Stress Testing: How to Link Scenarios to Risk Drivers

17

Stress Testing - How to link scenarios to risk drivers Dr. JUAN M. LICARI SENIOR DIRECTOR HEAD OF ECONOMIC & CONSUMER CREDIT ANALYTICS – EMEA MOODY’S ANALYTICS

-

Upload

moodys-analytics -

Category

Economy & Finance

-

view

776 -

download

2

Transcript of Stress Testing: How to Link Scenarios to Risk Drivers

Stress Testing - How to link scenarios to risk drivers

Dr. JUAN M. LICARI

SENIOR DIRECTOR

HEAD OF ECONOMIC & CONSUMER CREDIT ANALYTICS – EMEA

MOODY’S ANALYTICS

2 2

Today’s Presenter

2

Dr. Juan Licari - Senior Director - Moody’s Analytics – EMEA

Dr. Juan Licari is a Senior Director at Moody’s Analytics and the head of

the Economics and Consumer Credit Analytics team for EMEA. Dr.

Licari’s team is responsible for generating alternative macroeconomic

forecasts for Europe and for building econometric tools to model credit

risk phenomena. His team is an industry leader in developing and

implementing risk solutions that explicitly connect credit data to the

underlying economic cycle, allowing portfolio managers to plan for

alternative macroeconomic scenarios. These solutions are leveraged into

stress testing and reverse stress testing practices.

3 3

Independent provider of credit rating

opinions and related information for

nearly 100 years

Research, data, software, and related

professional services for financial risk

management

3

About Moody’s Analytics

Moody's Analytics operates independently of the credit ratings activities

of Moody's Investors Service. We do not comment on credit ratings or

potential rating changes, and no opinion or analysis you hear during this

presentation can be assumed to reflect those of the ratings agency.

Leading global provider of credit rating opinions, insight, and tools for credit risk

measurement and management

4 4

Access essential expertise on the economic and consumer credit trends that impact your business and investments

About Economic & Consumer Credit Analytics

Economic,

Consumer Credit,

and Financial Data

Forecasts with

Alternative

Scenarios

Economic Research

Consumer Credit

Analytics

Risk Management, Strategic Planning, Business and Investment Decisions

4

5 5

For more analysis and research on Europe and the

global economy please visit

www.economy.com

5

6 6

» Different methodologies as a response to alternative regulatory

guidelines.

» Stressing risk parameters directly vs. stressing the drivers behind

these risk models.

» Stressing credit migrations: A two stage approach to handle bi-

modal distributions.

» Q&A [email protected]

