Structuring Financial Covenants, EBITDA, Events of Default ...

35

Structuring Financial Covenants, EBITDA, Events of Default, and MAC Clauses in Loan Documents Maximizing Borrower Protection and Lender Remedies Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1. THURSDAY, JANUARY 21, 2021 Presenting a live 90-minute webinar with interactive Q&A Kristen V. Campana, Partner, Morgan Lewis & Bockius, New York David A. Surbeck, Partner, Holland & Knight, Philadelphia

Transcript of Structuring Financial Covenants, EBITDA, Events of Default ...

Structuring Financial Covenants, EBITDA,

Events of Default, and MAC Clauses in Loan

DocumentsMaximizing Borrower Protection and Lender Remedies

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

THURSDAY, JANUARY 21, 2021

Presenting a live 90-minute webinar with interactive Q&A

Kristen V. Campana, Partner, Morgan Lewis & Bockius, New York

David A. Surbeck, Partner, Holland & Knight, Philadelphia

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-877-447-0294 and enter your Conference ID and PIN when prompted.

Otherwise, please send us a chat or e-mail [email protected]

immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the ‘Full Screen’ symbol located on the bottom

right of the slides. To exit full screen, press the Esc button.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the link to the PDF of the slides for today’s program, which is located to the right of the slides,

just above the Q&A box.

• The PDF will open a separate tab/window. Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Table of Contents

I. Purposes of Financial Covenants

II. Types of Financial Covenants

III. Financial Definitions: Net Income, EBITDA, Fixed Charges

IV. Covenant-Lite Transactions

V. Distinctions between Cash Flow and Asset-Backed Loans

VI. Mandatory Prepayments; Excess Cash Flow

VII. Equity Cure Rights

I. Purpose of Financial Covenants

WHY? Because financial covenants measure the financial health of acompany by utilizing various calculations allowing lenders to monitor theperformance of the business.

They may be tested at all times or during a certain test period (e.g., end of eachfiscal quarter), in order to alert lenders to changes in the business and detect earlywarning sign of distress. Maintenance Covenants

Financial covenants are also used to ensure fiscal discipline by the company whenproposing to take certain actions (e.g., acquisitions, incurrence of incrementalloans, incremental equivalent debt or ratio debt) where the company mustdemonstrate pro forma compliance with such covenants. Incurrence Covenants

Purpose of Financial Covenants

Company Negotiation Point: Maximize FlexibilityMarket volatility or unanticipated lumpiness in cash flow could cause a breach of amaintenance covenants by an otherwise healthy company

Minimize frequency of seeking consent from the lenders for either a waiver offinancial covenants or consent to enter into a transaction

Do not want to be second-guessed by lenders who are financial investors and notoperators of the company as to business decisions.

Financial covenants are typically negotiated off the financial model showing theborrower’s projected performance over the term of the loan. Covenants are set at levelsequal to the projected performance plus or minus a negotiated cushion (25%-35%)that reflects market practice, conditions and company performance expectations.

Financial Covenants and COVID-19

Lenders generally have not sought to exercise rights and remedies resulting frompandemic-triggered events of default. These defaults do provide lenders anaudience with the company to devise a solution.

Solutions:

– Covenant holiday which suspends the company’s required compliance with thefinancial covenants for a period of time. Such covenants may be replaced with aminimum liquidity covenant.

– Modification of covenants by loosening the financial covenant testing levels and/oramending the applicable definitions, to account for adjustments related to the COVID-19 pandemic’s effects including specific EBITDA add-backs for losses or expensesarising from COVID-19.

Financial Covenants and COVID-19

In exchange for relief granted to companies, lenders often request:

a. additional information/reporting to continue to monitor the company,

b. credit support from current equity owners in the form of guarantees, lettersof credit or capital contributions/last out loans, and

c. Lock-down of access to incurrence-based baskets during the relief period.

