STRUCTURING PROFITS INTERESTS IN LLCS/PARTNERSHIPS …€¦ · · 2014-02-25STRUCTURING PROFITS...

95

STRUCTURING PROFITS INTERESTS IN LLCS/PARTNERSHIPS First Run Broadcast: February 26, 2014 1:00 p.m. E.T. (60 minutes) Profits interests in LLCs and partnerships are an effective mechanism for giving members, managers or employees a stake in the financial success of the company without ceding control or necessarily triggering immediate taxable gain. The recipient has an incentive to help grow the company and the LLC’s owners fund the incentive payments through future, additive revenue. But there are a wide variety of ways of structuring profits interests, each with subtle financial, tax and operational tradeoffs. Profits interests can be out of future “profit,” with all the definitional vagaries of that term, or can mimic capital interests, with appreciation rights. This program will provide you with a practical framework for understanding the types of profits interests and the tradeoffs of each in the context of an LLC and partnership. Understanding types of “profits interest” and alternatives in LLCs/partnerships Profits interests based on fixed percentages v. “fill up” allocations Payouts based on operating profits v. capital profits v. appreciation in the company State law status and rights of profits interest and governance/operating issues Federal income tax consequences of each type of profits interest Drafting issues related to allocations, distributions, vesting, and forfeiture Speakers: Lee Lyman is a shareholder in the Atlanta office of Carlton Fields, where she has more than 20 years’ experience in corporate and real estate transactions. She provides corporate and transactional advice, with an emphasis on advising clients engaged in ongoing business transactions, including joint ventures, mergers and acquisitions, and business restructurings. She has extensive experience in LLC and partnership law, organization, structure, and operations. She has extensive experience structuring equity and debt financing for the acquisition, development and sale of real estate and in general corporate transactions. Ms. Lyman received her B.S. from Florida State University, her M.A. from the University of Pittsburg, her J.D. from Duke University School of Law. Leon Andrew Immerman is a partner in the Atlanta office of Alston & Bird, LLP, where he concentrates on federal income tax matters, including domestic and international tax planning and transactional work for joint ventures, partnerships, limited liability companies and corporations. He formerly served as chair of the Committee on Taxation of the ABA Business Law Section and as chair of the Partnership and LLC Committee of the State Bar of Georgia Business Law Section. He is also co-author of “Georgia Limited Liability Company Forms and Practice Manual” (2d ed. 1999, and annual supplements). Mr. Immerman received his B.A., magna cum laude, from Carleton College, his M.A. from the University of Minnesota, and another M.A. and his Ph.D. from Princeton University, and his J.D. from Yale Law School.

Transcript of STRUCTURING PROFITS INTERESTS IN LLCS/PARTNERSHIPS …€¦ · · 2014-02-25STRUCTURING PROFITS...

STRUCTURING PROFITS INTERESTS IN LLCS/PARTNERSHIPS

First Run Broadcast: February 26, 2014

1:00 p.m. E.T. (60 minutes)

Profits interests in LLCs and partnerships are an effective mechanism for giving members,

managers or employees a stake in the financial success of the company without ceding control or

necessarily triggering immediate taxable gain. The recipient has an incentive to help grow the

company and the LLC’s owners fund the incentive payments through future, additive revenue.

But there are a wide variety of ways of structuring profits interests, each with subtle financial,

tax and operational tradeoffs. Profits interests can be out of future “profit,” with all the

definitional vagaries of that term, or can mimic capital interests, with appreciation rights. This

program will provide you with a practical framework for understanding the types of profits

interests and the tradeoffs of each in the context of an LLC and partnership.

Understanding types of “profits interest” and alternatives in LLCs/partnerships

Profits interests based on fixed percentages v. “fill up” allocations

Payouts based on operating profits v. capital profits v. appreciation in the company

State law status and rights of profits interest and governance/operating issues

Federal income tax consequences of each type of profits interest

Drafting issues related to allocations, distributions, vesting, and forfeiture

Speakers:

Lee Lyman is a shareholder in the Atlanta office of Carlton Fields, where she has more than 20

years’ experience in corporate and real estate transactions. She provides corporate and

transactional advice, with an emphasis on advising clients engaged in ongoing business

transactions, including joint ventures, mergers and acquisitions, and business restructurings. She

has extensive experience in LLC and partnership law, organization, structure, and operations.

She has extensive experience structuring equity and debt financing for the acquisition,

development and sale of real estate and in general corporate transactions. Ms. Lyman received

her B.S. from Florida State University, her M.A. from the University of Pittsburg, her J.D. from

Duke University School of Law.

Leon Andrew Immerman is a partner in the Atlanta office of Alston & Bird, LLP, where he

concentrates on federal income tax matters, including domestic and international tax planning

and transactional work for joint ventures, partnerships, limited liability companies and

corporations. He formerly served as chair of the Committee on Taxation of the ABA Business

Law Section and as chair of the Partnership and LLC Committee of the State Bar of Georgia

Business Law Section. He is also co-author of “Georgia Limited Liability Company Forms and

Practice Manual” (2d ed. 1999, and annual supplements). Mr. Immerman received his B.A.,

magna cum laude, from Carleton College, his M.A. from the University of Minnesota, and

another M.A. and his Ph.D. from Princeton University, and his J.D. from Yale Law School.

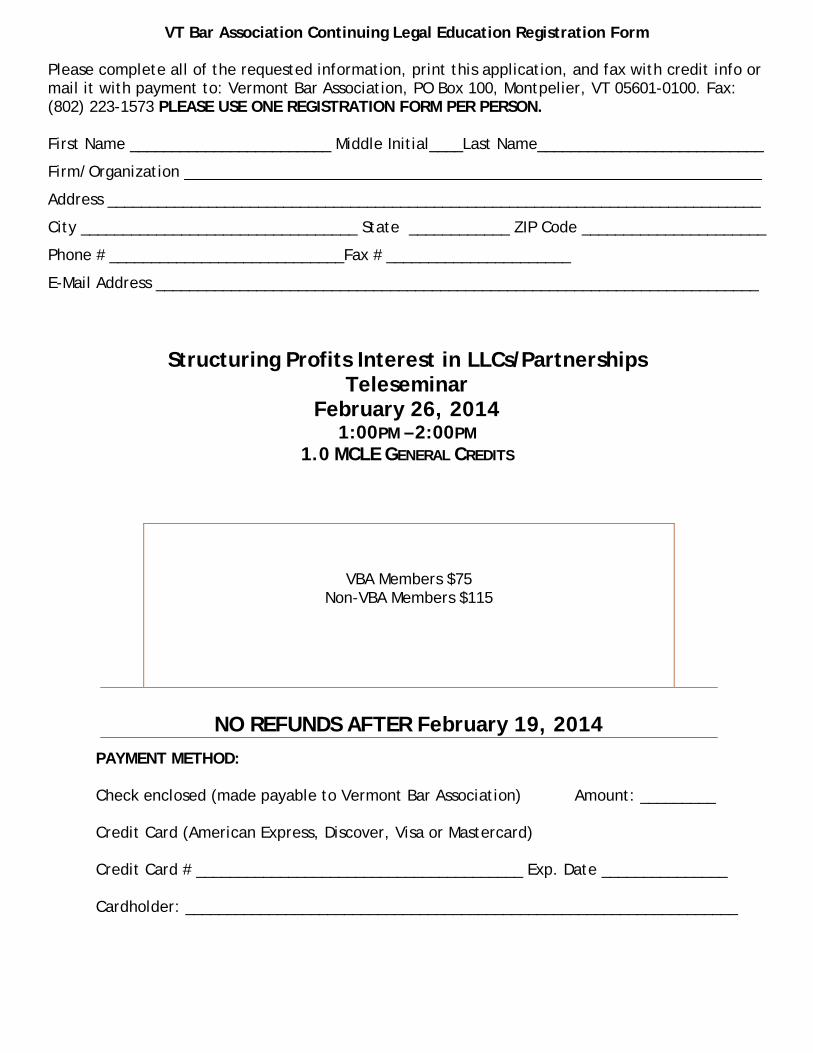

VT Bar Association Continuing Legal Education Registration Form

Please complete all of the requested information, print this application, and fax with credit info or mail it with payment to: Vermont Bar Association, PO Box 100, Montpelier, VT 05601-0100. Fax: (802) 223-1573 PLEASE USE ONE REGISTRATION FORM PER PERSON. First Name ________________________ Middle Initial____Last Name___________________________

