Steve McCann Group Chief Executive Officer & Managing Director Strategy and Business Overview.

25

Steve McCann Group Chief Executive Officer & Managing Director Strategy and Business Overview

-

date post

19-Dec-2015 -

Category

Documents

-

view

218 -

download

2

Transcript of Steve McCann Group Chief Executive Officer & Managing Director Strategy and Business Overview.

Steve McCannGroup Chief Executive Officer & Managing Director

Strategy and Business Overview

Agenda

1. Update on safety2. External business environment3. Key priorities for the Group4. Pipeline of opportunities5. Strategy update6. Continued focus on key trends7. Progress on strategy to date8. Key strategic deliverables 20119. Operational update Asia10. Operational update Europe

Good progress on safety

3

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY110123456789

10

Total Fatalities per Region 1

AUSTRALIA ASIA AMERICAS EMEA

As at May

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY110

100200300400500600700800

Total Lost Time Injuries per Region 1

AUSTRALIA ASIA AMERICAS EMEA

As at May

1. Excludes infrastructure business (Valemus)Gold Coast University Hospital, Queensland

External environment favourable

4

Region Outlook Opportunity/ Impact for Lend Lease

Australia

Favourable economic conditions present attractive opportunities across most sectors, particularly infrastructure

Short term impact from weak consumer sentiment Concerns of two speed economy and potential impact from interest rate rises Focus on delivery of secured pipeline of opportunities through existing

platform and integration of Valemus

Asia Strong fundamentals across most markets Focused on delivery of retail projects in Singapore Project management & construction – develop market leading positions in

pharmaceutical and life sciences

Americas Signs of recovery across key sectors Opportunity to leverage into market recovery and establish positions in new

sectors eg. healthcare development

Europe Early stages of recovery in residential and construction Focus on delivery of major projects and position project management &

construction business into market recovery

Key priorities for the Group

Integrate Valemus infrastructure business and deliver on earnings accretion Integration of business on track Strong infrastructure backlog

driven by Abigroup

Progress major projects

• Focus on portfolio management

• Position offshore businesses for market recovery

5

Mangoola Coal Rail Bottom Loop, NSW

Significant pipeline of opportunities

Dec 2010

Funds under management (A$b) 10.7

End development value of urban regeneration projects (A$b) 25.0

Construction backlog revenue (A$b) (including Valemus) 11.9

Retail assets under management (A$b) 9.4

Backlog of residential units 89,216

6

Strategy update

Our strategic direction

Our Strategic Direction:

To be the Leading International Property and Infrastructure Group

Be in the top 3 industry leaders within

our chosen market segments and sectors

Leading

Focus on 4 core regions with defined

geographies

International

Property and Infrastructure are our core sectors. We will participate in defined sub-sectors where we have core capabilities

Sectors Segments

Development Construction Investment

Management Services Ownership

8

Our segment position

9

Focused predominately on co-investments

Use capital to support fund growth

A leading development management, design & delivery capabilities

Development

Strong capabilities in project management, design and construction and new acquired capability in engineering and construction

