Strategic Analysis of United Bank Limited

75

PROJECT NAME - STRATEGIC ANALYSIS OF UBL Submitted By- Shahid Iqbal Student M. Phil at National Defence University Islamabad Pakistan Presented to: Dr Tahir Saeed NDU LMS Dept.

-

Upload

shahidpak126114364 -

Category

Documents

-

view

353 -

download

3

Transcript of Strategic Analysis of United Bank Limited

PROJECT NAME - STRATEGIC ANALYSIS OF UBL

Submitted By- Shahid Iqbal Student M. Phil at National Defence University Islamabad Pakistan

Presented to: Dr Tahir Saeed NDU LMS Dept.

OUTLINEUBL Introduction

President MessageUBL History, Today & OverviewGlobal Presence & Awards

Board Of DirectorsOrganizational StructureProducts & ServicesCore ValuesIncome Statement 2012Balance Sheet 2012Financial Ratios (Last four Quarters)

Vision & Mission

External Evaluation

List of Competitors Opportunities and Threats

EFE MatrixCompetitive Profile MatrixPorter's Five Forces Model

Internal Evaluation

Strength and WeaknessIFE

Strategy AnalysisSWOT MatrixSPACE MatrixBCG MatrixGrand Strategy Matrix

Decision Making QSPMStrategy Evaluation

Recommendations

President's MessageAtif R. Bokhari

We endeavor to offer you, our customer, the very best products and services. With our strong footprint of over 1300 branches, UBL has been in the forefront. We finance new businesses and assist existing businesses to expand. We work with our customers to turn their dreams into reality. We are proud to invest in our community's growth and prosperity and we are thankful that our employees are as committed as we are. We will continue to grow and strive to serve you better. We'll meet this challenge by insuring that our employees are well trained to deliver state-of-the-art products and superior service to you, because at UBL,

You come first!

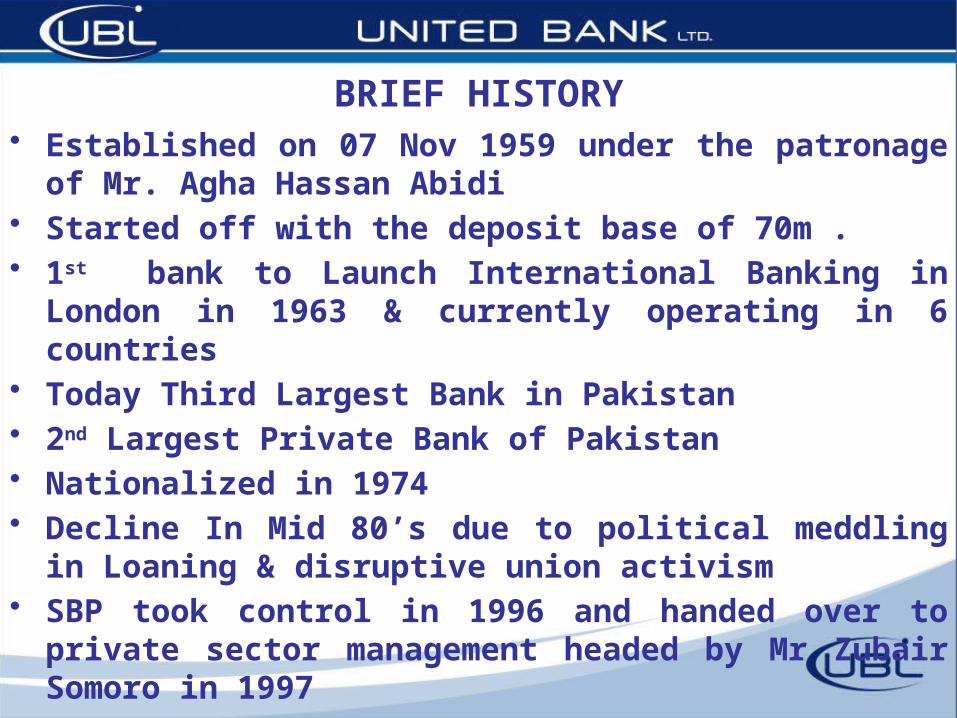

BRIEF HISTORY• Established on 07 Nov 1959 under the patronage of Mr.

Agha Hassan Abidi• Started off with the deposit base of 70m .• 1st bank to Launch International Banking in London in

1963 & currently operating in 6 countries• Today Third Largest Bank in Pakistan• 2nd Largest Private Bank of Pakistan• Nationalized in 1974• Decline In Mid 80’s due to political meddling in

Loaning & disruptive union activism• SBP took control in 1996 and handed over to private sector

management headed by Mr Zubair Somoro in 1997

• Privatized in Oct 2002• Jointly purchased by Abu Dhabi and Best Way Group• Revamped Products and Services• Huge investment in Information Technology and branch

renovations• Manifold increase in Assets, Deposits and Profits• UBL hold 51% of its total shares other 49% shares are

owned by Government• After the privatization of banking sector in Pakistan UBL

implemented its best strategies to achieve the comparative advantage in the Market place.

BRIEF HISTORY

• 1959 Agha Hasan Abedi founded UBL and inaugurates its first branch at I. I. Chundigarh at Karachi

• 1960 Extended its branches in Dacca, Lahore, Lyallpur, Chittagong and Narayanganj.

• 1960 Launched a saving scheme for school going children. • 1963 UBL became the first Pakistani bank to have an overseas branch – on

William Street in London. • 1964 UBL put the foundation of Pakistan's first Staff College Of Employees. • 1967 UBL introduced computer banking to Pakistan • 1967 UBL opens its branch in Abu Dhabi • 1967 United Bank A.G. Zurich, Switzerland a fully owned subsidiary was set

up on 8th of December 1967. • 1969 UBL opens for business in Kingdom of Bahrain with its branch in

Manama. • 1970 UBL launched UNICARD – Pakistan's first credit card.

UBL History, Today & Overview

• 1970 UBL opens another branch at busy commercial hub Bab Al Bahrain, inaugurated by H.E Abdul Karim, Finance minister at that time.

• 1970 UBL starts operations in Qatar with the opening of the branch in Musherib Doha.

