Strategic Analysis

22

Coursework - 1 Strategic Analysis & Planning (ST4S15) 20/12/2012 Tutor: Dr. Will Williams Submitted by: 12012661, Premkishan Sharma

-

Upload

premkishan-sharma -

Category

Documents

-

view

102 -

download

4

description

Strategic Analysis and Planning

Transcript of Strategic Analysis

Coursework - 1Strategic Analysis & Planning (ST4S15)

20/12/2012

Tutor: Dr. Will Williams

Submitted by:

12012661

Contents

INTRODUCTION...............................................................................................................2

1. ABOUT THE ORGANISATIONS INVOLVED IN THE EVENT & COMPETITIVE ANALYSIS.........32. STAKEHOLDERS ANALYSIS.................................................................................................53. WHAT ARE THE KEY EXTERNAL FACTORS DRIVING STRATEGIES BEHIND THIS ACQUISITION?............................................................................................................................ 6

Political................................................................................................................................ 6Economic.............................................................................................................................6Socio-cultural.....................................................................................................................7Technology.........................................................................................................................7

4. AN APPRAISAL OF VALUE ADDING ACTIVITIES THIS ACQUISITION OFFERS TO UMG.....105. BIBLIOGRAPHY..................................................................................................................13

1

12012661

Introduction

EMI-Universal deal cleared by EU and US regulators (BBC, 2012).

On 21st September 2012, the European Commission (“EC”) and US Federal Trade Commission (“FTC”) approved the acquisition of EMI’s recorded music business by Universal Music Group (“UMG”) after the latter announced its purchase of EMI for a sum of $ 1.9bn in November 2011(BBC, 2012). The deal was cleared after several months’ of review by EC, FTC and other antitrust authorities to facilitate fair and effective competition within the music industry. However, the deal is subject to condition that UMG will dispose a substantial fraction (approximately one third) of EMI’s assets (European Commission, 2012). These assets include the famous Parlophone Label, home to artists such as David Guetta, Pink Floyd, Coldplay and Kylie Minogue, EMI’s classical music labels, Chrysalis, Mute and numerous other local business units of EMI globally (EuropeanCommission, 2012).

For the purpose of this investigation EC specifically concentrated on online music market, where sales are expected to surpass the revenues generated by sale of conventional physical media (e.g. CDs, cassettes, etc.). (European Commission, 2012). Concentrating on same premise, the aim of this report is to strategically evaluate the acquisition of iconic British music company EMI by UMG. This evaluation document focuses on four major areas and they are categorised as below;

A brief introduction of both organisations; their core businesses, strategic business units (SBUs), their competitors and how they compete with each other?

Key stakeholders engaged in the event – a synopsis. An exhaustive analysis of key external factors driving this change. An appraisal of value adding activities this acquisition offers to UMG

and/or EMI.

2

12012661

1. About the organisations involved in the event & competitive analysis

EMI Music is one of the world’s largest music companies. It is primarily active in recorded music market (globally) with headquarters in London, UK. Before the acquisition, EMI Music was part of EMI Group which was owned by US based banking giant Citigroup Inc. since February 2011(BBC, 2011). EMI’s core business activities in recorded music business encompass physical (CDs, DVDs & other physical media) & digital distribution of music, promotion & sales of music albums, live recordings and merchandising besides discovery and acquisition of new artists. EMI owns various record labels such as Parlophone, Capitol, Virgin, EMI Christian Music Group, etc. Whereas, artists on roaster of EMI’s labels include renowned names like The Beatles, Coldplay, David Guetta, Kylie Minogue, Katy Perry, Pink Floyd, Snoop Dogg, to cite a few (EMI Music,2012).

Universal Music Group (UMG) is a solely-owned subsidiary of France based Vivendi Group and is world’s leading music company with offices in 60 countries spanning across Europe, North America and Asia, UMG is market leader in world’s biggest music markets, i.e. USA, Japan, UK, France and Germany (Marketline, 2012). It is active in wide array of businesses in music industry, viz.; recorded music, music publishing (through Universal Music Publishing Group) and merchandising of artists-and-music branded products (through Bravado) (Vivendi S.A., 2012a). Furthermore, UMG is engaged in, through its various subsidiaries, artist management, online music video services (VEVO), digital & physical distribution of music (mainly in USA) and also to a limited extent in online music retail, online music events management and event venue services (Universal MusicGroup, 2012a).

The music industry, in general, faces competition from other entertainment products for instance video games and movie industry which offers alternative avenues to consumer for spending. Globally and within various market segments, UMG competes for ownership of exclusive content (e.g. music catalogues) and artistic talent acquisition (new or established) with rival record labels such as Warner Music Group and Sony Music. To cite an example, UMG through its Schoolboy Records(Universal Music Group, 2012b) recently signed the Korean pop star Psy

3

12012661

(Gangnam Style fame) and gained exclusive publishing and management rights over him (Vena, 2012). Moreover, independent (Indie) labels also pose threat to company’s revenues, margins and market share in various segments and geographies worldwide (Marketline, 2012).

