Staying on Top of HSA Requirements

43

-

Upload

benefitexpress -

Category

Recruiting & HR

-

view

412 -

download

2

Transcript of Staying on Top of HSA Requirements

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

By Larry Grudzien Attorney at Law

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Similar to Archer Medical Savings Accounts (MSAs) in structure and benefits, but there are many important differences.

• Tax-exempt trust or custodial accounts created exclusively to pay for the qualified medical expenses of the account holder and his or her spouse and/or dependents.

Source: Code §223

What is an HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Funding flexibility-employer contributions, employee salary reduction contributions and tax-deductible contributions are all permissible.

• No use-it-or-lose-it rule-participants may accumulate funds and self-direct investment in a tax-exempt trust or custodial account.

• Ability to use funds for non-medical purposes without any effect on the tax-free character of amounts used for medical expenses.

• Account portability for employees changing jobs.

Why Consider an HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Participant self-substantiation of expenses is required.

• The tandem high-deductible plan that is required is almost a mainstream-design.

• Family members, employers and any other third party may make contributions to an HSA on behalf of the eligible individual.

Why Consider an HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• For any month, an eligible individual is defined as any individual who: is covered only by a high-deductible health plan (HDHP)

as of the first day of such month is not also covered by any other health plan that is not a

HDHP (with certain exceptions for plans providing certain limited types of coverage)

is not enrolled in benefits under Medicare may not be claimed as a dependent on another person’s

tax return.

Who is Eligible to Make or Receive Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• What is a High Deductible Health Plan (“HDHP”)? It is a insured or self-insured health plan that satisfies

certain requirements with respect to deductibles and out-of pocket expenses.

In the case of individual coverage, the plan must have

an annual deductible of not less than, $1,250 for 2013 and 2014 and $1,300 for 2015.

In the case of family coverage, the plan must have an

annual deductible of not less than $2,500 for 2013 and 2014 and $2,600 for 2015.

Who is Eligible to Make or Receive Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• What is a High Deductible Health Plan (HDHP)? A health plan may contain the following features and still

be considered a HDHP: • A reasonable lifetime limit on benefits. Any lifetime limit on benefits

designed to circumvent the maximum annual out-of pocket amount is not reasonable. Under the Affordable Care Act, there are no longer lifetime or annual limits on essential health benefits.

• Limitation of payments to usual, customary and reasonable (“UCR”). • Uses amounts toward the deductible from a prior health plan if newly

adopted during the year. • Different levels of payment of benefits depending on whether a participant

goes in or out of network.

Who is Eligible to Make or Receive Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• What is a High Deductible Health Plan (HDHP)? In the case of individual coverage, the maximum out-of-pocket

expense limit on covered expenses cannot exceed $6,350 for 2014 and $6,450 for 2015.

In the case of family coverage, the maximum out-of pocket expense

limit on covered expenses cannot exceed $12,700 for 2014 and $12,900 for 2015.

Out-of-pocket expenses include deductibles, co-payments, and

other amounts (other than premiums) that the individual must pay for covered benefits under the plan.

Who is Eligible to Make or Receive Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