• 1971 UBL launches 3 online branches in Karachi. • 1971 UBL introduces Pak Rupee Traveler Cheque. • 1972 UBL starts its operations in Yemen through a branch in Sanaa. • 1973 UBL opens its third branch at Muharraq ( Bahrain ). • 1974 The Government of Pakistan nationalized UBL. • 1977 UBL opens for business in the New York City, in March 1977. • 1978 UBL pledged economic department and acquired two international

banks • 1978 UBL launched supervised credit and small loan schemes for small to

medium sized firms as well as agriculture. • 1982 UBL introduces e-banking facilities at Hajj.

UBL History, Today & Overview

• 1983 UBL opens its Associate Company in Oman in collaboration with Oman United Exchange Co. L.L.C (OUECL).

• 1983 UBL starts its OBU- Branch in the Export Processing Zone, Karachi, on 6th of November 1983.

• 1989 UBL took over operations of HBL, which led to the addition of the Hodeidah branch in Yemen.

• 1990 Government of Pakistan decided to change the face of banking by creating a blueprint to privatize UBL.

• 1995 UBL opens its representative office in Iran. • 2002 H. H. Sheikh Nahayan Mabarak Al Nahayan is appointed as the

chairman of the board of directors of UBL. • 2002 UBL merged its operations in the UK with those belonging to National

Bank of Pakistan to form United National Bank Limited. • 2002 UBL launched its prime product Tezraftaar in Qatar and achieved

28000 transactions in the first year.

UBL History, Today & Overview

• 2002 Government of Pakistan privatized UBL, this brought the Abu Dhabi Group chaired by H. H. Sheikh Nahayan bin Mubarak Al Nahayan and the Bestways Group headed by Sir Anwar Pervaiz at the helm, following which the bank embarked on a major re-profiling and re-positioning strategy.

• 2000 UBL launched Tezraftaar home remittance in Bahrain. • 2006 UBL opens its representative office in Kazakhstan, on 21st of

September 2006. • 2006 UBL introduces UBL Ameen, an Islamic banking product. • 2006 UBL is awarded with an Islamic Banking Branch license by the State

Bank of Pakistan. • 2007 UBL received the Brand Leadership Award for Brand Excellence,

presented at the 16th Asian Brand Congress. • 2007 UBL launched Heritage Campaign blitz, a very successful and well-

received initiative as a strategic marketing and advertising effort to connect UBL-Middle East legacy of 40 years of customers' satisfaction to its re-positioned image and diversified deliverables across various banking portfolios.

UBL History, Today & Overview

• 2007 UBL relocates Bab Al Bahrain branch to Seef, the new upcoming business hub.

• 2007 UBL declares the profit before tax of PKR 13.8 billion. • 2008 UBL opens its second operating branch in Doha. • 2008 The main branch moved to Main Bank Street, opposite the Ministry of

Finance and Qatar Central Bank. • 2008 In Qatar UBL Tezraftaar transactions approached to 100,000. • 2008 UBL started its Customer Service Booths in Al-Khor and at the City

Center Shopping Mall, along with 7 ATM's at various prime locations throughout Qatar.

• 2008 UBL Bahrain holds 43% market share of remittances in the country with USD 23 million remittances.

• 2008 UBL inaugurates another operational branch in Aden Yemen. • 2008 USD 184 million was remitted through UBL-UAE to Pakistan. • 2008 The UAE nationals accounts for the highest workforce ratio of 42% at

UBL-UAE.

UBL History, Today & Overview

• 2008 UBL inaugurates its representative office in the Peoples Republic of China, on 20th of March 2008.

• 2009 UBL-UAE remitted USD 220 million to Pakistan. UBL shows devotion towards sports by inaugurating UBL Sports complex.

• 2009 UBL celebrates its Golden Jubilee on November 7, 2009 with the launch of an exclusive, world-class Signature UBL Priority Banking service, designed to cater to high-end, high-net-worth customers across Pakistan.

• 2010 UBL Launches Pakistan's First Premium Debit Card in Collaboration with MasterCard.

• 2010 UBL formally announces the launch of its unique and unmatched branchless banking service, under the brand name of UBL Omni.

• 2010 UBL and Avari Launch a Co-Branded Loyalty Card. United Bank Financial Services (Private) Limited. United Executors and trustees Company Limited.

• 2010 Launch of UBL Wiz ACCA Card

UBL History, Today & Overview

• 2011 UBL launches UBL Tezraftaar Account Services, an account that enables a Non Resident Pakistani (NRP) residing in a foreign country to open an account in any UBL branch in Pakistan

• 2011 UBL launches another product under the umbrella of Tezraftaar - UBL Tezraftaar Pardes Card, a prepaid remittance card on which the beneficiary can receive money without having to go to the bank's branch.

• 2011 UBL launches Platinum Credit Card. This card is designed to complement your lifestyle with credit limits befitting your stature, accompanied by the highest levels of services, unmatched rewards and myriad benefits

• 2011 UBL launches Silah Mila. Through this campaign, UBL acknowledges and rewards customers who have shown excellent performance in their loan repayments with other banks.

• 2011 Launch of UBL Mega Wallet VISA Debit Card on October 4, 2011 • 2011 UBL Priority Banking launches five new lounges nationwide at

Rawalpindi, Sialkot, Rahim Yar Khan, North Nazimabad Karachi and Multan Cantt

UBL History, Today & Overview

Present Management (Board of Directors)

Chairman - His Highness

Shaikh Nahayan Mabarak Al Nahayan

Deputy ChairmanSir Mohammed Anwar Pervez

President & CEO

Mr. Atif R. Bokhari

Organizational Structure

President & CEO

GE Retail Bank GE -HR

GE Corporate Banking

GE- SAM

GE- International Bank

GE- Audit & Inspection

GE Treasury & Capital Markets

GE-Compliance & Control

GE Credit Policy GE-Global Ops

GLOBAL PRESENCE

1. Pakistan2. United Arab Emirates3. Bahrain4. Qatar5. Yemen6. Oman7. United States of America (USA)8. China9. United Kingdom (UK)10. Switzerland

