STRATEGIC SEA SERVICES AGREEMENT

56

STRATEGIC SEA SERVICES AGREEMENT July 2017 Department of Infrastructure GD 2017/0027

Transcript of STRATEGIC SEA SERVICES AGREEMENT

STRATEGIC SEA SERVICES AGREEMENT

July 2017

Department of Infrastructure

GD 2017/0027

FOREWORD To the Hon Stephen Rodan, MLC, President of Tynwald, and the Hon Council and Keys in Tynwald assembled.

One of the most significant influences on our community is our sea links. Reliable, long term arrangements which enable people and goods to cross the Irish sea to neighbouring jurisdictions are

essential for the economic and social wellbeing of the people of the Isle of Man.

The Isle of Man Steam Packet Company Limited, an established Isle of Man company providing local

employment, has been serving the Island since 1830. In 1995, the Company entered into an agreement with the former Department of Transport for exclusive use of the Department’s linkspan on

King Edward VIII Pier, with negotiations and extensions being agreed in 2002 and 2004. The current agreement remains in place until 2026.

Discussions with the Isle of Man Steam Packet Company Limited regarding the future provision of services to the Isle of Man were instigated by the previous Administration, with the commitment that

Tynwald would consider a new offer. In the interim period, Tynwald approved the Strategic Sea Services Policy in December 2016; this approval was an integral part of the process to identify the

strategic options for the long term delivery of ferry services to the Isle of Man. The policy commits the Government to intervene in the ferry services market to provide for the social and economic

requirements of the Isle of Man.

Ferry service market intervention is currently achieved through the linkspan User Agreement. Since its

inception, the User Agreement has enabled Government to specify appropriate levels of service and controls on increases to standard fares and charges.

This paper presents the latest offer for a new Strategic Seas Services Agreement made by the Isle of Man Steam Packet Company, together with an analysis of that offer.

Hon R Harmer MHK

Minister for Infrastructure

1

TABLE OF CONTENTS Background ........................................................................................................ 2

The Isle of Man Steam Packet Company Limited Offer ........................................... 2

Assessing the Isle of Man Steam Packet Company Limited Offer ............................. 3

Risks to Sea Services if the offer is rejected .......................................................... 4

The Strategic Sea Services Policy ......................................................................... 4

Future long term options ..................................................................................... 4

Investment in the Shareholding of the Company ................................................ 4

Franchise ........................................................................................................ 5

Regulated Utility .............................................................................................. 5

Government Owned Vessels ............................................................................. 5

Future short terms options .................................................................................. 6

Accepting the Offer of a New Agreement ........................................................... 7

Rejecting the Offer of a New Agreement and Responding to Aggressive Operation

by IOMSPC ..................................................................................................... 7

Conclusions ........................................................................................................ 7

Recommendation ................................................................................................ 8

Appendices

Appendix 1 – Isle of Man Steam Packet Co Ltd Offer

Appendix 2 – Assessment of IOMSPC Revised Offer Terms – Oxera

Appendix 3 – IOMSPC’s Economic Contribution to the IOM – PWC UK

2

Background

1. In January 2016 the Isle of Man Stream Packet Company Ltd (IOMSPC) submitted an initial offer for a new Strategic Sea Services Agreement, at the request of the former Minister for Infrastructure. Although the offer had merit, there were concerns regarding the offer, particularly in relation to break clauses and the financial transparency of the Company. 2. The Department recommended to Tynwald in July 2016, in its Report on the Liverpool Landing Stage/Sea Services Agreement (GD 2016/0045), that it continue to negotiate a new draft Agreement with IOMSPC. The report was received by Tynwald, when it was also agreed that an independent economic appraisal of ferry services was required, together with investigation of all alternative ownership models. 3. An economic appraisal of ferry services was conducted by Oxera Consulting LLP. An evaluation of alternative ownership models was conducted by Park Partners Limited of London. Both reports were submitted to Tynwald in December 2016, (GD 2016/0080). During the same sitting, Tynwald approved the Strategic Sea Services Policy (GD2016/0079). Approval of the Policy was an integral part of the process to identify the strategic options for the long term delivery of ferry services to the Isle of Man, as the policy sets out the manner in which Government will intervene in the market to protect the Island’s social and economic wellbeing. The Isle of Man Steam Packet Company Limited Offer

4. The second formal offer for a new Strategic Sea Services Agreement was submitted by IOMSPC to the Minister for Infrastructure on 3rd March 2017. A copy is attached at Appendix 1. There has been no detailed negotiation on the offer, which has been submitted on a ‘best and final’ basis. 5. Officers of the Department of Infrastructure have worked with IOMSPC shareholder representatives and officers from Treasury, Cabinet Office, the Department of Economic Development and Attorney General’s Chambers to understand the detail of the offer, which can be summarised as follows:

Replacement of the MV Ben my Chree and the HSC Manannan sooner than possible without a new Agreement;

Guaranteed provision of a back-up vessel; Freight capacity of 10,000 lane metres per week; Expansion of special offer fares and other discounted travel offers for

passengers;

Expansion of discounted freight haulage rates; Revenue growth sharing of 50% with Government; Manx employment; Fare basket cap at MRPIJ; Guaranteed use of Liverpool ports.

6. In exchange IOMSPC would contract to have exclusive use of the Department’s King Edward Pier Linkspan until 2041.

3

Assessing the Isle of Man Steam Packet Company Limited Offer

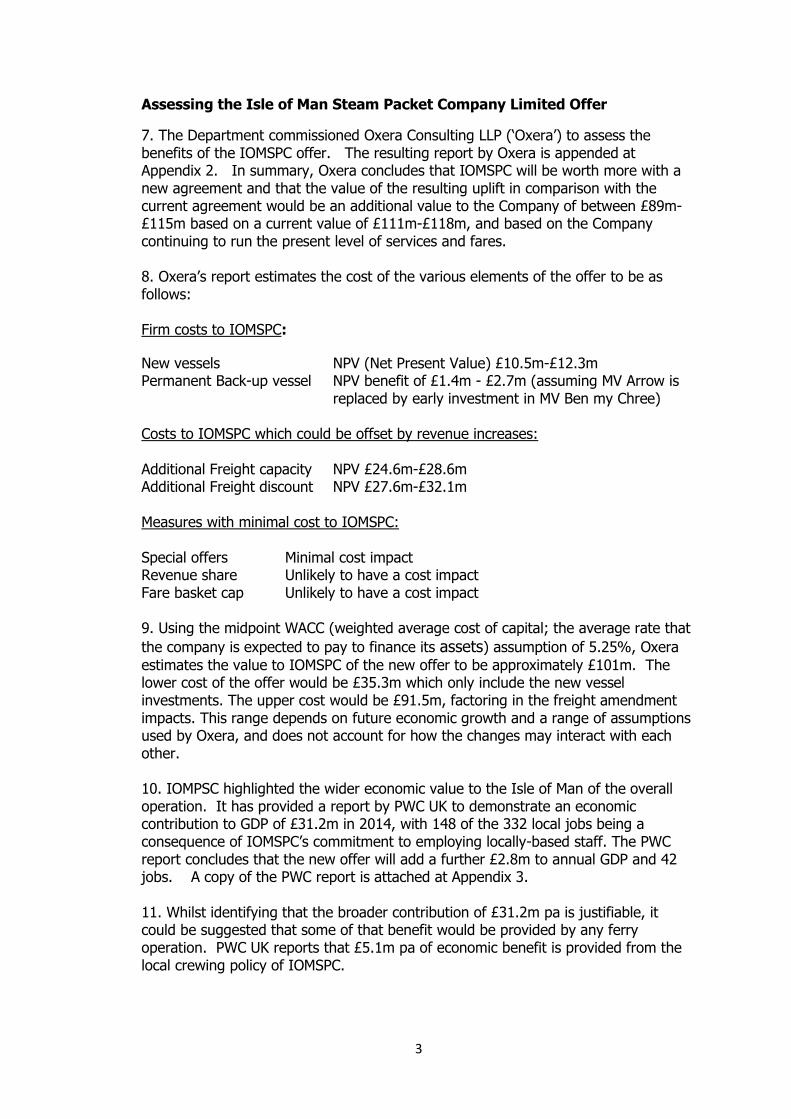

7. The Department commissioned Oxera Consulting LLP (‘Oxera’) to assess the benefits of the IOMSPC offer. The resulting report by Oxera is appended at Appendix 2. In summary, Oxera concludes that IOMSPC will be worth more with a new agreement and that the value of the resulting uplift in comparison with the current agreement would be an additional value to the Company of between £89m-£115m based on a current value of £111m-£118m, and based on the Company continuing to run the present level of services and fares. 8. Oxera’s report estimates the cost of the various elements of the offer to be as follows: Firm costs to IOMSPC:

New vessels NPV (Net Present Value) £10.5m-£12.3m Permanent Back-up vessel NPV benefit of £1.4m - £2.7m (assuming MV Arrow is

replaced by early investment in MV Ben my Chree) Costs to IOMSPC which could be offset by revenue increases: Additional Freight capacity NPV £24.6m-£28.6m Additional Freight discount NPV £27.6m-£32.1m Measures with minimal cost to IOMSPC: Special offers Minimal cost impact Revenue share Unlikely to have a cost impact Fare basket cap Unlikely to have a cost impact 9. Using the midpoint WACC (weighted average cost of capital; the average rate that

the company is expected to pay to finance its assets) assumption of 5.25%, Oxera

estimates the value to IOMSPC of the new offer to be approximately £101m. The lower cost of the offer would be £35.3m which only include the new vessel investments. The upper cost would be £91.5m, factoring in the freight amendment impacts. This range depends on future economic growth and a range of assumptions used by Oxera, and does not account for how the changes may interact with each other. 10. IOMPSC highlighted the wider economic value to the Isle of Man of the overall operation. It has provided a report by PWC UK to demonstrate an economic contribution to GDP of £31.2m in 2014, with 148 of the 332 local jobs being a consequence of IOMSPC’s commitment to employing locally-based staff. The PWC report concludes that the new offer will add a further £2.8m to annual GDP and 42 jobs. A copy of the PWC report is attached at Appendix 3. 11. Whilst identifying that the broader contribution of £31.2m pa is justifiable, it could be suggested that some of that benefit would be provided by any ferry operation. PWC UK reports that £5.1m pa of economic benefit is provided from the local crewing policy of IOMSPC.

