Strategic Procurement

74

Supply Chain Management S iP Strategic Procurement Course Introduction Course Introduction Section 1.0 Section 1.0

-

Upload

raluca-ungureanu -

Category

Documents

-

view

253 -

download

3

description

SUPPLY CHAIN MANAGEMENT

Transcript of Strategic Procurement

Supply Chain ManagementS i PStrategic Procurement

Course IntroductionCourse IntroductionSection 1.0Section 1.0

Course Introduction

• Objectives • Overview of SCMOverview of SCM• Class Schedule• Class Courtesy• Method of Instruction• Grading

Objectives of the Advanced Course

• be familiar with vocabulary and concepts• be familiar with vocabulary and concepts • be able to describe and implement advanced procurement

strategiesstrategies • have a greater understanding of the role of the

procurement department in strategic planning• have experience synthesizing course content to solve

questions that require combining concepts, techniques, and assumptions

• have the opportunity to demonstrate commitment to group effectivenesseffectiveness

Overview of (SCM) Certificate

Introduction to Supply Chain Management Introduction to Supply Chain Management Introduction to Procurement Strategies in Supply Chain Strategic Procurement in Supply Chain Management Planning and Scheduling in Supply Chain Management• Inventory, Warehousing and Analysis in Supply Chain Management

T h l d E P i S l Ch i M• Technology and E‐Procurement in Supply Chain Management• Project Management – An Overview• Managing High Performance TeamsManaging High Performance Teams• Effective Professional Communications• Final Assessment Paper

WeekendScheduleScheduled Timeframe Material CoveredWeeknight 6:30 – 9:30 pm

Course Introduction Objectives of Strategic Procurement Course Review – Case Methodology Group Presentation – Group Selection; Case Assignment; Discussion 2 0 Cost Management Discounts & Negotiation 2.0 Cost Management, Discounts & Negotiation

Saturday 8:30am ‐ 5:00 pm

Assigned Question Review Review Case 5‐1 “B&L Inc.” 3.0 Make, Buy, Insourcing / Outsourcing Video – “Is Walmart Good for America” Review Case 14‐1 “Trojan Technologies” 4.0 Global Supply Management

Weeknight 6:30 – 9:30 pm

Assigned Question Review Review Case 6‐1 “Moren Corporation (A)” 5.0 Capital Goods Group Work

Saturday Assigned Question ReviewSaturday 8:30am – 5:00 pm

Assigned Question Review 6.0 Services Review Case 2‐1 “Spartan Heat Exchangers Inc.” Group Case Study Presentations 7.0 Strategy in Purchasing & Supply Management SCM Concepts Review SCM Concepts Confirmation SCM Concepts Confirmation

Class Courtesy

• Prompt and regular in attendance• Discuss and participate enthusiastically• Personal experiences and opinions are valued• Allow & encourage others to contribute

L i i i l i & ll b ti• Learning is inclusive & collaborative• Respect the other person’s point of view• Respect confidentialityRespect confidentiality• Confine discussion to the topic• Asides discussed at break

Method of Instruction

• Lecture on materials 30%• Interactive class discussions 20%• Review of Questions / Answers 25%

C t di 25%• Case studies 25%

Grading Attendance 35% Concepts Confirmation 35% Group Case Study 30%

For Final Grades, see Grade Translation Table

Grading Translation Table

A + 95 – 100A 90 – 94A 85 89A ‐ 85 – 89B + 80 – 84B 75 – 795 9B ‐ 70 – 74C + 65 – 69C 60 – 64F 59 and below

Review Questions

• Chapter 11: page 307 ‐ #’s 1, 2, 8Ch 30 ’ 2 3• Chapter 5: page 130 ‐ #’s 2, 3, 5

• Chapter 14: page 412 ‐ #’s 3,6• Chapter 6: pages 155 156 #’s 3 5• Chapter 6: pages 155‐156 ‐ # s 3, 5• Chapter 6: pages 155‐156 ‐ #’s 4, 8• Chapter 2: pages 37‐38 ‐ #’s 1, 8, 10p p g , ,

In‐Class Case Studies

• Case 11‐1 “Deere Cost Management” pages 308‐309C 5 1 “B&L I ” 131 132• Case 5‐1 “B&L Inc.” – pages 131‐132

