Stock Pitch - Duke University Investment Club Pitch Nikolai Doytchinov, ... Hedging, refinery...

18

Stock Pitch Nikolai Doytchinov, Jonathan Im, Cheng Ma, Yang Wu

Transcript of Stock Pitch - Duke University Investment Club Pitch Nikolai Doytchinov, ... Hedging, refinery...

Stock Pitch

Nikolai Doytchinov, Jonathan Im, Cheng Ma, Yang Wu

2

Table of Contents

I. Investment Thesis

II. Industry Outlook

III. Company Analysis

IV. Valuation

I. Investment Thesis

4

Delta (NYSE: DAL)

Recommendation: Buy Current Price: $36.95 Price Target: $54.76 (48% upside)

Delta’s strong management team and network strategy have contributed to sustained earnings growth and will continue

to do so, making it a compelling investment based on undervalued market pricing.

Network strategy increases presence in major airports (NYC, London Heathrow, Seattle)

Recovering U.S. economy will increase both corporate and leisure demand for air travel

Effective nonfuel cost reductions are improving operating margins

Oil prices forecast to remain flat or decline over the next several years

Increased management emphasis on returning cash to shareholders

CATALYSTS

RISKS

Fluctuating oil price translates to uncertainty in a major cost driver

High fixed costs make profitability very sensitive to demand

Public concern about Ebola virus may reduce demand

Reduced services in Venezuela due to devalued currency

II. Industry Outlook

6

Industry Outlook

Source: IBISworld Industrial Report

IMF Crude Oil Price Estimates U.S. Per Capita Disposable Income

-1.5

-0.5

0.5

1.5

2.5

3.5

35

37

39

41

43

45

08 10 12 14 16 18 20

Tho

usa

nd

s

$ % Change

Growth Rate in Passenger Air Traffic Airlines Industry Revenue

2009 $

III. Company Analysis

8

Company Overview

Source: ir.delta.com

Delta Air Lines an American airline that provides services globally

Founded in 1924

Based in Atlanta, GA

Majority of revenue from domestic and Atlantic region

Strong management team

CEO (Richard Anderson) named one of the world’s best CEOs by Barron’s in March 2014

President (Ed Bastian) is also on the boards of Aeromexico and GOL and plays pivotal role in joint ventures

BUSINESS OVERVIEW

COMPETITIVE ADVANTAGES

Leader in industry

Higher pre-tax income in 3Q 2013 than all competitors

Likely to remain a big player since barrier to entry is strong

Strong cash flow

Delta is committed to reducing its debt and as a result only plans on spending $2.3b on CapEx compared to competitor American Airlines spending $5b

Owns refinery

Owns private refinery to hedge against fluctuations in oil prices; expected to save company $300m annually

9

Catalysts

Source: ir.delta.com

Network Strategy increases presence in major airports

Bought 49% stake in Virgin Atlantic to expand presence in London

Joint ventures to increase presence in NYC

International gateway from Seattle to Asia

Corporate spending on air travel expected to increase by 7% in 2014; companies like Delta according to survey

Recovering U.S. economy will increase demand for air travel

Effective cost reductions

10

Delta: Flying contrary to the pack

Old Planes?

Delta’s Strategic View

Costs of acquisition significantly lower

49 used MD-90s from China Southern Airlines

88 Boeing 717s leased from Southwest

Purchase of 100 new 737-900s, instead of 737 MAX

Purchase of 15 A- 321s, instead of A-320neo

Highest average age of 16.6 years

Other airlines are or are becoming younger

Fuel costs are limiting factor for old jet utility

Maintenance costs could potentially skyrocket

Subsidiary maintenance company is a mitigant

10 different models and 725 planes in their fleet

Delta has pursued strategies counter to prevailing industry practice

Acquisition of a refinery

Subsidiary maintenance company

Opportunistic acquisition of older planes

80% ownership of planes compared to on average 60%

11

New Jets and their Benefits

12

Risks & Mitigation

Venezuela and Latin America in general only affect a small portion of the total revenue

Unlikely given severe negative implications for Russian economy; few Delta flights use Russian airspace

Empirically, no impact on bookings; Ebola pathogen not transmitted as airborne particle

Hedging, refinery ownership, ability to pass costs to consumers, and secular trend of declining oil prices

Majority of business is U.S. domestic

Reduced services in Venezuela and cash trapped in country due to devalued currency

Russia threatens to close its airspace to western airlines

Ebola scare may reduce air traffic demand

Volatile fuel costs threaten margins

Weak economic recovery outside U.S.