4

12. It must be accepted that Oxera’s figures are only estimates and cannot be guaranteed to be completely accurate as there has been no access to the Company’s historical financial information nor its forecasts. Whilst Oxera suggest a very substantial uplift to the value of the Company, there are some benefits to renewing early. The most significant of these is likely to be the achievement of a modernised 3 vessel fleet, with associated improvements in reliability and quality. Risks to Sea Services if the offer is rejected

13. Should Tynwald decide not to accept the offer of a new Agreement with IOMSPC, there is a risk that the shareholders will seek to maximise the profitability of IOMSPC to pay back the performing loan on its books by 2022 and use dividends from the operations between 2022 and 2026 to recover as much as possible of the loans that are parked higher up the corporate structure. This would create risks for both parties, but would likely involve increases to passenger and freight charges and reduced levels of service provision. The Strategic Sea Services Policy

14. The Strategic Sea Services Policy approved by Tynwald in December 2016 committed the Department to intervening in the ferry services market to the extent necessary to provide for the social and economic requirements of the Isle of Man. This intervention is currently through the linkspan User Agreement. The detailed requirements of the Policy concerning freight, passenger and TT requirements and the overall needs of the taxpayer, the economy and our society are all currently met through the User Agreement. Future long term options

15. The Oxera report published in December 2016 (GD2016/0080) identified the following ownership models:

i) full state ownership, ii) company limited by guarantee, iii) partial state ownership, iv) negotiated concession (ie agreement to use the linkspan), v) regulated utility, vi) franchise, vii) joint venture.

Investment in the Shareholding of the Company 16. A move to any of the following four models further investigated by the Department before expiry of the current User Agreement in 2026 would require agreement or some control over the actions of IOMSPC:

i) full state ownership; ii) company limited by guarantee; iii) partial state ownership; ii) joint venture.

17. The sale of shares to Isle of Man Government or any other purchaser cannot be guaranteed so a change to service provision by any of these models would depend

5

on the successful negotiation of the purchase of a controlling shareholding or some form of agreement with shareholders. 18. These models remain valid options for any operation post-2026 once the current User Agreement expires, but cannot be progressed further at this time as the shareholders have not indicated that they are willing to surrender the current agreement and are not looking to sell the Company. Franchise 19. Another model which could not be progressed until post-2026 is a franchise. As it is unlikely that IOMSPC will voluntarily surrender the User Agreement, earlier movement to this model would depend on the ability of Government to obtain a controlling share of IOMSPC. Again, as successful negotiation of the purchase of a controlling shareholding cannot be guaranteed, the franchise model is therefore not a valid option at this time. Regulated Utility 20. A regulated utility was a further model considered by Oxera in 2016, although a regulated utility is not, in itself, a business model. 21. A move to a regulated utility would require Government to enact legislation which monitored the operator against certain requirements. 22. Regulation to safeguard the competitive provision of services is an issue which is being progressed as part of the Programme for Government, and the drafting instructions for the Competition Bill are currently being developed by the Department of Environment, Food and Agriculture and the Office of Fair Trading. 23. Whilst the possible interaction with any current or future Agreement has been considered, it is unlikely that current or future competition law could be used to over-ride the contractual arrangements for the use of the linkspan under the existing User Agreement or a new Sea Services Agreement. Government Owned Vessels 24. Vessel ownership would provide Isle of Man Government with control and protection of the national strategic assets. The current offer from IOMSPC includes an invitation to Isle of Man Government to fund the replacement vessels. Government owned vessels could be an aspect of a future company limited by guarantee, negotiated concession, franchise operation or joint venture 25. As the secondary charter market for suitable replacement vessels is extremely limited, security of the vessels is essential for the provision of strategic sea services. Under the current arrangement, IOMSPC could sell the vessels serving the Island at any time, without any Government involvement, although without suitable vessels the company would be unable to provide a service or meet the terms of the User Agreement and hence realise a profit. 26. The term of the operation and ownership of the vessels are inter-linked. Operators that are responsible for acquiring and funding the vessels usually require a

6

minimum term of 20 years to ensure payback on their investment. Ownership of the vessels could provide greater flexibility for Government when determining a model for ferry operation post-2026. 27. If vessel ownership is a route which Tynwald wished to progress, now could be the optimum time to do so. The shipbuilding industry is currently experiencing a down-turn in business, a consequence of the reduced demand for bulk carriers and oil tankers, and the huge increase in the size of container ships. Shipyards are reported to be now short of orders and likely to remain so for the next 3-4 years. Given the lead time to develop the specification and design of ferries, this could provide Isle of Man Government with a window of opportunity. 28. Although IOMSPC has offered to build a new 800 pax vessel as part of its proposal for a new Sea Services Agreement, this seems to be contrary to the reality that for most of the year, with the exception of the TT period, the MV Ben-my-Chree and the HSC Manannan operates with a passenger and vehicle load factor of around 35-40%. Two smaller vessels could provide the Island with greater levels of flexibility to better meet the Island’s strategic needs. A single larger vessel may be more economical to operate, but more frequent sailings are likely to be preferred by users. 29. Further work would be required to assess the optimal size of the vessels, balancing the needs of passenger comfort, meeting demands during peaks and the control of operating costs. 30. New vessels are likely to offer reduced fuel costs, reduced staffing costs through live-aboard accommodation and increased passenger demand so some additional value would be created in return for an investment of approximately £60m, either in the form of a new Ro-Pax ferry and nearly new fastcraft as proposed by IOMSPC or of two smaller Ro-Pax ferries. 31. Whilst the shareholders may not wish to accept this reduction in their capital employed on their ability to offer services post-2026, sale of their current vessels whilst still mid-life might be an attractive way to generate cash and offset the impact of the parked loans. 32. A further option might be to incentivise IOMSPC’s use of Government-owned vessels by allowing the Company the opportunity to have the first post-2026 operating franchise term. Future short terms options

33. Realistically, and in the light of all the information considered, Government currently has only a limited number of short term options:

Accept the offer of a new Agreement with IOMSPC (or negotiate a variation of that offer);

Reject the offer and continue with the current User Agreement until 2026, whilst planning to move to a different service delivery model post-2026.

7

34. Government could consider making an offer to purchase the Company, but as the shareholders have not indicated that the Company is for sale it is not considered appropriate to propose this as a currently viable option. Accepting the Offer of a New Agreement 35. Should Tynwald agree to accept the current IOMSPC offer, then the future delivery of strategic sea services is a straightforward matter. 36. Although the offer has been submitted on a ‘best and final’ basis, there has been no detailed negotiation on its content. Should Tynwald agree that it would like IOMSPC to continue to provide ferry services to the Isle of Man beyond 2026, but that the terms of the offer are not sufficient, the Department of Infrastructure could be instructed to negotiate with IOMSPC on the future content. Rejecting the Offer of a New Agreement and Responding to Aggressive Operation by IOMSPC 37. If the decision of Tynwald is not to accept the offer, the current Agreement will remain in place until 2026. Should IOMSPC respond by reducing services to increase profit generation, the Department of Infrastructure could make a number of responses. These would serve to limit cash generation by the Company and could therefore represent a worthwhile brake on its behaviour. 38. It is thought unlikely that IOMSPC shareholders would accept a financial incentive to continue the existing level of services, preferring instead some form of an extension of the contractual period for use of the linkspan. Conclusions

39. The option of whether to accept the IOMSPC offer to 2041 is finely balanced. That offer clearly benefits the shareholders, with Oxera estimating that the shareholders would be better off over the term of the proposed agreement. Consideration of the economic impact complicates the issue, with an estimated economic benefit of £5m - £5.1m pa from local crewing and £2.8m pa from a permanent third vessel in addition to the current estimated £32.1m pa GDP contribution from IOMSPC’s operations. 40. There are a number of public concerns about the IOMSPC operation. Some, such as the cost of fares, are longstanding but not supported by the evidence; indeed, several studies have shown fares to be reasonable. Concerns about debt levels are more valid but also tend to be misinformed; the debt has not affected fares as these are capped in the User Agreement, but it is true, if perhaps unlikely, that a debt free operator could have reduced prices and forgone profit. The trading of a lifeline service as a debt-bearing asset is also a concern, but the current shareholders have until now invested in the Company to secure long term income rather than short term cash. That may of course change in future. 41. The proposed offer does address some of these concerns by including safeguards on change of ownership and debt but these safeguards will have to be carefully negotiated if they are to offer effective protection for the Island’s interests in practice. The offer already provides for Government to purchase the vessels but the

8

length of the term precludes any subsequent change of model until 2041, when the vessels would be at best mid-life. There is a justifiable concern with the length of the agreement of 25 years, which is longer than the industry norm. 42. Should Tynwald decide not to accept the offer of a new Agreement with IOMSPC, the current plan of the shareholders appears to be to maximise the profitability of IOMSPC. Whilst this would create risks for both parties, increases to the cost of ferry services have clear implications for the Isle of Man. 43. Whilst the Department will have to monitor User Agreement compliance closely it is highly unlikely that IOMSPC will breach its terms as it is the Agreement that guarantees the long term income stream. 44. If the Company were to be for sale at a price judged by Tynwald to be acceptable there would be a number of options for future service delivery, including continued delivery by IOMSPC but under a changed corporate structure or franchising arrangement. As the position of the shareholders is that IOMSPC is not for sale, these options have not been explored further. 45. If the decision of Tynwald is to reject the IOMSPC offer the obvious course of action is to allow the User Agreement to expire and be ready at that point to move to a new model. Were this to be the preferred option, work to identify a solution to the future delivery of services will need to begin in about 5 years’ time. Recommendation

46. The Council of Ministers recommends that the offer dated 3rd March 2017 for a new Sea Services Agreement is declined as, in the opinion of the Council of Ministers, it does not provide the Island with an effective solution to securing a satisfactory and sustainable provision for sea services beyond the expiry of the current User Agreement. 47. The Department recommends that it be authorised to continue negotiations with IOMSPC with a view to seeking a more detailed and better structured solution and that it be instructed to consider all other options for achieving a more effective solution that offers greater benefit to the Island.

..

