Stock Presentation - Fisher College of Business · Stock Presentation Consumer ... Weakness in...

34

Presenters: Turki AlSabbar Ferny Angeles Paz July 13 th , 2016 SECURE Stock Presentation Consumer Discretionary Sector Student Investment Management

Transcript of Stock Presentation - Fisher College of Business · Stock Presentation Consumer ... Weakness in...

Presenters:

Turki AlSabbar

Ferny Angeles Paz

July 13th, 2016

SECURE

Stock PresentationConsumer Discretionary Sector

Student Investment Management

Agenda

Sector Overview (Recap)

Analysis of Stocks

Recommendation

Conclusion

Recommendation

Sector Overview (Recap)

Analysis of Stocks

Recommendation

Conclusion

4

Recommendation

Recommendation Stocks Analysis ConclusionSector Recap

Company Ticker Current Basis Proposed Basis Current Price Target Price Upside

(Downside)

Recommendation

Michael Kors KORS 469 bps 469 bps $51.91 $74.7 43.5% HOLD

Chipotle CMG 329 bps 0 bps $393.91 $234.7 40.4% SELL

Sector Overview (Recap)

Sector Overview (Recap)

Analysis of Stocks

Recommendation

Conclusion

6

Consumer Discretionary Sector

Recommendation Stocks Analysis ConclusionSector Recap

Automobiles & Components (7 members)

Consumer Durables & Apparel (20 members)

Consumer Services (12 members)

Media (15 members)

Retailing (33 members)

11.34%

21.97%

24.14%

42.47%

0.08%

Industries: 87 members and 5 industry groups

7

Consumer Discretionary Sector

Recommendation Stocks Analysis ConclusionSector Recap

Sector recommendation: BUY

Weights:

12.48% of S&P500 (as of July 11th)

12.82% of SIM (as of May 2016)

• Service Corp (SCI): 2%

• Chipotle (CMG): 3.29%

• Michael Kors (KORS): 4.69%

• Harley-Davidson (HOG): 2.84%

25.66%

15.59%

36.59%

22.16%

SIM: Consumer Discretionary

CMG

SCI

KORS

HOG

Analysis of Stocks

Sector Overview (Recap)

Analysis of Stocks

Recommendation

Conclusion

Michael Kors

10

Stock: Michael Kors

Recommendation Stocks Analysis ConclusionSector Recap

Michael Kors Michael Kors Holdings Ltd is a global

luxury designer, marketer, distributor and

retailer of women's apparel and accessories

and men's apparel. Founded in 1981, the

company has a presence in over 100

countries.

Retail, wholesale and licensing

Primary competitors: RL, KATE, COH

Market Data in U.S

Market Capitalization 9,088.9M

Shares Outstanding 176.4M

Dividend Yield DI

Dividend N.A

Beta 0.84

52 Week Price Range 34.83-59.49

Financial Data (TTM)

Revenue 4712.1M

Revenue Growth 7.8%

Gross Margin 59.4%

Operating Margin 18%

Earnings Per Share 4.48

Price to Earnings 11.45

11

Stock: Michael Kors – Business Segments

Recommendation Stocks Analysis ConclusionSector Recap

48%

48%

4%

2014

49%

47%

4%

2015

Retail Wholesale Licensing

51%45%

4%

2016

Retail: 50.8% of revenue

Largest wholesale customer: Macy’s contributed 12.7% of total revenue.

12

Stock: Michael Kors – Net Sales by segment and geography

Recommendation Stocks Analysis ConclusionSector Recap

Fiscal Years Ended

April 2, March 28, March 29,

2016 2015 2014

Retail net sales - The Americas $ 1,779.00 $ 1,656.10 $ 1,318.90

Retail net sales - Europe 509.60 412.10 235.60

Retail net sales - Asia 106.30 66.40 38.50

Wholesale net sales - The Americas 1,628.60 1,662.50 1,335.50

Wholesale net sales - Europe 406.40 401.10 242.00

Wholesale net sales - Asia 108.90 1.50 -

Licensing Revenue- The Americas 99.00 100.30 117.40

Licensing Revenue- Europe 74.30 71.50 22.90

Total revenue $ 4,712.10 $ 4,371.50 $ 3,310.80

• Slow retail in the Americas

• Retail and wholesale sales in Asia have

climbed up due to KORS’s acquisition of

Asiatic licenses

• Greater China License expected to contribute

$200M in retail sales next FY.

