STRATEGOS - tradewinds.iift.ac.intradewinds.iift.ac.in/Magazines/Strategos.pdf · Strategos |...

33

-

Upload

nguyenthuan -

Category

Documents

-

view

213 -

download

0

Transcript of STRATEGOS - tradewinds.iift.ac.intradewinds.iift.ac.in/Magazines/Strategos.pdf · Strategos |...

AUGUST Edition

Dear Reader,

We feel immense pleasure to bring before you the august edition

of STRATEGOS, the consulting magazine of Indian institute of

Foreign Trade.

Counted among the premiere B-schools of the country, IIFT

has a rich diversity of students and we have tried to provide a

platform for them to share their thoughts and ideas and

showcase their knowledge in the domains of consulting, strategy

and General Management.

We have various articles on the challenges faced by business due

to the ever changing global economy , opportunities for India in

this global economy as well as repositioning of brand India.

We hope that you have an enriching and learning experience and

that you enjoy yourself as much as we have in the entire process

of bringing out this magazine to you.

Team StrategosStrategos, magazine of Socrates Club of IIFT is the result of contribution of various stakeholders. We

would like to thank all the contributors of articles and SOCRATES – The consulting and strategy club of

IIFT.

The team comprises of the following:

Editors : Venkatraman Satyamurthy , Nimit Malhotra,

MBA(IB) 2014-16

Harshita Solanki, Somyanshu Arora

MBA(IB) 2015-17

Yours sincerely,

Team Strategos

Strategos | August 2015

Indian Institute of Foreign Trade

30

3

TABLE OF CONTENTS

Topic Page

The Evolving Patterns in the Global Political Economy

By: Prince Shaji 4

The Paradigm Shift in Today’s Geopolitical Climate

By: Rahul Khandelwal & Ankit Pathak 8

The Struggle to Adopt to the Evolving Global Economy

By: Rupam Jhawar & Nikhil Padmalayam 11

Challenges for Businesses due to Transformations in the Global

Economy

By: Snigdha Srivastava15

Some Interesting Facts, Figures & More

By: Harshita Solanki 18

The Need for Repositioning Brand India

By: Saurabh Kumar 19

Opportunities for India in Today’s Globalized World

By: Diganta Sarkar 24

Wordsworth – The Crossword

By: Somyanshu Arora 27

IIFT Speaks 28

A Glimpse of IIFT

By: Ruhi Gupta, Ivanshu Gupta & Shweta Baravani 30

Solution to Wordsworth

By: Somyanshu Arora 32

Strategos | August 2015Fo

cus

The

me

: Th

e R

ise

of

Afr

ica

The recent patterns which have emerged in the global economy which are forcing India to rethinkits brand and image. What has led this evolution and where do we see it going in the future?

By Prince Shaji,

MBA (IB) 2015-17

.

Indian Institute of Foreign Trade 4

“

After the fall of Soviet Union, the world hasseen two decades of moderate peace,engagements and the acceptance of USA asthe sole super power. The global decisionswere centralized in Washington and the finalsay in any global crisis came from WhiteHouse. But the great recession of 2008exposed deep trenches in global economyand provided an impetus to global players tolook towards their neighborhood and solveproblems within. This trend was coupled withthe emergence of BRICS as a major groupingand rise of China as the new hegemonicsuperpower.China, with its huge purchasing power anddeep pockets occupies a major role in globaleconomy now. China is trying to become analternative for USA by engaging more inglobal issues. The engagement of China inAfghanistan and Pakistan should be seen inthis ground. The setting up of AsianInfrastructure Investment Bank (AIIB) is seenas an alternative to the Bretton Woods twins.Despite the resistance from USA, most of thecountries including Europe rushed to join thisbank to make maximum use of China’s hugecash reserves.

Source : IMF report on PPP

China is also in the process of setting upNew Development Bank (NDB) along withother BRICS countries. The bank will beheadquartered in Shanghai, the economiccapital of China and China will providearound 50% of bank’s working capital.These moves represent China’s intention toassert its financial clout and to change thefinancial headquarters from New York toShanghai.

The Evolving Patterns in the Global

Political Economy

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

The projects like rejuvenation of Maritimesilk Route is one among several otherinitiatives of the Chinese government tospread the wings of the Chinese dragonacross the globe. China is also involved in acontinuous tussle with its neighbors Japan,Philippines and Vietnam over disputedislands in South China Sea. The issueaggravated when China encroached intoJapanese claimed islands and set up specialair defense zone over South China Sea. USAbeing a major ally of Japan and Philippinessee South China Sea as a strategic positionand opposes these Chinese assertions.

The docking of US and Chinese ships againsteach other created tensions across the globerecently. The region is also strategicallyimportant because of the presence of hugeoil reserves and all countries want to makethe maximum out of that.

Source: BBC report on Europe economic growth

The tensions in South China Sea seem tobe in an impasse because both fronts don’twant to concede their grounds andprovides a deadlock to diplomats andpoliticians.

One of the other turbulent areas of globaleconomy which poses serious threat to alleconomies is Europe. From the Ukrainiancrisis to the recent Greece debt crisis,Europe has been struggling to keep its footin land. The growth in Europe has beensluggish after the global crisis and this putsserious pressure on the European Uniondespite the fact that most responsibility oftaxation and spending lies with nationalgovernments.

The Ukrainian crisis and annexation ofCrimea stalled the European recovery afterthe economic crisis. The sanctions imposedby USA and European countries on Russialimited the supply of Oil and Natural whichhad a profound impact on Europe.

Economic Growth of Europe

5

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

Strategos – August Edition

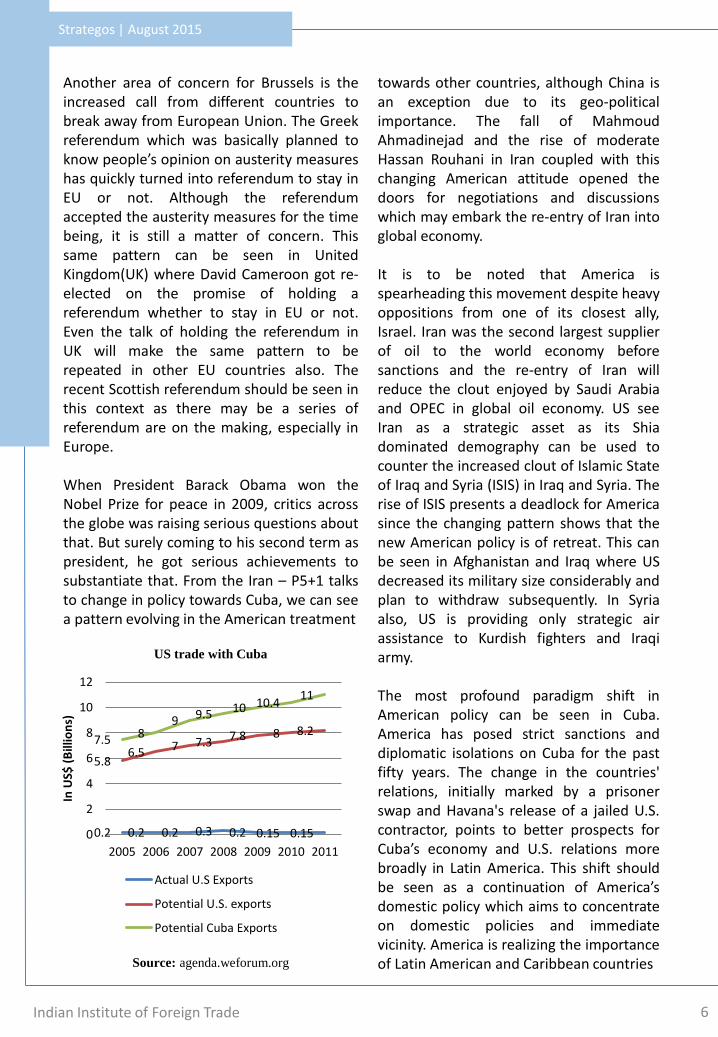

Another area of concern for Brussels is theincreased call from different countries tobreak away from European Union. The Greekreferendum which was basically planned toknow people’s opinion on austerity measureshas quickly turned into referendum to stay inEU or not. Although the referendumaccepted the austerity measures for the timebeing, it is still a matter of concern. Thissame pattern can be seen in UnitedKingdom(UK) where David Cameroon got re-elected on the promise of holding areferendum whether to stay in EU or not.Even the talk of holding the referendum inUK will make the same pattern to berepeated in other EU countries also. Therecent Scottish referendum should be seen inthis context as there may be a series ofreferendum are on the making, especially inEurope.

