Statoil Business Update - Jefferies Group › CMSFiles › Jefferies.com › files ›...

26

2012-10-24 Classification: Internal Statoil Business Update November 2016

Transcript of Statoil Business Update - Jefferies Group › CMSFiles › Jefferies.com › files ›...

2012-10-24Classification: Internal

Statoil Business UpdateNovember 2016

Forward-looking statements

These forward-looking statements reflect current views about future events and are, by their nature, subject

to significant risks and uncertainties because they relate to events and depend on circumstances that will

occur in the future. There are a number of factors that could cause actual results and developments to differ

materially from those expressed or implied by these forward-looking statements, including levels of industry

product supply, demand and pricing; price and availability of alternative fuels; currency exchange rate and

interest rate fluctuations; the political and economic policies of Norway and other oil-producing countries;

EU developments; general economic conditions; political and social stability and economic growth in

relevant areas of the world; global political events and actions, including war, political hostilities and

terrorism; economic sanctions, security breaches; changes or uncertainty in or non-compliance with laws

and governmental regulations; the timing of bringing new fields on stream; an inability to exploit growth or

investment opportunities; material differences from reserves estimates; unsuccessful drilling; an inability to

find and develop reserves; ineffectiveness of crisis management systems; adverse changes in tax regimes;

the development and use of new technology; geological or technical difficulties; operational problems;

operator error; inadequate insurance coverage; the lack of necessary transportation infrastructure when a

field is in a remote location and other transportation problems; the actions of competitors; the actions of

field partners; the actions of governments (including the Norwegian state as majority shareholder);

counterparty defaults; natural disasters and adverse weather conditions, climate change, and other

changes to business conditions; an inability to attract and retain personnel; relevant governmental

approvals; industrial actions by workers and other factors discussed elsewhere in this report. Additional

information, including information on factors that may affect Statoil's business, is contained in Statoil's

Annual Report on Form 20-F for the year ended December 31, 2015, filed with the U.S. Securities and

Exchange Commission, which can be found on Statoil's website at www.statoil.com.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we

cannot assure you that our future results, level of activity, performance or achievements will meet these

expectations. Moreover, neither we nor any other person assumes responsibility for the accuracy and

completeness of the forward-looking statements. Unless we are required by law to update these

statements, we will not necessarily update any of these statements after the date of this report, either to

make them conform to actual results or changes in our expectations.

2

This report contains certain forward-looking statements that involve risks and uncertainties. In some cases,

we use words such as "ambition", "continue", "could", "estimate", "expect", "focus", "likely", "may", "outlook",

"plan", "strategy", "will", "guidance" and similar expressions to identify forward-looking statements. All

statements other than statements of historical fact, including, among others, statements regarding plans and

expectations with respect to market outlook and future economic projections and assumptions; Statoil’s

focus on capital discipline; expected annual organic production through 2017; projections and future impact

related to efficiency programmes; capital expenditure and exploration guidance for 2016; production

guidance; Statoil’s value over volume strategy; Statoil’s plans with regard to its acquisition of 66% operated

interest in the BM-S-8 offshore license in the Santos basin; Statoil’s expected report on helicopter safety on

the Norwegian continental shelf; organic capital expenditure for 2016; Statoil’s intention to mature its

portfolio; exploration and development activities, plans and expectations, including estimates regarding

exploration activity levels; projected unit of production cost; equity production; planned maintenance and the

effects thereof; impact of PSA effects; risks related to Statoil’s production guidance; accounting decisions

and policy judgments and the impact thereof; expected dividend payments, the scrip dividend programme

and the timing thereof; estimated provisions and liabilities; the projected impact or timing of administrative or

governmental rules, standards, decisions, standards or laws, including with respect to the deviation notice

issued by the Norwegian tax authorities and future impact of legal proceedings are forward-looking

statements. You should not place undue reliance on these forward- looking statements. Our actual results

could differ materially from those anticipated in the forward-looking statements for many reasons.

