (2.6%) 0.7% 0.4% (0.7%) 0.6% 1.4% 1.9% (0.0%) 1.0%% of total 84.1% 81.7% 81.2% 81.2% 81.1% 80.0% 78.3% 76.8% (1.2%) (2.8%) (4.4%)Comp store growth (3.0%) (1.9%) 2.2% 0.7% 0.5% 2.2% 2.8% 3.6% - 2.1% 3.1%Sq. Ft. growth (3.6%) (4.5%) (4.7%) (0.1%) (0.1%) (4.7%) (0.1%) (0.1%) - - -

Credit sales 656 702 730 759 790 734 768 803 4 8 13% growth (21.1%) 7.0% 4.0% 4.0% 4.0% 4.6% 4.6% 4.6% 0.6% 0.6% 0.6%% of total 2.5% 2.7% 2.9% 3.0% 3.1% 2.8% 2.9% 2.9% (0.1%) (0.1%) (0.2%)

Net Revenues 26,564 25,641 25,124 25,286 25,395 26,016 26,716 27,645 892 1,430 2,250% growth (4.8%) (3.5%) (2.0%) 0.6% 0.4% 1.5% 2.7% 3.5% 3.5% 2.0% 3.0%

Gross profit 10,898 10,460 10,122 10,152 10,327 10,667 11,007 11,445 545 855 1,118% margin 41.0% 40.8% 40.3% 40.1% 40.7% 41.0% 41.2% 41.4% 0.7% 1.1% 0.7%

EBITDA 2,754 2,554 2,778 2,540 2,482 2,944 3,079 3,191 166 539 709% margin 10.4% 10.0% 11.1% 10.0% 9.8% 11.3% 11.5% 11.5% 0.3% 1.5% 1.8%

D&A (849) (447) (931) (896) (907) 1,005 1,033 1,068 1,937 1,928 1,976% of capex 93.1% 58.8% 98.3% 98.0% 102.0% (123.2%) (126.5%) (130.9%) (221.5%) (224.6%) (232.9%)

EBIT 1,905 2,107 1,847 1,644 1,575 1,938 2,047 2,122 92 403 547% margin 7.2% 8.2% 7.3% 6.5% 6.2% 7.4% 7.7% 7.7% 0.1% 1.2% 1.5%

Interest (363) (310) (260) (260) (260) (260) (260) (194) - - 66

Tax (341) 29 (365) (318) (302) (386) (411) (443) (21) (93) (141)% tax rate (22.1%) 1.6% (23.0%) (23.0%) (23.0%) (23.0%) (23.0%) (23.0%) - - -

Other (582) (279) 25 28 62 - - - (25) (28) (62)

Net income 619 1,547 1,247 1,094 1,074 1,292 1,376 1,485 45 282 411% margin 2.3% 6.0% 5.0% 4.3% 4.2% 5.0% 5.2% 5.4% 0.0% 0.8% 1.1%

# of shares (m) 311 307 307 307 307 307 307 307 - - -EPS ($) $3.14 $3.79 $4.06 $3.57 $3.50 $3.97 $4.21 $4.58 ($0.09) $0.64 $1.08% growth (16.7%) 20.7% 7.2% (12.3%) (1.8%) 4.7% 5.9% 9.0% (2.5%) 18.2% 10.8%

By stripping online from SSS growth we see the potential of this segment

Diligence around costs and increased revenues give margin expansion

Base Case Upside Case Downside Case

TP (Jan-20): $50.8 / 42% IRR TP (Jan-20): $60.2 / 63% IRR TP (Jan-20): $30.5 / (7%) IRR

EPS: $4.58 ’20E

Cum. EFCF: $2.2bn ‘18-19E

’20E EPS @ 9.5x

$ per share $ per share $ per share

50.8

60.2

2.1

4.9

2.4

Base Case

Online (mult exp.)

Credit (mult exp.)

blumercury (mult exp.)

Upside Case

’20E EPS @ 15.0x

’20E EPS @ 12.0x

’20E EPS @ 33.6x

Compelling 42% IRR base case with downside protection

33.3

50.8

3.0

7.3

7.3

Share price

EPS growth

EFCF yield

Multiple exp.