When President Barack Obama won theNobel Prize for peace in 2009, critics acrossthe globe was raising serious questions aboutthat. But surely coming to his second term aspresident, he got serious achievements tosubstantiate that. From the Iran – P5+1 talksto change in policy towards Cuba, we can seea pattern evolving in the American treatment

towards other countries, although China isan exception due to its geo-politicalimportance. The fall of MahmoudAhmadinejad and the rise of moderateHassan Rouhani in Iran coupled with thischanging American attitude opened thedoors for negotiations and discussionswhich may embark the re-entry of Iran intoglobal economy.

It is to be noted that America isspearheading this movement despite heavyoppositions from one of its closest ally,Israel. Iran was the second largest supplierof oil to the world economy beforesanctions and the re-entry of Iran willreduce the clout enjoyed by Saudi Arabiaand OPEC in global oil economy. US seeIran as a strategic asset as its Shiadominated demography can be used tocounter the increased clout of Islamic Stateof Iraq and Syria (ISIS) in Iraq and Syria. Therise of ISIS presents a deadlock for Americasince the changing pattern shows that thenew American policy is of retreat. This canbe seen in Afghanistan and Iraq where USdecreased its military size considerably andplan to withdraw subsequently. In Syriaalso, US is providing only strategic airassistance to Kurdish fighters and Iraqiarmy.

The most profound paradigm shift inAmerican policy can be seen in Cuba.America has posed strict sanctions anddiplomatic isolations on Cuba for the pastfifty years. The change in the countries'relations, initially marked by a prisonerswap and Havana's release of a jailed U.S.contractor, points to better prospects forCuba’s economy and U.S. relations morebroadly in Latin America. This shift shouldbe seen as a continuation of America’sdomestic policy which aims to concentrateon domestic policies and immediatevicinity. America is realizing the importanceof Latin American and Caribbean countries

6

0.2 0.2 0.2 0.3 0.2 0.15 0.15

5.86.5 7 7.3 7.8 8 8.2

7.5 89 9.5 10 10.4

11

0

2

4

6

8

10

12

2005 2006 2007 2008 2009 2010 2011

In U

S$ (

Bill

ion

s)

Actual U.S Exports

Potential U.S. exports

Potential Cuba Exports

US trade with Cuba

Source: agenda.weforum.org

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

and engaging with them more.

India, being the largest economy amongSouth Asian countries looks to be on thesame track as America, which aims to createa domestic harmony among itsimmediate neighbors. Prime Minister Modi’smove of inviting SAARC leaders to hisswearing-in ceremony and the rejuvenatedimportance of Look East policy should beseen in this context.

Mr. Modi has engaged with all the SAARC andAsian leaders in his first year at office, andprovided an impetus to India’s growing tieswith neighboring countries. Anotherparadigm shift in Indian policy can be seen inemploying the “Soft Power”. Instead offocusing on military clout, countries aretrying to promote their soft powers likedemography, economy and culture. The samecan be seen in China’s efforts to rejuvenateMaritime Silk Route concept.

The patterns emerging in the global politicaleconomy provide considerable questions anddoubts in the mind of any observer. FromChina’s hegemony in South China Sea toAmerica’s Cuban policy, a pattern is evolvingacross the globe towards immediate vicinity.In the after drop of global economic crisis,countries are concentrating on theirdomestic issues and are designing theirexternal policies to suit domestic policies.Another pattern can be seen in theemployment of military power. Countries areincreasing their arsenal to intimidate theirneighbors towards aligning to their softpower policies.

The Soft Power provides an opportunity forevery country to showcase its culture andheritage, and claim its part in the globalizedworld. Another pattern is the recedingimportance of global organizations.

Organizations like the UNO and WTO are

becoming ceremonial bodies whereasregional and economic groupings like BRICSare gaining stronghold. The next decadepresents a set of puzzling questions toobservers also. Is the US influence acrossthe world receding and whether China isgoing to overthrow US as the newsuperpower? Is European Union going toremain intact or whether we are going tosee the beginning of the end for EU?

But one thing can be concluded from allthe political and economic proceedingsacross the globe. The next decade’s winnerwill be decided based on the contestants’economic clout, not by military clout.

7

Strategos | August 2015In

war

d In

tro

spe

ctio

n

Taking a historical perspective to understand how our political scenario came to be what it istoday. The various key events and how they effected India, and what can we expect as we moveforward.

Indian Institute of Foreign Trade 8

By Rahul Khandelwal & Ankit Pathak,

MBA (IB) 2015-17

The Paradigm Shift in Today’s

Geopolitical Climate

A World Economy“Not everything that can be counted counts,and not everything that counts can becounted” - perhaps Einstein had differentmotives while articulating this statement, buthardly anything else can capture the essenceof global political economy more succinctly.Before the industrial revolution in theeighteenth century, the world was afragmented assortment of various factionsholding a chunk of power in various dividedand often isolated regions. Although somepowers had a relatively larger share ofinfluence, like the Roman Empire, theirimpact on global economics was almostnegligible. But the industrial revolutionheralded the dawn of a new era where theequations of power went through a paradigmshift and a uniformity was found to beemerging in the global economics trends.Britain emerged as the driver of globaleconomy along with certain other Europeancontemporaries such as France and Portugal,but they were largely overshadowed byBritain’s towering influence driven by theeconomic advantage it gained throughcolonization.

A Tale of Two SuperpowersThe sun finally set on the British empireafter the second World War, giving rise to abipolar world with the US and Soviet Unionfighting it out to take the helm, vying forpower and influence over the globaleconomy. The result was a long struggle forpower between the two superpowersaspiring to create a unilateral world. The‘Cold War’ lasted nearly four decades withthe USA emerging as the new world leader.It resulted in an arms race, with both thegovernments incurring a staggering militarycost of $6316 billion during 1945-86. Theperiod also saw both the nations formingmultiple coalitions and vying for influenceover the non-aligned nations.Many countries made significant gains outof their alliance with these twosuperpowers. One such event was theconsolidation of Europe, which the US sawas a necessity to validate its status as theforemost nation in the world. The BrettonWoods Conference, held in July 1944,promulgated a formal world economicstructure which intended to regulate theworld economic affairs. The Bretton Woods

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

Institutions, namely the World Bank and theInternational Monetary Fund, gave the UScurrency, which was linked to a goldstandard, a significant position in the worldeconomy. Due to its influence in the westernhemisphere and a large reservoir of gold, USemerged as the dominating member of theseinstitutions. The developing nations hugelyrelied upon these institutions to fund theirgrowth, and thus had no option but to keepon the right side of the US.Thus the US remained the sole superpowerand the world economy revolved around it. Itused tools such as economic sanctions andmilitary actions for coercion. Although it haddetractors, none of them had the means toconfront the ‘Big Brother’, and thus itmanaged to have a commanding influenceover the world economy.

A Paradigm ShiftWith prolonged wars in the Arab region andthe recession of 2008, the US is struggling tomaintain its dominance. Although it stillenjoys the status of being the most robusteconomy, it isn’t the sole runner anymore.The modern world is awash with a number ofnations emerging to be powerful, botheconomically and politically. Any discussionabout the modern world economy or politicalshifts would be incomplete without themention of China. With a GDP of $10.36trillion, as per the World Bank estimates,China has undoubtedly been the greatestthreat to US hegemony.Despite its relentless efforts, US has failed to

Source: Angus Maddison, IMF

Reducing US Share of Global GDP

have a significant presence in Asia, primarilydue to geographical disadvantage, and alsobecause of the emphasis of major countriessuch as India and China on sovereignty. Dueto its close involvement in the Arab regionand as a facilitator of the Arab Spring, itbecame essential for the US to have a basein Asia. It relied primarily on Pakistan tofulfill this necessity.The Arab spring and the rise of Chinaresulted in a major shift in the worldeconomic affairs. Having proved its mantleto the world by putting an exquisite show inthe Beijing Olympics in 2008, China markedits ascendency in the world political andeconomic spheres. The involvement of theUS in the Arab region also helped China, asthe war took a toll on the US economy andChina maneuvered the circumstances to itsown advantage.As the US gradually shifted towards aconsumer based economy, it boosted theChinese manufacturing sector, which madebillions on foreign exchange. Riding high onthe wave of manufacturing, China became acynosure for all major brands to set up amanufacturing plant. Be it Apple, Sony orSamsung, the product had to travel to Chinaat some point or the other of itsmanufacturing cycle. As it was a closedeconomy for the better part of the previouscentury, the world was unaware of thedepth of Chinese coffers and as it started tospread its wing in the twentieth century, ittook the world by surprise.

