Strategic Outlook of Select Sub-Saharan African Light ... · PDF fileStrategic Outlook of...

30

Strategic Outlook of Select Sub-Saharan African Light, Medium, and Heavy Commercial Vehicle Markets By 2020 Commercial Vehicle Sales to Reach 363 Thousand Units EXECUTIVE SUMMARY

Transcript of Strategic Outlook of Select Sub-Saharan African Light ... · PDF fileStrategic Outlook of...

Strategic Outlook of Select Sub-Saharan African Light, Medium, and Heavy Commercial Vehicle Markets

By 2020 Commercial Vehicle Sales to Reach 363 Thousand Units

EXECUTIVE SUMMARY

2M921-18

Contents

Section Slide Numbers

Executive Summary 5

Research Scope, Objectives, Methodology and Background 23

Definitions and Segmentation 28

External Challenges : Drivers and Restraints – Total market 31

Mega Trends in Sub-Saharan Africa 39

Overall Market Overview 48

• South Africa’s Commercial Vehicles Market 69

• Zambia’s Commercial Vehicles Market 78

• Zimbabwe’s Commercial Vehicles Market 86

• Botswana’s Commercial Vehicles Market 94

• Namibia’s Commercial Vehicles Market 102

• Angola’s Commercial Vehicles Market 110

• Mozambique’s Commercial Vehicles Market 118

• Kenya’s Commercial Vehicles Market 126

• Tanzania’s Commercial Vehicles Market 134

3M921-18

Contents (continued)

Section Slide Numbers

• Uganda’s Commercial Vehicles Market 142

• Nigeria’s Commercial Vehicles Market 150

• Ghana’s Commercial Vehicles Market 158

Conclusions and Future Outlook 166

4

Executive Summary

5M921-18

Market OverviewMost commercial vehicles currently imported from Europe and Asian markets.

� The sub-Saharan African commercial vehicles

market is mostly characterised by light duty

(LD), medium duty (MD) and heavy duty (HD)

trucks and buses.

� Since the 1980s, most sub-Saharan African

countries have experienced a steady decline in

the number of vehicles assembled locally.

� This has mainly been due to the limited

availability of raw materials and vehicle

components. Furthermore, the influx of low-

cost vehicles has reduced the price

competitiveness of locally assembled vehicles.

� Hence most countries currently import

commercial vehicles from Europe and Asia.

� However, in order to stimulate the local

assembly of commercial vehicles, some

governments are shifting towards providing tax

incentives to local assemblers.

� These include import duty exemptions on

vehicle components that are used for local

vehicle production.

Source: Multiple Sources, Frost & Sullivan analysis.

Light Duty Trucks

Medium Duty Trucks

Heavy Duty Trucks

Heavy Duty Buses

6M921-18

Lagos

Luanda

Johannesburg/Pretoria

Cairo

Dar es Salaam

Alexandria

Nairobi

Accra

Abidjan

Kinshasa

Addis Ababa

Main Developed Corridors Cape Town

DurbanSource: UN-Habitat, 2010; Frost & Sullivan analysis.

The Greater Ibadan Lagos Accra (GILA) Corridor

• Combined population >18.0 million

• Contributes combined GDP of $127,592,000.

The North Delta Region• Combined population of

77.0 million• Three emerging corridors:

Cairo-SuezCairo-AlexandriaCairo-Ismailia.

900 km Kampala-Nairobi-Mombasa urban corridor

1,000 km Abidjan-Ouagadougou Corridor

North-South Corridor• Facilitate inter-regional trade from

Cape to Cairo. • Free trade area comprising

533.0 million people. • Combined GDP of $833.00 billion

or 58% of Africa’s GDP.

Trans-Cunene Corridor• Will link the Democratic Republic of

Congo (DRC) with South Africa through Angola and Namibia.