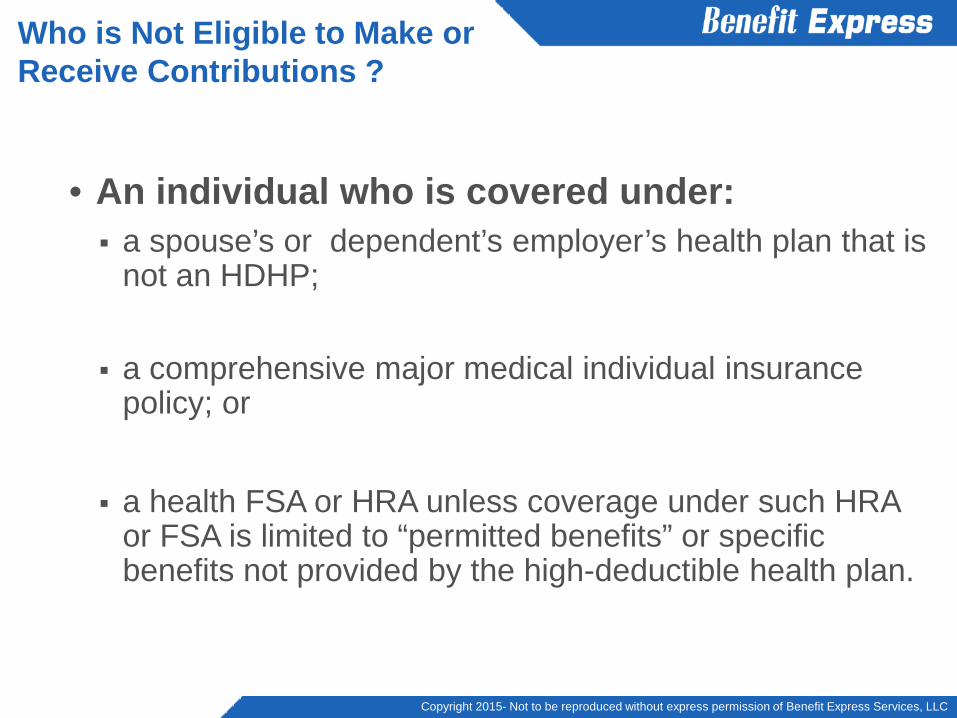

• An individual who is covered under: a spouse’s or dependent’s employer’s health plan that is

not an HDHP;

a comprehensive major medical individual insurance policy; or

a health FSA or HRA unless coverage under such HRA or FSA is limited to “permitted benefits” or specific benefits not provided by the high-deductible health plan.

Who is Not Eligible to Make or Receive Contributions ?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• H and W have family coverage covering each other and one of the plans is not a HDHP.

• H and W have family coverage, but not covering each other and one plan is not a HDHP.

• H and W have single coverage, but W participates in a Health FSA.

Who is Not Eligible to Make or Receive Contributions ?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Custodial or Trust Agreement

• Application and Eligibility Form

• Designation of Beneficiary Form

• Disclosure Statement

What Documents are Needed to Establish an HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• No - No coverage can be provided below deductible limits provided under a HDHP.

Can First Dollar Prescription Drug Coverage Be Provided?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• An employee may invest in investments approved for IRAs (e.g., bank accounts, annuities, certificates of deposit, stocks, mutual funds, or bonds).

• HSAs may not invest in life insurance contracts, or in collectibles.

Are There Any Restrictions on the Types of Investments Available Under an HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

