Structuring Private Placement Memorandum for the Private...

72

Presenting a live 90-minute webinar with interactive Q&A Structuring Private Placement Memorandum for the Private Sale and Solicitation of Securities Determining Materiality, Assessing Risk Factors and Conducting Due Diligence 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific WEDNESDAY, APRIL 20, 2016 The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Yelena M. Barychev, Partner, Blank Rome, Philadelphia Stuart Bressman, Partner, Proskauer Rose, New York Eric C. Perkins, Esq., Perkins Law, Glen Allen, Va.

Transcript of Structuring Private Placement Memorandum for the Private...

Presenting a live 90-minute webinar with interactive Q&A

Structuring Private Placement Memorandumfor the Private Sale and Solicitation of SecuritiesDetermining Materiality, Assessing Risk Factors and Conducting Due Diligence

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, APRIL 20, 2016

The audio portion of the conference may be accessed via the telephone or by using your computer'sspeakers. Please refer to the instructions emailed to registrants for additional information. If youhave any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Yelena M. Barychev, Partner, Blank Rome, Philadelphia

Stuart Bressman, Partner, Proskauer Rose, New York

Eric C. Perkins, Esq., Perkins Law, Glen Allen, Va.

Tips for Optimal Quality

Sound QualityIf you are listening via your computer speakers, please note that the qualityof your sound will vary depending on the speed and quality of your internetconnection.

If the sound quality is not satisfactory, you may listen via the phone: dial1-888-450-9970 and enter your PIN when prompted. Otherwise, pleasesend us a chat or e-mail [email protected] immediately so we canaddress the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen,press the F11 key again.

FOR LIVE EVENT ONLY

Sound QualityIf you are listening via your computer speakers, please note that the qualityof your sound will vary depending on the speed and quality of your internetconnection.

If the sound quality is not satisfactory, you may listen via the phone: dial1-888-450-9970 and enter your PIN when prompted. Otherwise, pleasesend us a chat or e-mail [email protected] immediately so we canaddress the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen,press the F11 key again.

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm yourparticipation in this webinar by completing and submitting the AttendanceAffirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you emailthat you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926ext. 35.

FOR LIVE EVENT ONLY

In order for us to process your continuing education credit, you must confirm yourparticipation in this webinar by completing and submitting the AttendanceAffirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you emailthat you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926ext. 35.

Program Materials

If you have not printed the conference materials for this program, pleasecomplete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see aPDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, pleasecomplete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see aPDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Structuring Private PlacementMemoranda for the Private Saleand Solicitation of Securities

Presenter:

Stuart Bressman, Partner

April 20, 2016

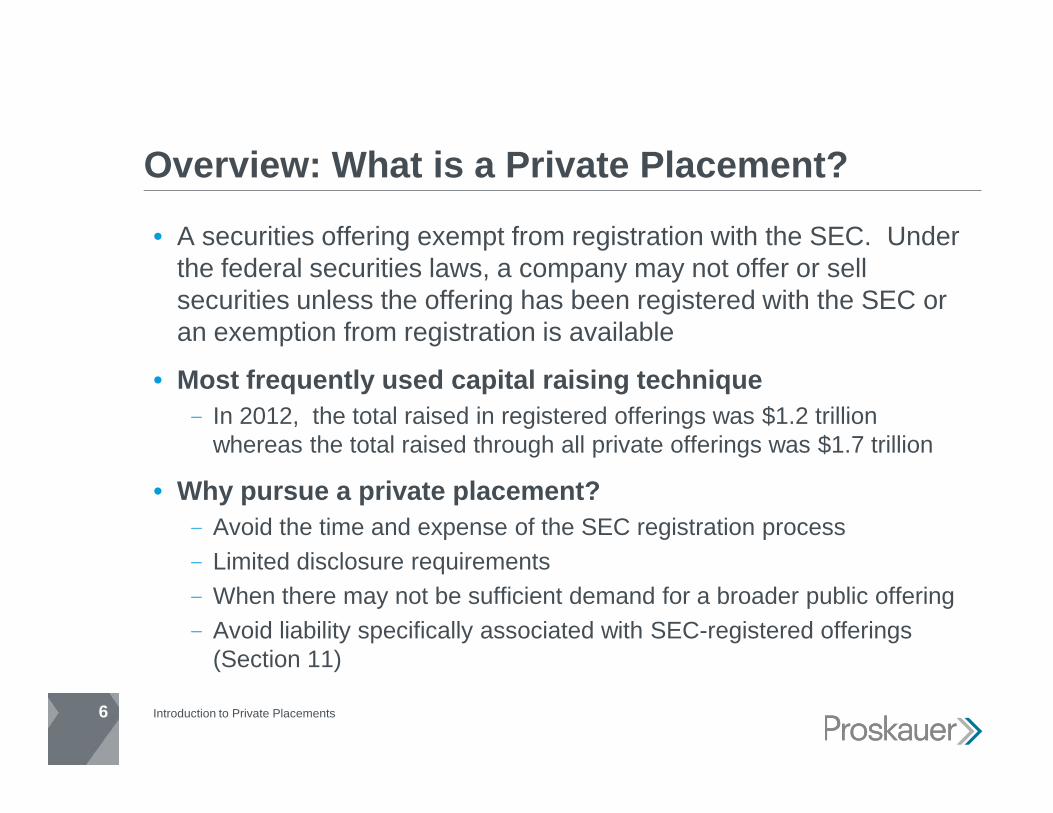

Overview: What is a Private Placement?

• A securities offering exempt from registration with the SEC. Underthe federal securities laws, a company may not offer or sellsecurities unless the offering has been registered with the SEC oran exemption from registration is available

• Most frequently used capital raising technique In 2012, the total raised in registered offerings was $1.2 trillion

whereas the total raised through all private offerings was $1.7 trillion

• Why pursue a private placement? Avoid the time and expense of the SEC registration process Limited disclosure requirements When there may not be sufficient demand for a broader public offering Avoid liability specifically associated with SEC-registered offerings

(Section 11)

6

• A securities offering exempt from registration with the SEC. Underthe federal securities laws, a company may not offer or sellsecurities unless the offering has been registered with the SEC oran exemption from registration is available

• Most frequently used capital raising technique In 2012, the total raised in registered offerings was $1.2 trillion

whereas the total raised through all private offerings was $1.7 trillion

• Why pursue a private placement? Avoid the time and expense of the SEC registration process Limited disclosure requirements When there may not be sufficient demand for a broader public offering Avoid liability specifically associated with SEC-registered offerings

(Section 11)

Introduction to Private Placements

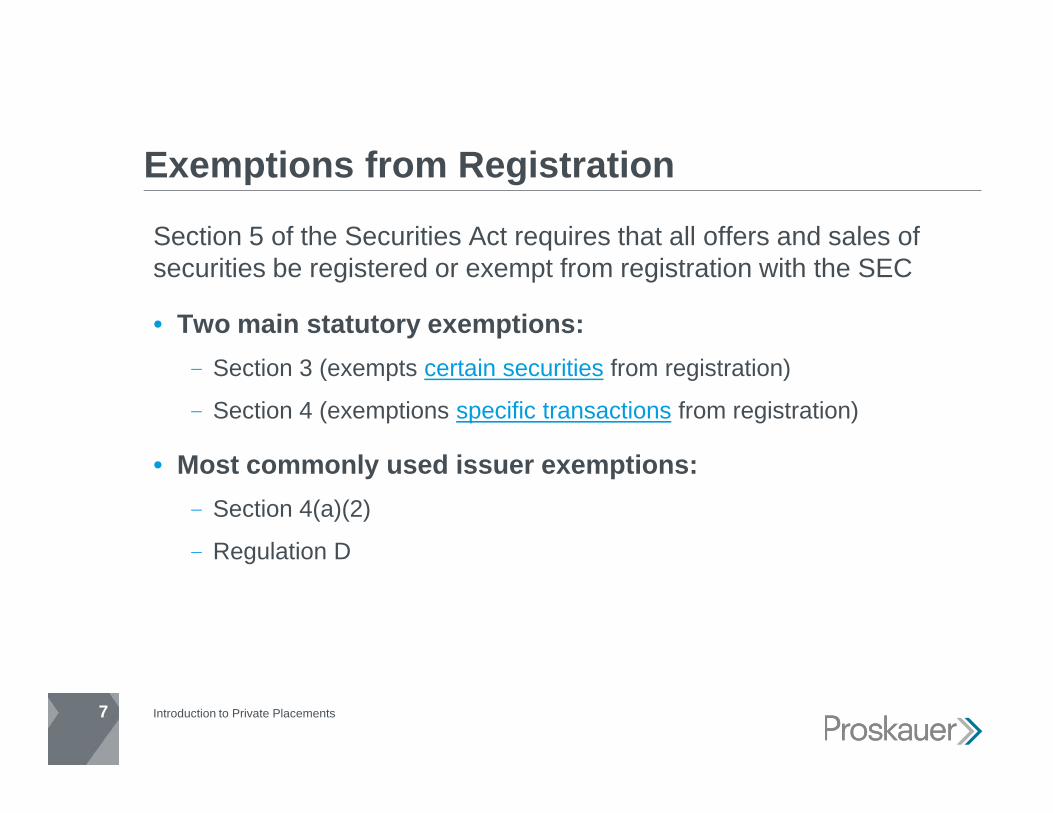

Exemptions from Registration

Section 5 of the Securities Act requires that all offers and sales ofsecurities be registered or exempt from registration with the SEC

• Two main statutory exemptions: Section 3 (exempts certain securities from registration)

Section 4 (exemptions specific transactions from registration)

• Most commonly used issuer exemptions: Section 4(a)(2)

Regulation D

Introduction to Private Placements7

Section 5 of the Securities Act requires that all offers and sales ofsecurities be registered or exempt from registration with the SEC

• Two main statutory exemptions: Section 3 (exempts certain securities from registration)

Section 4 (exemptions specific transactions from registration)

• Most commonly used issuer exemptions: Section 4(a)(2)

Regulation D

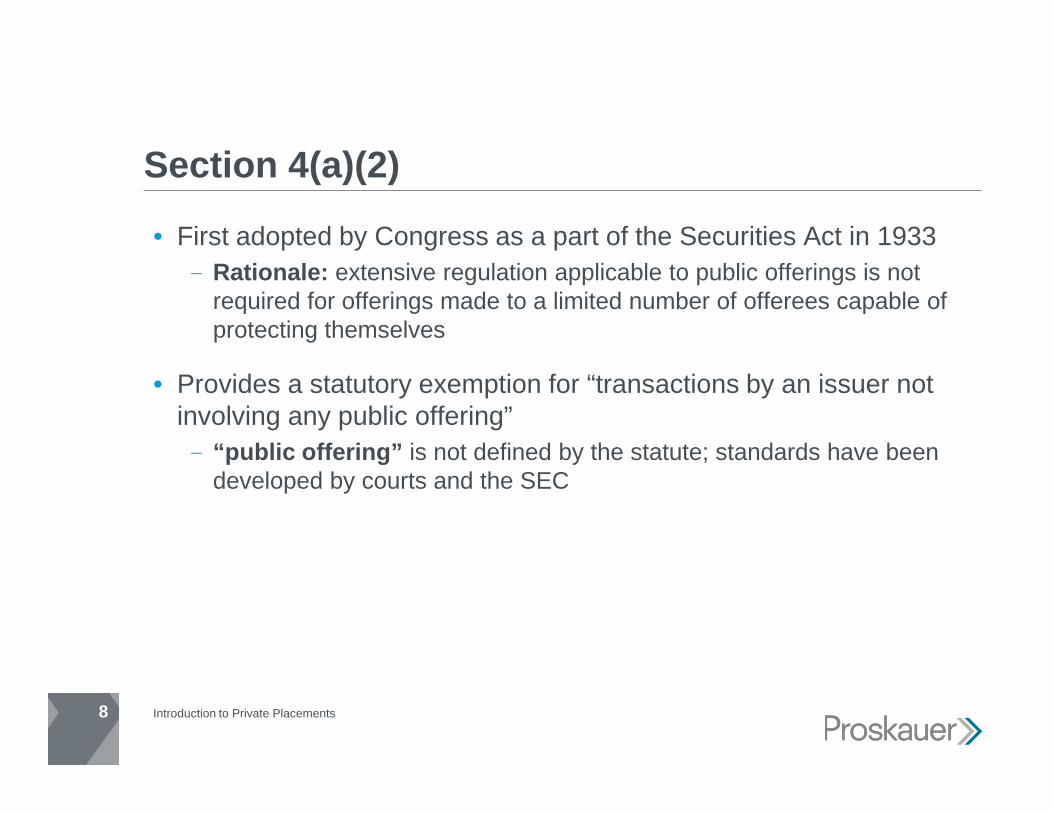

Section 4(a)(2)

