Steen Jakobsen, Chief Economist Currency Wars – the new extend -and- pretend ? 2013

30

Steen Jakobsen, Chief Economist Currency Wars – the new extend-and- pretend? 2013

-

Upload

bert-harris -

Category

Documents

-

view

18 -

download

1

description

Steen Jakobsen, Chief Economist Currency Wars – the new extend -and- pretend ? 2013. The Perception vs. Reality Gap. ‘Illusion’ vs. reality Stock market vs. Unemployment rate ECB ‘succes’ vs. Rising debt / gdp levels Optimism vs. Crisis management Momentum vs. Fundamentals - PowerPoint PPT Presentation

Transcript of Steen Jakobsen, Chief Economist Currency Wars – the new extend -and- pretend ? 2013

Steen Jakobsen, Chief Economist

Currency Wars – the new extend-and-

pretend?

2013

2

The Perception vs. Reality Gap

• ‘Illusion’ vs. reality• Stock market vs. Unemployment rate• ECB ‘succes’ vs. Rising debt/gdp levels• Optimism vs. Crisis management• Momentum vs. Fundamentals• Economic crisis vs. Political crisis

3

30 years of experience in a few lessons

Macro

Micro

Joseph Schumpeter

John Maynard Keynes

Denial

Protest

Mandate for change

4

Dominating Trends for 2013/14

Monetary Policy: QE replaced by currency manipulation and more ‘overt monetary financing’

Macro trends: 2013 will see the crisis evolve from an economic crisis to a full blown political crisis

Macro inputs: Lower energy costs, reshoring to the US, lower contribution from growth from EMG due to ‘Middle Income Trap’ and inflationary pressures, global lower disposable income and higher net tax levels.

Investment: Flat stock markets at best for balance of 2013, better fixed income performance(low growth+ tension), and rising agriculture prices. FX exposure will make up bulk of attribution to return for balance of 2013

5

Investment themes for 2013/14

Beta exposure: 70% in Permanent PortfolioAlpha exposure: 30% in directionals

Alpha risk:

FX Shorts: GBP, ZAR, SEK, HUF, PLN, AUD(fromQ3),CADFX Longs: USD(50%), EUR (vs. EEA), SGD, NOKFutures Long: Soybeans, Timber, Gold, Bunds, 10Y Notes, AUD bondsFutures short: BTP, OAT, CAC-40 and DAX (both in options)Neutral: JPY, Credit, Outright stocks

Opportunistic: Sub-Sahara excl. S-Africa, Aluminium, Gold miners, Insurance companies, energy trading

Political plays: France to underperform, Italy being non-compliant to OMT, Germany election, Eastern Europe in deep recession,Tyrkey: Middle East safe haven

6

Currency manipulation the new Extend-and-Pretend

7

FX Manipulation: Shades of grey

Open manipulation:

Switzerland & Japan

Semi-open manipulation:

UK, South Africa, Poland, Hungary, Taiwan, South Korea, China

‘Needs to intervene’:

Sweden, Canada, Australia, New Zealand

‘Agnostic’

