Strawberry Marketing- Problems and...

45

141 Chapter Four: Strawberry Marketing- Problems and Prospects 4.1. A Glance on Strawberry Marketing Marketing of strawberry is one of the divers among the other cultivates fruits. In beginning of winter season it is the first fruit, which available in market therefore it get best market rate. Demand for strawberry in market hikes day by day on account of its taste and nutrition contents. Strawberry fruit demands in cosmetics, medicine, and food processing sectors along with consumption. It’s international demand also in rise. Strawberry from these locations reaches in local market as well as APMC Mumbai, Pune, Banglore, Hydrabad and other famous cities all over in India. Export of strawberry in 2007 for Europe also done from Mahabaleshwar. But perishable nature of fruit cannot stand long time and not target the far market. Cultivator concentrates while in marketing process on the following operations. 4.1.1. Harvesting Clipping of strawberry fruits getting starts in mid November in Mahabaleshwar region and in October 1 st week in other tahsil’s. This fruit need not any special practice to ripe like Mango, Banana etc. because it can easily available in market after clipping from farm. After the natural improvement in plant, plant start to continue flowering and fruiting up to its life span. Cultivators therefore need to ready for every day harvesting. Mid November to mid June about seven months period seems to yield tenure in Mahabaleshwar region. In other tahsil’s it seems from October to March end or mid April. In which November to March is accessible to higher yield, after and before main period we able to attain only least yield. Proper stage for clipping fruits are depends upon cultivars variety

Transcript of Strawberry Marketing- Problems and...

141

Chapter Four:

Strawberry Marketing- Problems and Prospects

4.1. A Glance on Strawberry Marketing

Marketing of strawberry is one of the divers among the other cultivates

fruits. In beginning of winter season it is the first fruit, which available in

market therefore it get best market rate. Demand for strawberry in market

hikes day by day on account of its taste and nutrition contents. Strawberry

fruit demands in cosmetics, medicine, and food processing sectors along

with consumption. It’s international demand also in rise. Strawberry from

these locations reaches in local market as well as APMC Mumbai, Pune,

Banglore, Hydrabad and other famous cities all over in India. Export of

strawberry in 2007 for Europe also done from Mahabaleshwar. But

perishable nature of fruit cannot stand long time and not target the far

market. Cultivator concentrates while in marketing process on the

following operations.

4.1.1. Harvesting

Clipping of strawberry fruits getting starts in mid November in

Mahabaleshwar region and in October 1st week in other tahsil’s. This fruit

need not any special practice to ripe like Mango, Banana etc. because it

can easily available in market after clipping from farm. After the natural

improvement in plant, plant start to continue flowering and fruiting up to

its life span. Cultivators therefore need to ready for every day harvesting.

Mid November to mid June about seven months period seems to yield

tenure in Mahabaleshwar region. In other tahsil’s it seems from October

to March end or mid April. In which November to March is accessible to

higher yield, after and before main period we able to attain only least

yield. Proper stage for clipping fruits are depends upon cultivars variety

142

and distance between markets to farm. Mostly ¾ ripen fruits picks for

fresh sells in market because they can stand long time. Fully ripe fruit

collects for processing because they can’t endure long time. Fruit stems

cuts at proper distance from calyx. This stems plucks by thumbs and fruit

carries inside the palm.

4.1.2. Handling and Grading

Strawberry fruits gentle feature urge us to handle it in minimum time.

Every touch of hands forwards it towards to spoil. Spotted and nipped by

birds and other pests frits are apart separately while picking. Fruit grading

determines on fruit size. Large size considered in 1st, medium size

considered in 2nd, small size considered in 3rd grade. These three grades

are follows by All India Strawberry Growers Association, New Delhi

fruit grading management. Generally 1st and 2nd grades prefer to sells in

market and 3rd graded mainly use in processing. A fruit separates as per

grade while collects it in bamboo baskets while plucking. Stems and

calyx should be left on fruits for long staying but its clears in case of use

in processing unit.

4.1.3. Packaging

“Pan” and Thick paper box use to packing. Pan consists of eight plastic

rectangular shape jars. These jars mount inside the plastic tray, this

plastic tray keep inside the pan box cover. Approximate 250 gm fruits can

easily packs in one tray of pan. About 350 gm fruits can carriers into

paper box. Layer of leaves scatters inside the box while fruit packing.

Then fruit mounts closely near to each other. Before taping the box again

leaves layer put on the fruits. Jars laden have four holes on the top and

two holes on each left and right side on box maintains for ventilation.

This attractive packing of strawberry fruit allures its eaters.

143

4.1.4. Available Markets for Strawberry Marketing

There is not historical presence of this fruit in nationwide market. Most of

the consumers in our markets are unaware about this fruits. Most of the

consumers seem that, this is elite class fruit. Beside this the cultivation of

strawberry has been taking place since last some decades in

Mahabaleshwar not enough to create its nationwide awareness solely.

Therefore the markets are limited for its marketing. The produce of this

fruit can be sell in local market, APMC Mumbai, and other cities in

different states through the contract agents. Beside this the cultivators in

Mahabaleshwar tahsil are selling their produce in local market as well as

in other nearest cities without any intermediate. They himself take part it

produce marketing that’s why this is also one kind of marketing source of

this strawberry fruit. We in briefly focus on these markets.

4.1.4.1. Local Market -

Visitors enjoying Mahabaleshwar – Panchagani trips in millions of

number every year therefore restaurants, ice- cream parlors and juice

centers are in flourish. These firms demands fruits for different recipes

abstract from strawberry, which are well demanded by visitors. Beside

this some processing units are situated near by this area demand

strawberry fruits for processing and forming new recipes. These firms

directly keep in touch with cultivators and give its return in daily basis.

Fresh strawberry fruit always prefer to taste while roaming in

Mahabaleshwar – Panchgani market by visitors. These visitors’s

requirement fulfills by “Kawadwala”. Kawadwala take part in sells

procedure of strawberry fruit. They formulate fruit heaps in small

bamboo basket. This attractive heap allures customers. Kawadwala sales

fruit in kilogram and Shares measures to customers. There in one

144

praiseworthy things about the Kawadwala is this, they have originate

“Strawberry Kawad Sanghatan – Mahabaleshwar” in 2004.

Cultivators prefer to sales their some specific share of yield in local

market due to easy access and need not any good practice for handle. Its

returns are unrevealing but gets quickly in local market, which helps

cultivator to complete its daily needs. The underlying thing is that in

whole marketing mechanism he himself not taking part.

4.1.4.2. APMC Mumbai (Vashi)

Many cultivators from these tahsil's send their produce in to Agricultural

Produce Marketing Committee at Vashi (Mumbai) through the local

transport. They pack the produce in ½ kg. box and sends to selected

agents for marketing. These agents give them their final statement of

every delivery.

4.1.4.3. Contract Agents

Some specific cultivators attached with this market mechanism. Agents

belongs to different cities desire to buy goods from cultivators and

distribute it in seller in their local cities. Cultivators use pan in large scale

for packing goods. Pan abides together in thick paper and sends by S T

bus, private vehicle, and tourist bus to reach destination. All expenses are

born in transport practice carries by agents. Price for goods determines

for whole year and this is flat price. Though there are oscillations in price

levels in throughout year he pays flat rate price. This trade prefer by

cultivators because they do not need to search any other market source for

goods.

4.1.4.4. Self Marketing

This is noteworthy thing in strawberry marketing that’s cultivator himself

take part into the marketing of self grown fruit. These cultivators sell

their fruits directly to customers in local market as well as on the road

145

links to Mahabaleshwar from Pune, Mumbai and other cities by

becoming Kawadwalla. Similarly some the enthusiastic cultivators in

Mahabaleshwar region show their spontaneous efforts to sell this produce

outside of local market. These cultivators sell their produce in nearest

famous cities in nearby district i.e. Satara, Raigad, Ratnagiri, Pune etc.

Cultivators himself take part into the whole marketing mechanism and he

solely establish relation with customers without any intermediary.

According to these cultivators, this marketing method is convenient and

trustful from our angle. We accustomed to this system of marketing with

understanding the everyday changes and responses by market and

customers.

4.1.5. Expenses in Marketing

Marketing of produce involve some expenditure i.e. transport, packing,

weighing, commission and some other cost. The expenditure pattern is

varying from market to market and somewhat differ in degree also. There

is also crux that who is bearing the marketing expenditure.

4.1.6. Marketing Returns

Here is the final stage of his Hercules efforts. Cultivators rewarded by

appropriate price for his produce. He receives his returns on different

term basis and different mode of payment.

4.2. Study of Marketing Mechanism

4.2.1. Period of Fruit Harvesting

Strawberry fruits are gentle in nature. Usually fruits can be last for very

short period after ripe viz. two or three days. It is highly perishable that’s

why cultivators can’t wait until market response. Strawberry plants once

started to flowering then keep flowering continuously so the fruits too.

That’s why cultivators requires to cut the ripen fruits continuously. Some

146

of the cultivators who have much area under the strawberry cultivation

they have been plucking the fruits from plant one day later. There are

23.68% cultivators need to do daily fruit picking operation. Remaining

76.32 % cultivators cut the fruits every 2nd day in whole season. This is

also depending upon the markets. Those cultivators who send their

produce to other than domestic markets in bulk quantity do cut fruits

every one day later.

4.2.2. Categorization of Fruits

All cultivators have a good awareness of categorization of their produce

to fetch attractive price in market. Every cultivator categorizes the fruits

according to the standard of size. This standard is based on fruit size and

has set by All India Strawberry Growers Association as earlier

mentioned.

4.2.3. Packing of the Fruits

Cultivators require packing of fruits in boxes and Pan (plastic tray) to

avoid wastage while transporting and facilitate in marketing. 82.33%

famers need of packing the strawberry fruits whereas 17.67 cultivators

don’t need to packing produce for any specific purpose. Without packing

produce sells in domestic markets by cultivators to local Kawadwalla

that’s why they free from this troublesome work.

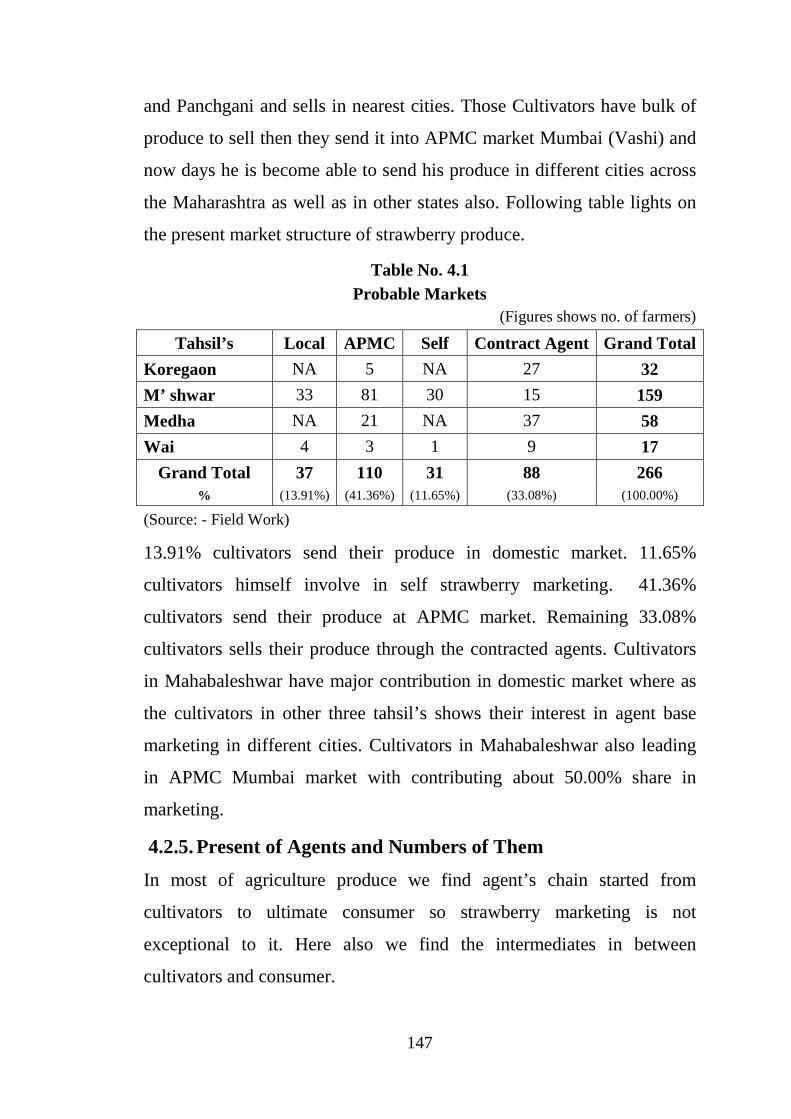

4.2.4. Probable Markets for Strawberry Fruits

A strawberry cultivator has not more option available since he has been

cultivating and marketing of this fruit. He has been following the tradition

ways of marketing which was been since some decade ago. He can sell

his produce at domestic market to kawadwalas, hotels – restaurant in

Mahabaleshwar and Panchgani, Ice cream parlors etc. Besides he can sell

his produce in Mahabaleshwar and Panchgani local market where market

always throng with tourist as well as on the way roads of Mahabaleshwar

147

and Panchgani and sells in nearest cities. Those Cultivators have bulk of

produce to sell then they send it into APMC market Mumbai (Vashi) and

now days he is become able to send his produce in different cities across

the Maharashtra as well as in other states also. Following table lights on

the present market structure of strawberry produce.

Table No. 4.1 Probable Markets

(Figures shows no. of farmers)

Tahsil’s Local APMC Self Contract Agent Grand Total

Koregaon NA 5 NA 27 32

M’ shwar 33 81 30 15 159

Medha NA 21 NA 37 58

Wai 4 3 1 9 17

Grand Total 37 110 31 88 266 % (13.91%) (41.36%) (11.65%) (33.08%) (100.00%)

(Source: - Field Work)

13.91% cultivators send their produce in domestic market. 11.65%

cultivators himself involve in self strawberry marketing. 41.36%

cultivators send their produce at APMC market. Remaining 33.08%

cultivators sells their produce through the contracted agents. Cultivators

in Mahabaleshwar have major contribution in domestic market where as

the cultivators in other three tahsil’s shows their interest in agent base

marketing in different cities. Cultivators in Mahabaleshwar also leading

in APMC Mumbai market with contributing about 50.00% share in

marketing.

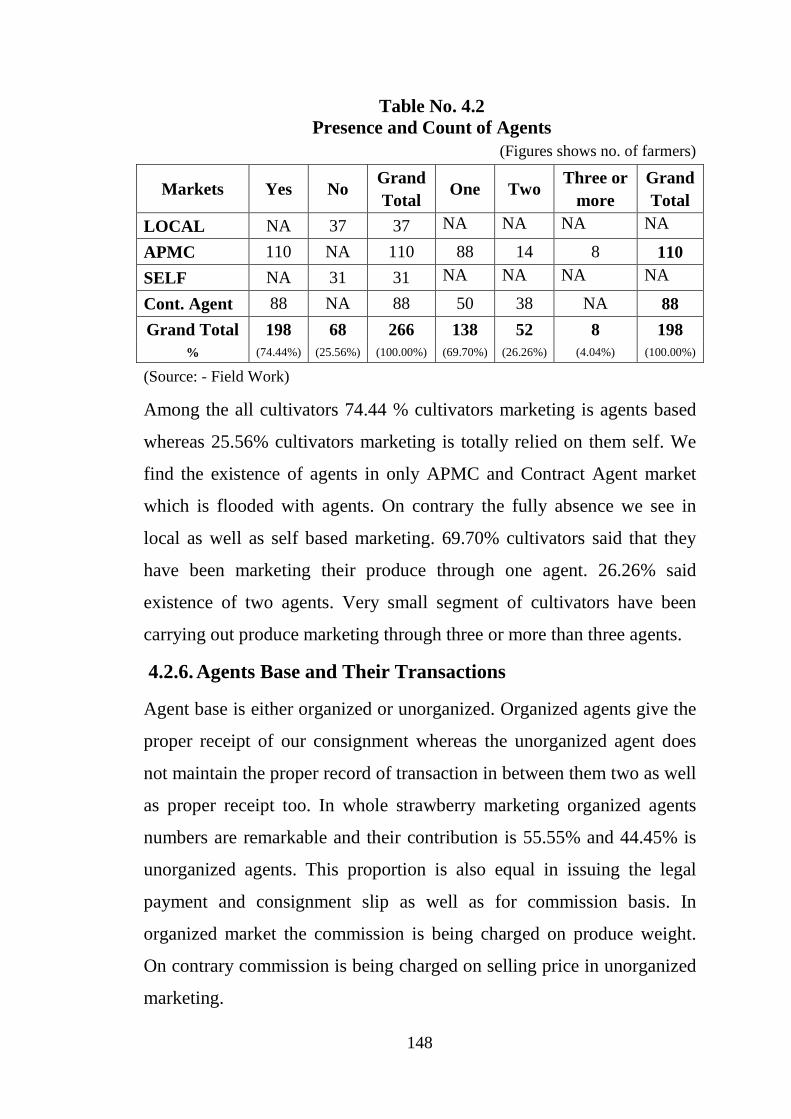

4.2.5. Present of Agents and Numbers of Them

In most of agriculture produce we find agent’s chain started from

cultivators to ultimate consumer so strawberry marketing is not

exceptional to it. Here also we find the intermediates in between

cultivators and consumer.