Ouagadougou

Ibadan

Future Corridor Development

Mega Corridors, Africa, 2050

Top Mega Trends in Sub-Saharan Africa : Regional IntegrationCorridors will Unlock Economic Potential of Landlocked Countries Leading to Better Inter-Dependence Among Cities and Regional Growth

7M921-18

Trucks & Bus Value Chain

Dealer

Component

Spare parts

Assembly

Vehicle Sales

Service

OEM

Assembly

Imports

Direct Sales

Service

Importers(Used Vehicle

Importers)

Used Vehicle Imports

Vehicle Sales

The entities involved in the sales of vehicles generate continuous

revenues through service and sales of spare parts

Demand Generation

Individual Repair shops/service

stations

Truck and Buses Industry - Outlook of Value ChainOEMs are likely to focus on supply base consolidation to improve market share and reduce cost

Source; Frost & Sullivan analysis

• Toyota• Nissan• Mazda• Ford• Chevrolet

Utility• Isuzu• MAN• Iveco• Mercedes

Benz• Hino• Fuso• Freightliner• Scania• TATA• Volvo• VDL• Renault• Foton• DongFEng• PACCAR• Navistar• Hyundai

• Toyota• Nissan• General

Motors• Ford• Mercedes

Benz• Kenya

Vehicle Manufacturers (KVM)

• INNOSON Vehicle Manufacturing (IVM)

Major OEMs Assemblers/Dealers

Truck and Bus Market: Value Chain Outlook, Sub-Saharan Africa, 2012

8M921-18

Global Market Share - By Country of Manufacturing OriginChinese imports currently account for nearly 1 in every 5 trucks and buses sold in the region

USA Chevrolet ,Ford,

Navistar

China JAC, FAW, JMC, Foton

Motors, Shaanxi, King

Long, Dongfeng, CNHTC

Japan Mitsubishi, Isuzu,

Toyota, Hino, Nissan

Europe Mercedes, Iveco,

Renault,Volvo, DAF,

Scania, MAN, VW

Truck and Bus Market: Country of Manufacturing Origin, Sub-Saharan Africa, 2012

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.Europe includes: France, Germany, Italy , Netherlands, Sweden, Turkey

LD Trucks : 128,669MD Trucks : 23,319HD Trucks : 11,877Buses : 3,805Total : 167,670

SOUTHERN AFRICA

LD Trucks : 17,000 MD Trucks : 11,400HD Trucks : 3,900Buses : 1,900Total : 34,200

WEST AFRICA

EAST AFRICA

LD Trucks : 11,219 MD Trucks : 6,908HD Trucks : 3,098Buses : 600Total : 21,825

India and Korea Tata, Ashok, Hyundai

9M921-18

Note: All figures are rounded. The base year is 2012..

Sub-Saharan Africa’s Commercial Vehicles Market In 2012, South Africa contributed the bulk of both imported used trucks and new cars sales in Sub-Saharan Africa

Source: Frost & Sullivan analysis.

Truck Market: New and Used Truck Sales, Sub-Saharan Africa, 2012

0

20,000

40,000

60,000

80,000

100,000

120,000

Imported Used Truck Sales New Truck Sales

Un

it S

ale

s

• In 2012, LD trucks contributed the bulk of both imported used trucks and new truck sales. Most importedused trucks came from Europe and Asia, while new trucks where either manufactured in South Africa orwere low-cost vehicles from Asia.

10M921-18

Note: All figures are rounded. The base year is 2012..

Sub-Saharan Africa’s Commercial Vehicles Market Between 2013 and 2020 all Sub-Saharan African economies are expected to achieve positive growth. This is expected to drive growth in the truck and bus markets

Truck and Bus Sales: Economic Growth, Sub-Saharan Africa, 2013-2020

Source: IMF and Frost & Sullivan analysis.

2013 2014 2015 2016 2017 2018 2019 2020

Unit Sales Growth 5.8 6.2 6.1 6.0 6.0 6.8 6.5 6.8

Economic Growth 6.1 6.0 6.1 6.0 5.9 5.9 6.0 6.1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Gro

wth

Rate

s (

%)

Unit Sales Growth Economic Growth

11M921-18

Note: All figures are rounded. The base year is 2012..

Sub-Saharan Africa’s Commercial Vehicles Market Currently, South Africa dominates Sub-Saharan Africa’s commercial vehicles market. This is expected to continue till 2020.