* Negotiation Point: Fixed period vs. performance-based termination of restrictions

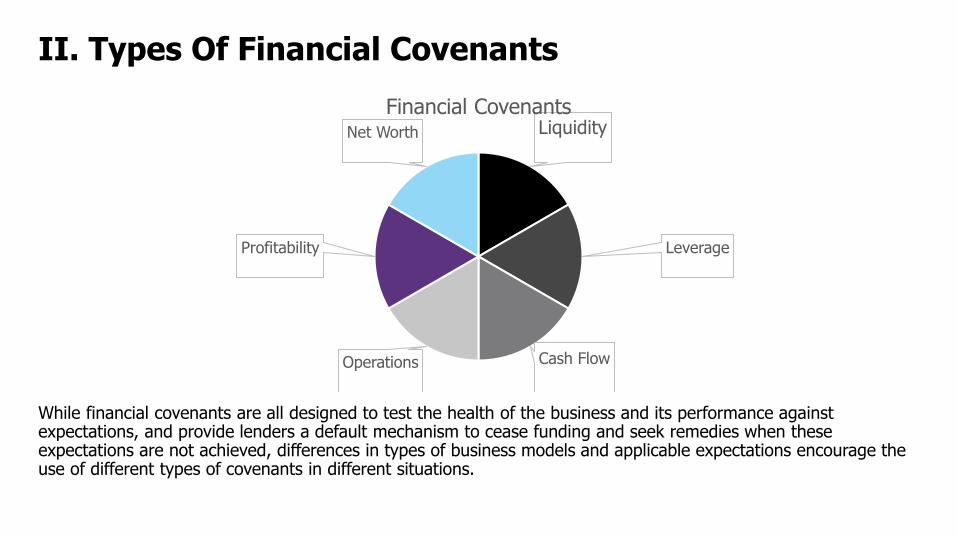

II. Types Of Financial Covenants

While financial covenants are all designed to test the health of the business and its performance against expectations, and provide lenders a default mechanism to cease funding and seek remedies when these expectations are not achieved, differences in types of business models and applicable expectations encourage the use of different types of covenants in different situations.

Liquidity

Leverage

Cash FlowOperations

Profitability

Net Worth

Financial Covenants

Liquidity

Measurements of liquidity look to test available cash and other liquid assets, as reduced by immediate calls on cash.

• Working Capital (i.e. current assets less current liabilities)

• Quick Ratio (i.e. ratio of liquid assets to current liabilities)

• Current Ratio (i.e. ratio of current assets to current liabilities)

• Minimum Liquidity (i.e. amount of liquid assets) Cash to debt (cash to debt)

Example: Current Ratio: The Borrower shall maintain a ratio of Total Current Assets to Total Current Liabilities of not less than [1.0] to 1.0 [at all times]. Total Current Assets means the sum of unrestricted cash and cash equivalents, and notes and accounts receivable not more than [thirty (30)] days past due. Total Current Liabilities means the sum of current maturities of long-term debt, trade accounts payable and ________________.

Leverage

Measurements of leverage look to test the long term health of a Borrower by looking at capacity to service liabilities.

• Debt to Net Worth (i.e. total liabilities to tangible net worth)

• Total Leverage (i.e. funded debt to EBITDA)

• Senior Leverage (i.e. senior funded debt to EBITDA)

• Debt to Book Capital (i.e. funded debt to book capital)

Example: Maximum Total Leverage Ratio: Borrower shall maintain [at all times] a ratio of (a) Funded Debt to (b) EBITDA of not greater than [3.0] to 1.0 measured [monthly, quarterly, annually]. Funded Debt means the sum of all [debt for borrowed money]. EBITDA means the sum of net income, interest expense, taxes, depreciation and amortization.

Cash Flow

Measurements of cash flow look to the Borrower’s current capacity to pay interest, debt and fixed charges when due.

• Interest Coverage (i.e. EBIT to interest expense)

• Debt Service Coverage (i.e. ratio of EBITDA to debt service)

• Fixed Charge Coverage (i.e. ratio of EBITDA to fixed charges)

Example: Minimum Fixed Charge Coverage Ratio: Borrower shall maintain [at all times] a ratio for the [trailing twelve month period] of (a) EBITDAR [minus distributions], to (b) Fixed Charges, of not less than [1.25] to 1.0 measured [monthly, quarterly, annually]. EBITDAR means the sum of net income, interest expense, taxes, depreciation, amortization, lease expense and rent expense. Fixed Charges means the sum of interest expense, scheduled payments of Funded Debt, lease expense and rent expense.