Agenda

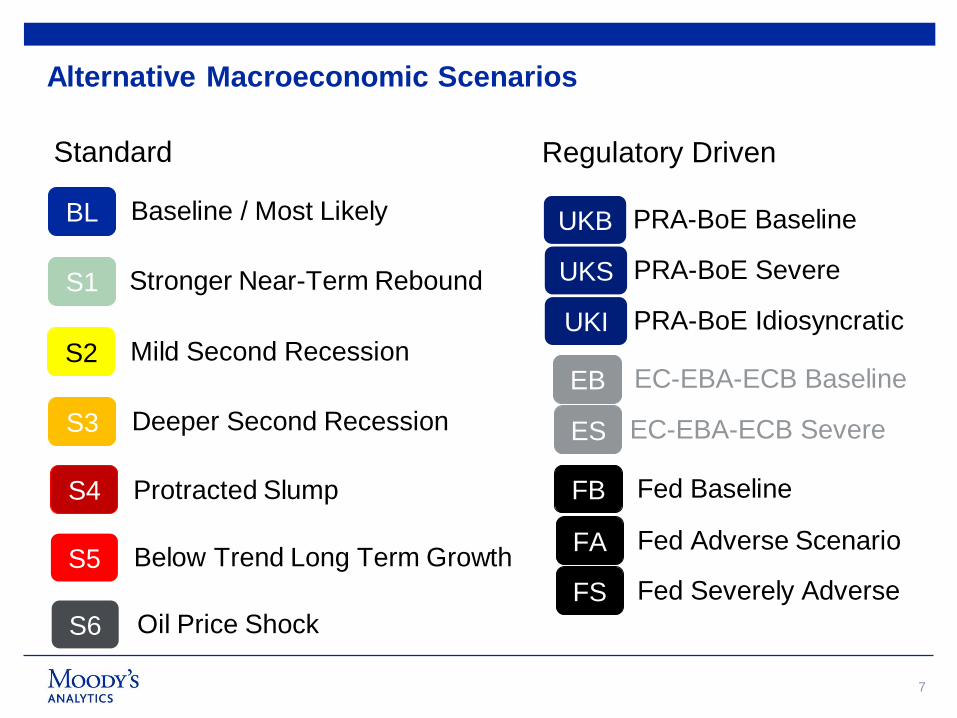

Alternative Macroeconomic Scenarios

7

Stronger Near-Term Rebound S1

S2 Mild Second Recession

S3 Deeper Second Recession

Protracted Slump S4

Baseline / Most Likely BL

Standard

Below Trend Long Term Growth S5

Oil Price Shock S6

Fed Baseline FB

Fed Adverse Scenario FA

EC-EBA-ECB Baseline EB

EC-EBA-ECB Severe ES

Regulatory Driven

PRA-BoE Baseline UKB

Fed Severely Adverse FS

PRA-BoE Severe UKS

PRA-BoE Idiosyncratic UKI

7

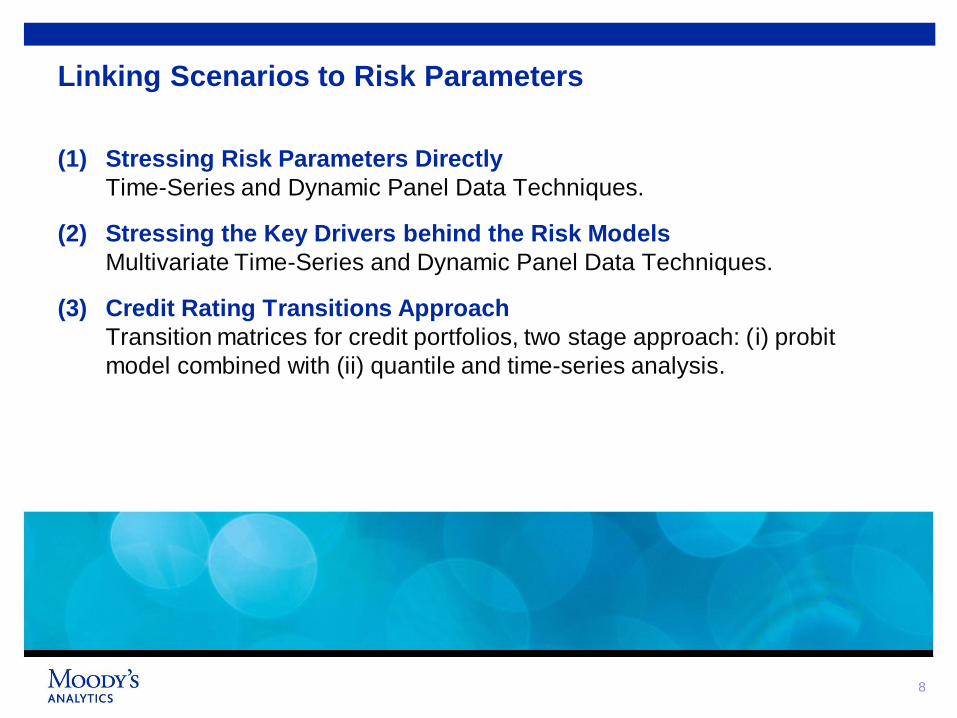

(1) Stressing Risk Parameters Directly

Time-Series and Dynamic Panel Data Techniques.

(2) Stressing the Key Drivers behind the Risk Models

Multivariate Time-Series and Dynamic Panel Data Techniques.

(3) Credit Rating Transitions Approach

Transition matrices for credit portfolios, two stage approach: (i) probit

model combined with (ii) quantile and time-series analysis.