Source: IMF and Frost & Sullivan analysis.

Truck and Bus Sales: Vehicle Sales Growth, Sub-Saharan Africa, 2012-2020

223,695363,600

Truck and Bus Sales: Vehicle Sales Growth, Sub-Saharan Africa, 2012

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

SouthAfrica

Nigeria Ghana Kenya Tanzania Others

Un

it S

ale

s

LD Trucks MD Trucks HD Trucks Buses

70.1%

18.6%

8.4%

2.8%

2012

LD Trucks MD Trucks

HD Trucks Buses

70.8%

18.2%

8.3%

2.7%

2020

LD Trucks MD Trucks

HD Trucks Buses

12M921-18

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

Sub-Saharan Africa’s Commercial Vehicles Market Toyota and Isuzu dominated the LD truck market in 2012 while Iveco and Isuzu where the most preferred MD trucks in Sub-Saharan Africa

LD Truck Market: Overview of Key Models, Sub-Saharan Africa, 2012

35.8

30.4

14.2

9.6

4.0

6.0

0.0 10.0 20.0 30.0 40.0

TOYOTA

ISUZU

NISSAN

FORD

MAZDA

Others*

Market Share (%)

MD Truck Market: Overview of Key Models, Sub-Saharan Africa, 2012

25.0

20.0

15.0

10.0

10.0

8.0

12.0

0.0 5.0 10.0 15.0 20.0 25.0 30.0

UD TRUCKS

IVECO

ISUZU

Nissan

Toyota

TATA

Others*

Market Share (%)

21.1

19.2

19.2

15.0

7.7

5.0

12.8

0.0 5.0 10.0 15.0 20.0 25.0

SCANIA

MAN

VOLVO

IVECO

RENAULT

TATA

*Others

Market Share (%)

HD Truck Market: Overview of Key Models, Sub-Saharan Africa, 2012

32.5

28.2

15.6

12.0

7.7

4.0

0.0 10.0 20.0 30.0 40.0

SCANIA

VOLVO

MAN

IVECO

MERCEDES BENZ

Others*

Market Share (%)

Buses Market: Overview of Key Models, Sub-Saharan Africa, 2012

13M921-18

Note: All figures are rounded. Source: Frost & Sullivan analysis.

Sub-Saharan Africa’s Commercial Vehicles Market South Africa contributed the bulk of commercial vehicle and bus sales in 2012

WEST AFRICAEAST AFRICA

SOUTHERN AFRICA

LD Trucks : 17,000 MD Trucks : 11,400HD Trucks : 3,900Buses : 1,900

Total : 34,200

Truck and Bus Sales: Vehicle Sales, Sub-Saharan Africa, 2012

LD Trucks : 128,669MD Trucks : 23,319HD Trucks : 11,877Buses : 3,805

Total : 167,670

LD Trucks : 11,219 MD Trucks : 6,908HD Trucks : 3,098Buses : 600

Total : 21,825

• In 2012, the top five Sub-Saharan Africa truck and bus markets contributed 86.3 per cent to total vehicleand bus sales.

Country Percentage Market

Share (%)

South Africa 63.7

Nigeria 10.1

Ghana 5.2

Kenya 4.4

Tanzania 3.0

*Other 13.7

Total 100

*Others include Zambia, Zimbabwe, Namibia, Botswana, Mozambique, Angola, and Uganda

Market Share, 2012

14M921-18

LD and MD Truck Market: Best Selling Models, Sub-Saharan Africa,2012

Source: Frost & Sullivan analysis.

Vehicle Category Model Key Features Winning Formula

Light Duty Trucks

Medium Duty Trucks

• Impact absorbing steer wheel• Door impact beams• Head impact protection trim• Brake system load sensing, proportioning and bypass valve• Integral power steering

•The Toyota Hilux 2.5D-4D trucks provide extensive comfort and safety features.•They are considered to be highly fuel efficient and have readily available spare parts.•The Toyota Hilux 2.5D-4D trucks offer some of the latest technical features such as a highly adjustable steering wheel.