• First adopted by Congress as a part of the Securities Act in 1933 Rationale: extensive regulation applicable to public offerings is not

required for offerings made to a limited number of offerees capable ofprotecting themselves

• Provides a statutory exemption for “transactions by an issuer notinvolving any public offering” “public offering” is not defined by the statute; standards have been

developed by courts and the SEC

Introduction to Private Placements8

• First adopted by Congress as a part of the Securities Act in 1933 Rationale: extensive regulation applicable to public offerings is not

required for offerings made to a limited number of offerees capable ofprotecting themselves

• Provides a statutory exemption for “transactions by an issuer notinvolving any public offering” “public offering” is not defined by the statute; standards have been

developed by courts and the SEC

What constitutes a “public offering”?

• SEC v. Ralston Purina (1953) The Supreme Court established the general principle that the

exemption is available only for an offer and sale made privately topersons able to fend for themselves.

Whether a purchaser can fend for itself is based, in part, on factorssuch as

1) the purchaser’s access to the same kind of information that would beincluded in a registration statement; and

2) the purchaser’s sophistication and ability to bear the economic risks of theinvestment.

Introduction to Private Placements9

• SEC v. Ralston Purina (1953) The Supreme Court established the general principle that the

exemption is available only for an offer and sale made privately topersons able to fend for themselves.

Whether a purchaser can fend for itself is based, in part, on factorssuch as

1) the purchaser’s access to the same kind of information that would beincluded in a registration statement; and

2) the purchaser’s sophistication and ability to bear the economic risks of theinvestment.

Since Ralston Purina…

• Other factors used in determining availability of the exemption: Number of offerees and their relationship to each other and to the

issuer Number of securities offered Size of the offering Manner of the offering Sophistication and experience of the offerees The nature and kind of information provided to the offerees or to which

the offerees have ready access Actions taken by the issuer to prevent the resale of securities

• Each factor is flexible and highly fact-dependent. No single factoralone is determinative.

Introduction to Private Placements10

• Other factors used in determining availability of the exemption: Number of offerees and their relationship to each other and to the

issuer Number of securities offered Size of the offering Manner of the offering Sophistication and experience of the offerees The nature and kind of information provided to the offerees or to which

the offerees have ready access Actions taken by the issuer to prevent the resale of securities

• Each factor is flexible and highly fact-dependent. No single factoralone is determinative.

Availability of the Exemption

• The person claiming a section 4(a)(2) exemption has the burden ofestablishing that the exemption is available for that particulartransaction.

• If securities were sold without a valid exemption from registration,section 12(a)(1) of the Securities Act gives the purchaser the rightto rescind the transaction for a period of one year after the sale.

• The right to rescind may be exercised against anyone that “sold”the security, including the issuer and the broker-dealer that actedas the financial intermediary or placement agent in connection withthe offering.

Introduction to Private Placements11

• The person claiming a section 4(a)(2) exemption has the burden ofestablishing that the exemption is available for that particulartransaction.

• If securities were sold without a valid exemption from registration,section 12(a)(1) of the Securities Act gives the purchaser the rightto rescind the transaction for a period of one year after the sale.

• The right to rescind may be exercised against anyone that “sold”the security, including the issuer and the broker-dealer that actedas the financial intermediary or placement agent in connection withthe offering.

Regulation D

• In 1982, the SEC adopted Regulation D, which provided greatercertainty regarding which transactions are exempt from registration.

• A series of eight rules, Rules 501-508, establishing threetransactional exemptions from the registration requirements of theSecurities Act of 1933. Rule 501 sets forth definitions Rule 502 sets out four general conditions to be met under the Regulation Rule 503 sets out the requirement to file a Form D Rules 504-506 establish the exemptions, each with particular qualifications and

limitations Rule 507 disqualifies an issuer from relying on Regulation D in certain situations Rule 508 provides that an insignificant failure to comply (when considered in

connection with the offering as a whole) with the terms or conditions of Rule504, 505, or 506 will not disqualify an offering from the exemption.

Introduction to Private Placements12

• In 1982, the SEC adopted Regulation D, which provided greatercertainty regarding which transactions are exempt from registration.

• A series of eight rules, Rules 501-508, establishing threetransactional exemptions from the registration requirements of theSecurities Act of 1933. Rule 501 sets forth definitions Rule 502 sets out four general conditions to be met under the Regulation Rule 503 sets out the requirement to file a Form D Rules 504-506 establish the exemptions, each with particular qualifications and

limitations Rule 507 disqualifies an issuer from relying on Regulation D in certain situations Rule 508 provides that an insignificant failure to comply (when considered in

connection with the offering as a whole) with the terms or conditions of Rule504, 505, or 506 will not disqualify an offering from the exemption.

Rule 502 – General Conditions for use of Reg D

• Integration Regulation D cannot be used as part of a scheme or plan to avoid

section 5 registration requirements. Several private placements offered within a short period of time, each

relying on separate offering exemptions, may be integrated, and whentaken together, may constitute a single plan of financing for which theprivate placement exemption is not available.

• Information Requirements If an issuer is selling securities to non-accredited investors pursuant to

Rule 505 or 506, or raising in excess of $1 million, the issuer mustcomply with the information requirements set forth in Rule 502.83 Thespecified information in Rule 502 must be furnished a reasonable timeprior to sale.

Introduction to Private Placements13

• Integration Regulation D cannot be used as part of a scheme or plan to avoid

section 5 registration requirements. Several private placements offered within a short period of time, each

relying on separate offering exemptions, may be integrated, and whentaken together, may constitute a single plan of financing for which theprivate placement exemption is not available.

• Information Requirements If an issuer is selling securities to non-accredited investors pursuant to

Rule 505 or 506, or raising in excess of $1 million, the issuer mustcomply with the information requirements set forth in Rule 502.83 Thespecified information in Rule 502 must be furnished a reasonable timeprior to sale.

Rule 502 – General Conditions for use of Reg D

• Manner of Offering Until the recent changes pursuant to the JOBS Act as discussed below,

this section prohibited the issuer or any person acting on its behalf tooffer or sell securities by any form of general solicitation or generaladvertising, including, but not limited to: (1) any advertisement, article,or other published or broadcast communication; or (2) any seminar ormeeting whose attendees have been invited by general solicitation oradvertising

• Limitations on Resale Regulation D is available only to issuers and applies only to a particular

transaction. Rule 502(d) provides that securities acquired in aRegulation D private placement are “restricted securities” and cannotbe resold by the purchaser without registration under the Securities Actor compliance with an available exemption from registration.

Introduction to Private Placements14

• Manner of Offering Until the recent changes pursuant to the JOBS Act as discussed below,

this section prohibited the issuer or any person acting on its behalf tooffer or sell securities by any form of general solicitation or generaladvertising, including, but not limited to: (1) any advertisement, article,or other published or broadcast communication; or (2) any seminar ormeeting whose attendees have been invited by general solicitation oradvertising

• Limitations on Resale Regulation D is available only to issuers and applies only to a particular

transaction. Rule 502(d) provides that securities acquired in aRegulation D private placement are “restricted securities” and cannotbe resold by the purchaser without registration under the Securities Actor compliance with an available exemption from registration.

Rule 504

• Applies to transactions in which no more than $1,000,000 ofsecurities are sold in any consecutive twelve-month period. Imposes no ceiling on the number of investors, permits the payment of

commissions, and imposes no restrictions on the manner of offering orresale of securities.

Securities may be sold to any type of investor.

Does not prescribe specific disclosure requirements.

Introduction to Private Placements15

• Applies to transactions in which no more than $1,000,000 ofsecurities are sold in any consecutive twelve-month period. Imposes no ceiling on the number of investors, permits the payment of

commissions, and imposes no restrictions on the manner of offering orresale of securities.

Securities may be sold to any type of investor.

Does not prescribe specific disclosure requirements.

Rule 505

• Applies to transactions in which not more than $5,000,000 ofsecurities is sold in any consecutive twelve-month period. Sales to thirty-five “non-accredited” investors and to an unlimited

number of accredited investors are permitted.

An issuer under Rule 505 may not use any general solicitation orgeneral advertising to sell its securities.

Introduction to Private Placements16

• Applies to transactions in which not more than $5,000,000 ofsecurities is sold in any consecutive twelve-month period. Sales to thirty-five “non-accredited” investors and to an unlimited

number of accredited investors are permitted.

An issuer under Rule 505 may not use any general solicitation orgeneral advertising to sell its securities.

What is an Accredited Investor?

• Pursuant to Rule 501(a), an individual will be considered anaccredited investor if he or she: earned income that exceeded $200,000 (or $300,000 together with a

spouse) in each of the prior two years, and reasonably expects thesame for the current year, OR

has a net worth over $1 million, either alone or together with a spouse(excluding the value of the person’s primary residence and any loanssecured by the residence (up to the value of the residence)).

Introduction to Private Placements17

• Pursuant to Rule 501(a), an individual will be considered anaccredited investor if he or she: earned income that exceeded $200,000 (or $300,000 together with a

spouse) in each of the prior two years, and reasonably expects thesame for the current year, OR

has a net worth over $1 million, either alone or together with a spouse(excluding the value of the person’s primary residence and any loanssecured by the residence (up to the value of the residence)).

Rule 506

• Most frequently used exemption

• Rule 506 is available to all issuers for offerings sold to not morethan thirty-five non-accredited purchasers and an unlimited numberof accredited investors. There is no dollar limitation on offerings under Rule 506. Until recently, general solicitation and advertising was prohibited under

Rule 506

Introduction to Private Placements18

• Most frequently used exemption

• Rule 506 is available to all issuers for offerings sold to not morethan thirty-five non-accredited purchasers and an unlimited numberof accredited investors. There is no dollar limitation on offerings under Rule 506. Until recently, general solicitation and advertising was prohibited under

Rule 506

Impact of the JOBS Act on Rule 506

• In April 2012, the JOBS Act was signed into law with the purpose ofeasing the methods of raising capital and relaxing the regulatoryburden on smaller companies.