Base Case

33.3

30.5

2.8

Share price

Downside

Downside Case

(RE value)

Sensitivities

Share price ($)

EPS '20E ($)

EPS CAGR '17-20 1.5% 4.0% 6.5% 9.0% 11.5%

3.96 4.26 4.58 4.91 5.26

7.5x 37.0 39.3 41.7 44.1 46.7

8.5x 41.0 43.5 46.2 49.1 52.0

9.5x 44.9 47.8 50.8 54.0 57.3

10.5x 48.9 52.1 55.4 58.9 62.5

11.5x 52.9 56.3 60.0 63.8 67.8

IRR

EPS '20E ($)

EPS CAGR '17-20 1.5% 4.0% 6.5% 9.0% 11.5%

3.96 4.26 4.58 4.91 5.26

7.5x 9.2% 14.6% 20.4% 26.3% 32.5%

8.5x 18.8% 24.9% 31.3% 37.9% 44.7%

9.5x 28.2% 34.9% 42.0% 49.3% 56.8%

10.5x 37.5% 44.9% 52.6% 60.4% 68.6%

11.5x 46.7% 54.6% 63.0% 71.5% 80.3%

fwd

P/E

fwd

P/E

Base Case

Share price ($)

RE Value '20E ($bn)

Implied yield 7.0% 8.0% 9.0% 10.0% 11.0%

16.2 14.2 12.6 11.3 10.3

- 37.1 30.5 25.4 21.3 17.9

(2.5%) 36.2 29.7 24.7 20.7 17.5

(5.0%) 35.2 29.0 24.1 20.2 17.0

(7.5%) 34.3 28.2 23.5 19.7 16.6

(10.0%) 33.4 27.5 22.8 19.1 16.1

IRR

RE Value '20E ($bn)

Implied yield 7.0% 8.0% 9.0% 10.0% 11.0%

16.2 14.2 12.6 11.3 10.3

- 9.4% (7.0%) (20.2%) (31.0%) (40.2%)

(2.5%) 7.1% (9.0%) (21.8%) (32.5%) (41.4%)

(5.0%) 4.8% (10.9%) (23.5%) (33.9%) (42.7%)

(7.5%) 2.5% (12.8%) (25.2%) (35.4%) (43.9%)

(10.0%) 0.2% (14.8%) (26.9%) (36.8%) (45.2%)

Liq

uid

ity

dis

c. (

%)

Liq

uid

ity

dis

c. (

%)

Downside Case

Mitigants Risks

Macroeconomic backdrop is weak and consumer/seasonal spending fails to materialize

Macy’s North Star omnichannel strategy does not improve operational performance

Amazon and other online retailers continue to make inroads into Macy’s core business model

Real estate strategy does not achieve monetization of intrinsic value

bluemercury and Macy’s Backstage retail efforts do not add to topline growth

Management is continuing its focus on restructuring and investing in cost-cutting efforts that should floor its bottom line. Margin pressure has eased off

Macy’s continues to boost its e-commerce efforts: hiring 6k more seasonal workers devoted to online sales for the 2018 holiday season and has stepped up efforts to expand the bluemercury online presence

In 2016, Macy’s finalized its alliance with Brookfield Asset Management that includes 2-year “pre-development plans” that enhance Macy’s operational and capital flexibility

Macy’s continues to accelerate investment in bluemercury with 24 and 36 new store openings in 2016 and 2017