Construction

A leading investment management platform

Strong access to capital

Investment Management

Property, asset and facilities management expertise

Services Ownership

Target risk adjusted capital

35-45%

Target risk adjusted capital

30-40%

Target risk adjusted capital

5-15%

Target risk adjusted capital

< 5%

Target risk adjusted capital

10-20%

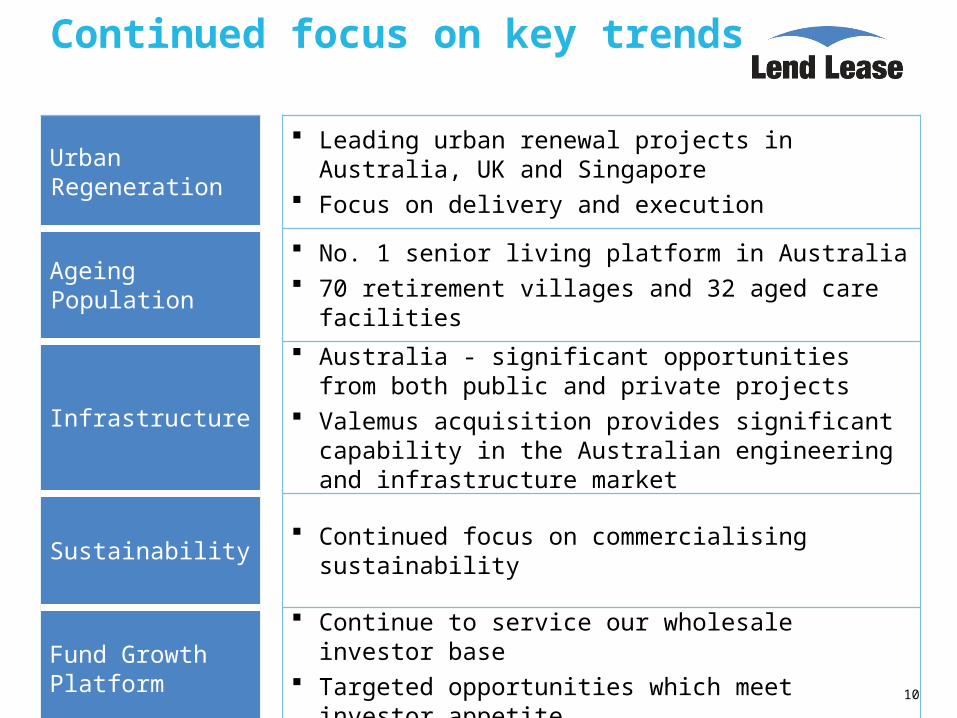

Continued focus on key trends

Urban Regeneration Leading urban renewal projects in Australia, UK and Singapore Focus on delivery and execution

Ageing Population No. 1 senior living platform in Australia 70 retirement villages and 32 aged care facilities

Infrastructure Australia - significant opportunities from both public and private

projects Valemus acquisition provides significant capability in the Australian

engineering and infrastructure market

Sustainability Continued focus on commercialising sustainability

Fund Growth Platform Continue to service our wholesale investor base Targeted opportunities which meet investor appetite

10

Our strategic pathway

RESTORE Right Structure

Right structure Cost out Drive efficiency Capital management

Reshape portfolio

Growth platforms

Operational excellence

Invest in people

World class property and infrastructure solutions company

Strong integrated offering

Trusted investment manager

RESTOREA Focused Core Business

BUILDDisciplined Expansion

LEADOutperformance

11

Continue to focus on business transformation Capital management

Divestment of non core assets

Valemus integration Talent management

Portfolio of successful projects

Best in class execution

Key strategic deliverables – 12 to 24 months

Reshape portfolio

Growth platforms

Operational excellence

Invest in people

BUILD

12

Major Development Projects

Successful delivery and execution of secured projects

Infrastructure Successful integration of the business Establish appropriate risk framework Extract synergies

Business Transformation

Drive business performance efficiency Deliver savings

Portfolio Reallocation Realise capital of A$1–2b from completed assets

UK and US market recovery

Position to outperform in recovering markets Realise intrinsic development value in UK projects