Through this acquisition UMG has not only further enhanced its brand image & position in leading music markets but have also strengthened its exclusive-content-portfolio & ownership of labels that will feature top-selling local and international artists including The Beatles, Katy Perry and Beach Boys. The combined company is expected to account for approximately 40% of global music market (Marketline, 2012). Thus, they have gained a distinctive edge over its competitors in realms of both physical and digital music markets.

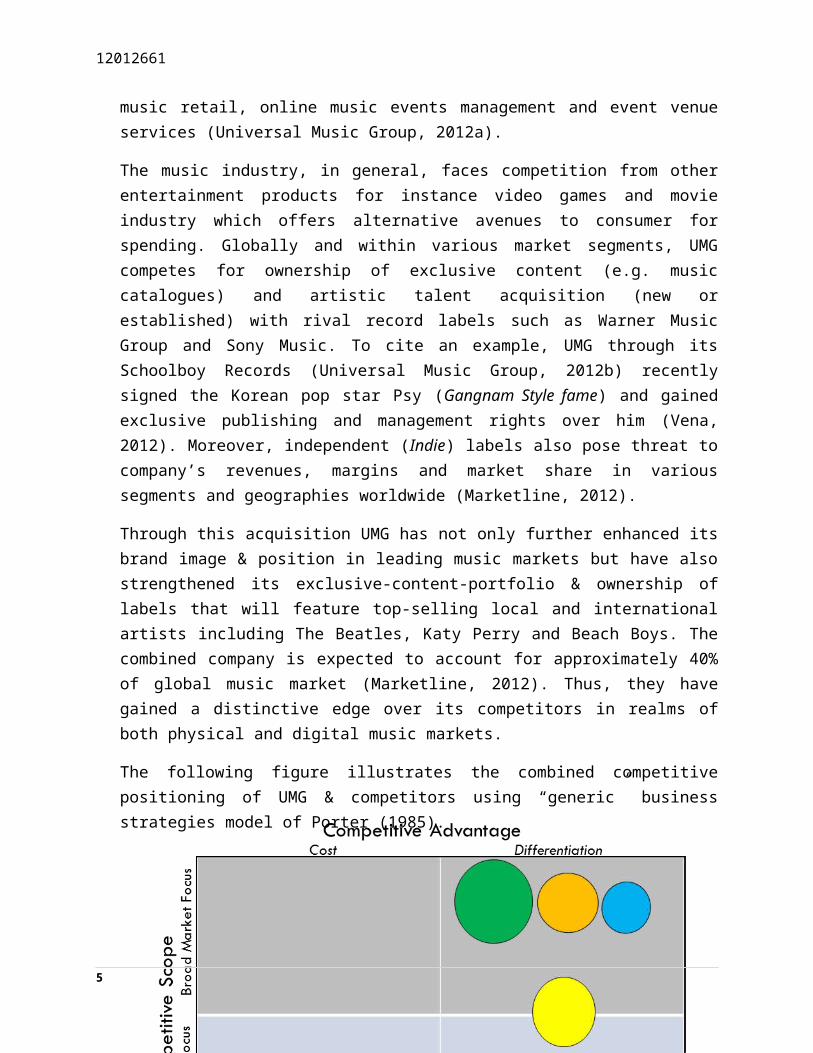

The following figure illustrates the combined competitive positioning of UMG & competitors using “generic” business strategies model of Porter (1985).

4

Figure 1: Competitive Analysis (Porter, 1985)

Legend:

Universal Music Group

Independent (Indie) Labels

Sony MusicWarner Music

12012661

As depicted in Figure 1, the key players in recorded music industry compete on broad focus scope and achieve differentiation based on perceived brand value of their labels, collection & content of music catalogues and more importantly by discovering-acquiring-promoting new artists and utilizing established artists on their respective roster of labels more effectively. However, Independent Labels which accounts for about 20% of market share (Association of Independent Music, 2012); contribute significantly by facilitating platform for smaller artists both budding and established ones in respective territories worldwide. It is worth noting that often Indies rely on established international distribution channels of major labels to promote their albums, songs and catalogues.