Firm/Organization _____________________________________________________________________

Address ______________________________________________________________________________

City _________________________________ State ____________ ZIP Code ______________________

Phone # ____________________________Fax # ______________________

E-Mail Address ________________________________________________________________________

Structuring Profits Interest in LLCs/Partnerships

Teleseminar February 26, 2014

1:00PM – 2:00PM 1.0 MCLE GENERAL CREDITS

PAYMENT METHOD:

Check enclosed (made payable to Vermont Bar Association) Amount: _________ Credit Card (American Express, Discover, Visa or Mastercard) Credit Card # _______________________________________ Exp. Date _______________ Cardholder: __________________________________________________________________

VBA Members $75

Non-VBA Members $115

NO REFUNDS AFTER February 19, 2014

Vermont Bar Association

CERTIFICATE OF ATTENDANCE

Please note: This form is for your records in the event you are audited Sponsor: Vermont Bar Association Date: February 26, 2014 Seminar Title: Structuring Profits Interest in LLCs/Partnerships Location: Teleseminar Credits: 1.0 MCLE General Credit Luncheon addresses, business meetings, receptions are not to be included in the computation of credit. This form denotes full attendance. If you arrive late or leave prior to the program ending time, it is your responsibility to adjust CLE hours accordingly.

Profits Interestsin

LLCs and Partnerships

L. Andrew ImmermanAlston & Bird LLP – Atlanta

(o) (404) [email protected]

22

LLC = Partnership

In this outline:Any LLC (other than a single-member LLC) is

assumed to be classified as a partnership forincome tax purposes. So in most of this outline, “partnership” and “LLC” are

interchangeable.

A single-member LLC is assumed to be“disregarded” as an entity separate from its ownerfor income tax purposes (but not, as explainedbelow, for employment tax purposes).

Classifying LLC members as “limited partners” forcompensation purposes is discussed below.

333

Introduction: Basic Investment Fund

2% Service Fee

Investors

Investments

IndividualManagers

20% Profits Interest

1% Capital

Manager,LLC

99% Capital

Affiliate, LLC

Fund,

LLC

4

Introduction: Different Kinds of Income

Fee/Salary: In private equity and many other types of investment vehicles, the

Manager (who may be an LLC member or a general partner) ispaid an annual fee (payable in quarterly installments equal to apercentage (typically 2%) of the total amount of capitalcommitments. While originally designed to cover day-to-dayexpenses of the fund manager, over time, it has come to be anindependent source of profits for the fund managers. Managersreceiving the annual fee are often affiliates of the LLC member orgeneral partner, and not members or partners directly.

In operating businesses, members are often paid a “salary” inaddition to (or instead of) a profits interest. If someone receivesboth a salary and a profits interest from the same LLC, the IRSsays that the person is self-employed and the salary is technicallynot treated as wages, as discussed below.

4

5

Introduction: Different Kinds of Income

Return on Capital:

Most investment funds want the Manager tohave some “skin in the game” and thusrequire a contribution of a specifiedpercentage of the invested capital (often just1%).

When capital is called from the investors,the Manager is obligated to contribute itsspecific share of invested capital.

Capital contributions are sometimesrequired by operating businesses grantingprofits interests, but this is less common.

5

6

Introduction: Different Kinds of Income

Profits Interest/Carried interest/Promote: The core concept of a profits interest (or “carry” or “promote”) is that the

member has a share of profits that is disproportionate to the member’sshare of contributed capital.

The words “carried interest” or “promote” are commonly used to refer toprofits interests in investment vehicles; for present purposes all theseterms refer to the same thing.

It is an interest in future income of the LLC, including operating incomeand/or appreciation in value.

Managers of investment vehicles often receive some fixed percentage ofnet profits (often 20%), after some hurdle is reached.

Operating businesses often grant profits interests to key individuals whowork for the business.

A profits interest is a form of equity compensation for services – theholder is considered a “partner” for tax purposes. This outline sometimesrefers to any holder of a profits interest as a Manager.

A “capital interest” also may be used as equity compensation, but asdiscussed later is less commonly used than a profits interest.

6

77

An employee or other service provider istaxable on the receipt of C Corp or S Corpstock as compensation for services,although the tax can be deferred until thestock is vested. Code § 83.

As explained below, a service provider isgenerally not taxable on receipt of a vestedor unvested "profits interest" in an LLC ascompensation for services to or for the LLC.

Equity for Services: Corp vs. LLC

88

Example: Equity for Services

A and B form X. Each hasan equal interest.

A contributes property witha fair market value of$1,000 and a basis of zero.

B contributes futureservices that he willperform for X, and receivesan unrestricted interest inX.

A B

FMV = $1,000Basis = 0 Services

X

99

Equity for Services: X is a Corp

If X is a corporation:

A and B both have taxable gain.

A has gain, equal to $1,000, because he isnot in control of X immediately after theexchange (and is not part of an 80% controlgroup). § 351.

B has taxable ordinary income equal to $500(assumed to be the value of his interest in X).

However, X may have a $500 deduction forthe compensation to B.

1010

Equity for Services: X is an LLC

If X is an LLC:

A has no taxable gain. § 721 (no

requirement of 80% control).

As explained below, in general B also will

have no taxable gain if he receives only a

profits interest in X.

However, if B receives a capital interest B will

be taxable.

1111

Property Transfers

A challenge in determining the taxconsequences of compensatory LLC interestsis coordinating and reconciling two perhapsirreconcilable sets of rules:

§ 83 (transfer of property in connection with theperformance of services), based on fair marketvalue concepts.

Subchapter K (partnership tax), based on capitalaccount concepts.

1212

Property Transfers

General rules of § 83 (not specific topartnerships):

Taxable event occurs at grant, or when propertyis transferable or no longer subject to substantialrisk of forfeiture (i.e., substantially vested).

Amount included in income of service provider isfair market value of property over amount paid (ifany).

Deduction allowed to business for amountincluded in income by service provider.

1313

Property Transfers

§ 83(b) election:

Service provider may elect to includevalue of unvested property incompensation income at time oftransfer.

Subsequent appreciation in value isgenerally capital gain.

Election must be made within 30 days oftransfer – no exceptions.

1414

Profits Interest Defined

Rev Proc 93-27, 1993-2 CB 343, definestwo types of partnership interests, asdetermined at time of issuance:Capital Interest: partnership interest that

would entitle the holder to a share ofliquidation proceeds if partnership assetswere sold at FMV.

Profits Interest: partnership interest that is nota capital interest; generally entitles holderonly to a share of post-issuance partnershipincome and gain.

1515

IRS will accept that the receipt of a profits interest inexchange for services is not a taxable event for thepartnership or the recipient, if:

The interest isn’t related to a substantiallycertain and predictable stream of income frompartnership assets.

The interest is not disposed of within two years.

The interest is not a limited partnership interestin a publicly traded partnership.

IRS treats § 83 as irrelevant for this purpose.

Receipt of Profits Interest

1616

Unvested Profits Interest

Rev Proc 2001-43, 2001-2 CB 191, says that RevProc 93-27 applies to a profits interest that issubject to a substantial risk of forfeiture ifpartnership and recipient treat the recipient as theowner of the partnership interest from the date ofgrant.

§ 83(b) election is not required, although is oftenrecommended by advisors as a protectivemeasure.

In effect, the two Rev Procs give precedence toSubchapter K principles over § 83.

1717

Unvested Profits Interest

If partnership grants an unvested profitsinterest, service provider will not be taxed onreceipt or vesting if:Conditions of Rev Proc 93-27 are met.

Partnership and service partner treat and reportservice partner as tax owner of the interest andservice partner includes its distributive share ofpartnership tax items for tax purposes.

Upon grant or vesting of interest, neitherpartnership nor any partner takes deductionsbased on the profits interest at grant or vesting.

1818

Safe Harbor vs. Substantive Law

Rev Proc 93-27 and Rev Proc 2001-43 aresafe harbors; follow them and the IRS won’tchallenge you.

They are not substantive rules of law, butdepart from them and you are thrown backto a confusing mass of authorities.

For example, § 83 seems irrelevant under thetwo Rev Procs, but how does § 83 apply outsideof them?

1919

2005 Proposals

Proposed regulations under several Code sections, andaccompanying proposed revenue procedure, Notice2005-43, issued in May 2005. REG-105346-03.