Europe, Singapore, Norway

8

Middle Class can’t save us now…

9

Need a war? We are ”at war”….economically

10

The Italian job

11

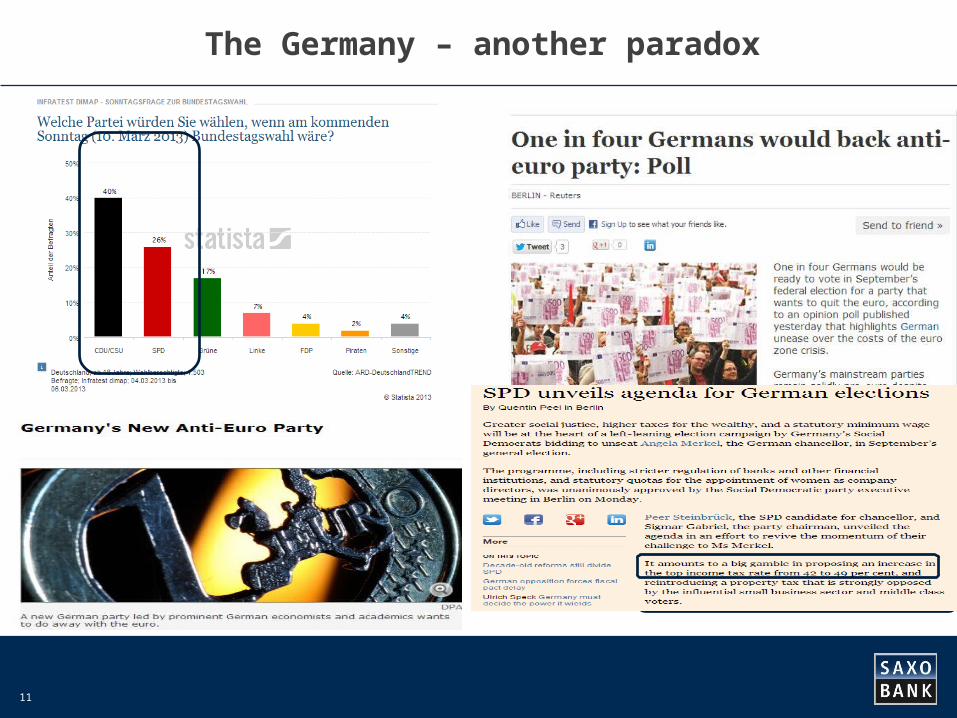

The Germany – another paradox

12

Growth? Where? EMG slowing down….

13

Eurozone indicators point towards more gloom

14

China – Bad growth – Middle Income trap

15

France – the new “weak”Germany – the new “spender”

16

Macro Overview

Slower growth, but is Spring coming?

17

Game changer: US shale gas

18

The wonders of micro economy and markets

(All sources are from external news sites)

19

Demographics are not a drag compared to peers

20

CEO’s buying back stocks but privately selling….

21

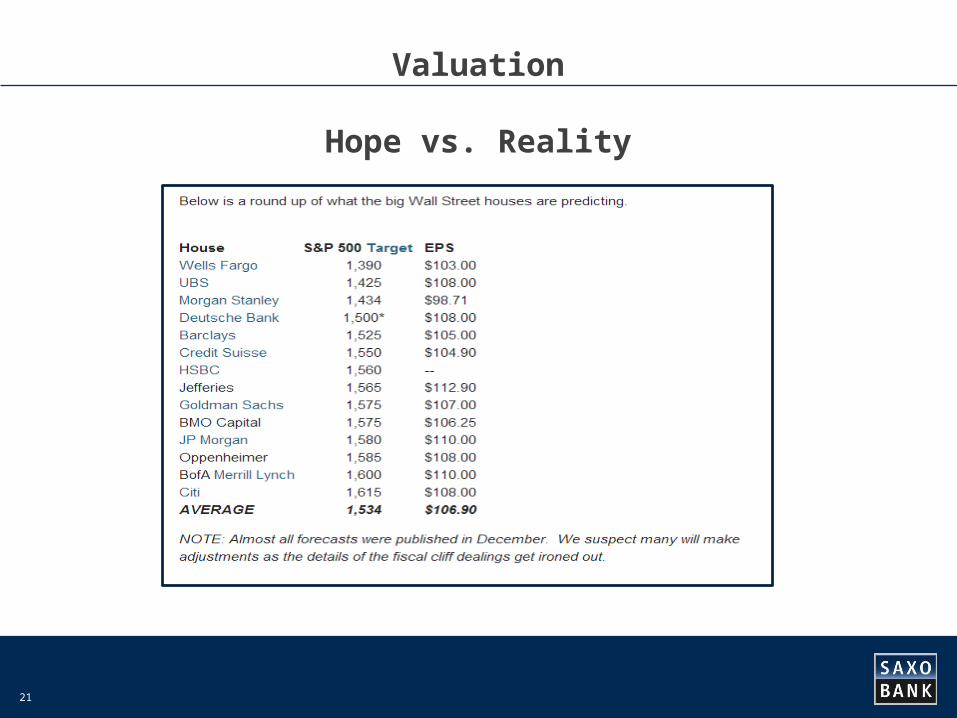

Valuation

Hope vs. Reality

22

Abe-nomics & JPY

(Data as of 2012-11-22) (All sources are from external news sites)