Modern equations and India –For the greater part of its existence, Indiahas been a mere spectator of the worldeconomic affairs. Even during the times ofcold war, it chose to remain neutral,although it was believed to have a softcorner for the Russian camp. As the clout ofIndia grew, the expectations also keptsoaring. As the Chinese dominanceaugmented, many smaller nations looked toIndia for assistance. The contentious issuesin Asia, be it the South China Sea or

9

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

the Tibet region, drove many nations toapproach India.Realizing the need of the hour, India hasstarted heeding to the pleas and its attitudetowards the region has changed. It hasstarted to play a more active part in worldeconomics and is well on the path to claim itsinfluence over the South Asia region. Thehuge investment in Afghanistan and abilateral deal with Japan of over $35 billiondollars investment over the next five years.Multiple visits by the current Indian PrimeMinister, Narendra Modi, to a multitude ofnations like Singapore, China, South Koreaand Russia.

The Road AheadWith the formation of BRICS, the developingnations have claimed their stake over theworld economy. The changing powersymmetric can be observed from the growinginvolvement of G20 in the economic affairsand the enthusiasm shown by the westernnations to become a founding member of theAsian Infrastructure Investment Bank (AIIB).The failure of the United States to impose arestriction on the developing economies onthe issue of carbon emissions can beinterpreted as a sign of its declininginfluence. The 21st century has seendeveloping nations such as India, Brazil andSouth Africa lobby over their fundamentalissues and standing strong againstinternational organizations. The recentdispute between India and WTO regardingthe exceeding of subsidy limit by India wasanother sign of the growing clout of thesenations. While there can be minorreverberations in the evolving path ofemergence of a multilateral world, such asthe recent stock market crash of China, it willhardly have any long lasting effects as Chinahas hardly around one-third of its GDPallocated for trading, as against more than100% in most of the developed nations.

The leaders of the BRICS countries in the

Brazilian city of Fortaleza at the launch a BRICS

development bank.

As Russia has also avowed to strengthen itsalliance with China and India, especiallyafter the Ukraine conflict, the center ofpower appears to be shifting east. But it’sstill too early to make any predictions asthe United State still remains the topeconomy with a GDP of over $15 trillionand an unmatched military structure. But itcan surely be concluded that it enjoys a lotless influence than it did earlier. It realizedthe hard way that economic sanctions andmilitary adventurism aren’t the solutions tothe global issues and perhaps that’s thereason it went the democratic way toobtain a nuclear agreement from Iran.The modern world is open to a lot morepossibilities with every country perceivinga chance to prosper in the emergingeconomic and political trends. China can beseen to emerge out as a clear leader in theroad to ascendency but at the same timeother important players, such as Russia,India and Brazil can’t be ignored. There aregoing to be a lot more interesting andsurprising developments and the worlddynamics are going to be transformed in abig way.

10

Strategos | August 2015

Dividing the problems faced by businesses in a global scenario into six different parts, and analyzing how each of them present their own challenges and problems.

By Rupam Jhawar & Nikhil Padmalayam,

MBA (IB) 2015-17

Indian Institute of Foreign Trade 11

The Struggle to Adopt to the

Evolving Global Economy

Businesses have truly gone global. A farmerin Argentina grows soya using Americancompany Monsanto’s genetically modifiedseeds, which are then shipped over to Chinain a carrier built in Korea and registered inPanama. Once the shipment reaches China itbecomes the feed for pigs which are thenbutchered for meat to be sold in countriesaround the world.

72.18 73.48

87.25

77.3

60

65

70

75

80

85

90

2011 2012 2013 2014

in Trillions of USD

Not only businesses but consumers havealso gone global with increased travelacross geographies, more exposure toglobal products, e-commerce etc.The demands of consumers have alsosubsequently changed over the past fewdecades.But here we will be limiting discussion tothe challenges faced by businesses in amore global and connected world.

Global economy has seen a lot of changesover the last century. Prominent eventssuch as the Great Depression, World Wars,Cold War, and Fall of Soviet Union etc. havechanged the way business is done.Globalization has been a boon for manybusinesses but it has also brought withitself a host of new challenges that theseglobal organizations have to face.We have categorized these challenges in sixbroad categories and have proposed a newmodel, P5S Model here:

. Source: CIA Fact-book

Graph representing World GDP data showing that

although the world is growing, events taking place

in one part of the world affect others too

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

Challenges

People

Portfolio

Procure-ment

Place-ment

Policies

Synergy

The P5S Model representing challenges faced by businesses in the modern World

25

17

21.2 21

0

5

10

15

20

25

30

2011 2012 2013 2014

Att

riti

on

Rat

e in

%

Attrition Rate in Indian IT Industry

Acquiring the right talent and retaining ithave become important for businesses, dueto the huge costs involved in selecting,training and acclimatization of employees.Uniform method of appraising a workforcespread across different geographies andcultures is also difficult.

Portfolio: It refers to the range of productsand services that a company offers to itscustomers.

People: Human Resources are no doubt themost valuable resources available to abusiness. It is the resource which is essentialfor proper utilization of all other resources.People are involved in all stages of a businessright from inception, planning, procurement,production to the last stage of distributionand taking customer feedback. In such ascenario it becomes all the more importantto maintain the human resources of yourorganization in the best shape possible.Employee loyalty and attrition have becomemajor issues for certain companies andindustries such as Indian IT Industry withattrition reaching levels as high as 25%.

Graph representing the Attrition Rate in Indian IT Industry. Source: Business Today

Changing expectations of the customer is atricky business in this dynamic world withtrends and preferences changingconstantly. A company might spendmillions developing a product and morepromoting it, but if that product doesn’tclick with the customer, then theenormous amount of time, capital andresources spent would go down the drain.Customizing products and services to suitreligious, social and personal preferencesof the customer has to be focused upon bycorporations. McDonald’s had to ditch ittrademark hamburgers in India,considering people’s religious sentimentsattached to cows and go for developing amenu suitable for the vegetarian palette ofIndian consumers. Similarly, Audimistakenly thought that male Germandrivers would take directions from a femalevoiced navigation system in its cars. Aproduct popular in Australia, say Foster’sbeer, may not be popular in India.

12

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

Demographics and psychometrics play asignificant role in determining the success ofany product or service. Catering to differentpopulations may leave you with ahumongous portfolio, like Coca-Cola, whichsells around 3000 different types of productall over the world. Managing the quality,production and distribution of such a hugeportfolio may prove to be challenging andcostly.

Procurement: Procurement of raw materialsis essential for every business. Formanufacturing firms, raw materials may be inthe form of cotton, steel, oil etc. while forservice firms it might be in the form ofcomputing power, talent etc.Ease and cost of procurement varies withgeography and industry of the procurer andsupplier, as well as demand and supply ofthat raw material or component. Some typesof raw material may only be available or be indemand only during certain periods of theyear. Procurement teams have to deal withdifferent government controls andregulations in various countries.Environmental disasters or suddenregulations may threaten the continuity ofproduction leading to increased cost ofproduction. In order to manage such risk, acertain level of inventory must bemaintained, which throws up the challengeof determining an optimum level of inventoryand methods to store raw materials topilferage, damage, spoilage and wastage.Big corporations such as Airbus Group, ordersits supplies from thousands of suppliersbased out of more than 100 countries. AnAirbus A380 consists of 4 million individualcomponents, produced by 1500 differentcompanies spread over 30 differentcountries. The absence of even a simplecomponent such as a particular type of boltcan halt the assembly line and delay an orderworth millions of dollars. The wings andengines for an A380 are made in England, tailand fuselage are made in Spain

and Germany.All the parts are then sent to France forassembling by ship or road. Building andmaintaining such enormous supply chains,dealing with hundreds of vendors and atthe same time keeping up with a strict timeschedule poses a huge challenge forcorporations around the world.Cartelization and monopolization of certaincommodities such as the one of rare earthmetals done by China around 2010 willpose challenges to manufacturers aroundthe world. Similar procurement challengesawait businesses around the world asconsumption increases and supplybecomes scarce. Securing theirprocurement chain has become a hugecause of worry for many businesses andhas probably been discussed in a lot ofboardrooms around the world.

