Status of Green Bonds · PDF fileManagement of Proceeds The net ... Real Estate, Waste &...

12

Michael Eckhart Managing Director Global Head of Environmental Finance Citigroup Capital Markets, Inc. [email protected] Status of Green Bonds

Transcript of Status of Green Bonds · PDF fileManagement of Proceeds The net ... Real Estate, Waste &...

Michael EckhartManaging Director

Global Head of Environmental FinanceCitigroup Capital Markets, Inc.

Status of Green Bonds

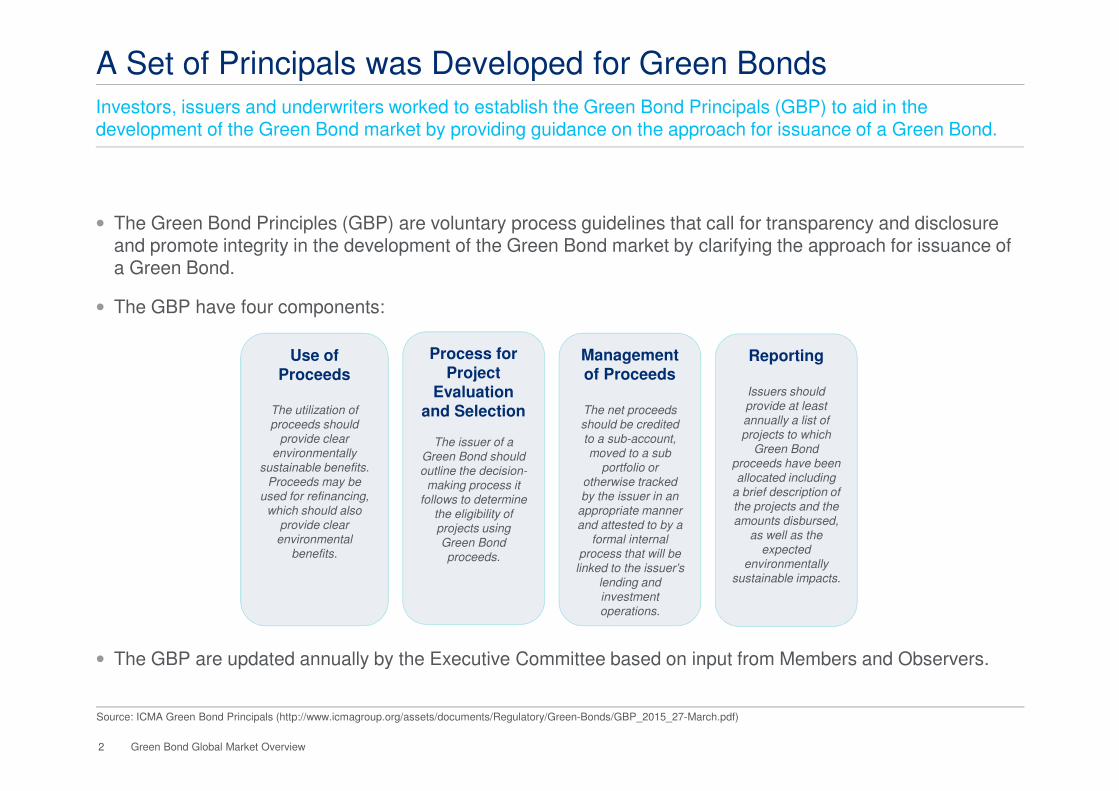

• The Green Bond Principles (GBP) are voluntary process guidelines that call for transparency and disclosure and promote integrity in the development of the Green Bond market by clarifying the approach for issuance of a Green Bond.

• The GBP have four components:

• The GBP are updated annually by the Executive Committee based on input from Members and Observers.

A Set of Principals was Developed for Green BondsInvestors, issuers and underwriters worked to establish the Green Bond Principals (GBP) to aid in the development of the Green Bond market by providing guidance on the approach for issuance of a Green Bond.