• Title II of the JOBS Act directed the SEC to: Remove the prohibition in Regulation D on general solicitation and

general advertising in offerings and sales under Rule 506, provided thatall purchasers of the securities sold in these offerings are accreditedinvestors

Require issuers to take reasonable steps to verify that purchasers areaccredited investors, using methods determined by the SEC

Introduction to Private Placements19

• In April 2012, the JOBS Act was signed into law with the purpose ofeasing the methods of raising capital and relaxing the regulatoryburden on smaller companies.

• Title II of the JOBS Act directed the SEC to: Remove the prohibition in Regulation D on general solicitation and

general advertising in offerings and sales under Rule 506, provided thatall purchasers of the securities sold in these offerings are accreditedinvestors

Require issuers to take reasonable steps to verify that purchasers areaccredited investors, using methods determined by the SEC

Adoption of Final Rules

• On July 10, 2013, the SEC adopted final rules creating subsection(c) of Rule 506, permitting issuers to use general solicitation inRule 506 offerings provided three conditions are met: Each purchaser in the offering is an accredited investor

The issuer takes reasonable steps to verify that each purchaser is anaccredited investors

All other terms and conditions of Rule 501, 502(a) and 502(d) are met

Introduction to Private Placements20

• On July 10, 2013, the SEC adopted final rules creating subsection(c) of Rule 506, permitting issuers to use general solicitation inRule 506 offerings provided three conditions are met: Each purchaser in the offering is an accredited investor

The issuer takes reasonable steps to verify that each purchaser is anaccredited investors

All other terms and conditions of Rule 501, 502(a) and 502(d) are met

Determining Accredited Investor Status

• “Principles-based” determination, depending on facts andcircumstances.

• Three factors identified by the SEC’s adopting release that impactthe determination: The nature of the purchaser and the type of accredited investor it

claims to be

The amount and type of information that the issuer has about thepurchaser

The nature of the offering, such as the manner of solicitation and theterms of the offering

Introduction to Private Placements21

• “Principles-based” determination, depending on facts andcircumstances.

• Three factors identified by the SEC’s adopting release that impactthe determination: The nature of the purchaser and the type of accredited investor it

claims to be

The amount and type of information that the issuer has about thepurchaser

The nature of the offering, such as the manner of solicitation and theterms of the offering

• The SEC has not mandated uniform procedures thatissuers must follow to verify accredited investor statusof purchasers participating in an offering under newRule 506(c).

• The SEC has said that “reasonableness” of steps takento verify status involves “an objective determination bythe issuer (or those acting on its behalf), in the contextof the particular facts and circumstances of eachpurchaser and transaction.”

Introduction to Private Placements22

• The SEC has not mandated uniform procedures thatissuers must follow to verify accredited investor statusof purchasers participating in an offering under newRule 506(c).

• The SEC has said that “reasonableness” of steps takento verify status involves “an objective determination bythe issuer (or those acting on its behalf), in the contextof the particular facts and circumstances of eachpurchaser and transaction.”

What is general solicitation?

• Regulation D does not define “general solicitation” but indicates inRule 502(c) that it includes “any advertisement, article, notice or other communication published in

any newspaper, magazine or similar media or broadcast over televisionor radio” or “any seminar or meeting whose attendees have beeninvited by general solicitation.” This concept was later extended tointernet activity.

Introduction to Private Placements23

• Regulation D does not define “general solicitation” but indicates inRule 502(c) that it includes “any advertisement, article, notice or other communication published in

any newspaper, magazine or similar media or broadcast over televisionor radio” or “any seminar or meeting whose attendees have beeninvited by general solicitation.” This concept was later extended tointernet activity.

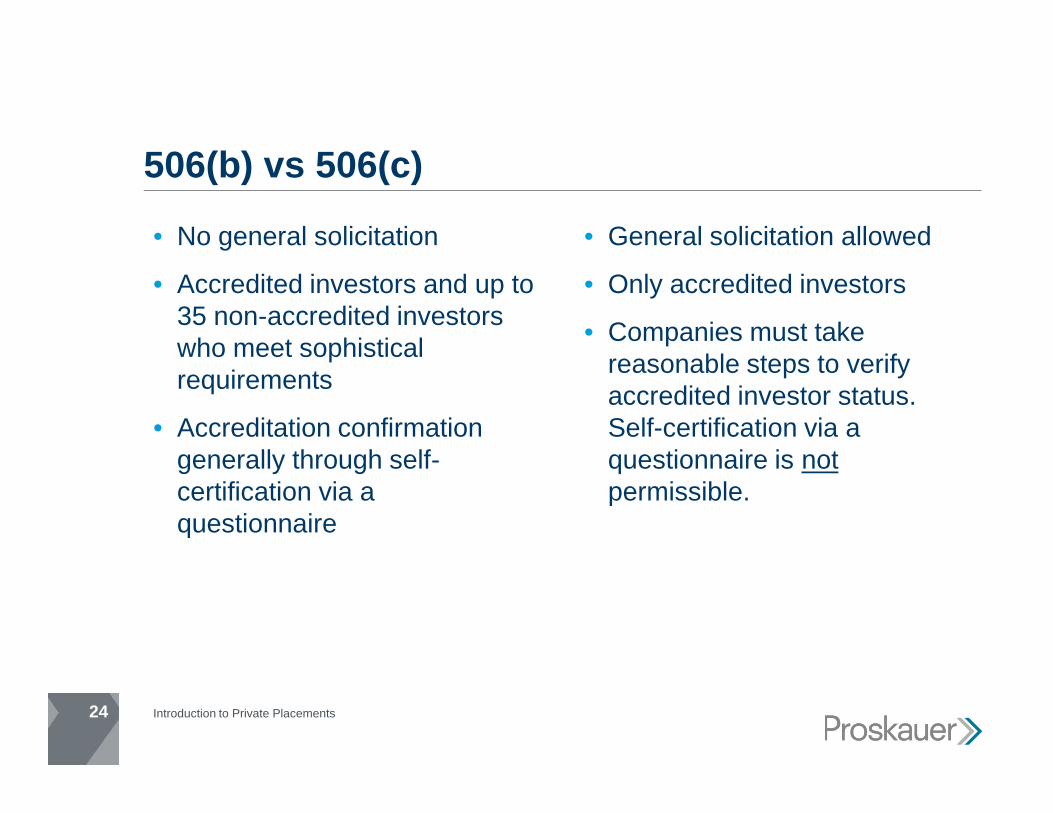

506(b) vs 506(c)

• No general solicitation

• Accredited investors and up to35 non-accredited investorswho meet sophisticalrequirements

• Accreditation confirmationgenerally through self-certification via aquestionnaire

• General solicitation allowed

• Only accredited investors

• Companies must takereasonable steps to verifyaccredited investor status.Self-certification via aquestionnaire is notpermissible.

24

• No general solicitation

• Accredited investors and up to35 non-accredited investorswho meet sophisticalrequirements

• Accreditation confirmationgenerally through self-certification via aquestionnaire

• General solicitation allowed

• Only accredited investors

• Companies must takereasonable steps to verifyaccredited investor status.Self-certification via aquestionnaire is notpermissible.

Introduction to Private Placements

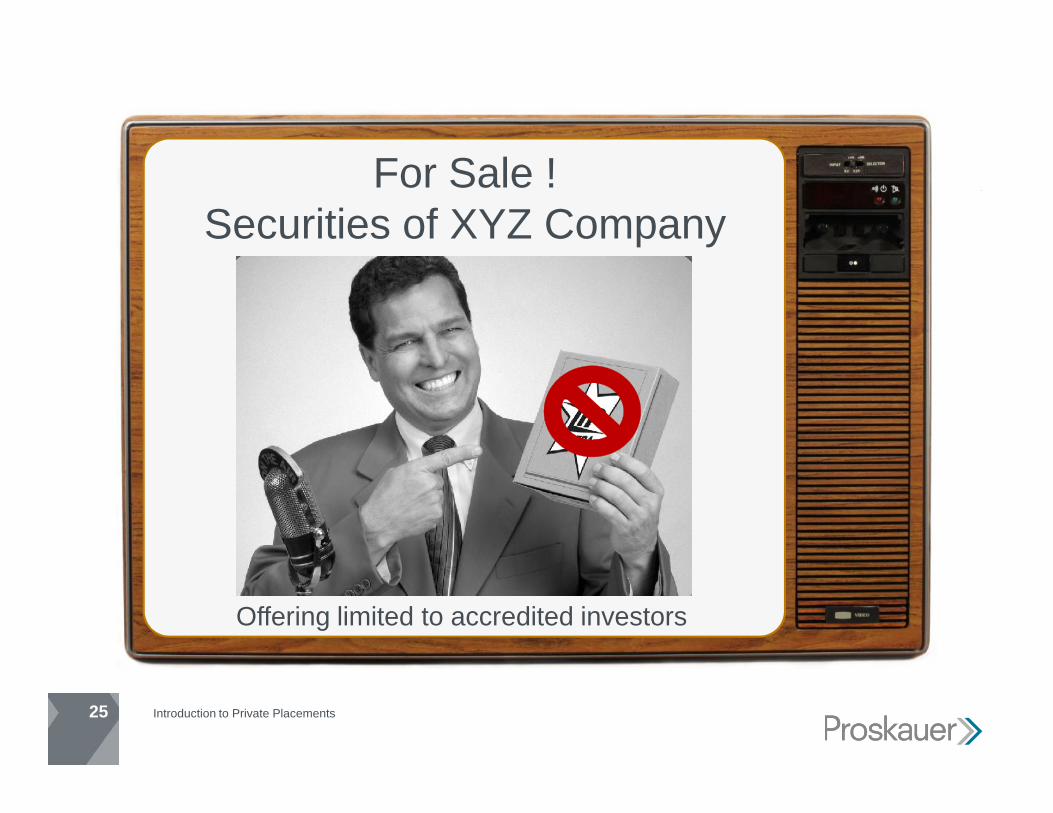

For Sale !Securities of XYZ Company

25

Offering limited to accredited investors

Introduction to Private Placements

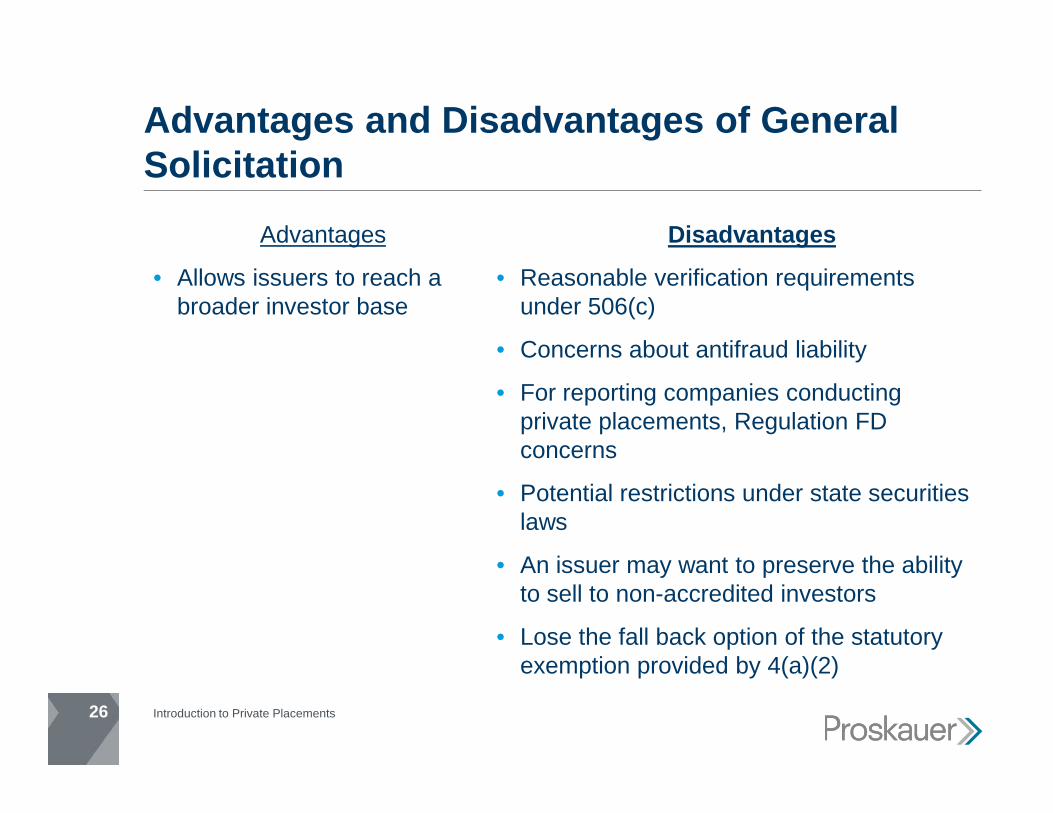

Advantages and Disadvantages of GeneralSolicitation

Advantages

• Allows issuers to reach abroader investor base

Disadvantages

• Reasonable verification requirementsunder 506(c)