Risks and mitigants

Appendix

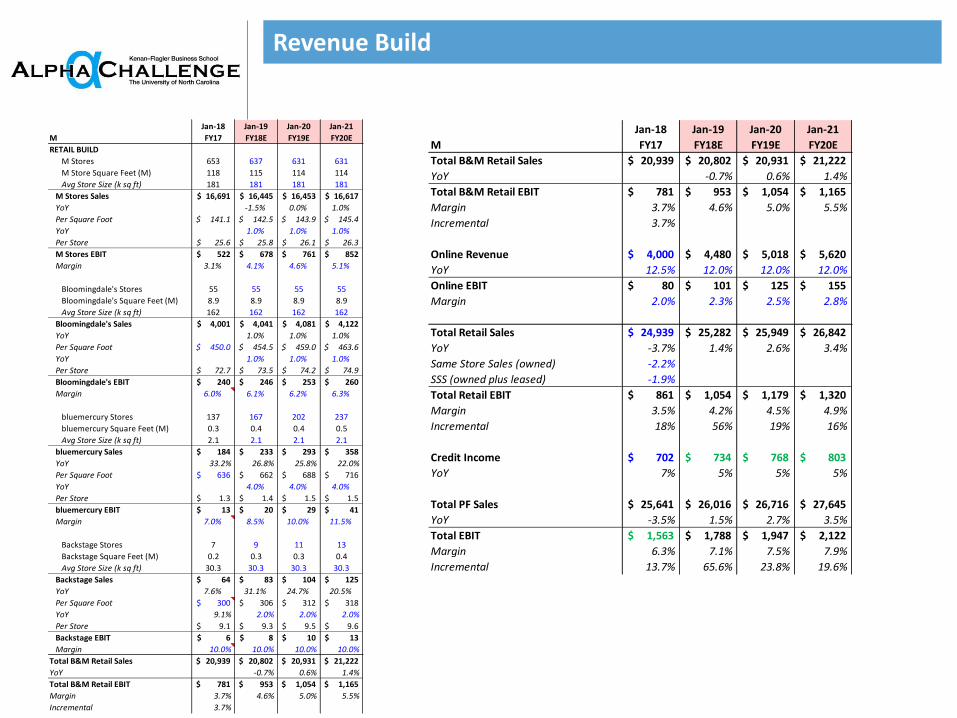

Revenue Build

Jan-18 Jan-19 Jan-20 Jan-21

M FY17 FY18E FY19E FY20E

RETAIL BUILD

M Stores 653 637 631 631

M Store Square Feet (M) 118 115 114 114

Avg Store Size (k sq ft) 181 181 181 181

M Stores Sales 16,691$ 16,445$ 16,453$ 16,617$

YoY -1.5% 0.0% 1.0%

Per Square Foot 141.1$ 142.5$ 143.9$ 145.4$

YoY 1.0% 1.0% 1.0%

Per Store 25.6$ 25.8$ 26.1$ 26.3$

M Stores EBIT 522$ 678$ 761$ 852$

Margin 3.1% 4.1% 4.6% 5.1%

Bloomingdale's Stores 55 55 55 55

Bloomingdale's Square Feet (M) 8.9 8.9 8.9 8.9

Avg Store Size (k sq ft) 162 162 162 162

Bloomingdale's Sales 4,001$ 4,041$ 4,081$ 4,122$

YoY 1.0% 1.0% 1.0%

Per Square Foot 450.0$ 454.5$ 459.0$ 463.6$

YoY 1.0% 1.0% 1.0%

Per Store 72.7$ 73.5$ 74.2$ 74.9$

Bloomingdale's EBIT 240$ 246$ 253$ 260$

Margin 6.0% 6.1% 6.2% 6.3%

bluemercury Stores 137 167 202 237

bluemercury Square Feet (M) 0.3 0.4 0.4 0.5

Avg Store Size (k sq ft) 2.1 2.1 2.1 2.1

bluemercury Sales 184$ 233$ 293$ 358$

YoY 33.2% 26.8% 25.8% 22.0%

Per Square Foot 636$ 662$ 688$ 716$

YoY 4.0% 4.0% 4.0%

Per Store 1.3$ 1.4$ 1.5$ 1.5$

bluemercury EBIT 13$ 20$ 29$ 41$

Margin 7.0% 8.5% 10.0% 11.5%

Backstage Stores 7 9 11 13

Backstage Square Feet (M) 0.2 0.3 0.3 0.4

Avg Store Size (k sq ft) 30.3 30.3 30.3 30.3

Backstage Sales 64$ 83$ 104$ 125$

YoY 7.6% 31.1% 24.7% 20.5%

Per Square Foot 300$ 306$ 312$ 318$

YoY 9.1% 2.0% 2.0% 2.0%

Per Store 9.1$ 9.3$ 9.5$ 9.6$

Backstage EBIT 6$ 8$ 10$ 13$

Margin 10.0% 10.0% 10.0% 10.0%

Total B&M Retail Sales 20,939$ 20,802$ 20,931$ 21,222$

YoY -0.7% 0.6% 1.4%

Total B&M Retail EBIT 781$ 953$ 1,054$ 1,165$

Margin 3.7% 4.6% 5.0% 5.5%

Incremental 3.7%

Jan-18 Jan-19 Jan-20 Jan-21

M FY17 FY18E FY19E FY20E

Total B&M Retail Sales 20,939$ 20,802$ 20,931$ 21,222$

YoY -0.7% 0.6% 1.4%

Total B&M Retail EBIT 781$ 953$ 1,054$ 1,165$

Margin 3.7% 4.6% 5.0% 5.5%

Incremental 3.7%

Online Revenue 4,000$ 4,480$ 5,018$ 5,620$

YoY 12.5% 12.0% 12.0% 12.0%

Online EBIT 80$ 101$ 125$ 155$

Margin 2.0% 2.3% 2.5% 2.8%

Total Retail Sales 24,939$ 25,282$ 25,949$ 26,842$

YoY -3.7% 1.4% 2.6% 3.4%

Same Store Sales (owned) -2.2%

SSS (owned plus leased) -1.9%