Source: ICMA Green Bond Principals (http://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/GBP_2015_27-March.pdf)

Use of Proceeds

The utilization of

proceeds should

provide clear

environmentally

sustainable benefits.

Proceeds may be

used for refinancing,

which should also

provide clear

environmental

benefits.

Process for Project

Evaluation and Selection

The issuer of a

Green Bond should

outline the decision-

making process it

follows to determine

the eligibility of

projects using

Green Bond

proceeds.

Management of Proceeds

The net proceeds

should be credited

to a sub-account,

moved to a sub

portfolio or

otherwise tracked

by the issuer in an

appropriate manner

and attested to by a

formal internal

process that will be

linked to the issuer’s

lending and

investment

operations.

Reporting

Issuers should

provide at least

annually a list of

projects to which

Green Bond

proceeds have been

allocated including

a brief description of

the projects and the

amounts disbursed,

as well as the

expected

environmentally

sustainable impacts.

2 Green Bond Global Market Overview

• As of 9/9/2015 the GBP Executive Committee has a total of 24 members reflecting a representative group of:

– 8 Investors: Actiam, Blackrock, CalSTRS, KFW, Natixis Asset Management / Mirova, Standish Melon Asset Management, TIAA-CREF, Zurich Insurance Group

– 8 Issuers: EDF, EBRD, European Investment Bank, ENGIE, International Finance Corporation, Unibail-Rodamco, Unilever, World Bank

– 8 Underwriters: Bank of America Merrill Lynch, Citi, Credit Agricole CIB, HSBC, JPMorgan Chase, Morgan Stanley, Rabobank, Skandinaviska Enskilda Banken

• ICMA serves as Secretariat to the GBP carrying out the governance of the Green Bond Principles

GBP Organizational Chart

Investors Underwriters

GBP Executive Committee

Has the authority to address all matters relating to the GBPand issues the annual update of the GBP.

A Governance document sets forth the rules for GBP administration and establishes a GBP Executive Committee

Issuers

3 Green Bond Global Market Overview

1) XXXXX

Member Organizations of the GBP (as of 21/8/2015)

Membership in the GBP is open to organizations that have issued, underwritten, or invested in a Green Bond.

Source: International Capital Markets Association

Investors• ACTIAM • BlackRock• Blue Morpho Investments • Breckinridge Capital Advisors• British Columbia IM• CalSTRS• CM-CIC • Erste• Generation • Humanis Gestion d'Actifs• ING Groep• KfW• MainStreet Capital • Natixis AM – Mirova• NN Investment Partners • OFI • PGGM Vermogensbeheer• Standish Mellon • State Street • TIAA-CREF • Union Investment • Wasmer, Schroeder & Co.• Zurich Insurance Group

Issuers• African Development Bank• Berlin Hyp AG• BNG Bank• Commonwealth of

Massachusetts• D.C. Water and Sewer

Authority• EDF SA• ENGIE (ex GDF Suez)• European Bank of

Reconstruction and Development

• European Investment Bank• FMO• Hannon Armstrong

Sustainable Infrastructure • IFC• Kommunalbanken• Nordic Investment Bank• NRW.BANK• NWB Bank• Overseas Private Investment

Corporation• Région Ile-de-France• Toronto-Dominion Bank• Unibail-Rodamco• Unilever• World Bank

Underwriters• ABN AMRO Bank• Banca IMI SpA• Banco Santander• Bank of America - Merrill

Lynch• Barclays• BBVA• Belfius Bank SA/NV• Bank of Montreal• BNP Paribas• Caixa Bank• Casgrain & Company Limited• CastleOak Securities• CIBC World Markets• Citi• CM-CIC securities• Commerzbank• Crédit Agricole• Crédit Suisse• Daiwa Capital Markets