148

Table No. 4.2 Presence and Count of Agents

(Figures shows no. of farmers)

Markets Yes No Grand Total

One Two Three or

more Grand Total

LOCAL NA 37 37 NA NA NA NA

APMC 110 NA 110 88 14 8 110

SELF NA 31 31 NA NA NA NA

Cont. Agent 88 NA 88 50 38 NA 88

Grand Total 198 68 266 138 52 8 198 % (74.44%) (25.56%) (100.00%) (69.70%) (26.26%) (4.04%) (100.00%)

(Source: - Field Work)

Among the all cultivators 74.44 % cultivators marketing is agents based

whereas 25.56% cultivators marketing is totally relied on them self. We

find the existence of agents in only APMC and Contract Agent market

which is flooded with agents. On contrary the fully absence we see in

local as well as self based marketing. 69.70% cultivators said that they

have been marketing their produce through one agent. 26.26% said

existence of two agents. Very small segment of cultivators have been

carrying out produce marketing through three or more than three agents.

4.2.6. Agents Base and Their Transactions

Agent base is either organized or unorganized. Organized agents give the

proper receipt of our consignment whereas the unorganized agent does

not maintain the proper record of transaction in between them two as well

as proper receipt too. In whole strawberry marketing organized agents

numbers are remarkable and their contribution is 55.55% and 44.45% is

unorganized agents. This proportion is also equal in issuing the legal

payment and consignment slip as well as for commission basis. In

organized market the commission is being charged on produce weight.

On contrary commission is being charged on selling price in unorganized

marketing.

149

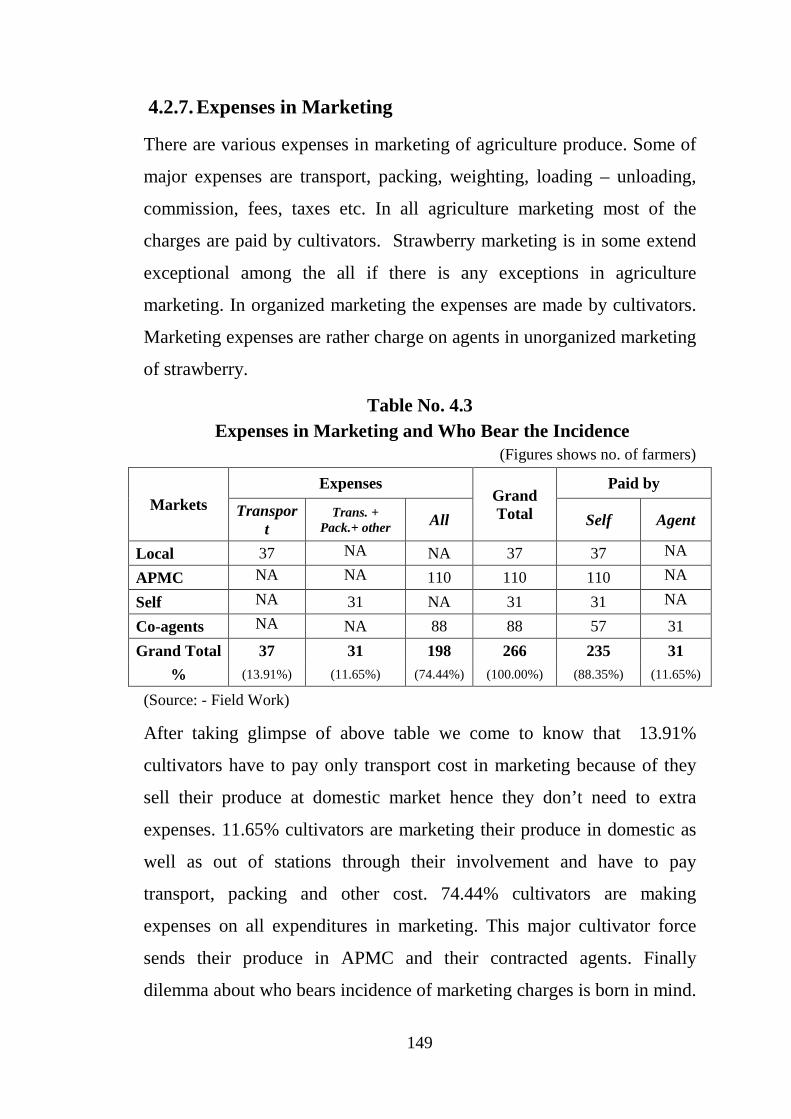

4.2.7. Expenses in Marketing

There are various expenses in marketing of agriculture produce. Some of

major expenses are transport, packing, weighting, loading – unloading,

commission, fees, taxes etc. In all agriculture marketing most of the

charges are paid by cultivators. Strawberry marketing is in some extend

exceptional among the all if there is any exceptions in agriculture

marketing. In organized marketing the expenses are made by cultivators.

Marketing expenses are rather charge on agents in unorganized marketing

of strawberry.

Table No. 4.3 Expenses in Marketing and Who Bear the Incidence

(Figures shows no. of farmers)

Markets Expenses

Grand Total

Paid by

Transport

Trans. + Pack.+ other All Self Agent

Local 37 NA NA 37 37 NA

APMC NA NA 110 110 110 NA

Self NA 31 NA 31 31 NA

Co-agents NA NA 88 88 57 31

Grand Total 37 31 198 266 235 31

% (13.91%) (11.65%) (74.44%) (100.00%) (88.35%) (11.65%)

(Source: - Field Work)

After taking glimpse of above table we come to know that 13.91%

cultivators have to pay only transport cost in marketing because of they

sell their produce at domestic market hence they don’t need to extra

expenses. 11.65% cultivators are marketing their produce in domestic as

well as out of stations through their involvement and have to pay

transport, packing and other cost. 74.44% cultivators are making

expenses on all expenditures in marketing. This major cultivator force

sends their produce in APMC and their contracted agents. Finally

dilemma about who bears incidence of marketing charges is born in mind.

150

88.35% cultivators are responsible to weighing this marketing

expenditure cost. Other 11.65% cultivators are may be lucky from this

point of view. The agents on behalf of cultivators lift burden of

marketing. These are the lucky once among the cultivators who

marketing their produce through their contract agents.

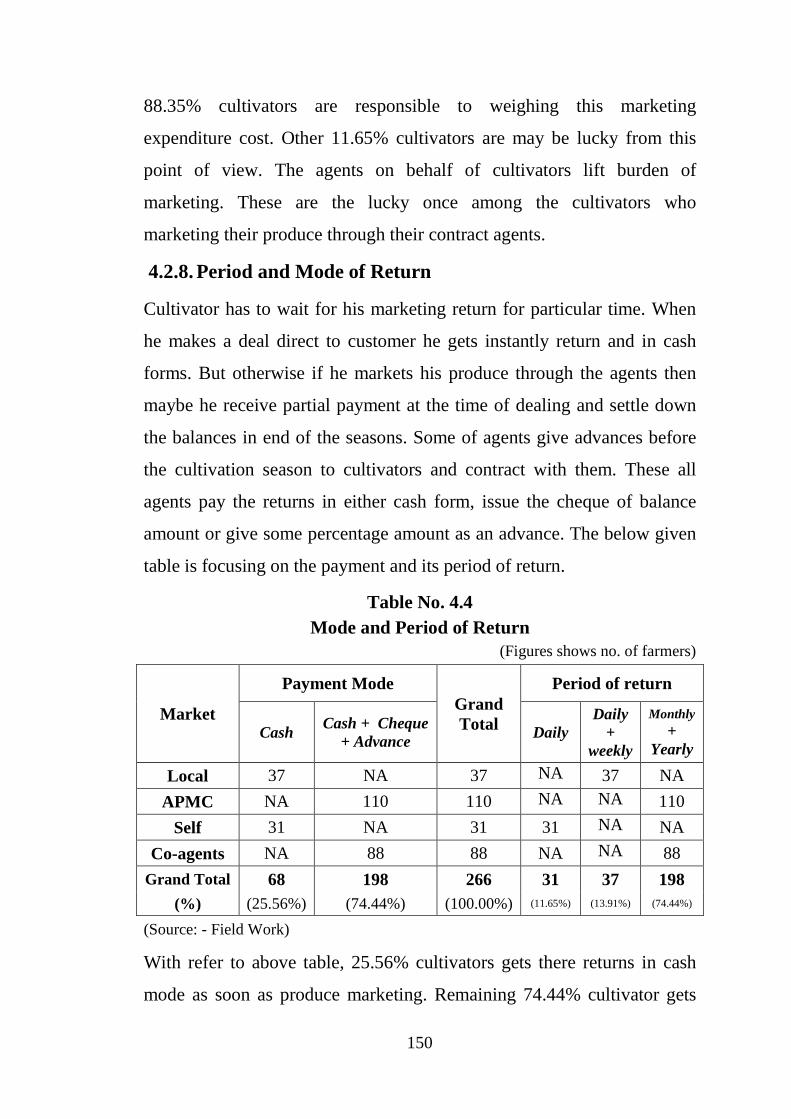

4.2.8. Period and Mode of Return

Cultivator has to wait for his marketing return for particular time. When

he makes a deal direct to customer he gets instantly return and in cash

forms. But otherwise if he markets his produce through the agents then

maybe he receive partial payment at the time of dealing and settle down

the balances in end of the seasons. Some of agents give advances before

the cultivation season to cultivators and contract with them. These all

agents pay the returns in either cash form, issue the cheque of balance

amount or give some percentage amount as an advance. The below given

table is focusing on the payment and its period of return.

Table No. 4.4 Mode and Period of Return

(Figures shows no. of farmers)

Market

Payment Mode Grand Total

Period of return

Cash Cash + Cheque

+ Advance Daily

Daily +

weekly

Monthly +

Yearly

Local 37 NA 37 NA 37 NA

APMC NA 110 110 NA NA 110

Self 31 NA 31 31 NA NA

Co-agents NA 88 88 NA NA 88

Grand Total 68 198 266 31 37 198 (%) (25.56%) (74.44%) (100.00%) (11.65%) (13.91%) (74.44%)

(Source: - Field Work)

With refer to above table, 25.56% cultivators gets there returns in cash

mode as soon as produce marketing. Remaining 74.44% cultivator gets

151

their return in three different ways viz. as an advance before season, cash

amount in mid season and finally they cleared in some proportionate

balance in cash and some in cheque mode.

This table no. 4.4 is also relevance to period of returns from marketing

of produce. 11.65% cultivators say’s that, they get as soon as returns

when they markets their produce because of they are participating this

market. 13.91% cultivator gets theirs returns on daily basis as well as on

weekly basis. These cultivators are mainly associated with local market

and local Kawadwalas. 74.44% are those cultivators who get their returns

on monthly and yearly basis. Because of their links are with the agents

situated in APMC and other unorganized agents in other cities.

4.2.9. Transport Facilities

The role of transport is inevitable in marketing procedure compare to

cultivation operations. Cultivators who send their produce at APMC need

only transport means to convey the produce up to its destination. But

transport facilities and adequate means are reached at the door step of

cultivators hence he doesn’t think anything lag in this system. The

contract agents also collect the produce from their centre point by their

own vehicle so cultivator duty is transport the produce up to that center

point so he also doesn’t wish any from this improvement point of view.

Some of cultivators send their produce at different cities across

Maharashtra and out of Maharashtra by bus and train. There is enough

and good frequency of S.T. buses for famous cities in Maharashtra from

Mahabaleshwar so that cultivators can easily dispatch produce. Similarly

Wathar (Dist. Satara) and Veer (Dist. Raigad) are two nearest railway

station to dispatch the produce by train in selected cities in other states.

152

4.2.10. Cold Storage Facility

It is a very gentle and highly perishable fruit. Many times cultivators as

well as kawadwalas in local market unable to sell whole produce every

day because of tourist frequency is less in week days. In this sense they

are expecting this kind of facility at least at local level markets. But there

is not enough endeavors by both cultivators and associate agency or

department of government. Finally they sell their surplus of produce to

processing units in mid and peak season to stop the ruins of produce.

4.2.11. Marketing Guidance

Today’s cultivators have good accessibility of information technology

and means so he does not need a particular person or agency as a

marketing guidance. These cultivators have good business

communication within them so they share the ups and down in all

markets. They come into connection with any agents in marketing

procedure on collective basis that’s why any ignorance among them can

be easily accommodated. But it is not applicable to all. Except this there

is no certain agency, institution, person to guide them on marketing and

they initiate in this light.

4.2.12. Difficulties in Marketing

While marketing their produce cultivators faces several of difficulties

relevance to i.e. price, demand, gluts in markets etc. whenever cultivator

assign his land for every agricultural produce he keeps his one eye on

cultivation season and another on the price will he get in market. When

the cultivator striving for marketing his produce he also face the

difficulties in somewhat extend like other agriculture produce. Following

table is an eye witness of difficulties arises in market and degree of faces

by cultivators.

153

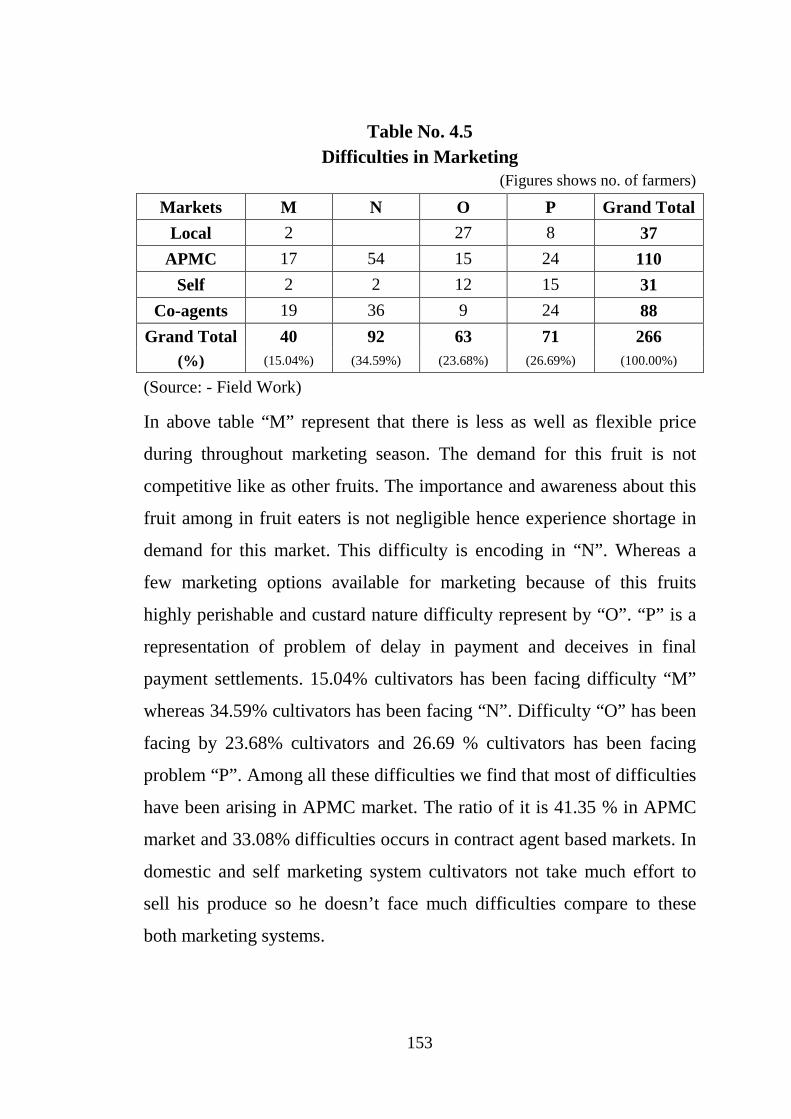

Table No. 4.5

Difficulties in Marketing (Figures shows no. of farmers)

Markets M N O P Grand Total

Local 2

27 8 37

APMC 17 54 15 24 110

Self 2 2 12 15 31

Co-agents 19 36 9 24 88

Grand Total 40 92 63 71 266 (%) (15.04%) (34.59%) (23.68%) (26.69%) (100.00%)

(Source: - Field Work)

In above table “M” represent that there is less as well as flexible price

during throughout marketing season. The demand for this fruit is not

competitive like as other fruits. The importance and awareness about this

fruit among in fruit eaters is not negligible hence experience shortage in

demand for this market. This difficulty is encoding in “N”. Whereas a

few marketing options available for marketing because of this fruits

highly perishable and custard nature difficulty represent by “O”. “P” is a

representation of problem of delay in payment and deceives in final

payment settlements. 15.04% cultivators has been facing difficulty “M”

whereas 34.59% cultivators has been facing “N”. Difficulty “O” has been

facing by 23.68% cultivators and 26.69 % cultivators has been facing

problem “P”. Among all these difficulties we find that most of difficulties

have been arising in APMC market. The ratio of it is 41.35 % in APMC

market and 33.08% difficulties occurs in contract agent based markets. In

domestic and self marketing system cultivators not take much effort to

sell his produce so he doesn’t face much difficulties compare to these

both marketing systems.