13

Stock: Michael Kors – Business Drivers

Recommendation Stocks Analysis ConclusionSector Recap

Retail sector weakness

Stock price has fallen by ~half over past 2 years.

Seasonality of market

93.27

40.06

49.48

0

20

40

60

80

100

120

140

160

180

200

9/30/2011 9/30/2012 9/30/2013 9/30/2014 9/30/2015

Stock Performance yearly

KORS COH LVMUY RL KATE

14

Stock: Michael Kors – Analysis

Recommendation Stocks Analysis ConclusionSector Recap

Revenue: Drop in retail consumption (Nordstrom).

Weakness in international tourism putting pressure on

margins.

New share repurchase program of 1Billion$:

established in last earnings report

Risks

• Economic slowdown in Europe and Asia

• Weakening pound

• E-commerce competition

• Brexit: prices for luxury items dropped 60% two weeks after

vs. two weeks before

Opportunities

• McLaren-Honda F1 partnership

• Acquisition of Great China and South Korea licensees

50.82%45.50%

3.68%

Revenue segmentation

Specialtyapparel stores

Apparel design

Apparel brandlicensing

15

Stock: Michael Kors – Operating Margin

Recommendation Stocks Analysis ConclusionSector Recap

15

20

25

30

35

40

45

50

55

Licensing Wholesale Retail

51.7

27.2

20.9

51.8

29.6

26.1

Operating Margin

FY 2016 FY 2015

Three segments have decreased their OM .

Retail went down 5.2%

16

Stock: Michael Kors – Gross Profit

Recommendation Stocks Analysis ConclusionSector Recap

0

500

1000

1500

2000

2500

3000

FY2016FY2015FY2014FY2013FY2012

Mill

ions

Gross Profit vs. Operating Income

Gross Profit Operating Income or Losses

Although gross profit increased, operating income

went down from FY 2015 to FY 2016

Company needs to trim costs or drive up revenue

performance.

Positive: Low cotton prices

17

Stock: Michael Kors – Key Ratios

Recommendation Stocks Analysis ConclusionSector Recap

KORS Valuation

Absolute Basis High Low Median Current

P/E 58.84

(03/2012)

9.11

(12/2015)

26.43 11.47

P/B 19.68

(03/2012)

3.64

(12/2015)

9.58 4.55

P/S 5.72 (09/2013) 1.66

(12/2015)

4.28 2.03

P/EBITDA 25.98

(03/2012)

5.62

(12/2015)

15.27 7.04

Competitor Multiples

Ticker P/E TTM P/S TTM P/B P/CF TTM EV/

EBITDA

TTM

Average 19.46 1.99 5.31 13.16 10.84

KORS 11.48 2.03 4.56 7.77 6.83

Peers

RL 16.50 1.13 2.17 8.32 7.15

KATE 26.86 2.13 10.06 19.80 18.36

COH 23.00 2.69 4.45 16.76 11.02

Valuation multiples lower than median by almost a half.

P/E ratio lower than industry’s average

18

Stock: Michael Kors – Recommendation

Recommendation Stocks Analysis ConclusionSector Recap

HOLD

Current Price: 51.91

Target Price: 74.47

Upside: 43.5%

Uncertainty about retail apparel stocks

Uncertainty coming from Brexit

Consumer spending going up but decreased sales at

department stores

Slower growth in foreign markets.

Chipotle Mexican Grill Inc.

20

Chipotle – Company Overview

Chipotle

Chipotle Mexican Grill, Inc. operates

Chipotle Mexican Grill restaurants. The

company was founded by Steve Ells, a

classically trained chef in 1993. Most of

these restaurants operate on fast-casual

Mexican food concept and are located in

the US. In order to diversify the risk, the

company has gradually been expanding

into international markets and other

food segments, See (Figure 1: Business

Segments).