5

12012661

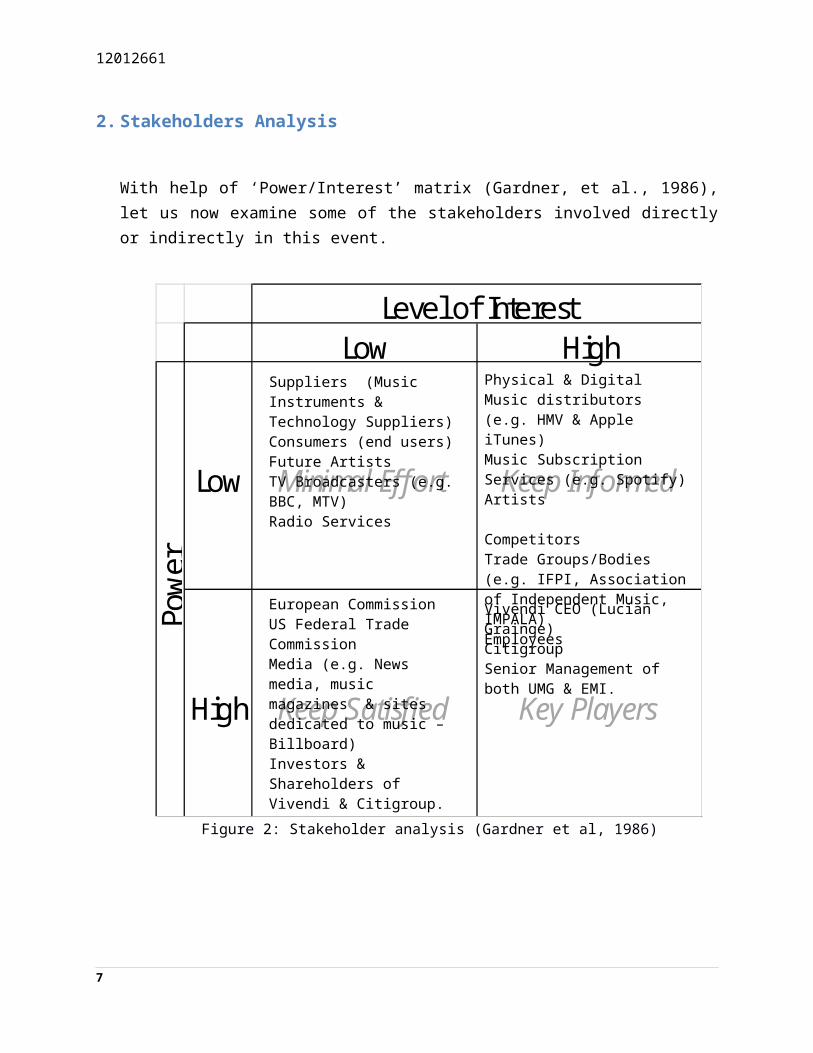

2. Stakeholders Analysis

With help of ‘Power/Interest’ matrix (Gardner, et al., 1986), let us now examine some of the stakeholders involved directly or indirectly in this event.

As portrayed in Figure 2, the key stakeholders in this event are respective parent companies, i.e. Vivendi & Citigroup and their CEOs, investors & shareholders for whom they intend to create value and management of both UMG & EMI. In addition to that, EC & FTC have played an important

6

Low High

Low Minimal Effort Keep Informed

High Keep Satisfied Key Players

Level of Interest

Pow

er

Figure 2: Stakeholder analysis (Gardner et al, 1986)

• Vivendi CEO (Lucian Grainge)

• Citigroup• Senior Management

of both UMG & EMI.

• European Commission

• US Federal Trade Commission

• Media (e.g. News media, music magazines & sites dedicated to music – Billboard)

• Investors & Shareholders of

• Suppliers (Music Instruments & Technology Suppliers)

• Consumers (end users)

• Future Artists• TV Broadcasters (e.g.

BBC, MTV)

• Physical & Digital Music distributors (e.g. HMV & Apple iTunes)

• Music Subscription Services (e.g. Spotify)

• Artists

• Competitors• Trade Groups/Bodies

(e.g. IFPI, Association of Independent Music, IMPALA)

• Employees

12012661

role not only as regulatory authorities but also by imposing conditions as part of approval requisites and this may affect the intended strategy of UMG.