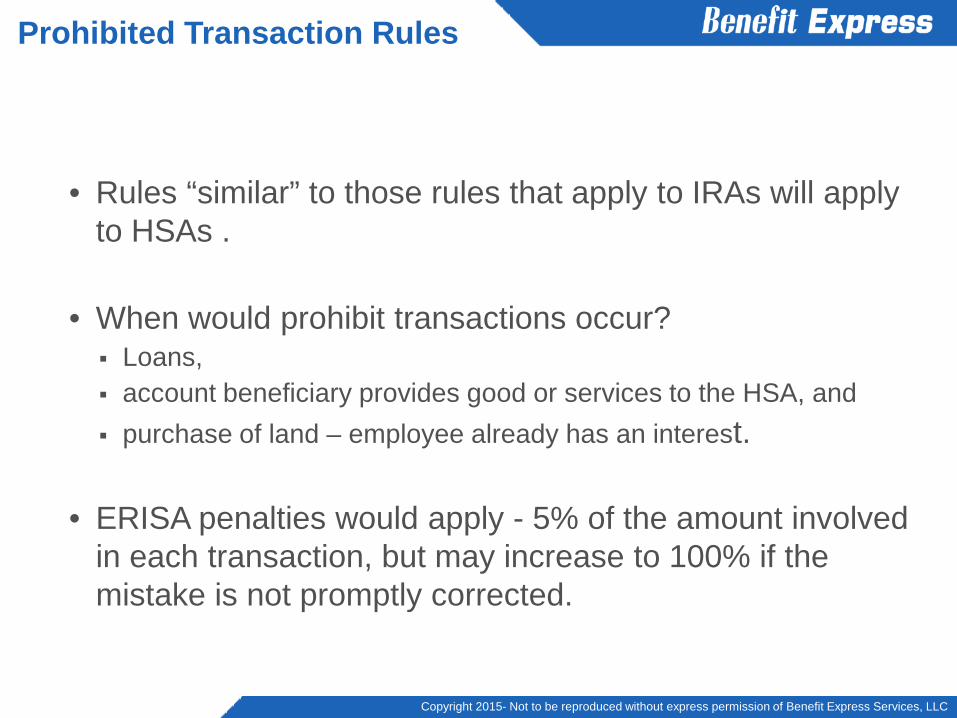

• Rules “similar” to those rules that apply to IRAs will apply to HSAs .

• When would prohibit transactions occur? Loans, account beneficiary provides good or services to the HSA, and purchase of land – employee already has an interest.

• ERISA penalties would apply - 5% of the amount involved in each transaction, but may increase to 100% if the mistake is not promptly corrected.

Prohibited Transaction Rules

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Employee Contributions: Contributions are deductible (within limits) in determining adjusted gross income .

• Employer Contributions: These contributions (including salary reduction contributions made through a cafeteria plan) are excludable from gross income and wages for employment tax purposes to the extent the contribution would be deductible if made by the employee.

• Other Contributions: Contributions may be made by family members and other third parties. These contributions are deductible by the eligible individual to the extent the contributions would be deductible if made by the individual.

What Contributions are Permitted and How are They Treated for Tax Purposes?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

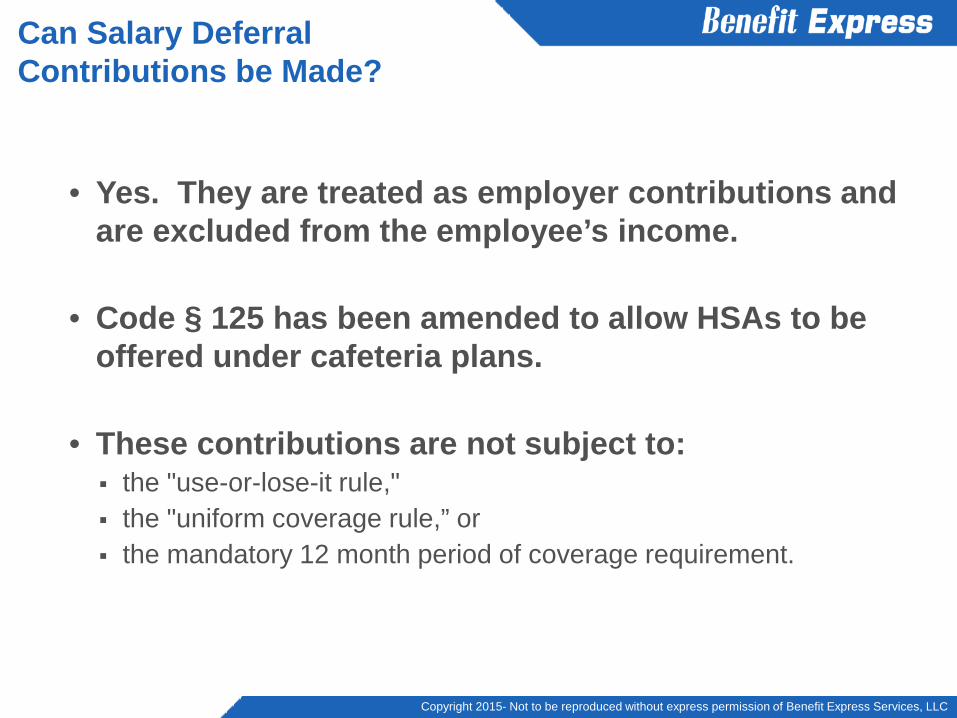

• Yes. They are treated as employer contributions and are excluded from the employee’s income.

• Code § 125 has been amended to allow HSAs to be offered under cafeteria plans.