Operating

Measurements of operating covenants follow the performance of various operating measures.

• AR Aging (i.e. average days accounts receivable outstanding)

• AP Aging (i.e. average days accounts payable outstanding)

• Inventory Days on Hand (i.e. inventory on hand to cover x days)

• Cash Days of Hand (i.e. cash on hand available to cover x days anticipated expenses)

Example: Minimum Days Cash on Hand. Unrestricted Cash divided by (Total Operating Expenses minus depreciation) per day of not less than __ days and shall be tested at least [quarterly, annually]. For the purpose of this calculation, Unrestricted Cash means the sum of all unrestricted cash and cash equivalents. Total Operating Expenses means ___________.

Profitability

Measurements of profitability over a selected period set a base line for performance.

• EBITDA (i.e. minimum EBITDA for any period)

• Minimum Net Income (i.e. minimum net income for any period)

Example: Minimum Profits. Borrower shall have profits before taxes of not less than $________ and shall be tested at least [quarterly, annually].

Net Worth

Measurements of net worth set a minimum value for the business as a whole.

• Net Worth (i.e. value of the business)

• Tangible Net Worth (i.e. worth of the tangible assets of the business)

Example: Minimum Tangible Net Worth. Borrower shall maintain a Tangible Net Worth not less than $______ and shall be tested at least [quarterly, annually]. Tangible Net Worth means net worth minus net intangibles (including, but not limited to goodwill, contract rights and distribution rights), and assets representing claims on shareholders and affiliates.

III. Financial Definitions

• Consolidated Net Income: Net income (or loss) of the company determined in accordance with GAAP

Gross Revenue – Direct costs of goods/services – ordinary course adjustments = Gross Operating Profit

Gross Operating Profit – SG&A (selling, general and administrative expenses) = Net Income

Financial Definitions

III. Financial Definitions

Consolidated Net Income is determined by making normalizing adjustments by adding back certain losses and subtracting certain gains:

• Extraordinary/unusual/infrequent non-recurring gains or losses

• Discontinued operations

• Non-ordinary course asset dispositions

• Refinancing, modification or early extinguishment of debt, non-cash effects attributable to market-to-market valuation of swaps

• Unrealized/non-cash gains or losses

• Fees and expenses with respect to certain transactions

Financial Definitions

Consolidated Net Income…more adjustments:

• Write-down from non-cash impairment charges

• Non-cash charges from application of purchase method accounting

• Effect of cumulative changes in accounting principles

• Net Income of Unrestricted Subsidiaries or minority interests or as accounted for bythe equity method of accounting, only to the extent dividends are received in cash;Exclusion of net income of Restricted Subsidiaries if prohibited to declare dividends

• non-cash expenses and gains and losses on interest rate and foreign currencyderivatives and foreign currency transactions

• Long term incentive plan accruals and non-cash compensation expenses from stockoptions/plans

Financial Definitions

EBITDA: Not a GAAP Concept. Measures a company’s cash generating capacity. Negotiations center around calculating the effects of extraordinary events and financial activities.

Earnings (Consolidated Net Income) Before:

– Consolidated Interest Expense (determined in accordance with GAAP)

– Includes interest on debt and under capital leases and certain financing costs incurred in connection with securitization programs

– Calculated after giving effect to net payments made or received and costs incurred in connection with swaps

– Consolidated Tax Expense (on income, profits and loss)

– Consolidated Depreciation Expense (non-cash)

– Consolidated Amortization Expense (non-cash)

Financial Definitions

• EBITDA adjustments without duplication (available to the extent such item reduced/increased CNI and was not already added back/deducted in the definition of CNI):

– Extraordinary, non-recurring, unusual cash items (cap)

– Discontinued operations

– Insurance/indemnification payments (timing of reimbursement)