The Isle of Man Steam Packet Company Limited

Imperial Buildings

Bath Place

Douglas

IM1 2BY 3rd March 2017

Hon. R. Harmer MHK, Minister for Department of Infrastructure

Sea Terminal

Douglas

IM1 2RF

Dear Minister,

Our Offer for a new Strategic Sea Services Agreement between the Isle of Man Government

and the Isle of Man Steam Packet Company will provide a framework for substantial service

improvements ten years earlier than would otherwise be the case.

The attached Heads of Terms reflects the issues we have discussed with your Officers and

those of Treasury and has been approved by our shareholders and our Board. The Offer will

remain open during the timetable your Officers have indicated is necessary to take it to

CoMin and on to Tynwald.

In February 2012, the Chief Minister indicated that he believed that the User Agreement

should be renegotiated to take account of changes since its introduction in 1995.

We have listened carefully. to feedback from the public, businesses, Travelwatch, Government and the Strategic Sea Services Working Group and believe our offer meets the

diverse aims of each of these groups. As you know we have already agreed to use a new Isle of Man Government (loMG) owned Liverpool facility in any event until the expiry of the

existing User Agreement and have also agreed to incorporate this use for the life of the new

agreement.

The Isle of Man Steam Packet Company is a major employer in the Isle of Man, operates our

vessels under the Manx flag and has played a vital role in our economy and society for over

185 years. Unlike other potential operators, we are an Isle of Man based carrier, and our

focus is solely on Isle of Man services. We welcome the opportunity to present our vision of

the future of ferry services for the Island.

The Isle of Man Steam Packet Company Limited Imperial Buildings, Douglas, Isle of Man IM1 2BY

Reservations TO 1624 661661 F O 1624 645608 [email protected]

T 08722 992992 (3-:- ia•.dline ::alls charged at IOp per mwiute ind.VAT. charges from other networ<S and mobile operators may vary)

Freight Reservations T O ! 624 645620 F O I 624 645627 [email protected]

Administration

Finance

T O 1624 645645

TO 1624 645645

F O 1624 645609

F O I 624 645716

Registered Office: Imperial Buildings, Douglas, Isle of Man IM1 2BY. Registered in the Isle of Man. Registration No. 002092v

. - � � ----# ...----- .._

STEAM-PACKET.COM

APPENDIX 1

A Strategic Sea Services Agreement has the potential to consolidate the real benefits that

we have delivered to the Island since the start of the User Agreement in 1995 as well as

providing a platform for bringing forward further investment and enhancements in service

delivery for future generations. Our Offer also provides Government with much greater

strategic control than the User Agreement.

In summary, our offer represents a cash investment of £120m in vessels, and a further £50m

in reduced fare initiatives and increased service provision to both passenger and freight

customers to help boost travel and the local economy. Of this more than £100m will be

committed in the next 10 years and within the life of the existing User Agreement.

We will act to secure the Island's sea lifeline through investment in a third back-up vessel to

provide self-sufficiency for the Island as well as allowing for extra passenger capacity to

grow events such as the TT and Festival of Motorcycling.

We will guarantee the majority of our employees are Isle of Man residents and ensure the

Island benefits from tax receipts, on-Island spending and a uniquely Manx commitment and

focus. PWC have independently estimated that this is worth more than £30m each year to

the Isle of Man economy.

We will introduce a generous frequent traveller discount scheme benefitting many times

more passengers than did the previous scheme.

We will deliver low fares through substantially increasing special offer guarantees so improving still further the competitive fares we offer as independently verified by

comparisons with other Irish Sea operators.

We will introduce an innovative revenue sharing mechanism which will result in us sharing

50% of future growth above an agreed level and is estimated to be worth £38m over the life

of the new agreement.

We will move from the current Manx RPI index for Schedule 6 fare and charge increases

(which currently applies until 2026) to Manx RPIJ from the introduction of the replacement

vessel for Ben-my-Chree. Manx RPIJ will then apply to all costs and charges by Government from that date as well as to all Schedule 6 increases. This is subject to the terms of Clause

11 of the Heads of Terms.

We will agree to a 'Strategic Reset' mechanism, per Clause 17, which will allow both parties to vary the agreement within certain parameters and makes clear that any future legislation

introduced by Government cannot be applied if the effect is to undermine the business case

on which the Offer is made.

We will make a payment, per Clause 21, to Government in the case of there being a sale to

another entity within 24 months of a new agreement. A worked example of this mechanism

is included in the Heads of Terms, which removes the previous cap discussed with Doi and

Treasury officers. The proposed model allows for a more generous payment based on a

hurdle of £150m which is broadly reflective of the Park Partners current estimate of the value

of the Company. We remain open to Government reverting to the previous 'ratchet'

mechanism explained to Department of Infrastructure and Treasury officials if that is preferred.

We believe the Offer we have made is firmly in the best interests of the Island. It secures

real benefits now for Island residents and businesses, in times of real economic uncertainty,

and does so at no cost to Government.

Yours sincerely,

��Ct Robert Quayle

Chairman

Cc Nick Black, Doi CEO

Cc Sheila Lowe, Treasury CFO

Mark Woodward

Chief Executive Officer

Amendments to the current User Agreement Framework

SlJ>ject to Contract and Without Prejudice

The Strategic Sea Services Agreement (SSSA) will be a new agreement based on the current Linkspan User Agreement obligations subject to the following amendments and or additional provisions:

(1) Clause 3.15 further investment of up to £45 million to replace the MV Ben-my-Chree by nolater than 2021 or, if later, 4 years from the start date of the Strategic Sea Services Agreementin a new minimum 800 passenger capacity multi-purpose vessel with modern on-board features.This will be a new vessel purpose built for Isle of Man unless the Department of Infrastructure(the Department) agrees that a refurbished vessel is in the Island's best Interests.

(2) Clause 3.15 further investment of up to £20 million to replace the existing fast craftManannan by 2023 or, if later, 6 years from the start date of the Strategic Sea ServicesAgreement with a new, nearly new or fully refurbished fast craft vessel.

The Isle of Man Steam Packet Company Limited will consult and obtain Department and Treasury concurrence prior to undertaking any vessel acquisitions but such concurrence shall not be unreasonably withheld or unduly delayed provided that the vessel must comply with the terms of the SSSA clause 3.15 (as amended).

When the Company develops its financing plan for any vessel acquisition, Isle of Man Government (loMG) will also have the option to bid to provide finance for the vessels. An appropriate contractual framework in conjunction with existing financing arrangements will be put in place if any new vessel financing arrangements are ultimately agreed by the Company.

The Company will commit to spending up to £80m to provide all vessels as part of the SSSA ("Planned Vessel Costs"). The final Investment sum will be subject to variations in vessel acquisition costs and in exchange rates and will include on-going cost of back up charter payments and replacement vessels, subject always to a minimum investment of £60m.

(3) A new clause requiring the company to provide a suitable third vessel. This will be scheduledinto service at TT and during Multi-purpose Vessel overhauls periods and if required at TTClassic/MGP periods to increase capacity. At other times of the year it will enhance back-upcapabilities. Until the delivery of the new multipurpose vessel by the specified date this thirdvessel will be MV Arrow or a freight vessel with an approximately similar capacity. Thereafterthe vessel will be MV Ben-my-Chree or a multi-purpose Passenger/Freight vessel with anapproximately similar capacity. The Company will not be entitled to charter out the third vesselduring the TT and Multi-purpose vessel scheduled statutory overhaul periods.

(4) The company must undertake consultation with a range of stakeholders including but notlimited to Department of Infrastructure, Department of Economic Development, Isle of ManChamber of Commerce, Travel Watch Isle of Man prior to the introduction of any new vesselsprovided in accordance with clause 3.15 with a view to reflecting any comments in the designand development process.

(5) Clause 3.2.1 of the agreement will be amended to increase the minimum inbound freightcapacity per week to 10,000 lane metres per week.

(6) Clause 2.1.6 of the supplemental agreement covering clause 5 of the main agreement willbe amended to require the company to provide special offer seats, which are equivalent to atleast 85% of the ·passenger and passenger vehicle traffic carried in the previous year. TheDepartment will be permitted to audit special offer fare availability is compliant with the SSSA.

(7) A new provision will be added requiring the company to guarantee the availability of thespecial offers which offer discounted travel to the following groups at off peak periods in theyear:

- Student discounts of at least 50% on the equivalent full fare rate.- Lower child fares within existing special offers which are 50% of the adult fare (excludingsupplements).- ITX rates for package holidays.- Non-landing 'cruise' trips to be available on all Irish sailings except at peak times.- The Company will introduce within eighteen months an automated Frequent Traveller Schemeunder which eligible passengers travelling on 3 occasions each year will be eligible for furtherdiscounted travel within a fixed period to help develop market growth.

(8) The Company will guarantee and incorporate in the Schedule 6 fare control the circa 40%reduction in volume freight rates implemented in 2010/11.

(9) The Company will share 50% of all revenue growth (fare ticket & freight revenues and subcharter income excluding fuel surcharges) above a pre-agreed annual benchmark "PlanRevenue" (calculated by reference to MRPl+1.0% pa until 31 December 2021, thereafterMRPIJ+1.0% pa). The allocation of the 'revenue growth share' between targeted special offerdiscounts and/or UK marketing will be discussed and agreed with the Department on an annualbasis to encourage market development.

(10) In addition to Clause 2.3.9 of the 2004 Agreement whereby not less than 50% of theDirectors of the Company from time to time shall be resident on the Isle of Man and the majorityof the Executive Directors shall work at the Company offices on the Isle of Man, The Companywill make reasonable endeavours to ensure in future that as a minimum a majority of itsemployees are resident in the Isle of Man. (Terminal staff in UK Ports will be exempted from therequirement).

(11) The existing fare controls (unless other measures are mutually agreed between theDepartment and the Company) will be maintained so that there will be no increases in realterms for User Agreement Standard fares and volume freight rates for the duration of the SSSA.

The company will accept a change of method in future revenue and cost indexing from Manx RPI to Manx RPIJ (MRIPJ) from 2021 (the latest date at which the Ben-my-Chree (BmC) is replaced in service by a new vessel). To avoid mid-year pricing changes, MRPIJ would be used from the 1st January in the year after the replacement vessel for BmC is introduced. The early adoption of MRPIJ would be subject to the following conditions:

(i) From the same date, loMG would rebase all harbour charges, leases, FuelSurcharge Agreement and any other inflation indexed costs levied by it on SPCin loM/UK to MRPIJ/RPIJ.