8

Linking Scenarios to Risk Parameters

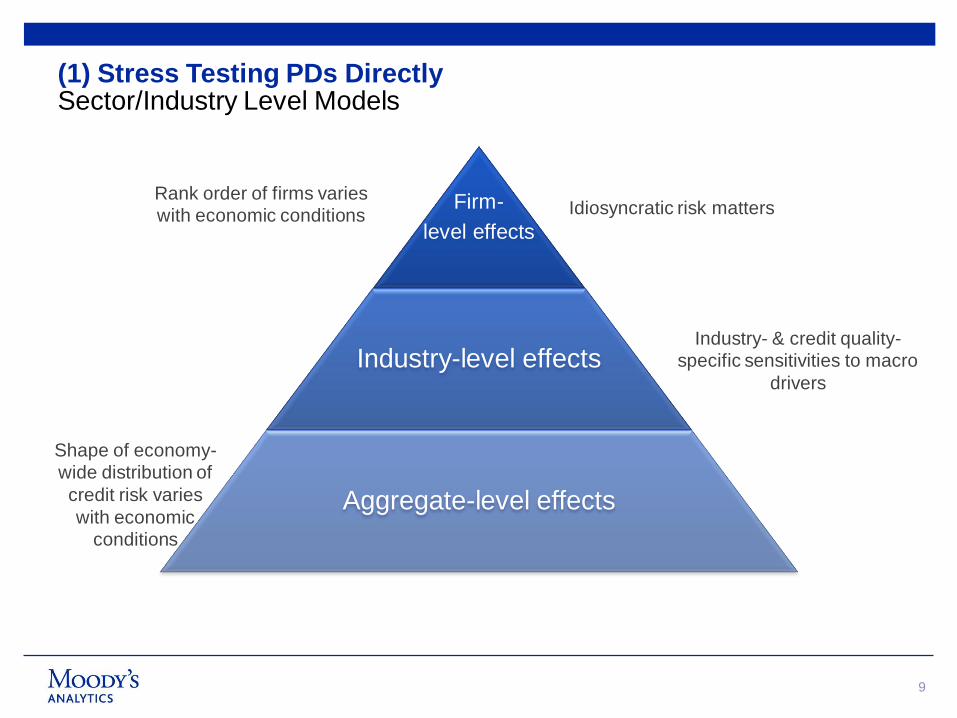

9

Firm-

level effects

Industry-level effects

Aggregate-level effects

Idiosyncratic risk matters

Industry- & credit quality-

specific sensitivities to macro

drivers

Rank order of firms varies

with economic conditions

Shape of economy-

wide distribution of

credit risk varies

with economic

conditions

(1) Stress Testing PDs Directly Sector/Industry Level Models

9

10

10

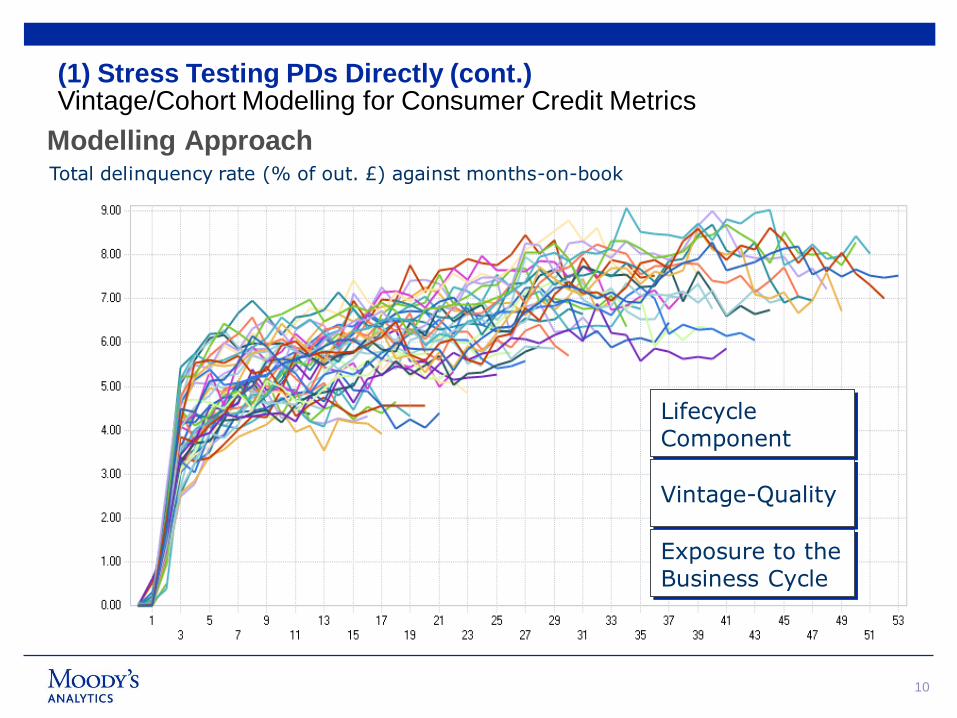

(1) Stress Testing PDs Directly (cont.) Vintage/Cohort Modelling for Consumer Credit Metrics

Modelling Approach

Lifecycle Component

Vintage-Quality

Exposure to the Business Cycle

Total delinquency rate (% of out. £) against months-on-book

Under the S4 scenario GDP growth is