In the unlikely event they ever become effective, theywould obsolete current guidance, including Rev Proc93-27 and Rev Proc 2001-43.

However, the proposals would generally allowpartnerships to achieve the same favorable results asunder current guidance, if the right elections are made:

“Safe harbor” liquidation value election.

§ 83(b) election for unvested interests.

2020

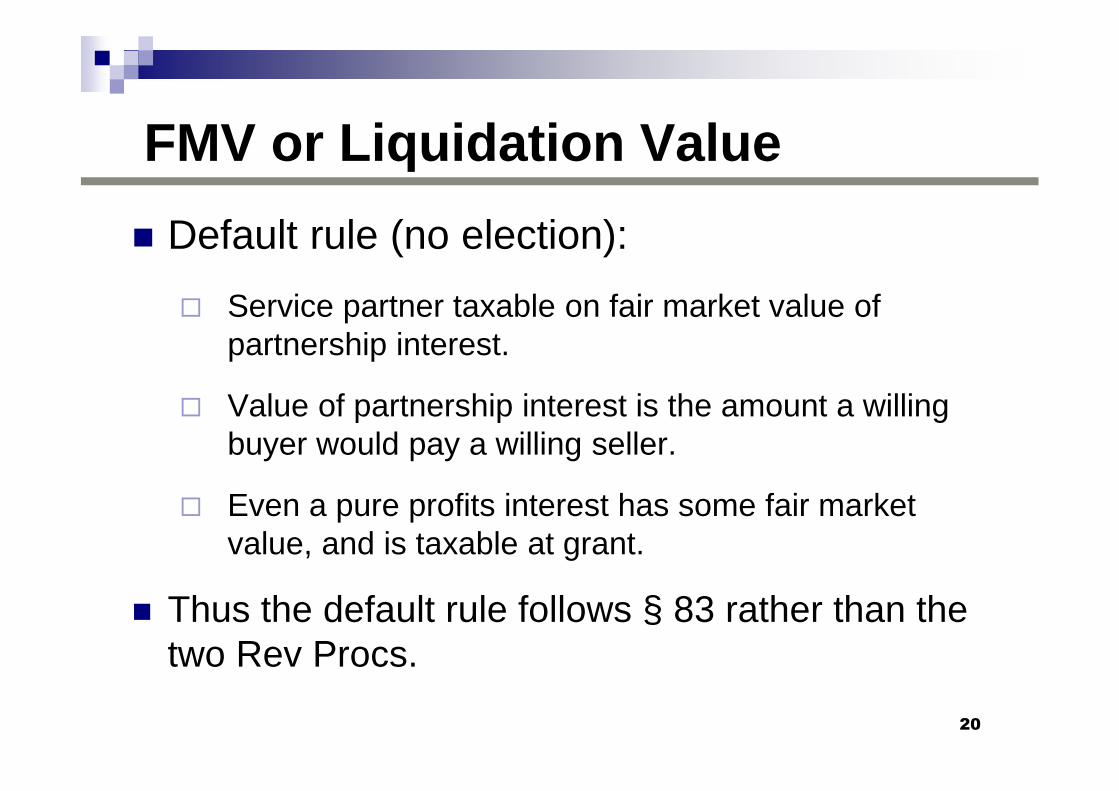

FMV or Liquidation Value

Default rule (no election):

Service partner taxable on fair market value ofpartnership interest.

Value of partnership interest is the amount a willingbuyer would pay a willing seller.

Even a pure profits interest has some fair marketvalue, and is taxable at grant.

Thus the default rule follows § 83 rather than thetwo Rev Procs.

2121

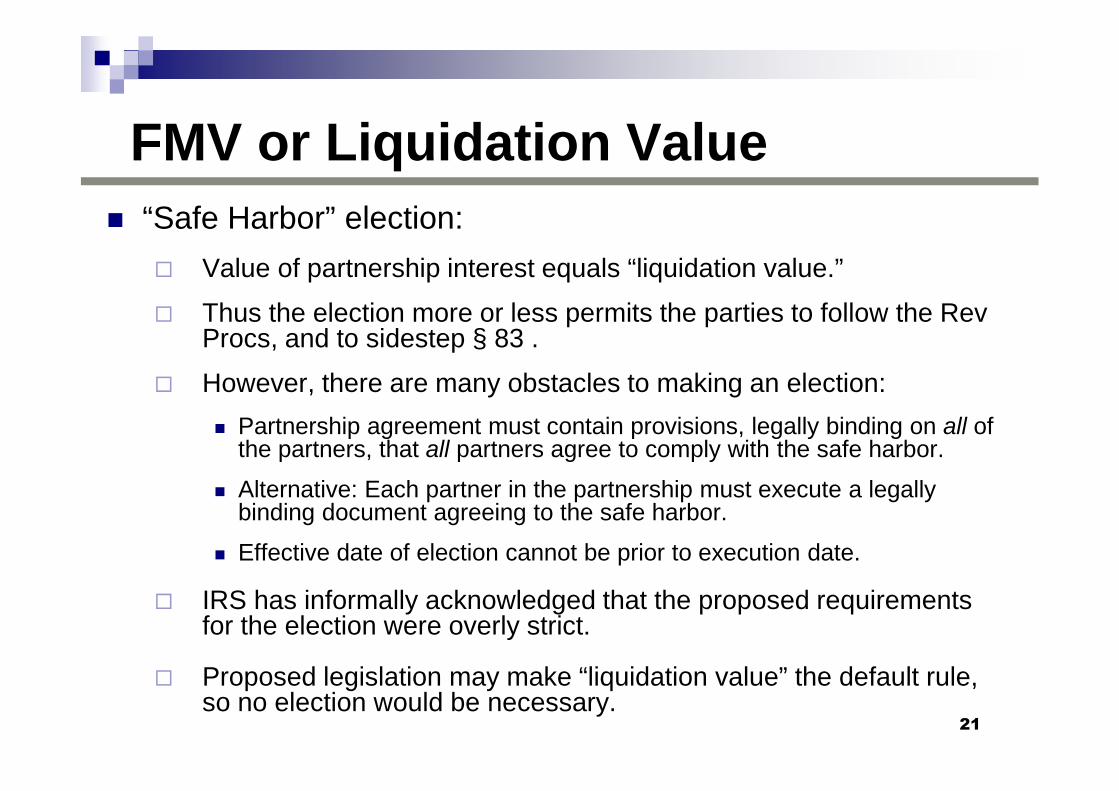

FMV or Liquidation Value

“Safe Harbor” election:

Value of partnership interest equals “liquidation value.”

Thus the election more or less permits the parties to follow the RevProcs, and to sidestep § 83 .

However, there are many obstacles to making an election:

Partnership agreement must contain provisions, legally binding on all ofthe partners, that all partners agree to comply with the safe harbor.

Alternative: Each partner in the partnership must execute a legallybinding document agreeing to the safe harbor.

Effective date of election cannot be prior to execution date.

IRS has informally acknowledged that the proposed requirementsfor the election were overly strict.

Proposed legislation may make “liquidation value” the default rule,so no election would be necessary.

2222

2005 Proposals: Unvested Interests

Under the proposals, an unvested compensatorypartnership interest in itself does not make theholder a partner for tax purposes.

Vesting of the interest makes the holder apartner.

The holder has compensation income.

Other partners have compensation deduction(subject to possible capitalization).

§ 83(b) election is treated like vesting; it makesthe holder a partner for tax purposes.

2323

2005 Proposals: Capital Shift

On issuance of a capital interest, some of the capital of theexisting partners shifts, in effect, to the new partner.

Similarly, on vesting of an unvested profits interest, capitaloften shifts from the existing partners to the new one.

If a service provider gets a capital interest without putting incapital, then the only place that the service provider’s capitalcan be coming from is the other partners.

Generally if property is transferred as compensation forservices, the transferor recognizes gain as if it sold the propertyto the service provider?

Issue: Do the existing partners recognize gain on a capital shift,as if they had sold an interest in the assets of the LLC to thenew partner?

2424

2005 Proposals: Capital Shift

The 2005 proposals take the pro-taxpayer (butsomewhat controversial) position that the existingpartners do not recognize gain. Prop Reg 1.721-1(b)(2)(i) and -1(b)(3).

Trap: Gain would be recognized by the LLCmember on the issuance or vesting to a newmember of an interest in a “disregarded” LLC thatbecomes a partnership for tax purposes as a resultof the issuance or vesting.