Chipotle Restaurants

• US (1,971)• Canada (11) • England (7) • France (4) • Germany (1)

Mexican food: Burritos, tacos,

burrito bowls, salads

ShopHouse Southeast Asian Kitchen

13

Asian cuisine

Pizzeria Locale restaurants

(Indirectly held through investment in a separate

entity)

3

Fast casual pizza concept

# of Outlets

Sub-segment

# of Outlets

Sub-segment

# of Outlets

Sub-segment

Figure 1: Business Segments

Recommendation Stocks Analysis ConclusionSector Recap

21

Chipotle – Business Overview

Economic Drivers Drivers of Profitability

Consumer Spending

Consumer Confidence

Real GDP

US Unemployment Rate

Labor Costs

Food Commodity Costs

Recommendation Stocks Analysis ConclusionSector Recap

22

Chipotle – Stock Overview

Stock Overview

Ticker CMG

Sector Consumer Discretionary

Industry Restaurants

Current Price (USD) as of (07/01/2016) $393.91

Price Target (USD) $234.7

Total Projected Return $111,447

Dividend Yield (N/A)

Downside 40.4%

Recommendation: SELL

Market Capitalization (USD) $11.57 Bn.

Shares Outstanding 29.20 Mn.

52-week Price Range $384.77 - $758.61

Beta 0.33

Market Data

Revenue (USD) $4.50

Revenue Growth (Y/Y) 10%

Operating Income (USD) $764 Mn.

Financial Data (FY2015)

Recommendation Stocks Analysis ConclusionSector Recap

23

Chipotle – Stock Overview

0

100

200

300

400

500

600

700

800

CMG 12-Month Stock Price Chart Sector's Stock Price Performance Chart Compared to S&P 500

0

500

1000

1500

2000

2500

3000

3500

7/7/2011 7/7/2012 7/7/2013 7/7/2014 7/7/2015

CMG S&P 500

Recommendation Stocks Analysis ConclusionSector Recap

24

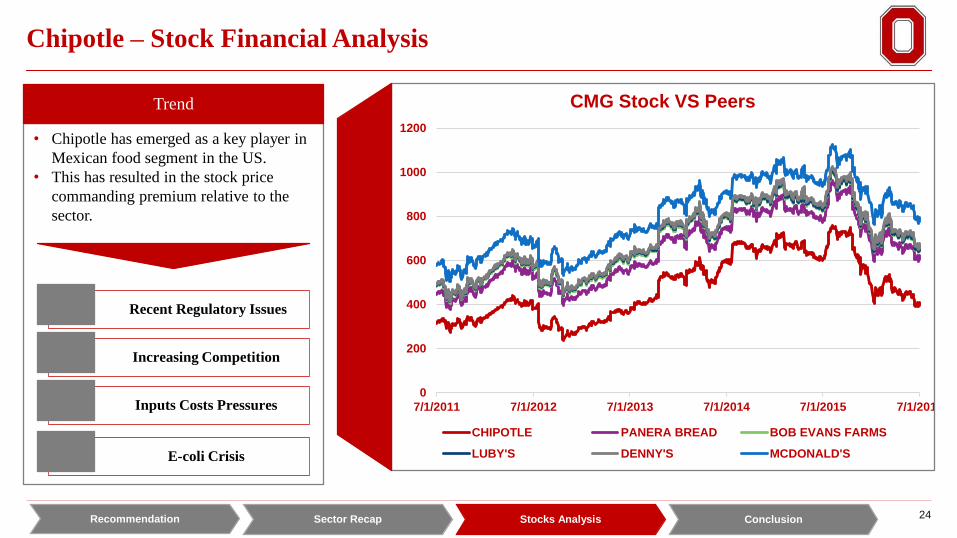

Chipotle – Stock Financial Analysis

• Chipotle has emerged as a key player in

Mexican food segment in the US.

• This has resulted in the stock price

commanding premium relative to the

sector.