TOTAL NUMBER OF BRANCHES

Total Number of ATMs = 490

Type of Branch Number of Branches

RB- Branches 1248

Commercial Centers 4

Corporate Branches 5

Treasury Branches 1

Islamic Branches 19

Sub Branches 37

Total 1314

NATIONAL/INTERNATIONAL AWARDS

• UBL OMNI - GSMA Global Mobile Award 2012 for “Best Use of Mobile in Emergency or Humanitarian Situations” Feb 2012• UBL OMNI - Financial Insights Innovation Award (FIA) for “Innovation in Cash Disbursements (G2P)” Feb, 12 • Best Credit Card Provider - Consumers Choice Awards 2011 - February 22, 2012 by The Consumers Association of Pakistan• Best Corporate Report Award 2010 – Joint Committee of ICAP & ICMAP.• Top Bank Partner in 2011 – EFU life

PRODUCTS & SERVICES1. Retail Asset Products2. Corporate Banking3. Investment Banking4. Omni – Branchless Banking5. UBL Ameen – Islamic Banking6. Priority Banking7. Consumer Loan Products8. UBL Net Banking9. Deposit/Liability Products – A Big Product Line10. Treasury & Capital Markets11. UB Online – Corporate Customers12. Banc assurance Products13. NRP Services 14. Remittances – Domestic & Foreign – TezRaftar15. Go Green – Internet Merchant Hiring

16. Rupee Traveler Cheques – Humrah 17. UBL Fund Managers – Mutual Funds Products 18. UBL Wiz Cards - A big Card product Line19. ATM Cards – Mega wallet Card & Premium Debit Master

Card20. UBL Watan Card21. UBL PRI – Pardes Card 22. Asset Products 23. Agriculture Products24. Flood Relief25. Charity26. Donations

PRODUCTS & SERVICES

CORE VALUES

• Honesty and integrity• Commitment and dedication• Fairness and meritocracy• Teamwork and collaborative spirit• Humility and mutual respect• Caring and socially responsible

Income Statement 2012

Balance Sheet 2012

Financial RatiosLiquidity Ratios

Current 0 0Quick 0 0

Leverage RatiosDebt to total assets - -Debt to equity 78.08 169.47Long-term debt to equity 9.51 50.25Times-interest-earned ratio -

Activity RatiosFixed Assets Turnover - -Total Assets Turnover 0 0Inventory Turnover 0 0

Profitability Ratios Gross profit margin 0 3.32Operating profit margin 47.96 18.11Net profit margin 32.55 19.5Return on assets 2.18 0.59

Return on equity 21.7 8.19Price-earnings ratio 5.57 36.14EPS 14.71

Growth Ratios 5 YearsSales Growth% 12.43 12.47Net Income Growth% 25.9 16.35Earnings per share Growth% 16.46 7.73Dividends per share Growth% 33.78 8.85

UBL VISION & MISSION

UBL Vision

To be a world class bank dedicated to excellence, and to surpass the highest expectations of our customers and all other stakeholders

Evaluation of Vision Statement

UBL vision statement is brief, concise and one sentence statement. It provides base to create mission statement and also reflects future prospective (i.e. To be a world class Bank)

Proposed Vision statement For UBL

To be the bank of first choice in the world, partnering with our customers for a more prosperous and secure future.

Mission

• Set the highest industry standard for quality, across all areas of operation, on a sustained basis4

• Optimize people, processes and technology to deliver the best possible financial solution to our customers

• Become the most sought after investment• Be recognized as the employer of choice

Components UBL Missionn Statement UBL Mission

1) Customer Yes2) Product Yes3) Market No4) Technology Yes5) Concern for survival , growth and profitability Yes6) Philosophy Yes7) Self Concept No8) Concern for public Image Yes9) Concern for employee Yes

Components of UBL’s Mission

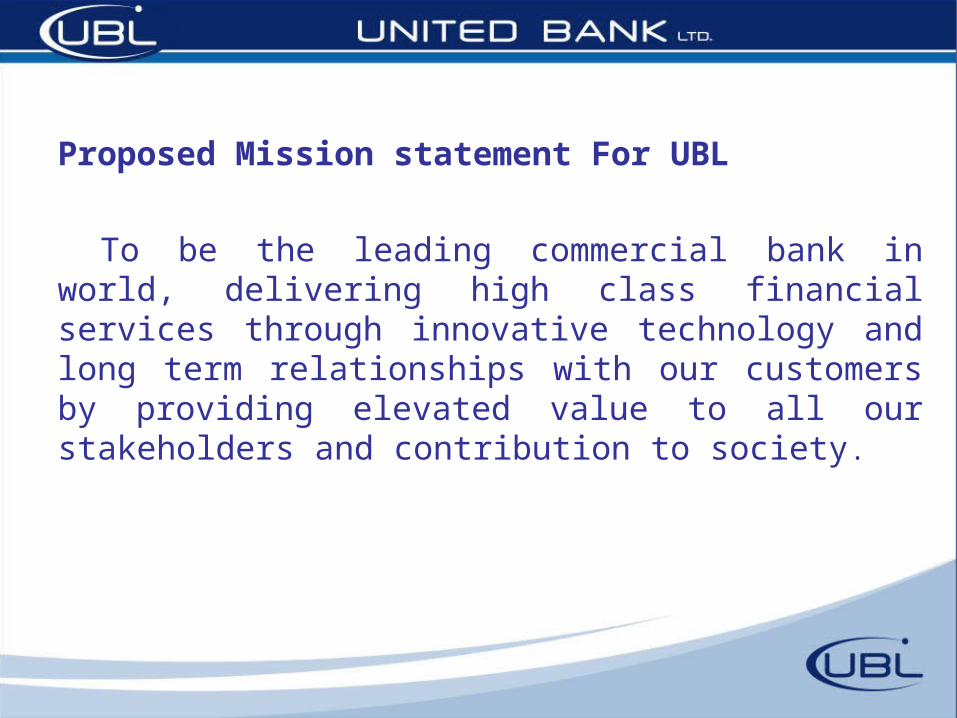

Proposed Mission statement For UBL

To be the leading commercial bank in world, delivering high class financial services through innovative technology and long term relationships with our customers by providing elevated value to all our stakeholders and contribution to society.