2525

Final Regulations?

Treasury reportedly is not working onfinalizing the 2005 proposals.

Treasury, very sensibly, is waiting tosee what Congress comes up with.

Proposed legislation is discussedbelow.

2626

Fee vs. LLC Equity

For one illustration of the stakes incharacterizing amounts as fees rather thanas the return on an LLC equity interest,see Rigas v. United States, 2011-1 USTC50,372 (S.D. Tex. 2011), aff’d, 2012-2USTC 50,530 (5th Cir. 2012)

Even in what appears to be a simplecontract for services, tax advice on dealstructure can sometimes make a bigdifference.

2727

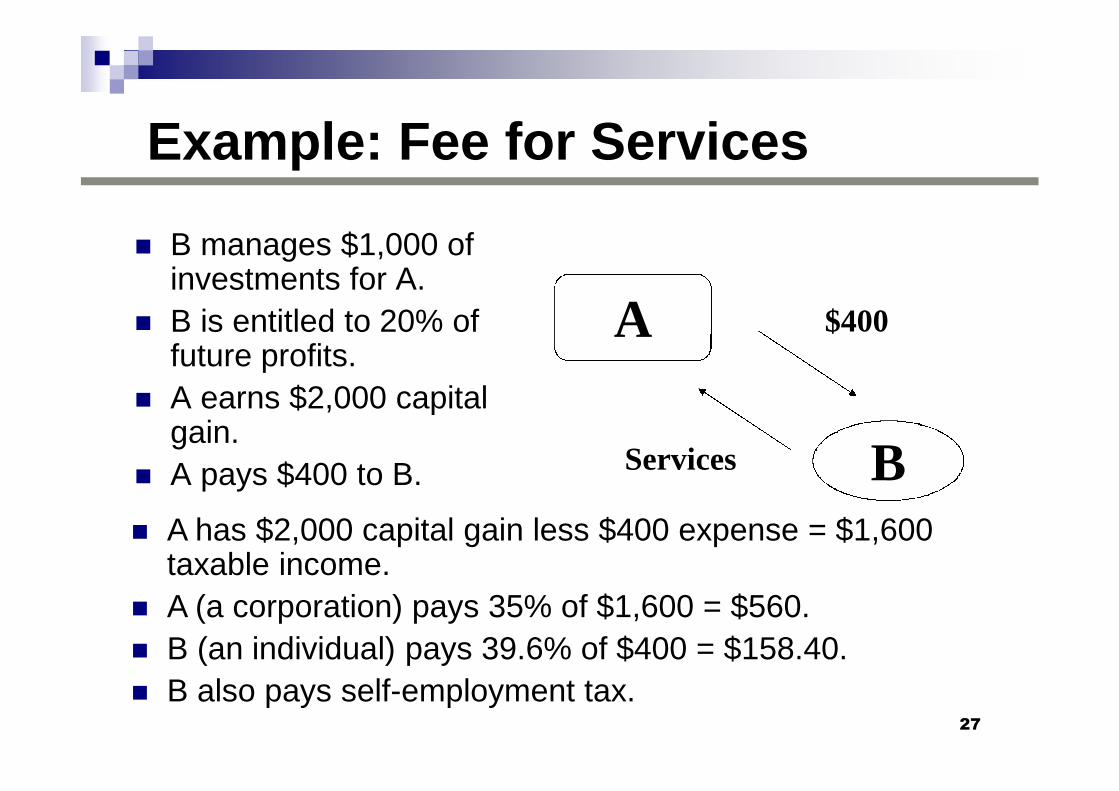

Example: Fee for Services

B manages $1,000 ofinvestments for A.

B is entitled to 20% offuture profits.

A earns $2,000 capitalgain.

A pays $400 to B. B

$400

Services

A has $2,000 capital gain less $400 expense = $1,600taxable income.

A (a corporation) pays 35% of $1,600 = $560.

B (an individual) pays 39.6% of $400 = $158.40.

B also pays self-employment tax.

A

2828

Example: Equity for Services Suppose instead A and B form X

LLC.

A contributes $1,000 for 80% offuture profits.

B contributes services for 20% offuture profits.

X earns $2,000 capital gain.

A pays 39.6% of $1,600 =$633.60.

B pays 20% of $400 = $80.

No self-employment tax.

However, net investment incometax likely applies.

B

$1,000 Services

X

A

2929

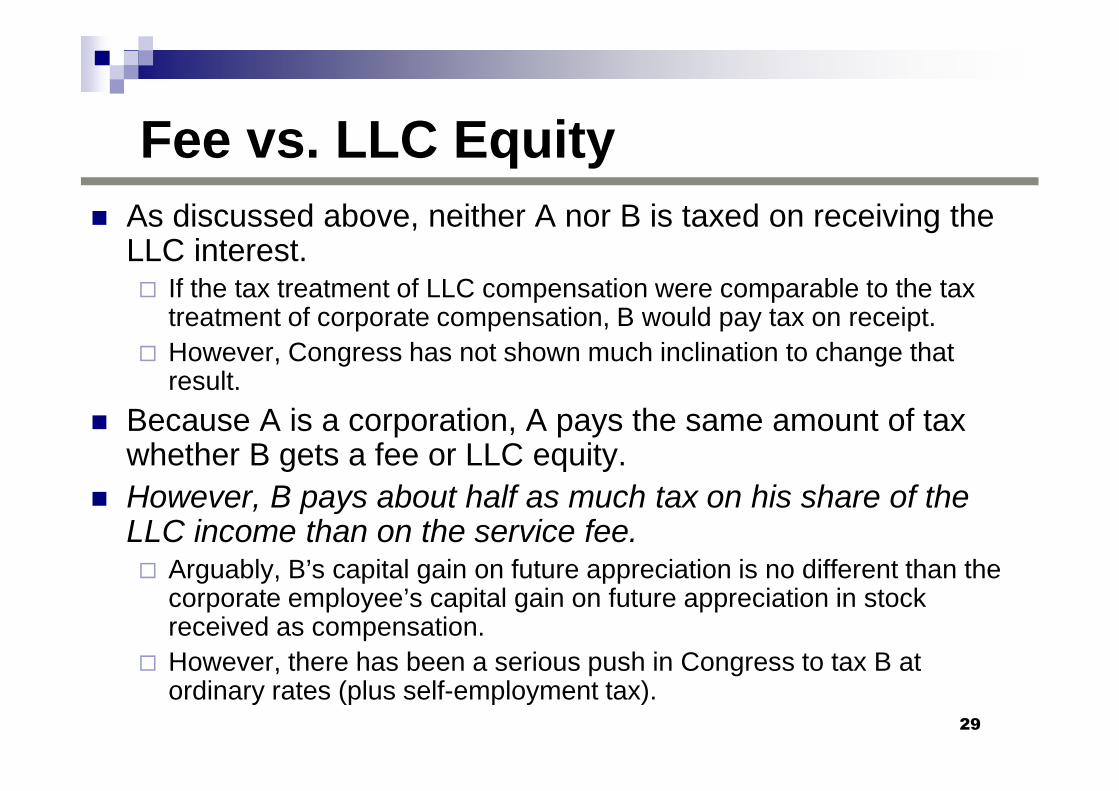

Fee vs. LLC Equity

As discussed above, neither A nor B is taxed on receiving theLLC interest. If the tax treatment of LLC compensation were comparable to the tax

treatment of corporate compensation, B would pay tax on receipt.

However, Congress has not shown much inclination to change thatresult.

Because A is a corporation, A pays the same amount of taxwhether B gets a fee or LLC equity.

However, B pays about half as much tax on his share of theLLC income than on the service fee. Arguably, B’s capital gain on future appreciation is no different than the

corporate employee’s capital gain on future appreciation in stockreceived as compensation.

However, there has been a serious push in Congress to tax B atordinary rates (plus self-employment tax).