(ii) loMG will not seek to apply any new costs in the areas in (i) above on to theCompany and would agree that in the event of changes to UK/loM legislation orinternational regulations, any additional costs incurred could be recovered via theexisting User Agreement mechanism.

(iii) SPC would be entitled to minimum 2% fares and charges increase in each andevery year of the agreement in which MRPIJ was below 2%. The month on whichMRPIJ is based should be agreed by both parties and remain consistent unlessboth parties agree, by mutual consent, to its variation.

As part of the Department's audit of special offer fare availability (Clause 6 above), the Company will demonstrate to the Department each year that these special offer fares included in the availability calculations offer genuine discounts off peak Standard fares and the Company will also include special offers discounts of at least 50% off peak standard fares.

(12) The Company will commit to operate from existing ports approved by the Department (perUser Agreement obligations) and will not make any changes to the ports served without theDepartment's prior approval and will wherever possible/practical operate from ports and berthsowned or controlled by the Department. The Port Selection obligations (Clause 3.9 of theAgreement) will be amended to require the company to commit to a long-term lease of the loMGproposed new Liverpool River berth facilities for the period of the SSSA always provided termsand total port costs are consistent with present Liverpool Landing stage commitments and theberth is practical in all respects from an operational perspective).

(13) Undertake annual consultation on future schedules and will as far as reasonably practicalensure links with onward public transport.

Carry out annual Service Reviews to support ongoing informal work with the Department. The aim of the reviews is to be that both parties shall annually confirm on their compliance with the key performance indicators of the contract;

The publication of fare comparisons on an annual basis to demonstrate that the price of the Company's services relative to those provided on comparable routes are reasonable and competitive when compared to other operators on a cost per mile basis.

The continued commitment to the support of local charities, good causes and their fundraising efforts.

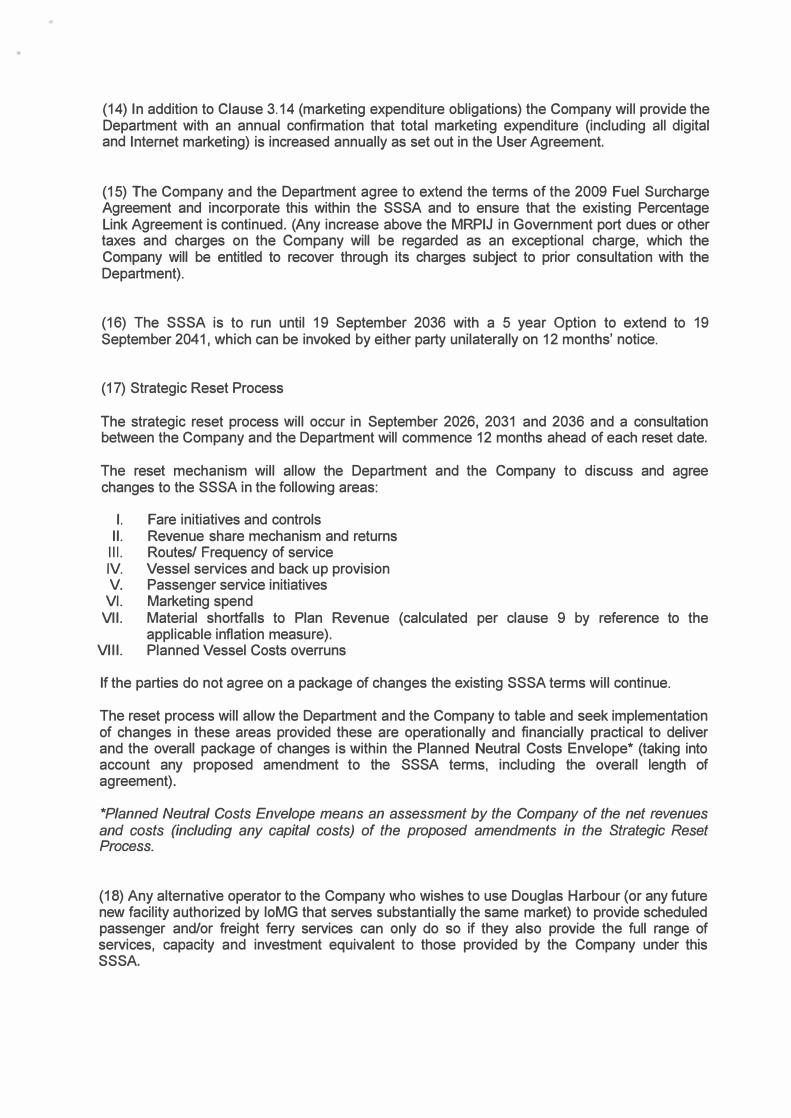

(14) In addition to Clause 3.14 (marketing expenditure obligations) the Company will provide theDepartment with an annual confirmation that total marketing expenditure (including all digitaland Internet marketing) is increased annually as set out in the User Agreement.

(15) The Company and the Department agree to extend the terms of the 2009 Fuel SurchargeAgreement and incorporate this within the SSSA and to ensure that the existing PercentageLink Agreement is continued. (Any increase above the MRPIJ in Government port dues or othertaxes and charges on the Company will be regarded as an exceptional charge, which theCompany will be entitled to recover through its charges subject to prior consultation with theDepartment).

(16) The SSSA is to run until 19 September 2036 with a 5 year Option to extend to 19September 2041, which can be invoked by either party unilaterally on 12 months' notice.

(17) Strategic Reset Process

The strategic reset process will occur in September 2026, 2031 and 2036 and a consultation between the Company and the Department will commence 12 months ahead of each reset date.

The reset mechanism will allow the Department and the Company to discuss and agree changes to the SSSA in the following areas:

I. Fare initiatives and controlsII. Revenue share mechanism and returns

111. Routes/ Frequency of serviceIV. Vessel services and back up provisionV. Passenger service initiatives

VI. Marketing spendVII. Material shortfalls to Plan Revenue (calculated per clause 9 by reference to the

applicable inflation measure).VIII. Planned Vessel Costs overruns

If the parties do not agree on a package of changes the existing SSSA terms will continue.

The reset process will allow the Department and the Company to table and seek implementation of changes in these areas provided these are operationally and financially practical to deliver and the overall package of changes is within the Planned Neutral Costs Envelope* (taking into account any proposed amendment to the SSSA terms, including the overall length of agreement).

*Planned Neutral Costs Envelope means an assessment by the Company of the net revenuesand costs (including any capital costs) of the proposed amendments in the Strategic ResetProcess.

(18) Any alternative operator to the Company who wishes to use Douglas Harbour (or any futurenew facility authorized by loMG that serves substantially the same market) to provide scheduledpassenger and/or freight ferry services can only do so if they also provide the full range ofservices, capacity and investment equivalent to those provided by the Company under thisSSSA.

(19) The Company shall take no action that would result in any part of the outstandingShareholder Loan to Sealion (loM) Ltd becoming an actual or contingent obligation of theCompany.

(20) Majority Control of the Company shall at all times be held by persons, which satisfy theconditions of the Fit & Proper Operator Test. Fit & Proper Operator means any person (whethercorporate or otherwise) that is:

I. an Existing Shareholder or its group companies, successor organisation OR11. regularly engaged in making investments in infrastructure or maritime assets, or a trade

buyer for which any of maritime trade, passenger transport and logistics is a keybusiness focus (but this category shall exclude any person which held Majority Control ofthe Company during the period 2005-2010 and any company which has been inliquidation) OR

Ill. designated in writing for the purpose of this provision by the Department, such approval,if requested by the Company, not to be unreasonably withheld.

(21) Without prejudice to paragraph 20, if there is a change of Majority Control of the Companywithin 24 months of the start date of this SSSA, a one-off payment will be made to loMG,calculated as 10% of the Enterprise Value of the Company in excess of £150 million. (A workedexample is attached as an Appendix to illustrate this and compares this to the previouslyproposed payment).

No payment would be due in respect of any shareholding transfers between Existing Shareholders. No payment would be due in respect of any subscription for new shares in the Company. Any payment due under this clause will be prorated if less than 100% of the shares in the Company are sold.

(22) In the event of a change of Majority Control of the Company, it would be subject to a onetime indebtedness test. The purpose of the test is to limit the amount of any additional debtplaced on the Company balance sheet at the closing of any transaction resulting in a change ofMajority Control to 2.0x EBITDA of the Company. Debt for the purposes of this test shallexclude any finance provided to the Company by its shareholders in the form of equity,preference shares or shareholder loans.

Within 180 days of closing the transaction the Company shall provide a letter signed by the Company's auditors (or a top 4 accounting firm of the Company's choice) confirming the amount of any additional debt on the Company balance sheet at the closing of the transaction, compliance with the indebtedness test set out in this paragraph and that any such additional debt was approved by the Company's Board after appropriate whitewash or equivalent procedures.

(23) In the event of a change of Majority Control of the Company shall, within 180 days ofclosing such transaction, provide a letter signed by its Board giving evidence of compliance withthe conditions of the Fit & Proper Operator Test, the letter giving evidence of compliance withthe indebtedness test set out in paragraph 22 and a certificate signed by its Board setting outthe calculation of any fee payable in accordance with paragraph 21.

(24) The new SSSA to contain provision for a 'run-off' plan of up to 3 years.

(25) Failure of the Company to deliver the services outlined in the agreement will result intermination subject to a requirement that the Department must give the company a period of sixmonths to rectify the breach of the agreement, which must be of a material nature.

(26) The Company will provide the Department annually, on a confidential basis, with sight ofits management accounts.

(27) The Company will report any 'Going Concern' qualification to a formal audit opinion andadvise on the plan that is being adopted to address any related concerns.

(28) The SSSA will include specific provisions whereby the Company will ensure it hasadequate financial resources and management expertise to meet its financial, and other,obligations as they become due.

(29) Failure to comply with any substantive undertaking contained in paragraphs 19, 20, 22, 28shall constitute a SSSA 'Default Event', which would allow the Department to terminate theSSSA.