External Analysis

OPPORTUNITIES Bank can also enhance its branchless banking network Call centers Customer service quality can be improved Extensive range of 100% online branches network can be used to

cater/accommodate low cost deposit Implementation of Basel II & Basel III Accord by SBP i.e. product

and market development through acquisition More focus on Low cost deposits as compared to high cost

deposits Bank can enhance its Islamic banking network

THREATS SBP Anti Money Laundering tight policy Customer service Attitude Problem High Operating Cost Withholding tax on banking transaction Big Number of Non-Performing Consumer Loans Social pressure on Govt. to reduce bank’s spread Change in recent SBP regulations which lowered the profits of

banks Shrinking Margins Due to New Entrants

EFE

Weighted Score

Rating Weight External Factor (General and Specific)

Opportunities

Enhancement in branchless banking network 0.08 3 0.24Improving customer service quality of call centers 0.09 4 0.36

Extensive range of 100% online branches network can be used to Cater/ accommodate low cost deposit

0.07 4 0.28

Implementation of Basel II & Basel – III Accord by SBP i.e product and market development through acquisition

0.06 2 0.12

More focus on Low cost deposits as compared to high cost deposits

0.08 2 0.16

Diversification towards Islamic banking 0.07 3 0.21

Threats/ChallengesSBP Anti Money Laundering tight policy 0.09 3 0.27Customer service Attitude Problem 0.07 3 0.21High Operating Cost 0.09 3 0.16Withholding tax on banking transactions 0.06 2 0.12Big Number of Non-Performing Consumer Loans

0.08 3 0.24

Social pressure on Govt. to reduce bank’s spread

0.07 3 0.21

Change in recent SBP regulations which lowered the profits of banks

0.04 3 0.12

Shrinking Margins Due to New Entrants 0.05 2 0.10Total 1.00 2.80

The above score shows that UBL is effectively responding to opportunities and threats present in its industry because its score is more than average

score of 2.50.

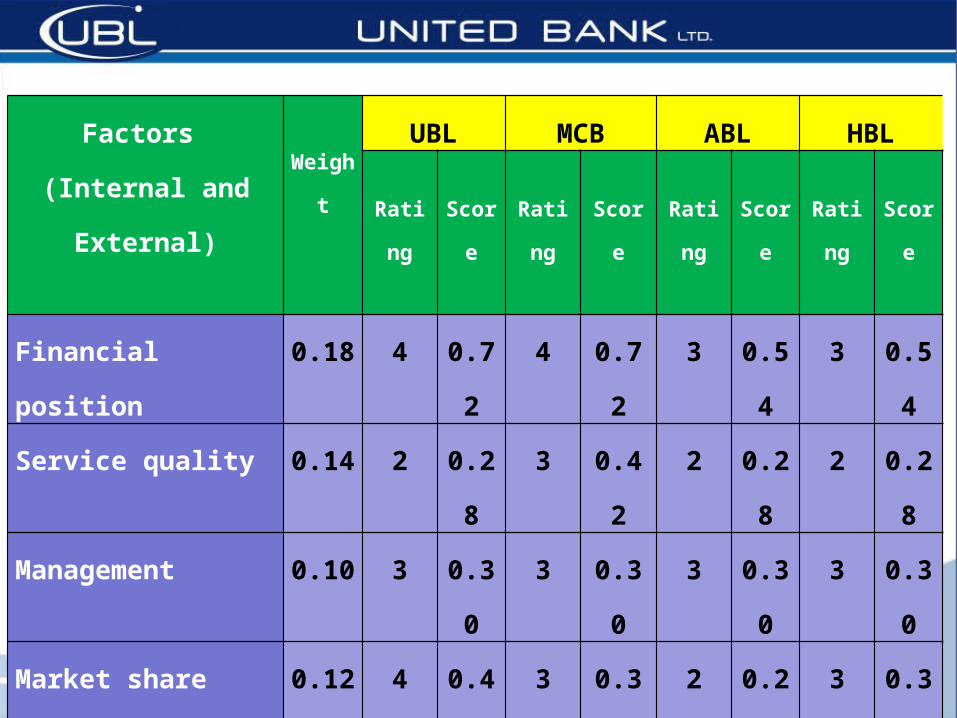

COMPETITOR PROFILE MATRIX(CPM)

MAJOR COMPETITORS OF UBL

Muslim Commercial Bank Limited (MCB)Allied Bank Limited (ABL) Habib Bank Limited (HBL) These three banks are also privatized

banks of Pakistan like UBL.

Factors (Internal and External)

WeightUBL MCB ABL HBL

Rating Score Rating Score Rating Score Rating Score

Financial position 0.18 4 0.72 4 0.72 3 0.54 3 0.54

Service quality 0.14 2 0.28 3 0.42 2 0.28 2 0.28

Management 0.10 3 0.30 3 0.30 3 0.30 3 0.30

Market share 0.12 4 0.46 3 0.36 2 0.24 3 0.36

Customer loyalty 0.10 2 0.20 3 0.30 2 0.20 2 0.20

Price competitiveness 0.10 3 0.30 2 0.20 2 0.20 2 0.20

Expansion 0.14 4 0.40 2 0.28 2 0.28 3 0.42

Advertising/Promotion 0.06 3 0.18 2 0.12 1 0.06 1 0.06

New Product 0.06 3 0.18 2 0.12 3 0.18 3 0.18

1.0 3.04 2.82 2.28 2.54

INTERNAL EVALUATION

STRENGTH & WEAKNESSES

STRENGTHS

Highest deposit: 747 (B), ABL= 381 (B), MCB = 531(B) and HBL = 9.8(B)Largest network of branches: 1314, ABL= 890, MCB = 1280 and HBL = 1451High total Assets: 946 (B), ABL= 449 (B), MCB = 484(B) and HBL = 725 (B)Banking software: Symbol 8.3 Version purchased in 2011 from Sun Guard Singapore based companyTrusted brand: more than 5.0 (M) customer Human resource (Trainings and pay band system) Diversified customer portfolio

Weaknesses:

High ratio of high cost deposit to total deposit (57%, net profitability as compared to HBL) In efficient customer service (As per service audit report of UBL 2012, every 9th customer has complained about customer service)High Non performing loan (1 Billion upto year 2012) High turnover of employeesIncreasing trend in bank service chargesThe physical environment of some of UBL branches is not attractive to the people