23

Investors needs to be ”agnostic” on economics

24

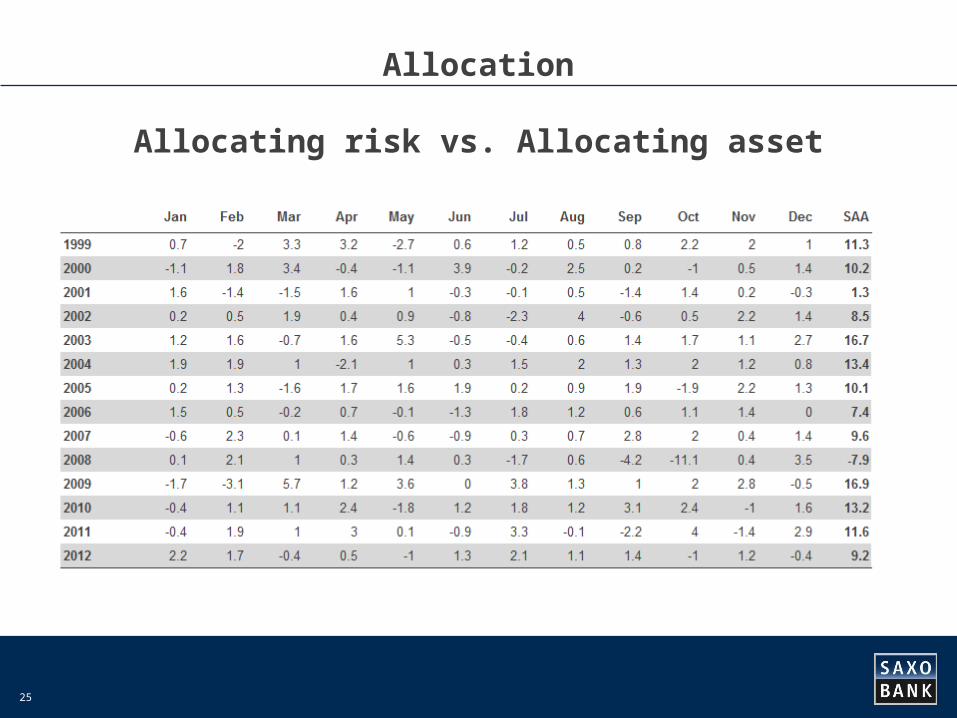

Allocation

Allocating risk vs. Allocating asset

Stocks:SPY US (18.75%)EM Bonds:EMB US (14.50%)Commodities:DBC US (10.00%)GLD (4.50%)Corp. Bonds:LQD US (6.25%)Treasuries:IEF US (25.00%) GovernmentIPE US (21.00%) TIPS

25

Allocation

Allocating risk vs. Allocating asset

26

Housing – Better and better

.

27

GBPUSD

• GBPUSD – lowest monthly close since 1985: 1.4100

28

USDZAR

• USDZAR – recent upside despite strong risk appetite…

29

AUDUSD

• AUDUSD – coiling for a big move?

Thank you!

![11C]-Labeled Metformin Distribution - Diabetesdiabetes.diabetesjournals.org/content/diabetes/65/6/1724.full.pdf · Jonas B. Jensen,1,2 Elias I. Sundelin,1 Steen Jakobsen,2 Lars C.](https://static.fdocuments.in/doc/165x107/5a829be87f8b9ada388dfdad/11c-labeled-metformin-distribution-b-jensen12-elias-i-sundelin1-steen-jakobsen2.jpg)