Trend

Recent Regulatory Issues

Increasing Competition

Inputs Costs Pressures

E-coli Crisis

0

200

400

600

800

1000

1200

7/1/2011 7/1/2012 7/1/2013 7/1/2014 7/1/2015 7/1/2016

CMG Stock VS Peers

CHIPOTLE PANERA BREAD BOB EVANS FARMS

LUBY'S DENNY'S MCDONALD'S

Recommendation Stocks Analysis ConclusionSector Recap

25

Chipotle – Stock Financial Analysis

10Y CMG Absolute Valuation

High Low Median Current

P/E 64.79 21.66 36.86 25.92

P/S 5.17 1.52 3.43 2.75

P/B 10.75 3.20 7.42 5.73

P/CH 32.70 10.23 22.32 18.13

P/EBIT

DA30.42 10.57 18.23 13.86

10Y CMG Relative to S&P 500

High Low Median Current

P/E

4.12 1.54 2.74 1.95

P/S

4.32 1.19 2.51 1.52

P/B

5.78 1.23 3.15 2.67

P/CH

4.82 0.92 2.48 2.19

P/EBIT

DA5.05 1.33 2.70 1.71

9Y CMG vs Peers

P/E P/S P/B P/CHP/EBI

TDA

Average 23.53 1.48 3.06 11.55 9.92

CHIPOTLE 41.92 2.22 3.91 17.63 18.23

LUBY'S INC 13.71 0.78 1.64 9.92 7.52

MCDONALD'S

CORP18.71 2.53 3.45 12.60 9.38

BOB EVANS

FARMS23.49 0.81 1.85 8.85 7.76

PANERA BREAD 29.66 2.10 4.43 16.56 12.87

Recommendation Stocks Analysis ConclusionSector Recap

26

Chipotle – Stock Valuation

Weight

Implied value

by using the

model

DCF 60% 226.0

Valuation multiples based 40% 247.9

Final target price 234.7

Discount to the current market

price (%)40.4

Resolution of E-Coli and Norovirus incidents earlier than expected

Lower agriculture and crude oil prices

Successful international expansion earlier than anticipated

More successful and quicker scalability of diversification in other food segments

Quicker break-even period for newly opened stores

Risks

Recommendation Stocks Analysis ConclusionSector Recap

Conclusion

Sector Overview (Recap)

Analysis of Stocks

Recommendation

Conclusion

28

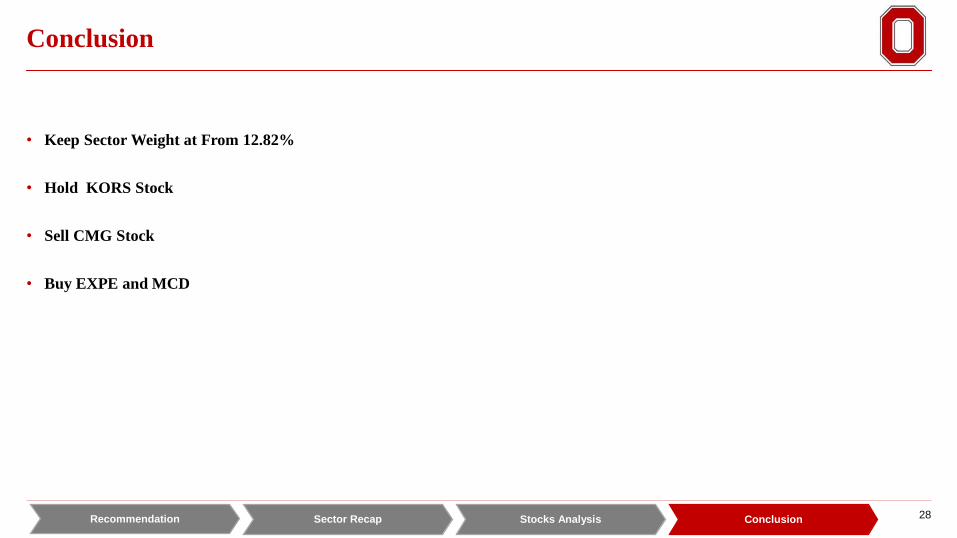

Conclusion

Recommendation Stocks Analysis ConclusionSector Recap

• Keep Sector Weight at From 12.82%

• Hold KORS Stock

• Sell CMG Stock

• Buy EXPE and MCD

29

Recommendation

Recommendation Stocks Analysis ConclusionSector Recap

Company Ticker Current Price Target PriceUpside

(Downside)Recommendation # of Shares

Expected Return

(USD)

Expedia Inc. EXPE $117.19 $182.24 55.5% BUY 1,755 $114,192

McDonalds MCD $126.06 $134.96 7.1% BUY 699 $6,220

Company Ticker Current Price # of Shares Proceeds

Chipotle CMG $419.68 700 $293,776

End of Presentation

Thank You For Listening

31

Appendix

Michael Kors (KORS)

Analyst: Ferny Angeles Paz Terminal Discount Rate = 10.0%

Terminal FCF Growth = 4.0%

(000s)

Year 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E 2027E

Revenue 4,901,904 5,196,018 5,507,779 5,673,013 5,843,203 6,018,499 6,199,054 6,416,021 6,672,662 6,939,568 7,217,151