3030

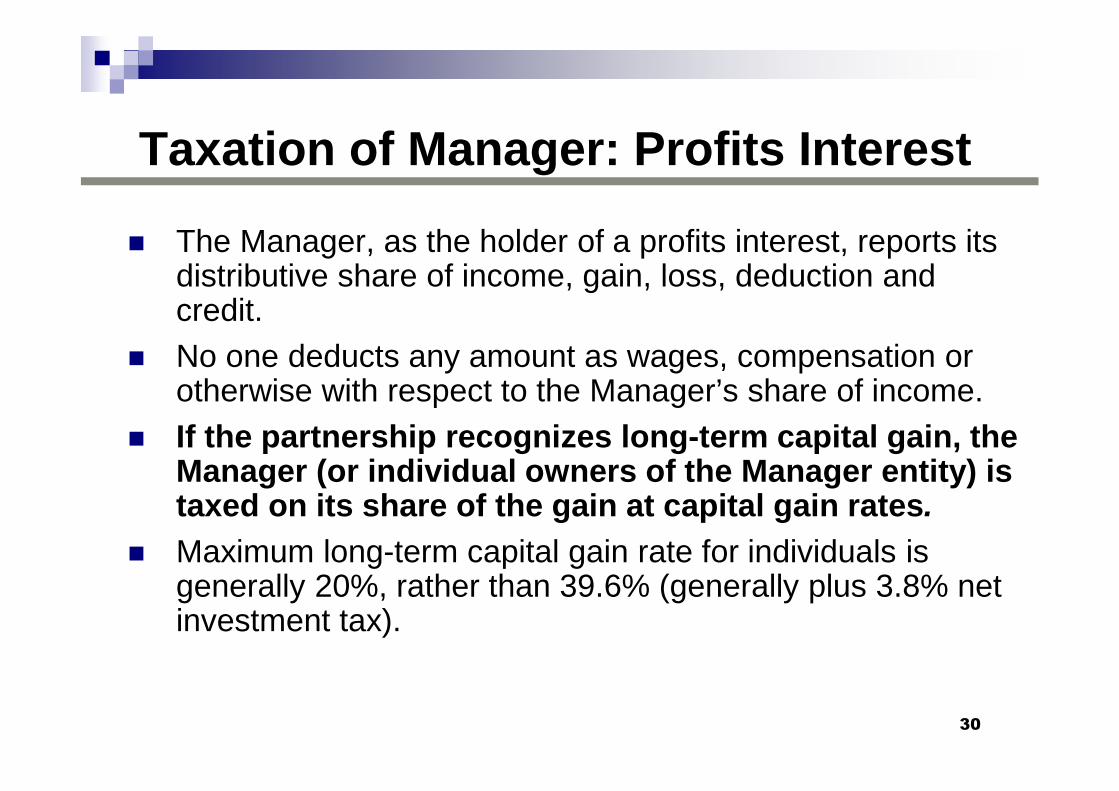

Taxation of Manager: Profits Interest

The Manager, as the holder of a profits interest, reports itsdistributive share of income, gain, loss, deduction andcredit.

No one deducts any amount as wages, compensation orotherwise with respect to the Manager’s share of income.

If the partnership recognizes long-term capital gain, theManager (or individual owners of the Manager entity) istaxed on its share of the gain at capital gain rates.

Maximum long-term capital gain rate for individuals isgenerally 20%, rather than 39.6% (generally plus 3.8% netinvestment tax).

3131

Taxation of Manager: Fee for Services

If a payment for services is determined without regard tothe net income of the LLC, it is a “guaranteed payment”as defined under Code § 707(c), which does not mean itis truly “guaranteed.” It is determined without regard to the partnership’s income.

It is made to the partner in its capacity as a partner.

It is ordinary income to the partner and generally deductible bythe partnership.

“Salary” to service providers of an operating business aregenerally “guaranteed payments” if made to a partner.

If the management fee is paid to an affiliate of the partner(rather than to the member) it is generally just a businessexpense of the partnership.

3232

Non-Partner Capacity Payments

Payments made to a partner who is not acting in hiscapacity as a partner are generally treated as if madebetween the partnership and a non-partner. Code § 707(a).

In many contexts, the difference between a 707(a) paymentand guaranteed payment is not of great importance.

But if allocations under a profits interest could berecharacterized as 707(a) payments, the tax consequenceswould be enormous. Such recharacterization is theoretically possible, especially if the

recipient of the profits interest does not bear “entrepreneurial risk.”

However, it generally would be hard position for the IRS to sustain.

The IRS has never issued regulations on point and does not appearto be pursuing that line of attack.

3333

Carried Interests: Proposed Legislation

Several bills have been introduced in Congress to add new“Section 710” to the Code.

There are differences among the bills but all would: Characterize allocations attributable to many carried interests as

ordinary income, subject to:

Ordinary income tax rates plus,

Self-employment tax.

Tend to apply to many entities besides private equity funds,although private equity funds are the main target.

Deny any compensation deduction to the other LLC members.

Continue to permit carried interests to be received free of initial tax,unlike compensatory corporate stock.

3434

Carried Interests: Proposed Legislation

All versions have some exception forinvested capital.

To the extent Managers receive a return ontheir own invested capital, § 710 does notapply.

However, the exception has been draftednarrowly.

Versions have been passed several times bythe House but not enacted.

3535

What Can Managers Do?

Techniques that might work under some versionsof § 710 are prohibited under others.

Be skeptical of reports suggesting that managersare rushing en masse to restructure their carriedinterests.

For example, it won’t help for the managers to:

Borrow from the cash investors to make abigger capital investment in the LLC.

Take convertible or contingent debt, options, orderivatives, with respect to the LLC.

3636

What Won’t Section 710 Affect?

The scope of § 710 – if enacted -- isimpossible to predict.

However, although the versions that havepassed the House are overbroad, Congress’target has been investment managers.

LLC members active in operatingbusinesses are the least likely to beaffected, even though they (like recipients ofcorporate stock) often earn capital gain byperforming services.

3737

Profits Interests vs. Options

Corporate options and carried interests both enableworkers to participate in future growth.

The strike price of the corporate option usually must beat least the fair market value of the stock on the date ofgrant. Thus the option holder does not have a share of the existing fair

market value, value, but can profit from future increases in value.

The profits interest by definition does not entitle themember to share in any of the liquidation value that theLLC has on the date of grant. Thus the option holder does not have a share of the existing

liquidation value, but can profit from future increases in value.

Compensatory options – in corporations or LLCs – donot result in capital gains for the holders when exercised.

Profits interests often generate capital gains for theholders.

3838

Profits Interests vs. Options

For partnerships, carried interests traditionally (anddeservedly) have been more popular than options.

Options are familiar in the corporate world, and aresometimes used by LLCs only because of thisfamiliarity.

LLC clients who want to issue options sometimeswill prefer profits interests once they understandhow profits interests work.

The 2005 proposals have little detail oncompensatory options, but do take the positionthat the existing partners recognize no gain onissuing a partnership interest on the exercise ofa compensatory option.

3939

LLC Options

If the LLC does grant options, then the following treatmentseems reasonable (assuming that the optionholder istreated only as an optionholder) : The optionholder continues to be treated as an employee.

The employee should not have any income on receipt of the option.

The employee has ordinary compensation income (presumablybased on “fair market value”) on exercising the option.

The partnership should have a deduction (or in some cases acapitalized cost) when the employee exercises the option.

The partnership should not recognize income on the granting orexercise of the option (but gain is likely recognized on the exerciseof a an option on an interest in a single-member LLC).

40

Fee Conversion

Goal: Convert management fees into additional carried interest whileretaining, to the maximum extent possible, the basic economicarrangement between the Manager and the investors. If the conversion issuccessful, it can convert ordinary income into capital gain.

Example: Suppose that a Manager’s 1% capital contribution would havebeen $1 million, and that her management fees would have been $2million. A portion of the management fee payable by the fund (let’s say $1million) is reduced. In lieu of an actual capital contribution to the fund, thegeneral partner is credited with a hypothetical capital contribution to thefund (“Hypothetical Contribution”).

Distributions: The Manager is entitled to receive the same amount ofdistributions with respect to its Hypothetical Contribution that otherinvestors receive with respect to an actual contribution in the amount of $1million. Assume the fund has an overall return of 30%. In exchange for waiving its right to

receive $1 million in management fees, the general partner would receive (i) $1million return of capital (return of its Hypothetical Contribution) + (ii) $300,000representing the return that any other investor of $1 million would receive.

The distributions typically come from the profit realized by the fund on the sale of itsportfolio companies. (Not contributions of other investors, or loan proceeds.)

40

41

Fee Conversion – Different Types

Depending on the particular arrangement, there may bemore or less risk that the fee the Manager attempted toconvert will still be treated as a management fee, ratherthan as a carried interest.