• Case 14‐1 “Trojan Technologies” – pages 413‐415• Case 6‐1 “Moren Corporation (A)” – pages 156‐158• Case 6‐1 Moren Corporation (A) – pages 156‐158• Case 6‐2 “Moren Corporation (B)” – pages 158‐159• Case 2‐1 “Spartan Heat Exchangers Inc.” – pages 39‐40p g p g

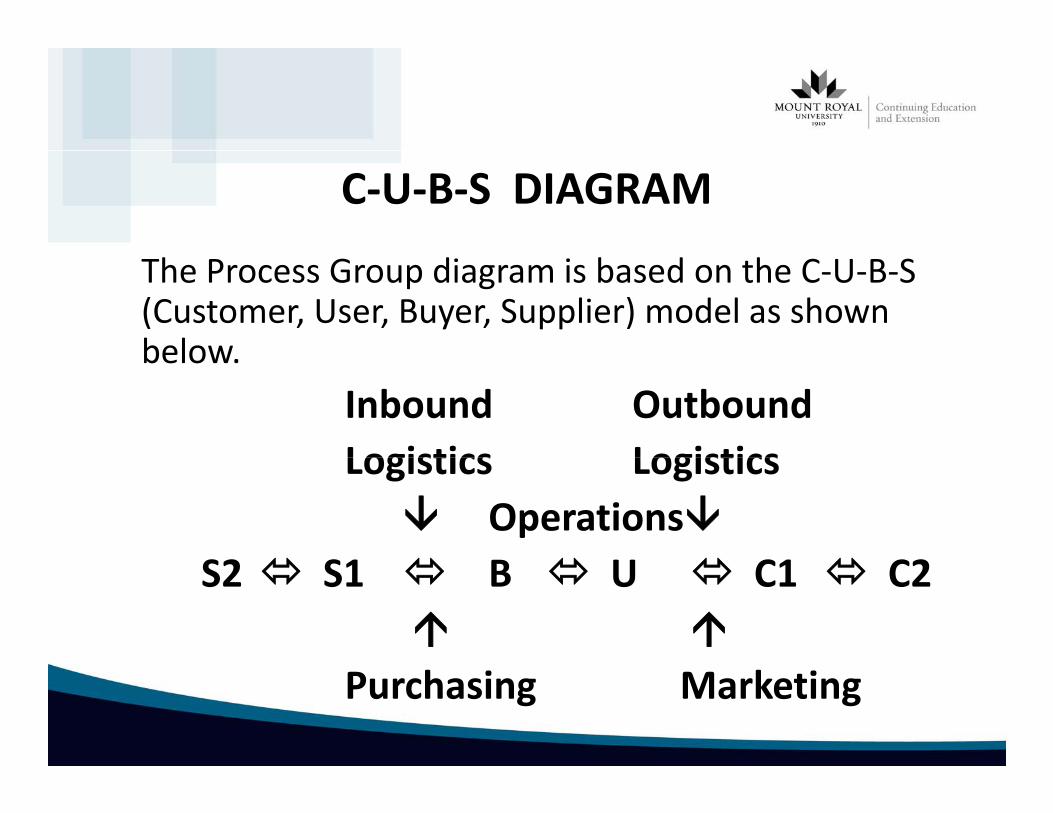

C‐U‐B‐S DIAGRAM

The Process Group diagram is based on the C‐U‐B‐S (Customer, User, Buyer, Supplier) model as shown belowbelow.

Inbound OutboundLogistics LogisticsLogistics Logistics Operations

S2 S1 B U C1 C2S2 S1 B U C1 C2

Purchasing Marketing

Case Study Format

• Organization BackgroundD fi i th I• Defining the Issue

• Analyzing Case Data• Decision CriteriaDecision Criteria• Alternative Analysis and Evaluation• Action and Implementation Planp• Assumptions, Presentation & Organization

Final Assessment Paper• The goal of the Final Assessment paper in the Mount Royal

University (MRU) Supply Chain Management Certificate Program is to give the learner an opportunity to apply supply chain management fundamentals principles and practices tochain management fundamentals, principles and practices to a real‐life project.