% Grow th 6.0% 6.0% 3.0% 3.0% 3.0% 3.0% 3.5% 4.0% 4.0% 4.0%

Operating Income 1,313,710 1,395,131 1,478,839 1,701,904 1,752,961 1,805,550 1,859,716 1,924,806 2,001,799 2,081,871 2,165,145

Operating Margin 26.8% 26.9% 26.9% 30.0% 30.0% 30.0% 30.0% 30.0% 30.0% 30.0% 30.0%

Interest Income 1,961 2,078 2,203 2,269 2,337 2,407 2,480 2,566 2,669 2,776 2,887

Interest % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Taxes 458,769 487,205 516,437 594,872 612,718 631,100 650,033 672,784 699,695 727,683 756,790

Tax Rate 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%

Net Income 853,400 906,209 960,497 1,104,762 1,137,905 1,172,043 1,207,204 1,249,456 1,299,434 1,351,412 1,405,468

% Grow th 6.2% 6.0% 15.0% 3.0% 3.0% 3.0% 3.5% 4.0% 4.0% 4.0%

Add Depreciation/Amort 196,076 207,841 220,311 170,190 175,296 180,555 185,972 192,481 200,180 208,187 216,515

% of Sales 4.0% 4.0% 4.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

Plus/(minus) Changes WC (67,377) (36,009) (43,543) (44,849) (46,194) (47,580) (49,008) (50,723) (52,752) (54,862) (57,056)

% of Sales -1.375% -0.7% -0.8% -0.8% -0.8% -0.8% -0.8% -0.8% -0.8% -0.8% -0.8%

Subtract Cap Ex 392,152 415,681 440,622 425,476 409,024 391,202 371,943 352,881 333,633 277,583 288,686

Capex % of sales 8.0% 8.0% 8.0% 7.500% 7.000% 6.500% 6.000% 5.500% 5.000% 4.000% 4.000%

Free Cash Flow 589,947 662,359 696,643 804,628 857,983 913,815 972,225 1,038,333 1,113,229 1,227,154 1,276,240

% Grow th 12.3% 5.2% 15.5% 6.6% 6.5% 6.4% 6.8% 7.2% 10.2% 4.0%

NPV of Cash Flows 5,549,265 39%

NPV of terminal value 8,528,794 61% Terminal Value 22,121,496

Projected Equity Value 14,078,059 100%

Free Cash Flow Yield 6.01% Free Cash Yield 5.77%

Current P/E 11.5 10.8 10.2 Terminal P/E 15.7

Projected P/E 16.5 15.5 14.7

Current EV/EBITDA 6.0 5.7 5.4 Terminal EV/EBITDA 9.0

Projected EV/EBITDA 8.9 8.3 7.9

Shares Outstanding 189,054

Current Price 51.91$ premarket after preannouncement

Implied equity value/share 74.47$

Upside/(Downside) to DCF 43.5%

Debt 2,000

Cash 702,000

Cash/share 3.71

32

Appendix

Chipotle Mexican Grill, Inc. (CMG)

Analyst: Turki AlSabbar Terminal Discount Rate = 10.00%

6/7/2016 Terminal FCF Growth = 4.0%

(000s)

Year 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E

Revenue 4,276,162 4,447,208 4,625,097 4,810,101 5,002,505 5,202,605 5,410,709 5,681,244 5,965,307 6,263,572 6,576,751 % Growth 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 5.0% 5.0% 5.0% 5.0%

Operating Income 218,084 582,584 883,393 769,616 800,401 832,417 865,713 908,999 954,449 1,002,172 1,052,280 Operating Margin 5.1% 13.1% 19.1% 16.0% 16.0% 16.0% 16.0% 16.0% 16.0% 16.0% 16.0%

Interest Income 4,276 4,447 4,625 4,810 5,003 5,203 5,411 5,681 5,965 6,264 6,577 Interest % of Sales 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%

Taxes 82,316.12 222,582.78 338,325.82 294,450.3 306,228.3 318,477.4 331,216.5 347,777.4 365,166.2 383,424.6 402,595.8 Tax Rate 38.5% 38.5% 38.5% 38.5% 38.5% 38.5% 38.5% 38.5% 38.5% 38.5% 38.5%

Net Income 131,492 355,554 540,443 470,356 489,170 508,737 529,086 555,540 583,318 612,483 643,108 % Growth 170.4% 52.0% -13.0% 4.0% 4.0% 4.0% 5.0% 5.0% 5.0% 5.0%