Placement: Consumers now are not whatthey used to be 2 decades ago. Today’sconsumer is more alert, aware andconscious of the products he/she buys.Increased competition and globalizationhave flooded the markets with largenumber of products. In this cut-throatcompetition, it becomes important tounderstand consumer psyche and how tobest position the product in the customer’smind. Apart from placement of yourproduct in the consumer’s mind, it is alsoimportant that it is within his/her reach.Hence distribution becomes important sothat the consumer is able to buy yourproduct. As penetration of the productincreases and you are able to target peoplein the untapped markets, even there theplacement of your product and service is achallenge. The challenge before a biscuitmaker’s marketer for instance is how to dohis company’s cream biscuit’s placement inyour nearby supermarket shelves in orderto maximize sales and make your creambiscuits stand out from 20 other equallygood brands available in the market.

13

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

Policies: Policies framed by external agentssuch as governments, regulators andinternational bodies as well as the onesformed by internal boards, committees andmanagement affect the working andactivities of an organization. These policiesmay affect any particular part of a businesslike HR policies, products, productionprocesses etc. or even the structure andbusiness model of the business. For instance,increasing environmental regulations mayforce businesses to close down a particularproduction center. In countries, where lawscan be changed by the government as andwhen they please, it is very risky to set-upfacilities.Legal and regulatory tussles regardingtaxation and product quality have becomecommon even in India, with notices forretrospective taxes worth billions of dollarsbeing sent to companies, for exampleVodafone. Policies on Intellectual PropertyRights, pirating and digital content also varyin different countries leading to huge lossesfor some businesses.

14.83 T

17.67 T

16.69 T

17.18 T

14,500.00

15,000.00

15,500.00

16,000.00

16,500.00

17,000.00

17,500.00

18,000.00

2010 2011 2012 2013

Bill

ion

s

Source: WITS

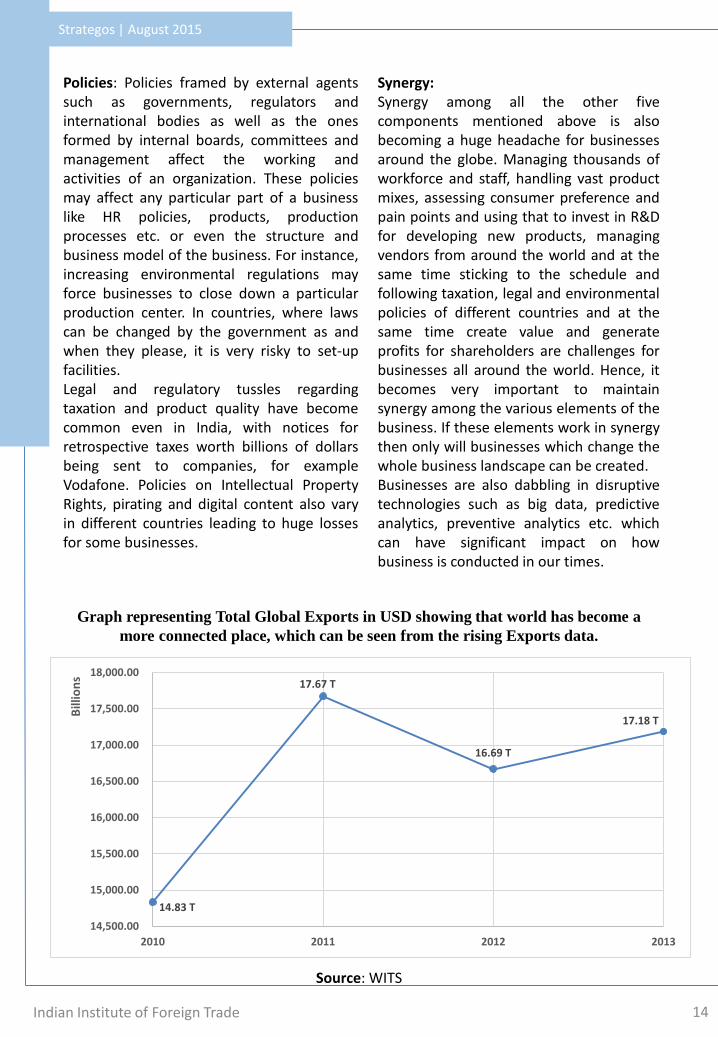

Synergy:Synergy among all the other fivecomponents mentioned above is alsobecoming a huge headache for businessesaround the globe. Managing thousands ofworkforce and staff, handling vast productmixes, assessing consumer preference andpain points and using that to invest in R&Dfor developing new products, managingvendors from around the world and at thesame time sticking to the schedule andfollowing taxation, legal and environmentalpolicies of different countries and at thesame time create value and generateprofits for shareholders are challenges forbusinesses all around the world. Hence, itbecomes very important to maintainsynergy among the various elements of thebusiness. If these elements work in synergythen only will businesses which change thewhole business landscape can be created.Businesses are also dabbling in disruptivetechnologies such as big data, predictiveanalytics, preventive analytics etc. whichcan have significant impact on howbusiness is conducted in our times.

Graph representing Total Global Exports in USD showing that world has become a

more connected place, which can be seen from the rising Exports data.

14

Strategos | August 2015

Analyzing the current global scenario by focusing on the four key challenges that dominate the business environment today, and what are their impacts on a global scale.

By Snigdha Srivastava,

MBA (IB) 2015-17

Indian Institute of Foreign Trade 15

Challenges for Businesses due to

Transformations in the Global Economy

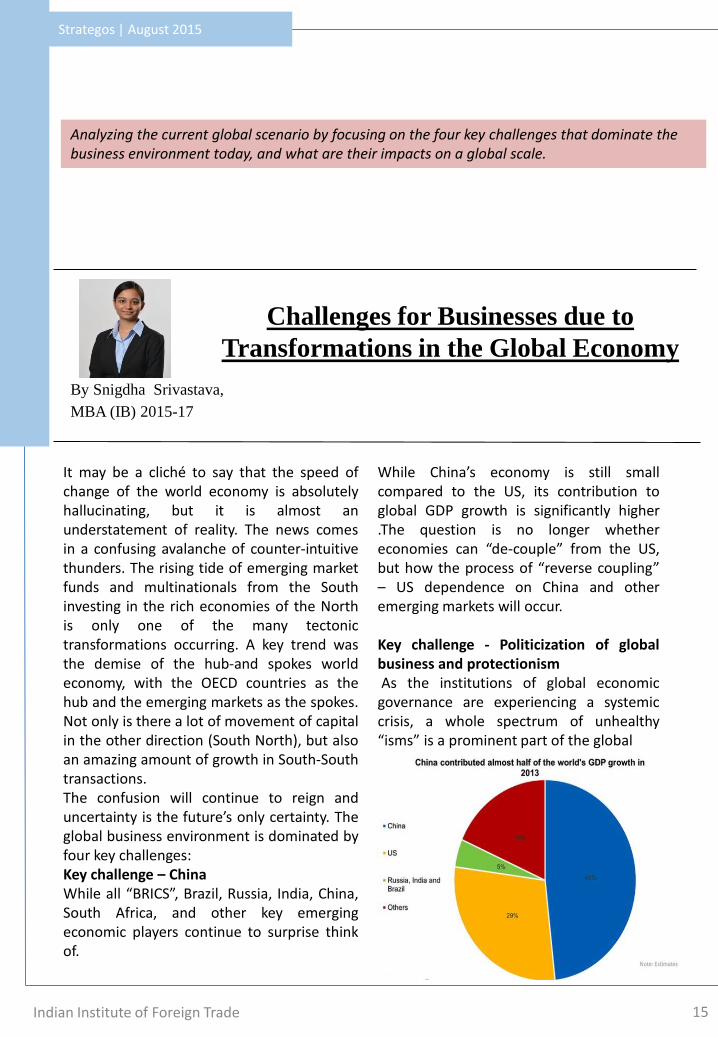

It may be a cliché to say that the speed ofchange of the world economy is absolutelyhallucinating, but it is almost anunderstatement of reality. The news comesin a confusing avalanche of counter-intuitivethunders. The rising tide of emerging marketfunds and multinationals from the Southinvesting in the rich economies of the Northis only one of the many tectonictransformations occurring. A key trend wasthe demise of the hub-and spokes worldeconomy, with the OECD countries as thehub and the emerging markets as the spokes.Not only is there a lot of movement of capitalin the other direction (South North), but alsoan amazing amount of growth in South-Southtransactions.The confusion will continue to reign anduncertainty is the future’s only certainty. Theglobal business environment is dominated byfour key challenges:Key challenge – ChinaWhile all “BRICS”, Brazil, Russia, India, China,South Africa, and other key emergingeconomic players continue to surprise thinkof.