• Concerns about antifraud liability

• For reporting companies conductingprivate placements, Regulation FDconcerns

• Potential restrictions under state securitieslaws

• An issuer may want to preserve the abilityto sell to non-accredited investors

• Lose the fall back option of the statutoryexemption provided by 4(a)(2)

26

Advantages

• Allows issuers to reach abroader investor base

Disadvantages

• Reasonable verification requirementsunder 506(c)

• Concerns about antifraud liability

• For reporting companies conductingprivate placements, Regulation FDconcerns

• Potential restrictions under state securitieslaws

• An issuer may want to preserve the abilityto sell to non-accredited investors

• Lose the fall back option of the statutoryexemption provided by 4(a)(2)

Introduction to Private Placements

SEC Guidance on General Solicitation

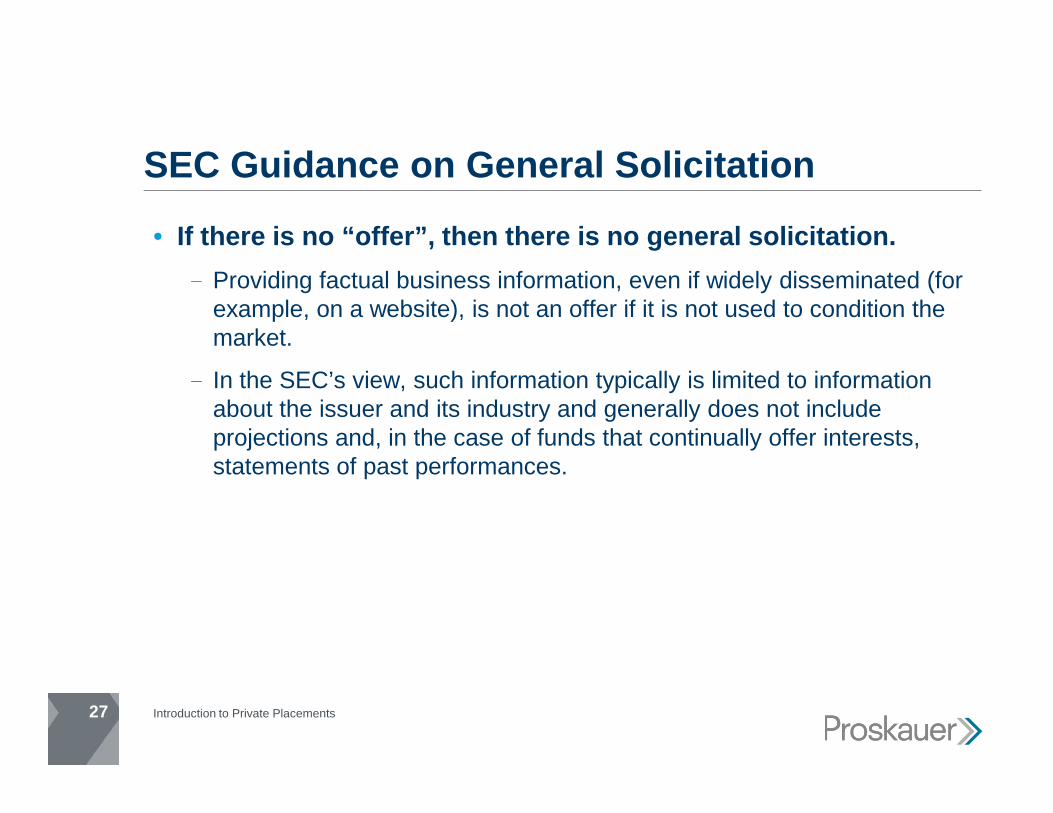

• If there is no “offer”, then there is no general solicitation. Providing factual business information, even if widely disseminated (for

example, on a website), is not an offer if it is not used to condition themarket.

In the SEC’s view, such information typically is limited to informationabout the issuer and its industry and generally does not includeprojections and, in the case of funds that continually offer interests,statements of past performances.

Introduction to Private Placements27

• If there is no “offer”, then there is no general solicitation. Providing factual business information, even if widely disseminated (for

example, on a website), is not an offer if it is not used to condition themarket.

In the SEC’s view, such information typically is limited to informationabout the issuer and its industry and generally does not includeprojections and, in the case of funds that continually offer interests,statements of past performances.

SEC Guidance on General Solicitation

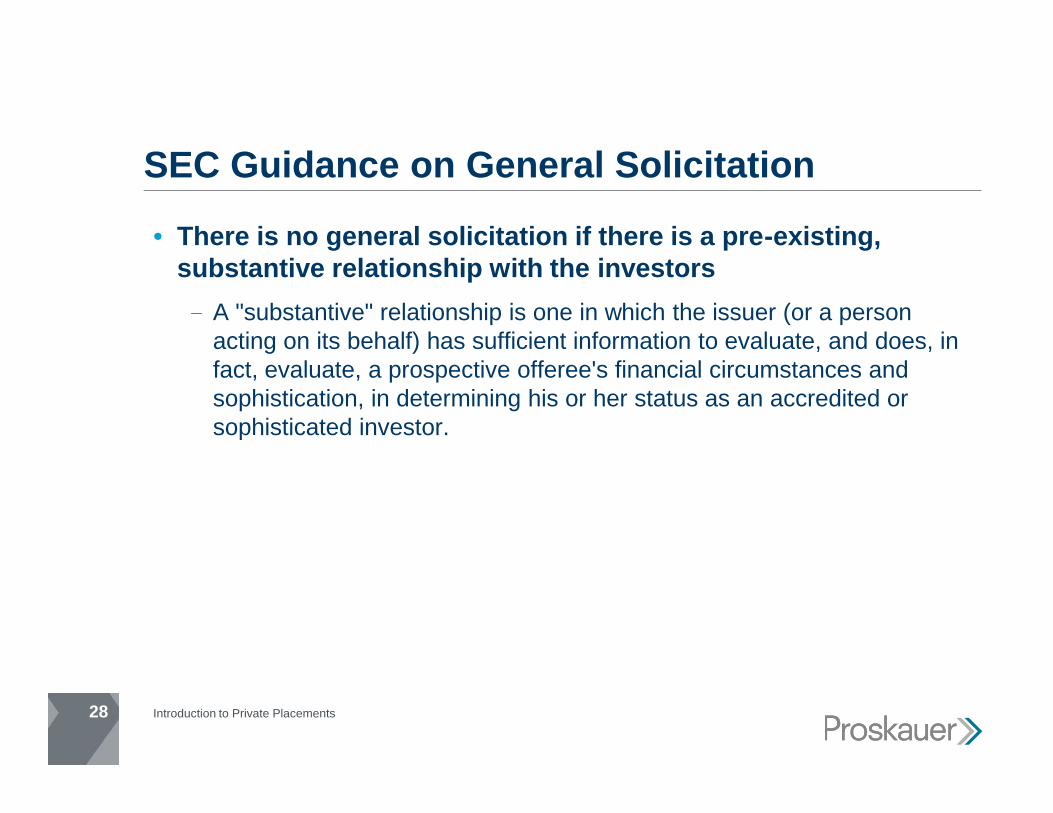

• There is no general solicitation if there is a pre-existing,substantive relationship with the investors A "substantive" relationship is one in which the issuer (or a person

acting on its behalf) has sufficient information to evaluate, and does, infact, evaluate, a prospective offeree's financial circumstances andsophistication, in determining his or her status as an accredited orsophisticated investor.

Introduction to Private Placements28

• There is no general solicitation if there is a pre-existing,substantive relationship with the investors A "substantive" relationship is one in which the issuer (or a person

acting on its behalf) has sufficient information to evaluate, and does, infact, evaluate, a prospective offeree's financial circumstances andsophistication, in determining his or her status as an accredited orsophisticated investor.

What Constitutes a Pre-Existing, SubstantiveRelationship?

• A registered broker-dealer can create a relationship with an investorand then use that relationship to make an offer as placement agent foran issuer without that offer being a general solicitation. (The “two-callrule”)

• Registered investment advisers can form the requisite substantiverelationship the same as registered broker-dealers.

• Under certain circumstances, other third parties also can form therequisite relationship with investors, including operators of angelinvestor networks and investor platforms.

• An issuer can rely on the relationship established by others, when thatreliance is justified. Thus, an issuer can make offers to investorsintroduced by a broker-dealer or an investment adviser even if thatintroducing party is not acting as an agent of the issuer, as aplacement agent would.

Introduction to Private Placements29

• A registered broker-dealer can create a relationship with an investorand then use that relationship to make an offer as placement agent foran issuer without that offer being a general solicitation. (The “two-callrule”)

• Registered investment advisers can form the requisite substantiverelationship the same as registered broker-dealers.

• Under certain circumstances, other third parties also can form therequisite relationship with investors, including operators of angelinvestor networks and investor platforms.

• An issuer can rely on the relationship established by others, when thatreliance is justified. Thus, an issuer can make offers to investorsintroduced by a broker-dealer or an investment adviser even if thatintroducing party is not acting as an agent of the issuer, as aplacement agent would.

What about online investor platforms?

• Citizen VC, Inc. No Action Letter Guidance (August 2015) Citizen VC is the manager of a venture capital investment platform

through which it aggregates investments of prospective investors inspecial purpose vehicles that invest in seed, early-stage, emerginggrowth and late-stage private companies.

Citizen VC requested no-action letter confirmation that the policies andprocedures described in its letter “will create a substantive, pre-existingrelationship between Citizen VC and prospective investors, such that itcould take advantage of the 506(b) exemption

Introduction to Private Placements30

• Citizen VC, Inc. No Action Letter Guidance (August 2015) Citizen VC is the manager of a venture capital investment platform

through which it aggregates investments of prospective investors inspecial purpose vehicles that invest in seed, early-stage, emerginggrowth and late-stage private companies.

Citizen VC requested no-action letter confirmation that the policies andprocedures described in its letter “will create a substantive, pre-existingrelationship between Citizen VC and prospective investors, such that itcould take advantage of the 506(b) exemption

What about online investor platforms?