Total Retail EBIT 861$ 1,054$ 1,179$ 1,320$

Margin 3.5% 4.2% 4.5% 4.9%

Incremental 18% 56% 19% 16%

Credit Income 702$ 734$ 768$ 803$

YoY 7% 5% 5% 5%

Total PF Sales 25,641$ 26,016$ 26,716$ 27,645$

YoY -3.5% 1.5% 2.7% 3.5%

Total EBIT 1,563$ 1,788$ 1,947$ 2,122$

Margin 6.3% 7.1% 7.5% 7.9%

Incremental 13.7% 65.6% 23.8% 19.6%

Income Statement

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

M FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

INCOME STATEMENT

Revenue 24,892$ 23,489$ 25,003$ 26,405$ 27,686$ 27,931$ 28,105$ 27,079$ 26,564$ 25,641$ 26,016$ 26,716$ 27,645$

YoY -5.4% -5.6% 6.4% 5.6% 4.9% 0.9% 0.6% -3.7% -1.9% -3.5% 1.5% 2.7% 3.5%

Organic

Cost of Sales 15,009$ 13,973$ 14,824$ 15,738$ 16,538$ 16,725$ 16,863$ 16,496$ 15,666$ 15,181$ 15,349$ 15,709$ 16,200$

Gross Profit 9,883$ 9,516$ 10,179$ 10,667$ 11,148$ 11,206$ 11,242$ 10,583$ 10,898$ 10,460$ 10,667$ 11,007$ 11,445$

Margin 39.7% 40.5% 40.7% 40.4% 40.3% 40.1% 40.0% 39.1% 41.0% 40.8% 41.0% 41.2% 41.4%

SG&A 8,458$ 8,062$ 8,260$ 8,281$ 8,482$ 8,519$ 8,447$ 8,468$ 9,257$ 8,954$ 8,936$ 9,117$ 9,380$

Other -$ -$ -$ -$ -$ -$ -$ -$ (55)$ (57)$ (57)$ (57)$ (57)$

EBIT 1,425$ 1,454$ 1,919$ 2,386$ 2,666$ 2,687$ 2,795$ 2,115$ 1,696$ 1,563$ 1,788$ 1,947$ 2,122$

Margin 5.7% 6.2% 7.7% 9.0% 9.6% 9.6% 9.9% 7.8% 6.4% 6.1% 6.9% 7.3% 7.7%

Incremental 46.2% -2.1% 30.7% 33.3% 21.9% 8.6% 62.1% 66.3% 81.4% 14.4% 60.0% 22.7% 18.9%

(Gain) on Property Sales (79)$ (92)$ (212)$ (209)$ (544)$ (150)$ (100)$ -$

Interest 560$ 556$ 535$ 443$ 426$ 388$ 393$ 361$ 363$ 310$ 260$ 260$ 194$

Taxes 334$ 301$ 482$ 703$ 814$ 839$ 903$ 713$ 574$ 645$ 471$ 508$ 533$

Tax Rate 16.8% 15.0% 19.7% 24.9% 26.3% 35.3% 36.2% 36.2% 37.2% 35.9% 23.0% 23.0% 23.0%

Non-controlling Interest 2$ 8$ 11$ 11$ 11$ 11$

Adjusted Net Income 531$ 597$ 902$ 1,240$ 1,426$ 1,539$ 1,591$ 1,255$ 976$ 1,163$ 1,218$ 1,290$ 1,406$

Adjusted EPS 1.26$ 1.41$ 2.11$ 2.88$ 3.46$ 4.00$ 4.40$ 3.77$ 3.14$ 3.79$ 3.97$ 4.21$ 4.58$

YoY -41.4% 11.9% 49.6% 36.5% 20.1% 15.6% 10.0% -14.3% -16.7% 20.7% 4.7% 5.9% 9.0%

Diluted Shares 421.2 423.2 427.3 430.4 412.2 384.8 361.7 333.0 310.8 306.8 306.8 306.8 306.8

Dividends 0.53$ 0.20$ 0.20$ 0.35$ 0.80$ 0.95$ 1.19$ 1.39$ 1.49$ 1.51$ 1.66$ 1.83$ 2.01$