While China’s economy is still smallcompared to the US, its contribution toglobal GDP growth is significantly higher.The question is no longer whethereconomies can “de-couple” from the US,but how the process of “reverse coupling”– US dependence on China and otheremerging markets will occur.

Key challenge - Politicization of globalbusiness and protectionismAs the institutions of global economic

governance are experiencing a systemiccrisis, a whole spectrum of unhealthy“isms” is a prominent part of the global

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

business fare: economic nationalism,mercantilism, bilateralism, preferentialism,unilateralism and protectionism. America –and increasingly also EU– protectionist sabre-rattling vis-à-vis the Chinese has becomemore threatening. As the temperaturemounts on one side, retaliation can beexpected on the other. Backlashes in onedirection generate backlashes in the other. Ina highly volatile global political andideological environment, companies can alsoexpect unpredictable events in which theymay find themselves to be “innocentvictims”.

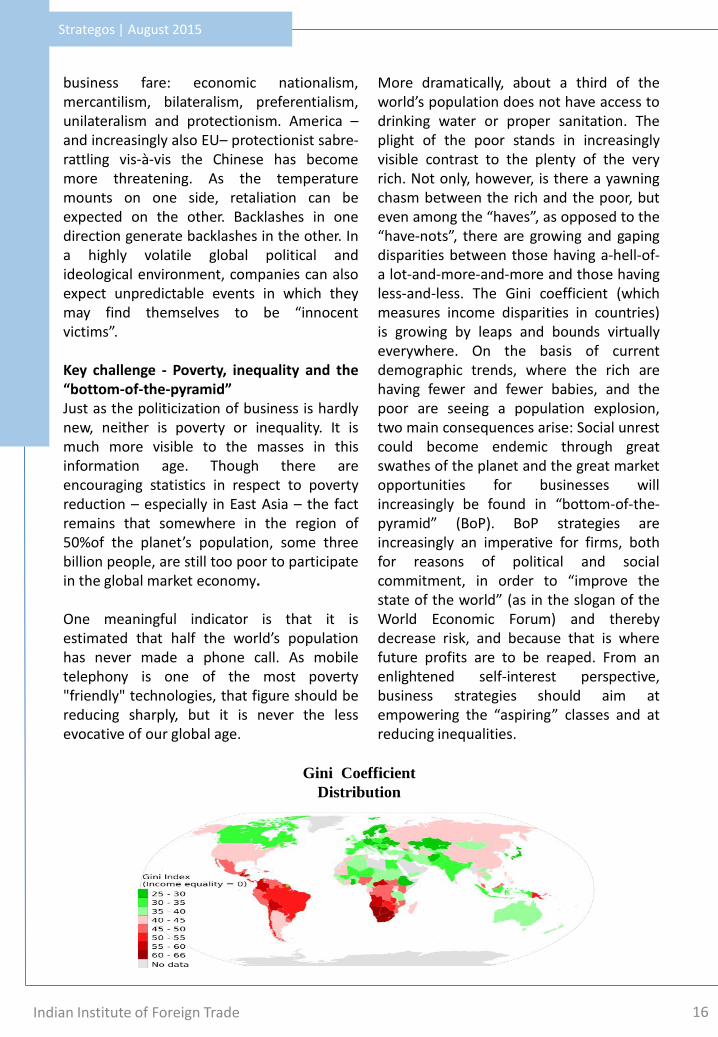

Key challenge - Poverty, inequality and the“bottom-of-the-pyramid”Just as the politicization of business is hardlynew, neither is poverty or inequality. It ismuch more visible to the masses in thisinformation age. Though there areencouraging statistics in respect to povertyreduction – especially in East Asia – the factremains that somewhere in the region of50%of the planet’s population, some threebillion people, are still too poor to participatein the global market economy.

One meaningful indicator is that it isestimated that half the world’s populationhas never made a phone call. As mobiletelephony is one of the most poverty"friendly" technologies, that figure should bereducing sharply, but it is never the lessevocative of our global age.

More dramatically, about a third of theworld’s population does not have access todrinking water or proper sanitation. Theplight of the poor stands in increasinglyvisible contrast to the plenty of the veryrich. Not only, however, is there a yawningchasm between the rich and the poor, buteven among the “haves”, as opposed to the“have-nots”, there are growing and gapingdisparities between those having a-hell-of-a lot-and-more-and-more and those havingless-and-less. The Gini coefficient (whichmeasures income disparities in countries)is growing by leaps and bounds virtuallyeverywhere. On the basis of currentdemographic trends, where the rich arehaving fewer and fewer babies, and thepoor are seeing a population explosion,two main consequences arise: Social unrestcould become endemic through greatswathes of the planet and the great marketopportunities for businesses willincreasingly be found in “bottom-of-the-pyramid” (BoP). BoP strategies areincreasingly an imperative for firms, bothfor reasons of political and socialcommitment, in order to “improve thestate of the world” (as in the slogan of theWorld Economic Forum) and therebydecrease risk, and because that is wherefuture profits are to be reaped. From anenlightened self-interest perspective,business strategies should aim atempowering the “aspiring” classes and atreducing inequalities.

Gini Coefficient

Distribution

16

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

Key challenge – A green agenda

The environment issue is another radicalrecent transformation. Today, environment isa key policy and an increasing strategypriority. But while the public policy process –in environment as in so many other issues –is advancing at a snail’s pace, increasingly theagenda is being driven by visionarybusinesses.

The term “sustainable” has becomeintegrated in the rhetoric, strategy andconsciousness of business. As with povertyand inequality, it is probably the case that theprivate sector may have the mostcontribution to make in the face of theenvironmental challenge through innovativegreen technologies and business practices.Corporations –not only in the industrializedcountries, but also in developing countries –are much more susceptible to environment-driven external perceptions and pressures.Policy makers must balance the need toencourage growth with their responsibility tolook out for the public welfare as newtechnologies reshape economies and lives.

17

Strategos | August 2015

Indian Institute of Foreign Trade 18

Source : E&Y

Strategos | August 2015

By Saurabh Kumar,

MBA (IB) 2015-17

Indian Institute of Foreign Trade 19

The Need for Repositioning Brand India

Through its history, India as a country hasseen itself being viewed in a veritable bedlamof perceptions across the globe. In the 40sand 50s, we were mostly perceived as anunstable experimentation of the newlyfounded idea of democracy, on the verge of aviolent disintegration into 100 differentwarring states. 50s came and went but Indiatrudged on and the tags associated melloweddown a bit, never quite gone.

A different brand image emerged throughthe 60s when a series of natural calamitieshit India and widespread hunger led to animage of a destitute former colony thathad to be aided. Till 90s our imagestabilized as an inward looking economyridiculed as a ‘lumbering elephant’ tohighlight the Hindu rate of growth that wecould manage through extensive planning

Source: Reputation Institute Reptrack™

A brief view of how the image of India has change over the years and the current picture that isdenoted by our country on the international platform, analyzing the same on the external andinternal fronts and steps taken towards repositioning brand India.

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

19

But come the era of liberalization, BrandIndia was revitalized to an entirely differentform. A continuous growth rate of 7-8% through 2000s coupled with targetedslogans of ‘India Shining’ pushed through animage of a rising power. And now we havecome to 2015. A series of sub-par growthyears during the ‘Policy Paralysis’ during UPA-II government dimmed our prospects a littlebit, but the new NDA government has comein full majority on the back of a ‘growth’agenda and is taking the task of repositioningBrand India as a high priority agenda.