154

4.3. Critical study of Marketing

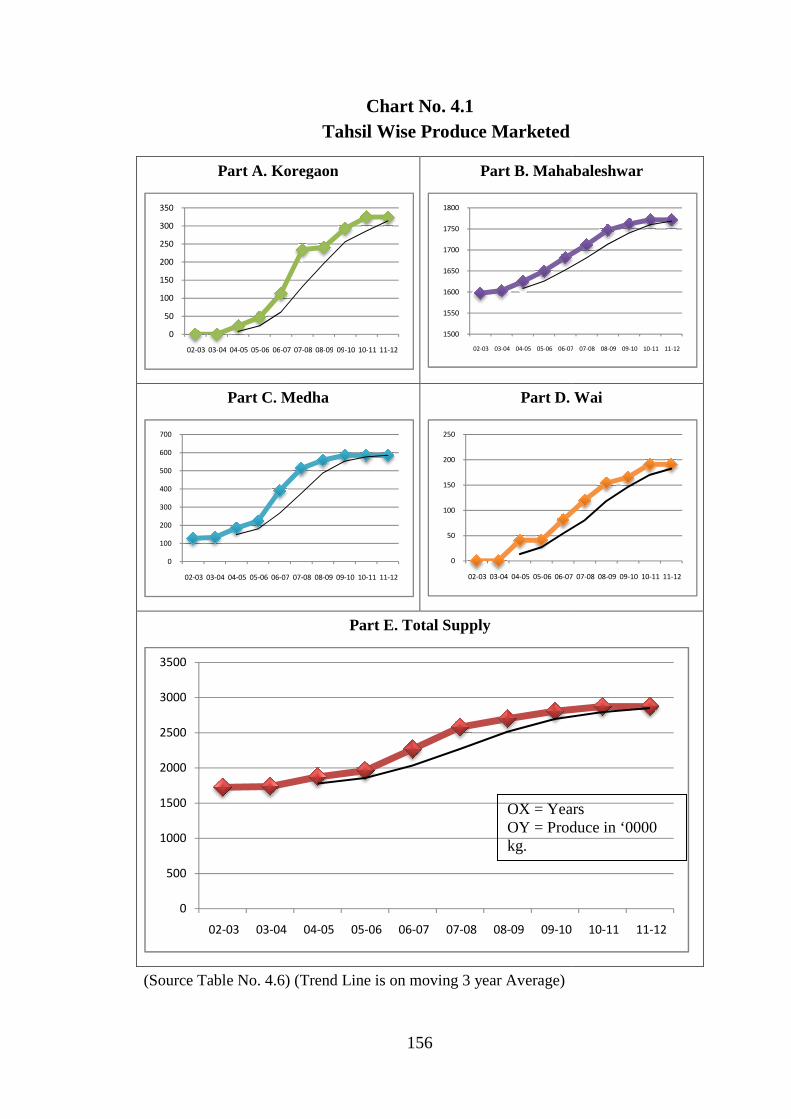

4.3.1. Tahsil wise Produce Marketed

Producers send their produce from tahsil's in different marketing

channels. Following table no. 4.6 focus on the actual produce sells by the

tahsil’s in markets since last ten years as well as it is counting increasing

moving average trend of last ten years. From the table no.4.6 we can

reach up to the conclusion that the major market has been covered by

Mahabaleshwar tahsil. If we consider the last ten year data of marketing

then it show this contribution of market share. The share of

Mahabaleshwar tahsil is around 62 % in last year 2011-12. Then Medha

20%, Koregaon 12% and Wai is 6% share in market in same year.

Table No. 4.6 Tahsil wise Produce Marketed

(Produce in ‘0000 kg.)

Tahsil 02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

Koregaon

NA NA 2.29 4.70 11.30 23.41 24.05 29.32 32.44 32.44

(06.10) (13.14) (19.59) (25.59) (28.60) (31.40)

M’SHWAR

159.72 160.31 162.50 165.00 168.17 171.22 174.70 176.18 177.15 177.15

(160.85) (162.61) (165.22) (168.13) (171.36) (174.03) (176.01) (176.83)

Medha 12.83 13.37 18.43 22.41 39.11 51.36 55.91 58.52 58.53 58.53

(14.88) (18.07) (26.65) (37.63) (48.80) (55.26) (57.65) (58.52)

Wai NA NA 4.08 4.08 8.10 11.99 15.38 16.54 19.10 19.10

(05.42) (08.06) (11.83) (14.64) (17.01) (18.25)

Total 172.54 173.68 187.31 196.19 226.69 257.97 270.05 280.56 287.23 287.23

(177.84) (185.73) (203.40) (226.95) (251.57) (269.53) (279.28) (285.00)

(Source: - Field Work) (Figures in bracket are 3 year moving average)

With evidence table no.4.6 we find the increase in the produce send

in market from tahsil's every year. If we make comparison form the start

year to last year then we see average increase in produce supply. If we

calculate this increase on moving average trend then we find there is

increase production and trend also. If we compare the starting supply with

last year supply of every tahsil it is obvious to say there is many fold

increase in Koregaon tahsil produce supply. There is growth but it is

155

negligible in Mahabaleshwar and trend also indicates this thing. Medha

and Wai tahsil also show remarkable increase in produce supply during

the last years. Aggregate produce supply also showing increase in

produce supply throughout the last ten years and it is remarkable one.

Because it is comparatively about 66% more than the first year value.

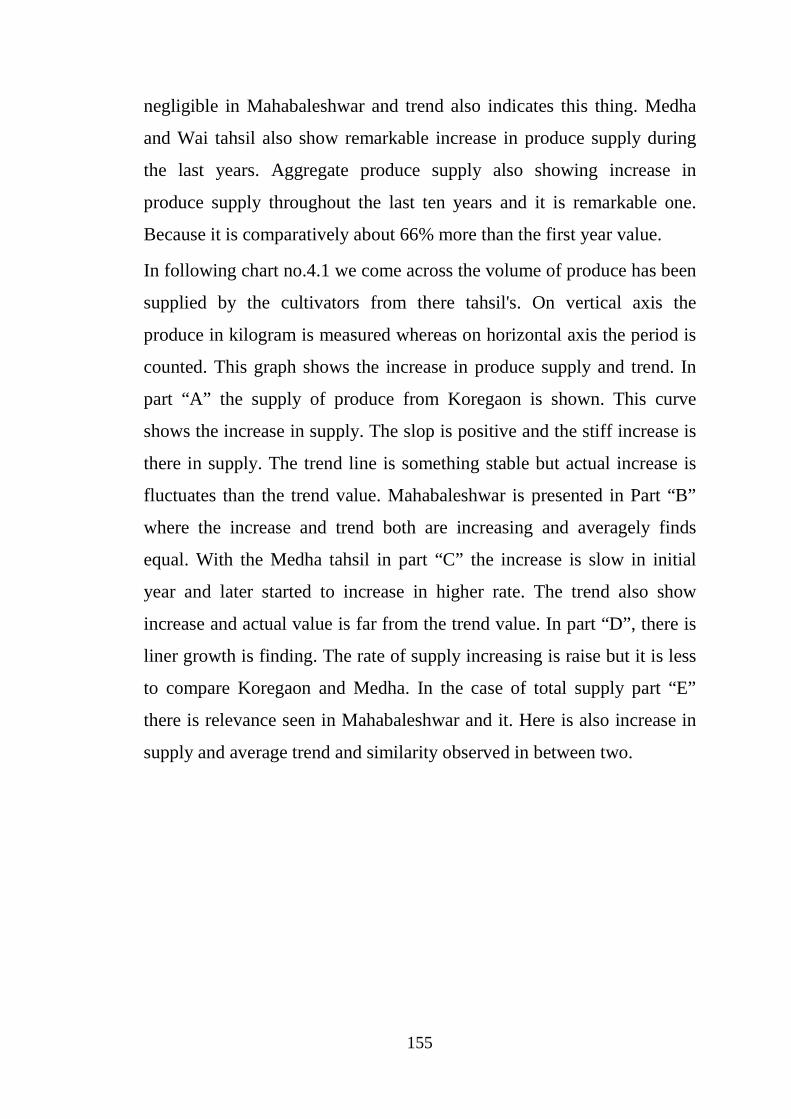

In following chart no.4.1 we come across the volume of produce has been

supplied by the cultivators from there tahsil's. On vertical axis the

produce in kilogram is measured whereas on horizontal axis the period is

counted. This graph shows the increase in produce supply and trend. In

part “A” the supply of produce from Koregaon is shown. This curve

shows the increase in supply. The slop is positive and the stiff increase is

there in supply. The trend line is something stable but actual increase is

fluctuates than the trend value. Mahabaleshwar is presented in Part “B”

where the increase and trend both are increasing and averagely finds

equal. With the Medha tahsil in part “C” the increase is slow in initial

year and later started to increase in higher rate. The trend also show

increase and actual value is far from the trend value. In part “D”, there is

liner growth is finding. The rate of supply increasing is raise but it is less

to compare Koregaon and Medha. In the case of total supply part “E”

there is relevance seen in Mahabaleshwar and it. Here is also increase in

supply and average trend and similarity observed in between two.

Part A. Koregaon

Part C. Medha

(Source Table No. 4.6)

0

50

100

150

200

250

300

350

02-03 03-04 04-05 05-06 06-07

0

100

200

300

400

500

600

700

02-03 03-04 04-05 05-06 06-07

0

500

1000

1500

2000

2500

3000

3500

02-03 03-04

156

Chart No. 4.1 Tahsil Wise Produce Marketed

Part A. Koregaon

Part B. Mahabaleshwar

Part C. Medha

Part D. Wai

Part E. Total Supply

(Source Table No. 4.6) (Trend Line is on moving 3 year Average)

07 07-08 08-09 09-10 10-11 11-12

1500

1550

1600

1650

1700

1750

1800

02-03 03-04 04-05 05-06 06-07

07 07-08 08-09 09-10 10-11 11-12

0

50

100

150

200

250

02-03 03-04 04-05 05-06 06-07

04 04-05 05-06 06-07 07-08 08-09 09-10

OX = Years OY = Produce in ‘0000 kg.

Part B. Mahabaleshwar

Part D. Wai

07 07-08 08-09 09-10 10-11 11-12

07 07-08 08-09 09-10 10-11 11-12

10-11 11-12

OX = Years OY = Produce in ‘0000

157

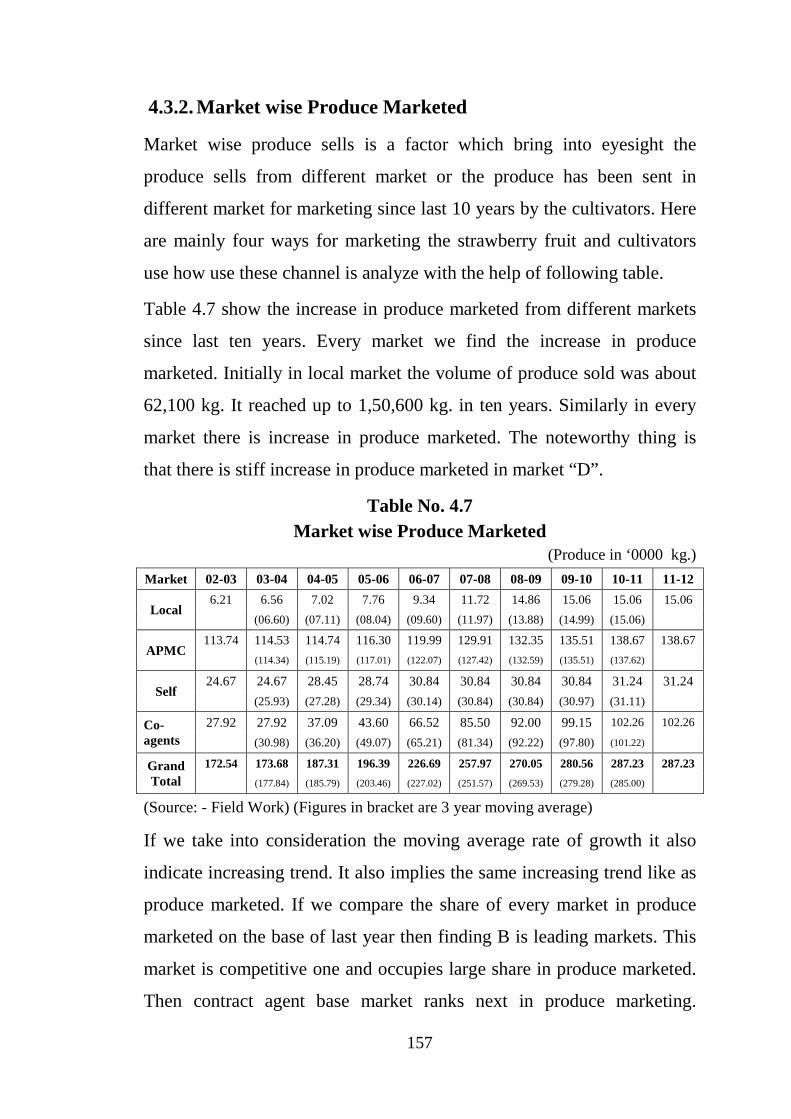

4.3.2. Market wise Produce Marketed

Market wise produce sells is a factor which bring into eyesight the

produce sells from different market or the produce has been sent in

different market for marketing since last 10 years by the cultivators. Here

are mainly four ways for marketing the strawberry fruit and cultivators

use how use these channel is analyze with the help of following table.

Table 4.7 show the increase in produce marketed from different markets

since last ten years. Every market we find the increase in produce

marketed. Initially in local market the volume of produce sold was about

62,100 kg. It reached up to 1,50,600 kg. in ten years. Similarly in every

market there is increase in produce marketed. The noteworthy thing is

that there is stiff increase in produce marketed in market “D”.

Table No. 4.7 Market wise Produce Marketed

(Produce in ‘0000 kg.)

Market 02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

Local 6.21 6.56 7.02 7.76 9.34 11.72 14.86 15.06 15.06 15.06

(06.60) (07.11) (08.04) (09.60) (11.97) (13.88) (14.99) (15.06)

APMC 113.74 114.53 114.74 116.30 119.99 129.91 132.35 135.51 138.67 138.67

(114.34) (115.19) (117.01) (122.07) (127.42) (132.59) (135.51) (137.62)

Self 24.67 24.67 28.45 28.74 30.84 30.84 30.84 30.84 31.24 31.24

(25.93) (27.28) (29.34) (30.14) (30.84) (30.84) (30.97) (31.11)

Co-agents

27.92 27.92 37.09 43.60 66.52 85.50 92.00 99.15 102.26 102.26

(30.98) (36.20) (49.07) (65.21) (81.34) (92.22) (97.80) (101.22)

Grand Total

172.54 173.68 187.31 196.39 226.69 257.97 270.05 280.56 287.23 287.23

(177.84) (185.79) (203.46) (227.02) (251.57) (269.53) (279.28) (285.00)

(Source: - Field Work) (Figures in bracket are 3 year moving average)

If we take into consideration the moving average rate of growth it also

indicate increasing trend. It also implies the same increasing trend like as

produce marketed. If we compare the share of every market in produce

marketed on the base of last year then finding B is leading markets. This

market is competitive one and occupies large share in produce marketed.

Then contract agent base market ranks next in produce marketing.

158

Initially the share of this market was many folds less then this recent year.

Among these markets the Contract agent based D market shows the

fastest growth in produce marketing. Another most important thing is that

the produce marketed increase remaining stable form the year 2008-09 in

A market where as in C market it show the stability trend from year 2006-

07.