3. What are the key external factors driving strategies behind this acquisition?

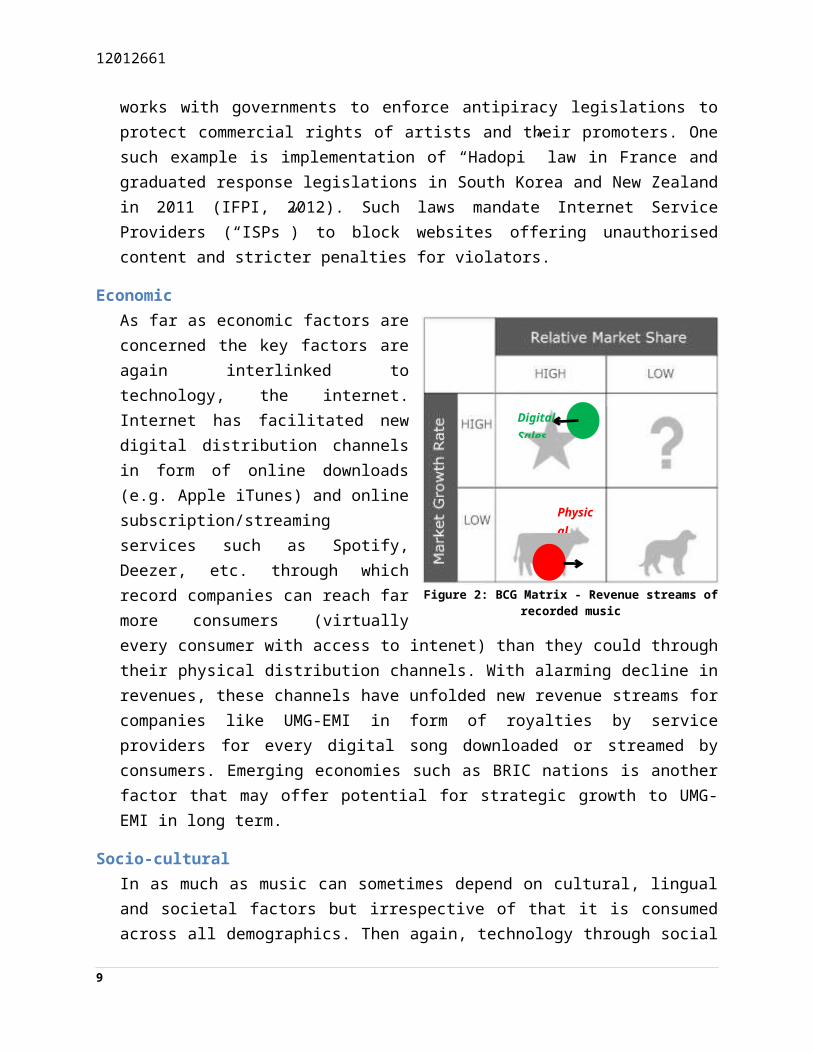

The landscape of music industry has transformed dramatically over the past decade with advent of new technological platforms (online and mobile) and the way music is being made available to the consumers. However, it is not just technology which is acting as catalyst in UMG-EMI case, there are other factors (such as political, economic & socio-cultural) which are interlaced and deserve a detailed scrutiny. These factors will help us shed light on the rationale behind UMG’s takeover of EMI at a time when the global sales of recorded music have declined by 33% when compared against $23.3bn in 2003 to $15.9bn in 2010 (Vivendi S.A.,2011). The current trend in recorded music industry is depicted using BCG matrix in Figure 3.

PoliticalGovernments play an important role in protecting original creations of artists through copyright laws. In recent times, the anti-piracy legislations introduced by several governments have proved instrumental in restoring momentum within industry (IFPI, 2012). International Federation of the Phonographic Industry (“IFPI”) which represents recording industry globally works with governments to enforce antipiracy legislations to protect commercial rights of artists and their promoters. One such example is implementation of “Hadopi” law in France and graduated response legislations in South Korea and New Zealand in 2011 (IFPI,2012). Such laws mandate Internet Service Providers (“ISPs”) to block websites offering unauthorised content and stricter penalties for violators.

EconomicAs far as economic factors are concerned the key factors are again interlinked to technology, the internet. Internet has facilitated new digital distribution channels in form of online downloads (e.g.

7

Digital

Physical

12012661

Apple iTunes) and online subscription/streaming services such as Spotify, Deezer, etc. through which record companies can reach far more consumers (virtually every consumer with access to intenet) than they could through their physical distribution channels. With alarming decline in revenues, these channels have unfolded new revenue streams for companies like UMG-EMI in form of royalties by service providers for every digital song downloaded or streamed by consumers. Emerging economies such as BRIC nations is another factor that may offer potential for strategic growth to UMG-EMI in long term.

Socio-cultural

In as much as music can sometimes depend on cultural, lingual and societal factors but irrespective of that it is consumed across all demographics. Then again, technology through social media (Facebook & Twitter) is transforming the way fans can associate with artists or vis-à-vis. This offers an open avenue for UMG-EMI to promote their artists at virtually no cost.

TechnologyAs discussed above, undoubtedly the most important external factor of all is technology which has entirely changed the way music is experienced & accessed by consumers and will continue to do so in foreseeable future. As per IFPI’s Digital Music Report (2012), digital music subscribers have grown by 65% in 2011 from 8.2 million of 2010 to 13 million and there are approximately 500 online music service providers worldwide (download, subscribe, video streaming, etc.). Besides this, ISPs and telecom companies too are creating digital business models for music companies, e.g. in the UK, Virgin Media partnered with Spotify and Orange with Deezer for their mutual benefits (IFPI, 2012). Furthermore, smartphones are now shifting music from PCs to mobile phones, with growth and penetration of broadband internet and handheld devices in both developed and emerging markets (Jackson, 2012) (Kennedy, 2012) it is likely that digital sales will continue to grow through services such as Apple iTunes, Spotify, on demand music videos and similar subscription based digital services. In order to offer extra value and broader service to consumers, innovations have also led to birth of cloud based music services such as Apple iTunes Match that allows users to access their entire music collection, including songs obtained from sources other than iTunes, on devices of their choice at an annual subscription fee of $24.99 (Apple Inc., 2012). The launch was welcomed and regarded as a revenue booster by Paul Smernicki, director of digital for Universal Music UK and

8

12012661

some reports also suggested that it will help record labels monetize illegal downloads with Apple agreeing to share a portion of subscription fee with them (BBC, 2011).