Firm strategy to capture value in the upturn

3

Efficiency

improvements and

market effects

Strict financial discipline

Faster and deeper cost

reductionsPreparing to invest in next-

generation portfolio

Radically improved

break-evens

Maintaining dividend,

introducing scrip option

Sustained efficiency

gains

Significant new volumes

2018-2022

Capturing the upturn in oil

and gas prices

Johan Castberg Johan Sverdrup

Additional

reduction of

USD 3.3 billion

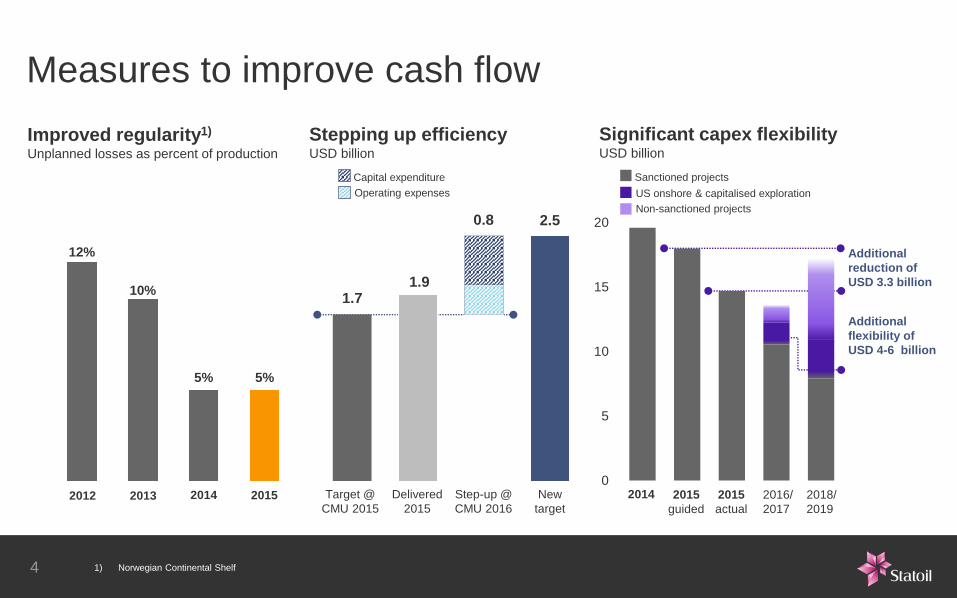

Measures to improve cash flow

Stepping up efficiencyUSD billion

1.7

0.8 2.5

1.9

Capital expenditure

Operating expenses

Improved regularity1)

Unplanned losses as percent of production

12%

10%

5% 5%

2012 20142013 2015

4

0

5

10

15

20

2016/

2017

2018/

2019

2015

guided

2015

actual

Sanctioned projects

Non-sanctioned projects

US onshore & capitalised exploration

Additional

flexibility of

USD 4-6 billion

Significant capex flexibilityUSD billion

2014Target @

CMU 2015

Delivered

2015

Step-up @

CMU 2016

New

target

1) Norwegian Continental Shelf

Capturing value from next-generation portfolio

2013 2016

Production potential to 2022Production from non-sanctioned1) projects2), mboe/d

29%below

$50/boe

82%below

$50/boe

Break-even

per barrel

Capex

Optimised portfolioOperated non-sanctioned projects starting up by 2022, weighted by volume