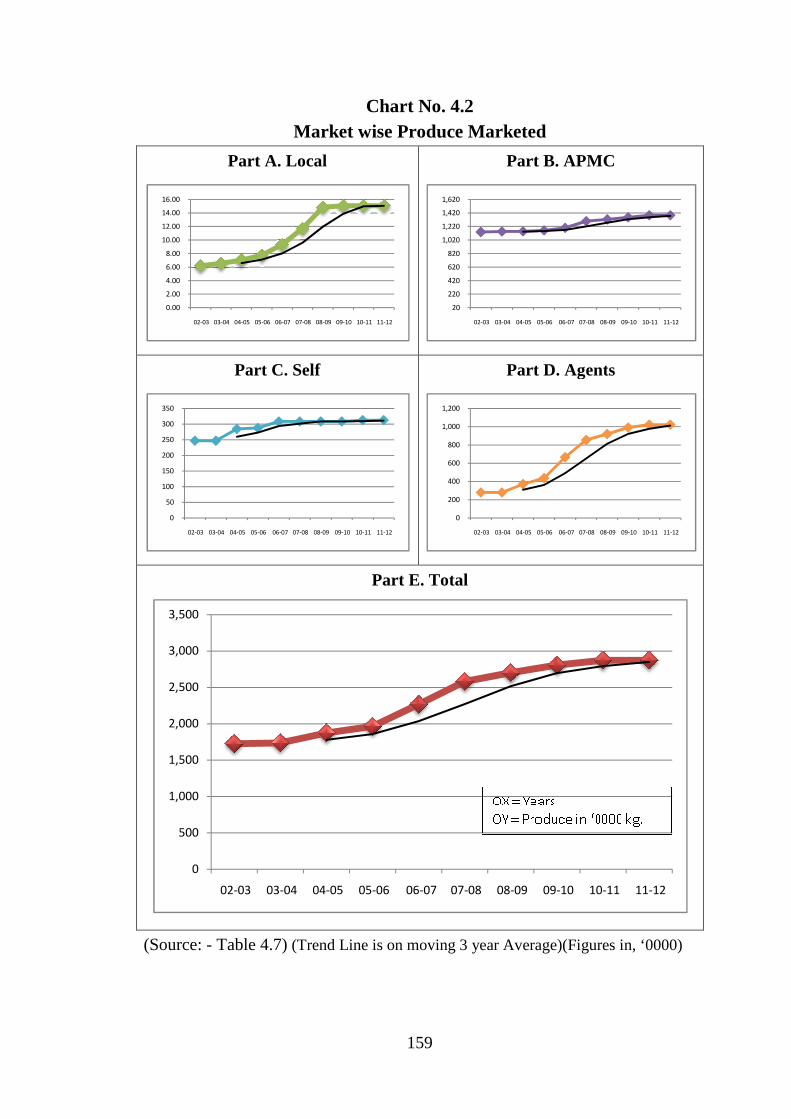

Chart no.4.2 is the graphical representation of table no.4.7 and

representing the increase in marketed produce as well as the increasing

trend on the basis of three year moving average trend. Part I in concern to

domestic market and show the stiff increase in up to first seven years and

later increase is constant. Therefore the actual increase in particular

period is more than the average increase and the cause to more fluctuate

than the average value. In part B alias in APMC market show the increase

but the rate of increase in not much greater to consider the increase rate.

Therefore the rate of increase and average trend is somewhat similar. In

part C- self marketing method the rate of marketing was started to

increase in 2nd year and keep continue for next four year and later

remained minimum stable. It is a reason behind the equality between the

actual rate and average moving rate and trend line too. But part D; agent

based marketing show the continuous increase in produce marketed and

that’s why the curve is showing increasing rate similarly the trend line is

also showing the increasing trend but the actual value is greater than

average value therefore in middle period it is far from trend line. There is

also increase in total produce marketing since last ten year but rate of

increasing is low. The trend also shows increase but the actual value is

more vary than the average value and result to gap in average and actual

curve.

Part A. Local

Part C. Self

(Source: - Table 4.7)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

02-03 03-04 04-05 05-06 06-07

0

50

100

150

200

250

300

350

02-03 03-04 04-05 05-06 06-07

0

500

1,000

1,500

2,000

2,500

3,000

3,500

02-03 03-04

159

Chart No. 4.2 Market wise Produce Marketed

A. Local

Part B. APMC

Part C. Self

Part D. Agents

Part E. Total

Table 4.7) (Trend Line is on moving 3 year Average)(Figures in, ‘0000

07 07-08 08-09 09-10 10-11 11-12

20

220

420

620

820

1,020

1,220

1,420

1,620

02-03 03-04 04-05 05-06 06-07

07 07-08 08-09 09-10 10-11 11-12

0

200

400

600

800

1,000

1,200

02-03 03-04 04-05 05-06 06-07

04 04-05 05-06 06-07 07-08 08-09 09-10

Part B. APMC

Part D. Agents

(Figures in, ‘0000)

07 07-08 08-09 09-10 10-11 11-12

07 07-08 08-09 09-10 10-11 11-12

10 10-11 11-12

160

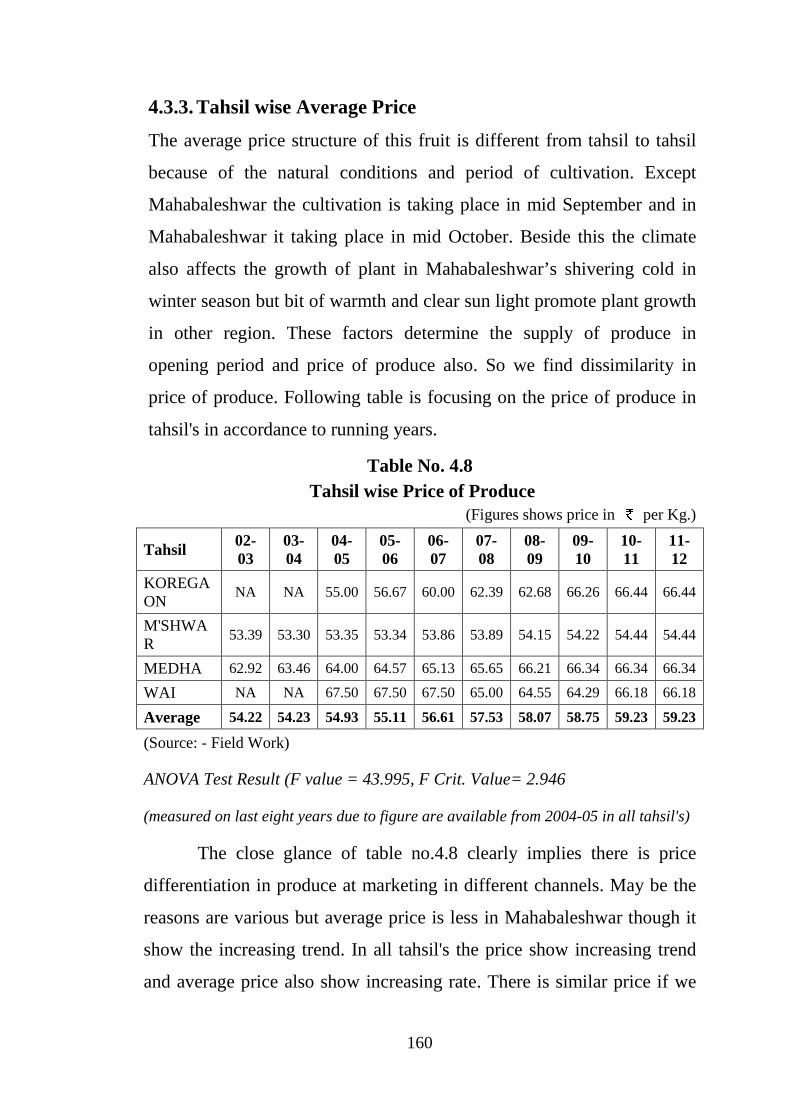

4.3.3. Tahsil wise Average Price

The average price structure of this fruit is different from tahsil to tahsil

because of the natural conditions and period of cultivation. Except

Mahabaleshwar the cultivation is taking place in mid September and in

Mahabaleshwar it taking place in mid October. Beside this the climate

also affects the growth of plant in Mahabaleshwar’s shivering cold in

winter season but bit of warmth and clear sun light promote plant growth

in other region. These factors determine the supply of produce in

opening period and price of produce also. So we find dissimilarity in

price of produce. Following table is focusing on the price of produce in

tahsil's in accordance to running years.

Table No. 4.8 Tahsil wise Price of Produce

(Figures shows price in per Kg.)

Tahsil 02-03

03-04

04-05

05-06

06-07

07-08

08-09

09-10

10-11

11-12

KOREGAON

NA NA 55.00 56.67 60.00 62.39 62.68 66.26 66.44 66.44

M'SHWAR

53.39 53.30 53.35 53.34 53.86 53.89 54.15 54.22 54.44 54.44

MEDHA 62.92 63.46 64.00 64.57 65.13 65.65 66.21 66.34 66.34 66.34

WAI NA NA 67.50 67.50 67.50 65.00 64.55 64.29 66.18 66.18

Average 54.22 54.23 54.93 55.11 56.61 57.53 58.07 58.75 59.23 59.23

(Source: - Field Work)

ANOVA Test Result (F value = 43.995, F Crit. Value= 2.946

(measured on last eight years due to figure are available from 2004-05 in all tahsil's)

The close glance of table no.4.8 clearly implies there is price

differentiation in produce at marketing in different channels. May be the

reasons are various but average price is less in Mahabaleshwar though it

show the increasing trend. In all tahsil's the price show increasing trend

and average price also show increasing rate. There is similar price if we

161

neglect the difference of paisa above on the main value of final year in

Koregaon, Medha and Wai tahsil.

The result of ANOVA test thesis that there is actual difference

between average prices in tahsil's. For finding the difference of prices

between the tahsil’s this test has applied. ANOVA test here taking prices

in these tahsil’s as samples and calculated them altogether. The actual

value after calculating these sample means got (F=43.995) is greater than

the critical value (f crit. 2.946685).It also denotes the difference between

all prices is having significant importance though it is in paisa.

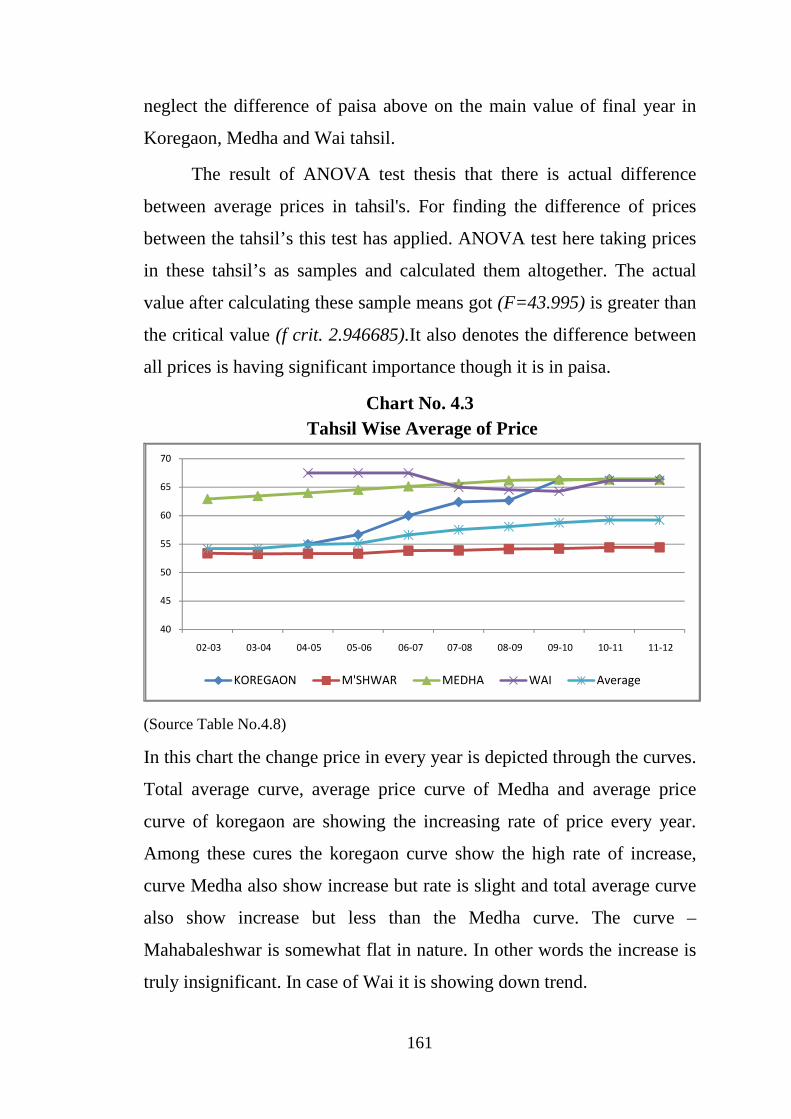

Chart No. 4.3 Tahsil Wise Average of Price

(Source Table No.4.8)

In this chart the change price in every year is depicted through the curves.

Total average curve, average price curve of Medha and average price

curve of koregaon are showing the increasing rate of price every year.

Among these cures the koregaon curve show the high rate of increase,

curve Medha also show increase but rate is slight and total average curve

also show increase but less than the Medha curve. The curve –

Mahabaleshwar is somewhat flat in nature. In other words the increase is

truly insignificant. In case of Wai it is showing down trend.

40

45

50

55

60

65

70

02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

KOREGAON M'SHWAR MEDHA WAI Average

162

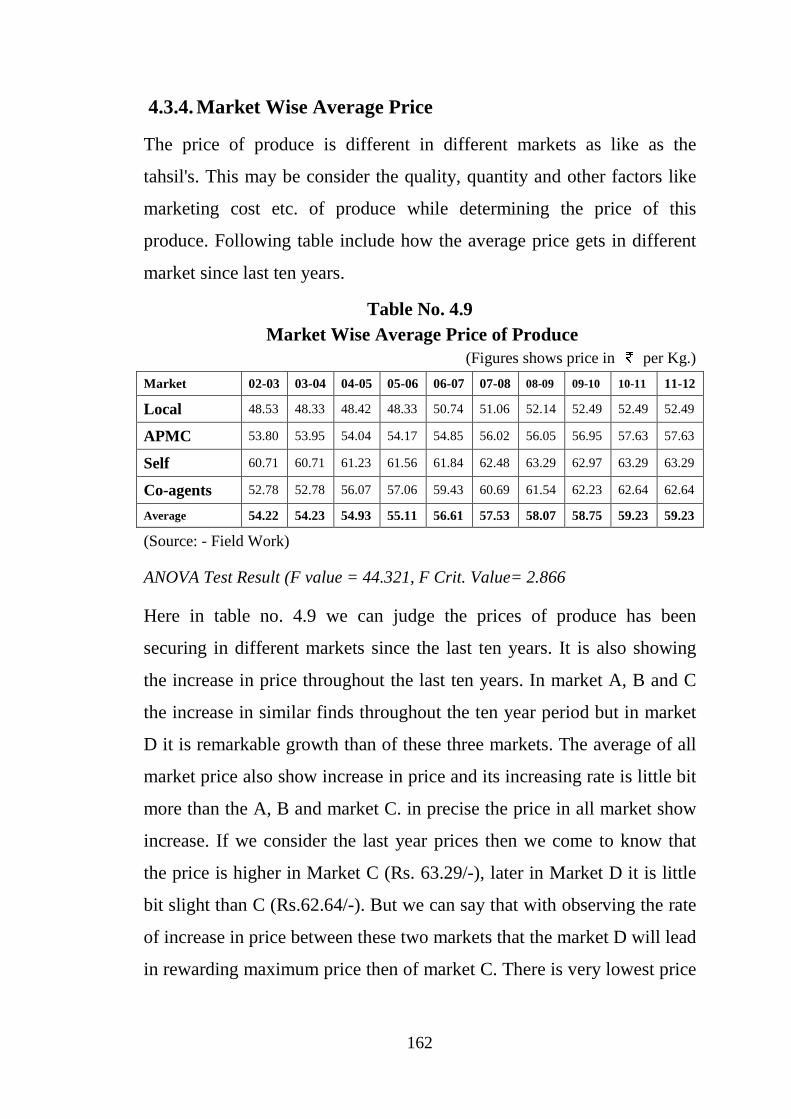

4.3.4. Market Wise Average Price

The price of produce is different in different markets as like as the

tahsil's. This may be consider the quality, quantity and other factors like

marketing cost etc. of produce while determining the price of this

produce. Following table include how the average price gets in different

market since last ten years.

Table No. 4.9 Market Wise Average Price of Produce

(Figures shows price in per Kg.)

Market 02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

Local 48.53 48.33 48.42 48.33 50.74 51.06 52.14 52.49 52.49 52.49

APMC 53.80 53.95 54.04 54.17 54.85 56.02 56.05 56.95 57.63 57.63

Self 60.71 60.71 61.23 61.56 61.84 62.48 63.29 62.97 63.29 63.29

Co-agents 52.78 52.78 56.07 57.06 59.43 60.69 61.54 62.23 62.64 62.64

Average 54.22 54.23 54.93 55.11 56.61 57.53 58.07 58.75 59.23 59.23

(Source: - Field Work)

ANOVA Test Result (F value = 44.321, F Crit. Value= 2.866

Here in table no. 4.9 we can judge the prices of produce has been

securing in different markets since the last ten years. It is also showing

the increase in price throughout the last ten years. In market A, B and C

the increase in similar finds throughout the ten year period but in market

D it is remarkable growth than of these three markets. The average of all

market price also show increase in price and its increasing rate is little bit

more than the A, B and market C. in precise the price in all market show

increase. If we consider the last year prices then we come to know that

the price is higher in Market C (Rs. 63.29/-), later in Market D it is little

bit slight than C (Rs.62.64/-). But we can say that with observing the rate

of increase in price between these two markets that the market D will lead

in rewarding maximum price then of market C. There is very lowest price

163

than others markets in market A which is also lower than average of total

market price.

ANOVA test result also says that there is difference between

average prices in markets. The actual value (F=44.32156) and critical

value (F crit. =2.866266 ) are not equal. Here the critical value is less

than the actual value therefore the average of price different in different

markets. The difference is also significant to take into consideration.

Following chart is representing this table into its graphical form.