– Sponsor fees/expenses/indemnification (transaction specific; management fees)

– Non-cash charges including stock-based compensation expenses, unrealized foreign currency gains or losses, non-cash charges attributable to purchase price accounting principles or gain/loss from re-appraisal or write-up/write-down of assets

– Losses attributable to early extinguishment of debt

– Unrealized losses attributable to mark-to-market accounting

– Non-cash expenses or losses that reduce CNI

Financial Definitions

• EBITDA adjustment for one-time events:

– Restructuring charges (cap/requirement of Borrower certification/time limit)

– Cost-savings synergies/revenue synergies, operating expense reductions and integration (pro forma) (cap). May include “Run rate cost savings”: extrapolation of financial results in future periods. Negotiation around:

– Timing: realized/taken, committed or expected to be taken

– Consistent with Regulation S-X: directly attributable to the transaction, factually supportable and expected to have a continuing impact on the income statement

– Borrower certificate of being reasonably identifiable and factually supportable

– Supported by Sponsor Model or QoE

– Transaction specific:

– Cash expenditures for acquisitions (failed acquisition cap)

– Fees and expenses for amendments/modifications of subject loan documentation

– Subject loan transaction/acquisition expenditures as of the closing date and those incurred in the future (time limit and/or cap)

Financial Definitions

Consolidated Fixed Charges

• Fixed charges may include:

– Unfinanced capital expenditures

– Interest Expense paid in cash

– Scheduled principal payments of debt

– Taxes paid in cash

– Payment of Sponsor management fees

– Certain cash dividends and distributions

Financial Definitions

• Definition of Debt: Not a GAAP concept

• As used in leverage covenants, debt is intended to capture debt for borrowed money including from loans, debt securities and L/C reimbursement obligations

• Also captures other financial liabilities:

– Termination value of hedges

– Earn-outs (timing)

– Deferred purchase price of assets

– Principal of capitalized leases and sale/lease back transactions

– Guarantees and obligations of third parties secured by assets of the company

– Payment obligations related to mandatorily redeemable preferred stock

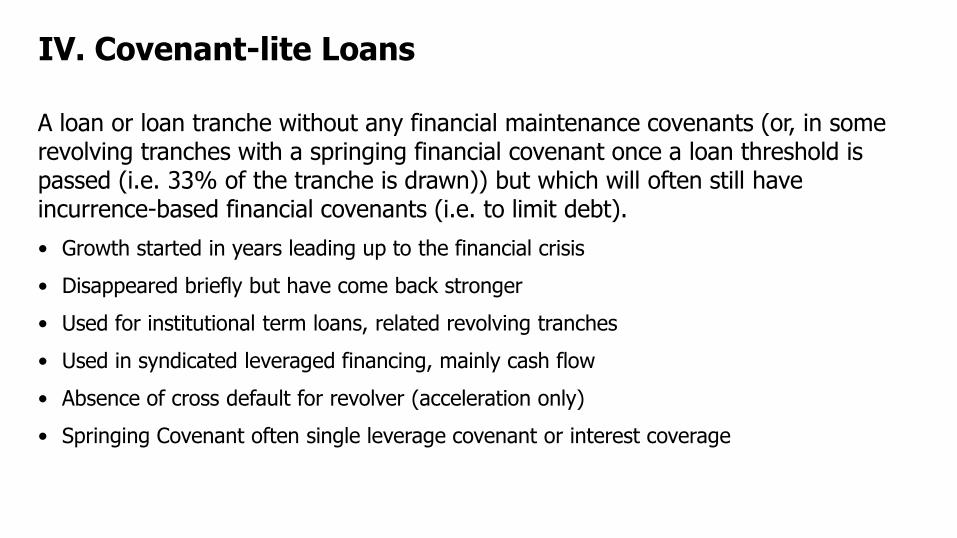

IV. Covenant-lite Loans

A loan or loan tranche without any financial maintenance covenants (or, in some revolving tranches with a springing financial covenant once a loan threshold is passed (i.e. 33% of the tranche is drawn)) but which will often still have incurrence-based financial covenants (i.e. to limit debt).