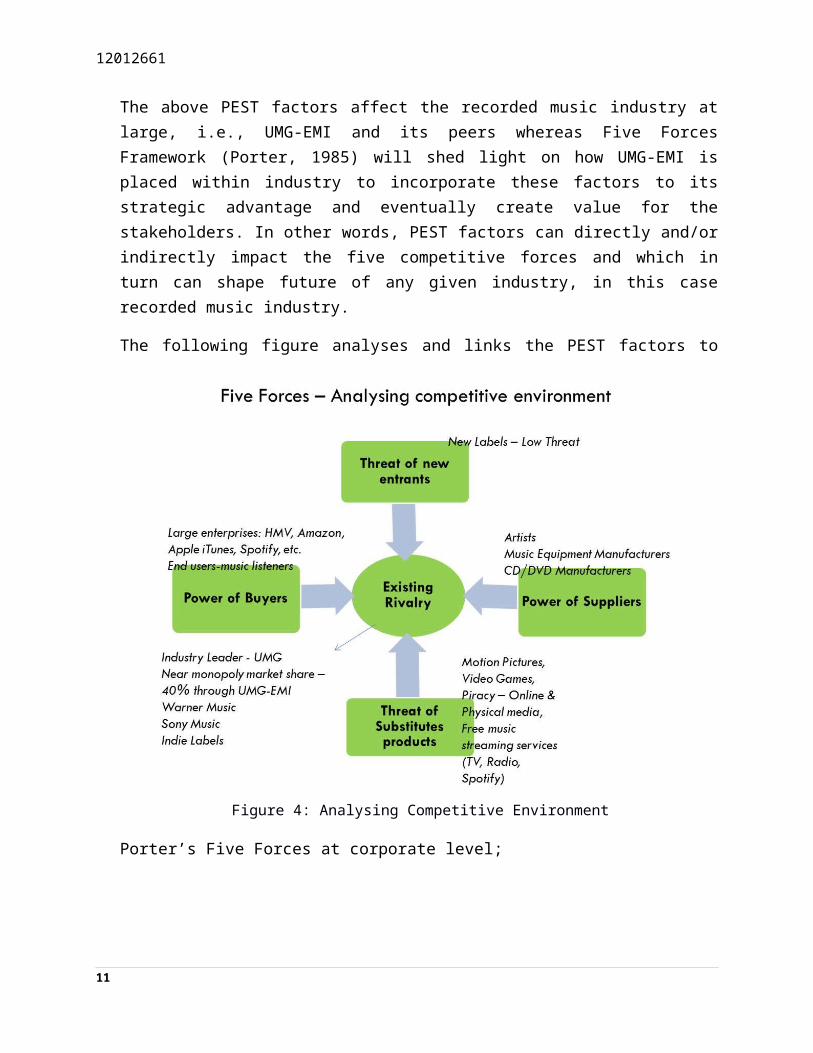

The above PEST factors affect the recorded music industry at large, i.e., UMG-EMI and its peers whereas Five Forces Framework (Porter, 1985) will shed light on how UMG-EMI is placed within industry to incorporate these factors to its strategic advantage and eventually create value for the stakeholders. In other words, PEST factors can directly and/or indirectly impact the five competitive forces and which in turn can shape future of any given industry, in this case recorded music industry.

The following figure analyses and links the PEST factors to Porter’s Five

Forces at corporate level;

9

Figure 4: Analysing Competitive Environment

12012661

Power of Buyers: Buyers for UMG-EMI can be categorised as Corporates and End-users; large enterprises like HMV, Amazon, Apple iTunes and Spotify buy albums and songs in bulk through contract negotiations. Power of buyers potentially depend on the size of deal being negotiated, however, it can be assumed that with more and more revenues streams shifting towards online channels corporates like Apple iTunes and Spotify will have relatively higher power. On the other hand, consumers who have low switching cost, also have high power due to alternative channels to source music are available to them in form of online or offline piracy.

Power of Suppliers: Artists serves as supplier for music labels of any music company for through artists UMG gets access to music. The bargaining power of such suppliers is arguably high as each singer is unique and has a distinct voice and fan following which cannot be substituted. Moreover, artists can now utilise technology to promote themselves on internet and sell their albums/songs, thus rendering them even more power.

Threat of New entrants: New entrants pose a minimal threat to UMG-EMI because music industry is much specialised industry and requires lot of financial prowess and skilful resources for promotion, marketing and distribution.

Threat of substitutes: Substitute for the products and services offered by UMG-EMI can be characterised as primary and secondary, primary

10

12012661

substitutes offer similar products and services. These can be in form of Radio services, TV channels dedicated to music and ad-based subscription services provided by Spotify, Deezer and YouTube. In addition to these, freely downloadable pirated music is a primary substitute. Thus, primary substitutes pose high threat as they can hinder sales revenue of UMG-EMI. However, secondary substitutes are alternative entertainment products such as motion pictures and video games pose a low threat.