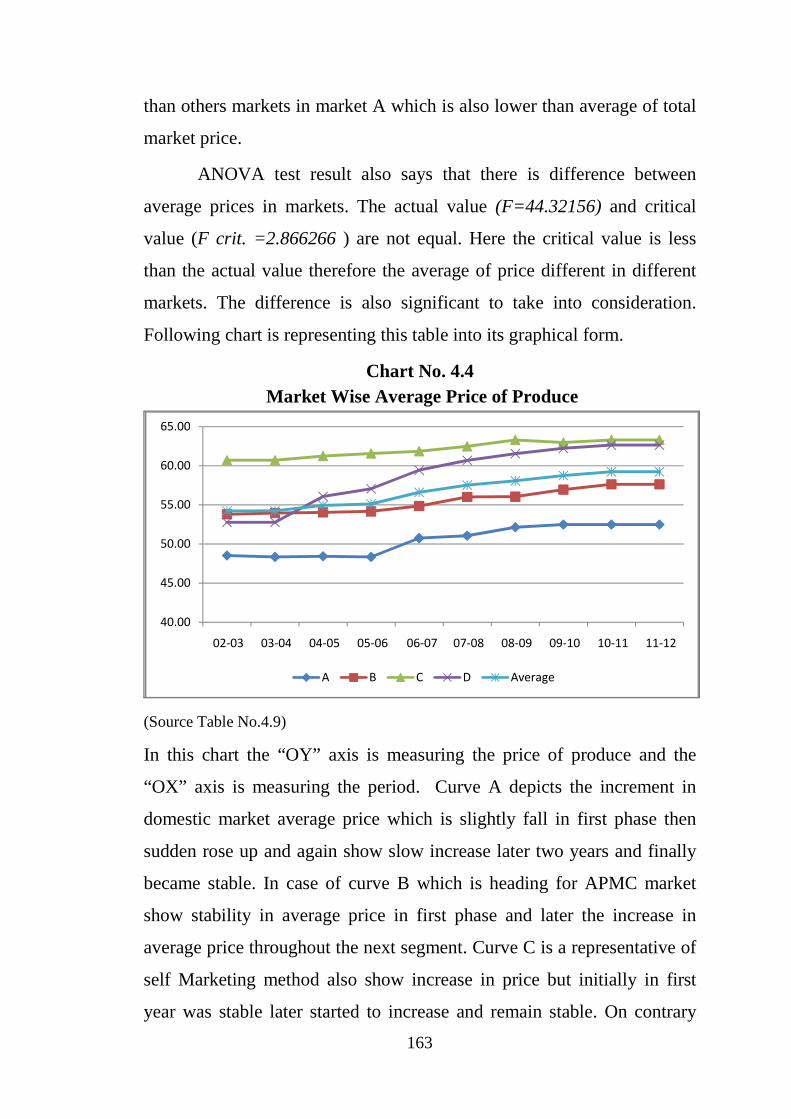

Chart No. 4.4 Market Wise Average Price of Produce

(Source Table No.4.9)

In this chart the “OY” axis is measuring the price of produce and the

“OX” axis is measuring the period. Curve A depicts the increment in

domestic market average price which is slightly fall in first phase then

sudden rose up and again show slow increase later two years and finally

became stable. In case of curve B which is heading for APMC market

show stability in average price in first phase and later the increase in

average price throughout the next segment. Curve C is a representative of

self Marketing method also show increase in price but initially in first

year was stable later started to increase and remain stable. On contrary

40.00

45.00

50.00

55.00

60.00

65.00

02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

A B C D Average

164

the D curve assumed name agents base market curve is showing higher

rate of increase in average of price than any other market. Similarly the

average of total price is also showing the increasing trend in price.

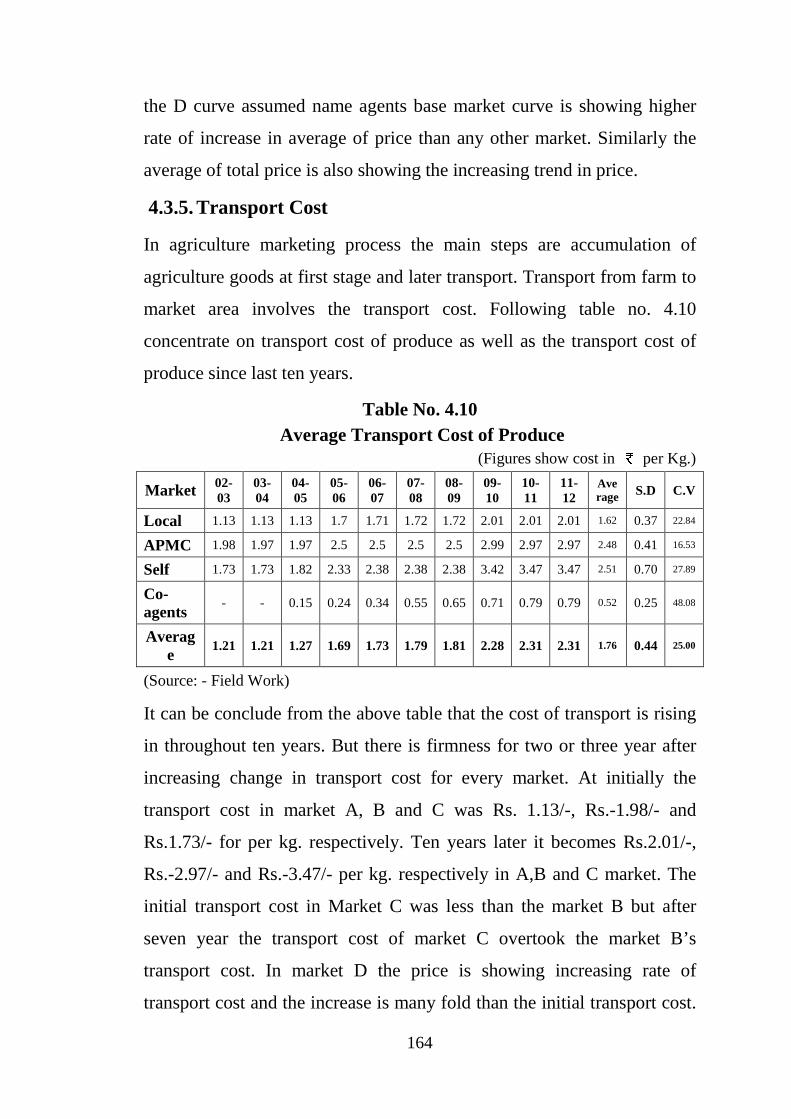

4.3.5. Transport Cost

In agriculture marketing process the main steps are accumulation of

agriculture goods at first stage and later transport. Transport from farm to

market area involves the transport cost. Following table no. 4.10

concentrate on transport cost of produce as well as the transport cost of

produce since last ten years.

Table No. 4.10 Average Transport Cost of Produce

(Figures show cost in per Kg.)

Market 02-03

03-04

04-05

05-06

06-07

07-08

08-09

09-10

10-11

11-12

Average S.D C.V

Local 1.13 1.13 1.13 1.7 1.71 1.72 1.72 2.01 2.01 2.01 1.62 0.37 22.84

APMC 1.98 1.97 1.97 2.5 2.5 2.5 2.5 2.99 2.97 2.97 2.48 0.41 16.53

Self 1.73 1.73 1.82 2.33 2.38 2.38 2.38 3.42 3.47 3.47 2.51 0.70 27.89

Co-agents

- - 0.15 0.24 0.34 0.55 0.65 0.71 0.79 0.79 0.52 0.25 48.08

Average

1.21 1.21 1.27 1.69 1.73 1.79 1.81 2.28 2.31 2.31 1.76 0.44 25.00

(Source: - Field Work)

It can be conclude from the above table that the cost of transport is rising

in throughout ten years. But there is firmness for two or three year after

increasing change in transport cost for every market. At initially the

transport cost in market A, B and C was Rs. 1.13/-, Rs.-1.98/- and

Rs.1.73/- for per kg. respectively. Ten years later it becomes Rs.2.01/-,

Rs.-2.97/- and Rs.-3.47/- per kg. respectively in A,B and C market. The

initial transport cost in Market C was less than the market B but after

seven year the transport cost of market C overtook the market B’s

transport cost. In market D the price is showing increasing rate of

transport cost and the increase is many fold than the initial transport cost.

165

It is also increasing about the average of total transport cost. If we

analyze the S.D. then we come to know the more variations are there in

market C’s transport cost. Later in total average of market cost. And

minimum variations in market D’s transport cost. In same sense we can

observe the C.V. which state that there is stability in transport cost in B

market where as more unstable is market D’s transport cost.

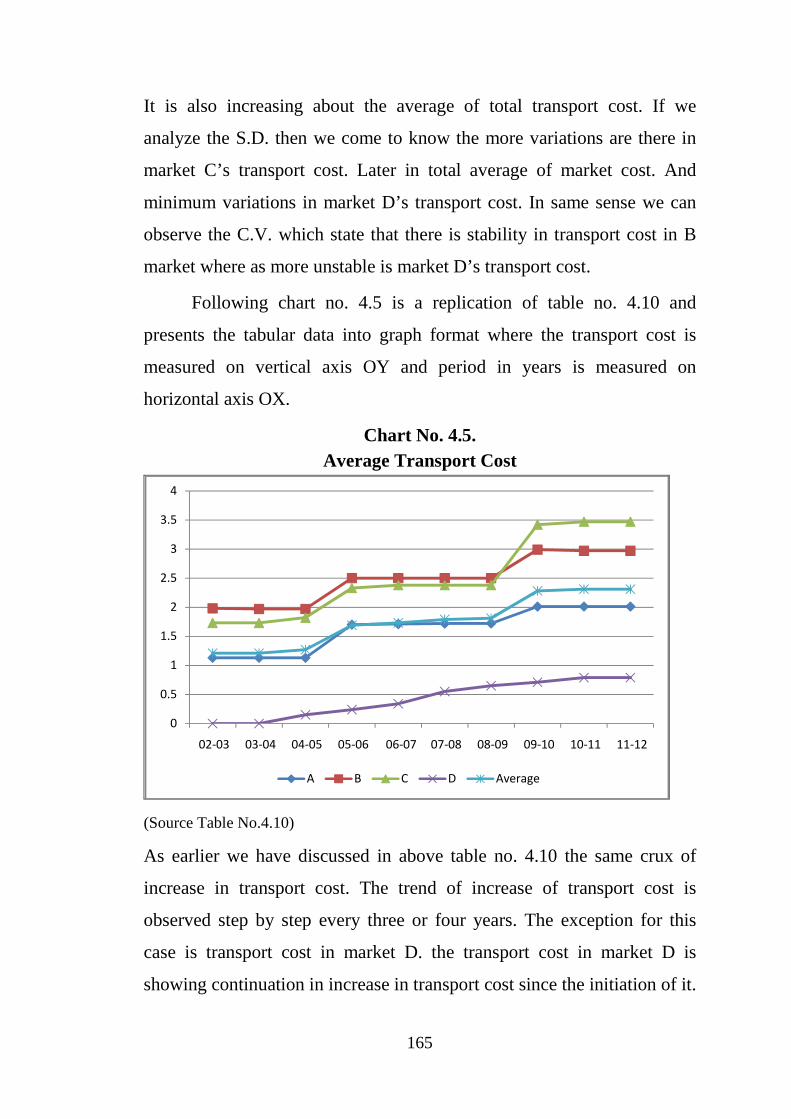

Following chart no. 4.5 is a replication of table no. 4.10 and

presents the tabular data into graph format where the transport cost is

measured on vertical axis OY and period in years is measured on

horizontal axis OX.

Chart No. 4.5. Average Transport Cost

(Source Table No.4.10)

As earlier we have discussed in above table no. 4.10 the same crux of

increase in transport cost. The trend of increase of transport cost is

observed step by step every three or four years. The exception for this

case is transport cost in market D. the transport cost in market D is

showing continuation in increase in transport cost since the initiation of it.

0

0.5

1

1.5

2

2.5

3

3.5

4

02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

A B C D Average

166

The transport cost in market C was lying below the transport cost in

market B in first seven years and then it increase and dropped the market

B’s transport cost curve below it. Curve A and Average of all transport

cost show the same variation in transport cost of first seven years and

later average transport cost rate increase is more than of rate market A’s

transport cost.

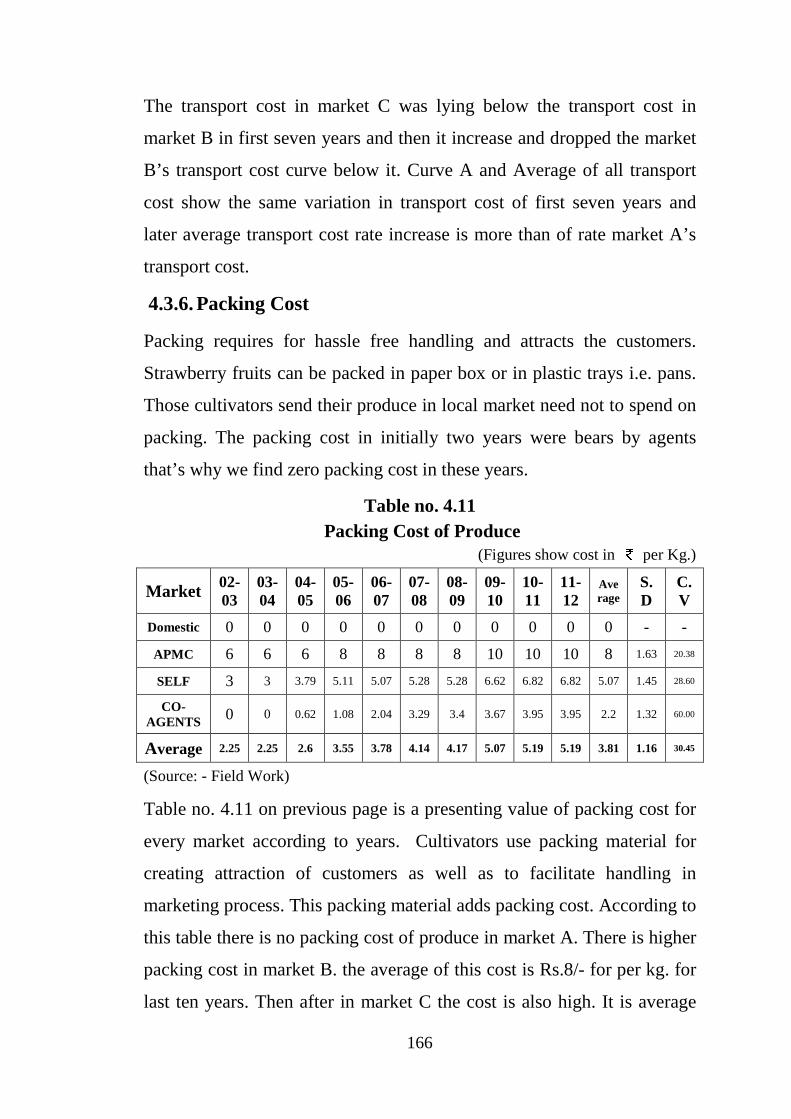

4.3.6. Packing Cost

Packing requires for hassle free handling and attracts the customers.

Strawberry fruits can be packed in paper box or in plastic trays i.e. pans.

Those cultivators send their produce in local market need not to spend on

packing. The packing cost in initially two years were bears by agents

that’s why we find zero packing cost in these years.

Table no. 4.11 Packing Cost of Produce

(Figures show cost in per Kg.)

Market 02-03

03-04

04-05

05-06

06-07

07-08

08-09

09-10

10-11

11-12

Average

S.D

C.V

Domestic 0 0 0 0 0 0 0 0 0 0 0 - -

APMC 6 6 6 8 8 8 8 10 10 10 8 1.63 20.38

SELF 3 3 3.79 5.11 5.07 5.28 5.28 6.62 6.82 6.82 5.07 1.45 28.60

CO-AGENTS 0 0 0.62 1.08 2.04 3.29 3.4 3.67 3.95 3.95 2.2 1.32 60.00

Average 2.25 2.25 2.6 3.55 3.78 4.14 4.17 5.07 5.19 5.19 3.81 1.16 30.45

(Source: - Field Work)

Table no. 4.11 on previous page is a presenting value of packing cost for

every market according to years. Cultivators use packing material for

creating attraction of customers as well as to facilitate handling in

marketing process. This packing material adds packing cost. According to

this table there is no packing cost of produce in market A. There is higher

packing cost in market B. the average of this cost is Rs.8/- for per kg. for

last ten years. Then after in market C the cost is also high. It is average

167

Rs. 5.27/- per kg. for last ten years. Lastly for agent base market it is

average Rs. 2.2/- per kg. for last eight years. If we seen this from angle

of increasing rate of packing cost then it reflect the step by step increase

in packing cost in B , C and Average total market though there is

negligible difference.

If we observe the S.D. then we come to know that average of total

packing cost is less deviate from mean whereas packing cost in market B

is more deviate from the mean. While considering the C.V. we find there

is stability in packing cost of produce in market B while in market D it’s

unstable.