Risks Mitigation

IV. Valuation

14

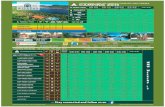

Comparable Companies Analysis

Source: SEC Filings and Bloomberg

Company Share Price

(US$) Market Value

(US$mm) Enterprise

Value (US$mm)

Enterprise value as a multiple of Price / Earnings (x)

Revenue (x) EBITDA (x)

LTM 2014 2015E LTM 2014 2015E LTM 2014 2015E

AMERICAN AIRLINES GROUP INC 33.9 24,764 32,448 1.09 0.79 0.75 7.39 5.57 4.60 20.51 6.74 5.25

UNITED CONTINENTAL HOLDINGS 46.1 16,986 23,510 0.57 0.63 0.61 6.86 5.93 4.88 17.04 10.48 8.09

SOUTHWEST AIRLINES CO 32.5 22,301 21,065 0.95 1.17 1.10 8.15 7.08 6.28 23.32 18.34 15.41

JETBLUE AIRWAYS CORP 10.6 2,990 4,579 0.84 0.82 0.75 6.28 5.82 4.86 19.19 15.69 12.12

ALASKA AIR GROUP INC 42.9 5,765 5,114 1.09 0.99 0.93 4.14 4.61 4.30 12.89 11.55 10.62

Mean 33 14,561 17,343 0.91 0.88 0.83 6.56 5.80 4.99 18.59 12.56 10.30

Median 34 16,986 21,065 0.95 0.82 0.75 6.86 5.82 4.86 19.19 11.55 10.62

High 46 24,764 32,448 1.09 1.17 1.10 8.15 7.08 6.28 23.32 18.34 15.41

Low 11 2,990 4,579 0.57 0.63 0.61 4.14 4.61 4.30 12.89 6.74 5.25

<--------------- 2015E EBITDA Multiples range ------------>

4.0 4.5 5.0 5.5 6.0

Implied EV: 31,379.79 35,316.94 39,254.09 43,191.24 47,128.39

Implied MCAP: 37,620.79 41,557.94 45,495.09 49,432.24 53,369.39

Implied Share Price: 44.63 49.30 53.97 58.64 63.31

<--------------- 2015E Revenue Multiples range ------------>

0.6 0.7 0.8 0.9 1.0

Implied EV: 26,532.07 30,754.87 34,977.67 39,200.47 43,423.27

Implied MCAP: 32,773.07 36,995.87 41,218.67 45,441.47 49,664.27

Implied Share Price: 38.88 43.89 48.90 53.90 58.91

<--------- P/E Multiples range --------->

EPS 8.5 9.5 10.5 11.5 12.5 2.88 24.48 27.4 30.2 33.1 36.0 3.38 28.73 32.1 35.5 38.9 42.3 3.88 32.98 36.9 40.7 44.6 48.5 4.38 37.23 41.6 46.0 50.4 54.8 4.88 41.48 46.4 51.2 56.1 61.0

- Exchange Rates as of 10/01/14

- Share Prices as of 10/01/14

- EV Adjusted for Minority Interests based on Market Value

- EV Adjusted for Equity Value in Associates based on market Value

15

Financial Performance: Historical and Projected

Sources: Bloomberg; NASDAQ; authors’ projections

Revenue, $mil EBITDA Margin

EBITDA, $mil Share Price

0

10000

20000

30000

40000

50000

Base

Bear

Bull

0%

5%

10%

15%

20%

25%

Base

Bear

Bull

0

2000

4000

6000

8000

10000

12000

Base

Bear

Bull

$-

$10

$20

$30

$40

$50

$60

$70

10/3/2012 10/3/2013 10/3/2014 10/3/2015

Base

Bear

Bull

16

Discounted Cash Flow Analysis (Base Case)

Discounted Cash Flow (Base Case), cont.

17

Valuation Summary In Millions, except per share

Present Value of Enterprise $38,579.4

Less: Total Debt 10,322.0

Less: Minority Interest 0.0

Less: Preferred Equity 0.0

Plus: Cash 4,081.0

Equity Value $52,982.4

Shares Outstanding 852.0

Equity Value Per Share $62.19

Sensitivity Analysis

Exit Discount Rate

Multiple 8.00% 9.00% 10.00% 11.00% 12.00%

2.5x 51.79 50.59 49.44 48.35 47.30

3.5x 58.78 57.26 55.81 54.44 53.13

4.5x 65.76 63.93 62.19 60.53 58.95

5.5x 72.75 70.60 68.56 66.62 64.78

6.5x 79.74 77.27 74.93 72.71 70.60

18

Share Price Calculation