and focus on healthcare opportunities in the US

Operational update

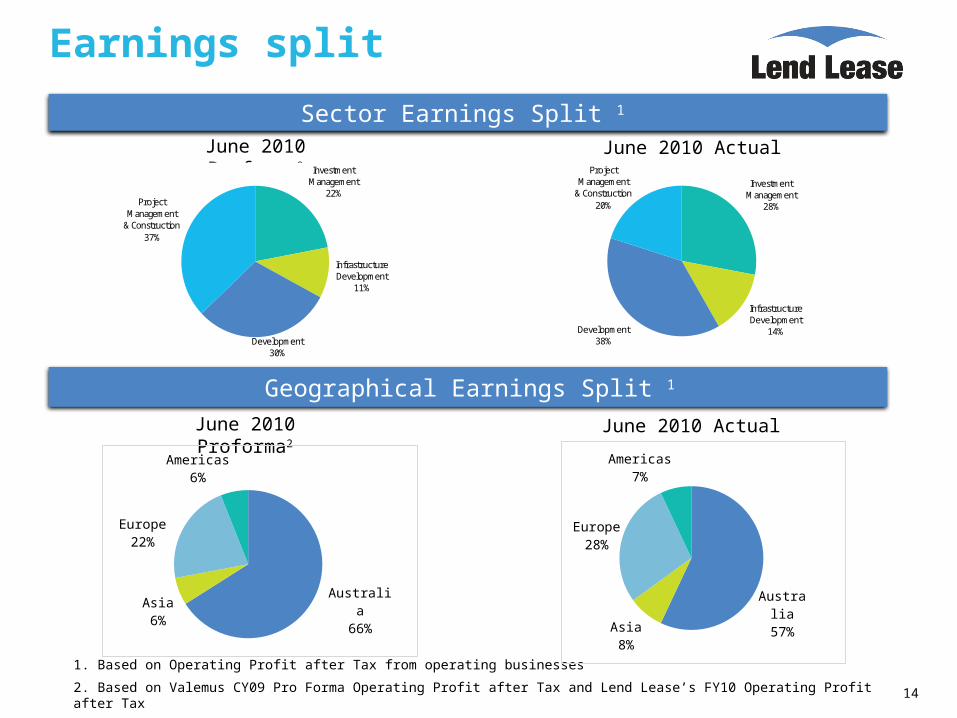

Sector Earnings Split 1 June 2010 Actual

Geographical Earnings Split 1

Earnings split

June 2010 Actual

1. Based on Operating Profit after Tax from operating businesses

2. Based on Valemus CY09 Pro Forma Operating Profit after Tax and Lend Lease’s FY10 Operating Profit after Tax

June 2010 Proforma2

June 2010 Proforma2

Investment Management

22%

Infrastructure Development

11%

Development30%

Project Management

& Construction37%

Investment Management

28%

Infrastructure Development

14%Development38%

Project Management

& Construction20%

14

Australia66%Asia

6%

Europe22%

Americas6%

Australia57%Asia

8%

Europe28%

Americas7%

Asia business update

15

Key MetricsDec 2010

Dec 2009

Operating Profit after tax (A$m) 15.8 21.5

Construction new work secured (A$m) 412.0 156.8

Dec 2010

June 2010

Construction backlog revenue (A$m) 546.1 289.9

Funds under management (A$b) 2.0 1.6

Retail assets under management (A$b) 1.8 1.8

Investment Management

34%

Project Manage-ment &

Construction66%

Opportunities

Additional mixed use development sites coming to market in Singapore

Global client strategy in pharma and life sciences sectors

Opportunities in China and Japan Focus on global capital relationships

Outlook

Signed government tenancy for Jurong Gateway commercial and progressing retail leasing

Increasing competition for retail spend in Singapore

Strong investor demand for regional assets

Operating profit after tax for the six month period ended 31 Dec 2010

Europe business overview

Key MetricsDec 2010

Dec 2009

Profit after tax (million) 94.6 64.0

Construction new work secured (m) 764.5 540.0

Dec 2010

June 2010

Construction backlog revenue (A$m) 1,381.7 1,473.9

Number of residential units 15,196 12,425

PPP equity invested(A$m) 78.3 147.3

Infrastructure Development

62%

Investment Management

29%

Project Manage-ment &

Construction5%

Development5%

16

Opportunities

Focus on large projects (Greenwich Peninsula, Elephant & Castle, Stratford International Quarter)

Rationalise CEMEA operations Appointment of new Head of project

management & construction - Michael Dyke Athletes’ Village project on track Infrastructure Fund has undrawn capacity Focus on capital recycling opportunities

Outlook Residential in early stages of recovery –

fits well with timing of major projects Construction market conditions remain

subdued but activity levels improving

Operating profit after tax for the six month period ended 31 Dec 2010

Development - Communities

17

Operational Update

NSW/ ACT remain strong, Victoria is solid while South Australia and South East Queensland are subdued

Flood impacting sentiment in Queensland Targeting zoning on current unzoned project

backlog in FY2012

Opportunities

New projects secured – Alkimos, Toolern, Werribee, Fernbrooke

Zoning progressed – Calderwood, Yarrabilba Continue to target affordable projects and

replenish pipeline Maintain balanced portfolio

Outlook

Long term fundamentals of residential market remain solid, short term impacted by market uncertainty and consumer sentiment

Going into FY2012 – strong carry forward of contracts / commence trading on a number of new projects Varsity Lakes, Gold Coast, QLD