• The Takeaway: The pre-existing relationship is not time based nor is it satisfied by

answering a mere two questions. Rather, the establishment of a pre-existing relationship depends on the QUALITY of the relationshipbetween the issuer and a potential investor

Online investor platforms can avoid general solicitation although widelysoliciting potential investors if they establish the requisite relationshipbefore making any specific offer

Introduction to Private Placements31

• The Takeaway: The pre-existing relationship is not time based nor is it satisfied by

answering a mere two questions. Rather, the establishment of a pre-existing relationship depends on the QUALITY of the relationshipbetween the issuer and a potential investor

Online investor platforms can avoid general solicitation although widelysoliciting potential investors if they establish the requisite relationshipbefore making any specific offer

Rule 507 and Bad Actors

• Section 926 of the Dodd-Frank Act required the SEC to adopt rules thatwould make the Rule 506 exemption unavailable for any securities offeringin which certain “felons” or other “bad actors” are involved

• In light of concerns raised by investor and consumer advocates that therelaxation of the prohibition against general solicitation in certain Rule 506offerings would lead to an increased incidence of fraud, the SEC tookaction on the bad actor provisions at the same time as it promulgated thefinal Rule 506 amendments

• On July 10, 2013, the SEC adopted the final amendment that adds “badactor” disqualification requirements to Rule 506 of the Securities Act, whichprohibit issuers and others, such as underwriters, placement agents,directors, executive officers, and certain shareholders of the issuer fromparticipating in exempt securities offerings, if they have been convicted of,or are subject to court or administrative sanctions for, securities fraud orother violations of specified laws.

Introduction to Private Placements32

• Section 926 of the Dodd-Frank Act required the SEC to adopt rules thatwould make the Rule 506 exemption unavailable for any securities offeringin which certain “felons” or other “bad actors” are involved

• In light of concerns raised by investor and consumer advocates that therelaxation of the prohibition against general solicitation in certain Rule 506offerings would lead to an increased incidence of fraud, the SEC tookaction on the bad actor provisions at the same time as it promulgated thefinal Rule 506 amendments

• On July 10, 2013, the SEC adopted the final amendment that adds “badactor” disqualification requirements to Rule 506 of the Securities Act, whichprohibit issuers and others, such as underwriters, placement agents,directors, executive officers, and certain shareholders of the issuer fromparticipating in exempt securities offerings, if they have been convicted of,or are subject to court or administrative sanctions for, securities fraud orother violations of specified laws.

Thank You

The information provided in this slide presentation is not, is not intended to be, and shall not be construed to be, either the provisionof legal advice or an offer to provide legal services, nor does it necessarily reflect the opinions of the firm, our lawyers or ourclients. No client-lawyer relationship between you and the firm is or may be created by your access to or use of this presentation orany information contained on them. Rather, the content is intended as a general overview of the subject matter covered. ProskauerRose LLP (Proskauer) is not obligated to provide updates on the information presented herein. Those viewing this presentation areencouraged to seek direct counsel on legal questions. © Proskauer Rose LLP. All Rights Reserved.

Presenter:

Stuart Bressman, Partner

Structuring PrivatePlacement Memorandumfor the Sale and Solicitationof Securities

Strafford Publications

April 20, 2016

Eric C. Perkins, [email protected]

Strafford Publications

April 20, 2016

Eric C. Perkins, [email protected]

Essential Elements of a PPM

Big Picture Considerations The dual purposes of a PPM – Compliance and Marketing The style and substance of a PPM will often vary depending upon

the targeted audience, deal structure, sales distribution channel(s),and the specific exemption being relied upon.

PRIMARY GOAL = Full and fair disclosure of all material information tosatisfy the antifraud provisions of the federal securities laws as well asthe specific disclosure requirements associated with the exemptionupon which the issuer is relying.

Big Picture Considerations The dual purposes of a PPM – Compliance and Marketing The style and substance of a PPM will often vary depending upon

the targeted audience, deal structure, sales distribution channel(s),and the specific exemption being relied upon.

PRIMARY GOAL = Full and fair disclosure of all material information tosatisfy the antifraud provisions of the federal securities laws as well asthe specific disclosure requirements associated with the exemptionupon which the issuer is relying.

35

Essential Elements of a PPM Disclosure of all material facts about:

1. The Issuer

2. Management

3. Business model (market, competition, etc.)

4. Operating history and investment objectives

5. Finances

6. Significant Legal, Compliance, and Tax Issues

Disclosure of all material facts about:

1. The Issuer

2. Management

3. Business model (market, competition, etc.)

4. Operating history and investment objectives

5. Finances

6. Significant Legal, Compliance, and Tax Issues

36

Essential Elements of a PPM Cover Page Company name Amount being raised Type of security Brief summary of issuer’s business or purpose of offering Brief description of a few key risk factors Abbreviated uses and proceeds table Date and Copy Number (for PPM tracking purposes)

Cover Page Company name Amount being raised Type of security Brief summary of issuer’s business or purpose of offering Brief description of a few key risk factors Abbreviated uses and proceeds table Date and Copy Number (for PPM tracking purposes)

37

Essential Elements of a PPM

Cover “page” might actually run for several pages

Trying to give a basic overview of the offering

Make sure the cover page disclosure is consistent withthe main body of the PPM

Cover “page” might actually run for several pages

Trying to give a basic overview of the offering

Make sure the cover page disclosure is consistent withthe main body of the PPM

38

Essential Elements of a PPM

WHO MAY INVEST Describe investor suitability requirements for the offering Accredited vs Nonaccredited Minimum Investment Investment Experience Limitations on Investment Amount (e.g., no more than 5%

of an investor’s net worth) Risk Tolerance

WHO MAY INVEST Describe investor suitability requirements for the offering Accredited vs Nonaccredited Minimum Investment Investment Experience Limitations on Investment Amount (e.g., no more than 5%

of an investor’s net worth) Risk Tolerance

39

Essential Elements of a PPM

SUMMARY OF THE OFFERING An executive summary or basic term sheet of the offering,

such as: Type of Securities Offered Contingency/Escrow Requirements Description of the Business Acquisition Strategy Debt Financing Structure

SUMMARY OF THE OFFERING An executive summary or basic term sheet of the offering,

such as: Type of Securities Offered Contingency/Escrow Requirements Description of the Business Acquisition Strategy Debt Financing Structure

40

Essential Elements of a PPM

SUMMARY OF THE OFFERING (continued) Summary of Management Team and Experience Compensation of Issuer and Affiliates Summary of Key Agreements Summary of any Significant Conflicts of Interest

SUMMARY OF THE OFFERING (continued) Summary of Management Team and Experience Compensation of Issuer and Affiliates Summary of Key Agreements Summary of any Significant Conflicts of Interest

41

Essential Elements of a PPM

RISK FACTORS From a risk management perspective, probably the most

important section of the PPM Source of vigorous debate between legal and marketing Look to SEC registration statements and PPMs from similar

industries and offering structures Refer to NASAA risk factor guidelines

(http://www.nasaa.org/wp-content/uploads/2011/07/3-Risk_Disclosure.pdf)

RISK FACTORS From a risk management perspective, probably the most

important section of the PPM Source of vigorous debate between legal and marketing Look to SEC registration statements and PPMs from similar

industries and offering structures Refer to NASAA risk factor guidelines

(http://www.nasaa.org/wp-content/uploads/2011/07/3-Risk_Disclosure.pdf)

42

Essential Elements of a PPM

SUMMARY OF NASAA RISK FACTOR GUIDELINES

Risk factors should be prioritized by level of significance

Risk factor captions (headings) should be underlined or inbold type and should succinctly identify the risk elementof the risk factor (i.e., a quick but complete statement,not a single word or a full paragraph).

Don’t be repetitive, use cross references to other sections

SUMMARY OF NASAA RISK FACTOR GUIDELINES

Risk factors should be prioritized by level of significance

Risk factor captions (headings) should be underlined or inbold type and should succinctly identify the risk elementof the risk factor (i.e., a quick but complete statement,not a single word or a full paragraph).

Don’t be repetitive, use cross references to other sections

43

Essential Elements of a PPM

RISK FACTORS Use general categories Real Estate Risks Financing Risks Industry Risks Deal Structure Risks Private Offering and Lack of Liquidity Risks Tax Risks

RISK FACTORS Use general categories Real Estate Risks Financing Risks Industry Risks Deal Structure Risks Private Offering and Lack of Liquidity Risks Tax Risks

44

Essential Elements of a PPM

RISK FACTORS In theory, you should avoid generic, boiler plate risk factors

(but most practitioners can’t help themselves and leantoward more disclosure in the risk factors section).

Don’t try to explain away or minimize risk in the risk factorsection.

RISK FACTORS In theory, you should avoid generic, boiler plate risk factors

(but most practitioners can’t help themselves and leantoward more disclosure in the risk factors section).

Don’t try to explain away or minimize risk in the risk factorsection.

45

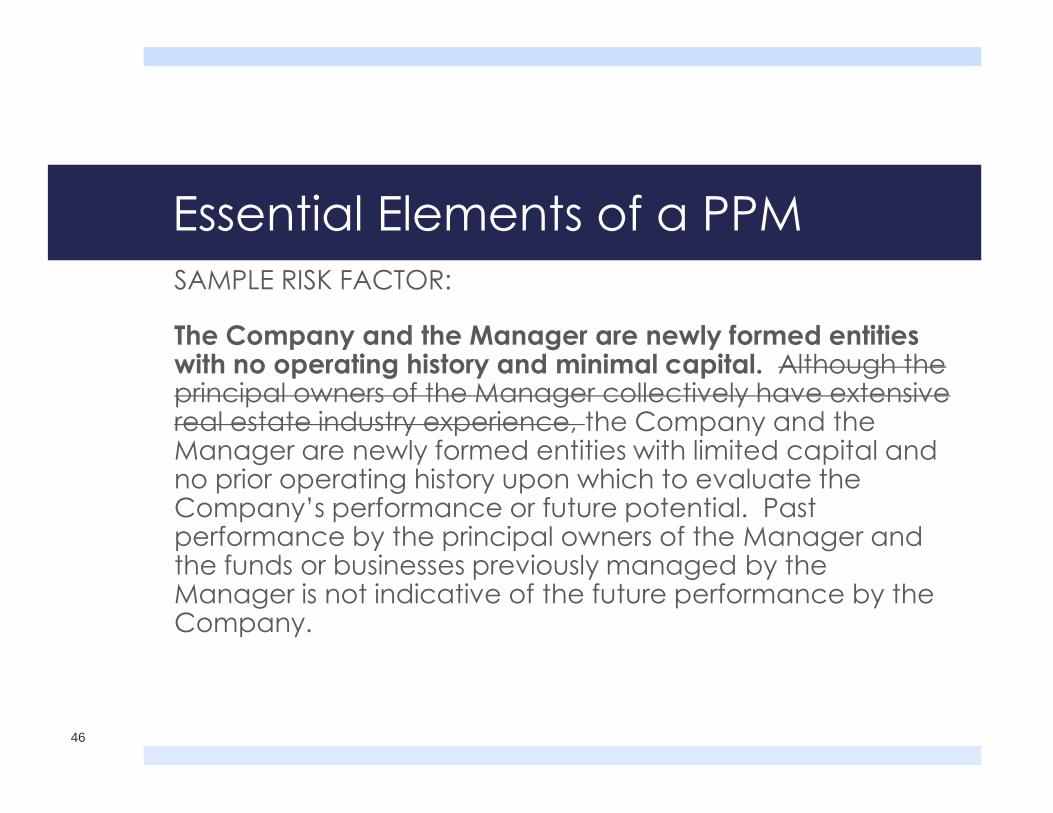

Essential Elements of a PPMSAMPLE RISK FACTOR:

The Company and the Manager are newly formed entitieswith no operating history and minimal capital. Although theprincipal owners of the Manager collectively have extensivereal estate industry experience, the Company and theManager are newly formed entities with limited capital andno prior operating history upon which to evaluate theCompany’s performance or future potential. Pastperformance by the principal owners of the Manager andthe funds or businesses previously managed by theManager is not indicative of the future performance by theCompany.