• Side impact protection bars• Collapsible steering wheel column

Toyota Hilux 2.5D

Isuzu KB 240i

Light Duty Trucks

UD 40A

•The Isuzu KB 240i has high load capacity and economical fuel consumption.•It has readily available spare parts and after-sales support services.•The Isuzu KB 240i is highly affordable to small business operators and incurs minimum maintenance costs.

• UD Trucks has an extensive distribution network of its vehicles• The UD 40A trucks are easy to operate and are highly fuel efficient. • They are easy to maintain and have readily available spare parts. The UD40A truck cabins can till at an angle of 65 degrees, allowing access to areas of the engine that are usually difficult to reach.

• SRS drivers airbag• A-Pillar grab handle• Climate controlled air-conditioning, • Cruise control

Best Selling LD and MD Trucks in Sub-Saharan Africa In 2012 Toyota Hilux, Isuzu KB 240i and UD 40A were the best selling LD and MD trucks in Southern Africa

15M921-18

LD and MD Truck Market: Best Selling Models, Sub-Saharan Africa,2012

Source: Frost & Sullivan analysis.

Vehicle Category Model Key Features Winning Formula

Heavy Duty Trucks

Extra Heavy Duty Trucks

• Sleeper cab with high roof.• Electronic brake –force limitation (EBL) combined with anti-lock braking system (ABS). •Low engine tunnel.• Park brake control is conveniently positioned.• Dashboard well positioned and easily visible to the driver.

• Iveco’s Euro Cargo models are highly durable and reliable. They are able to withstand some of the toughest and most difficult terrain.•Iveco has an established presence across the region and the Euro Cargo spare parts are readily available.•Its range of trucks are highly fuel efficient making them ideal for commercial operations •The Euro Cargo models offer some of the technical features that comply with EEC safety standards.IVECO Euro Cargo MLL 160E24

Scania P360

•Scania has a strong brand and well established distribution network across Sub-Saharan Africa.•The P360 models are highly fuel efficient which makes them ideal for long-haul transportation.•In addition these models are cable of transporting high volumes of cargo.•Spare parts for these models are readily available and they have minimum break down due to built in quality with durability of spare parts.

• Wide and convenient boarding steps.• Straight 6-cylinder direct injection diesel engine that full-fills Euro3 emissions ratings.• Turbo and charge air cooler• Large and safe cab to protect the driver and passenger.

Best Selling HD and Extra HD Trucks in Sub-Saharan Africa Iveco and Scania were the best selling HD and Extra HD trucks in Southern Africa in 2012

16M921-18

MD and BD Bus Market: Best Selling Models, Sub-Saharan Africa,2012

Source: Frost & Sullivan analysis.

Vehicle Category Model Key Features Winning Formula

Medium Duty Buses

Heavy Duty Buses

• Impact absorbing steer wheel• High mounted gear lever and excess storage space. • Brake system load sensing, proportioning and bypass valve• Air-conditioning vents throughout the vehicle ensure fresh air and passenger comfort. •Height adjustable head restraints.• Integral power steering.

• Toyota Quantum commercial vehicles are easy to drive due to the power steering and high-mounted gear lever.•They have plenty of passenger and storage thereby increase the level of comfort .•The air conditioning vents and adjustable head restraints also increase the levels of comfort in these vehicles.•They have high fuel consumption efficiency.

Toyota Quantum

Scania F94 HB

• The Scania F94 HB buses are considered to be highly reliable and durable.•They have high levels of comfort to enhance passenger satisfaction. •The Scania F94 HB buses experience minimum break down due to built in quality with durability of spare parts.•The are highly efficient with regards to fuel consumption.

•Longitudinal front-engine chassis that is adaptable to the most diverse urban applications.• Mechanical suspension with semi-elliptic leaf springs ensure comfortable ride under all road conditions.• Six-speed manual gear box is well positioned and easy to operate thereby reducing driver fatigue.