Add Depreciation/Amort 128,285 133,416 138,753 144,303 150,075 156,078 162,321 170,437 178,959 187,907 197,303 % of Sales 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

Plus/(minus) Changes WC 1,239 1,339 1,385 1,441 1,499 1,558 1,621 1,702 1,787 1,876 1,970 % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Subtract Cap Ex 259,974 262,574 265,199 275,807 286,840 298,313 216,428 227,250 238,612 250,543 263,070 Capex % of sales 6.1% 5.9% 5.7% 5.7% 5.7% 5.7% 4.0% 4.0% 4.0% 4.0% 4.0%

Free Cash Flow 1,041.63 227,735.56 415,381.43 340,292.12 353,903.80 368,059.96 476,599.88 500,429.87 525,451.36 551,723.93 579,310.13 % Growth 21763.4% 82.4% -18.1% 4.0% 4.0% 29.5% 5.0% 5.0% 5.0% 5.0%

NPV of Cash Flows 2,504,535 39%

NPV of terminal value 3,871,385 61% Terminal Value 10,041,376

Projected Equity Value 6,375,920 100%

Free Cash Flow Yield 0.01% Free Cash Yield 5.77%

Current P/E 87.5 32.3 21.3 Terminal P/E 15.6

Projected P/E 48.5 17.9 11.8

Current EV/EBITDA 31.3 15.1 10.6 Terminal EV/EBITDA 7.5

Projected EV/EBITDA 16.5 8.0 5.6

Shares Outstanding 29,200

Current Price $ 393.91

Implied equity value/share $ 218.35

Upside/(Downside) to DCF -44.6%

Debt -

Cash 667,470

Cash/share 22.86

As on Dec 31, 2015

Cash 248005

Investments 415199

Total 663204

Cash for regular operations and liquidity 7.619520548

Implied value from DCF 226.0Discount

Upside/(Downside) to DCF (after adding cash) 0.573666462 0.426333538

33

Appendix

Expedia Inc. (EXPE)

Analyst: Turki AlSabbar Terminal Discount Rate = 12.00%

7/20/2016 Terminal FCF Growth = 0.25%

(000s)

Year 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E

Revenue 8,674,012 10,929,255 12,787,229 14,961,058 17,504,437 20,480,192 23,961,824 27,316,480 31,140,787 35,500,497 40,470,566

% Growth 26.0% 17.0% 17.0% 17.0% 17.0% 17.0% 14.0% 14.0% 14.0% 14.0%

Operating Income 520,441 1,704,964 3,529,275 4,039,486 4,726,198 5,529,652 6,469,693 5,463,296 6,228,157 7,100,099 8,094,113

Operating Margin 6.0% 15.6% 27.6% 27.0% 27.0% 27.0% 27.0% 20.0% 20.0% 20.0% 20.0%

Interest Income 346,960 218,585 127,872 149,611 175,044 204,802 239,618 273,165 311,408 355,005 404,706

Interest % of Sales 4.0% 2.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

Taxes 182,153.25 384,708.78 731,428.48 777,975.0 910,230.7 1,064,970.0 1,246,014.9 1,038,026.2 1,183,349.9 1,349,018.9 1,537,881.5

Tax Rate 21.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0% 20.0%

Net Income 1,049,554 2,308,258 4,388,576 3,111,900 3,640,923 4,259,880 4,984,059 4,152,105 4,733,400 5,396,076 6,151,526

% Growth 119.9% 90.1% -29.1% 17.0% 17.0% 17.0% -16.7% 14.0% 14.0% 14.0%

Add Depreciation/Amort 86,740 76,505 51,149 59,844 70,018 81,921 95,847 109,266 124,563 142,002 161,882

% of Sales 1.0% 0.7% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4%

Plus/(minus) Changes WC 47,640 202,972 167,218 195,645 228,904 267,818 313,347 357,216 407,226 464,237 529,230

% of Sales 0.5% 1.9% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3% 1.3%

Subtract Cap Ex 794,911 802,861 810,889 948,740 1,110,026 1,298,731 958,473 1,092,659 1,245,631 1,420,020 1,618,823