Many advisors believe a waived management fee maybe exchanged for a profits interest if: The conversion is done before the right to the payment of the

management fee accrues.

The right the Manager receives in exchange for the waivedmanagement fee is the right to future profits, if any.

There is a realistic risk that the future profits will not materialize,although commonly the Manager does have a priority claim withrespect to the amount of the waived fee.

41

42

Possible Tax Issues

Constructive Receipt. If Managers have already earned the fees and have a right to

them, it is a basic rule of taxation that they cannot turn theirback on the fees and avoid the income.

This risk is minimized if the Managers are required to waivethe fees before the period to which they relate. In most private equity funds, the management fees are paid

semiannually or quarterly in arrears. Some funds will require thewaiver prior to the quarter or semiannual period for which thefees accrue.

Because the Managers have no right to the payment of thefees prior to their performance of management services, theycannot be said to have constructively received the fees at thetime of that waiver.

42

4343

Code § 409A

409A (enacted 2004) caused an upheaval in thetreatment of corporate executive compensation.

Under 409A, amounts deferred under anonqualified deferred compensation plan arecurrently includible in gross income to the extentnot subject to a substantial risk of forfeiture, unlessstrict requirements are met.

Failure to meet the requirements subjects theservice provider to interest plus a 20% penalty.

409A is not intended to apply to transfers of“property” that are subject to Code § 83.

4444

Code § 409A Partnerships are not exempt from 409A.

Preamble to the final 409A regulations: “taxpayers may apply the principles applicable to stock

options or stock appreciation rights under these finalregulations, as effective and applicable, to equivalentrights with respect to partnership interests.” TD 9321, 72Fed Reg 19234 (April 11, 2007).

There is not much authority on applying 409A toLLC compensation, but in general the impact of409A on equity-based LLC compensation has beenvery muted compared to its pervasive influence oncorporations.

4545

LLC Compensation Exempt from 409A

Profits interests that qualify under Rev Proc 93-27 are exempt from 409A . Notice 2005-1, 2005-1 CB 274, 279 (Q&A 7) Yet another reason to prefer profits interests over

other forms of LLC compensation.

Since capital interests seem to clearly be“property” subject to Code § 83, they areprobably not subject to 409A.

“Guaranteed payments” (Code § 707(c)) aregenerally not subject to 409A, unless paymentby a cash-basis LLC is delayed more than 2 ½months after the end of the year.

4646

LLC Compensation Exempt from 409A

“Retirement payments” (described in Code § 736)are generally not subject to 409A.

Exception: 409A does apply to retirementpayments under Code § 1402(a)(10). Payments to an individual that continue at least until

death.Made after all capital has been returned. Individual provides no services to the LLC. The other partners have no obligations to the individual

except for these payments.

The advantage of 1402(a)(10) payments isexemption from self-employment tax.

4747

LLC Compensation Subject to 409A

Code § 707(a) payments are subject to 409A.

As noted above, these are payments made to a partner,other than in his capacity as a member of thepartnership.

They are generally treated as occurring between thepartnership and a non-partner.

Options are subject to 409A.

LLC options seem to treated under 409A much likecorporate options.

Most importantly, the option exercise price must not beless than the fair market value of the employer stock (orLLC interest) on the date of grant.

4848

LLC Compensation and 457A

Code § 457A (enacted 2008) is in some ways an expansion of 409A. It accelerates tax on deferred compensation paid by "nonqualified

entities,” even if the deferred compensation complies with 409A. The provision was directed at hedge fund managers who were deferring

compensation through foreign corporations; however, the provisionapplies much more broadly.

Nonqualified entities include: A foreign corporation (unless substantially all of its income is effectively

connected with the conduct of a U.S. trade or business or subject to a"comprehensive foreign income tax“).

A partnership (unless at least 80% of its income is allocated to persons otherthan foreign persons not subject to a comprehensive foreign income tax, andorganizations that are exempt from U.S. federal income tax).

Partnerships that have substantial foreign or tax-exempt ownershipshould consider 457A carefully.

See Notice 2009-8, 2009-4 IRB 347.

4949

Allocations and Distributions

An LLC distribution is an amount that the LLC member receives.

An LLC allocation is an amount of profits, losses, or other items thatare attributed to the member on the LLC's books.

Typically -- although there are many exceptions -- the distribution istax-free and the allocation is taxable. The allocation is taxable whether or not there is a corresponding

distribution.

It may seem exactly backwards that you can receive distributions tax-free but must pay tax on accounting entries. However, for holders ofLLC equity interests, that is the normal pattern.

Contributions, distributions, and allocations are interrelatedconcepts. Over the life of the LLC, contributions plus or minus allocations equal

distributions.

Any time you change one of these items – contributions, distributions,and allocations – you must consider how the others may be affected.

5050

Two LLC Drafting Approaches

Layer-cake allocation (the more traditionalapproach).

Specifies the allocation of income and loss.

Liquidating distributions are made so as to matchallocations. More precisely, the distributions are made in accordance with

the capital accounts, which in turn reflect the allocations thathave been made.

Considered the safer approach under the taxregulations.

However, may give the members less certainty aboutthe way liquidating distributions will be made.

5151

Two LLC Drafting Approaches Targeted (forced) allocation.

Specifies the distribution of proceeds on liquidationof the LLC.

Allocations are made so as to match liquidatingdistributions. More precisely, allocations are made so that capital accounts

(subject to some adjustment) equal the amounts that would bedistributed on a liquidation of the LLC at book value.

Validity of approach under tax regulations is less clear.

However, it is now widely used, and may give themembers more certainty about the way liquidatingdistributions will be made.

This approach requires special care when dealing withprofits interests.

5252

Example: Layered Allocations

Investors put in $1,000 and get 50 Class A Units.

Workers put in services and get 100 Class B Units.

50 Class B Units are issued on the first day of Year One,when the net value of all the LLC's assets is $1,000.

Class B Unitholders receive nothing unless operatingprofits and/or appreciation in value increase the value ofthe LLC to more than $1,000, but above that pointdistributions are pro rata by unit.

50 Class B Units are issued on the first day of Year Two,when the net value of all the LLC's assets has increasedto $3,000.

Nothing else of relevance occurs during the year (i.e., nocapital contributions, distributions, profits, or losses).

5353

Example: Layered Allocations

Allocation of Profit and Loss: Allocate profits to offset prior losses. Allocate all remaining profits pro rata by unit. Allocate losses in accordance with capital accounts.

Before the Year Two Class B Units areissued, the $2,000 of increased value istreated as profit for purposes of “booking up”(restating) capital accounts of all unit holders. Capital accounts for Class A Units and Year One

Class B Units are increased by $2,000/150 = $13.33per unit.

5454

Example: Layered Allocations

Liquidating Distributions: Distribute proceeds in accordance with capital accounts.

Does this work? Greatly oversimplified, but generally yes.

On immediate liquidation after the Year Two units arereceived: Class A Units first get back $1,000. $2,000 is distributed pro rata between Class A Units and Year One

Class B Units. Holders of Year Two Class B Units get nothing. Even if all Class B Units looked the same on the surface, they in fact

carried different rights; they were associated with different capitalaccounts.

All Class B Units are profits interests

However, some Class B Units carry greaterdistribution rights than others.

5555

Example: Targeted Allocations

Same basic facts.

Investors put in $1,000 and get 50 Class A Units.

Workers put in services and get 100 Class B Units.

50 Class B Units are issued on the first day of Year One,when the net value of all the LLC's assets is $1,000.

Class B Unitholders receive nothing unless operatingprofits and/or appreciation in value increase the value ofthe LLC to more than $1,000, but above that pointdistributions are pro rata by unit.

50 Class B Units are issued on the first day of Year Two,when the net value of all the LLC's assets has increasedto $3,000. So there are now 150 Class B Units.

Nothing else of relevance occurs during the year (i.e., nocapital contributions, distributions, profits, or losses).

5656

Example: Targeted Allocations

Allocation of Profit and Loss: Allocate as needed so that capital accounts are equal to the

required liquidating distributions.

$2,000 of increased value is treated as Profit for purposesof “booking up” (restating) capital accounts of all unitholders, so that capital accounts equal amounts that wouldbe distributed on liquidation. Capital accounts for Class A Units and Class B Units are increased

by $2,000/200 = $10.00 per unit.

On liquidation, Class A Units get back their capital, andthen all distributions are pro rata by unit.