Key MetricsDec

2010 June 2010

Number of zoned residential land lots 38,170 31,960

Number of unzoned residential land lots 22,335 27,080

Total backlog lots 60,505 59,040

Overview of communities market

18

Quality of enquiry at Lend Lease projects improving, however conversion time has increased on back of decline in sentiment

Affordability pressures continue to be driven by interest rate rises and higher living costs

Tightening bank lending criteria resulting in lower Loan to Value Ratios

Lend Lease product mix focused on affordable end of the market

Pricing and margins across Lend Lease portfolio remain resilient

Long term fundamentals are positive with strong underlying demand and ongoing stock shortfall and supported by solid employment outlook

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Stock Deficiency

Stock Deficiency Supply Demand

60

70

80

90

100

110

120

130

Apr-82 Mar-85 Feb-88 Jan-91 Nov-93 Oct-96 Sep-99 Aug-02 Jul-05 Jun-08

Inde

x (1

00=n

etur

al)

Consumer Sentiment IndexMonthly observations ending April 2011

CSI LR Average (101.4)

Source: Westpac-Melbourne Institute, RBA and Lend Lease Research

Source: BIS Shrapnel

Communities portfolio strategy update

19

Capital model to match size and nature of project – land management, joint ventures or direct ownership

New project acquisitions focused on replenishing existing portfolio in affordable growth corridors

Recent entry into WA market

Focus on product innovation and builder partnerships to deliver sales volume

Strong reputation in place, creation and delivery of key infrastructure to drive value and competitive advantage

Flexible business model and diverse geographic spread of projects

Mawson Lakes, SA

Lakeside Pakenham, VIC

Senior Living

20

Operational Update

FY2011 reflects first full year of 100% ownership of Primelife

Aged Care – has increased EBITDA per bed by >35% since acquisition

Opportunities

Recycle capital and introduce capital partners Increase development pipeline Standardise retirement contracts across the

portfolio for simplification and efficiency benefits

Outlook

Long term dynamics of senior living sector remain positive – supported by an ageing population, undersupply of stock and government focus on senior housing

Penetration in Australia remains low relative to overseas markets

Key MetricsDec 2010

June 2010

Number of retirement villages 70 70

Number of retirement units 12,416 12,357

Number of aged care facilities 32 32

Number of aged care beds 2,372 2,370

Aged care occupancy (%) 94.4 94.5

Development pipeline – number of retirement units 1,255 1,310

Woodlands Park, Berwick VIC

Investment Management

MidCity Centre, Sydney, NSW

21

Operational Update

FUM growth of over 15% per annum over last 5 years – strong growth expected to continue

Continued strong performance across key funds Integration of ING Retail Fund assets complete

Opportunities

Internal development pipeline to support strong growth outlook

Focus on capital recycling opportunities across the Group

Diversify investor base and scale up retail platform

Grow separate mandates business

Outlook

Investors seeking alignment with asset creators and best in breed managers

Lend Lease seen as attractive partner with strong track record, governance framework and end to end property skills

Retail sales environment remains flat

Key MetricsDec 2010

Dec 2009

Operating profit after Tax (A$m) 17.2 11.9

Dec 2010

A$

June 2010

A$Funds under management (A$b) 7.6 7.1

Market value of investments (A$b) 0.3 0.3

Retails assets under management 15 15

Key priorities

Grow construction backlog Focus on health pipeline and convert internal

opportunities Leverage multi-sites/ capital services platform

Deliver key development projects Achieve key planning outcomes, secure

tenants and capital partners Replenish communities backlog in key

affordable markets Continue to drive operational excellence

across senior living platform Simplify operating model in preparation for

capital recycling Continue to grow funds under management

Strong performance in existing funds is key

22

Steve McCannGroup Chief Executive Officer & Managing Director

Closing Comments

Key priorities for the Group

Integrate Valemus infrastructure business and deliver on earnings accretion

Focus on execution and delivery of major projects

Ongoing portfolio management

• Position offshore businesses for market recovery

24

Darling Quarter, Sydney, NSW

Positive outlook

Significant backlog, development pipeline and access to capital Continued deal momentum Capital invested is supported by third party equity Focus on capital recycling Emphasis on quality and consistency of execution

Strong long term outlook with positive EPS trend Expect accretion from Valemus deal Strong 1st half result positions the Group well for the full year Key projects expected to begin to deliver returns from 2nd half of financial year 2012

25