Porter ’s Five Forces Model

Forces High/ LowRivalry of competition High

Entry of New Competitors High

Bargaining Power of Suppliers

Low

Bargaining Power of Buyers

Low

Entry of Substitute Products

High

Porter’s Model & UBL

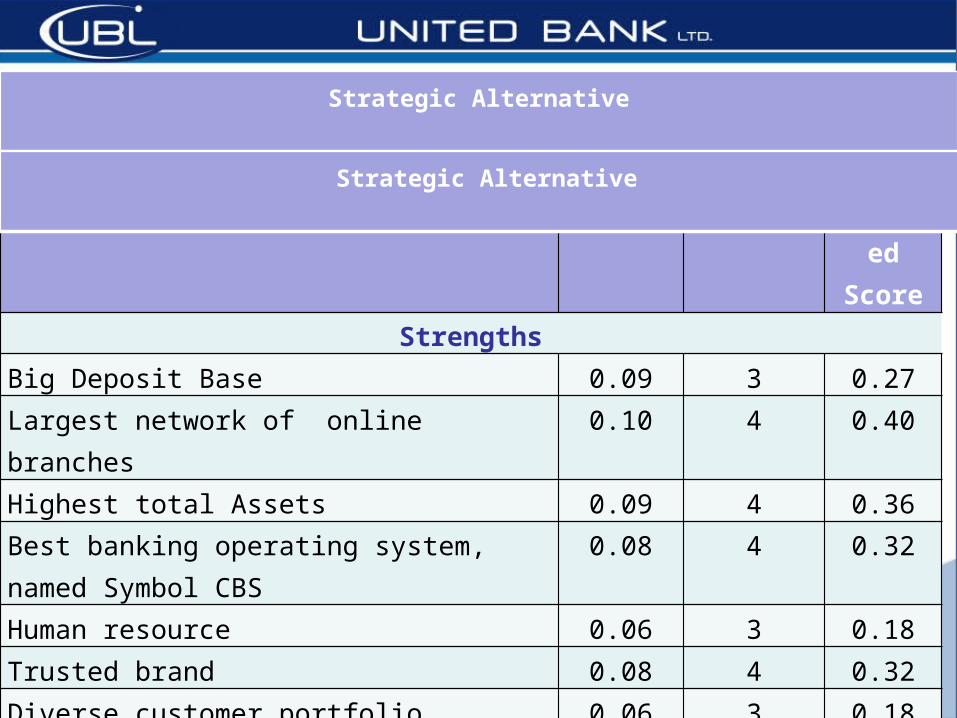

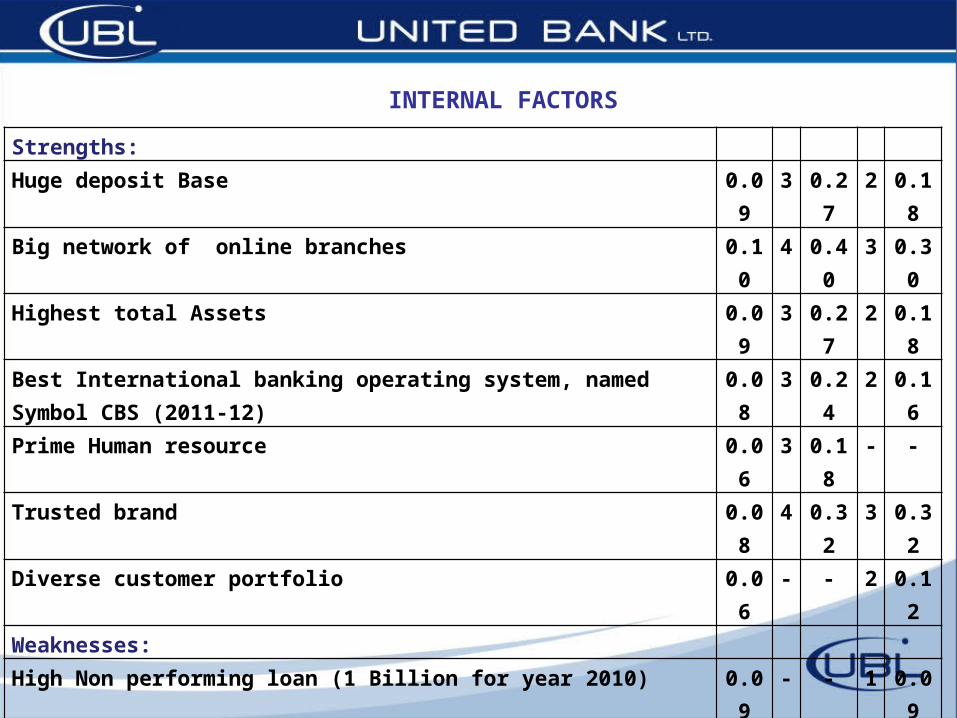

IFE

Internal Factor Weight Rating Weighted

ScoreStrengths

Big Deposit Base 0.09 3 0.27Largest network of online branches 0.10 4 0.40Highest total Assets 0.09 4 0.36Best banking operating system, named Symbol CBS

0.08 4 0.32

Human resource 0.06 3 0.18Trusted brand 0.08 4 0.32Diverse customer portfolio 0.06 3 0.18

Strategic AlternativeStrategic Alternative

Strategic Alternative

WeaknessesHigh Non performing loan (1.4 Billion for year 2010)

0.09 1 0.09

High ratio of high cost deposit to total deposit 0.10 1 0.10Customer service 0.07 1 0.07High turnover of employees 0.05 2 0.10Always increasing bank service charges 0.06 2 0.12The physical environment of HBL’ branches is not attractive to the people

0.07 2 0.14

Total 1.00 2.65

As the score is above than average score i.e. 2.50, which means UBL has better internal position.