Europe• Danske Bank• Deutsche Bank • DNB• DZ Bank • Goldman Sachs• Handelsbanken• HSBC Bank• Incapital

• ING Bank• JCI Capital• Jefferies International• JP Morgan Chase & Co• KBC Bank• LBBW• Lloyds Bank• Mitsubishi UFJ • Morgan Stanley & Co • National Australia Bank• National Bank Financial• Natixis• Nomura International• Nordea Bank Finland Oyj• Piper Jaffray & Co• Rabobank• RBC Europe• RBI• Royal Bank of Scotland• Skandinaviska Enskilda

Banken• SMBC Nikko• Société Générale• Standard Chartered• Stifel, Nicolaus & Co• UBS• UniCredit Bank• Wells Fargo Bank• Westpac Institutional Bank

4 Green Bond Global Market Overview

Green Bond Market has Experienced Rapid GrowthOver $30 billion of bonds related to climate change were issued in 2014, against $13 billion in the whole of 2013. Volume in 2015 will exceed 2014, with a decline in SSA1 issuance offset by growth in corporate and municipal.

Source: Bloomberg and Citi.1. Corporate includes: Real Estate, Waste & Environment Services & Equipment, Financial Services, Food & Beverage, Consumer Products, Consumer Finance, Educational Services, Consumer Services, Semiconductors and Industrial Other

Since 2009, interest in green bonds has expanded globally, as investors have looked to invest capital in products that support environmental sustainability.

$1.8 $0.6

$1.7

$13.2

$31.1

$23.2

$31.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

$35.0

2009 2010 2011 2012 2013 2014 2015 YTD

Power Generation and Utilities Corporate¹ Government Agencies

Supranationals Banks and Diversified Banks Renewable Energy

Government Development Banks Government Regional and Local Projected

5 Market Dynamics and Key Developments

Green Bonds Are Issued by Public and Private EntitiesSo far in 2015, the green bond market has seen increased activity from a wider range of issuers over the past few years.

Source: Bloomberg.

Illustrative Green Bond Issuers

Power Generation and

Utilities21%

Corporate21%

Government Agencies

2%

Supranationals29%

Banks and Diversified

Banks2%

Renewable Energy

1%

Government Development

Banks20%

Government Regional and

Local4%

Power Generation and

Utilities25%

Corporate23%

Government Agencies

12%

Supranationals12%

Banks and Diversified

Banks10%

Renewable Energy

9%

Government Development

Banks5%

Government Regional and

Local4%

2015 YTD

2014

Green Bonds: By issuer type 2014 to 2015

6 Market Dynamics and Key Developments

• The bulk of green issuance continues to be in USD and EUR, however development banks have been increasingly issuing new green bond transactions in local currencies

The Green Bond Market is Becoming Increasingly More GlobalThe globalization of green bonds can be viewed from two perspectives: the currency and the location of the issuer.

Green Bonds: by Currency 2014 to 2015 YTD

Source: Bloomberg.1. Other1 includes: BRL, CAD, CHF, CNY, COP, HUF, IDR, INR, JPY, MXN, MYR, NOK, NZD, PEN, PLN, RUB, TRY and ZAR.2. Other2 includes: BRL, CHF, CNY, COP, HUF, IDR, INR, JPY, MXN, MYR, NOK, NZD, PEN, PLN, RUB, TRY and ZAR.

Green Bonds have been Issued by Organizations in Many Countries

> $10bn issued< $10bn issued

2015 YTD

2014

USD45%

EUR37%

GBP6%

SEK5%

AUD4%

Other¹3%

EUR49%

USD20%

SEK9%

GBP8%

CAD4%

AUD2%

Other²8%

7 Market Dynamics and Key Developments

Additional Detail on GlobalizationThe globalization of green bonds can be viewed from two perspectives: the currency and the location of the issuer.