Competitive Rivalry: Decline in physical sales and growth in digital revenues has changed the industry paradigm, innovative digital monetizing models are being explored by existing players to compensate declining CD sales revenues. Although rivalry within industry remains intense, the acquisition of EMI has certainly made UMG more powerful in the industry due to the sheer size of combined labels, artists, repertoire and back catalogues. The combined market share of UMG-EMI is now approximately 40% (Marketline, 2012) whereas the industry rivalry is now just among 3 major labels i.e. UMG-EMI, Warner Music and Sony Music. This lends UMG-EMI a distinct advantage at least in terms of content ownership, copyrights, artist and repertoire.

11

12012661

4. An appraisal of value adding activities this acquisition offers to UMG.

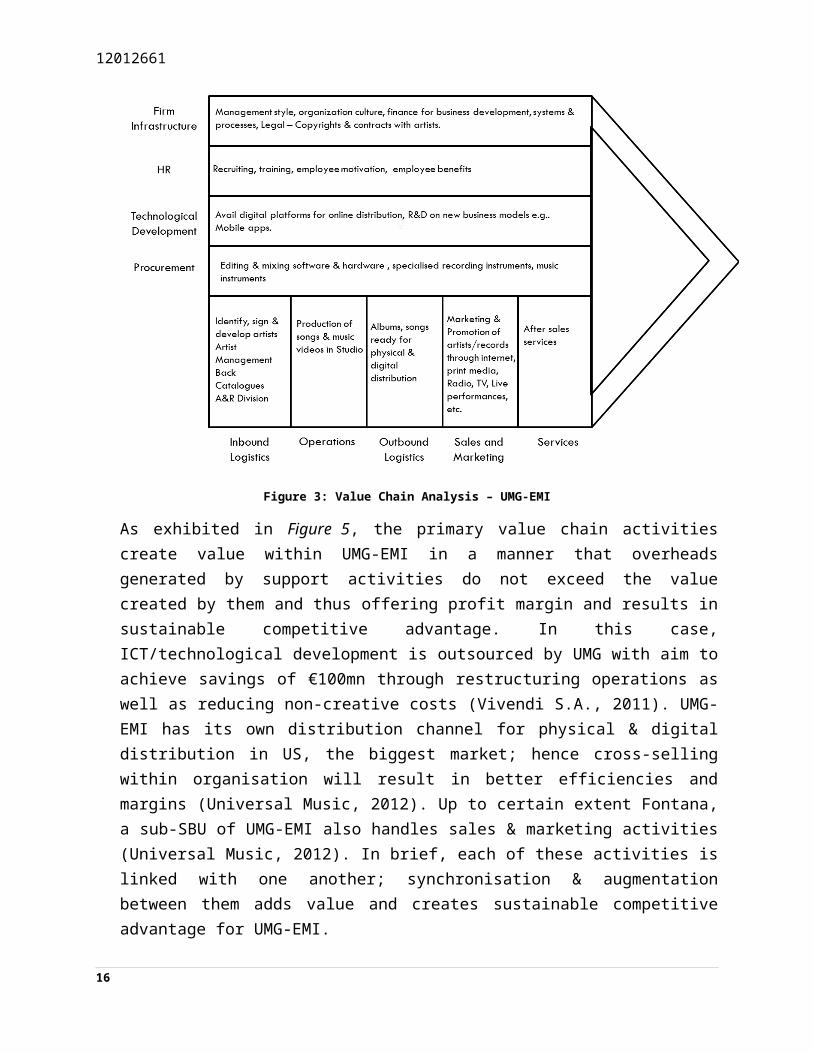

Having examined the external environment of UMG-EMI it is essential now to inspect how UMG-EMI aligns its combined resources to exploit the opportunities as well as tackle the threats, and finally conclude whether this acquisition adds value or cost using Porter’s value chain model at corporate level. A summary of UMG-EMI’s resources is tabulated below;

PHYSICAL RESOURCES FINANCIAL RESOURCES Combined Operations in more

than 60 countries across the globe

Established physical and online music distribution channels

World renowned state-of-art studios in US & UK

Strong list of music labels & back catalogues under combined umbrella

SBUs: Bravado & Publishing Group

Universal Music Group - Recorded Music (Vivendi S.A.,2012b)

Annual revenues: €3,367mn for FY2011

EBITDA 2011: €304mn (+14.3% of 2010)

Parent company Vivendi’s new €5.0bn credit facility

Approximate value of EMI assets to be divested: €500mn

EMI Recorded Music (MaltbyCapital Ltd, 2010)

Annual Revenues of ₤1,173mn for FY2009/2010

EBITDA: ₤184mn (+15% of 2008/2009)

HUMAN RESOURCES INTANGIBLE RESOURCES

Trained & motivated human capital: about 6,500 employees

Talented & Dynamic A&R executives

Share-based compensation plan for employees

Dedicated workforce for digital markets & digital services.