(30) Following the occurrence of a change in law which supersedes or renders unenforceable orillegal any material term of the SSSA the Parties shall seek to agree the effect of such change inlaw. They shall also seek to agree any consequential amendments to the terms of the SSSA toensure that the Company is in a no better or worse position than pursuant to the original termsof the SSSA.

(31) These commercial heads of terms ('Terms") summarise the Company's offer as of 3rd

March 2017 The Terms are subject, inter alia, to contract and to amendment or withdrawal bythe Company at any time in response to changes in external conditions or for any other reason.

APPENDIX: Clause 21 Working Illustration

O�lonal Ratchet

1Share of £xcessO'leragreed floor

Sale Value fm 90.0 100.0 110.0 UO.O 130.0 llO,O 150.0 160.0 170.0 180.0 190.0 200.0 • J ..

Payment £m 0.00

Paymentfm 0 0 0

210.0 No Cap Ii

Assessment of IOMSPCo revised offer terms

Prepared for

Isle of Man

Department of Infrastructure

25 April 2017

APPENDIX 2

Introduction (I)

• The Isle of Man Department of Infrastructure has asked Oxera to provide a high

level assessment of the cost implications of the recent offer by the Isle of Man

Steam Packet Company Limited (IOMSPCo).1

• The offer outlines IOMSPCo’s proposed changes to the current linkspan User

Agreement (the UA), which is due to expire in 2026. In return for an extension

to the UA to 2041, the offer outlines amendments to the current UA that would

change minimum service levels. Additionally, several amendments guarantee

investments that are not included in the current UA.

• These slides describe the proposed key amendments that are most likely to

have a cost or revenue impact on IOMSPCo.

25 April 2017 2

1 Provided as a letter by IOMSPCo to Hon. R. Harmer MHK, Minister for the Department of Infrastructure,

dated 3 March 2017.

Introduction (II)

• Based on information provided by the Department of Infrastructure, we

provide an assessment of the cost or revenue implications of these

amendments.

• It is likely that some of the measures would have more complex effects

such as impacts on demand. We do not consider such effects here and

our estimates should be treated as broadly indicative of the cost rather

that definitive.

• where there are significant limitations or unquantified effects we note

these as part of the description.

• Further, some of the measures are likely to interact with one another.

We do not take these interactions into account.

25 April 2017 3

Background

• Any agreement between the Department of Infrastructure and IOMSPCo is likely to have an impact on

several stakeholders. The benefits of an agreement can be roughly allocated to the following

stakeholder groups.

25 April 2017 4

Benefits to direct

users (passenger

and freight) and the

Government

Benefits to

IOMSPCo

Wider economic

benefits to the

Isle of Man

1 PwC (2017), ‘IoMSPC’s Economic Contribution to the Isle of Man’, March.

Benefits shared through the terms of the UA

• The proposed extension of the UA would provide an uplift in value to IOMSPCo in the form of a

guaranteed, long-term revenue stream. The benefit of this is shared through the proposed

amendments and their impact on direct users in service improvements, or through increased payments

to the Government, both of which would represent a cost impact to IOMSPCo.

• IOMSPCo commissioned a report assessing the wider economic impacts of the ferry service. However,

the impacts discussed in the economic impact assessment arise indirectly out of the UA and are not

relevant to the direct benefit allocation between the users and IOMSPCo from any proposed

amendments.1

Approach

Context

Estimate of the value of an extension of current UA

• We first estimate the value to IOMSPCo of the extension of the current UA terms to 2041,

based on existing revenue and cost forecast assumptions and assuming no revenue

growth over time. This is likely to provide benefits to IOMSPCo in the form of an

extended, guaranteed revenue stream, and provides a baseline against which to

compare the costs or revenue impacts IOMSPCo is proposing as part of its amendments

Estimate of the revenue and cost impacts of the proposed UA amendments

• In the second stage, we assess whether specific amendments proposed will have a cost

or revenue impact on IOMSPCo. The proposed amendments to the current UA offer

changes to what IOMSPCo are expected to provide under minimum service levels. We

estimate the cost to IOMSPCo of these amendments to the UA:

• we estimate the immediate cost or revenue impact of certain amendments. In some

cases, there could be a demand impact that could offset the cost to some extent;

• we do not consider the interaction between amendments. Some of the clauses would

interact with one another, meaning that these individual estimates cannot be summed

together.

25 April 2017 5

Approach

Estimated value of a UA extension to IOMSPCo

• The Park Partners report implies a value of the business at £111m–£118m on a

discounted cash-flow basis under the current agreement.1 Extrapolating these cash flows

over the extended UA would mean an uplift in the region of £89m–£115m to the

company.2

• Current value estimates assume no potential revenue/cost impacts from any continued

use of the linkspan by IOMSPCo after the expiry of the current UA in 2026.

25 April 2017 6

Note: estimates presented are subject to rounding

1 Park Partners (2016), ‘Isle of Man Steam Packet Review of Strategic Options’, 31 March, slide 80.

2 We use the Park Partners projections to 2026 and no control premium. From 2026 we take a linear extrapolation of

operating cash flows inflated by average MRPI to 2041. We assume that cash flows cease at 2041 and there is no

terminal value at this point.

4.5% WACC 6% WACC

Current value under existing UA (£m) 118 111

Value with extension (£m) 234 200

Approach

IOMSPCo revised offer amendments

Amendment Description

1-2) Offer to replace ro-pax and fast craft vessel sooner than possible without New

Agreement

3) Guaranteed provision of a back-up vessel

5) Freight capacity of 10,000 lane meters per week

6-7) Expansion of special offer fares and other discounted travel offers for passengers

8) Expansion of discounted freight haulage rates

9) Revenue growth sharing of 50% with Government

10) Manx employment

11) Fare basket cap at MRPIJ

12) Guaranteed use of Liverpool ports

25 April 2017 7

We compare the cost impact on IOMSPCo of key amendments with minimum service level conditions.

Approach

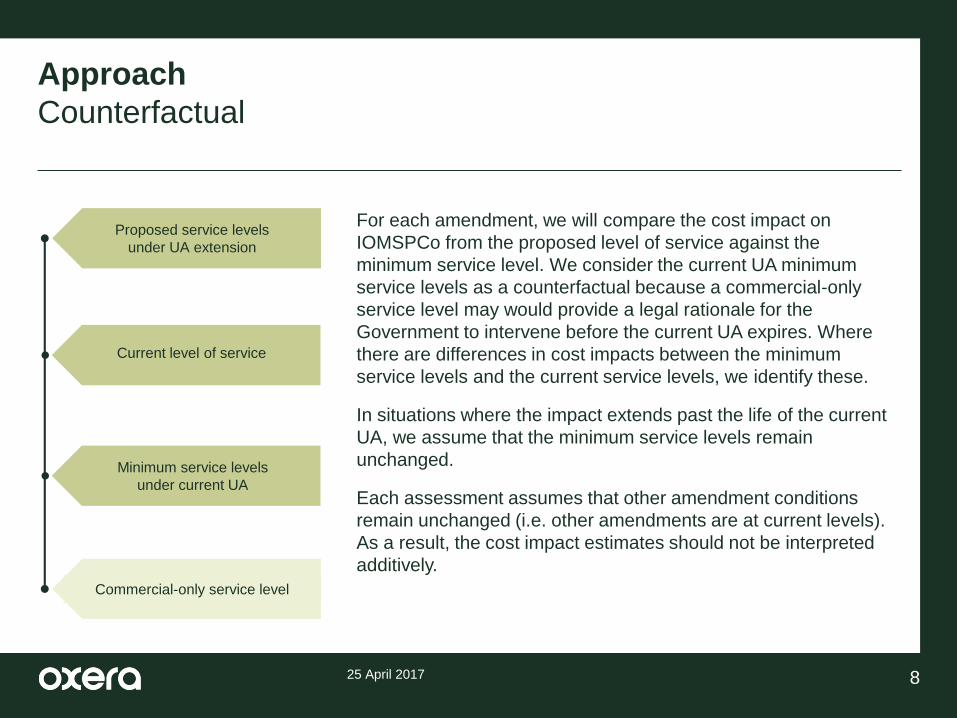

Counterfactual

25 April 2017 8

Proposed service levels

under UA extension

Current level of service

Minimum service levels

under current UA

Commercial-only service level

For each amendment, we will compare the cost impact on

IOMSPCo from the proposed level of service against the

minimum service level. We consider the current UA minimum

service levels as a counterfactual because a commercial-only

service level may would provide a legal rationale for the

Government to intervene before the current UA expires. Where

there are differences in cost impacts between the minimum

service levels and the current service levels, we identify these.

In situations where the impact extends past the life of the current

UA, we assume that the minimum service levels remain

unchanged.

Each assessment assumes that other amendment conditions

remain unchanged (i.e. other amendments are at current levels).

As a result, the cost impact estimates should not be interpreted

additively.

Amendment 1-2

New investment in vessels

25 April 2017 9

Background

• The Ben-my-Chree and Manannan vessels were built in 1998. Without a UA extension, based

on an asset life of 30 years, they would both need to be replaced in 2028. The amendment

would guarantee investment in vessels before current vessels are fully depreciated.

Assessment

• The impact on IOMSPCo would arise from moving the investment costs forward in time.

• We assessed the net present value (NPV) of costs incurred by IOMSPCo under two scenarios:

• minimum level—IOMSPCo would be required to replace both Ben-my-Chree and Manannan in

2028, based on the asset life reported in accounts (up to 30 years);

• new offer—IOMSPCo would replace Ben-my-Chree in 2021 and Manannan in 2023 using their

maximum estimated cost of replacement.

• Assuming a financing cost of 4.5–6% (WACC range indicated in the Park Partners report):

• minimum level—NPV of investment costs of £24.7m–£29.8m;

• new offer—NPV of investment costs of £37.0m–£40.3m;

• additional cost to IOMSPCo of £10.5m–£12.3m.