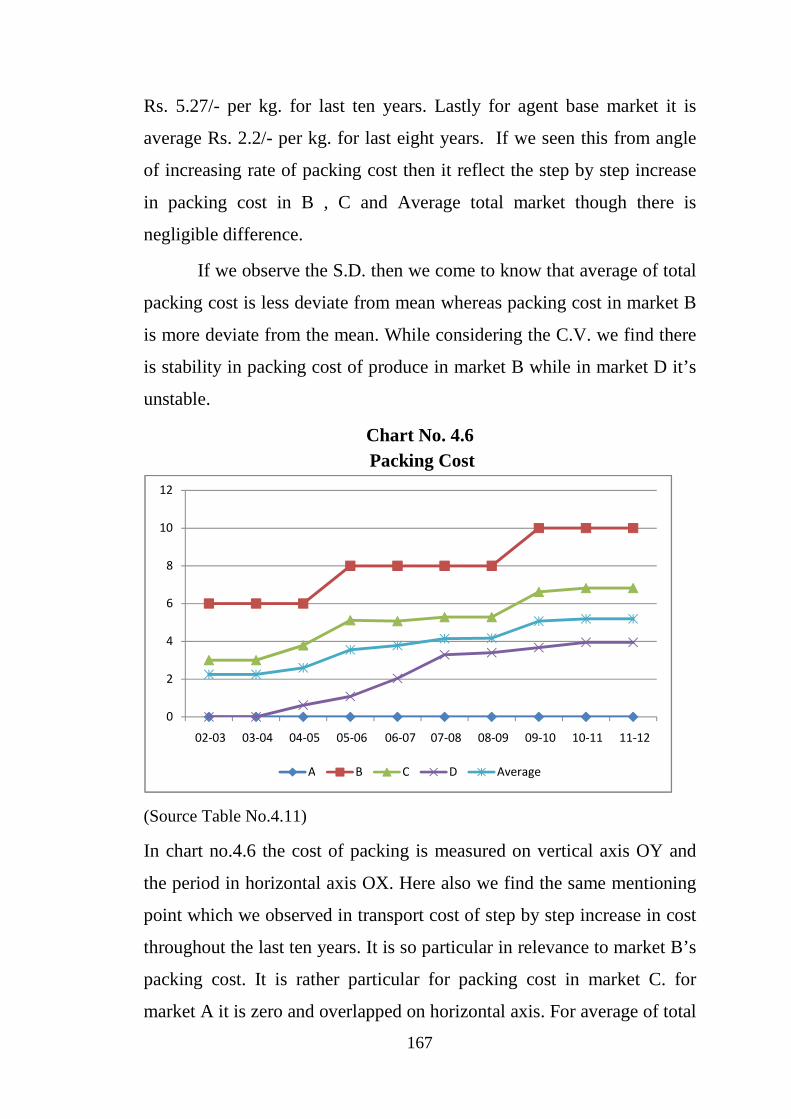

Chart No. 4.6 Packing Cost

(Source Table No.4.11)

In chart no.4.6 the cost of packing is measured on vertical axis OY and

the period in horizontal axis OX. Here also we find the same mentioning

point which we observed in transport cost of step by step increase in cost

throughout the last ten years. It is so particular in relevance to market B’s

packing cost. It is rather particular for packing cost in market C. for

market A it is zero and overlapped on horizontal axis. For average of total

0

2

4

6

8

10

12

02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

A B C D Average

168

packing cost it is increasing but show the step by step increase. But

difference is that at every segment it maintains increase on low rate and

on next segment it rise sudden and again follow the same trend of

increase. Packing cost in market D show higher rate of increasing in first

four years and in later four years it become slow but increasing.

4.3.7. Commission Cost

Commission is a charge of agents who involved in marketing process of

produce. In local market there is no intermediate so commission too. In

self market cultivator sells the produce so that he performs all activities

without agents. Contract agents are intermediate but there is contract

between cultivator and him and therefore they fix the produce rate for per

season of harvesting. Lastly there is APMC market where the chain of

agents is exists and they charge commission on this produce. So the

cultivator has to paid commission cost to this agents/ agents only.

Following table focus on the commission cost.

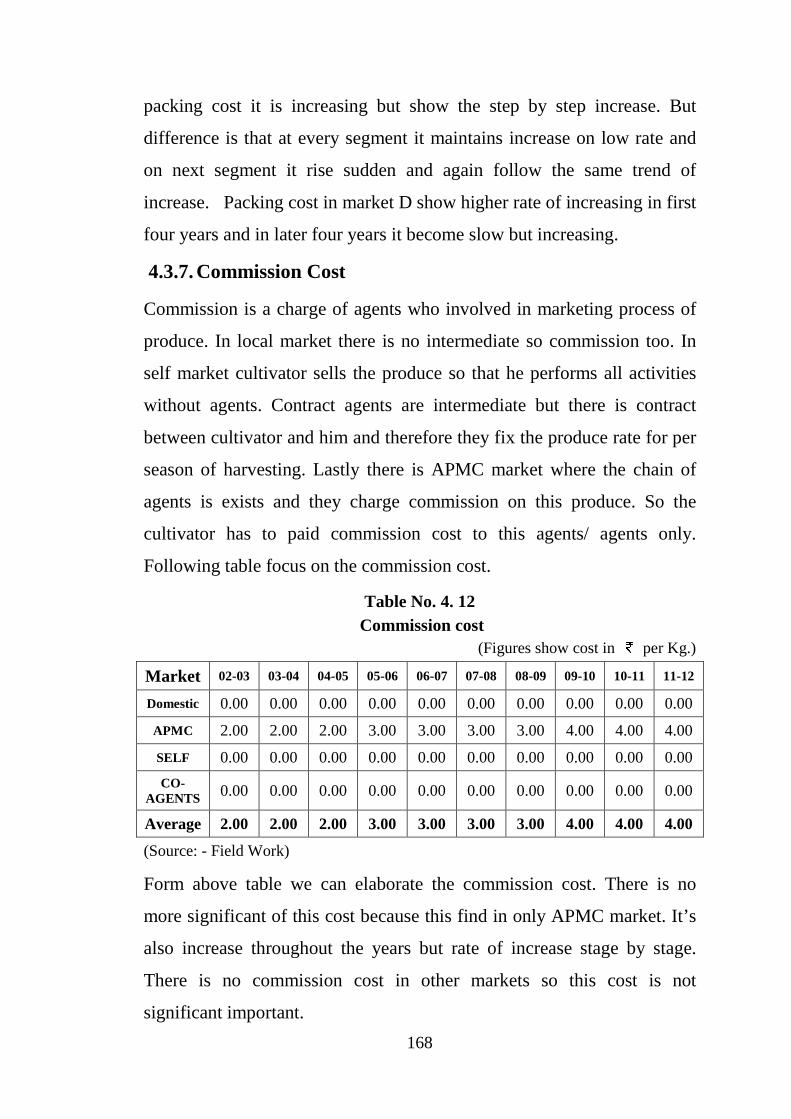

Table No. 4. 12 Commission cost

(Figures show cost in per Kg.)

Market 02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

Domestic 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

APMC 2.00 2.00 2.00 3.00 3.00 3.00 3.00 4.00 4.00 4.00

SELF 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

CO-AGENTS 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Average 2.00 2.00 2.00 3.00 3.00 3.00 3.00 4.00 4.00 4.00

(Source: - Field Work)

Form above table we can elaborate the commission cost. There is no

more significant of this cost because this find in only APMC market. It’s

also increase throughout the years but rate of increase stage by stage.

There is no commission cost in other markets so this cost is not

significant important.

169

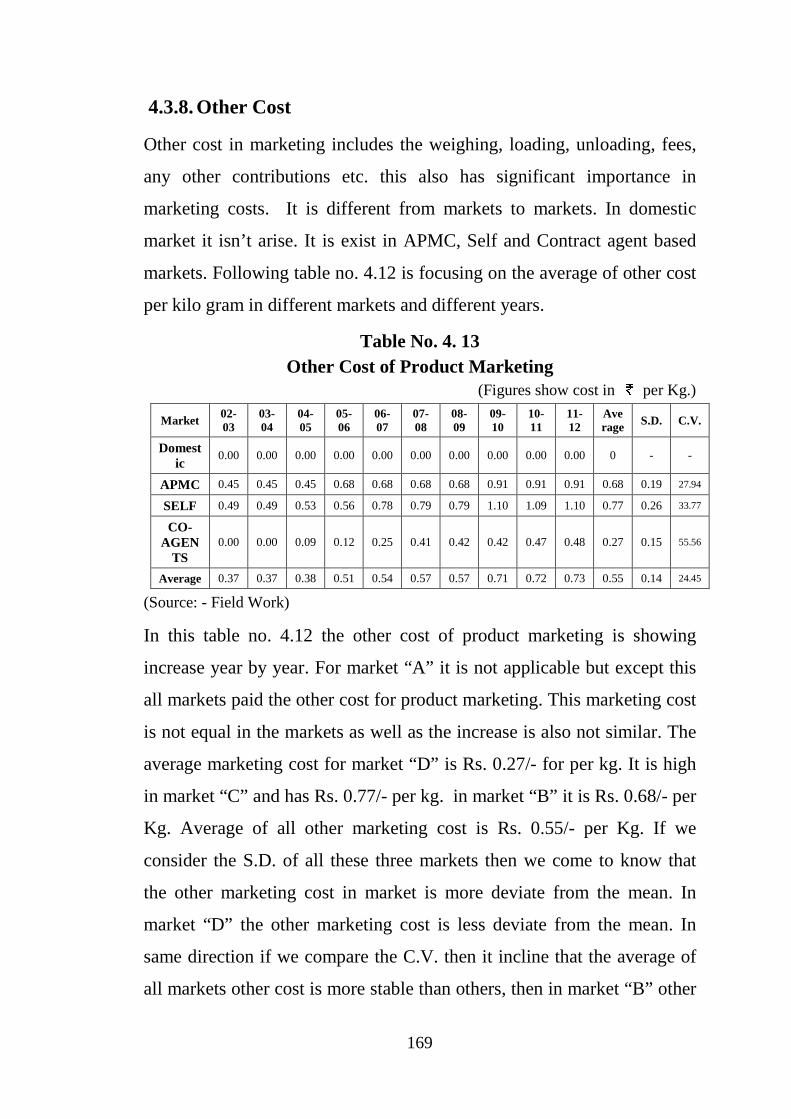

4.3.8. Other Cost

Other cost in marketing includes the weighing, loading, unloading, fees,

any other contributions etc. this also has significant importance in

marketing costs. It is different from markets to markets. In domestic

market it isn’t arise. It is exist in APMC, Self and Contract agent based

markets. Following table no. 4.12 is focusing on the average of other cost

per kilo gram in different markets and different years.

Table No. 4. 13 Other Cost of Product Marketing

(Figures show cost in per Kg.)

Market 02-03

03-04

04-05

05-06

06-07

07-08

08-09

09-10

10-11

11-12

Average S.D. C.V.

Domestic

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0 - -

APMC 0.45 0.45 0.45 0.68 0.68 0.68 0.68 0.91 0.91 0.91 0.68 0.19 27.94

SELF 0.49 0.49 0.53 0.56 0.78 0.79 0.79 1.10 1.09 1.10 0.77 0.26 33.77

CO-AGEN

TS 0.00 0.00 0.09 0.12 0.25 0.41 0.42 0.42 0.47 0.48 0.27 0.15 55.56

Average 0.37 0.37 0.38 0.51 0.54 0.57 0.57 0.71 0.72 0.73 0.55 0.14 24.45

(Source: - Field Work)

In this table no. 4.12 the other cost of product marketing is showing

increase year by year. For market “A” it is not applicable but except this

all markets paid the other cost for product marketing. This marketing cost

is not equal in the markets as well as the increase is also not similar. The

average marketing cost for market “D” is Rs. 0.27/- for per kg. It is high

in market “C” and has Rs. 0.77/- per kg. in market “B” it is Rs. 0.68/- per

Kg. Average of all other marketing cost is Rs. 0.55/- per Kg. If we

consider the S.D. of all these three markets then we come to know that

the other marketing cost in market is more deviate from the mean. In

market “D” the other marketing cost is less deviate from the mean. In

same direction if we compare the C.V. then it incline that the average of

all markets other cost is more stable than others, then in market “B” other

170

marketing cost in show stability. The other marketing cost in market “D”

is more unstable.

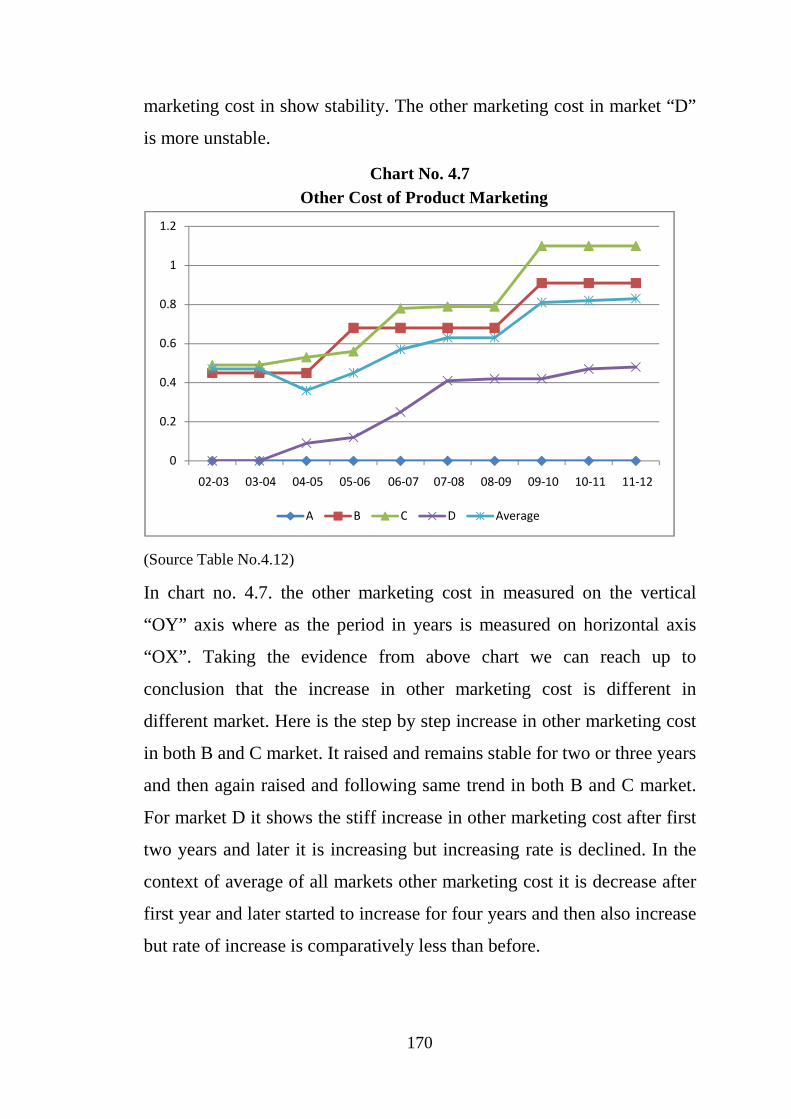

Chart No. 4.7 Other Cost of Product Marketing

(Source Table No.4.12)

In chart no. 4.7. the other marketing cost in measured on the vertical

“OY” axis where as the period in years is measured on horizontal axis

“OX”. Taking the evidence from above chart we can reach up to

conclusion that the increase in other marketing cost is different in

different market. Here is the step by step increase in other marketing cost

in both B and C market. It raised and remains stable for two or three years

and then again raised and following same trend in both B and C market.

For market D it shows the stiff increase in other marketing cost after first

two years and later it is increasing but increasing rate is declined. In the

context of average of all markets other marketing cost it is decrease after

first year and later started to increase for four years and then also increase

but rate of increase is comparatively less than before.