negative…

… which translates into high probabilities

of default

11

EDF (Expected Default Frequency):

Market-driven estimate of the probability that a company will default within the next year

EDF Drivers: (i) Asset Returns, (ii) Asset Volatility and (iii) Default Point

11

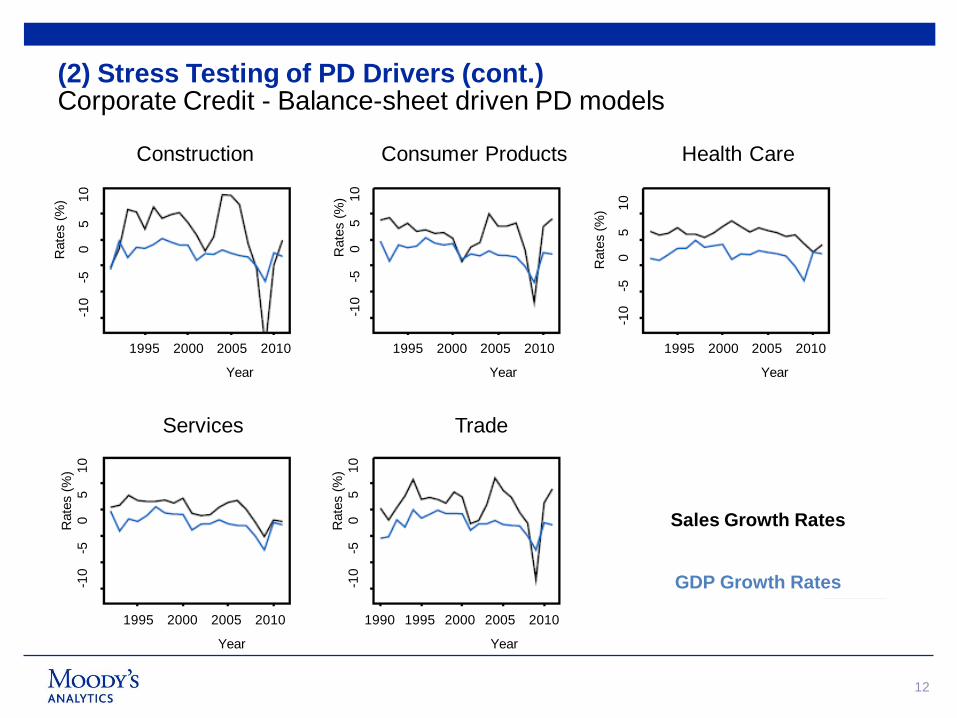

(2) Stress Testing of PD Drivers Corporate Credit - Illustration from option-pricing PD modes

1995 2000 2005 2010

Year

1995 2000 2005 2010

Year

1995 2000 2005 2010

Year

1995 2000 2005 2010

Year

1990 1995 2000 2005 2010

Year

Construction Consumer Products Health Care

Services Trade

Rate

s (

%)

-10

-5

0

5

1

0

R

ate

s (

%)

-1

0 -5

0

5

1

0

R

ate

s (

%)

-10

-5

0

5

1

0

Rate

s (

%)

-10

-5

0

5

1

0

Rate

s (

%)