YoY 1.9% -62.1% 0.0% 75.0% 128.6% 18.8% 25.0% 17.3% 7.2% 1.2% 10.0% 10.0% 10.0%

EBITDA 2,703$ 2,664$ 3,069$ 3,471$ 3,715$ 3,707$ 3,831$ 3,176$ 2,754$ 2,554$ 2,794$ 2,979$ 3,191$

NOPAT 1,185$ 1,236$ 1,542$ 1,793$ 1,964$ 1,739$ 1,784$ 1,348$ 1,065$ 1,002$ 1,377$ 1,499$ 1,634$

Balance Sheet

BALANCE SHEET FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Cash & Equivalents 1,306$ 1,686$ 1,516$ 2,879$ 1,918$ 2,310$ 2,283$ 1,146$ 1,334$ 1,492$ 1,642$ 2,525$ 3,443$

Accounts Receivable 439$ 358$ 392$ 368$ 371$ 438$ 424$ 558$ 522$ 363$ 374$ 394$ 422$

Inventory 4,769$ 4,615$ 4,758$ 5,117$ 5,308$ 5,557$ 5,516$ 5,506$ 5,399$ 5,178$ 5,235$ 5,358$ 5,525$

Other Current Assets 226$ 223$ 233$ 413$ 279$ 383$ 456$ 442$ 371$ 411$ 411$ 411$ 411$

Total Current Assets 6,740$ 6,882$ 6,899$ 8,777$ 7,876$ 8,688$ 8,679$ 7,652$ 7,626$ 7,444$ 7,663$ 8,688$ 9,802$

PP&E 10,442$ 9,507$ 8,813$ 8,420$ 8,196$ 7,930$ 7,800$ 7,616$ 7,017$ 6,672$ 6,438$ 6,197$ 5,948$

Goodwill & Intangibles 4,462$ 4,421$ 4,380$ 4,341$ 4,304$ 4,270$ 4,239$ 4,411$ 4,395$ 4,385$ 4,385$ 4,385$ 4,385$

Other LT Assets 501$ 490$ 539$ 557$ 615$ 746$ 743$ 2,186$ 2,126$ 880$ 880$ 880$ 880$

Total Assets 22,145$ 21,300$ 20,631$ 22,095$ 20,991$ 21,634$ 21,461$ 21,865$ 21,164$ 19,381$ 19,365$ 20,150$ 21,015$

ST Debt 966$ 242$ 454$ 1,103$ 124$ 463$ 76$ 642$ 309$ 22$ 22$ 22$ 22$

Accounts Payable 1,893$ 1,796$ 1,980$ 2,262$ 2,204$ 2,437$ 2,526$ 2,340$ 2,177$ 2,325$ 2,351$ 2,406$ 2,481$

Other Current Liabilities 2,267$ 2,416$ 2,631$ 2,898$ 2,747$ 2,826$ 2,934$ 2,746$ 3,161$ 2,728$ 2,728$ 2,728$ 2,728$

Total Current Liabilities 5,126$ 4,454$ 5,065$ 6,263$ 5,075$ 5,726$ 5,536$ 5,728$ 5,647$ 5,075$ 5,101$ 5,156$ 5,231$

LT Debt 8,733$ 8,456$ 6,971$ 6,655$ 6,806$ 6,728$ 7,265$ 6,995$ 6,562$ 5,861$ 5,111$ 5,111$ 5,111$

Other LT Liabilities 3,640$ 3,689$ 3,065$ 3,244$ 3,059$ 2,931$ 3,282$ 4,892$ 4,632$ 2,784$ 2,784$ 2,784$ 2,784$

Total Liabilties 17,499$ 16,599$ 15,101$ 16,162$ 14,940$ 15,385$ 16,083$ 17,615$ 16,841$ 13,720$ 12,996$ 13,051$ 13,126$

Total Equity 4,646$ 4,701$ 5,530$ 5,933$ 6,051$ 6,249$ 5,378$ 4,250$ 4,323$ 5,661$ 6,369$ 7,099$ 7,889$

Total Liabilities & Equity 22,145$ 21,300$ 20,631$ 22,095$ 20,991$ 21,634$ 21,461$ 21,865$ 21,164$ 19,381$ 19,365$ 20,150$ 21,015$