Amendment 3

Guaranteed back-up vessel (I)

25 April 2017 10

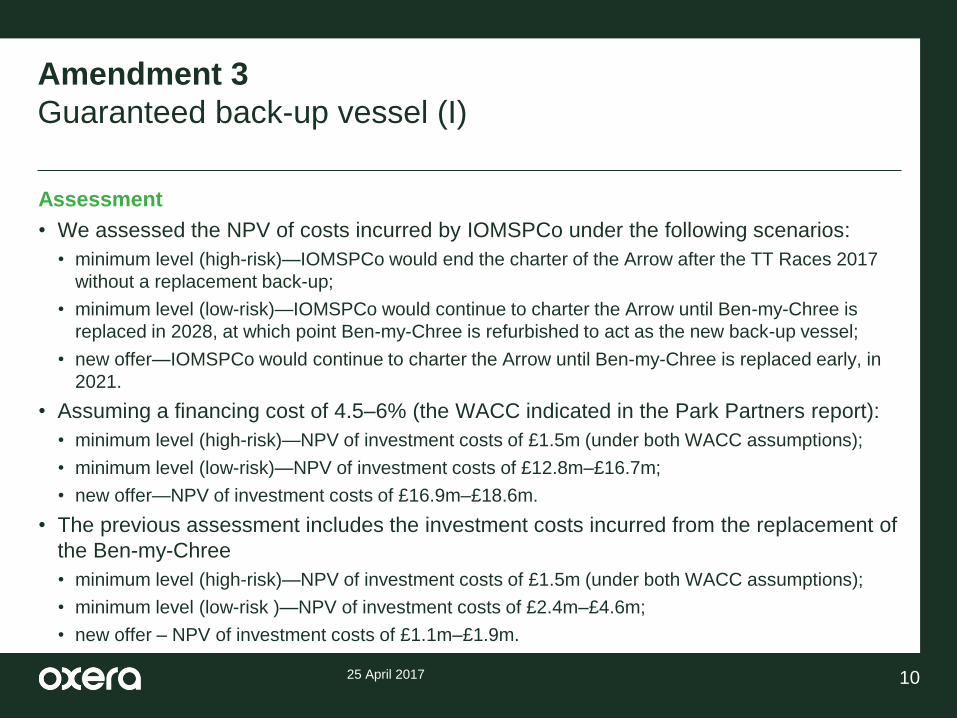

Assessment

• We assessed the NPV of costs incurred by IOMSPCo under the following scenarios:

• minimum level (high-risk)—IOMSPCo would end the charter of the Arrow after the TT Races 2017

without a replacement back-up;

• minimum level (low-risk)—IOMSPCo would continue to charter the Arrow until Ben-my-Chree is

replaced in 2028, at which point Ben-my-Chree is refurbished to act as the new back-up vessel;

• new offer—IOMSPCo would continue to charter the Arrow until Ben-my-Chree is replaced early, in

2021.

• Assuming a financing cost of 4.5–6% (the WACC indicated in the Park Partners report):

• minimum level (high-risk)—NPV of investment costs of £1.5m (under both WACC assumptions);

• minimum level (low-risk)—NPV of investment costs of £12.8m–£16.7m;

• new offer—NPV of investment costs of £16.9m–£18.6m.

• The previous assessment includes the investment costs incurred from the replacement of

the Ben-my-Chree

• minimum level (high-risk)—NPV of investment costs of £1.5m (under both WACC assumptions);

• minimum level (low-risk )—NPV of investment costs of £2.4m–£4.6m;

• new offer – NPV of investment costs of £1.1m–£1.9m.

Amendment 3

Guaranteed back-up vessel (II)

25 April 2017 11

Assessment cont.

• The impact on IOMSPCo would arise from the provision of a back-up vessel through the

Arrow charter being extended, at an additional cost of approx. £15.4m–£17.1m (high-risk

minimum levels) or £1.9m–£4.0m (low-risk minimum levels). This accounts for the

investment in the Ben-my-Chree replacement.

• When evaluated in conjunction with Amendment 1-2, the impact to IOMSPCo absent

investment costs would be cost impact of £0.4m to a savings of £0.4m (high-risk

minimum levels), to a savings range of £1.4m-£2.7m in NPV terms (low-risk minimum

levels). In these assessments, the cost impact of early investment in the Ben-my-Chree is

removed to avoid double-counting.

• The removal of the investment in vessels means Amendment 3 represents a pure cost

savings to IOMSPCo of the chartering costs of the Arrow.

Amendment 5

Revised minimum freight capacity (I)

25 April 2017 12

Background

• This amendment would increase the minimum number of freight lane metres from 7,800

per week to 10,000 per week.

• Freight data from IOMSPCo indicates that it is already in excess of the clause offer for

many weeks of the year. It is not possible to reduce service frequency to the current

minimum of 7,800 lane meters in every week: both frequency of sailings and lane meters

are specified in the current agreement.

Assessment

• The cost impact on IOMSPCo was estimated in two parts:

• frequency impact—estimate of i) the number of sailings in addition to the current level needed to

reach the new offer conditions; and ii) the number of sailings currently above the current minimum

level in the UA;

• cost impact—we estimate the costs or savings of running more or fewer services under both i) and

ii).

• In all cases, we assume that the amount of freight and passenger volumes are not

affected by the number of sailings (revenue impacts are not considered). However, an

increase in service frequency is likely to increase freight traffic, offsetting the cost.

Amendment 5

Revised minimum freight capacity (II)

25 April 2017 13

Assessment cont.

• Frequency impact— We use reported sailings from two sources; Department of

Infrastructure’s records and in records provided by IOMSPCo. Based on IOMSPCo

sailings from 2015.1 The two sources give differing figures. We therefore use a range for

our analysis.

• to meet Amendment 5, IOMSPCo would need to provide 84–181 return sailings above

the current minimum level. This is primarily due to differences in the number of an

additional 54 return sailings would be needed to meet the 10,000 lane metre minimum in every week

of the year;

• IOMSPCo would be able to reduce its current sailings by 30–127 return sailings and still be

compliant with the minimum service levels in the current UA. According to information provided by

the Department of Infrastructure, IOMSPCo is 30 return sailings above the minimum level,2 but it is

unclear whether this accounts for the minimum inbound freight meters. The assessment based on

the schedule provided by IOMSPCo estimates the number of additional sailings above the UA in

2015 at 127 sailings, but these sailings may include required sailings conducted by the Mannanan

or to non-GB ports. Therefore, the 30 return sailings estimate is our preferred estimate.

1 Based on schedule of sailings provided by IOMSPCo for 2015.

2 Based on 2016 estimates.

Amendment 5

Revised minimum freight capacity (III)

25 April 2017 14

Assessment cont.

• Cost impact—under a new offer, IOMSPCo would incur an additional NPV of costs of

approx. of £24.6m-£28.6m above the current service levels:1

• an additional 54 return sailings would incur £1.4m in variable costs annually

• A reduction of 127 return sailings would save £3.3m in variable costs annually. A

reduction of 30 return sailings would save £0.8m in variable costs annually.

• While not estimated, the new higher service level would be likely to generate additional

cargo traffic, which could offset these additional costs. Conversely, a reduction in sailings

is also likely to have traffic impacts, which is likely to reduce revenues.

1 This assessment is based on IOMSPCo’s public accounts and the ratio of variable and fixed operating costs available

from previous Oxera analysis on ferry services.

Amendment 6-7

Expansion of special discount offers (I)

25 April 2017 15

Background

• The previous UA compliance report indicates that 900,000 special offer or discounted

fares were offered in 2016.

• Over this same period, 440,000 journeys were made under the special offers, above the

minimum of 275,000 required.

• This suggests that an extension of special offer fares above the current level is unlikely to

have a significant revenue impact on IOMSPCo, so the additional cost of meeting

Amendments 6-7 is zero compared with the status quo.

• However, because the number of tickets sold at a special offer fare is above the minimum

level, IOMSPCo may be able to generate additional revenue if it were to restrict the

provision of special offer fares to the minimum level. The overall effect would depend on

the elasticity of demand with respect to price.

• We do not consider the possibility of a demand response resulting from the removal of

discounts in this assessment.

Amendment 6-7

Expansion of special discount offers (II)

25 April 2017 16

Assessment

• We assess the additional revenue impacts under two scenarios:

• minimum level—revenue savings from the reduction of special offer fares to minimum (275,000).

Assuming no second-order impacts on passenger demand, 165,000 fares that are currently sold at

discount would be sold at standard rates;

• new offer—additional revenue loss under new Amendments 6 and 7 are expected to be negligible.

Availability of special offer fares already significantly exceeds the numbers sold.

• Based on IOMSPCo fare schedules from 2015, we estimate the revenue-weighted

average standard fare (Class A), and compare to with the revenue-weighted average

discounted fare (Classes B–E) in order to determine an overall average discount on the

standard fare of 10%.

• Given the total number of passenger journeys in 2015, we estimate the average revenue

per passenger journey at the standard fare.

• Relative to current service levels, the impact of the amendment is expected to have

negligible cost implications for IOMSPCo

Amendment 6-7

Expansion of special discount offers (III)

25 April 2017 17

Assessment

• Compared to current minimum service levels, given a revenue gain of 10% for 165,000

journeys, IOMSPCo would gain £0.4m in revenue annually by reducing the number of

special offer fares to the current minimum level. This is equivalent to £7.2m–£8.4m in NPV

terms over the 25-year agreement.

• The assessment does not consider any impacts on traffic from the removal of discounts

(i.e. passengers paying discount fares currently would purchase fares at standard rates,

rather than switch to other modes of travel).

• Because of this assumption, this is a higher-bound estimate based on IOMSPCo’s public

accounts and the estimated ratio of freight and passenger revenues provided by the

Department of Infrastructure.

Amendment 8

Expansion of discount freight haulage rates

25 April 2017 18

Background

• We understand that a majority of freight using IOMSPCo is on a long-term discounted rate of

approx. 40%.

• The volume discounts are applicable for long-term contracts, the terms of which are

unknown.

Assessment

• We assess the revenue impacts under two scenarios:

• minimum level—IOMSPCo would not expand the volume discount, but because of the long-term

arrangements with current customers, it may not be possible to end the current discounts. In this

case, the minimum service level would be equivalent to the current service level;

• new offer—the remaining freight transported by IOMSPCo would be offered a 40% discount on

standard rates.

• Assuming that 80–90% of freight meters are on discounted rates,1 the revenue loss to

IOMSPCo under the new offer would be approximately £27.6m–£32.1m in NPV terms. This

is based on IOMSPCo’s public accounts and the ratio of freight and passenger revenues

provided by Isle of Man Department of Infrastructure.