Strategy Analysis

Strengths -S Weaknesses-W

SWOT MATRIX 1) Competitively High deposit Base

2) Big network of online branches3) Best banking operating system, 4) Human resource5) Trusted brand 6) Highest total assets7) Diverse customer portfolio

1) High Non Performing Loan2) High ratio of high cost deposit to total deposit3) Inefficient Customer service4) High turnover of employees5) Always increasing bank service charges6) The physical environment of some of UBL

branches is not attractive to the people

Opportunities-O SO Strategies WO Strategies

1. Implementation of Basel II & III Accord by SBP2. Growing no of people using banking facilities,

especially in peripheral areas.3. Wide range of online network of branches can be

used to cater low cost deposit.4. Increase Low cost deposits decrease high cost5. Expand globally6. Diversification towards islamic banking and non-

banking services

1) Acquire banks which are not in a position to meet Basel –II requirements (S1,S3,S4, O1) (Horizontal Integration)

2) Continue to Provide banking facility to those people who are not using this facility at the movement(S2,O2) (Market Development)

1)Take over an islamic bank having better customer service , Earning Sufficient Fee based Income and having low operating cost ( W2,W3,O6) (Horizontal Integration)

Threats-T ST Strategies WT Strategies

1) SBP Tight Monetary policy2) Customer service attitude problem3) Shrinking Margins Due to New Entrants and less

investment opportunities4) Withholding tax on banking transaction5) People’s low savings due to High Inflation 6) Social pressure on Govt. to reduce bank’s spread7) SBP Anti Money Laundering/KYC/CDD/EDD

Regulations8) High Operational Cost

1) Use large branch network to cater low-cost deposit from market by introducting new products

(T3, S2) Product development

1) Lending should be prudent to avoid NPL (W1, T1)

2) High cost deposit should be reduced (T3, W2)

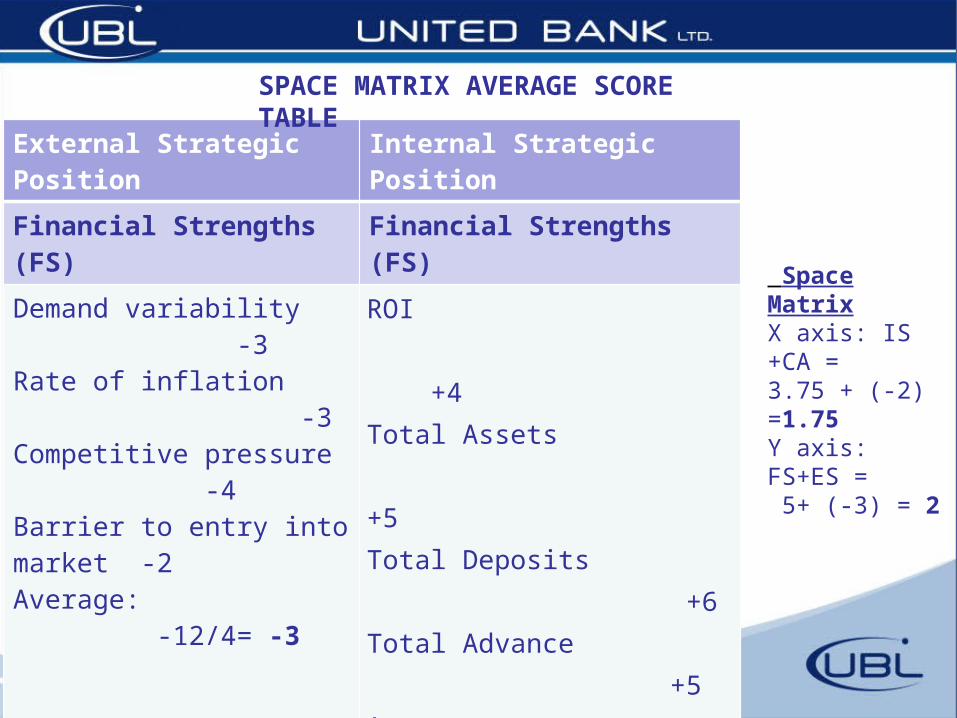

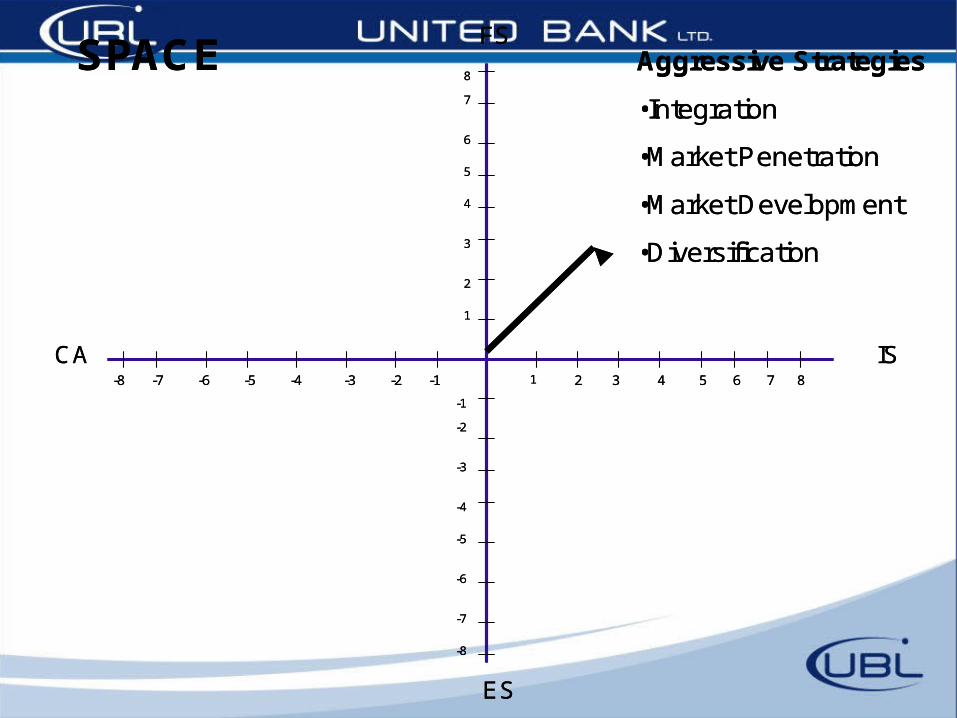

SPACE MATRIX

External Strategic Position

Internal Strategic Position

Financial Strengths (FS)

Financial Strengths (FS)

Demand variability -3Rate of inflation -3Competitive pressure -4Barrier to entry into market -2 Average: -12/4= -3

ROI +4Total Assets +5Total Deposits +6Total Advance +5Average : 20/4= 5

Industry Growth (IS) Competitive Advantage (CA)

Growth potential +5Profit potential +5Ease of entry into market +1Financial stability +4 Average : 15/4= 3.75

Market share -1Service quality -3Trusted brand -2Technological knowhow -2 Average: -8/4= -2