5

70USD

41USD

0

50

100

150

200

250

300

2017/18 2019/20 2021/22

1) Non-sanctioned projects exclude exploration

2) Includes partner-operated projects

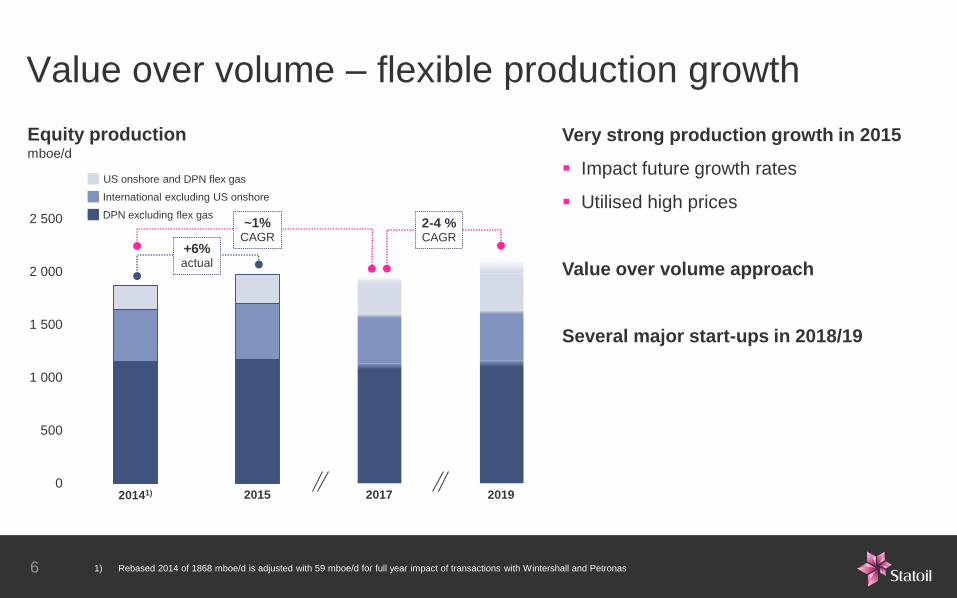

Value over volume – flexible production growth

Very strong production growth in 2015

Impact future growth rates

Utilised high prices

Value over volume approach

Several major start-ups in 2018/19

Equity productionmboe/d

0

500

1 000

1 500

2 000

2 500

20141) 2015 2017 2019

DPN excluding flex gas

International excluding US onshore

US onshore and DPN flex gas

+6% actual

~1% CAGR

2-4 % CAGR

6 1) Rebased 2014 of 1868 mboe/d is adjusted with 59 mboe/d for full year impact of transactions with Wintershall and Petronas

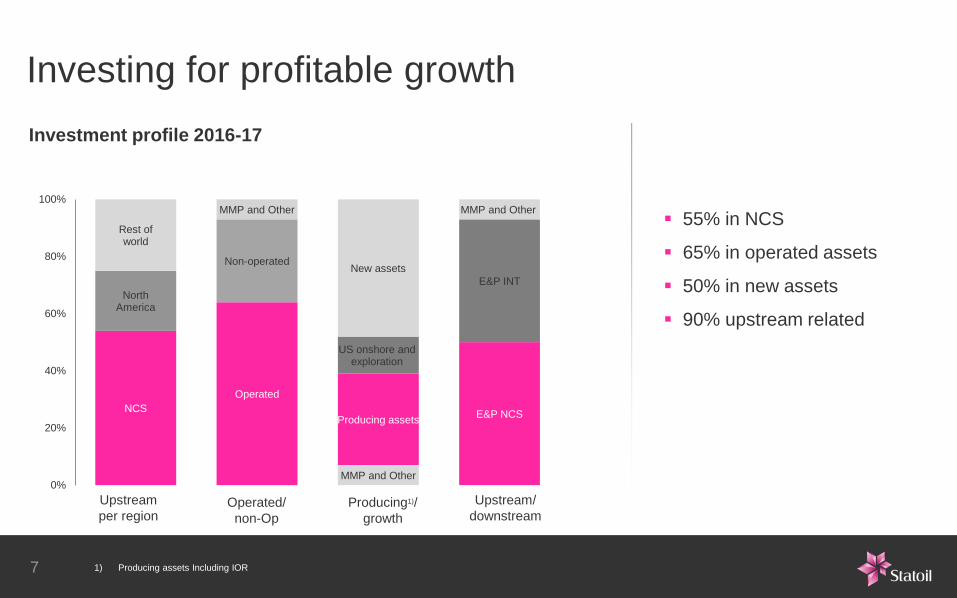

Investing for profitable growth

55% in NCS

65% in operated assets

50% in new assets

90% upstream related

Investment profile 2016-17

NCS

NorthAmerica

Rest of world

Operated

Non-operated

MMP and Other

MMP and Other

Producing assets

US onshore and exploration

New assets

E&P NCS

E&P INT

MMP and Other

0%

20%

40%

60%

80%

100%

Upstream

per regionProducing1)/

growth

Upstream/

downstream

7

Operated/

non-Op

1) Producing assets Including IOR

Phase 1 break-even price

Current below

25USD/bbl

Phase 1 production capacity

Increased to

440 000Boepd

Phase 1 capex reductions1)

123.2

108.5

99

50

60

70

80

90

100

110

120

130

PDO Simplification Strategy andmarket

CMU Drilling andWell

Executionquality

Currentforecast

NO

K b

illi

on

20%

8

Johan Sverdrup

1) Capex numbers in NOK nominal terms based on project currency

Johan Sverdrup – Full field development

Production capacity

boepd

140-170 bn

Investment estimate

NOK (2016 value)

Below 30

Break-even

USD/bbl

1.9-3.0 bn

Resources

bbl

660 000

Expected

start-up

2022

9

Johan Castberg

100

50-60

0

20

40

60

80

100

120

2013 Conceptchange

Drillingand well

Subsea Floater Market CurrentFC

NO

K b

illio

n

40-50%

Capex reductions 1)