Current ScenarioBut before going all out to improve ournation’s outlook, we have to analyse whatexactly it currently is like:

According to a study conducted by theReputation Institute which sampled datafrom more than 48,000 consumersworldwide to put together a perception indexRepTrack in July 2015, India is ranked 33rd outof 50 largest economies of the world with aPerception index of 52.7 as compare to theglobal index average of 56.3

A 2014-published report by TransparencyInternational report on CorruptionPerceptions Index also ranked India at adismal 85 out of 175 nations. According to TI,India improved slightly from the past year,with a score of 38, compared to 36 in 2013.

Corruption

Perceptions

Index

Source:

Transparency

International

Its ranking though an improvement fromlast year's 94th was still lower thannondescript sub-Saharan countries such asBenin and Burkina Faso.

One of the most highlighted and quotedfigures- the Ease of Doing Business Indexreleased by World Bank ranks India 142nd in179 countries of the world compared to91st for China

Apart from statistics, too we have hadincidents like ‘Nirbhaya Rape Case’ inDecember 2013 and subsequent eventswhich have pulled down the affinity offoreign tourists as well as our own citizensto visit the Indian Heritage Sites pullingdown revenues

A dismal picture of India does come out ofthese facts and figures. But how exactly dothey affect India’s growth prospects. Let’slook at the importance of improving India’sbrand both on External and Internal fronts:

External NeedsFor growth to happen, we needinvestments. Global Investment inflowsreached $1.2 trillion last year and isprojected to grow by 15-16% this year. Forcapturing these investments, we need toportray ourselves as a lucrative businesshub.

20

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

After all, who wants to invest in a sub-parspot when other regions of the world likeAfrica and South East Asia are gleaming inglobal spotlight?Also, the tourism industry which is growingby 3-4% annually to reach $1.135 billion in2014 is largely dependent on the country’sperception index. To tap into this industry,India must improve its perception among thecustomers of its Tourism Industry, which isincidentally, the entire globe. The correlationbetween the perceptions of a country to thetourist footfalls in the country is estimated tobe 0.7 (which is quite high).The international trade volume is forecastedto grow 4% annually of the Global GDP. Aswe all know, trade between nations boomsonly when they have mutual affinity (the lowvolume of India-Pakistan trade which flies inthe face of trade theories is a point in case).This gives us another important reason toimprove our global brand image.

Source: Economic Times

Source: World Bank

Internal NeedsOne of the most idiosyncrasies of IndianGDP breakdown has been thedisproportionate GDP share of the servicessector with respect to its share inemployment.This has caused massive income disparitiesin the Indian economy with majoritywealth being concentrated in the hands ofa minority Services Sector. The issue canalso have severe repercussions in the lawand order situation if not addressed.The disparity has its roots in the IT boomwhich happened in late 90s before ourIndustrial sector could pick up. Themajority of talent went into the servicessector in search of better incomeopportunities and Indian IT was hailed allover the world as being extremelytalented. The brand of Indian servicessector may have dwarfed and undercut themanufacturing growth at that time. Lowgrowth in the secondary sector shareessentially meant that a lot of Indianpopulation remained in Primary sectors,

51%

26%

23%

Employment Share

Primary Secondary Tertiary

18%

26%56%

GDP Share

Primary Secondary Tertiary

21

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

disguised as being employed. To maximizethe potential of the population currently inthe primary sector, India needs to rebranditself from being a services hub to amanufacturing hub so that the industry getsenough spotlight to exploit the advantage ofour working population.The next imperative to rebrand ourselvescomes, for a change, from one of ourstrengths rather than a weakness. Themedian age of our population is 27 years.The enormity of this statement may0sometimes be lost in its simplicity. Forcomparison, US’ median age is 36 years.China is 37 years old on a median scale. Indiahas one of the youngest populations in theemerging nations of the world, the youngestin BRICS.And youth signifies change. This youth needswork opportunities. It is in the process of orhas already shed the age old limitations ofthe Indian cultural history. It has never seenthe pangs of destitute poverty. In such anelectric atmosphere, the country needs to re-brand itself to accommodate, if nothing else,its own potential.

Perceptions Tracking Economic Analysis Action review and Planning

The Reputation Management Flowchart

The InitiativesAs stated earlier, the government is alreadytreating the brand repositioning as a highpriority agenda. The India Brand EquityFoundation (IBEF), a public-privatepartnership between the CommerceMinistry and CII aims to effectively presentthe India business perspective and leveragebusiness partnerships in a globalisingmarket-place. IBEF is already in fulloperation demonstrated by its successfulrepresentation of India in business summitsat Hannover Messe and Davos in Germanythis year

Make In IndiaAnnounced by Prime Minister Modi fromthe ramparts of the Red Fort in hisIndependence Day Speech on August 15,2014, Make in India has been the centre-point of all branding activities of thegovernment since its inception.It has focused on resolving various issues ofcontention including Single WindowClearances, Intellectual Property Rights,electronic databases in place of manualbook-keeping, fast-tracking of industrial

22

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

projects along with revitalizing public moodthrough slogans of “Zero Defect, Zero Effect”initiative. Some of the projects launchedunder this are: Work on 5 smart cities in progress as a partof the Delhi-Mumbai Industrial Corridor Chennai-Bengaluru Industrial Corridor:master Planning for 3 new Industrial NodesNorth-eastern part of India to be linked withother ICs in cooperation with Japan etc.However, some complications remain due tothe unresolved policies of Land Acquisition,GST and the general mayhem which hasbecome the norm of the Parliament thesedays. Further, the sensitive issues such aswomen’s safety still needs to be addressedregularly in the mass communicationchannels by the authorities.All in all, the success of rebranding Indiarevolves around the tenacity of thegovernment to resolve these logjams and thegeneral outlook of the masses to grow andaspire.

23

Strategos | August 2015In

war

d In

tro

spe

ctio

n

India is outperforming itself year after year. How Make in India campaign will give a boost to the all-round growth of the nation; initiatives being taken and the road ahead.

Indian Institute of Foreign Trade 24

By Diganta Sarkar,

MBA (IB) 2015-17

Opportunities for India in Today’s Globalized World

India currently ranks as the seventh-largest inthe world in terms of nominal GDP, and it isthe third-largest in terms purchasing powerparity (PPP). It is one of the G-20 majoreconomies, a member of BRICS, anda developing economy with approximately7% average growth rate for the last twodecades. India's economy became theworld's fastest growing major economy fromthe last quarter of 2014, replacing China. Theabundance of natural resources, theavailability of cheap labour, and a renewedoutlook towards the global economy underan outspoken Prime Minster has boosted theIndian economy to quite some extent in thelast year. Even according to the IMF, theIndian economy is predicted to be on anupward trend; and the country alsotopped World Bank’s growth outlook for theyear 2015-16 for the first time with economyhaving grown 7.3% in 2014-15 & expected togrow at 7.5-8.3% in 2015-16.Keeping this in mind itself, the newly-founded government under the leadership ofMr. Narendra Modi has pioneered the visionof Brand India as the way the country isprojected

to the world investors, for attracting capitalinflow into the country. The venture usesthe country as a huge market for productsand services, and highlights its advantagesto segregate itself from the globaleconomy; and portrays the country as alucrative destination for future businessfoundations and partnerships. The Indianforeign policy for the last one year hasbeen as such, so as to foster partnershipswith most of its neighbouring nations andthe other powers of the world; and also tocurb the growing Chinese influence in theIndian sub-continent itself. The visits toJapan have seen major partnerships beingstruck up in terms of technology, andbuilding towards the upliftment ofinfrastructure in India; with FDI inflowbeing as high as 35 Bn in US$. The TokyoDeclaration for Japan-India SpecialStrategic and Global Partnership that Mr.Modi signed with Japan's Prime MinisterShinzo Abe could help alleviate India’sissues to a great extent. Mr. Modi also re-kindled the country’s partnership withRussia at the early stages of his tenure,opening up new pathways for inflow of

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

investment, and trade in Defence, RenewableEnergy (mainly nuclear), and othercommodities. His visit to the USA not onlyuplifted the status of the country as a whole,but also fostered action towards resolving ofthe long-standing disputes over the NuclearNon-Proliferations Treaty (NPT), andattracted further investment inflow to India.In order to sustainably direct these capitalinflows towards their proper channels, and tofoster the employment scenario and GDPscene of the country as a whole, the conceptof “Make in India” was brought in.The Make in India campaign came intobearing on 25th September 2014; with thepurpose of encouraging companies tomanufacture their products in India; therebyincreasing both the GDP and the tax revenue.What Make in India has tried to do is re-position the image of India from a red-tapeprone, bureaucracy-heavy, unfavourable-for-business nation; to one which is much moreconducive for the establishment of newventures, by highlighting its ample resources,both natural and human. It is supposed tocreate more industries and bring in bettertechnological innovation, which in turnwould generate more jobs and income to thegovernment; and hence devise a mechanismfor an all-round progress of the nation.