• Through the writing of a paper showing the integration of all h i hi h S l Ch i Mthe processes within the Supply Chain Management Knowledge Areas, a learner is able to show evidence of their understanding of the key components of the nine classroom courses in the Supply Chain Management Certificate Programcourses in the Supply Chain Management Certificate Program.

• A requirement for cross‐institution recognition of the Certificate in Supply Chain Management.

Supply Chain Management

Strategic Procurement g

Cost Management, Discounts, & NegotiationSection 2.0 (Chapter 11)

Supplier’s CostsSuppliers often not challenged as to their own supply chain costsSuppliers often not challenged as to their own supply chain costs due to several misconceptions:

1. Suppliers do not know their own costs.2 Interpretation of what constitutes a cost subjective2. Interpretation of what constitutes a cost subjective.3. Refusal to disclose such information.4. Seller’s costs not always what market prices at.5. Many SCM professionals not interested in suppliers costs, only focus on how

low they can get the price.

Overriding concern – achieve the best price consistent with quality, quantity, delivery and service.q y, q y, yNeed to be able to judge the reasonableness of a suppliers proposed pricing regime.

Estimating Input CostsSeveral methods to help SCM professionals in estimatingSeveral methods to help SCM professionals in estimating supplier’s costs:• Cost‐based Pricing – readily available data (market, indices)• Overhead Costs – indirect costs for mfg facilities (fixed %, allocated cost for entire

estimated yearly production)• Tooling & Engineering Costs – incl. in overhead, need to segregate for analysis and

determine what is reasonabledetermine what is reasonable• Gen. & Admin. Costs – selling, promotion, advertising. Need to analyze in relation to

own requirements• Material Costs – estimate using a sample bill of materials or from reverse engineering a

sample under consideration

• Direct Labour Estimates – use of indices, geographical considerations

l f hi ( )Total Cost of Ownership (TCO)TCO includes all relevant costs such as:

• Direct material • Storage• Administration• Follow‐up

E diti

• Scrap• Warranty

S i• Expediting • Inbound transportation • Inspection and testing

• Service• Downtime• Customer returnsInspection and testing

• ReworkCustomer returns

• Lost sales

TCO (cont’d)TCO Analysis to be used for:y

• Highlighting cost reduction opportunities• Aiding supplier evaluation and selection• Providing data for negotiationsProviding data for negotiations• Focusing suppliers on cost reduction opportunities• Highlighting the advantages of expensive high‐quality versus cheap, low‐cost

materials• Clarifying and defining supplier performance expectations;• Creating a long‐term supply perspective• Forecasting future performanceg p

Do this by; having seller willingly share some, most, or all, of cost data, developing own cost model, or a combination of both.

Target Pricing• In most basic form; derived by the organization establishing aIn most basic form; derived by the organization establishing a

price at which it plans to sell its finished product.

• All organizational prerequisite costs, including expected g p q , g pnormal operating profit, are subtracted from this final sales price to derive a basic target cost for each item. Sourcing works with potential suppliers to achieve the materials and services cost targets.

• Design to cost, on the part of design engineering

• Manufacture to cost, on the part of production

• Purchase to cost, on the part of sourcing / supply, p g / pp y

Activity Based Costing (ABC)

• Attempts to turn indirect costs into direct costs; by specifically and methodically tracking the cost drivers behind all direct and indirect y goverhead costs related to a specific manufacturing activity.

• ABC can be used as a tool to reduce supplier costs by eliminating non‐value added activities, reducing activity occurrences, and reducing the , g y , gcost driver rate.

• Data is the essential key element in all of this activity. Suppliers work cooperatively to provide as much of data as possible. p y p p

• The cost of an activity itself may be targeted for improvements in efficiency through further value analysis and system redesign.

Discounts• Cash Discounts – securing of prompt payment of an account; g p p p y

acknowledging the time value of money and the potential return of monies used for additional production. The focus should be on the net priceprice.

• Trade Discounts – most often granted because the purchaser is a particular type of distributor, or user, who is able to sell an item at a lower price due to existing infrastructure and business contacts. The discount often approximates the cost of doing business for the manufacturer.