Changes in break-even price

2013

above

80USD/bbl

Current

below

45USD/bbl

10 1) Capex numbers in real term NOK 2016

World class drilling performance

Meter per day Days per well Spend per well1)

70% 40% 30%

Continued improvements production drilling

"More for less"

2015: 95 wells planned | 117 wells delivered

2016: 113 wells planned | 120-125 wells forcasted

Rushmore benchmark: Meter per day 2006-2015 (2Q)

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Brazil Canada Offshore DenmarkNetherlands Norway UKUS GoM Deep Grand total Statoil

1) Nominal currency adjusted 11

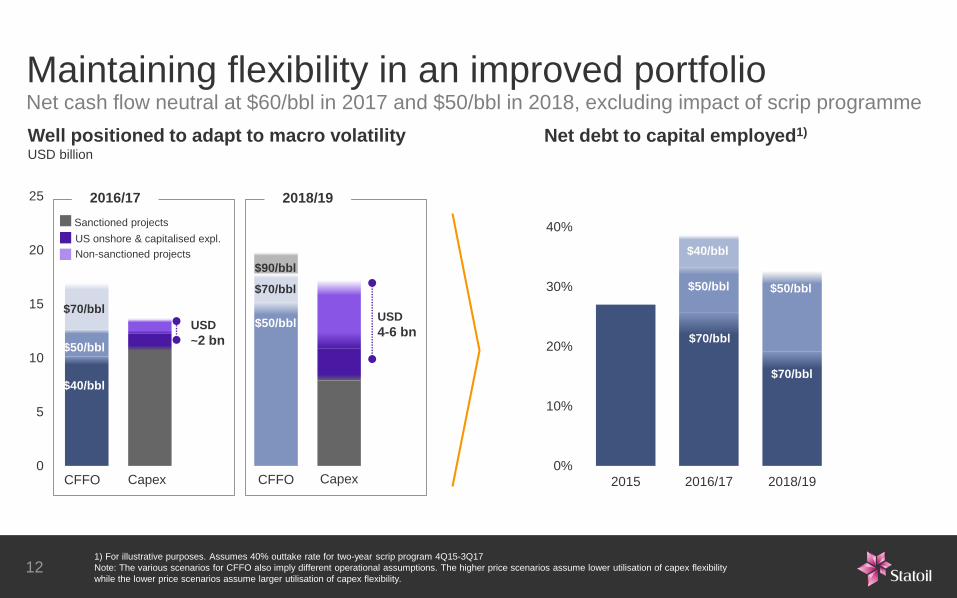

0

5

10

15

20

25

0%

10%

20%

30%

40%

2015 2016/17 2018/19

Maintaining flexibility in an improved portfolio

Well positioned to adapt to macro volatilityUSD billion

$70/bbl

$50/bbl

$40/bbl

$50/bbl

$70/bbl

CFFO CFFOCapex Capex

2016/17 2018/19

USD

~2 bn

USD

4-6 bn

Net cash flow neutral at $60/bbl in 2017 and $50/bbl in 2018, excluding impact of scrip programme

Sanctioned projects

Non-sanctioned projects

US onshore & capitalised expl.

Net debt to capital employed1)

$70/bbl

$50/bbl

$40/bbl

$50/bbl

$70/bbl

$90/bbl

121) For illustrative purposes. Assumes 40% outtake rate for two-year scrip program 4Q15-3Q17

Note: The various scenarios for CFFO also imply different operational assumptions. The higher price scenarios assume lower utilisation of capex flexibility

while the lower price scenarios assume larger utilisation of capex flexibility.

13

DPUSA: a diverse and high-potential portfolio

US Offshore

Producing ~40 mboe/d 1)

Several project start-ups

High-value barrels

2005

Statoil & Norsk Hydro merger

Marcellus

Eagle Ford

Bakken operatorship

Marcellus operatorship

2015 Eagle Ford full operatorship

Eagle Ford partial

operatorship

Encana GoM portfolio

US Onshore

Producing ~210 mboe/d 1)

Premium portfolio in core plays

Proven operator

1) Average daily equity production in 2015

14

DPUSA three-year plan: Transform the US business

Grow with qualityMake money Improve

Profitable investments

>50% production growth potential

Double EBITDA/boe

Reduce price needed to achieve

NOI=0

From $90/bbl to $50/bbl1)

Step up improvements

Reduce costs

One onshore organisation

~ $5

2014 2018

>100%

240

2014 2018

>50%

Production potential

mboe/d

EBITDA $/boe

@ $50 WTI

- 25%

- 25%

- 20%

Onshore capex

$/boe

Onshore opex

$/boe

SG&A costs

$/boe

2015

baseline

90

50

2014 2015 2016 2017 2018

$/b

bl(W

TI)

100

80

60

40

1) Adjusted NOI; figures exclude exploration and downstream.