0

0.2

0.4

0.6

0.8

1

1.2

02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

A B C D Average

171

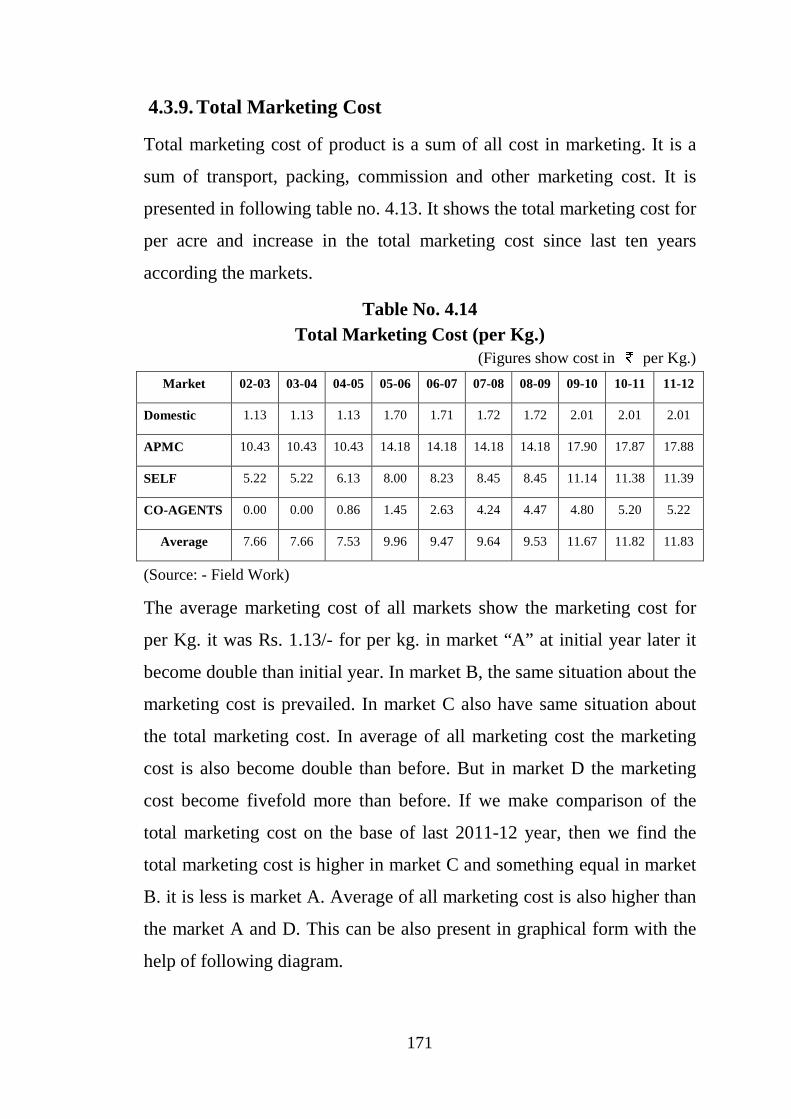

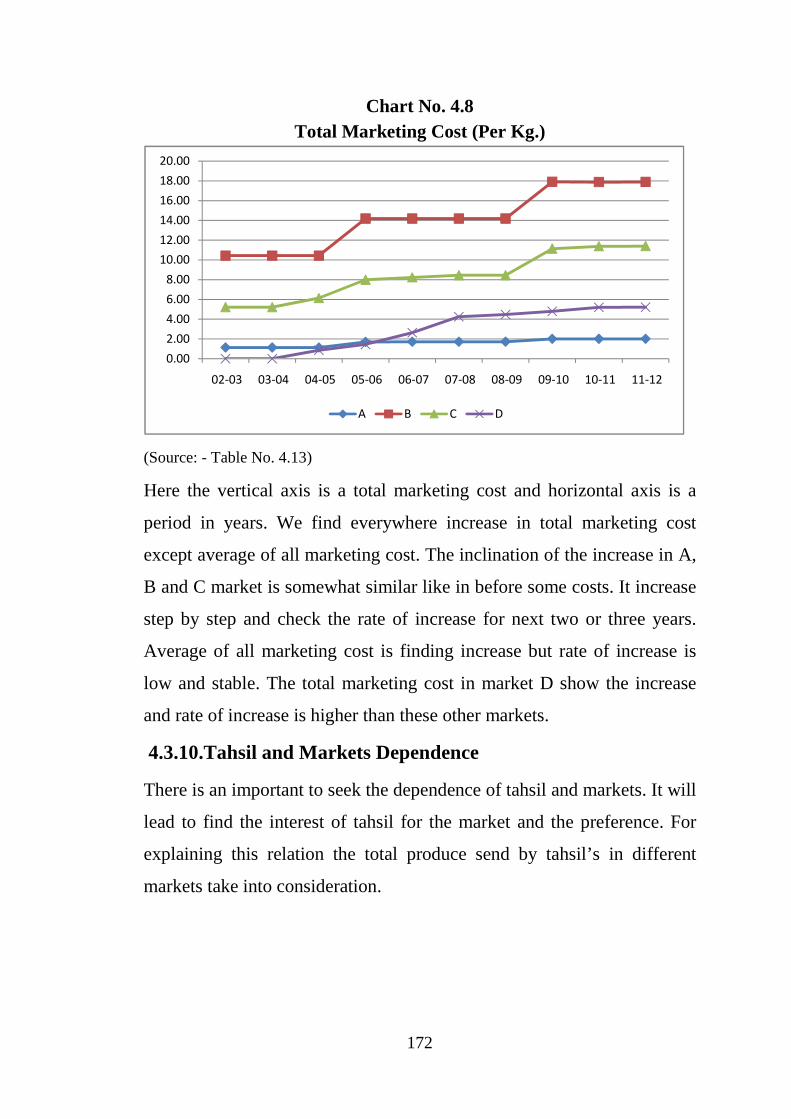

4.3.9. Total Marketing Cost

Total marketing cost of product is a sum of all cost in marketing. It is a

sum of transport, packing, commission and other marketing cost. It is

presented in following table no. 4.13. It shows the total marketing cost for

per acre and increase in the total marketing cost since last ten years

according the markets.

Table No. 4.14 Total Marketing Cost (per Kg.)

(Figures show cost in per Kg.)

Market 02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

Domestic 1.13 1.13 1.13 1.70 1.71 1.72 1.72 2.01 2.01 2.01

APMC 10.43 10.43 10.43 14.18 14.18 14.18 14.18 17.90 17.87 17.88

SELF 5.22 5.22 6.13 8.00 8.23 8.45 8.45 11.14 11.38 11.39

CO-AGENTS 0.00 0.00 0.86 1.45 2.63 4.24 4.47 4.80 5.20 5.22

Average 7.66 7.66 7.53 9.96 9.47 9.64 9.53 11.67 11.82 11.83

(Source: - Field Work)

The average marketing cost of all markets show the marketing cost for

per Kg. it was Rs. 1.13/- for per kg. in market “A” at initial year later it

become double than initial year. In market B, the same situation about the

marketing cost is prevailed. In market C also have same situation about

the total marketing cost. In average of all marketing cost the marketing

cost is also become double than before. But in market D the marketing

cost become fivefold more than before. If we make comparison of the

total marketing cost on the base of last 2011-12 year, then we find the

total marketing cost is higher in market C and something equal in market

B. it is less is market A. Average of all marketing cost is also higher than

the market A and D. This can be also present in graphical form with the

help of following diagram.

172

Chart No. 4.8 Total Marketing Cost (Per Kg.)

(Source: - Table No. 4.13)

Here the vertical axis is a total marketing cost and horizontal axis is a

period in years. We find everywhere increase in total marketing cost

except average of all marketing cost. The inclination of the increase in A,

B and C market is somewhat similar like in before some costs. It increase

step by step and check the rate of increase for next two or three years.

Average of all marketing cost is finding increase but rate of increase is

low and stable. The total marketing cost in market D show the increase

and rate of increase is higher than these other markets.

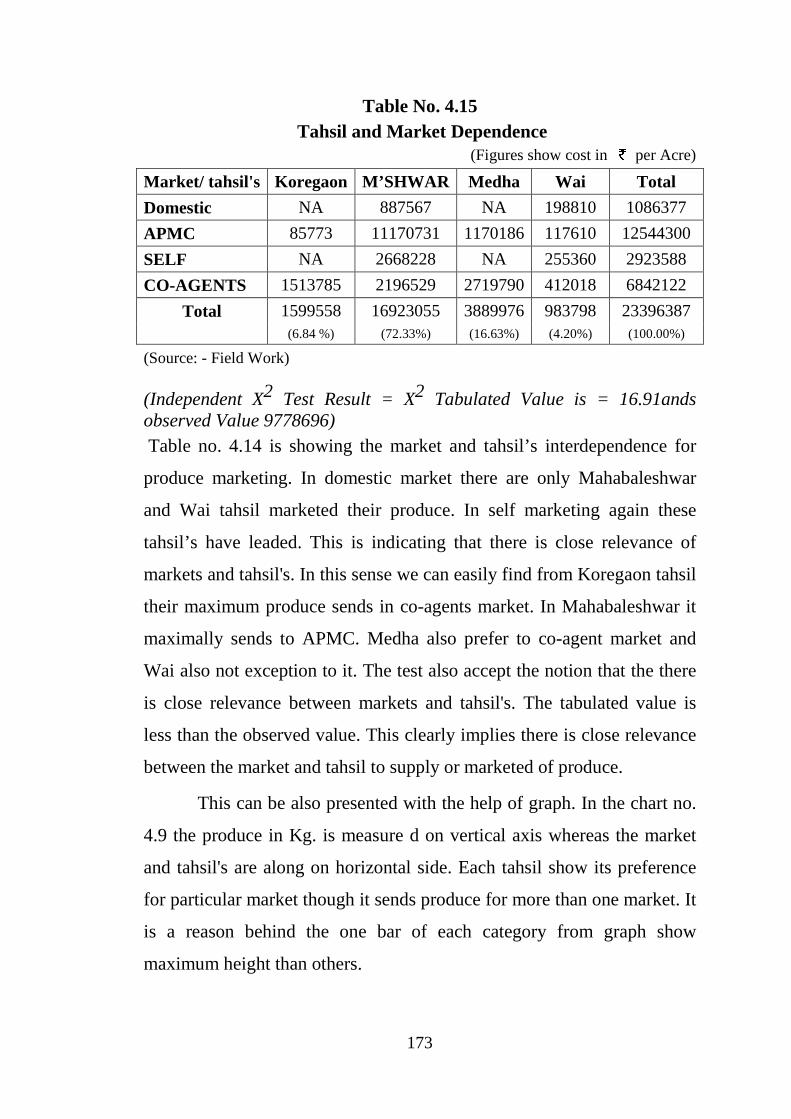

4.3.10. Tahsil and Markets Dependence

There is an important to seek the dependence of tahsil and markets. It will

lead to find the interest of tahsil for the market and the preference. For

explaining this relation the total produce send by tahsil’s in different

markets take into consideration.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

02-03 03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

A B C D

173

Table No. 4.15 Tahsil and Market Dependence

(Figures show cost in per Acre)

Market/ tahsil's Koregaon M’SHWAR Medha Wai Total

Domestic NA 887567 NA 198810 1086377

APMC 85773 11170731 1170186 117610 12544300

SELF NA 2668228 NA 255360 2923588

CO-AGENTS 1513785 2196529 2719790 412018 6842122

Total 1599558 16923055 3889976 983798 23396387

(6.84 %) (72.33%) (16.63%) (4.20%) (100.00%)

(Source: - Field Work)

(Independent X2 Test Result = X2 Tabulated Value is = 16.91ands observed Value 9778696) Table no. 4.14 is showing the market and tahsil’s interdependence for

produce marketing. In domestic market there are only Mahabaleshwar

and Wai tahsil marketed their produce. In self marketing again these

tahsil’s have leaded. This is indicating that there is close relevance of

markets and tahsil's. In this sense we can easily find from Koregaon tahsil

their maximum produce sends in co-agents market. In Mahabaleshwar it

maximally sends to APMC. Medha also prefer to co-agent market and

Wai also not exception to it. The test also accept the notion that the there

is close relevance between markets and tahsil's. The tabulated value is

less than the observed value. This clearly implies there is close relevance

between the market and tahsil to supply or marketed of produce.

This can be also presented with the help of graph. In the chart no.

4.9 the produce in Kg. is measure d on vertical axis whereas the market

and tahsil's are along on horizontal side. Each tahsil show its preference

for particular market though it sends produce for more than one market. It

is a reason behind the one bar of each category from graph show

maximum height than others.

174

Chart No. 4.9

Tahsil and Market Dependence

(Source: - Table No. 4.14)

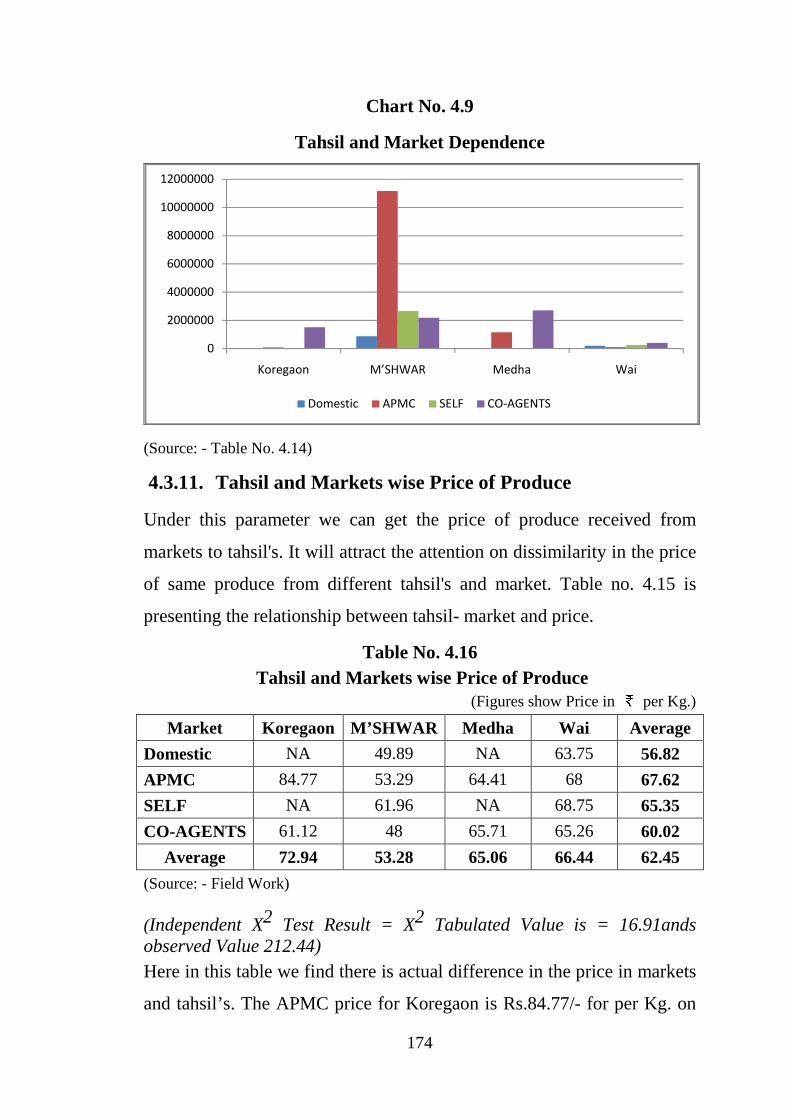

4.3.11. Tahsil and Markets wise Price of Produce

Under this parameter we can get the price of produce received from

markets to tahsil's. It will attract the attention on dissimilarity in the price

of same produce from different tahsil's and market. Table no. 4.15 is

presenting the relationship between tahsil- market and price.

Table No. 4.16 Tahsil and Markets wise Price of Produce

(Figures show Price in per Kg.)

Market Koregaon M’SHWAR Medha Wai Average

Domestic NA 49.89 NA 63.75 56.82

APMC 84.77 53.29 64.41 68 67.62

SELF NA 61.96 NA 68.75 65.35

CO-AGENTS 61.12 48 65.71 65.26 60.02

Average 72.94 53.28 65.06 66.44 62.45

(Source: - Field Work)

(Independent X2 Test Result = X2 Tabulated Value is = 16.91ands observed Value 212.44) Here in this table we find there is actual difference in the price in markets

and tahsil’s. The APMC price for Koregaon is Rs.84.77/- for per Kg. on

0

2000000

4000000

6000000

8000000

10000000

12000000

Koregaon M’SHWAR Medha Wai

Domestic APMC SELF CO-AGENTS

175

contrary Rs. 53.29/- for Mahabaleshwar tahsil. In same manner we find

the differences. It is clearly seen that the APMC market is offering higher

price per kilo gram for strawberry fruits and domestic market gives less.

Similarly koregaon tahsil secures higher price and Mahabaleshwar tahsil

secures low price. This can also prove by the independent X2 test. The

results of this test also accept the same thesis of price difference from

market to market and tahsil to tahsil. Here also the tabulated value is less

than observed value. Which indicate that the interdependence of tahsil

and market and price. It can be present in graphical form like thud in

following graph.