Does this work?

No.

5757

Example: Targeted Allocations

On liquidation, Class A Units get back anyunrecovered capital, and then all distributions arepro rata by unit. Class A Units first get $1,000. Additional $2,000 is shared pro rata by all units

($10.00 per unit), including Class B Units issued inYear Two.

Class B Units issued in Year One are profitsinterests, generally not taxable to the workers onreceipt. On immediate liquidation after the units were received,

Class B Units would get none of the $1,000. On liquidation after a year, Class B Units do get $10.00

per unit.

5858

Example: Targeted Allocations

On these facts, Class B Units issued in Year Twoare capital interests, generally taxable to theworkers on receipt. On immediate liquidation after the units are received,

these Class B Units get $10.0 per unit. The right to receive proceeds on a liquidation is the

definition of a capital interest. Class B Units issued in Year Two are capital interests;

they would share in a liquidating distribution even ifthere are no future profits or growth.

All Class B Units had equal distribution rights, but theYear Two Class B Units were taxable capital interests.

5959

Example: Targeted Allocations

Class B Units issued in Year Two should have had lowerdistribution rights than Class B Units issued in Year One,the same as in the layered allocation example.

It is possible to use targeted allocations even whenworkers receive profits interests at different times, but becareful. For example, LLC could have granted only “Class C Units” in Year

Two, and provided that Class C Units only share in liquidatingdistributions over $3,000.

Regardless of the allocation method, or the labels thatare given to the units, profits interests granted atwidely different times normally will not have the exactsame rights to receive LLC distributions; and if theydo have the exact same distribution rights they likelyare not strictly profits interests.

60

“Catch-Up” Allocations Assume same facts of the previous example.

Investors put in $1,000 and get 50 Class A Units.

Workers put in services and get 100 Class B Units.

50 Class B Units are issued on the first day of Year One, when the netvalue of all the LLC's assets is $1,000.

Class B Unitholders receive nothing unless operating profits and/orappreciation in value increase the value of the LLC to more than$1,000, but above that point distributions are pro rata by unit.

Assume that the only Class B Units are the ones issued at the outset.

If the LLC liquidates and distributes the proceeds and theproceeds are $3,000, Class A Unit get all of the first $1,000,and then proceeds are distributed pro rata by unit.

Class A Units have a permanent advantage over Class BUnits.

60

61

“Catch-Up” Allocations

There is a way for the Class B Units to eventually catch-up to, and beon a par with Class A Units, if that is what the parties want.

Under the first example, Class B Units are entitled to 2/3 of amounts abovethe first $1,000.

However, the parties could instead give the Class B Units a right to allamounts above the first $1,000, until Class B Units are entitled to the sameamount per unit as Class A Units.

Under this approach, Class B Units are entitled to all of the $2,000increase in value that accrued while they held their units.

Class B Units then receive 2/3 of all amounts distributed on liquidation, andthey have the same right per unit as the Class A Units.

All units receive $20 per unit.

61

62

“Catch-Up” Allocations

Under the Catch-Up Allocation approach, Class BUnits still qualify as profits interests because theirright to anything above $1,000 is contingent onfuture profits.

If the LLC had liquidated on day one and the proceedswere only $1,000 – the amount the investor put in – theClass B Units would have been entitled to nothing.

Whether or not Class B Units should ever catch-upto Class A Units is a business decision – itdepends on the particular business deal.

62

63

Operating Incomevs. Capital Appreciation

A profits interest typically gives the Manager theright to a share of:

Future operating income.

Future appreciation or capital gain.

However, the parties often are more concernedabout giving the Manager an equity stake incapital gain than in operating income.

It is possible to give the Manager a larger share offuture capital gain than of future operating income.

Arguably it is possible to give the Manager a shareonly of future capital gain, with no share of operatingincome. 63

6464

Partners Cannot be Employees Before the Internal Revenue Code of 1954, courts ruled that

it was impossible for a person to serve the dual role ofemployer and employee in a single transaction.

Each partner is in some sense the employer of thepartnership’s employees, so if a partner were an employeethe partner would be both employer and employee – whichwas (at least at that time) thought to be an absurd result.

Under state law nowadays, it is possible for a partner orLLC member to be considered an employee, depending onthe facts.

However, tax law has not kept up, and technically the IRSconsiders it impossible for a partner to be an employee ofhis or her own partnership.

6565

Partners Cannot be Employees

The law seems reasonably well-settled that for taxpurposes partners are not considered employees oftheir own partnership. Rev Rul 69-184, 1969-1 CB 256. Instead, partners who work for their partnerships are considered

self-employed.

It is unclear if the IRS is actively enforcing this rule; manypractitioners are under the impression that the IRS is not.

IRS officials have informally expressed some interest inreconsidering this rule, but a change is very unlikely in the nearfuture.

The same rules apply to LLC members who are taxed aspartners.

Partners receive a Schedule K-1 each year and not a FormW-2.

6666

Guaranteed Payments

Fixed “salary” of partners is characterized as a“guaranteed payment” for services under § 707(c)rather than as wages.

As noted above, a guaranteed payment is made to apartner in his capacity as a partner, but is determinedwithout regard to the partnership’s income.

For key purposes, a guaranteed payment is nottreated as a distribution or allocation; it does notdirectly affect the recipient’s capital account.

6767

Guaranteed Payments

Includable in income of recipient partner(§ 61(a)) and deductible (§ 162(a)) bypartnership unless required to becapitalized under § 263.

Inclusion occurs in partner’s taxableyear in which or with which thepartnership’s tax year ends.

Deduction to partnership when paidor accrued.

6868

Withholding

Federal Insurance Contributions Act (“FICA”) andincome taxes are withheld from employees’ paychecks. Employee generally does not file quarterly estimated income tax.

FICA is not paid with annual Form 1040.

For FICA taxes, the employee pays a portion and the employerpays a portion.

There is no payroll tax withholding on partners. Partner typically files quarterly estimated income tax and annual

Form 1040.

Self-Employment Contributions Act (“SECA”) is also paidthrough quarterly tax and on annual Form 1040.

Partner pays 100% of SECA.

6969

SECA Compared to FICA

SECA and FICA are intended to be equal:

Both comprise:

Old-age, survivor and disability insurance (“OASDI”) or social securitycomponent, plus

Hospital insurance (“HI”) or Medicare component.

SECA rates:

OASDI rate of 12.4%, on the first $113,700 (in 2013), plus

HI rate of 2.9% on all amounts -- no ceiling.

Partners are allowed a deduction for ½ of the self-employment tax paid. §164(f).

SECA equals combined rate of employer's and employee's share ofFICA.

Beginning in 2013, additional 0.9% Medicare tax above a threshold($250,000 for married taxpayers filing jointly).

707070

Income Subject to SECA

Self-employment tax is payable on net earningsfrom self-employment. § 1402(a).

Generally includes all business income. Does not include:

Dividends.

Rental from real property.

Capital gain.

Interest on any bond, debenture, note, certificate, orother evidence of indebtedness, issued with interestcoupons or in registered form.

§ 1402(a)(10) payments to retired partners.

7171

SECA and Profits Interests

Capital gain is not subject to SECA.

However, if capital gain isrecharacterized as ordinary incomeunder § 710 (the legislative proposalon carried interests discussed above)the recharacterized income would besubject to SECA.

7272

Comparing SECA and FICA

Since partner pays 100% of SECA, butemployee pays only part of FICA, a partner in aservice partnership will pay more on a givenamount of net earnings from self-employmentthan an employee will pay on the same amountof wages.

Should a partner be paid more than acomparable employee, to take SECA intoaccount?

737373

SECA and “Limited Partners”

“Limited Partners” are subject to SECA only on“guaranteed payments” for services. Code § 1402(a)(13).

Are LLC members “general partners” or “limited partners”? Proposed regulations from 1997 would have provided

guidance on when LLC members (and also partners inpartnerships) would be treated as limited partners forpurposes of self-employment tax. Prop Reg § 1.1402(a)-2.

The proposed regulations became a political hot potato;they won’t be finalized without direction from Congress.

However, the IRS says it is planning to issue regulationson the treatment of LLC members as “limited partners” forpurposes of the “passive activity loss” rules of Code § 469.