• M lti l Di t th di t b ild h th d t• Multiple Discounts – these discounts build upon each other; used to further incent a customer to purchase from a particular manufacturer, and to remain with them over the long run.

Discounts (cont’d)Q tit Di t t d f b i i ti l titi d• Quantity Discounts – granted for buying in particular quantities, and vary roughly in proportion to the amount purchased. Setup costs, transportation costs, and production costs all come into play in considering the type and amount of quantity discounts offered by a particular seller.

Inventory cost considerations

Early production order considerations

Cumulative discount considerations

Follow‐on order discount considerations

NegotiationsThe most expensive means of price determination requiringThe most expensive means of price determination, requiringboth seller and buyer to come to a common understanding,after intense discussion, of the essentials of a purchase / sale

t t i l dicontract, including: Quality

Support

Supply

Transportation

Price

Terms

Remember: Both parties must be able to reach theirobjectives in order to consider the negotiations a success!!!objectives in order to consider the negotiations a success!!!

Negotiations (cont’d)Negotiations not to be confused with price haggling; “nickle‐and‐diming” a seller to as low a price as possible without recognizing their costs and need for a profit Bad andrecognizing their costs and need for a profit. Bad and unethical business practices include:

Misleading the seller in any way

Erroneous volumes

Fictitious competitors

Unnecessarily prolonged negotiations, with no intent to settle

Negotiations (cont’d)Planning & Preparing for Negotiations:Negotiations:1. Develop specific objectives/outcomes

based on scenarios.

2 Gather pertinent data; especially cost

6. Set each other’s positions on each issue, assumed or otherwise, and develop strategies to overcome or2. Gather pertinent data; especially cost

data.

3. Determine the facts of the situation; what is known and unknown.

develop strategies to overcome or strengthen.

7. Plan the negotiation strategy; which items come first, second, and which what is known and unknown.

4. Determine the issues that may generate disagreements and develop potentially acceptable resolutions.

, ,items can be compromised.

8. Brief all individuals on the team who will be participating.

5. Analyze the positions of strength as well as weaknesses for both sides; develop solutions to both.

9. Dress rehearsal.

10. Actual conduct of the negotiations in accordance with the plan.

Review Questions for Next Class

• Chapter 11: page 307 #’s 1 2 8• Chapter 11: page 307 ‐ #’s 1, 2, 8• Chapter 5: page 130 ‐ #’s 2, 3, 5

In‐Class Case Study for Next Class

• Case 5‐1 “B & L Inc.” – pages 131‐132• Case 14‐1 “Trojan Technologies” – pages 413‐415

Supply Chain Management

Strategic Procurement

Make, Buy, Insourcing / OutsourcingMake, Buy, Insourcing / OutsourcingSection 3.0 (Chapter 5)

Reasons for Making Instead of iBuying

• quantities are too smallquantities are too small • quantity requirements may be unusual as to require special processing

methods• to preserve technological secrets• to obtain lower costs• to take advantage of idle equipment and labor• to ensure steady running of the corporation’s own facilities• to avoid sole sourcing dependencies• competitive, political, social, or environmental reasons • emotional or personal attachment to in‐house production

Reasons for Buying Outside

• lack administrative or technical experiences• excess production capacity

l h d h b l l f f h• suppliers may have a reputation and have built a real preference for their component

• challenges of maintaining long‐term technological and economic viability for a non core activityfor a non‐core activity

• a decision to make, once made, is difficult to reverse• it is difficult to determine the true long term costs of the make decision• there is more flexibility in selecting possible sources and substitute itemsthere is more flexibility in selecting possible sources and substitute items• superior supply management expertise• acquisition generally requires less overhead

SubcontractingManaging a sub‐contract is a complex activity. Some points to g g p y premember are:

• Cost control of the subcontract begins with the negotiation of a• Cost control of the subcontract begins with the negotiation of a fair and reasonable price

• Schedule control requires the development of a good master schedule

• Technical control must be instigated to ensure that the end product conforms to all of the performance parameters