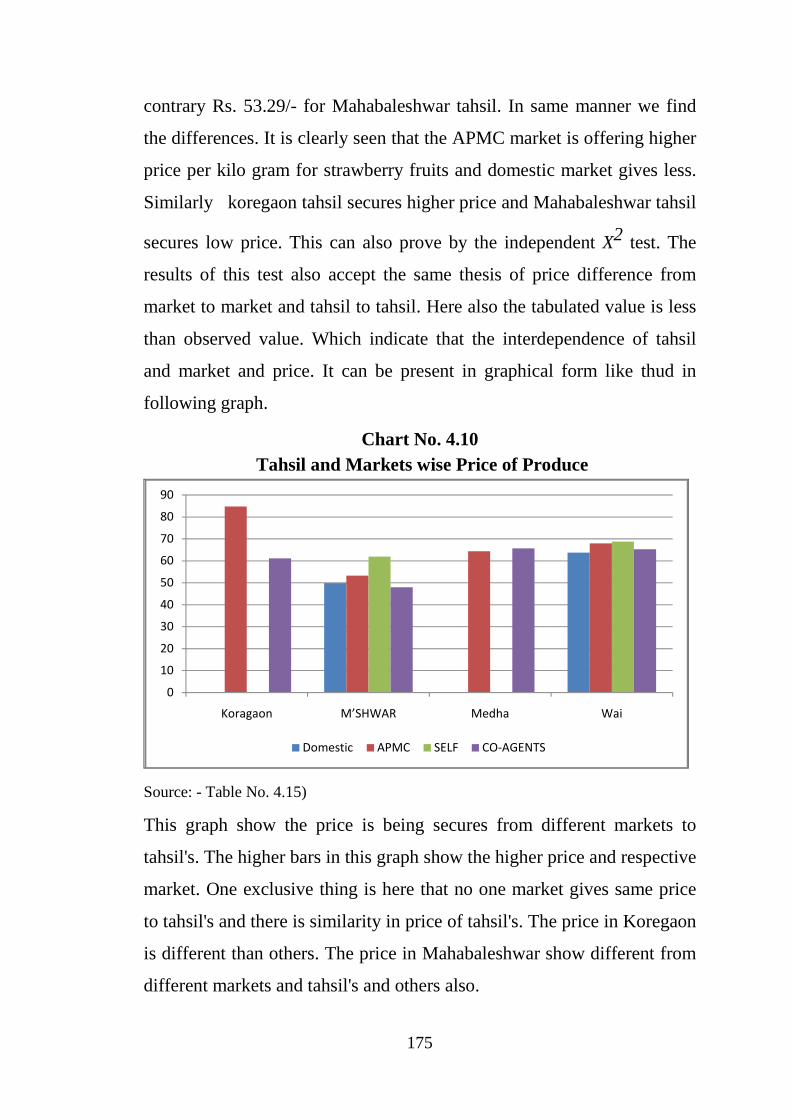

Chart No. 4.10 Tahsil and Markets wise Price of Produce

Source: - Table No. 4.15)

This graph show the price is being secures from different markets to

tahsil's. The higher bars in this graph show the higher price and respective

market. One exclusive thing is here that no one market gives same price

to tahsil's and there is similarity in price of tahsil's. The price in Koregaon

is different than others. The price in Mahabaleshwar show different from

different markets and tahsil's and others also.

0

10

20

30

40

50

60

70

80

90

Koragaon M’SHWAR Medha Wai

Domestic APMC SELF CO-AGENTS

176

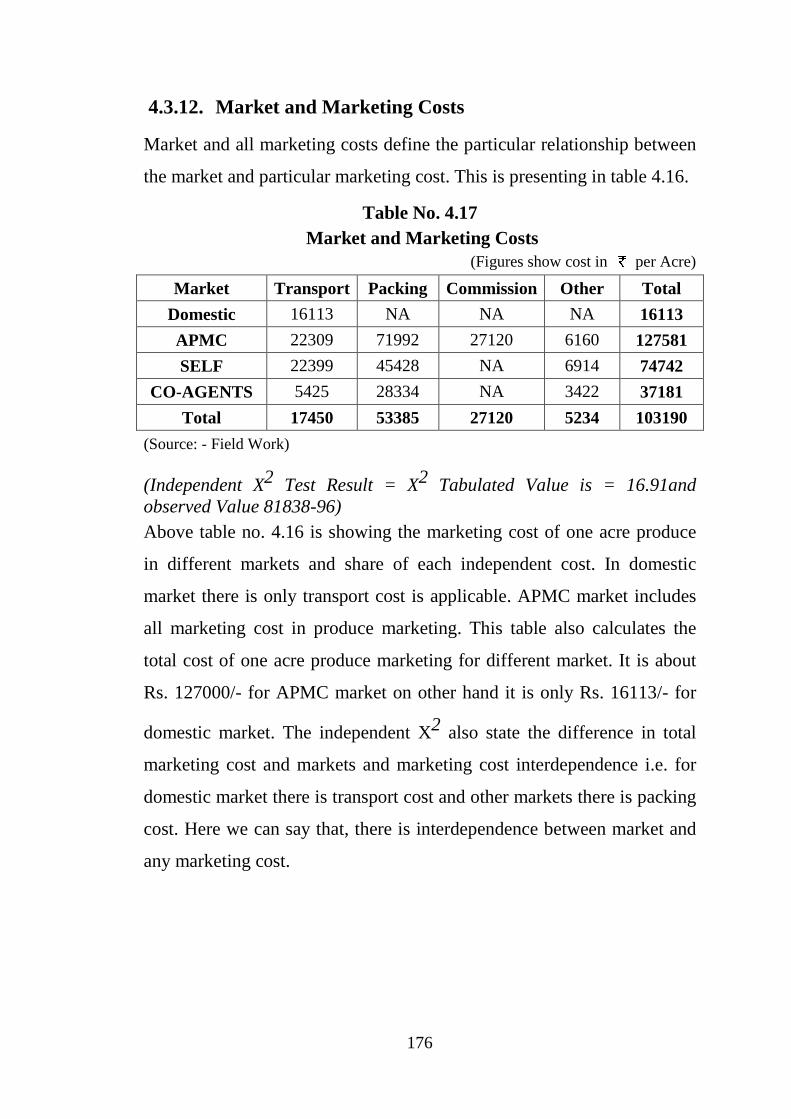

4.3.12. Market and Marketing Costs

Market and all marketing costs define the particular relationship between

the market and particular marketing cost. This is presenting in table 4.16.

Table No. 4.17 Market and Marketing Costs

(Figures show cost in per Acre)

Market Transport Packing Commission Other Total

Domestic 16113 NA NA NA 16113

APMC 22309 71992 27120 6160 127581

SELF 22399 45428 NA 6914 74742

CO-AGENTS 5425 28334 NA 3422 37181

Total 17450 53385 27120 5234 103190

(Source: - Field Work)

(Independent X2 Test Result = X2 Tabulated Value is = 16.91and observed Value 81838-96) Above table no. 4.16 is showing the marketing cost of one acre produce

in different markets and share of each independent cost. In domestic

market there is only transport cost is applicable. APMC market includes

all marketing cost in produce marketing. This table also calculates the

total cost of one acre produce marketing for different market. It is about

Rs. 127000/- for APMC market on other hand it is only Rs. 16113/- for

domestic market. The independent X2 also state the difference in total

marketing cost and markets and marketing cost interdependence i.e. for

domestic market there is transport cost and other markets there is packing

cost. Here we can say that, there is interdependence between market and

any marketing cost.

177

4.4. Problems in Marketing

4.4.1. The daily ache of cultivator is unmanageable fruit picking. It must

be undertakes early sunrise at least before 8.00 am in morning. It is

essential but exhaustive work. In this practice cultivator loose his whole

day working capacity. On account of its essentiality and without option

work mechanism cultivator must keep him assign with this work.

4.4.2. The packing of strawberry fruit is a skillful work and it takes a long

time to pack the whole produce in packing material. As soon as after

completion of fruit clipping this work starts. Cultivator can bring the

specialization in packing and have to cut the packing time for his rest.

In specialization he can work with his colleagues and distributes the

different work for different and skillful person so that there is increase

the work speed in minimum time.

4.4.3. The expenditure in marketing is also major difficulty. In domestic

market it is near to about twenty thousand. It is about Rs. 125000/- in

APMC market which is half of one acre cultivation cost. In these

context cultivators have to concentrate on these independent

expenditure heads in marketing cost and try to cut down the marketing

cost. Here is chance to cut down the packing cost as well as other cost.

Just like usually for packing the all process is manually done. If there is

invention of this kind of machine which automatically weigh the fruits

and fill into box without human touch result to spend time in other

activities as well as for rest.

4.4.4. Another difficulty is relevance to existence of transaction of these

agents. As per cultivators view agents stand between transactions of

178

cultivators and ultimate customers and charge the commission of his

interferes. In this light of agents works cultivators have to keep in mind

that he cannot eliminate this chain similarly he can’t sells his produce

without agents. But cultivators can overcome on this difficulty if one of

the cultivation partner either brother or son or any may perform the

direct marketing function of his strawberry fruit.

4.4.5. Cultivator chooses the suitable market for better return from his

produce sell. He need cash in meantime to foster his family and meet

the all maintenance cost. Therefore he needs instant return form

marketing. There is instant return in domestic and self marketing

method but rate is usually less and risky in nature. He sends his produce

in APMC and his Contracted agents where he gets his return truly late.

Some time they make full payment as an advance for next year. This

payment system collapses the economic schedule of cultivators. The

best way to avoid this economic situation is to use multi markets for

marketing so they can give you payment when you needed it.

4.4.6. While marketing of this fruit about 15% cultivators utters that there

is much flexibility in price during the year. It is a result of demand and

supply and which influence the price. We can’t interfere in this

mechanism with our squirrel share in market. As a producer we can

make plan of production on cooperative basis and try to keep constant

supply throughout year.

4.4.7. 35 % cultivators state that there is no awareness about this fruit in

common consumer so that consumption too. In light of this statement

we have to create awareness among the consumer about benefits of this

fruits as well as the various recipes. Now days the strawberry festival

179

has been organizing in Mahabaleshwar tahsil to create awareness in

consumers. But it is limited up to visitors who visit Mahabaleshwar

tahsil. So we should have to organize this festival on state and national

level to create awareness. Simultaneously we can present our stall in

various exhibitions and fairs to increase in demand.

4.4.8. About 24% cultivators have opinion that they have limited

available options to sell their produce. Instead of these traditional

markets there is no alternative market available for produce marketing.

Today we send our produce in selected cities in Maharashtra and nearest

and famous other State cities. Yet our produce is not reached more than

these selected cities so we have to show our interest in other markets.

4.4.9. About 27% cultivators say their respective intermediate person

doesn’t give them payment on time and some time he makes

misappropriation in final amount. As a cultivator our bargaining power

is less and economic condition doesn’t force us to movement against

well settled agent chain. So we can become self independent to sell our

own product to ease form these incidences. If we come together and on

cooperative basis raise our noise for the price and transaction then it

will lead to eliminated bad conduction in market.

4.4.10. This fruit is perishable so it can’t send very far market and dump

for more days. It can be possible if cold storage facility is available for

storing it and same facility for transporting it to far markets. This will

lead to manage supply according to demand and helpful in capture

nationwide market for increasing aggregate demand.

4.4.11. In India strawberry fruit is generally consumed in fresh form.

Beside this the strawberry we can make available in frozen form for

180

consuming and utilizing in different products. It will helpful in off

season viz. monsoon where produce is not available for marketing. It is

also helpful in stabilize the market price of this fruit. When there are

gluts of produce in market we can transform it into frozen form and sell

out it in scare supply condition.

4.4.12. One more possibility is there to increase the demand for this fruit.

Mostly it is used fresh consumption purpose but if we give stress on the

secondary product in processing units then the demand tend to rise.

4.4.13. Beside this the international market is also allure to our strawberry

and generate maximum benefits from it export to some worldwide

countries.

4.5. Prospects of Strawberry Marketing

4.5.1. Besides the traditional marketing of strawberry fruit in fresh form it

also trades in frozen form in international markets. Cultivators have to

develop this frozening technique and promote the marketing activities.

4.5.2. Find out secondary use of fruit for creating additional demand.

4.5.3. Capture the popular city markets in Indian Territory for widen the

markets.

4.5.4. Advertisement of strawberry fruits through proper media which

will turn to bear awareness in among customer.

4.5.5. Beside these following is international market potential for Indian

strawberry growers.

Strawberry fruits most likes from consumers at global level. Strawberry

cultivates in Europe and America on large scale. Spain, Italy, Poland,

Israel, Kenya, China, Japan etc. are major producers of strawberry.

Though Europe – America produce major parts of strawberry fruits, they

found shortage in October to March due to vagaries of climate situation.

181

This period considers nourishing for strawberry cultivation in Satara.

Abundant yield attains in this period, if diverts in foreign market may be

advantageous to cultivators. We seen pace associated with this intention

in year 2007. About 300 ton exports if strawberry done in Europe and

expected 2000 ton in 2008 – 09 stuck in world recession.

4.6. Export Pricing and Costing -

Export pricing is the most important tool for promoting sells and

facing international Competition. The price has to be realistically worked

out taking into consideration all export benefits and expenses. However

there is no fixed formula for pricing strategies it will differ from exporter

to exporter. The current wholesale market price of strawberry in India is

ranging from Rs 240 to 300 per kg depends on the grades.

4.6.1. Export Standards

EU Market Standards - The marketing standards for quality and labeling

of fruit and vegetables are laid down in basic regulation EC 2200/96 (of

28 October 1996), in the framework of the Common Agricultural Policy

(CAP). Products, which do not comply with these standards, are barred

from the market. Besides EU legislation, importers of frozen fruit and

vegetables have their own quality standards. The EU requirements must

therefore be seen as indicative for the Quality that is demanded by the

European importers. The care and handling between harvests and delivery

to the country of import is often one of the weakest points in the

relationship between producer and importer. The UN standards apply in

the case of a product, which is not covered by the EU quality standards.

The Standards organizations are able to inform the quality standards that

apply to the various products.

4.6.2. EUREPGAP :- A code for fruit and vegetables that is gaining

ground in Europe is EurepGap. The Euro- Retailer Produce Working

182

Group (EUREP) has developed the Good Agricultural Practice

standards. The Working Group has responded to increasing consumer

interest in food safety and environmental issues. The framework of

EurepGap requires companies to have a good management system in

place to deal with quality, hygiene and environmental matters. Although

EurepGap standards are yet not common practice in all the EU member

states, it is expected that they will be increasingly accepted and applied

in the future, particularly by the large supermarket chains.

4.6.3. Major Markets in the World for Frozen Strawberry

A) the Unites States

The United States can be termed as the single largest market for

frozen fruits and vegetables in the world. The US market consumed an

approximate of 4.5 million tones of frozen fruits and vegetables in 2005.

With an annual growth rate of around 3%, it is expected to reach the 6

million tones level by 2010. Frozen vegetables totally dominate the

frozen fruits and vegetables category in US with a share of 93% in 2005.

With future even better for frozen vegetables, the share is expected to

increase to 94% by 2010, meaning 5.6 million tons. Frozen fruits

category’s share is projected to plunge to 5.9% by 2010.

B) The United Kingdom -

United Kingdom is the largest European market for frozen fruits

and vegetables with a total volume of around 1 million tons in 2005. The

market has been clocking a growth rate of around 2.5% for this decade

and is expected to contribute over 26% to the total frozen fruits and

vegetables market in Europe at the end of this decade. Similar to the US

market, frozen vegetables contribute 99% to the category. The frozen

fruits market in UK is expected to grow at a CAGR of 2.15%. Consumers

183

in United Kingdom are getting more and more inclined towards healthy

food as a part of a lifestyle change.

C) France -

France represents one of the largest market in the European Frozen

fruits and Vegetables market. French frozen fruit and vegetable market is

estimated to total 962 thousand tons in 2005. The market for these

products is projected to grow at a compounded annual rate of 2.56% to

reach 1,088 thousand tons by 2010. Frozen vegetables segment is

estimated to hold a lion’s share in the total French Frozen fruits and

vegetables market in 2005. The market is projected to reach 1,077

thousand tons by 2010. Frozen fruit market is estimated to total 9

thousand tons in 2005. The segment is projected to grow at a CAGR of

4.17% to during the ten-year analysis period.

D) Germany -

German market for frozen fruits and vegetables was estimated to

total 886 thousand tons in 2005, and is 906 thousand tons in 2006. The

market is projected to grow at a moderate rate of 2.49% over the analysis

period 2001-2010 to reach 999 thousand tons by 2010. Frozen vegetables

segment is projected to account for a share of 90.43% of the German

frozen fruits and vegetables market in 2005. The market for frozen fruits

is projected to grow at a compounded annual rate of about 2.64% to reach

97 thousand tons by 2010. This segment is projected to experience a

market share gain over the 2001- 2010 periods, to represent 9.67% of the

total market by 2010.

E) Belgium -

The Belgian frozen food market grew by 5.2% in 2003 to reach a

value of $785 million. In 2008, the market is forecast to have a value of

$979 million, an increase of 24.7% since 2003. Frozen meat, fish and

184

seafood remained the leading segment in the market. In 2003, frozen

meat, fish and seafood generated 44.9% of the frozen food sales. In 2003,

the Belgian market generated 1.8% of the European frozen food sales.

During the next five years, the market is expected to experience strong

but gradually decelerating growth rates. By 2008, the market is forecast

to reach a value of $979 million, which equates to a CAGR of 4.5% in the

period of 2003 – 2008, higher than the European market. Indeed, it is

expected that the Belgian market will be the strongest performing frozen

food market in Western Europe in the next five years, heavily outpacing

the larger markets of France, Germany and the UK.

F) Japan -

The Japanese market for frozen fruits and vegetables was estimated

at 1,153 thousand tons in 2005, and is 1,189 thousand tons in 2006. The

market is projected to grow at a compounded annual rate of about 3.44%,

to reach 1,324 thousand tons by 2010. The Japanese frozen fruits market

was estimated to be 247 thousand tons in 2005, and is projected to grow

at a CAGR of 2.31% to reach 268 thousand tons by 2010. The frozen fruit

segment is projected to experience a decline in market share through the

ten-year period and account for 20.23% of the total market by 2010.

We are standing on the threshold of world’s liberalization,

privatization and globalization policy. In line of this policy we have to

accept the agricultural as a commercial activity where fittest can only

survive. Every commodity and service is becoming global and customer

too. Now day we have to accept the new challenges and our old

discrepancies as opportunities and major thrust areas. Tough there are

several difficulties occurs in strawberry marketing since we have been

185

starting the marketing of this fruits but we never stop our proceeding of