Best Selling MD and HD Buses in Sub-Saharan Africa In 2012 Toyota Quantum and Scania F94 HB were the best selling MD and HD buses in Southern Africa

17M921-18

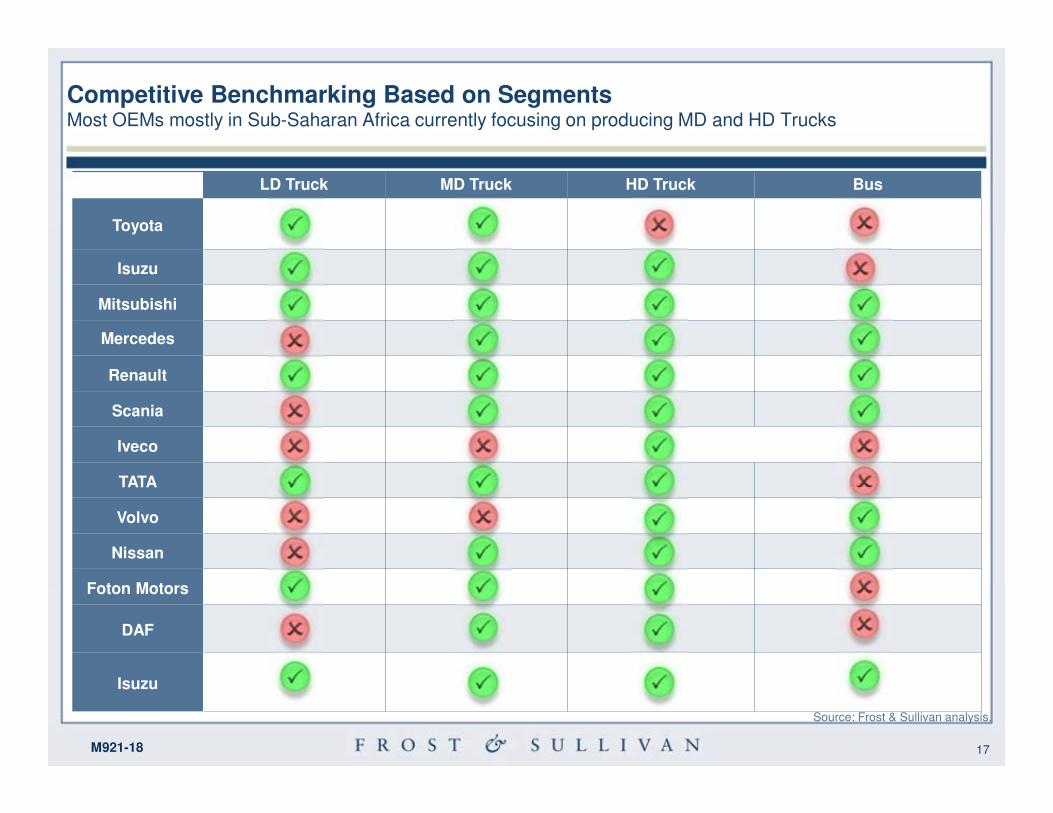

LD Truck MD Truck HD Truck Bus

Toyota

Isuzu

Mitsubishi

Mercedes

Renault

Scania

Iveco

TATA

Volvo

Nissan

Foton Motors

DAF

Isuzu

Source: Frost & Sullivan analysis.

Competitive Benchmarking Based on SegmentsMost OEMs mostly in Sub-Saharan Africa currently focusing on producing MD and HD Trucks

18M921-18

Key Findings for Trucks MarketBetween 2012 and 2020 Sub-Saharan African’s truck market is anticipated to grow from 217,390 to 353,713 units. It is expected to achieve a CAGR of 6.3 per cent during this period.

The overall truck market is expected to achieve high growth due to sustained economic growth which is expected toaverage 6.0 per cent between 2012 and 2020.1

Truck and Bus Market: Key Findings for Truck Market, Sub-Saharan Africa, 2012

Significant investment in infrastructure projects across the entire Sub-Saharan African region is expected to be themajor driver of growth. However, the unavailability of raw materials in local markets and as well as the high costs ofproducing vehicles locally are expected to continue undermining market development.