• These contributions are not subject to: the "use-or-lose-it rule," the "uniform coverage rule,” or the mandatory 12 month period of coverage requirement.

Can Salary Deferral Contributions be Made?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• The maximum aggregate annual contribution that can be made to an HSA is the maximum deductible limit for the year (as adjusted for inflation): For individual coverage, the maximum amount is $3,300

for 2014 and $3,350 for 2015. For family coverage, the maximum amount is $6,550 for

2014 and $6,650 for 2015.

What are the Limits for Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

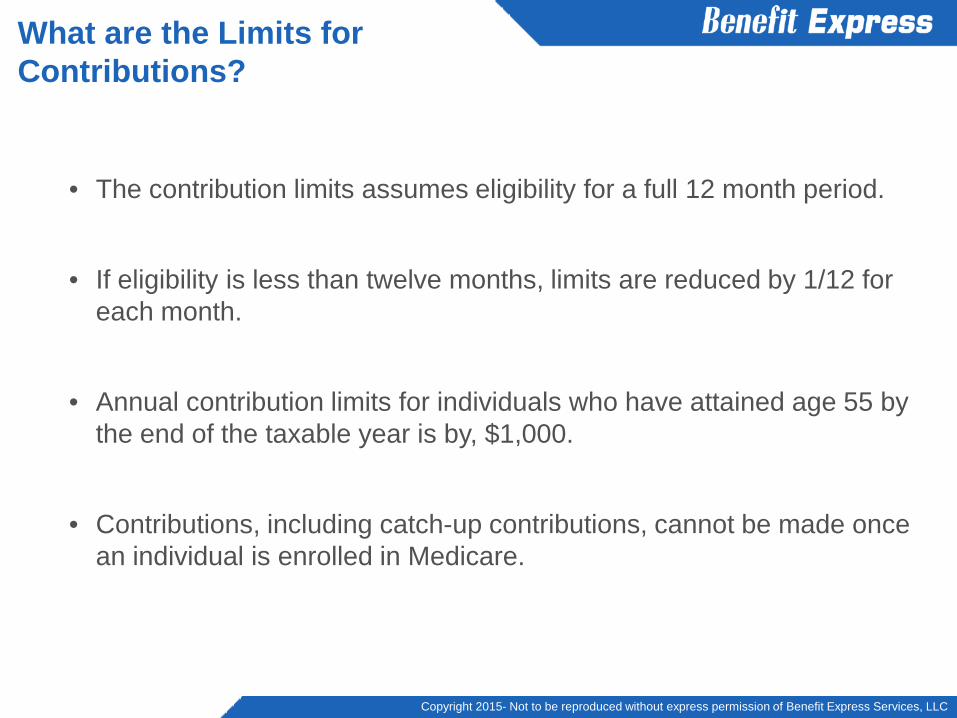

• The contribution limits assumes eligibility for a full 12 month period.

• If eligibility is less than twelve months, limits are reduced by 1/12 for each month.

• Annual contribution limits for individuals who have attained age 55 by the end of the taxable year is by, $1,000.

• Contributions, including catch-up contributions, cannot be made once an individual is enrolled in Medicare.

What are the Limits for Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• An individual, who becomes eligible to contribute to an HSA a month other than January and who is eligible in December of that year, may make a full deductible HSA contribution for the year if he or she has HDHP coverage for the entire “testing period.”

• The testing period is the period beginning with the last month of the taxable year and ending on the last day of the 12th month following such month.

• If an individual does not remain an eligible individual during the testing period, the amount of the contributions attributable to months preceding the month in which the individual was not an eligible individual (which could have not have been made but for the provision) will be includible in the individual’s gross income.

What are the Limits for Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• The amount is includible for the taxable year of the first day during the testing period that the individual was not an eligible individual.

• A 10-percent additional tax also applies to the amount includible.

• An exception applies if the individual ceases to be an eligible individual by reason of death or disability.

What are the Limits for Contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Any contributions exceeding the limits are not deductible.

• Contributions made by an employer over the limits are included in the employee’s income.