Source: J.P. Morgan.1. Count of signatories, only includes Asset Owners and Investment Managers (excludes Professional Service Partners)

Legend1

100 – 200

30 – 100

10 – 30

0 – 10

Global Distribution of Green SRI Investors (UN PRI Signatories)

UK

USA

France

Australia

Brazil

Netherlands

Switzerland

Canada

Germany

South Africa

Sweden

Finland

Japan

Spain

Denmark

New Zealand

Luxembourg

Italy

Norway

Hong Kong

Austria/Liechtenstein

Iceland

Ireland

Singapore

South KoreaTurkey

Channel Islands

Estonia

China

India

Indonesia

Nigeria

Puerto Rico

Vietnam

Bermuda

Botswana

British Virgin IslandsCayman Islands

ColumbiaGhana

Malaysia

Namibia

Peru

Portugal

Thailand

UnitedArab

Nations

Mauritius

Belgium

• The bulk of green issuance continues to be in USD and EUR, however development banks have been increasingly issuing new green bond transactions in local currencies

8 Market Dynamics and Key Developments

SSA Bonds: Wide Range of Deal Size and CouponsThe majority of SSA green bonds have been large scale, low coupon, low risk bonds, however, there are many examples of higher risk, higher coupon, higher risk bonds as well.

Source: Bloomberg.

• How to interpret: Coupon on y-axis, date on x-axis, bubble size based on size of issuance, bubble color based on issuer industry

10 Market Dynamics and Key Developments

0.0

2.0

4.0

6.0

8.0

10.0

12.0%

Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15

Coupo

n

Supranationals Government Agencies Government Development Banks Government Regional and Local

Scale

$1bn

$500mm

Corporate Bonds: Also a Wide Range of Deal Size and CouponsThe majority of corporate green bonds have been large scale, low coupon, low risk bonds, however, there are many examples of higher risk, higher coupon, higher risk bonds as well.

Source: Bloomberg.

• How to interpret: Coupon on y-axis, date on x-axis, bubble size based on size of issuance, bubble color based on issuer industry

0.0

2.0

4.0

6.0

8.0

10.0

12.0%

Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15

Cou

pon

Power Generation and Utilities Corporate Banks and Diversified Banks Renewable Energy

Scale

$1bn

$500mm

11 Market Dynamics and Key Developments

Major Investors in Green BondsThe success of a Green Bond is often judged in part by support from the ‘deep green’ investors. Below is an overview of both well-known & niche buyers.

Illustrative Green Bond Investors: Green Bond Investors Expectations

Some investors have a dedicated SRI/Green Portfolio while others who have a particular interest in green bonds purchase these from a general fund.

Some investors may have a preference for Green bonds to adhere to voluntary standards such as the Green Bond Principles.

To avoid the risk of green washing, investors are increasingly interested in impact reporting over the life of a green bond.

Investors have begun to add ESG (Environmental Social Governance) as a key component of their credit / equity research reports. At times their investment decision is linked to the issuers overall ESG score.

In general, as the green bond market grows investors are developing a better understanding of what level of transparency they want from the issuers of green bonds.

12 Market Dynamics and Key Developments

Outlook for Green Bonds

The Green Bond market is just starting, but the upside potential is $1 trillion/year or more, to meet climate goals.

Source: International Energy Agency World Energy Outlook 2012, IEA, Ceres, IRENA.

• Recent estimates by reputable sources suggest that an enormous amount of capital investment in green uses will be required over the next 50 years

• If debt capital markets provide 50% of the needed capital, then the Green Bond market could exceed $1 trillion/year of new issuances.

20

25

30

35

40

45

1990 2000 2010 2020 2030

Gt

Current Policies Scenario

New Policies Scenario

Efficient World Scenario

450 Scenario (2ºC)

IEA’s Global Energy-Related CO2 Emissions by Scenario

IRENA

Ceres

IEA $8.25 trillion (between now and 2030)

$48 trillion (between now and 2035)

$44 trillion (between now and 2050)

16 Issues and Outlook