2

Currently, there is limited production of local vehicles across the region. Most vehicles available are either low-costvehicles from Asia or second-hand models from Europe.3

South Africa remains the single biggest market of commercial vehicles across the region with a market share ofapproximately 63.7 per cent.4

Due to the urgent need to resuscitate their automotive sectors, most governments are imposing restrictions on theimportation of vehicles older than five years.

5

Light duty truck sales volumes are expected to continue dominating the market between 2012 and 2020.6

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

19M921-18

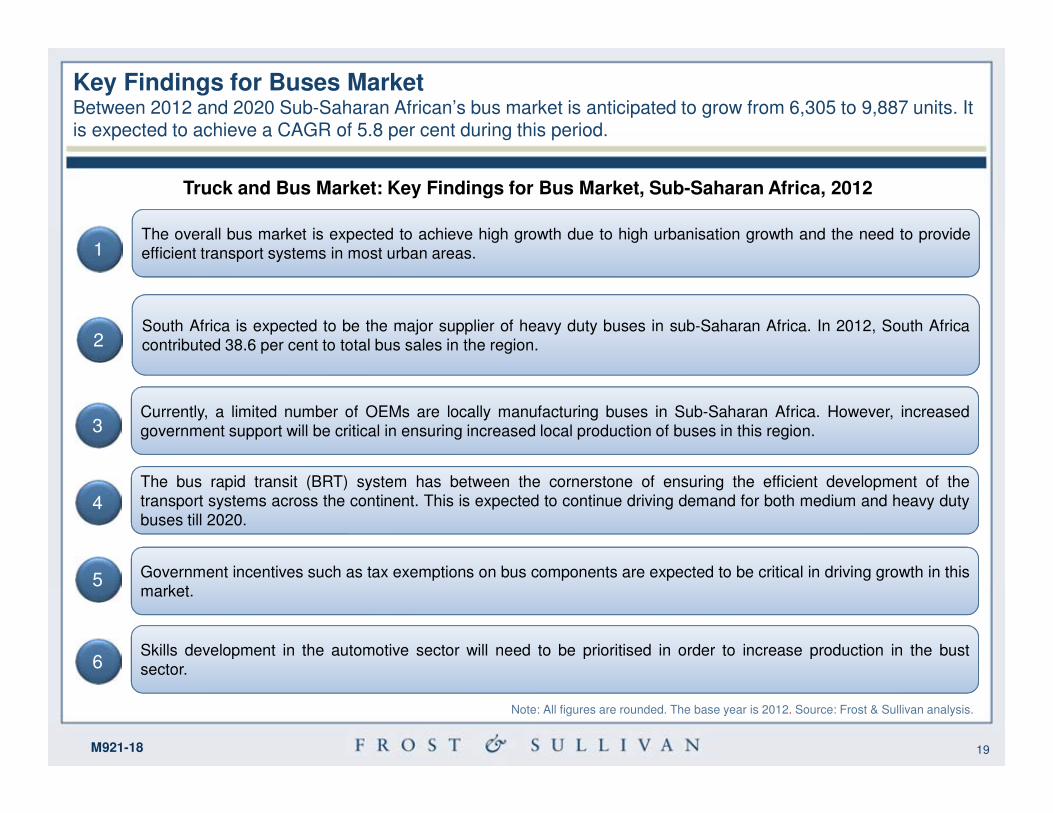

Key Findings for Buses MarketBetween 2012 and 2020 Sub-Saharan African’s bus market is anticipated to grow from 6,305 to 9,887 units. It is expected to achieve a CAGR of 5.8 per cent during this period.

The overall bus market is expected to achieve high growth due to high urbanisation growth and the need to provideefficient transport systems in most urban areas.1

Truck and Bus Market: Key Findings for Bus Market, Sub-Saharan Africa, 2012

South Africa is expected to be the major supplier of heavy duty buses in sub-Saharan Africa. In 2012, South Africacontributed 38.6 per cent to total bus sales in the region.2

Currently, a limited number of OEMs are locally manufacturing buses in Sub-Saharan Africa. However, increasedgovernment support will be critical in ensuring increased local production of buses in this region.3

The bus rapid transit (BRT) system has between the cornerstone of ensuring the efficient development of thetransport systems across the continent. This is expected to continue driving demand for both medium and heavy dutybuses till 2020.