Check - - - - - - - - - - - - -

Operational Metrics

Day Sales Outstanding 6 6 6 5 5 6 6 8 7 5 5 5 6

Inventory Days 116 121 117 119 117 121 119 122 126 125 125 125 125

Days Payable 46 47 49 52 49 53 55 52 51 56 56 56 56

Working Capital % of Revenue 13% 14% 13% 12% 13% 13% 12% 14% 14% 13% 13% 13% 13%

ROIC 9% 9% 12% 14% 15% 13% 14% 12% 10% 9% 12% 12% 13%

Tangible ROIC 12% 14% 18% 19% 23% 19% 21% 18% 16% 14% 19% 19% 19%

Leverage & Debt

Gross Debt/ TTM EBITDA 3.6x 3.3x 2.4x 2.2x 1.9x 1.9x 1.9x 2.4x 2.5x 2.3x 1.8x 1.7x 1.6x

Net Debt/ TTM EBITDA 3.1x 2.6x 1.9x 1.4x 1.3x 1.3x 1.3x 2.0x 2.0x 1.7x 1.2x 0.9x 0.5x

Interest on Net Debt 6.7% 7.9% 9.1% 9.1% 8.5% 7.9% 7.8% 5.6% 6.6% 7.1% 7.4% 7.4% 7.4%

Cash Flow Statement

CASH FLOW STATEMENT FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Net Income (4,803)$ 350$ 847$ 1,256$ 1,335$ 1,486$ 1,526$ 1,074$ 611$ 1,536$ 1,218$ 1,290$ 1,406$

D&A 1,278$ 1,210$ 1,150$ 1,085$ 1,049$ 1,020$ 1,036$ 1,061$ 1,058$ 991$ 1,005$ 1,033$ 1,068$

SBC 43$ 76$ 66$ 70$ 61$ 62$ 73$ 65$ 61$ 58$ 58$ 58$ 58$

Changes in Working Capital (101)$ (350)$ (798)$ (431)$ (187)$ 43$ (37)$ (485)$ (144)$ 69$ (42)$ (88)$ (120)$

Other 5,449$ 464$ 241$ 113$ 3$ (62)$ 111$ 269$ 215$ (710)$ -$ -$ -$

Cash From Operations 1,866$ 1,750$ 1,506$ 2,093$ 2,261$ 2,549$ 2,709$ 1,984$ 1,801$ 1,944$ 2,239$ 2,293$ 2,413$

Capex (897)$ (460)$ (505)$ (764)$ (942)$ (863)$ (1,068)$ (1,113)$ (912)$ (760)$ (771)$ (792)$ (819)$

Net M&A -$ -$ -$ -$ -$ -$ -$ (212)$ -$ -$ -$ -$ -$

Other 105$ 83$ 40$ 147$ 79$ 75$ 98$ 238$ 729$ 400$ -$ -$ -$

Cash From Investing (792)$ (377)$ (465)$ (617)$ (863)$ (788)$ (970)$ (1,087)$ (183)$ (360)$ (771)$ (792)$ (819)$

Change in Debt (150)$ (995)$ (1,221)$ 375$ (902)$ 291$ 298$ 260$ (691)$ (970)$ (750)$ -$ -$

Share Repurchase/Issuance 6$ 7$ 42$ (340)$ (1,163)$ (1,256)$ (1,643)$ (1,838)$ (280)$ 5$ (58)$ (58)$ (58)$

Dividends (221)$ (84)$ (84)$ (148)$ (324)$ (359)$ (421)$ (456)$ (459)$ (461)$ (510)$ (561)$ (617)$

Other -$ -$ -$ -$ -$ -$ -$ -$ -$ -$ -$ -$ -$

Cash From Financing (365)$ (1,072)$ (1,263)$ (113)$ (2,389)$ (1,324)$ (1,766)$ (2,034)$ (1,430)$ (1,426)$ (1,318)$ (619)$ (675)$

Net Change in Cash 709$ 301$ (222)$ 1,363$ (991)$ 437$ (27)$ (1,137)$ 188$ 158$ 150$ 882$ 919$

Beginning Cash 676$ 1,385$ 1,686$ 1,464$ 2,827$ 1,836$ 2,273$ 2,246$ 1,109$ 1,297$ 1,455$ 1,605$ 2,488$

Ending Cash 1,385$ 1,686$ 1,464$ 2,827$ 1,836$ 2,273$ 2,246$ 1,109$ 1,297$ 1,455$ 1,605$ 2,488$ 3,406$

Operational Metrics

Capex % of Sales 3.6% 2.0% 2.0% 2.9% 3.4% 3.1% 3.8% 4.1% 3.4% 3.0% 3.0% 3.0% 3.0%