-10

-5

0

5

1

0

Sales Growth Rates

GDP Growth Rates

12

(2) Stress Testing of PD Drivers (cont.) Corporate Credit - Balance-sheet driven PD models

13

13

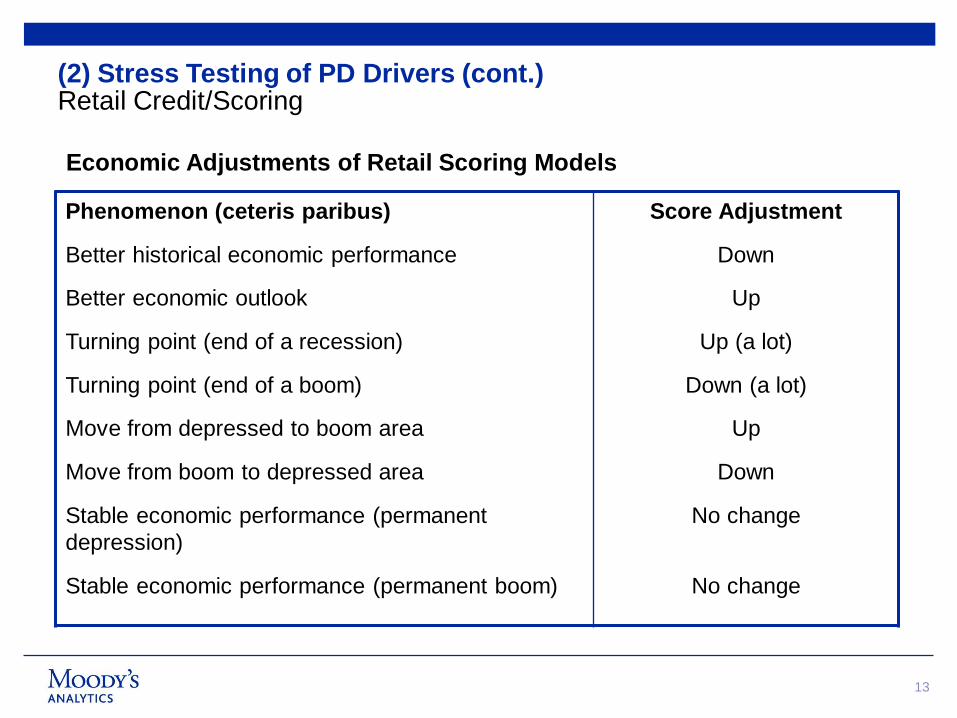

(2) Stress Testing of PD Drivers (cont.) Retail Credit/Scoring

Phenomenon (ceteris paribus)

Better historical economic performance

Better economic outlook

Turning point (end of a recession)

Turning point (end of a boom)

Move from depressed to boom area

Move from boom to depressed area

Stable economic performance (permanent

depression)

Stable economic performance (permanent boom)

Score Adjustment

Down

Up

Up (a lot)

Down (a lot)

Up

Down

No change

No change

Economic Adjustments of Retail Scoring Models

14

Table 1 Average probabilities (1983M1 - 2007M1)

Aaa Aa A Baa Ba B Caa-c Def

Aaa 92.10% 7.52% 0.33% 0.00% 0.04% 0.00% 0.00% 0.00%

Aa 0.99% 90.49% 8.07% 0.37% 0.04% 0.03% 0.00% 0.02%

A 0.07% 2.76% 90.65% 5.67% 0.65% 0.15% 0.03% 0.02%

Baa 0.05% 0.24% 5.51% 87.91% 4.75% 1.14% 0.23% 0.17%

Ba 0.01% 0.07% 0.47% 6.35% 82.56% 8.60% 0.60% 1.33%

B 0.01% 0.05% 0.18% 0.52% 5.52% 82.90% 4.74% 6.08%

Caa-c 0.00% 0.02% 0.10% 1.20% 1.19% 7.12% 69.42% 20.96%

Table 2 Average probabilities (2007M6 - 2009M10)