SPACE MATRIX AVERAGE SCORE TABLE

Space MatrixX axis: IS +CA = 3.75 + (-2) =1.75Y axis: FS+ES = 5+ (-3) = 2

FS

IS

ES

CA1 2 3 4 5 6 7 8-8 -7 -6 -5 -4 -3 -2 -1

8

7

6

5

4

3

2

1

-8

-7

-6

-2

-3

-4

-5

-1

Aggressive Strategies

•Integration

•Market Penetration

•Market Development

•Diversification

SPACEFS

IS

ES

CA1 2 3 4 5 6 7 8-8 -7 -6 -5 -4 -3 -2 -1

8

7

6

5

4

3

2

1

-8

-7

-6

-2

-3

-4

-5

-1

Aggressive Strategies

•Integration

•Market Penetration

•Market Development

•Diversification

SPACE

Matching Stage

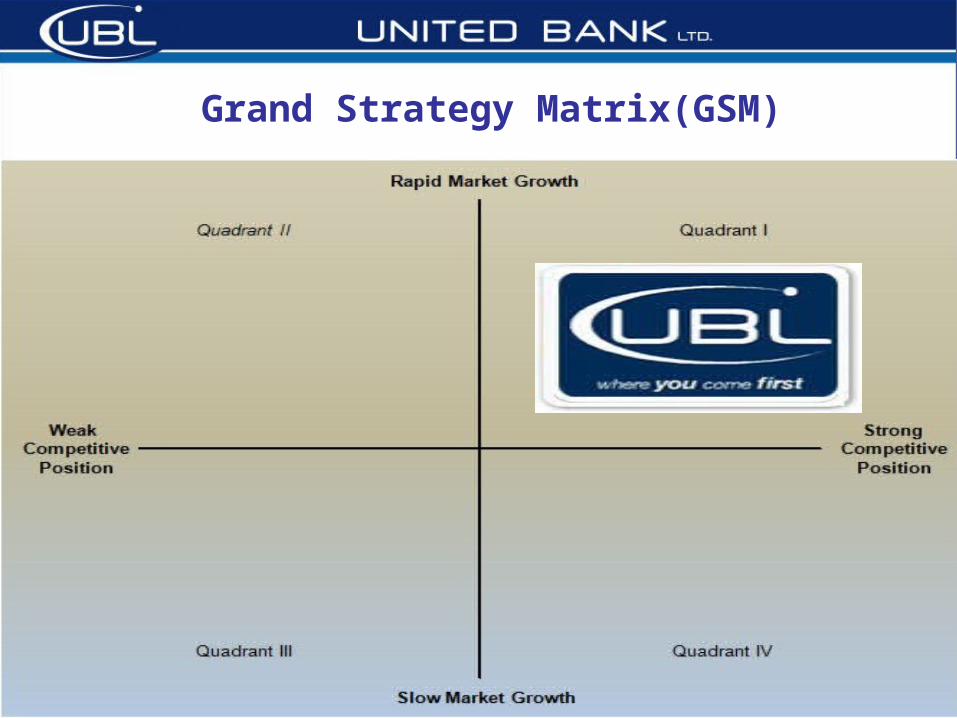

Grand Strategy Matrix(GSM)

BCG MATRIX

“Star” is recommended for UBL

DECISION MAKING

Quantitative Strategic Planning Matrix (QSPM)

EXTERNAL FACTORSKey Factors Weight AS TAS AS TAS

Market Development

Product Development

Opportunities:Implementation of Basel II Accord by SBP i.e. product and market development through acquisition

0.08 3 0.24 2 0.16

Increasing no of people using banking facilities to fulfill their financial and non financial needs

0.09 4 0.36 4 0.36

Vast online network of branches can be used to cater low cost deposit 0.07 3 0.21 3 0.21Partial Shift of Banking culture from deposit based income to fee based income

0.06 2 0.12 3 0.18

Increase Customer base through joint ventures and acquisition and mergers 0.08 4 0.32 2 0.16Diversification towards Islamic banking and non banking services 0.07 1 0.07 3 0.21

Threats:SBP Strict monetary policy/ High discount rate 0.09 1 0.09 2 0.18Customer service Attitude Problem 0.07 2 0.14 - -Shrinking Margins Due to New Entrants and less investment opportunities 0.09 2 0.18 3 0.27Withholding tax on banking transactions 0.06 - - - -People’s Low savings due to High inflations/ Price fluctuations 0.08 2 0.16 3 0.24Social pressure on Govt. to reduce bank’s spread 0.07 1 0.07 - -SBP A/Money Laundering & Know your Customer – CDD- EDD Policy 0.04 - - - -High Operational Cost 0.05 2 0.10 2 0.10

1.00

Strengths:Huge deposit Base 0.09 3 0.27 2 0.18Big network of online branches 0.10 4 0.40 3 0.30Highest total Assets 0.09 3 0.27 2 0.18Best International banking operating system, named Symbol CBS (2011-12) 0.08 3 0.24 2 0.16Prime Human resource 0.06 3 0.18 - -Trusted brand 0.08 4 0.32 3 0.32Diverse customer portfolio 0.06 - - 2 0.12Weaknesses:High Non performing loan (1 Billion for year 2010) 0.09 - - 1 0.09Big ratio of high cost deposit to total deposit 0.10 2 0.20 4 0.40Inefficient Customer service 0.07 - - 1 0.07High turnover of employees 0.05 - - - -increasing trend in bank service charges 0.06 - - 3 0.18The physical environment of UBL most branches is not attractive to the people 0.07 2 0.14 3 0.21

1.00 4.08 4.28

INTERNAL FACTORS

The sum of Total Attractiveness Score (TAS) shows that product development is slightly better alternative then

market development.