Capex % of sales 9.2% 7.3% 6.3% 6.3% 6.3% 6.3% 4.0% 4.0% 4.0% 4.0% 4.0%

Free Cash Flow 389,023.26 1,784,873.85 3,796,053.26 2,418,648.51 2,829,818.75 3,310,887.94 4,434,780.69 3,525,927.13 4,019,556.93 4,582,294.90 5,223,816.19

% Growth 358.8% 112.7% -36.3% 17.0% 17.0% 33.9% -20.5% 14.0% 14.0% 14.0%

NPV of Cash Flows 18,817,992 57%

NPV of terminal value 14,350,075 43% Terminal Value 44,569,155

Projected Equity Value 33,168,067 100%

Free Cash Flow Yield 1.82% Free Cash Yield 11.72%

Current P/E 20.3 9.2 4.9 Terminal P/E 7.2

Projected P/E 31.6 14.4 7.6

Current EV/EBITDA 34.3 11.7 5.8 Terminal EV/EBITDA 5.3

Projected EV/EBITDA 53.8 18.3 9.1

Shares Outstanding 182,000

Current Price $ 117.19

Implied equity value/share $ 182.24

Upside/(Downside) to DCF 55.5%

Debt 402,500

Cash 900,281

Cash/share 4.95

34

Appendix

McDonald's (MCD)

Analyst: Turki AlSabbar Terminal Discount Rate = 9.00%

7/20/2016 Terminal FCF Growth = 6.0%

$ In millions

Year 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E

Revenue 26,430 28,015 30,257 32,677 35,291 38,114 41,164 37,459 34,088 31,020 28,228

% Growth 6.0% 8.0% 8.0% 8.0% 8.0% 8.0% -9.0% -9.0% -9.0% -9.0%

Operating Income 11,867 12,579 13,585 8,823 9,529 10,291 11,114 10,114 9,204 8,375 7,622

Operating Margin 44.9% 44.9% 44.9% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0%

Interest Income 550 530 510 817 882 953 1,029 936 852 775 706

Interest % of Sales 2.1% 1.9% 1.7% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5%

Taxes (3,507.11) (3,734.13) (4,052.34) 2,481.8 2,680.4 2,894.8 3,126.4 2,845.0 2,589.0 2,355.9 2,143.9

Tax Rate 31.0% 31.0% 31.0% 31.0% 31.0% 31.0% 31.0% 31.0% 31.0% 31.0% 31.0%

Net Income 7,806 8,311 9,020 5,524 5,966 6,443 6,959 6,332 5,763 5,244 4,772

% Growth 6.5% 8.5% -38.8% 8.0% 8.0% 8.0% -9.0% -9.0% -9.0% -9.0%

Add Depreciation/Amort 1,538 1,520 1,500 1,620 1,750 1,890 2,041 1,857 1,690 1,538 1,399

% of Sales 5.8% 5.4% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

Plus/(minus) Changes WC (64) (71) (78) (85) (91) (99) (107) (97) (88) (80) (73)

% of Sales -0.2% -0.3% -0.3% -0.3% -0.3% -0.3% -0.3% -0.3% -0.3% -0.3% -0.3%

Subtract Cap Ex 1,542 1,311 1,114 1,203 1,299 1,403 1,647 1,498 1,364 1,241 1,129

Capex % of sales 5.8% 4.7% 3.7% 3.7% 3.7% 3.7% 4.0% 4.0% 4.0% 4.0% 4.0%

Free Cash Flow 7,737.84 8,449.59 9,327.29 5,856.21 6,324.71 6,830.69 7,246.21 6,594.05 6,000.59 5,460.54 4,969.09

% Growth 9.2% 10.4% -37.2% 8.0% 8.0% 6.1% -9.0% -9.0% -9.0% -9.0%

NPV of Cash Flows 44,597 38%

NPV of terminal value 74,165 62% Terminal Value 175,574

Projected Equity Value 118,762 100%

Free Cash Flow Yield 6.98% Free Cash Yield 2.83%

Current P/E 14.2 13.3 12.3 Terminal P/E 36.8

Projected P/E 15.2 14.3 13.2

Current EV/EBITDA 9.5 9.0 8.4 Terminal EV/EBITDA 21.3

Projected EV/EBITDA 10.1 9.6 9.0

Shares Outstanding 880

Current Price $ 126.06

Implied equity value/share $ 134.96

Upside/(Downside) to DCF 7.1%

Debt 24,122

Cash 7,686

Cash/share 8.73