• Configuration control ensures that all of the changes aredocumented

Reasons for Outsourcing

• reduce and control operating units• improve company focus

i t ld id biliti• gain access to world‐wide capabilities• free up internal resources for other purposes• resources that are not available internally• accelerate re‐engineering initiatives and benefits• function is difficult to manage or is currently out of control• make capital funds available for other projects / initiativesmake capital funds available for other projects / initiatives• share risks with supplier (there is a cost to this)• cash infusion, if equipment / processes / technology sold

Purchasing Role in Outsourcing

• providing a comprehensive, competitive process

• identifying opportunities for outsourcingy g pp g

• aiding in the identification and selection of potential sources

• identifying potential relationship issues, and solving them

• Developing, negotiating and finalizing the contract

• ongoing performance measurement, monitoring and management of the

relationship

Purchaser‐Supplier Relationships

Traditional• Lowest Price

Partnership• Total cost of ownership

• Specification driven• Short term; reacts to market• Trouble avoidance

• End customer driven• Long term• Opportunity maximization

• Purchaser’s responsibility• Tactical• Little sharing of information on both

id

• Cross functional teams & top management involvement

• StrategicSh h t & l t lsides • Share short & long term plans

• Share risk & opportunity• Standardization

J i• Joint venture• Share data

Review Questions for Next ClassReview Questions for Next Class

• Chapter 5: page 130 ‐ #’s 2, 3, 5p p g , ,

In‐Class Case Study for NextIn‐Class Case Study for Next Class

• Case 6‐1 “Moren Corporation (A).” – pages 156‐158

Supply Chain Management

Strategic ProcurementStrategic Procurement

Global Supply ManagementS i 4 0 (Ch 14)Section 4.0 (Chapter 14)

Reasons for Global Purchasing

•Labour costs in the producing country may be substantially lower E h f b i ff h•Exchange rates may favor buying off‐shore

•Equipment and processes used by the international supplier may be more efficient

•Availability may be an issue, and given short lead times, you may have no choice but to source internationally

•Delivery may be quicker across the USA border versus shippingDelivery may be quicker across the USA border versus shipping from another distant part of the country (east‐west typically slower than north‐south in Canada)

International Purchasing Challenges• source locations and evaluation• source locations and evaluation• lead/delivery time•physical delivery• language/customs•ethics; at home and abroad•exchange ratesg• labour issues; at home and abroad• time zones/management issues•hidden costs•hidden costs •customs• Incoterms (who is responsible for insurance, shipping claims, insurance claims, customs, taxes, duties)

Intermediaries

•brokers•agents•agents• trading companies•barter/swaps•offsets

Review Questions for Next ClassReview Questions for Next Class

•Chapter 14: page 412 ‐ #’s 3,6

In‐Class Case Study for Next ClassIn Class Case Study for Next Class

• Case 6‐1 “Moren Corporation (A).” – pages 156‐158Case 6 1 Moren Corporation (A). pages 156 158

Supply Chain Management

Strategic ProcurementStrategic Procurement

Capital GoodsS i 5 0 (Ch 6)Section 5.0 (Chapter 6)

Challenges of Equipment Buying•Strategic risk •Large dollars• Infrequent purchaseInfrequent purchase•Total cost difficult to calculate•The best time to buyE i t l i t•Environmental impact

•Tax consideration•Technology forecasting•Length of start‐up• Integration with established procedures

Reasons to Purchase Equipment•capacity•economy in operation and maintenance• increased productivity• increased productivity•better quality•dependability in use• savings in time or labor costs•durability• safety, pollution, and emergency protectiony, p , g y p

Cost Considerations

• Is the equipment intended for replacement only, or to provide additional capacity?

• What is the installed cost of the equipment?What is the installed cost of the equipment? • What will start‐up costs be? • Will the equipment installation create problems with plant layout? • What will be the maintenance and repair costs, who will provide repair parts, and at what cost? Who will do the actual repairs when required?

• What will be the operating costs; including power and labour? • What are the machine hours the equipment will be used? • At what rate is the machine to be depreciated? • What financing costs are involved?