• Growth started in years leading up to the financial crisis

• Disappeared briefly but have come back stronger

• Used for institutional term loans, related revolving tranches

• Used in syndicated leveraged financing, mainly cash flow

• Absence of cross default for revolver (acceleration only)

• Springing Covenant often single leverage covenant or interest coverage

Covenant-Lite Loans

Benefit to Borrower

• Added flexibility

• Reduce default risk and need to negotiate with lender group

• Reduce risk of loss of ownership or control

Detriment to Lenders

• Delay inevitable (fewer early warnings)

• Undermine enterprise value (additional debt/liens)

• Impair recovery– See https://www.spglobal.com/ratings/en/research/articles/201013-settling-for-less-covenant-lite-loans-have-lower-recoveries-

higher-event-and-pricing-risks-11687612

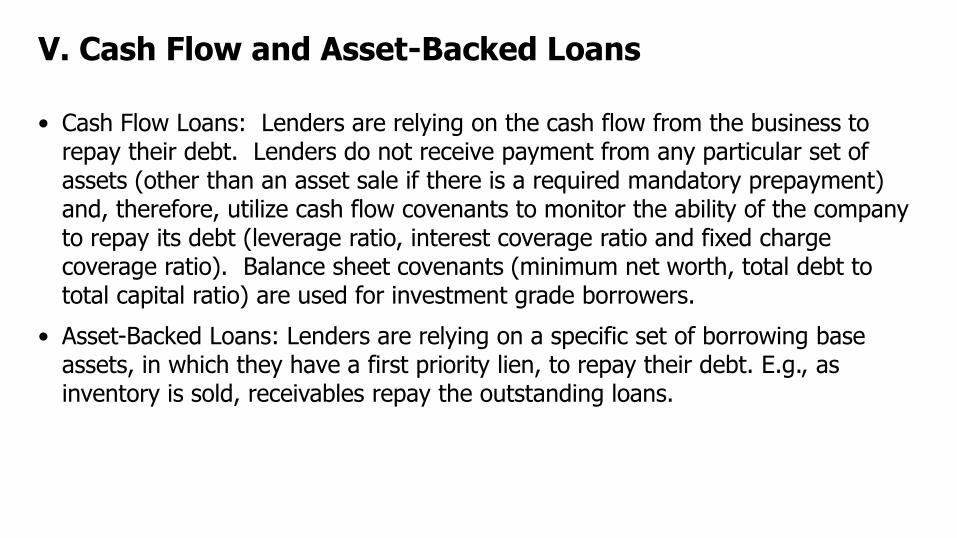

V. Cash Flow and Asset-Backed Loans

• Cash Flow Loans: Lenders are relying on the cash flow from the business to repay their debt. Lenders do not receive payment from any particular set of assets (other than an asset sale if there is a required mandatory prepayment) and, therefore, utilize cash flow covenants to monitor the ability of the company to repay its debt (leverage ratio, interest coverage ratio and fixed charge coverage ratio). Balance sheet covenants (minimum net worth, total debt to total capital ratio) are used for investment grade borrowers.

• Asset-Backed Loans: Lenders are relying on a specific set of borrowing base assets, in which they have a first priority lien, to repay their debt. E.g., as inventory is sold, receivables repay the outstanding loans.

VI. Mandatory Prepayments

• Generally used to pay down senior secured debt

• May be to address specific risk (borrowing base; clean downs; change of control)

• Or to reduce leverage (asset sales and casualty events; debt and equity issuances; ECF)

• Payments made with cash on the company books or net cash proceeds

• Net Cash Proceeds payments may adjust for:

– Agreed portion to be paid from proceeds

– Transaction costs

– Taxes and/or estimated taxes

– Other debt secured by asset

– Negotiated permitted uses of proceeds

Mandatory Prepayments

• Borrowing Base Triggers

• Revolving Clean Downs

• Net Cash Proceeds from:

– Equity Issuances (varied percentages)

– Dependent on initial structure, availability of equity (i.e. not generally applicable for public companies)

– Intent to fund acquisitions and investments

– Equity Cure use

– Asset Sales (typically 100%)