1 Based on estimates provided by the Department of Infrastructure.

Amendment 9

Revenue growth sharing

25 April 2017 19

• IOMSPCo will share 50% of revenue growth above MRPIJ in each year

• Historical average MRPI +1% is 3.6%, based on the 2012–15 annual index. This is higher

than the average growth rate of turnover assumed by Park Partners, of 2.1%. This

suggests that revenue sharing would not be activated in most years and there would

be no cost to IOMSPCo.

• In principle, one-off years of high growth could trigger the revenue-sharing clause. We

considered historical turnover growth from 2001 to 2015, comparing against MRPI +1%.

• IOMSPCo turnover growth exceeded MPRI +1% in seven years out of 15.

• An NPV of revenue-sharing payments to the Government (brought forward by MRPI) would be

between £20.1m over the 15 years, or £25.1m in NPV over the length of the new agreement.

• This estimate is based on historical data, meaning the events that triggered the above-

average revenue growth would need to occur in the future. A more steady revenue growth

path would mean the clause would not be triggered.

Amendment 10

Manx employment

25 April 2017 20

1,2 Provided by the Department of Infrastructure.

Assessment

• This clause maintains the existing commitment that senior staff will be resident on the Isle

of Man and IOMSPCo will aim for the majority of its staff also to be resident on the Isle of

Man.

• IOMSPCo currently employs about 300 Manx residents, and IOMSPCo management

already has IoM presence.

• A move to replace current crew with EU crew could achieve savings of approx. £2.5m.1

• If the model adopted is similar to that used by Condor Ferries, the replacement of current

crew might incur some cost to IOMSPCo due to searching, transporting and housing the

crew on rotations in Liverpool or Douglas, in addition to costs associated with the

redundancies of current crew.

• Further, IOMSPCo appears to be contributing 15% annually to the current pension

scheme for IOMSPCo staff. Estimates of current payroll salaries of £3.5m suggest a tax

and NI contribution of £920k per year.2

Amendment 11

Fare basket cap by MRPIJ

25 April 2017 21

Assessment

• Under the current UA there is a control on fare increases such that the fare basket does

not increase in real terms.

• The current measure for inflation is MRPI. IOMSPCo has proposed that this would

change to MRPIJ.

• Data on MRPIJ is restricted to two years, so a meaningful comparison with MRPI is not

possible at present. RPI has exceeded RPIJ by approximately 0.7% in the UK.

• We understand that current passenger revenues are in the region of £26.8m.

• Assuming that the RPI–RPIJ wedge in the UK is similar to that in IoM, the fare basket cap would be

worth £0.2m per year at current passenger volumes.

• Given current volumes of freight and passenger traffic, the fare cap would be worth £0.4m per year,

or £6.3m–£7.3m in NPV terms over the length of the new agreement.

• This is a broad estimate and does not account for compositional changes to the fare basket.

• The cost is dependent on the evolution of the MRPI–MRPIJ wedge.

Amendment 12

Guaranteed use of Liverpool ports

25 April 2017 22

Assessment

• The UA specifies a current minimum of 1,040 sailings to NW UK ports. This also specifies

that services must be daily to Liverpool in summer and weekly in winter, the remainder of

which could, in theory, be diverted to Holyhead.

• IOMSPCo has already agreed to use the new Liverpool landing stage in 2026.

• In order to assess the impact of this amendment, it would be relevant to consider whether

there are current contract conditions IOMSPCo has with its current freight customers

which would reduce its ability to immediately divert routes to Holyhead. In cases where

such conditions exist, diversion from Liverpool to Holyhead could also result in significant

pressure from current customers or even demand reductions.

• Depending on conditions in current freight contracts, it may not be credible for IOMSPCo

to propose the immediate diversion of services to Holyhead.

Summary of quantitative assessment

Likely and significant costs of the agreement

25 April 2017 23

Amendments which

are likely to result in

costs above current

UA minimum

These represent a cost

to IOMSPCo and are

less likely to be offset by

a commercial rationale

• Amendment 1-2 New investment in vessels

• These amendments are estimated to represent a cost to IOMSPCo

of approx. £10.5m–£12.3m in NPV terms, depending on financing

cost assumptions.

• This does not include the likely revenue increase to IOMSPCo of

new vessels from increased demand, so the cost impacts are likely

to be lower.

• Amendment 3 Guaranteed back-up vessel

• Provision of a back-up represents a cost to IOMSPCo of approx.

£15.4m–£17.1m in NPV terms in a high-risk scenario where the

charter for the Arrow ends in 2017, or £1.9m–£4.0m in the low-risk

scenario.

• When considered in conjunction with the Amendment 1-2, the cost

impact considers IOMSPCo’s investment cost in a Ben-my-Chree

replacement twice. Removing this investment, the high-risk impact

becomes £0.4m to -£0.4m (a benefit) in the high-risk scenario, and a

benefit of £1.4m-£2.7m in the low-risk scenario.

Summary of quantitative assessment

Potentially significant costs of the agreement

25 April 2017 24

• Amendment 5 Revised minimum freight capacity

• Revised minimum freight capacity is estimated to incur £24.6m-

£28.6m in NPV terms (above current service levels)

• However, these costs are likely to be offset by revenue increases.

• Amendment 8 Expansion of discount freight haulage rates

• This is expected to represent a cost to IOMSPCo of approx. £27.6m-

£32.1m in NPV terms relative to current service levels, depending on

the current share of full-priced freight traffic.

• This is likely to be a higher estimate, as any expanded discount

would be likely to have revenue impacts. It is also not clear whether

it would be in the commercial interest of IOMSPCo to withdraw these

discounts even in the absence of a new agreement

Amendments that may

create costs above

current UA minimum

Cost likely to be offset

by a commercial

rationale

Summary of quantitative assessment

Low or unlikely costs of the agreement

25 April 2017 25

Amendments unlikely

to create significant

cost above current UA

minimum

• Amendment 6-7 Expansion of special discount offers

• Costs of the amendment relative to current service levels is

expected to be zero. Relative to current minimum service levels,

these amendments are expected to represent a cost of £7.2m–

£8.4m in NPV terms. These costs are expected to be offset by

revenue increases.

• Amendment 9 Revenue growth sharing

• This represents a cost to IOMSPCo of approx. £25.1m in NPV terms

over the span of a new UA (until 2041).

• However, this assessment is based on assumptions about the

revenue growth and volatility being similar to historical levels. If

revenue growth is smooth, then the expected value of this to the

Government is zero.

• Amendment 11 Fare basket cap by MRPIJ

• This represents a cost to IOMSPCo of approx. £6.3m–£7.3m in NPV

terms over the span of a new UA (until 2041).

• However, because of the recent introduction of MRPIJ, the actual

cost impact is dependent on the evolution of the wedge between

MRPI and MRPIJ over time.

Conclusions

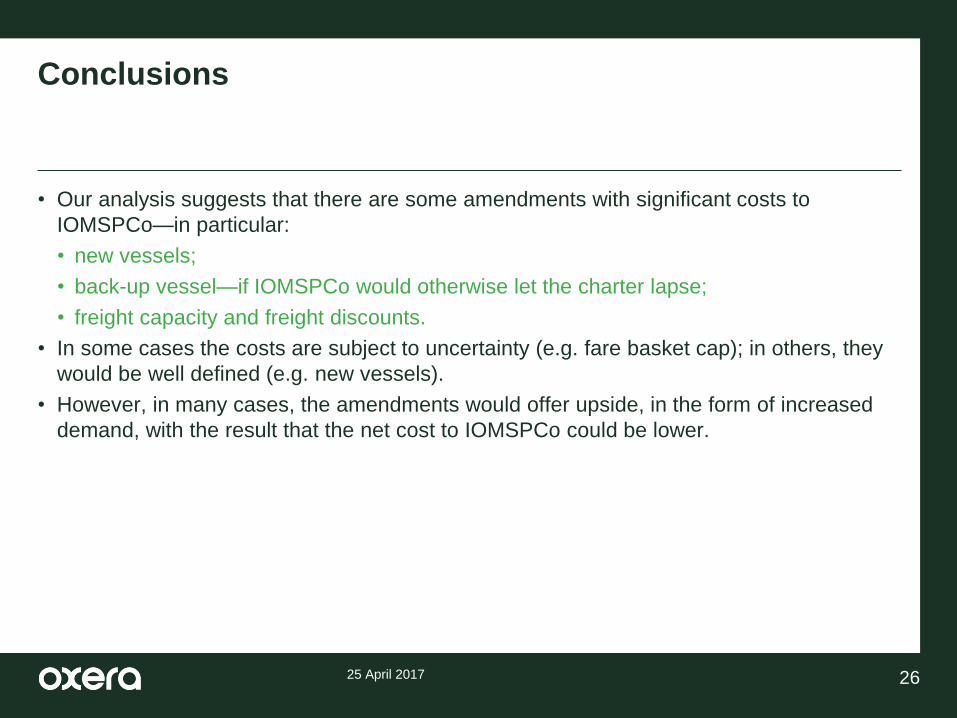

• Our analysis suggests that there are some amendments with significant costs to

IOMSPCo—in particular:

• new vessels;

• back-up vessel—if IOMSPCo would otherwise let the charter lapse;

• freight capacity and freight discounts.

• In some cases the costs are subject to uncertainty (e.g. fare basket cap); in others, they

would be well defined (e.g. new vessels).

• However, in many cases, the amendments would offer upside, in the form of increased

demand, with the result that the net cost to IOMSPCo could be lower.

25 April 2017 26

Contact:

Sean Thomas

+44 (0) 20 7776 6687

www.oxera.comFollow us on Twitter @OxeraConsultingOxera Consulting LLP is a limited liability partnership registered in England

and Wales No. OC392464, registered office: Park Central, 40/41 Park End

Street, Oxford, OX1 1JD, UK. The Brussels office, trading as Oxera

Brussels, is registered in Belgium, SETR Oxera Consulting LLP 0651 990

151, registered office: Avenue Louise 81, Box 11, 1050 Brussels, Belgium.

Oxera Consulting GmbH is registered in Germany, no. HRB 148781 B

(Local Court of Charlottenburg), registered office: Rahel-Hirsch-Straße 10,

Berlin 10557, Germany.