7474

LLC Members as “Limited Partners”

Under the 1997 Proposed Regulations, a partner is nottreated as a limited partner if the partner:

Has personal liability for the debts of or claims againstthe partnership by reason of being a partner;

Has authority to contract on behalf of the partnershipunder the statute or law pursuant to which the partnershipis organized; or

Participates in the partnership's trade or business formore than 500 hours during the taxable year.

However, for service partnerships (in health, law,engineering, architecture, accounting, actuarial science, orconsulting), any individual who provides services as part ofthe partnership’s trade or business will not be considered alimited partner.

757575

LLC Members as “Limited Partners”

In the absence of final regulations, LLCs takedifferent positions. The most conservative LLCs assume LLC

members are never limited partners. Reasonably conservative LLCs follow the 1997

proposed regulations. More aggressive LLCs exclude amounts above

reasonable compensation from self-employment tax.

The most aggressive LLCs assume all LLCmembers are limited partners.

767676

LLCs vs. S Corps

S Corp shareholder/employees are subject to FICA andnot SECA.

A portion of earnings that would be subject to self-employment taxes if earned by a sole proprietor orpartner may in some cases escape employment tax ifgenerated by an S Corp.

Dividends from S Corps are not subject to employmenttax, even if paid to a shareholder/employee.

However, the IRS has been actively challenging closely-held S Corps for failure to pay reasonablecompensation.

777777

LLCs vs. S Corps

Congress has considered proposals to subject many SCorp shareholders to the same treatment as generalpartners.

If you are choosing an S Corp over an LLC taxed as apartnership in order to save employment taxes, considerthat: Saving may be illusory even under current law.

Congress may amend the rules to ensure that many S Corpshareholders/employees pay the same amounts as generalpartners.

Unlike LLCs, S Corps generally cannot be liquidated tax-free (orconverted into partnerships); you likely will be stuck as an S Corpindefinitely, even if Congress changes the rules.

Many other disadvantages of S Corps over LLCs.

Reduced compensation may limit the opportunity for qualifiedretirement plan contributions.

787878

Tax on “Net Investment Income”

A special additional tax on “net investmentincome” (i.e., investment) income of higher-income individuals went into effect in 2013. Code§ 1411; see TD 9644 (Dec. 2, 2013) (adoptingfinal regulations)

The tax is 3.8% of “modified adjusted grossincome” above a threshold ($250,000 for jointreturns).

This net investment income tax is sometimesreferred to as a Medicare tax.

797979

Tax on “Net Investment Income”

Net investment income includes active businessincome of a partnership if the partner does notactively participate in the business.

Incorporates concepts from “passive activity loss” rules.

Same rule for S corporation shareholders.

However, it has been argued that S corporationshareholders who actively participate in theirbusinesses may have a greater opportunity thanpartners to avoid both FICA/SECA and the newtax on net investment income.

808080

Increased Medicare Tax on “Earned Income”

Additional 0.9% Medicare (hospital insurance or HI) taxapplies to wages in excess of: $250,000 (joint return or surviving spouse).

$125,000 (married filing separate).

$200,000 (other cases).

Also applies to self-employment income in excess ofthese amounts.

Previously, there had been no progressivity in the ratesof employment and self-employment tax.

Although the 0.9% increase was enacted in 2010, theeffective date was delayed until 2013.

8181

Employee Benefits

Some favorable benefit rules do not cover partners.

For example, a partner may not exclude fromincome: Premiums paid by the partnership for accident and

health insurance. § 105.

However, a partner is entitled to deduct 100% of thepremium the partner pays. § 162(l).

Group-term life insurance. § 79; Reg § 1.79-1(b)(2).

Value of meals and lodging furnished for theconvenience of the employer. § 119.

Qualified transportation fringes or qualified movingexpense reimbursement. Reg § 1.132-1(b).

8282

Deduction of Business Expenses

One potentially significant benefit ofpartnership treatment is that a partner isentitled to deduct business expenses. § 162.

An employee may only deduct businessexpenses to the extent they -- along withother “miscellaneous itemized deductions” --exceed 2% of adjusted gross income. § 67(and alternative minimum tax is a problemalso).

8383

Phantom Income Employees are generally not taxed on amounts

they don’t receive. However,

Some non-cash compensation may be taxable.

Sometimes deferred compensation may be taxablebefore it is received.

Partners holding profits interests are taxed on theirdistributive share of partnership income, whetheror not received.

The risk of “phantom income” (taxable incomewithout a corresponding payment to thepartner) can be reduced but never entirelyeliminated.

8484

State Tax

An employee is only taxable where the employee livesand/or works.

A partner may be taxable in every state in which thepartnership does business.

Tax credits in the partner’s home state can greatly reducethe financial burden, but do not necessarily eliminate it.

If the home state has no income tax, the tax the partnerpays to other states is a pure cost (no offsetting benefit athome).

“Composite returns,” filed by the partnership on behalf ofnon-resident partners, can greatly reduce the complianceburden, but sometimes increase the amount tax payable.

8585

Converting Partners to Employees

Many individuals prefer the simplicity of wage withholding.

This preference is especially pronounced outsideprofessions -- like law and accounting -- that traditionallyoperated in partnership form.

At the same time, it is often important for those individualsto have an equity stake in the business. “Phantom” equity plans may be an alternative that enable the

individuals to retain employee status.

Phantom equity will not generate capital gains for the individuals.

Will it incentivize as well as true equity?

As the partnership and LLC form of doing business keepsexpanding, this dilemma becomes more acute

Is there any solution?

8686

Converting Partners to Employees

Partners “A” and “B” contribute LLC interests to LLC Holdco.

Since A and B are no longer partners in LLC, they likely can be employees ofLLC.

LLC

Other OwnersLLC

Holdco

A B

8787

Phantom Equity

LLCs sometimes try to avoid reclassifying employees aspartners by giving them only “phantom equity.” Designed to replicate or resemble the economic benefits of a

partner’s equity interest, but without partner status for tax purposes.

“Virtual options” or “equity appreciation rights” are a kind ofphantom equity, intended to give the employee a share ofthe LLC’s appreciation in value, without turning theemployee into a partner for tax purposes.

Phantom equity likely needs to comply with the 409A rules

applicable to corporations.

8888

Phantom Equity

There is good authority that the holder ofcorporate stock appreciation rights (“SARs”) isnot a stockholder for tax purposes. See, forexample, Rev Rul 80-300, 1980-2 CB 165.

There is no comparable express authority thatthe holder of LLC equity appreciation rights isnot a partner for tax purposes.

However, LLCs generally take the position that thecorporate precedents apply.

8989

Phantom Equity

There are not even proposed regs on phantominterests in partnerships.

However, the following treatment seems reasonable: Assuming the phantom interest is not treated as an actual

interest for tax purposes, the employee is not be treated asa partner.

The employee should not have any income on receipt ofthe interest.

The employee has ordinary compensation income equal tothe payments from the partnership.

The partnership should have a deduction (or at worst acapitalized cost) when it pays the employee.

The partnership should not recognize income on grantingthe interest.

9090

Single-Member LLCs

In most cases a single-member LLC isclassified as a disregarded entity (treatedmore or less like a branch or division of itsowner) for federal income tax purposes.

Effective January 1, 2009, disregardedLLCs are treated as corporations for federalemployment tax purposes.

Reg § 301.7701-2(c)(2)(iv), as amendedby TD 9356, 2007-39 IRB 675.

9191

Single-Member LLCs

If the single-member LLC has employees, itmust report and pay federal employmenttaxes under its own name and have its owntaxpayer identification number.This rule covers FICA, FUTA, and income tax

withholding on wages.

This rule does not cover self-employment taxwhen a single-member LLC is owned by anindividual. An individual employed by his own single-member LLC

must pay his own self-employment tax.

9292

Single-Member LLCs

Previously, Notice 99-6, 1999-1 CB 321, gavetaxpayers two reporting choices:

Single-member LLC is employer, or

Owner of single-member LLC is employer.

Excise tax is also now reported separately bysingle-member LLC.

Income tax treatment of single-member LLCsis not affected by employment tax and excisetax rules.

![TAXING PARTNERSHIP PROFITS INTERESTS: THE CARRIED INTEREST …harvardlawreview.org/.../vol124_carried_interest_problem.pdf · 2016-10-05 · 2011] THE CARRIED INTEREST PROBLEM 1775](https://static.fdocuments.in/doc/165x107/5e90160ff1f02b7dff77e39c/taxing-partnership-profits-interests-the-carried-interest-2016-10-05-2011-the.jpg)