Joint Ventures: Vevo with Google Strategic Marketing Partnerships

(SMPs) in Emerging markets Involvement with Media:

American Idol & The Voice Combined Brand Value Vivendi’s S&P & Moody’s Credit

Ratings: Stable (BBB, Baa2 respectively)

Access to exclusive & vast music content through music publishing arm

12

12012661

It can be argued that UMG-EMI may have common resources as its peers due to nature of the industry they operate in; however, the size of these resources gives them distinction. It can also be stated that resources acquired from EMI will not only complement UMG’s brand value but will attract more artistic talent. Easy access to capital for investment in business development & innovations through Vivendi adds to the strength of UMG-EMI. Furthermore, higher employee motivation due to share-based compensations is an added advantage to UMG-EMI’s core resources. Arguably, UMG-EMI’s unique & most valuable resources are its suppliers i.e. the artists, a resource that have rarity and cannot be imitated by other labels.

Using Porter’s Value Chain model it can be demonstrated how these resources are linked with each other and help in creating value for UMG-EMI, if any.

Figure 5: Value Chain Analysis – UMG-EMI

As exhibited in Figure 5, the primary value chain activities create value within UMG-EMI in a manner that overheads generated by support activities do not exceed the value created by them and thus offering profit margin and results in sustainable competitive advantage. In this case, ICT/technological development is outsourced by UMG with aim to achieve

13

12012661

savings of €100mn through restructuring operations as well as reducing non-creative costs (Vivendi S.A., 2011). UMG-EMI has its own distribution channel for physical & digital distribution in US, the biggest market; hence cross-selling within organisation will result in better efficiencies and margins (Universal Music, 2012). Up to certain extent Fontana, a sub-SBU of UMG-EMI also handles sales & marketing activities (Universal Music,2012). In brief, each of these activities is linked with one another; synchronisation & augmentation between them adds value and creates sustainable competitive advantage for UMG-EMI.

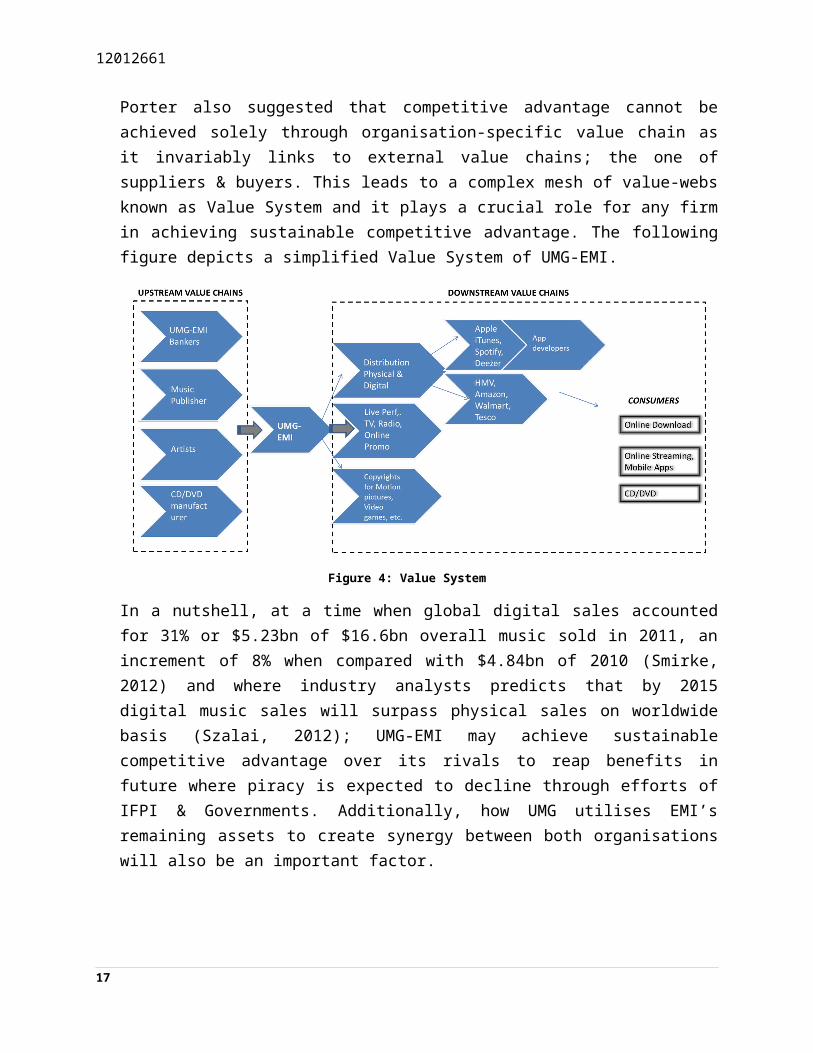

Porter also suggested that competitive advantage cannot be achieved solely through organisation-specific value chain as it invariably links to external value chains; the one of suppliers & buyers. This leads to a complex mesh of value-webs known as Value System and it plays a crucial role for any firm in achieving sustainable competitive advantage. The following figure depicts a simplified Value System of UMG-EMI.

Figure 6: Value System

In a nutshell, at a time when global digital sales accounted for 31% or $5.23bn of $16.6bn overall music sold in 2011, an increment of 8% when compared with $4.84bn of 2010 (Smirke, 2012) and where industry analysts predicts that by 2015 digital music sales will surpass physical sales on worldwide basis (Szalai, 2012); UMG-EMI may achieve sustainable competitive advantage over its rivals to reap benefits in future where piracy is expected to decline through efforts of IFPI & Governments. Additionally, how UMG utilises EMI’s remaining assets to

14

12012661

create synergy between both organisations will also be an important factor.