Although every effort has been made to ensure the accuracy of the

material and the integrity of the analysis presented herein, Oxera accepts

no liability for any actions taken on the basis of its contents. No Oxera

entity is either authorised or regulated by the Financial Conduct Authority

or the Prudential Regulation Authority. Anyone considering a specific

investment should consult their own broker or other investment adviser.

Oxera accepts no liability for any specific investment decision, which must

be at the investor’s own risk.

© Oxera, 2017. All rights reserved. Except for the quotation of short

passages for the purposes of criticism or review, no part may be used or

reproduced without permission.

www.pwc.co.uk

IoMSPC’s EconomicContribution to the Isleof Man

This report has been prepared for and only for the Isle of Man Steam Packet Company

Limited (IoMSPC) in accordance with the engagement letter dated 4 December 2015,

subsequently varied by an agreement dated 16 March 2017, and for no other purpose.

We do not accept or assume any liability or duty of care for any other purpose or to any

other person to whom this report is shown or into whose hands it may come save

where expressly agreed by our prior consent in writing.

March 2017

APPENDIX 3

1

The IoMSPC’s Economic Contribution

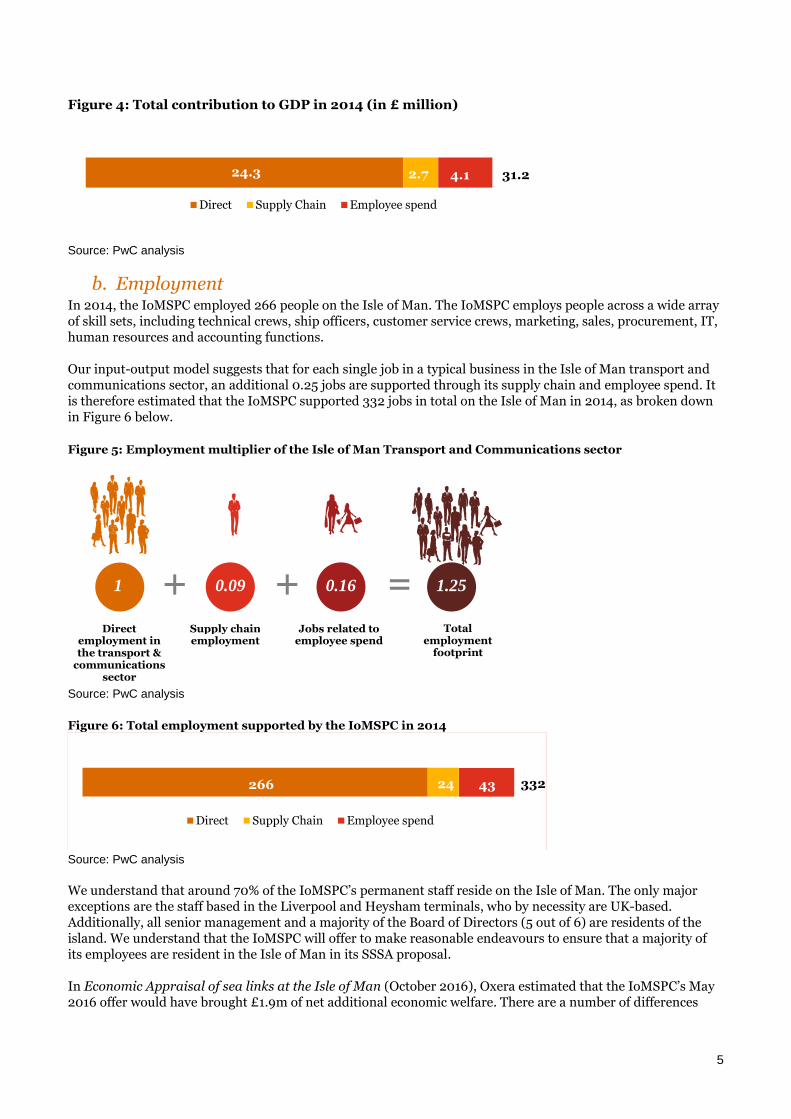

1. Summary of Findings We set out the background to this work and our methodology in Section 2 and Section 3 respectively.

In 2014, we estimate the Isle of Man Steam Packet Company Ltd (IoMSPC) contributed a total of£31.2 million per annum to the Isle of Man’s GDP and supported 332 jobs on the island. For everyperson employed by the IoMSPC on the island, it supported an additional 0.25 jobs elsewhere in the Isle ofMan economy. This is set out in more detail in Section 4.

We estimate that the IoMSPC’s current policy of employing a predominantly Isle of Man-based workforcecontributed an additional £5.1 million and supported an extra 148 jobs in the island’s economy in 2014,compared to an operator with a workforce profile comparable to the European average. This is set out inmore detail in Section 5.

In its Strategic Sea Services Agreement (SSSA) proposal, IoMSPC suggested to replace Ben-my-Chree witha new Ro-Pax vessel in 2020/21. IoMSPC estimates that it could allow additional visitors to travel to theisland during the TT Motorcycle Festival. Based on the consumption pattern suggested by a surveyconducted by the Isle of Man Government Treasury, these additional visitors could potentially add £2.8million to the island’s GDP in 2014 prices on a yearly basis. We also estimate an additional 42 jobs couldbe created. This is set out in more detail in Section 6.

2. BackgroundThis is a PwC study commissioned by the Isle of Man Steam Packet Company Ltd (IoMSPC), the only operatorof scheduled ferry services to and from the Isle of Man. This study explores the size and significance of theIoMSPC’s economic and employment impacts on the island. The purpose of this report is to build awarenesswithin the IoMSPC and amongst its stakeholders of the economic value that the company brings to the island.

This study covers the IoMSPC as a whole. We first estimated the Company’s contribution to the Isle of Maneconomy and employment in gross terms, i.e. without taking into account what would have happened in theabsence of the IoMSPC.

We then estimate how this gross contribution might have been affected by the Company’s commitment to usingManx staff, and how it could have been enhanced by a key provision with the Company’s offer of replacing Ben-my-Chree, the Company’s current roll-on/roll-off passenger (Ro-Pax) ferry with a new vessel with largercapacity.

We understand that the Company currently operates under the terms and conditions of an existing UserAgreement. Based on discussions with the IoMSPC we understand that the current level of operations is inexcess of the User Agreement levels. It should be noted that PwC has not undertaken any work to estimate theimpact on GDP if the SSSA does not proceed and IoMSPC reverts to operating at the mandatory levels outlinedin the existing agreement.

In our work for this report, we treated the IoMSPC as a typical business in the Isle of Man transport andcommunications sector. We only looked at its operations, procurement, and employment effects on the Isle ofMan. Except where explicitly stated, we did not take into account the changes in visitor flow into or out of theisland as a result of the IoMSPC’s operations or any proposed change to them. We have also based ourcalculations on financial information provided by the IoMSPC, which we did not audit. There are othereconomic, social and environmental indicators that may capture the general welfare of the Manx populationmore fully, but impacts that are not measured by GDP and employment are outside of the scope of this study.

2

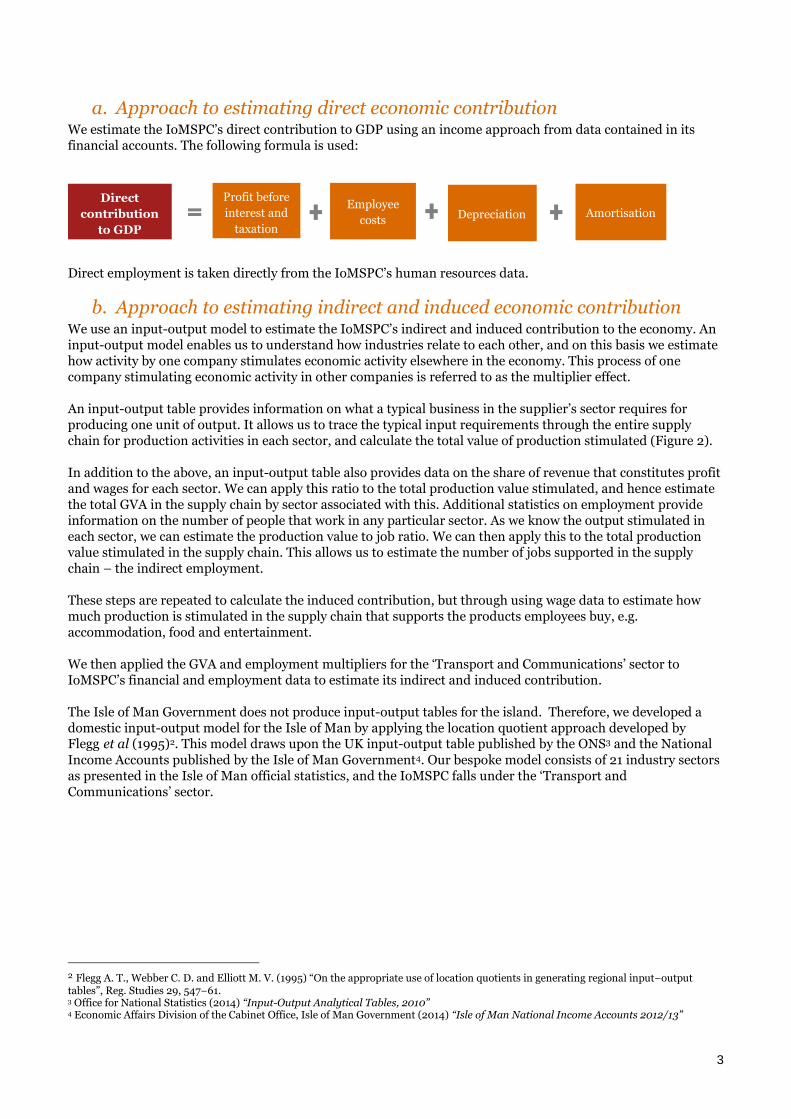

3. Measuring economic contributionWe capture the IoMSPC’s economic contribution to the Isle of Man economy using two indicators. These are:

1. Contribution to GDP: Measured in terms of Gross Value Added (GVA); and

2. Employment supported: Expressed as the number of jobs (headcount).

GVA measures the value that is generated, or added, by a business or an industry sector. It is measured as thedifference between the value of goods and services produced and the goods and services used as an input totheir production. It is the company-level and sector-level equivalent of GDP: if we sum the GVA of all individualsectors in an economy, we arrive at a measure of that economy’s GDP1.