Selection of the Sourceli bili f h ll• reliability of the seller

• reasonable price• selection of the right type of equipment• proper installation• proper installation• common interests in efficient operation• availability of repair parts and services• satisfactory past relationshipssatisfactory past relationships• patent infringement considerations• extent of liability for accidents to employees• full regulatory safety complianceg y y p• consequential damage considerations• old or obsolete equipment disposal

Reasons for Buying Used Equipmenty g q p

•buyer’s funds are scarce• for use in a pilot or experimental plant• for use in a pilot or experimental plant• for use with a special or temporary order•where the machine will be idle substantial amounts of time• for the use of apprentices• for maintenance departments• for faster delivery when time is essentialy•when a used machine can be easily modernized in relatively little time

Advantages of Leasing Equipmentg g q p

• lease rentals are expenses for income tax purposesp p p• small initial outlay (may actually cost less)•availability of expert service• risk of obsolescence reduced• risk of obsolescence reduced•adaptability to special jobs and seasonal business• test period provided before purchase•burden of investment shifted to supplier

Disadvantages of Leasing EquipmentDisadvantages of Leasing Equipment• final cost may be too high• surveillance by lessor entailedsurveillance by lessor entailed• less freedom of control and use

Types of Leasesyp

•Financial leaseFinancial lease•Operational lease

Review Questions for Next ClassQ

•Chapter 6: pages 155 156 #’s 3 5•Chapter 6: pages 155‐156 ‐ #’s 3, 5•Chapter 6: pages 155‐156 ‐ #’s 4, 8•Chapter 2: pages 37‐38 ‐ #’s 1, 8, 10

In‐Class Case Study for Next ClassIn Class Case Study for Next Class

• Case 2‐1 “Spartan Heat Exchangers Inc.” – pages 39‐40

Supply Chain Management

Strategic Procurement

S i S i 6 0 (Ch 6)Services Section 6.0 (Chapter 6)

Diversity of Services Purchasing

• advertising• architecturalarchitectural• banking & auditing• programming• construction• consulting• courier• customs brokerage• data processing• environmental cleanup• engineering design

t t• waste management

What Makes Services Different?

• the inability to store services is the most common attribute differentiating services from goodsdifferentiating services from goods

• timing of the delivery has to coincide with the purchaser’s specific needs

•difficulty in assessing quality is another differentiating attribute of services

• inspection prior to delivery is often very difficultp p y y• specification and measurement of quality in a service may also present significant difficulties

Framework for Analyzing Services

•Value of the service•Degree of repetitivenessg p•Degree of tangibility•Direction of the service•Production of the service•Production of the service•Nature of the demand•Nature of the service delivery

f•Degree of customization•Skills required for the service

The Acquisition Process for Servicesq

•Need recognition and specification•Analysis of supply alternatives•Analysis of supply alternatives•The Purchase Agreement; including special provisions

sourcing i i pricing source options make or buy

•Contract AdministrationContract Administration follow‐up and expediting quality control and supplier evaluation payment records & other aspects of contract administration records & other aspects of contract administration

Review Questions for Next ClassQ

• Chapter 6: pages 155‐156 ‐ #’s 4, 8p p g ,• Chapter 2: pages 37‐38 ‐ #’s 1, 8, 10

In‐Class Case Study for Next ClassIn Class Case Study for Next Class

• Case 2‐1 “Spartan Heat Exchangers Inc.” – pages 39‐40

Supply Chain ManagementSupply Chain Management

Strategic ProcurementStrategic Procurement

Strategy in Purchasing & Supply Management

Section 7.0 (Chapter 2)( p )

Levels of Strategic Planning

• Corporate: What business are we in? How will we efficiently and effectively allocate our resources? y y

• Unit: Plans of each of the business units molded to contribute to the corporate strategy?F ti Th “h ” f h f ti l ’• Function: The “how” of each functional area’s contribution to the business strategy, involving the allocation of all internal resources.