15

12012661

5. Bibliography

Apple Inc., 2012. Apple - iTunes - Match. [Online] Available at: http://www.apple.com/itunes/itunes-match/[Accessed 9 December 2012].

Association of Independent Music, 2012. Our Members. [Online] Available at: http://www.musicindie.com/about/aimmembers[Accessed 28 November 2012].

BBC, 2011. BBC News - Apple iTunes match music service launches with outage. [Online] Available at: http://www.bbc.co.uk/news/technology-16217630[Accessed 9 December 2012].

BBC, 2011. EMI taken over by Citigroup in deal to write off debts. [Online] Available at: http://www.bbc.co.uk/news/business-12339299[Accessed 26 November 2012].

BBC, 2012. EMI-Universal deal cleared by EU and US regulators. [Online] Available at: http://www.bbc.co.uk/news/business-19672277[Accessed 26 November 2012].

EMI Music, 2012. EMI Music. [Online] Available at: http://www.emimusic.com/about/[Accessed 26 November 2012].

European Commission, 2012. Press Release - Mergers: Commission clears Universal's acquisition of EMI's recorded music business, subject to conditions. [Online] Available at: http://europa.eu/rapid/pressReleasesAction.do?reference=IP/12/999[Accessed 26 November 2012].

Gardner, J. R., Rachlin, R. & Sweeny, A., 1986. Handbook of Strategic Planning. 99 ed. New York: John Wiley and Sons Ltd.

16

12012661

IFPI, 2012. Digital Music Report 2012. [Online] Available at: http://ifpi.org/content/library/DMR2012.pdf[Accessed 2 December 2012].

Jackson, M., 2012. Growth Slows as Global Broadband Subscribers Total 624.1M in Q2 2012. [Online] Available at: http://www.ispreview.co.uk/index.php/2012/10/growth-slows-as-global-broadband-subscribers-total-624-1m-in-q2-2012.html[Accessed 3 December 2012].

Kennedy, J., 2012. Smartphone penetration keeps accelerating (info graphic). [Online] Available at: http://www.siliconrepublic.com/digital-life/item/26074-smartphone-penetration-keep[Accessed 3 December 2012].

Maltby Capital Ltd, 2010. EMI Reports. [Online] Available at: http://www.emimusic.com/about/reports/[Accessed 5 December 2012].

Marketline, 2012. Universal Music Group, Swot Analysis. [Online] Available at: http://web.ebscohost.com.ergo.glam.ac.uk/ehost/pdfviewer/pdfviewer?vid=7&hid=125&sid=3abda080-5451-46d0-8051-541a1d79074a%40sessionmgr104[Accessed 28 November 2012].

Porter, M., 1985. Competitive Strategy. New York: Free Press.

Smirke, R., 2012. IFPI 2012 Report: Global Music Revenue Down 3%; Sync, PRO, Digital Income Up. [Online] Available at: http://www.billboard.biz/bbbiz/industry/global/ifpi-2012-report-global-music-revenue-down-1006571352.story[Accessed 3 December 2012].

Szalai, G., 2012. Forecast: U.S. Digital Recorded Music Sales to Top Physical Sales This Year. [Online] Available at: http://www.hollywoodreporter.com/news/download-music-streaming-digital-revenue-362799[Accessed 3 December 2012].

Universal Music Group, 2012a. Overview. [Online] Available at: http://www.universalmusic.com/company

17

12012661

[Accessed 26 November 2012].

Universal Music Group, 2012b. UNIVERSAL MUSIC GROUP (UMG) AND SCOOTER BRAUN’S SCHOOLBOY RECORDS EXPAND THEIR STRATEGIC PARTNERSHIP. [Online] Available at: http://www.universalmusic.com/corporate/detail/1875[Accessed 28 November 2012].

Universal Music, 2012. Overview. [Online] Available at: http://www.universalmusic.com/company[Accessed 26 November 2012].

Vena, J., 2012. Justin Bieber's Manager Signs Korean YouTube Star Psy. [Online] Available at: http://www.mtv.com/news/articles/1693103/justin-bieber-manager-signs-psy.jhtml[Accessed 28 November 2012].

Vivendi S.A., 2011. UMG Investor Meeting Nov 2011. [Online] Available at: http://www.vivendi.com/wp-content/uploads/2011/11/umg-investor-presentation-november-2011-final.pdf[Accessed 2 December 2012].

Vivendi S.A., 2012a. Music | Vivendi Corporate. [Online] Available at: http://www.vivendi.com/activities/music/[Accessed 26 November 2012].

Vivendi S.A., 2012b. Financial Report 2011. [Online] Available at: http://www.vivendi.com/wp-content/uploads/2012/03/120302_2011_Financial_Report.pdf[Accessed 5 December 2012].

18