– Out of ordinary course

– Allowance to designate for re-use (absent default and within timeframes)

– Allowance for limited size exclusions (annual/term)

– Debt Incurrence (typically 100%)

– For debt not otherwise permitted (and sometimes general debt baskets)

– Casualty (i.e. insurance proceeds) / Condemnation / Key Man (typically 100%)

– Similar treatment to assets sales (except key man insurance proceeds)

• Change of Control

• Excess Cash Flow Sweeps

Excess Cash Flow (“ECF”) Sweep

• Allows flexibility vs fixed amortization payments

• Intended to capture a portion of annual cash flow to pay down term debt in order to reduce leverage

• Payments required in connection with delivery of annual audit based on cash flow for most recent fiscal year, but may exclude stub periods, which can be complicated to calculate

• Applied to term loans (and sometimes second lien term loans)

• Sweep of 50%, often with step-downs to 25% and 0%

• Step downs based on leverage test (i.e. 3.0x; 2.5x; 2.0x)

• Include reductions for voluntary prepayments of term loans during related fiscal year

• Generally Borrowers look for ways to reduce this number unless there are allowances or builder baskets that incorporate ECF

ECF Sweep

Calculating Cash Flow

• Start with EBITDA or Consolidated Net Income (“CNI”) as an approximation of increased cash for the year.

• In starting with EBITDA, borrowers will want to make sure there are deductions for all non-cash addbacks to EBITDA

• In addition, borrowers will want this amount reduced by various cash expenditures that don’t reduce the EBITDA or CNI calculations, such as for Capital Expenditures

• Further, adjustments will often also be made to reflect changes in Working Capital (i.e. current assets over current liabilities) from the start to the end of the related fiscal year, such that:

– If Working Capital has increased, ECF would be adjusted down, and

– If Working Capital has decreased, ECF would be adjusted up.

ECF Sweep

Negotiated ECF Adjustments

In addition to the above, borrowers may request further reductions from ECF for other expenditures that are not addressed in the EBITDA or CNI calculation, but that they nonetheless anticipate, in order to maintain as much flexibility as possible, including:

• Prepayments of other debt

• Permitted Acquisitions and Investments

• Certain dividends, distributions and other Restricted Payments

• Amounts otherwise coming due after the end of the fiscal year, but before the required payment is to be made.

VII. Equity Cure Rights

Certain financial covenants may be subject to an Equity Cure Right where an equitycontribution may be made to the company to prevent a default.

The cure right is subject to limitations on:

• Type of equity (common vs. preferred), but not Disqualified Equity

• Amount contributed (limited to cure amount)

• The number of times it may be exercised over the life of the loan [5],

• The number of times it may be exercised in a fiscal year and/or four consecutive fiscalquarters [2], and

• If the contribution may be added to EBITDA or if it must be used to pay downoutstanding debt. If added to EBITDA, only added to cure the covenant.

Cure Period: From the end of the applicable fiscal quarter until [10] business days afterthe date the financial statements are required to be delivered.

COVID MAE Considerations

Material Adverse Effect: Lenders have generally permitted modification to MAEdefinitions to carve-out the effects of COVID-19. Sample language follows:

– “…during the period from and including the Amendment Effective Date through and including[March 31, 2021][date the covenant testing suspension ends], the impact of COVID-19 on thefinancial condition, operations, business or properties of the Company and its Subsidiaries,taken as a whole, that occurred and were disclosed to the holders of the Notes on or prior tothe Amendment Effective Date will be disregarded.”

– “; provided that, only from April 27, 2020 until December 31, 2020, the impacts of the COVID-19 pandemic on the business, operations, properties, assets, liabilities or condition (financialor otherwise) of the Loan Parties and their Subsidiaries taken as a whole that were disclosedin writing to the Lenders in the Lender Presentation Materials distributed on April 21, 2020(which included Holdings’ Consolidated First Lien Leverage Ratio covenant projections, aCovenant Forecast and Working Forecast Model) will be disregarded for purposes ofdetermining whether a Material Adverse Effect has occurred.”