Supply’s Contribution to Business StrategySupply

ObjectivesOrganizational Objectives

Supply St t

Organizational St tStrategy Strategy

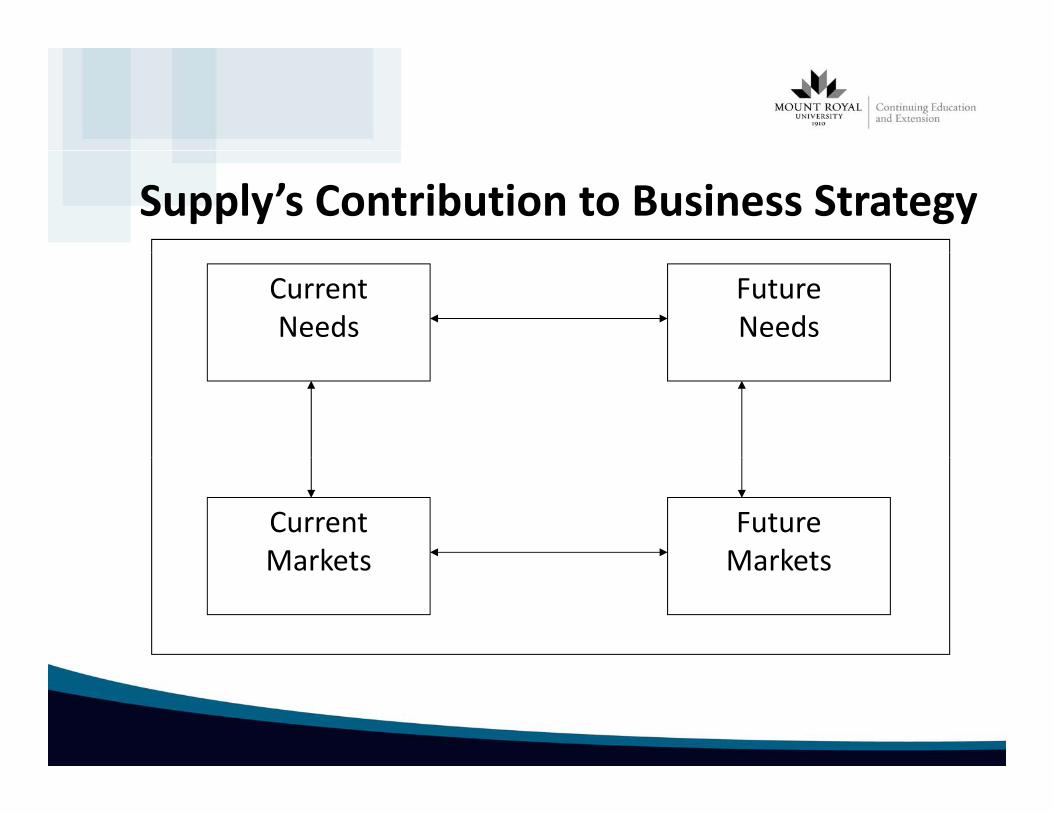

Supply’s Contribution to Business Strategy

Current Needs

Future Needs

CurrentMarkets

Future MarketsMarkets Markets

Supply’s Contribution to Business Strategy• social issues and trends• government regulations and controls• financial planning with suppliersfinancial planning with suppliers• product liability exposure• economic trends and environment• organizational changes• product or service line• competitive intelligence• technology• e‐commerce• investment• mergers/acquisitions/divestmentti b d titi• time‐based competition

Competitive Intelligence

•How will competitors’ directions affect the supply market? p pp y•How will the market react to a move against the prevailing trends?

•What current commodities may be redundant in the short•What current commodities may be redundant in the short, medium, and long‐term?

•What is being done to mitigate the effects of that redundancy?