Aaa Aa A Baa Ba B Caa-c Def

Aaa 78.15% 21.71% 0.04% 0.11% 0.00% 0.00% 0.00% 0.00%

Aa 0.05% 82.65% 16.03% 0.99% 0.11% 0.02% 0.07% 0.09%

A 0.00% 0.88% 89.58% 8.24% 0.44% 0.30% 0.15% 0.41%

Baa 0.01% 0.14% 2.20% 91.95% 4.40% 0.72% 0.20% 0.38%

Ba 0.00% 0.00% 0.04% 5.10% 81.25% 10.46% 1.83% 1.32%

B 0.00% 0.00% 0.07% 0.17% 3.35% 78.31% 13.55% 4.55%

Caa-c 0.00% 0.00% 0.00% 0.14% 0.23% 5.74% 71.19% 22.70%

14

Figure I: Bi-Modal Nature of Credit Transitions Bi-Modal Distribution of Baa to Ba Credit Migrations (Bar Chart) vs. a Normal, Symmetric Distribution (Green Solid Line)

01

02

03

04

0

Den

sity

0 .02 .04 .06 .08 .1baa_ba

(3) Stress Testing of Credit Migrations Example of Global Corporate Credit Transitions

No Change in Policy Collection Policy "A" Collection Policy "B"

% of Cured Accs, 1 month later % of Cured Accs, 1 month later % of Cured Accs, 1 month later

0 96.75% 97.72% 98.70%

1 34.78% 40.86% 44.95%

2 11.97% 13.77% 15.14%

3 6.45% 7.21% 7.93%

4 5.20% 6.13% 6.75%

5 0.40% 0.48% 0.52%

6 0.42% 0.59% 0.65%

Sta

rtin

g s

tatu

s

BASELINE

0 1 2 3 4 5 6 7

0 97.48% 2.35% 0.15% 0.02% 0.00% 0.00% 0.00% 0.00%

1 39.33% 37.87% 22.22% 0.32% 0.03% 0.02% 0.00% 0.20%

2 14.69% 11.23% 28.79% 44.22% 0.39% 0.01% 0.00% 0.67%

3 6.15% 4.34% 5.25% 24.07% 57.57% 0.47% 0.03% 2.12%

4 3.06% 0.64% 1.22% 3.05% 21.51% 68.08% 0.14% 2.29%

5 1.43% 0.73% 1.04% 0.58% 3.03% 18.07% 72.52% 2.62%

6 0.50% 0.22% 0.02% 0.13% 0.08% 1.71% 9.34% 88.00%

Status 1 month later

Sta

rtin

g s

tatu

s

STRESSED

0 1 2 3 4 5 6 7

0 96.75% 3.03% 0.19% 0.03% 0.00% 0.00% 0.00% 0.00%

1 28.57% 40.17% 30.44% 0.44% 0.05% 0.03% 0.00% 0.30%

2 9.63% 7.38% 27.39% 54.28% 0.47% 0.01% 0.00% 0.83%

3 3.72% 2.61% 3.19% 21.46% 65.94% 0.54% 0.03% 2.50%

4 1.73% 0.37% 0.71% 1.77% 18.25% 74.44% 0.15% 2.58%

5 0.85% 0.43% 0.63% 0.34% 1.76% 15.04% 78.12% 2.84%

6 0.28% 0.12% 0.01% 0.07% 0.04% 0.94% 7.47% 91.06%

Status 1 month later

Sta

rtin

g s

tatu

s

15

(3) Stress Testing of Credit Migrations (cont.) Retail Credit Transitions

15

16 16

Q&A Session

Please use the chat function to ask questions

After the webinar please send your questions to:

Join Us for the next webinar in our Stress Testing Webinars

• Stress Testing – Making it Part of Risk Management Best Practice

Eric Leman discusses the advantages of a dedicated framework for

enterprise-wide model consolidation and storage.

>>Monday May 12, 2014; Time: 9:30 - 10:00 AM GMT (London)

To Register, please email: [email protected]

17 17

www.economy.com

United States

121 North Walnut Street

Suite 500

West Chester PA 19380

+1.610.235.5299

Australia

Level 10

1 O'Connell Street

Sydney, NSW, 2000

Australia

+61.2.9270.8111

United Kingdom

One Canada Square

Canary Wharf

London E14 5FA

+44.20.7772.5454

Prague

Washingtonova 17

110 00 Prague 1

Czech Republic

+420.22.422.2929