• An eligible individual is responsible for withdrawing any excess.

What Happens if the Limits are Exceeded for any Year?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Excise tax applies to contributions in excess of the maximum contribution amount.

• The excise tax is generally equal to 6% of the cumulative amount of excess contributions that are not distributed from the HSA .

• If the excess contributions for a taxable year and the net income are paid to the individual before the due date of tax return (including extensions) for filing, then the net income is included in the individual’s gross income for the taxable year in which the distribution is received but the excise tax is not imposed on the excess contribution and the distribution of the excess contributions is not taxed.

What Happens if the Limits are Exceeded for any Year?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• By the due date of your tax return for the year (excluding extensions).

• Contributions may be made any time during calendar year.

When Must Contributions be Made for any Year?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Yes. Amounts can be rolled over into an HSA from a MSA or another HSA on a tax-free basis.

• Rollovers need not be made in cash.

• Amounts can be rolled over into an HSA from another HSA.

• Amounts transferred from another HSA or a MSA are not taken into account under the annual contribution limits.

Can Amounts be Rolled Over to Another HSA or Another Type of Account?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• An individual may make only one rollover contribution to an HSA during a 1 year period.

• To qualify as a rollover, any amount paid or distributed from an HSA to an eligible individual must be paid over to an HSA within 60 days after the date of receipt of the payment or distribution.

Can Amounts be Rolled Over to Another HSA or Another Type of Account?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Yes. You are allowed to make a one-time contribution to an HSA of an amount distributed from his or her IRA.

• The contribution must be made in a direct trustee-to trustee transfer.

• Amounts distributed from the IRA are not includible in the individual’s income to the extent that the distribution would otherwise be includible in income.

• Such distributions are not subject to the 10-percent additional tax on early distributions.

Can Amounts be Rolled Over from an IRA to your HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• The amount that can be distributed from the IRA and contributed to an HSA is limited to the otherwise maximum deductible contribution to the HSA computed on the basis of the type of coverage under the HDHP at the time of the contribution.

• For the IRA rollover to be nontaxable, you must continue to be eligible to make contributions to HSA for 12 months following the rollover.

• If not, then the rollover becomes taxable to you.

Can Amounts be Rolled Over from an IRA to your HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Yes The employer must satisfy the following “comparability rules” or be subject to an excise tax.

• If an employer makes contributions to employees’ HSAs, the employer must make available comparable contributions (e.g. the same amount or the same percentage of deductible) on behalf of all employees with comparable coverage during the same period (e.g. single/family) with certain exceptions.

Are there any nondiscrimination rules for employer contributions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Distributions for qualified medical expenses of the individual and his or her spouse or dependents generally are excludable from gross income.

• Amounts in an HSA can be used for qualified medical expenses even if the individual is not currently eligible for contributions to the HSA.

• Qualified medical expenses generally are defined as under Code §§ 105 and 213(d) and include expenses for diagnosis, cure, mitigation, treatment, or prevention of disease, including prescription drugs, transportation primarily for and essential to such care, and qualified long term care expenses.

When Can Distributions Be Made?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Example: Ann establishes an HSA in 2012 and makes a contribution of

$2,000.

She has an medical expense in 2013 of $10,000 which is not

reimbursed by her health plan or can a deduction on her Form 1040.

She continues to contribute $2,000 each year during 2013, 2014,

2015 and 2016.

In 2016, she withdraws $10,000 from her HSA tax free.

When Can Distributions Be Made?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• General rule is health insurance premiums cannot be paid from HSA .

• Exceptions are for long-term care, COBRA, Medicare Part A and B, Medicare HMOs, and employer-sponsored retiree health insurance.

• Distributions from an HSA that are not for qualified medical expenses are includible in gross income .

• These taxable distributions are also subject to an additional 20% tax unless made after death, disability, or the individual attains the age of Medicare eligibility (i.e., age 65).

When Can Distributions Be Made?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Example: Eric, age 35. establishes and contributes $3,000 to his HSA in

March 2014.

Later, he withdrawals to $1,500 to buy a big screen TV.