SAMPLE RISK FACTOR:

The Company and the Manager are newly formed entitieswith no operating history and minimal capital. Although theprincipal owners of the Manager collectively have extensivereal estate industry experience, the Company and theManager are newly formed entities with limited capital andno prior operating history upon which to evaluate theCompany’s performance or future potential. Pastperformance by the principal owners of the Manager andthe funds or businesses previously managed by theManager is not indicative of the future performance by theCompany.

46

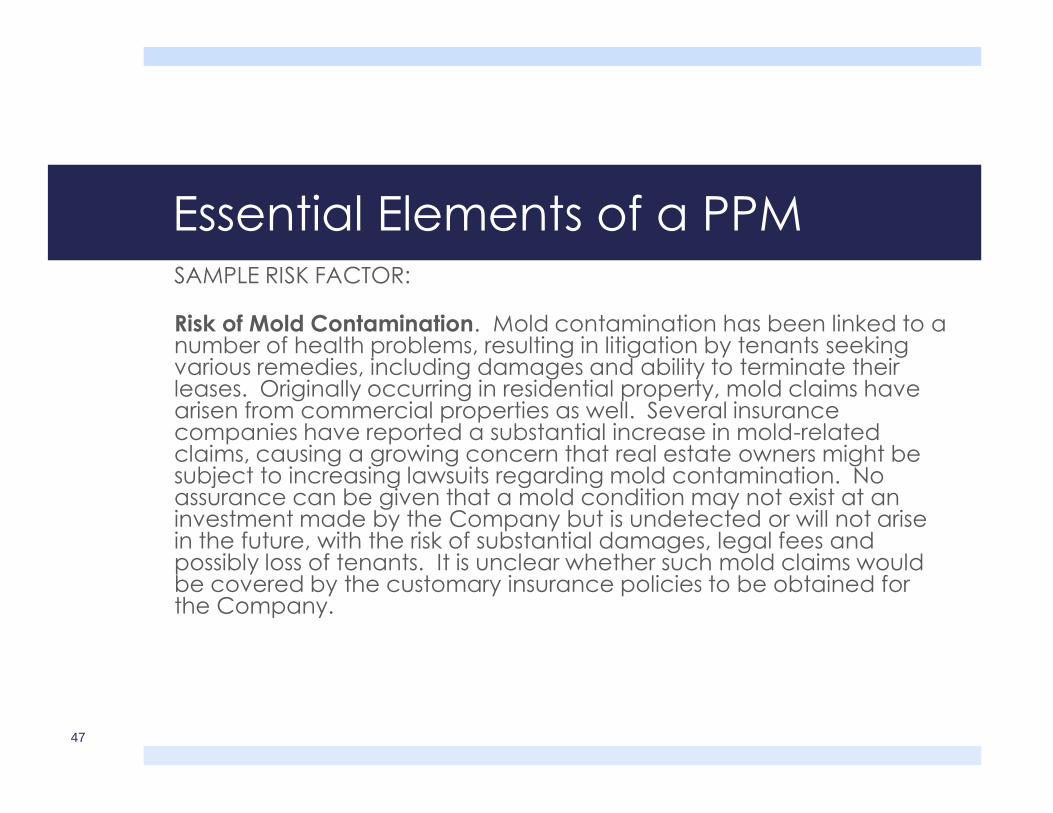

Essential Elements of a PPMSAMPLE RISK FACTOR:

Risk of Mold Contamination. Mold contamination has been linked to anumber of health problems, resulting in litigation by tenants seekingvarious remedies, including damages and ability to terminate theirleases. Originally occurring in residential property, mold claims havearisen from commercial properties as well. Several insurancecompanies have reported a substantial increase in mold-relatedclaims, causing a growing concern that real estate owners might besubject to increasing lawsuits regarding mold contamination. Noassurance can be given that a mold condition may not exist at aninvestment made by the Company but is undetected or will not arisein the future, with the risk of substantial damages, legal fees andpossibly loss of tenants. It is unclear whether such mold claims wouldbe covered by the customary insurance policies to be obtained forthe Company.

SAMPLE RISK FACTOR:

Risk of Mold Contamination. Mold contamination has been linked to anumber of health problems, resulting in litigation by tenants seekingvarious remedies, including damages and ability to terminate theirleases. Originally occurring in residential property, mold claims havearisen from commercial properties as well. Several insurancecompanies have reported a substantial increase in mold-relatedclaims, causing a growing concern that real estate owners might besubject to increasing lawsuits regarding mold contamination. Noassurance can be given that a mold condition may not exist at aninvestment made by the Company but is undetected or will not arisein the future, with the risk of substantial damages, legal fees andpossibly loss of tenants. It is unclear whether such mold claims wouldbe covered by the customary insurance policies to be obtained forthe Company.

47

Essential Elements of a PPMSOURCE AND USE OF PROCEEDS

Typically a table with columns identifying the primarysources and uses of proceeds from the offering, withexplanatory footnotes.

SOURCE AND USE OF PROCEEDS

Typically a table with columns identifying the primarysources and uses of proceeds from the offering, withexplanatory footnotes.

48

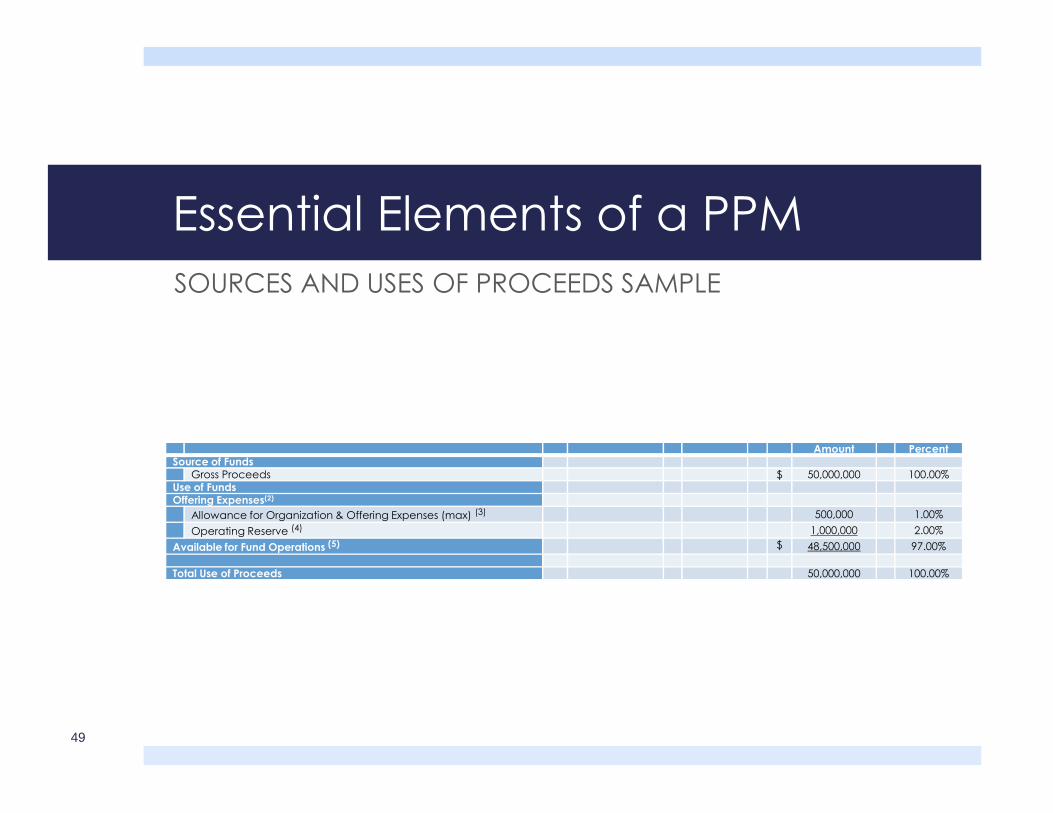

Essential Elements of a PPMSOURCES AND USES OF PROCEEDS SAMPLE

Amount PercentSource of Funds

Gross Proceeds $ 50,000,000 100.00%Use of FundsOffering Expenses(2)

Allowance for Organization & Offering Expenses (max) (3) 500,000 1.00%Operating Reserve (4) 1,000,000 2.00%

Available for Fund Operations (5) $ 48,500,000 97.00%

Total Use of Proceeds 50,000,000 100.00%

49

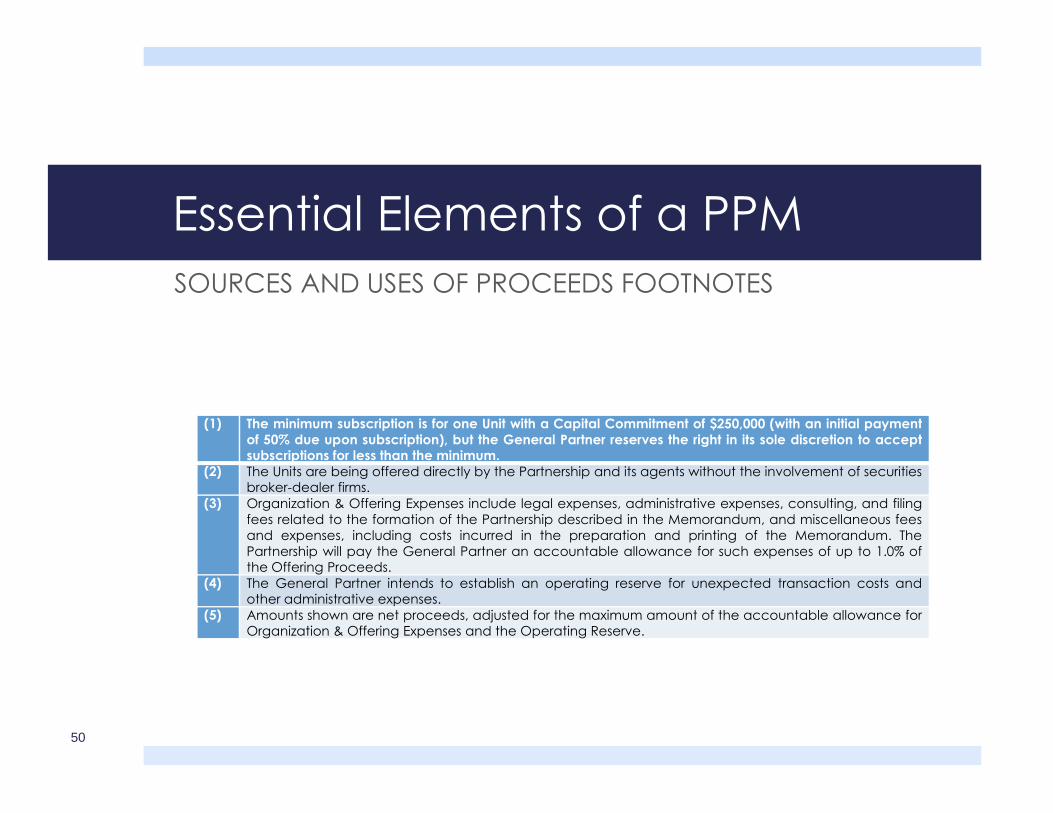

Essential Elements of a PPMSOURCES AND USES OF PROCEEDS FOOTNOTES

(1) The minimum subscription is for one Unit with a Capital Commitment of $250,000 (with an initial paymentof 50% due upon subscription), but the General Partner reserves the right in its sole discretion to acceptsubscriptions for less than the minimum.