D&A % of Sales 5.1% 5.2% 4.6% 4.1% 3.8% 3.7% 3.7% 3.9% 4.0% 3.9% 3.9% 3.9% 3.9%

1$

FCF 969$ 1,290$ 1,001$ 1,329$ 1,319$ 1,686$ 1,641$ 871$ 889$ 1,184$ 1,468$ 1,501$ 1,593$

Conversion (on adj. EPS) 182.6% 216.2% 111.0% 107.2% 92.5% 109.5% 103.1% 9.0% 91.1% 101.8% 120.5% 116.3% 113.3%

Margin 3.9% 5.5% 4.0% 5.0% 4.8% 6.0% 5.8% 3.2% 3.3% 4.6% 5.6% 5.6% 5.8%

FCF/Share 2.30$ 3.05$ 2.34$ 3.09$ 3.20$ 4.38$ 4.54$ 2.62$ 2.86$ 3.86$ 4.78$ 4.89$ 5.19$

uFCF 1,435$ 1,763$ 1,431$ 1,662$ 1,633$ 1,937$ 1,892$ 1,101$ 1,117$ 1,383$ 1,668$ 1,701$ 1,743$

Valuation Over Time

Valuation Vs Comps

1,830

213

128

95 86

70

Herald Square Bloomingdale's (owned &

ground leased)

Tier 1 (owned malls)

ToysRus Tier 2-3 (owned malls)

Ground leased

$ sq. ft.

…leading to our conservative assumptions RE value not always there…

$ sq. ft.

Source: ToysRUs CMBS

~10-30% discount to

ToysRUs fire sale values

~10-30% discount to

ToysRUs fire sale values

Fully priced based on already conservative

view

Downside valuation – conservative words of caution

~$161

~$93

Appraisal Final value

(42%) below

• Loyalty efforts + omni-channel investment strengthen high-value customer relationships

• Nascent Backstage concept (TJX analog) could build younger customer base

Macy’s sticky customer base is high-income

Source: Coresight Research

Macy’s customer demographic

Best Buy Case Study

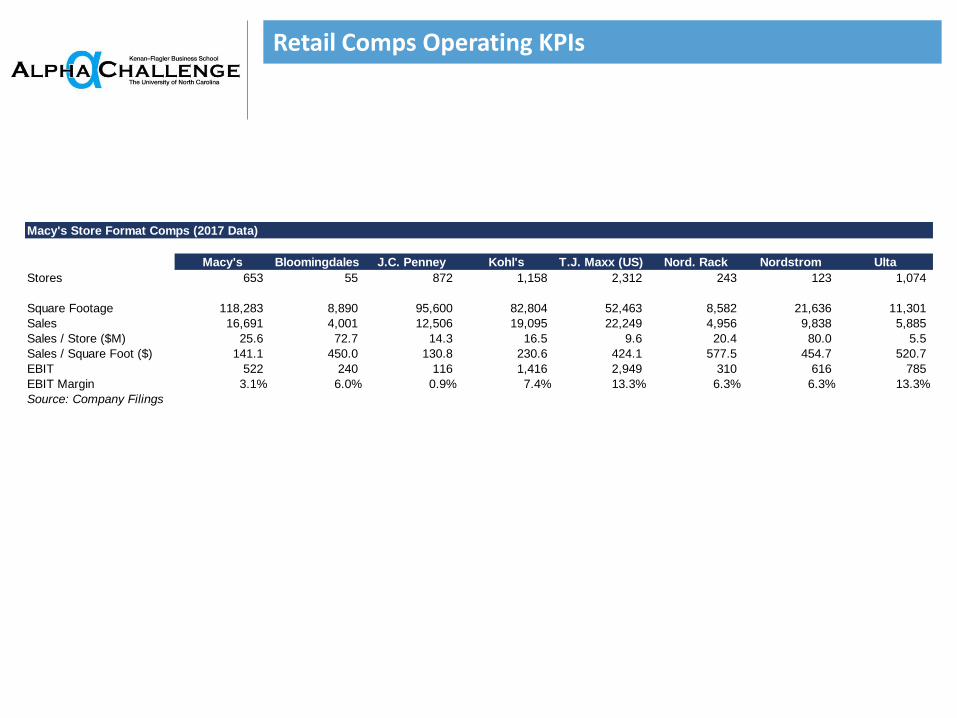

Retail Comps Operating KPIs

Macy's Store Format Comps (2017 Data)