When Eric later files his tax return for 2014, he must report $1,500

as income and pay an excise tax of $150.

Would the answer be different if Erie had eligible medical expense of $1,500 later in

2014?

When Can Distributions Be Made?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• It is the eligible individual because he or she claims treatment on Form 1040.

• The HSA custodian are not permitted to substantiate claims.

• The employer is not permitted to substantiate.

Who Substantiates if Paid for Medical Expenses?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Any balance remaining in the decedent’s HSA is includible in his or her gross estate.

• If the HSA holder’s surviving spouse is the named beneficiary of the HSA, then, after the death of the HSA holder, the HSA becomes the HSA of the surviving spouse and the amount of the HSA balance may be deducted in computing the decedent's taxable estate, pursuant to the estate tax marital deduction.

What Happens to an Individual’s HSA Upon his or her Death?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• If, upon death, an HSA passes to a named beneficiary other than the decedent’s surviving spouse, the HSA ceases to be an HSA as of the date of the decedent's death, and the beneficiary is required to include the fair market value of HSA assets as of the date of death in gross income for the taxable year that includes the date of death.

• A non-spouse beneficiary may reduce the taxable amount by payments made from the HSA for qualified medical expenses incurred by the decedent before death, but only if the payments are made within one year after the death.

What Happens to an Individual’s HSA Upon his or her Death?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Yes. An individual’s interest in a HSA may be transferred to an HSA established for the spouse (or ex-spouse) under a decree of divorce or separate maintenance or a written instrument incident to such decree.

• Such distribution is not taxable or subject to a 20% excise tax and the spouse (or ex-spouse) becomes the holder of the HSA.

Can Amounts be Transferred Because of Divorce?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• An HSA custodian may not accept annual contributions to any HSA that exceed the sum of:(1) the maximum family dollar limit for the year, plus (2) the catch-up contributions.

• All contributions must be in cash, other than rollover contributions or trustee to trustee transfers.

• The HSA custodian is responsible for determining whether contributions to an HSA exceeds the maximum family statutory dollar limit for a particular account beneficiary.

What Responsibilities Does an HSA Custodian Have?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• No. Since employees own the HSA, an employer, trustee or custodian may not place limitation on withdrawals.

• An HSA custodian may place reasonable restrictions on both frequency and the minimum amount from an HSA.

• The HSA custodian may prohibit distributions for amounts of less than $50 or only allow a certain number of distributions per month.

• An HSA custodial agreement may not restrict the account holder’s ability to rollover or transfer an amount from that HSA.

May the Employer, HSA Custodian put any Restrictions on the Withdrawals from an HSA?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• Eligible individuals will report contributions to their HSAs, contributions to their spouse’s HSAs, any employer contributions and distributions on Form 8889. Form 8889 is an attachment to eligible individual’s Form 1040.

• Employer contributions are required to be reported in Box 12 on the Form W-2 of the employee, using code W.

• In addition, the HSA custodian must report contributions to an HSA for a year on Form 5498-SA and distributions for the year on Form 1099-SA.

What Reporting is Required?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

• When you contribute to an HSA, you must: Determine whether he or she is eligible.

Determine the proper amount to contribute.

Remove any excess contributions.

Make distributions.

Determine whether distributions are taxable or

nontaxable.

Individual’s New Responsibility

Questions?

Copyright 2015- Not to be reproduced without express permission of Benefit Express Services, LLC

Contact Information

Larry Grudzien

• Phone: 708-717-9638

• Email: [email protected]

• Site: www.larrygrudzien.com

![HSA Stud anchor - Hilti - Hilti Saudi Arabia€¦ · HSA Stud anchor 6 11 / 2016 Geometry washer Anchor Size M6 M8 M10 M12 M16 M20 Inner diameter d 1 HSA, HSA-R2/ R, HSA-F d 1 [mm]](https://static.fdocuments.in/doc/165x107/5b61cb307f8b9a09498cd093/hsa-stud-anchor-hilti-hilti-saudi-arabia-hsa-stud-anchor-6-11-2016-geometry.jpg)