(2) The Units are being offered directly by the Partnership and its agents without the involvement of securitiesbroker-dealer firms.

(3) Organization & Offering Expenses include legal expenses, administrative expenses, consulting, and filingfees related to the formation of the Partnership described in the Memorandum, and miscellaneous feesand expenses, including costs incurred in the preparation and printing of the Memorandum. ThePartnership will pay the General Partner an accountable allowance for such expenses of up to 1.0% ofthe Offering Proceeds.

(4) The General Partner intends to establish an operating reserve for unexpected transaction costs andother administrative expenses.

(5) Amounts shown are net proceeds, adjusted for the maximum amount of the accountable allowance forOrganization & Offering Expenses and the Operating Reserve.

50

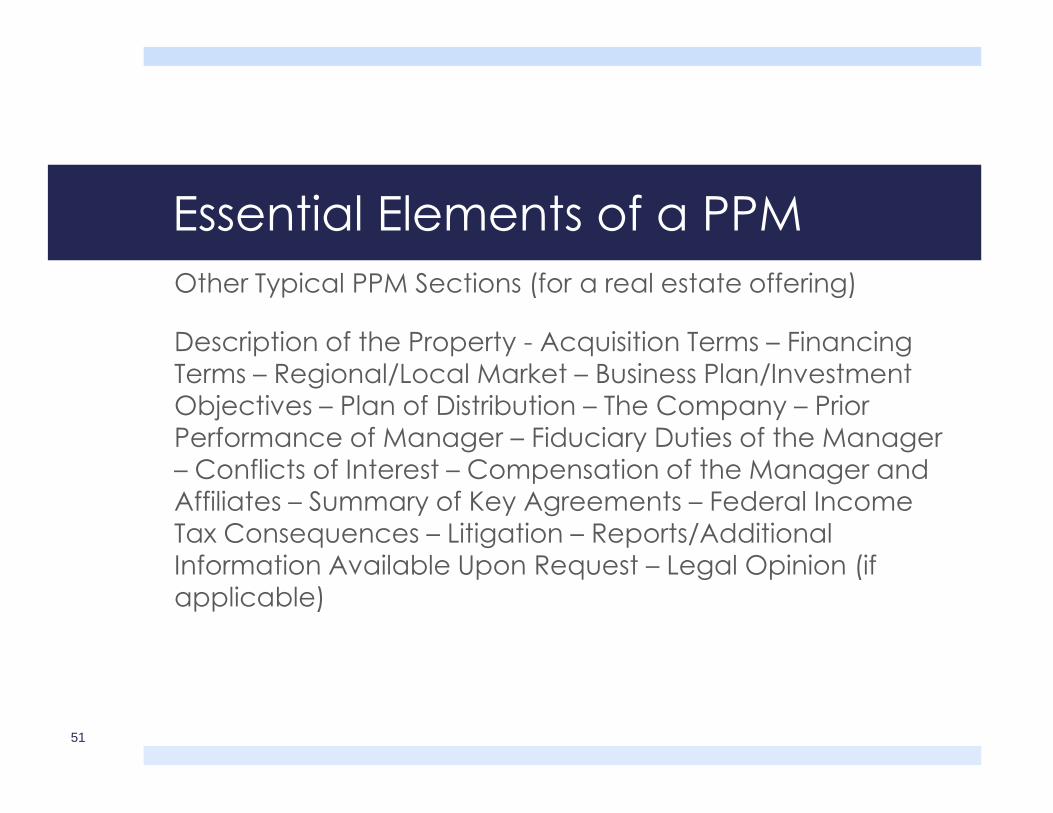

Essential Elements of a PPMOther Typical PPM Sections (for a real estate offering)

Description of the Property - Acquisition Terms – FinancingTerms – Regional/Local Market – Business Plan/InvestmentObjectives – Plan of Distribution – The Company – PriorPerformance of Manager – Fiduciary Duties of the Manager– Conflicts of Interest – Compensation of the Manager andAffiliates – Summary of Key Agreements – Federal IncomeTax Consequences – Litigation – Reports/AdditionalInformation Available Upon Request – Legal Opinion (ifapplicable)

Other Typical PPM Sections (for a real estate offering)

Description of the Property - Acquisition Terms – FinancingTerms – Regional/Local Market – Business Plan/InvestmentObjectives – Plan of Distribution – The Company – PriorPerformance of Manager – Fiduciary Duties of the Manager– Conflicts of Interest – Compensation of the Manager andAffiliates – Summary of Key Agreements – Federal IncomeTax Consequences – Litigation – Reports/AdditionalInformation Available Upon Request – Legal Opinion (ifapplicable)

51

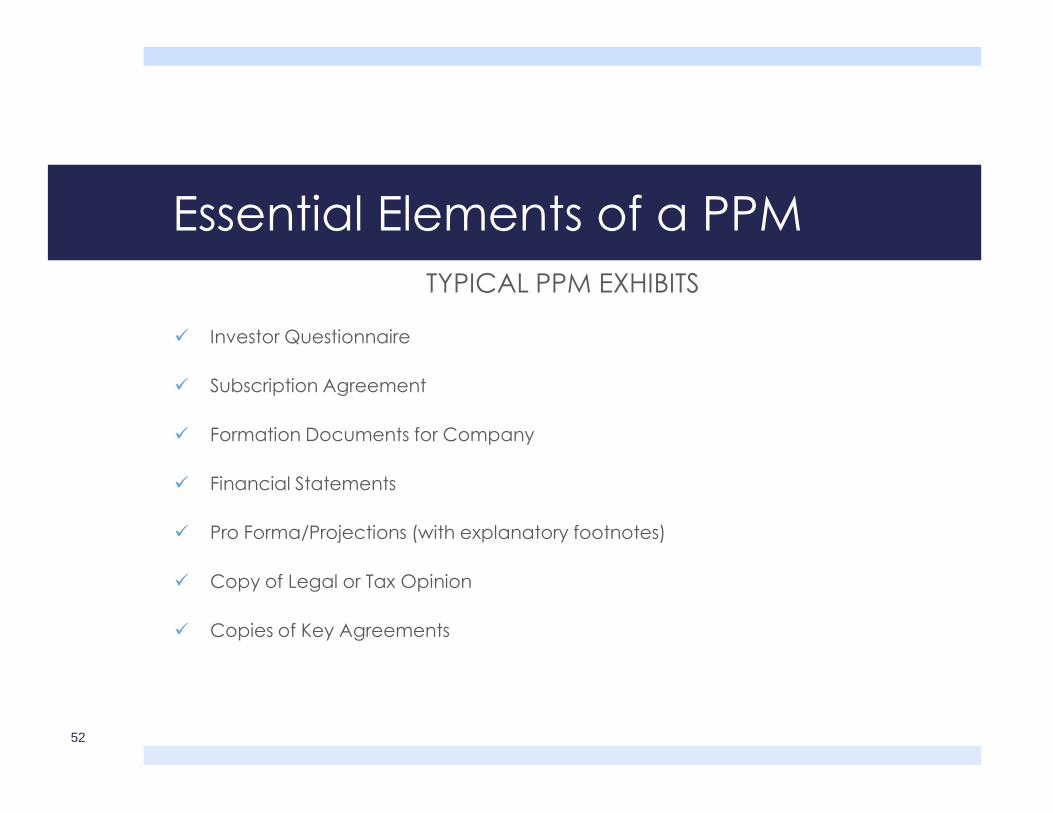

Essential Elements of a PPMTYPICAL PPM EXHIBITS

Investor Questionnaire

Subscription Agreement

Formation Documents for Company

Financial Statements

Pro Forma/Projections (with explanatory footnotes)

Copy of Legal or Tax Opinion

Copies of Key Agreements

TYPICAL PPM EXHIBITS

Investor Questionnaire

Subscription Agreement

Formation Documents for Company

Financial Statements

Pro Forma/Projections (with explanatory footnotes)

Copy of Legal or Tax Opinion

Copies of Key Agreements

52

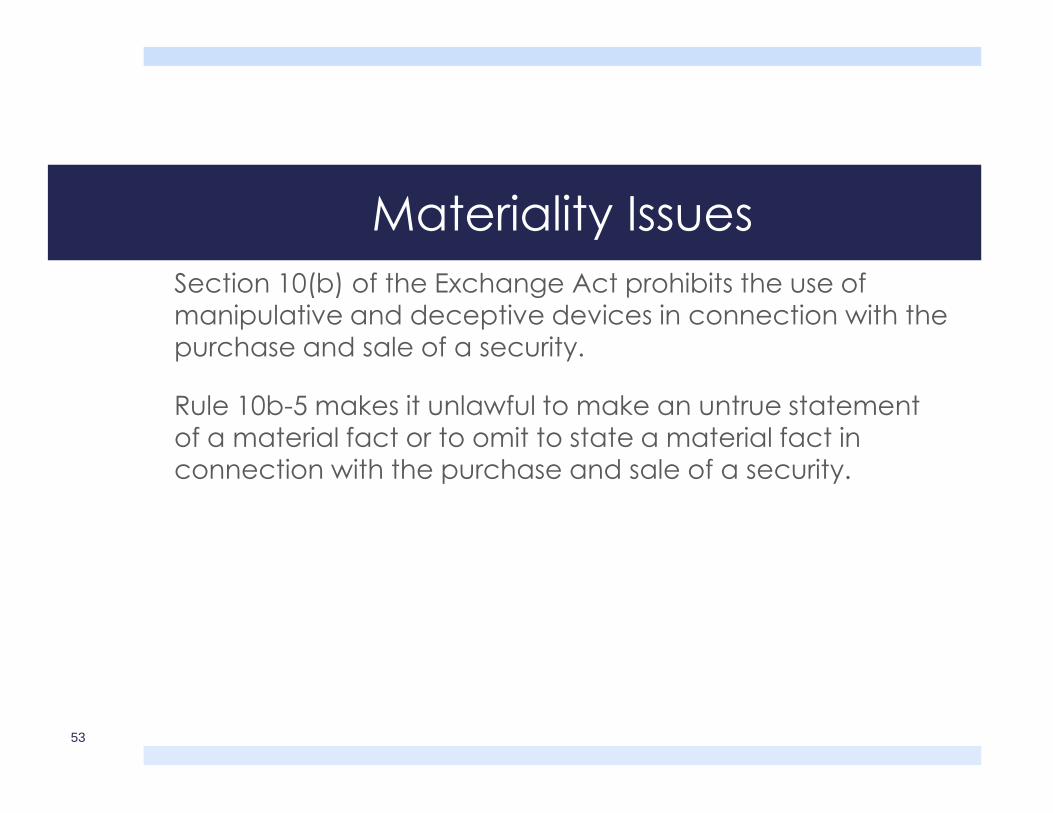

Materiality IssuesSection 10(b) of the Exchange Act prohibits the use ofmanipulative and deceptive devices in connection with thepurchase and sale of a security.

Rule 10b-5 makes it unlawful to make an untrue statementof a material fact or to omit to state a material fact inconnection with the purchase and sale of a security.