We will recommend for UBL management to keep on improving their growth strategies as following:-• Product development by:-

– Freedom Acct– Straight to bank – online banking like std chartered

• Market penetration by:- – Fees off/ lending criteria soft– More Branches at remote

• Horizontal Diversification by:- – Branchless Banking like Omni to be matured– Easy Paisa like Tameer Bank– Insurance

• Market Development by:-– More advertisement through celebrities

Recommended Strategies

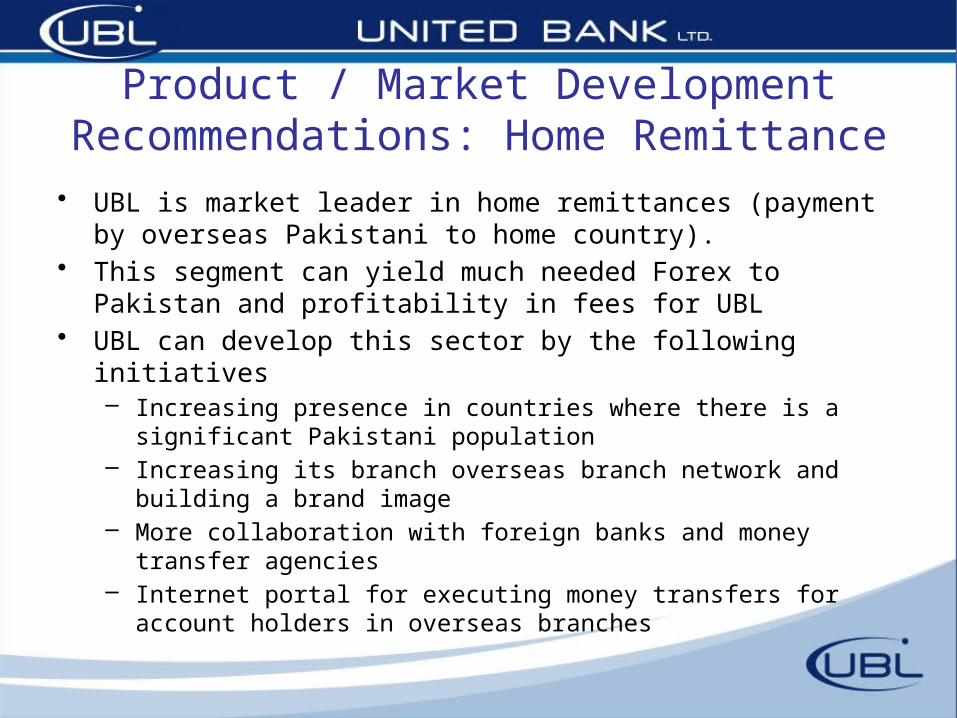

Product / Market Development Recommendations: Home Remittance

• UBL is market leader in home remittances (payment by overseas Pakistani to home country).

• This segment can yield much needed Forex to Pakistan and profitability in fees for UBL

• UBL can develop this sector by the following initiatives– Increasing presence in countries where there is a significant

Pakistani population– Increasing its branch overseas branch network and building a

brand image– More collaboration with foreign banks and money transfer

agencies– Internet portal for executing money transfers for account

holders in overseas branches

Product / Market Development Recommendations: Mobile Banking

• UBL is a significant competitor in the mobile banking services segment in the country via its flagship product UBL Omni

• The launch of instantaneous ATM/Debit card feature to UBL Omni customer should build even further to truly harness the potential of branchless banking

• UBL can develop this sector by the following initiatives– Expansion of the Omni Network Outlets– Introduction of phone banking to Omni Account holders– Share significant commissions on transactions with Omni

Outlet owners to penetrate the market aggressively– More aggressively price money transfers and bill payment

products in UBL Omni– Offer other services such as Bancassurance and small loans of

PKR 1000 to Omni account holders

Product / Market Development Recommendations: Bancassurance

• UBL has collaborated with State Life, Jublee Life and EFU Life for life bancassurance of its customers

• UBL can develop this segment by the following initiatives– Introducing health insurance products– Introducing wallet protection products (theft of ATM

card and cash)– Enable UBL customers to obtain bancassurance for

their clients and customers

Product / Market Development Recommendations: Islamic Banking

• UBL has an Islamic banking division of UBL Ameen however it is not as competitive as other players in Islamic Baking

• UBL can develop this segment by the following initiatives– Increasing the number of Ameen branches– Increasing the product line and building a brand image– Offer similar convenience products to Ameen customers

as offered to UBL conventional banking customers with linkages with the conventional banking setup

Product / Market Development Recommendations: Cash Management

Solution• UBL currently offers cash management solutions to its

corporate customers which caters to their need of payment to suppliers and cash collection from customers

• UBL can develop this segment by the following initiatives– Implementing a strong and state of the art cash management

portal on the internet such as the product Straight2Bank offered by Standard Chartered Bank

– Lower fees and actively promote cash management solutions to medium size enterprises as they are expected to grow in future

– Build on the phone banking collection mechanism recently introduced and further enhance the phone banking experience

General Internal Systems related recommendations

• Proper and complete implementation of the new Investment in a new core banking system and state of the art treasury management systems

• Another change in core banking application may be necessary due to the dynamic chnages in the Banking Industry, IT and development of branchless banking with huge database requirements

• Investment in Security Systems and procedures to reduce the likelihood of bank robberies and risk of fraud

• More investment in infrastructure and branch outlook to enhance customer experience

• Improve Human telent retention and talent acquisition programs

• Institute job rotation and internal training programs• Reduce influence of UBL unions “collective bargaining

agents’

General Internal Financial Condition related recommendations

• Offset spread compression through balance sheet growth in deposits

• Shedding of opportunistic and expensive deposits and Improve CASA ratio

• Refocus on growth of advances portfolio despite reduction in interest rates to stimulate economic growth and interest in UBL by medium scale companies

• Check on the delinquency ratio • Restructuring and rescheduling of non performing loans• Derivative market entrance (Market making)• Most of the banking sector is investing excess liquidity in

government securities, alternative channels of investments should be determined

External Environmental Concerns

• Pakistan’s economy continues to underperform• Underlying fundamental problems of energy crisis, circular

debt, law and order situation, depleting foreign reserve and widening budget deficit (according to IMF the budget deficit is expected to reach 7% of GDP against a target of 4.7%)

• Unprecedented depreciation of the Rupee• Continuous borrowing from government may lead to

banking circular debt crisis• Uncertainty regarding the upcoming election which may

lead to a hung parliament and as a result the government may not be able to secure more funds from the IMF

• Large scale manufacturing growth is still meager

Strategy Implementation

Annual ObjectivesPoliciesResource allocationManaging conflictsOrganizational designChangeMarketing issuesFinancial Issues

Thank You For your patience

and active participation