Macy's Bloomingdales J.C. Penney Kohl's T.J. Maxx (US) Nord. Rack Nordstrom Ulta

Stores 653 55 872 1,158 2,312 243 123 1,074

Square Footage 118,283 8,890 95,600 82,804 52,463 8,582 21,636 11,301

Sales 16,691 4,001 12,506 19,095 22,249 4,956 9,838 5,885

Sales / Store ($M) 25.6 72.7 14.3 16.5 9.6 20.4 80.0 5.5

Sales / Square Foot ($) 141.1 450.0 130.8 230.6 424.1 577.5 454.7 520.7

EBIT 522 240 116 1,416 2,949 310 616 785

EBIT Margin 3.1% 6.0% 0.9% 7.4% 13.3% 6.3% 6.3% 13.3%

Source: Company Filings

Trading Comparables

Comps Market Net Debt / EBITDA Margin Net Margin Div

Ticker Name Cap EV EBITDA '19E '20E '19E '20E '19E '20E '19E '20E '19E '20E Yield

JCP-US J. C. Penney Company, Inc. 408 4,707 6.8x 0.4x 0.4x 7.4x 6.8x 5.4% 6.0% NM NM -1.6% -1.8% 0.0%

JWN-US Nordstrom, Inc. 8,780 10,339 0.9x 0.6x 0.6x 6.1x 5.9x 10.3% 10.4% 13.7x 12.9x 3.9% 4.0% 3.0%

KSS-US Kohl's Corporation 12,033 14,899 1.2x 0.7x 0.7x 6.1x 6.1x 12.4% 12.3% 13.0x 12.4x 4.7% 4.9% 3.7%

Department Store Average 3.0x 0.6x 0.6x 6.5x 6.3x 9.3% 9.6% 13.4x 12.7x 2.3% 2.4% 2.2%

TJX-US TJX Companies Inc 65,182 64,542 -0.1x 1.6x 1.5x 12.1x 10.6x 13.0% 14.0% 19.7x 18.9x 8.1% 7.9% 1.7%

ROST-US Ross Stores, Inc. 35,608 34,609 -0.4x 2.2x 2.0x 13.4x 12.4x 16.2% 16.4% 21.7x 20.2x 10.3% 10.4% 1.1%

BURL-US Burlington Stores, Inc. 11,123 12,170 1.2x 1.7x 1.6x 13.7x 12.4x 12.3% 12.6% 23.2x 20.9x 6.6% 6.9% 0.0%

Off-Price Retail Average 0.2x 1.8x 1.7x 13.1x 11.8x 13.8% 14.3% 21.6x 20.0x 8.3% 8.4% 0.9%

ULTA-US Ulta Beauty Inc 18,931 18,545 -0.3x 2.5x 2.2x 14.4x 12.8x 17.2% 17.5% 25.2x 22.5x 10.0% 10.2% 0.0%

M-US Macy's Inc 10,396 15,194 1.8x 0.6x 0.6x 5.8x 6.1x 10.3% 9.9% 9.3x 9.1x 4.4% 4.5% 4.7%

EV/Sales EV/EBITDA P/E

Real Estate value supported by attractive portfolio

Source: Brookfield Property Partners

Omnichannel Macy’s has staying power

Newpark Mall (San Francisco) case study:

Closing Target, JC Penny, and Burlington Coat Factory to build 1,200 new apartments and restaurants

Macy’s will remain, which provides excellent future opportunity for increase in patronage coupled with less retail competition

Reduction in retail competition leads to pockets of opportunity for well-prepared Macy’s; recently:

Bon-Ton closing all 256 department stores after April bankruptcy

Sears announced 142 store closures with its October Chapter 11 announcement

Source: Goldman Research

% of 2018 closed Sears stores within X miles of other retailers

Closure of marginal retailers reduces competition

Live events drive traffic..

Mobile enables fast checkout..

Ecommerce leverages stores..

Online and mobile integrate with store experience

Backstage trials show promise

“We took swift action to accelerate inventory turns, strengthen our core assortment and improve our execution in stores. Our second quarter comp sales exceeded our plans by a couple of hundred basis points, and we expect to carry and build upon this momentum during the second half of the year” – CEO, 2Q18 Earnings

CLEARING THE RACKS, A NICE COMP SURPRISE - “Comps improved +4.0%... well ahead of Cowen's and Street's estimates (+0.8%)” – Cowen Research

Management Reaction

Sell-side Reaction

Comp sales increase surprised many, including management, JWN up 9% on these earnings

Nordstrom Upside Surprise Case Study