Section 10(b) of the Exchange Act prohibits the use ofmanipulative and deceptive devices in connection with thepurchase and sale of a security.

Rule 10b-5 makes it unlawful to make an untrue statementof a material fact or to omit to state a material fact inconnection with the purchase and sale of a security.

53

Materiality IssuesWhat is material?

Whether a fact is material “depends on the significance thereasonable investor would place on the withheld ormisrepresented information.” Basic Inc. v. Levinson, 485 U.S.224, 240 (1988).

TIP: When drafting a PPM, the materiality question oftenboils down to common sense, so when in doubt, go aheadand disclose.

What is material?

Whether a fact is material “depends on the significance thereasonable investor would place on the withheld ormisrepresented information.” Basic Inc. v. Levinson, 485 U.S.224, 240 (1988).

TIP: When drafting a PPM, the materiality question oftenboils down to common sense, so when in doubt, go aheadand disclose.

54

Materiality Issues

When the issue is litigated, materiality is a mixed question oflaw and fact, thus it can be decided as a matter of law onlyif reasonable minds could NOT disagree on the issue.

When the issue is litigated, materiality is a mixed question oflaw and fact, thus it can be decided as a matter of law onlyif reasonable minds could NOT disagree on the issue.

55

Materiality IssuesExamples of facts deemed by courts to be immaterial insecurities litigation:

--CEO’s misrepresentation about not finishing college wasnot “material” because it was not substantially likely thatreasonable investors would devalue the securities whenviewed against the total mix of available information.Greenhouse v. MCG Capital Corp., 392 F. 3d 650 (4th Cir.2004).

Examples of facts deemed by courts to be immaterial insecurities litigation:

--CEO’s misrepresentation about not finishing college wasnot “material” because it was not substantially likely thatreasonable investors would devalue the securities whenviewed against the total mix of available information.Greenhouse v. MCG Capital Corp., 392 F. 3d 650 (4th Cir.2004).

56

Materiality IssuesExamples of facts deemed by courts to be immaterial insecurities litigation:

Issuer had no duty to disclose the imminent collapse of asignificant merger until it actually collapsed; informationregarding the likely merger termination was deemed notmaterial because, prior to the actual occurrence, such anevent was speculative or contingent. In re CDNOW, Inc.,Sec. Litig., 138 F. Supp. 2d 624 (E.D. Pa 2001).

Examples of facts deemed by courts to be immaterial insecurities litigation:

Issuer had no duty to disclose the imminent collapse of asignificant merger until it actually collapsed; informationregarding the likely merger termination was deemed notmaterial because, prior to the actual occurrence, such anevent was speculative or contingent. In re CDNOW, Inc.,Sec. Litig., 138 F. Supp. 2d 624 (E.D. Pa 2001).

57

Materiality IssuesExamples of situations where a court foundmisrepresentations or omissions to be material:

Failure to disclose company’s supply problems was materialwhere company issued statements that its past supplyproblems “had been resolved” and emphasized that amajority of its projected revenue would be based on thesale of products dependent on such supply. Marucci v.Overland Data, Inc., No. 97-C-0833, 1999 U.S. Dist. LEXIS12194 (S.D. Cal. Aug. 2, 1999).

Examples of situations where a court foundmisrepresentations or omissions to be material:

Failure to disclose company’s supply problems was materialwhere company issued statements that its past supplyproblems “had been resolved” and emphasized that amajority of its projected revenue would be based on thesale of products dependent on such supply. Marucci v.Overland Data, Inc., No. 97-C-0833, 1999 U.S. Dist. LEXIS12194 (S.D. Cal. Aug. 2, 1999).

58

Materiality IssuesExamples of situations where a court foundmisrepresentations or omissions to be material:

U.S. Supreme Court ruled that company violated Section 10b-9 by failing todisclose information regarding instances of anosmia (loss of sense of smell)in a number of consumers using its Zicam Cold Remedy product, includinginfo from medical studies indicating a causal link between the product andanosmia because consumers would “likely view the risks of Zicam asoutweighing the benefits and that investors would view the information asmaterial.” Matrixx Initiatives, Inc. v. Siracusano, 131 S. Ct. 1309 (2011).

Examples of situations where a court foundmisrepresentations or omissions to be material:

U.S. Supreme Court ruled that company violated Section 10b-9 by failing todisclose information regarding instances of anosmia (loss of sense of smell)in a number of consumers using its Zicam Cold Remedy product, includinginfo from medical studies indicating a causal link between the product andanosmia because consumers would “likely view the risks of Zicam asoutweighing the benefits and that investors would view the information asmaterial.” Matrixx Initiatives, Inc. v. Siracusano, 131 S. Ct. 1309 (2011).

59

Materiality IssuesConsiderations on Materiality in Private Offerings

Ask company officers what “keeps them up at night” to flesh outpotential risk factors and other material disclosure issues.

When company officers protest against a risk factor or item of disclosureor try to explain why its not a risk, that is often a good litmus test that it isa material risk and should be included in the final PPM.

Look to SEC registration statements, SEC Industry Guides(https://www.sec.gov/about/forms/industryguides.pdf), industryassociation “best practices” guides as points of reference andguidance on materiality.

Considerations on Materiality in Private Offerings

Ask company officers what “keeps them up at night” to flesh outpotential risk factors and other material disclosure issues.

When company officers protest against a risk factor or item of disclosureor try to explain why its not a risk, that is often a good litmus test that it isa material risk and should be included in the final PPM.

Look to SEC registration statements, SEC Industry Guides(https://www.sec.gov/about/forms/industryguides.pdf), industryassociation “best practices” guides as points of reference andguidance on materiality.

60

Structuring PPMs:Assessing Relevant Risk Factors and

Due Diligence

Yelena BarychevPartner, Blank Rome LLP

www.securitiesnewswatch.com

Yelena BarychevPartner, Blank Rome LLP

www.securitiesnewswatch.com

61

Assessing Relevant Risk Factors

• Why do we need risk factors (RFs)?

• Does the SEC require RFs in the PPM?

• What are best practices in RF disclosures?

• What RFs are usually included in the PPM?

62

• Why do we need risk factors (RFs)?

• Does the SEC require RFs in the PPM?

• What are best practices in RF disclosures?

• What RFs are usually included in the PPM?

62

Why Do We Need Risk Factors?

• SEC’s position: to provideimportant context forassessing the company’sfinancial potential (youmay lose all or part ofyour investment)

• Issuer’s position: toprovide protection in caseof investors’ claims

63

• SEC’s position: to provideimportant context forassessing the company’sfinancial potential (youmay lose all or part ofyour investment)

• Issuer’s position: toprovide protection in caseof investors’ claims

63

Does the SEC Require RFs in the PPM?

• No,if the issuer is selling securities to an accredited investor,but the issuer should still including risk factors in the PPM

to:– provide management’s perspective on factors that mayadversely impact the company and its securities– provide information that is material to an understanding ofthe issuer, its business and the securities being offered• Regulation S-K: Item 503(c)

• No,if the issuer is selling securities to an accredited investor,but the issuer should still including risk factors in the PPM

to:– provide management’s perspective on factors that mayadversely impact the company and its securities– provide information that is material to an understanding ofthe issuer, its business and the securities being offered• Regulation S-K: Item 503(c)

64

64

What Are Best Practices in RF Disclosures?• Focus on the most significant or principal RFs that

make the company’s offering of securitiesspeculative or risky

• RF disclosures must be concise and organizedlogically (most significant risks should go first)

• Avoid “boiler plate” RFs:- do not present risks that could apply to any issuer

or any offering- explain how the risk affects the issuer or the

securities being offered

• Use “plain English”

• Set forth each risk factor under a caption thatadequately describes the risk

• The risk factor discussion must be at thebeginning of the PPM

65

• Focus on the most significant or principal RFs thatmake the company’s offering of securitiesspeculative or risky

• RF disclosures must be concise and organizedlogically (most significant risks should go first)

• Avoid “boiler plate” RFs:- do not present risks that could apply to any issuer

or any offering- explain how the risk affects the issuer or the

securities being offered

• Use “plain English”

• Set forth each risk factor under a caption thatadequately describes the risk

• The risk factor discussion must be at thebeginning of the PPM

65

What RFs Are Usually Included in the PPM?

Item 503(c) principles-based disclosure – risk factorsmay include, amongother things, the following:

• the company’s lack of an operating history

• the company’s lack of profitable operations in recent periods

• the company’s financial position

• the company’s business or proposed business

• the lack of a market for the company’s common equity securities orsecurities convertible into or exercisable for common equity securities

Item 503(c) principles-based disclosure – risk factorsmay include, amongother things, the following:

• the company’s lack of an operating history

• the company’s lack of profitable operations in recent periods

• the company’s financial position

• the company’s business or proposed business

• the lack of a market for the company’s common equity securities orsecurities convertible into or exercisable for common equity securities

66

66

What RFs Are Usually Included in the PPM?(cont’d)

• Business risk factors: company and industry RFs – look for sample industry RFs

- Challenges posed by competition- Reliance on current management- Effect of general economic conditions- Regulatory requirements- Seasonality- Reliance on a limited number of customers- Reliance on a few suppliers- Price fluctuations

• Risk factors related to investment in the company’s securities

- Concentration of stock ownership – lack of ability to influence key decisions- Risk of dilution from future rounds of financing or conversion of convertible debt or exercise of

options/warrants- No liquidity- Anti-takeover provisions in the charter or bylaws

• Risk factors related to the terms of the offering

• Business risk factors: company and industry RFs – look for sample industry RFs

- Challenges posed by competition- Reliance on current management- Effect of general economic conditions- Regulatory requirements- Seasonality- Reliance on a limited number of customers- Reliance on a few suppliers- Price fluctuations

• Risk factors related to investment in the company’s securities

- Concentration of stock ownership – lack of ability to influence key decisions- Risk of dilution from future rounds of financing or conversion of convertible debt or exercise of

options/warrants- No liquidity- Anti-takeover provisions in the charter or bylaws

• Risk factors related to the terms of the offering

67

67

Due Diligence

• What is due diligence (DD)?

• Why do we need to conduct DD?

• What types of DD are usually conducted?

• What is due diligence (DD)?

• Why do we need to conduct DD?

• What types of DD are usually conducted?

68

68

What Is Due Diligence?

DD is comprehensiveinvestigation of:

• the company’s business• the company’s financial

position and prospects• major risks facing the

company

69

DD is comprehensiveinvestigation of:

• the company’s business• the company’s financial

position and prospects• major risks facing the

company

69

Why Do We Conduct Due Diligence?

• To develop, or confirm theaccuracy of, the disclosurein the PPM:

- Concerns aboutreputational risk

- Risk of antifraud liabilityunder Rule 10b-5

70

• To develop, or confirm theaccuracy of, the disclosurein the PPM:

- Concerns aboutreputational risk

- Risk of antifraud liabilityunder Rule 10b-5

70

What Types of DD Are Usually Conducted?• Legal DD:

- Corporate structure- Minutes- Organizational documents: charter and bylaws- Material agreements- Stockholder information- Litigation- Regulatory framework

• “Bad actor” DD

• Business DD:

- Production- Competitors- Sales and marketing- R&D- Strategy

• Financial DD

• Legal DD:

- Corporate structure- Minutes- Organizational documents: charter and bylaws- Material agreements- Stockholder information- Litigation- Regulatory framework

• “Bad actor” DD

• Business DD:

- Production- Competitors- Sales and marketing- R&D- Strategy

• Financial DD

71

71

Drafting PPM Is Like Building a Puzzle

72

72