It was mainly focussed on 25 sectors of theeconomy for job creation and developmentof skills – automobiles, chemicals, IT,textiles, aviation, tourism, renewableenergy, bio-tech and electronics, to name afew.Under the initiative, brochures on thesectors and a web portal was released;foreign equity caps were relaxed; and theapplications for licenses were madeavailable online, with their validityincreased to three yearsThe Cabinet allowed a 49% FDI in theDefence sector, up from 26%; and 100%FDI, up from 0%, in Railways Infrastructurein August, 2014; with a view to bringingdown the level of military imports•Timelines were defined for all clearances;and Central and State governments couldprovide exemptions from certain rules andregulations related to labour, environmentetc. subject to the fulfilment of particularconditions•Interest towards the cultivation of GreenTechnology and Practices was alsoinculcated by schemes like:5% interest in reimbursement & 10%capital subsidy for the production ofequipment/machines/devices forcontrolling pollution, reducing energyconsumption, etc.A 10% one-time capital subsidy for unitspractising zero water discharge

10.3%

6.6%

5.1%

6.9%

7.4%

7.5%

0.0% 5.0% 10.0% 15.0%

2010

2011

2012

2013

2014

2015 (projected)

Growth

Source: The World Bank

The Great Indian GDP Growth

7.74

12.4

100,000

150,000

200,000

250,000

0

5

10

15

Budget Allocated (in Rs. Crores)

Growth Over the Previous Year (%)

Source : idsa.in (Institute for Defence Studies and Analyses)

India’s Defense Budget

25

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

In one of the recently concluded defencedeals as well -- the Rafale fighter jet project –France will need to spend 50% of thecontract value, almost four billion dollars, asinvestments in the Indian defence andaerospace sector. The Defence MinisterManohar Parrikar said that the Rafale jetproject will "unleash Make-in- India".Parrikar also said that with India buyingaround 36 Rafale jets for now, governmentsavings on this project is likely to be up Rs60,000-65,000 crore. Such savings, whentaken in at a more holistic level, wouldaccount for a much greater amount in thecountry’s savings.But, no talk of the economy of India couldever be complete without a discussion on theservices sector of the country, which hasplayed a major role in re-shaping its imageand economy. India had one of the fastestgrowing service sectors in the world, with anannual growth rate of above 9% since 2001;contributing to as much as 57% of the GDP in2012-13.It has become a major exporterof IT services, BPO services, and softwareservices, with $167.0 billion worth of serviceexports in 2013-14. It is also the fastest-growing part of the economy, and the ITindustry continues to be the largest privatesector employer in India.Another interesting thing has been theskyrocketing desire amongst the country’syouth to establish start-ups and individualbusinesses. India is the fourth largest start-uphub in the world, with over 3,100 technologystart-ups in 2014-15. Companies like Flipkart,Snapdeal, Ola, etc. have been the top choicesfor many of the students graduating out ofpremier institutions like IITs, NITs, and IIMs.They have been giving established globalplayers like Amazon, eBay, etc. a run for theirmoney; and what a close shave it is turningout to be!India also has the second largest Diaspora inthe world. The overseas Indian communityestimated at over 25 million is

spread across every major region in theworld.In spite of all this, scenes are notnecessarily very colourful. India stilllanguishes at the 142nd spot in the “Ease ofDoing Business” nations in 2015; and thered tape and bureaucracy surroundingbusiness matters hasn’t been extinguishedcompletely.However, with all that has been going on torepel that; and with the RBI cutting interestrates to bring in greater amounts ofinvestments into the country; as well as thefall in the oil prices, we hope that India canraise itself as a major player in the globaleconomy, and portray itself as a majorsuperpower.

26

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

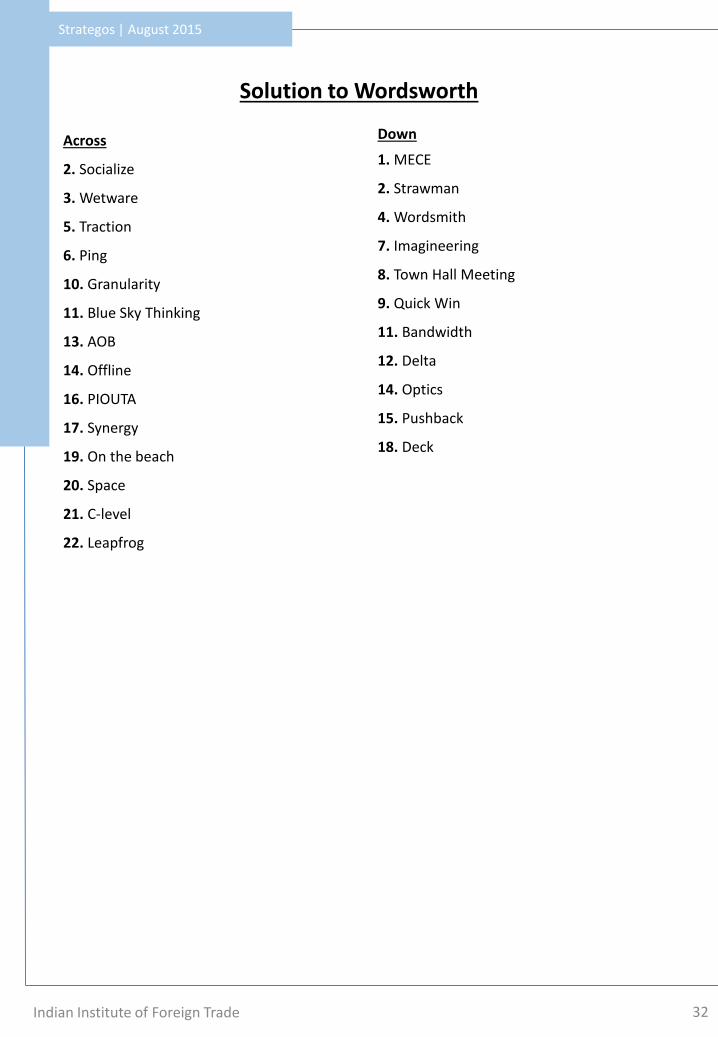

WORDSWORTH

Across 2. Share a document or plan within an organization3. A human-based solution5. A term to measure performance6. To follow-up11. A special line of thinking which brings out random ideas and concepts13. Used in a meeting agenda to block out time for miscellaneous discussion14. In private; outside the meeting16. Random Guesswork17. Aftermath of a successful merger19. A working holiday20. Niche of the company21. At the top of the organization tree22. Overtake your competition

Down1. Divide and conquer2. Output’s first draft4. A goldsmith who works with words7. Turning thinking into reality8. An informal gathering9. Easy success10. Minutes11. Capacity to work12. A fact of life14. Perception of outside world15. Resistance to ideas18. Pack of cards

Hints

27

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

IIFT SPEAKS

“At GeP, I worked on strategic sourcing across different categorieslike Marketing, Logistics, MRO and Capital for a major NorthAmerican CPG (Consumer Packaged goods) client with revenue ofalmost USD $ 14 billionStrategic sourcing includes different stages like supply marketanalysis(market intelligence),RFP development, suppliermanagement, RFQ negotiations, supplier selection, vendormanagement etc.It is basically a systematic process to reduce thetotal costs of externally purchased materials, and services whilemaintaining or improving the level of quality and service ;therebyhelping the client achieve huge savings”

“My internship project was to identify the potential agri-commodity export markets in Africa for Mahindra Agribusiness. Acustom index was utilized for the same. Also, value chainbenchmarking of the key market players was conducted and marketentry strategy was proposed. The project involved meeting traderswho have presence in the African markets, faculty for guidance ontheoretical aspects and export promotion council for policyperspective. All in all, a great experience with theoretical learningand massive number crunching!”