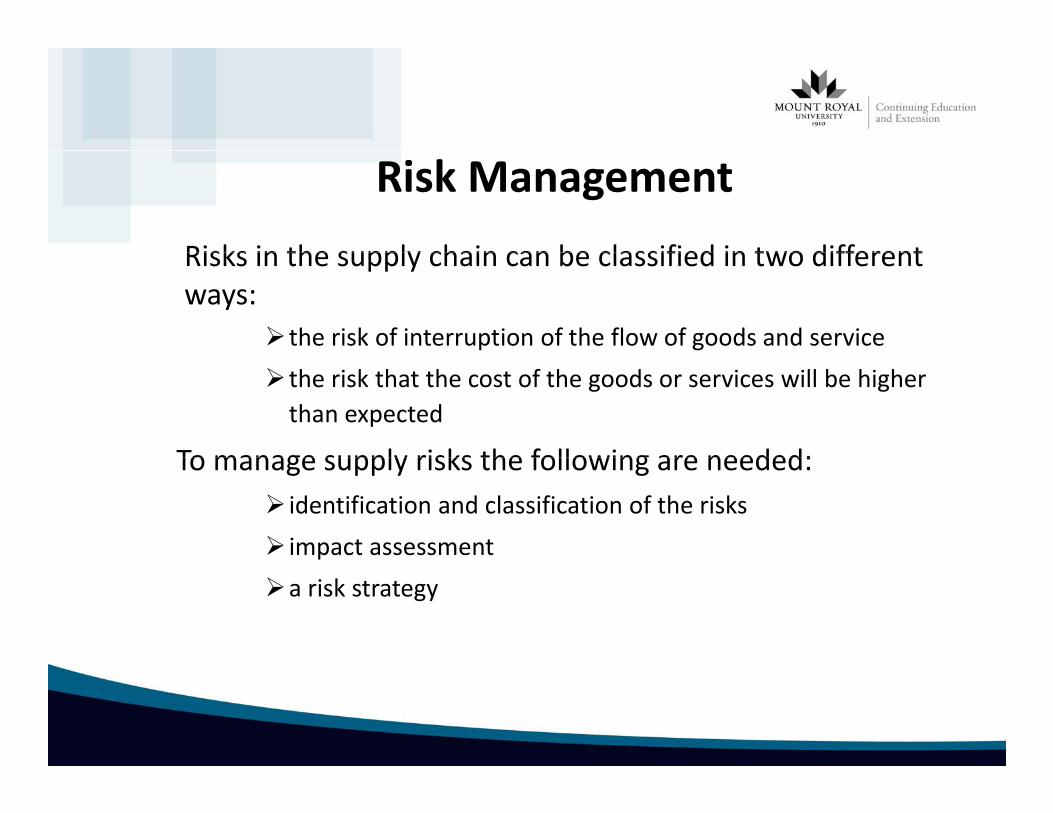

Risk ManagementRisks in the supply chain can be classified in two differentRisks in the supply chain can be classified in two different ways:

the risk of interruption of the flow of goods and service the risk that the cost of the goods or services will be higher than expected

To manage supply risks the following are needed:To manage supply risks the following are needed: identification and classification of the risks impact assessmenta risk strategy

Major Purchasing Functional Strategy Areas

•Assurance of supply strategies•Cost reduction strategies•Supply support strategiesSupply support strategies•Environmental change strategies•Competitive edge strategies

Strategic Components

• What? To make or buy• Quality?What is being procured • How much? Large versus small, maintenance of inventory or not• Who? Centralize or decentralize, quality of staff• When? Now versus later, forward buying• What price? Premium, standard, cost based, market based• Where? Local, regional, global• How? Systems and procedures, negotiations, systems, contracting, ethics, value analysisvalue analysis

• Why? Objectives congruent, internal reasons, outside supply, inside supply

Trends and the Future• Non‐traditional staffing in supply management positions• Technical entry route into purchasing• Emphasis on total quality management and customer satisfactionEmphasis on total quality management and customer satisfaction• Emphasis on the process used in acquisition, rather than just the transaction itself

• Purchase of systems, services, and products• Strategic cost management• Design engineering and purchasing capitalizing on their potential synergy• The supplier base will be reformulated• Longer term contracts• e‐Commerce

Trends and the Future (cont’d)

• Global supply management• MRO items handled by third party contractors

l d h l d d d b l d• Sourcing to include the complete end product, or service, and be completed proactively

• Closer supplier relationships teaming• Empowerment• Empowerment• End‐product manufacturers will focus on design and assembly• Consortiums for purchasing• Separation of strategic and tactical purchasingSeparation of strategic and tactical purchasing• Greater involvement of purchasing in non‐traditional purchases• Environmental purchasing• Value enhancement vs. cost reductions

Assigned Question Reviewg Q

Ch t 6 155 156 #’ 4 8• Chapter 6: pages 155‐156 ‐ #’s 4, 8• Chapter 2: pages 37‐38 ‐ #’s 1, 8, 10 • Review of all of the assigned questions• Review of all of the assigned questions.

Confirmation Exam

• Open book, in‐class, hand‐in SCM Strategic Procurement concepts exam.