4

Government incentives such as tax exemptions on bus components are expected to be critical in driving growth in thismarket.

5

Skills development in the automotive sector will need to be prioritised in order to increase production in the bustsector.6

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

20

Research Scope, Objectives, Background, and Methodology

21M921-18

Research Scope

Trucks and BusTrucks and BusVehicle Type

2013 to 20202013 to 2020Forecast Period

2008 to 20202008 to 2020Study Period

20122012Base Year

Sub-Saharan AfricaSub-Saharan AfricaGeographical Scope

Market Segment

2008 2009 2010 2011 2012

Trucks 306,494 205,845 233,899 264,200 217,390

Bus 10,501 7,052 8,013 9,052 6,305

Total 316,995 212,897 241,912 273,252 223,695

Truck and Bus Market: Unit Sales, Sub-Saharan Africa , 2008-2012

Source: Frost & Sullivan analysis.

22M921-18

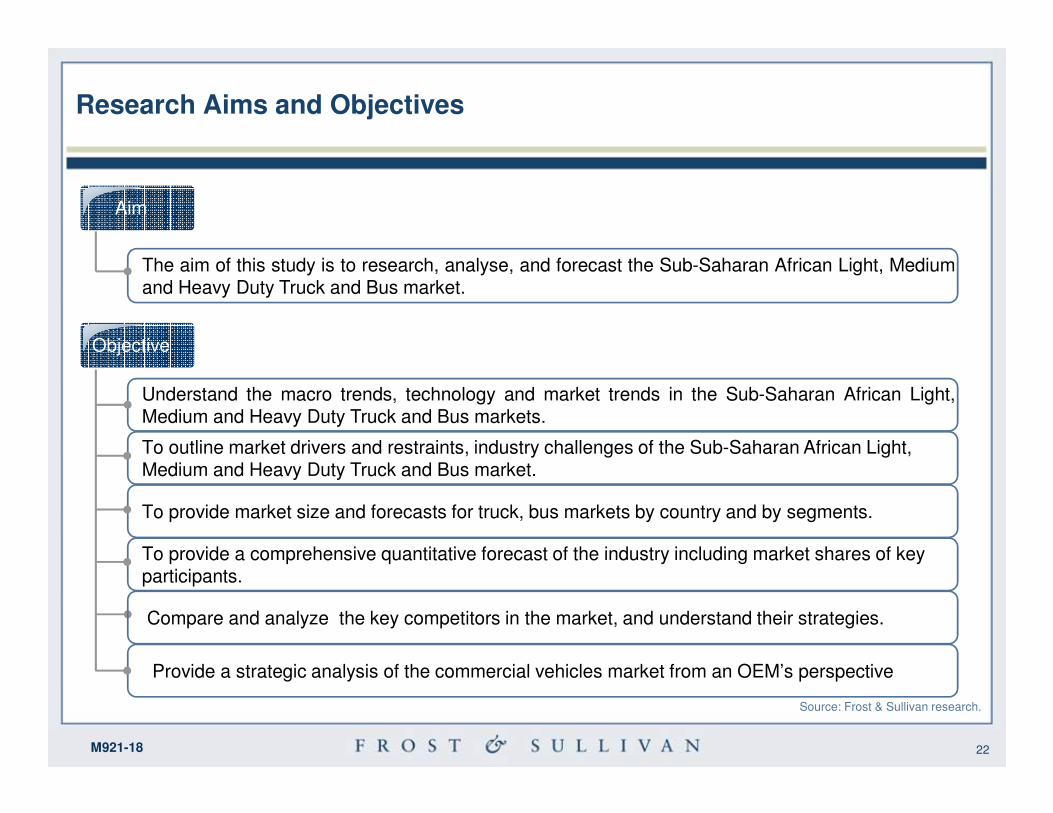

Research Aims and Objectives

Source: Frost & Sullivan research.

Objective

Understand the macro trends, technology and market trends in the Sub-Saharan African Light,Medium and Heavy Duty Truck and Bus markets.