“My project at BMGF (Bill & Melinda Gates Foundation) was todevelop and implement a Partner Scorecard to benchmark/assessour partners on both technical and financial parameters.I needed to have a comprehensive understanding of the grantallocation process by interacting with Senior Program Officers,Program Managers and various other stakeholders in order todevelop a framework .Next was creating a dynamic excel tool on the basis of theframework developed which is user friendly and scalable. TheCountry Leadership Team appreciated the efforts and decided toscale up the tool in the near future.My overall learning was an overview of the functioning of a Not forProfit organization in India’s vibrant social sector.”

Shweta BaravaniMBA (IB) 2014-16Internship: GeP

Mihir AnandMBA(IB) 2014-16Internship: Mahindra & Mahindra

Akhil KhannaMBA(IB) 2014-16Internship: BMGF

28

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

“I did my summer internship at Mahindra Susten in thestrategy domain. I was based out of Mumbai and my projectentailed formulating a Go-To-Market strategy for Third PartyO&M of Solar PV plants for Susten.During the course of the project, I assessed the marketpotential, recommended service portfolio with price pointsand provided a list of immediate target customers. Inaddition to this, I also recommended internal costoptimization alternatives and based on that evaluatedpotential profit margin. To ensure efficacy of the analysis, Ialso assessed the risks involved and recommended adjacentbusiness ideas to be implemented simultaneously.The project gave me an opportunity to interview lot ofstakeholders involved, both internal and external (includingcompetitors, existing and potential customers). In addition tothis, I also got a rare chance of visiting all solar PV plants ofSusten in Rajasthan.Overall, it was truly a very enriching experience with mebeing able to contribute tangibly towards the organization.The recommendations suggested by me have been approvedby the senior leadership and are currently under execution.”

Ruhi GuptaMBA (IB) 2014-16Internship: Mahindra & Mahindra

Navneet SharmaMBA (IB) 2014-16Internship: Deloitte

“My internship project at Deloitte was to conceptualize andprepare financial feasibility model for PPP road projects. Theproject required an in-depth study of the Infrastructure PPPprojects in India, majorly in road sector, at different stages ofPPP life-cycle and different levels of complexity. The studyincluded different aspects, namely, project identification,project feasibility, structuring of the contract/concession, bidprocess, risk allocation framework, financing and value formoney analysis. Subsequent to this, needs, challenges andrisks associated with road PPP projects were identified and aroadmap was proposed to improve quality of projectidentification, preparation, award and monitoring. Followingthis variables were identified and a model was created thatwill hep private players to decide if they should invest in aspecific road sector PPP project in India.”

29

Strategos | August 2015

Indian Institute of Foreign Trade 30

A GLIMPSE OF IIFT…..

IIFT provides a juxtaposition of corporateinteraction, rigorous academic curriculumand a wide array of projects in the domain ofConsulting and Strategy. There is a renewedsense of passion and enthusiasm amongstudents in Consulting with several of themwinning Corporate and B-schoolcompetitions. This passion was corroboratedwith new recruiters along with industrystalwarts in the domain showing renewedinterest in the institute’s offerings.

Some of the student achievements in thisdomain are:• National CEO Round Winners, MahindraWar Room• Winners ,TCS CaseWiz, ITG Manufacturing• Winners, KPMG Consilium’2014• National Finalist, GE Genius• National Finalists, GEP Case Challenge2014• First Runners Up, CRISIL Young ThoughtLeader 2014• Grand Finalist, Strategists’League, Accenture Management Consulting• National Winners- EY Knowledge Quiz• National Runners Up, SP Jain - Chakravyuh• 3rd Position, ISB - Advaita Energy Wars

Some of the Live Projects that were floated inthe campus are:Redseer Consulting :- LEAP Program- Projectinvolving primary and secondary researchthrough questionnaires.Infonative Solutions, Malaysia- Marketresearch analysis of Malaysia,Australia, Singapore, Indonesia, Japan, ChinaC-Zentrix- Market research for SAS productsin Asia PacificTMG Advisory- Market Entry Strategy for GasFeed systems used for Chlorination in IndiaAccenture Strategy- Analyze global supply &demand and import to India for certaincommodities

Nmore- Live project related to their MNCclient in the automotive industryAxereal Live Project: Analysis of tradefeasibility between India and Middle Eastfor cerealsJubilant Foodworks - Internalcommunication strategy for the companythat to have direct impact on its 25000employees

Major Events conducted by the clubinclude:Tradewinds 2014 (Annual BusinessSummit of IIFT) National LeadershipSummitTheme for the Summit was “Changing Faceof Strategy Consulting”. There were twosessions with several business leaders asthe panelists:Session I: Importance of StrategicManagement Consulting in turbulent timesSession II: The Rise of Internal Consultinggroups in OrganizationsSpeakers from the last year summit are:Mr. Massimo Geloso Grosso, SeniorEconomist, OECD ParisMr. Subhajit Mazumder, Principal- BusinessConsulting, InfosysMr. Harish Agarwal, Partner, Ernst & YoungMr. Avnish Sabharwal, MD, Accenture IndiaMr. Gaurav Moda, Partner, KPMGMr. Rajan Kalia, Co-Founder, Salto Dee FeConsultingMs. Priyanka Gulati, Founder ManthanAdvisorsEternity’s callInter-B-school case study competitionorganized at Quo-Vadis, in which manyteams from across the countryparticipated, including several IIMs.Stratanalysis

Intra-IIFT competition which provided anopportunity to students to showcase theanalytical skills and perform the sectoranalysis based on different parameters.

Strategos | August 2015

Indian Institute of Foreign Trade 31

Theatre of DreamsCase based intra IIFT competition thatrequired employing multiple frameworks aswell as performing guesstimates to analysecritical business problems.

Tradewinds 2015 (Annual Business Summitof IIFT) National Leadership SummitTheme for this year's Leadership Summit is"Transformations in the Global Economy:Repositioning Brand India". The event isscheduled for the 20th of August and wouldsee speakers from across industries to have apanel discussion on the topic, giving anopportunity to students to have aninteractive industry exposure.Headstart Guest Lecture SeriesMcKinsey & Company- Mr. Alok Kshirsagar,Director (Senior Partner) and Risk PraticeAsia HeadThe Boston Consulting Group- Mr. NeerajAggarwal, Senior Partner & DirectorKPMG- Mr. Akhilesh Tuteja, Partner AdvisoryServicesAditya Birla Group- Smt Rajashree Birla,Director on BoardBain & Company- Mr. Deepak Jain, Partner &Practice LeaderA.T. Kearney- Mr. Debashish Mukherjee,Partner, Co-Head, Consumer & RetailIndustriesOliver Wyman- Mr. Atul Khosla, SeniorPartner and HeadVedanta Group- Mr. Anil Agarwal, ExecutiveChairmanTata Strategic Management Group- Mr.Susnato Sen, Practice Head-InfrastructureReliance Industries Limited- Mr. SouvikChakraborty, Chief Talent OfficerRoland Berger – Mr. Rahul Gangal, PrincipalSchneider Electric- Dr. Shalini Sarin, VP &Country Partner-HR and CSRDuPont- Mr. Vijay Srinivas, Global CorporateStrategic Account ManagerThomson Reuters- Mr. Rantej Singh, HeadStrategy

Cairn India- Mr. Sanjay Singh, Director-HRCognizant Business Consulting- Mr. AshishChawla, Senior Director-Information,Media & EntertainmentHoneywell- Mr. Ajay Kukreja, Country HRDirectorDB Schenker- Ms. Renu Bohra, Director-HRTecnova Consulting- Mr. Ashit Ranjan, VicePresident (Human Resources)

Strategos | August 2015

Indian Institute of Foreign Trade

7

10

13

30

19

Across

2. Socialize

3. Wetware

5. Traction

6. Ping

10. Granularity

11. Blue Sky Thinking

13. AOB

14. Offline

16. PIOUTA

17. Synergy

19. On the beach

20. Space

21. C-level

22. Leapfrog

Down

1. MECE

2. Strawman

4. Wordsmith

7. Imagineering

8. Town Hall Meeting

9. Quick Win

11. Bandwidth

12. Delta

14. Optics

15. Pushback

18. Deck

Solution to Wordsworth

32

33Indian Institute of Foreign Trade