To outline market drivers and restraints, industry challenges of the Sub-Saharan African Light, Medium and Heavy Duty Truck and Bus market.

To provide market size and forecasts for truck, bus markets by country and by segments.

To provide a comprehensive quantitative forecast of the industry including market shares of key participants.

Aim

The aim of this study is to research, analyse, and forecast the Sub-Saharan African Light, Mediumand Heavy Duty Truck and Bus market.

Compare and analyze the key competitors in the market, and understand their strategies.

Provide a strategic analysis of the commercial vehicles market from an OEM’s perspective

23M921-18

How are CV’s classified and how is the market structured?

Key Questions this Study Will Answer

Who are the market leaders and what are their market shares?

What are the technology trends?

Is there potential for growth within the market?

How is the macro-economic trends impacting the sales and production of commercial vehicles?

Truck and Bus Market: Key Questions This Study Will Answer, Sub-Saharan Africa, 2012

Source: Frost & Sullivan analysis.

24M921-18

Research Methodology: Frost & Sullivan’s research services are based on secondary and primary

research data.

Secondary Research: Extraction of information from existing reports and project material within the

Frost & Sullivan database, to include data and information gathered form technical papers, specialized

magazines, seminars and internet research.

Primary Research: Many interviews have been conducted over the phone by senior

consultants/industry analysts with original equipment suppliers, regulation authorities, governmental

statistics department and distributors. Primary research has accounted for 70.0 per cent of the total

research.

Research Methodology

Source: Frost & Sullivan analysis.

25

Definitions and Segmentation

26M921-18

Key Industry Participants

OEM

Chevrolet

Mitsubishi Fuso

Isuzu

Toyota

Hyundai

MAN

Mercedes

Volvo

Scania

Renault

JAC

Ford

Shaanxi

Foton Motors

Hino

DAF

IvecoSource: Frost & Sullivan analysis.

Truck and Bus Market: Key Industry Participants, Sub-Saharan Africa, 2012

27M921-18

Vehicle Definitions

• Commercial vehicles are defined as trucks and buses that are used for transporting goods, materials

and people.

• Based on gross vehicle weight (GVW), which is the combined weight of the vehicle and load,

commercial vehicles are classified into four segments: Light Duty Trucks (LDs), Medium Duty Trucks

(MDs), Heavy Duty trucks (HDs), Medium Duty (MD) & Heavy Duty (HD) Bus

Truck & Bus Market: Overall Commercial Vehicle Segment, Sub-Saharan Africa, 2012

• This study covers light duty trucks, medium duty trucks, heavy duty trucks, and buses.

• Buses can be categorized into Medium Duty and Heavy Duty.

• The base year for the analysis is 2012 and the forecast period is 2013–2017 and 2020..

• This study focuses on the South Africa, Zambia, Zimbabwe, Botswana, Namibia, Angola, Mozambique,

Kenya, Tanzania, Uganda, Nigeria, Ghana trucks and bus market.

Light Trucks Medium Trucks Heavy Trucks Bus

3.5 ton ≤ GVW ≤ 6.5 ton

6.6 ton ≤ GVW ≤ 16 ton GVW greater than 16 ton MD Bus HD Bus

28

Market Engineering Methodology

One of Frost & Sullivan’s core deliverables

is its Market Engineering studies. They

are based on our proprietary Market

Engineering Methodology. This approach,

developed across 50 years of experience

assessing global markets, applies

engineering rigor to the often nebulous art

of market forecasting and interpretation.

A detailed description of the methodology

can be found here.

Source: Frost & Sullivan research.

29

FOR MORE INFORMATION, CONTACT

Subhash Joshi

Industry Manager

Automotive & Transportation Practice

Middle East, North Africa and South Asia

Frost & Sullivan International Inc.

210, EIB-4 BT Building

Dubai Internet City

PO Box: 502395

Dubai, United Arab Emirates

Ph: +971 4 4331 893

Tanu Chopra

Senior Manager- Corporate CommunicationsMiddle East & North Africa

Ph: +91 22 6607 2046Email: [email protected]

Website: www.frost.com

30M921-18

THANK YOU