Assumes product and gas prices correlate to changes in the WTI price.

Realised price in the US portfolio is significantly lower than WTI due to the mix of gas / oil / products and local market conditions

European gas price drivers – more than oil

Forward prices*

The price fall for gas is less severe than for oil

European gas market drivers

Demand

Temperature

Competing fuels and CO2

Politics

Supply

Long-term contracts

LNG supply

Domestic production

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015 2016 2017 2018

Japan - Korea Spot LNG NBP spot (UK)

Henry Hub (US) Brent

FW market1)

Brent and global gas prices USD/MMBtu

Sources: Platts, ICE, NYMEX, Statoil ASA

1) Forward prices as of 3 Jun 2016, NYMEX Henry Hub Forward 3 Jun 2016 (USD5/MMBtu = 157 Øre/Scm) Conversion 40MJ/Sm3 (GCV)15

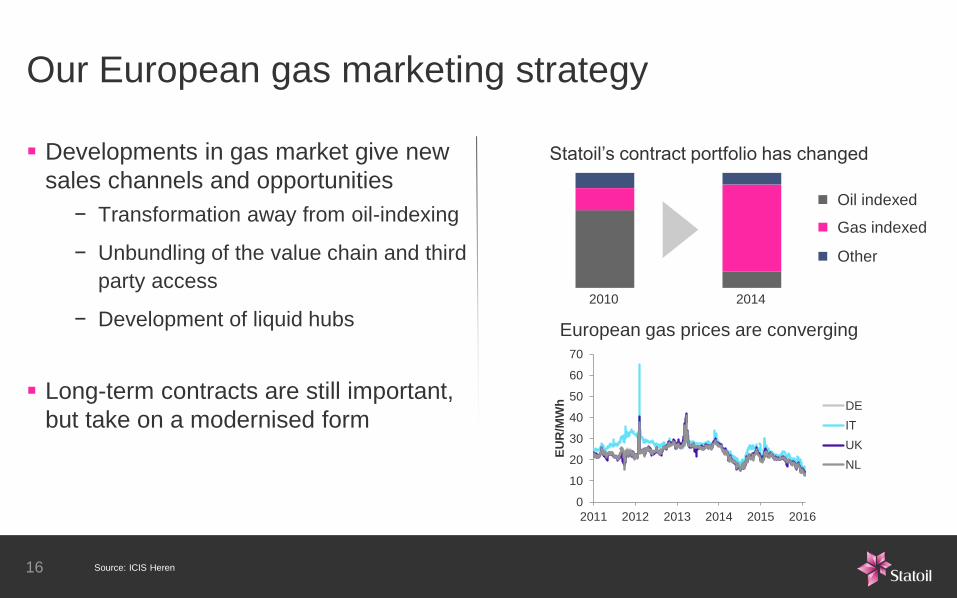

Our European gas marketing strategy

Developments in gas market give new

sales channels and opportunities

− Transformation away from oil-indexing

− Unbundling of the value chain and third

party access

− Development of liquid hubs

Long-term contracts are still important,

but take on a modernised form

European gas prices are converging

Statoil’s contract portfolio has changed

2010 2014

Oil indexed

Gas indexed

Other

0

10

20

30

40

50

60

70

2011 2012 2013 2014 2015 2016

EU

R/M

Wh DE

IT

UK

NL

16 Source: ICIS Heren

JKM Shipping HH Shipping/Regas NBP

Asia USD/MMBtu

Europe USD/MMBtu

North America USD/MMBtu

3.0*

0.5

5.0 - 5.7 4.3 - 4.7

Currently in “the money” in Europe

0.8 - 1.21.5 – 2.2

Short-run marginal cost ranges for US 2017 LNG supply to Asia and Europe

5.4**

US LNG will flow according to price signals

* NYMEX Henry Hub Forward curve for Calendar 2017 22 Aug 2016

** ICE NBP Forward curve for Calendar 2017 22 Aug 2016

Source: NYMEX, ICE, Platts, Pira, Statoil ASA17

Brazil’s Santos basin

Accessing an excellent resource base

One of the most prolific

petroleum systems in the world

53 billion bbl already discovered*

Estimated 36 billion bbl YTF*

Excellent reservoir properties

Very high producibility

* Source: IHS18

The BM-S-8 licence

Accessing an excellent resource base

Carcará discovery:

More than 300m

hydrocarbon column

High net/gross reservoir

High porosity and permeability

High resource density

1 remaining drill stem test

Contract signature

3D seismic acquisition

Carcará-1 high impact oil discovery

Two Carcará appraisal wells and

one DST

Statoil farm-in/operatorship

Declaration of commerciality

2000 2002 2012 2015 2016 2018

19

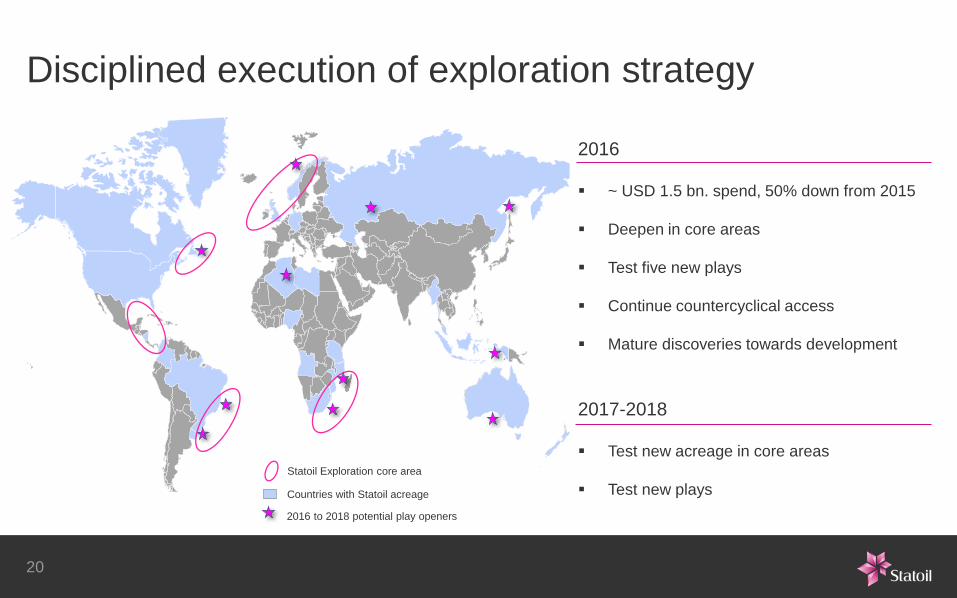

BM-S-8 licence:

Considerable exploration upside

Remaining commitments: 1 well

Statoil Exploration core area

Countries with Statoil acreage

2016 to 2018 potential play openers

2016

~ USD 1.5 bn. spend, 50% down from 2015

Deepen in core areas

Test five new plays

Continue countercyclical access

Mature discoveries towards development

2017-2018

Test new acreage in core areas

Test new plays

Disciplined execution of exploration strategy

20

Outlook 2016

Capex USD ~11 bn1)

Production ~1% organic CAGR (2014-17)

Maintenance60 mboe per day

40 mboe per day in 4Q

Exploration USD ~1.5 bn1)

Dividend 3Q16USD 0.2201 per share, with 5%

discounted scrip dividend option

21 1) Assuming NOK/USD of 8.50

Johan Castberg

Alta/Gotha

Snøhvit

Goliat

Wisting

Honningsvåg

Alta

Tromsø

Vardø

Kirkenes

VadsøHammerfest

Harstad

Gas pipeline

Statoil operator

Other leases

Statoil partner

Oil

Gas

Oil w/gas Other 23rd licensing round awarded areas

Statoil partner 23rd licensing round awarded areas

Statoil 23rd licensing round awarded areas

Kayak

Korpfjell

Gemini North

Koigen Central

Blåmann

2017 – the Year of the North

23

Opportunities in European gas markets

Europe has a large and growing supply gap

Norwegian gas is well placed as a cost-efficient supply source for the long term

Due to its cleanness and versatility, gas will remain a key part of European energy supply

Outlook for Norwegian gas productionOutlook for EU demand and indigenous supply

0

100

200

300

400

500

600

2012 2020 2025 2030

Norway

Indigenous

EC reference

EC 2030 policies

IEA WEO 2015

Import needs

24 Sources: IEA, European Commission, Norwegian Petroleum Directorate

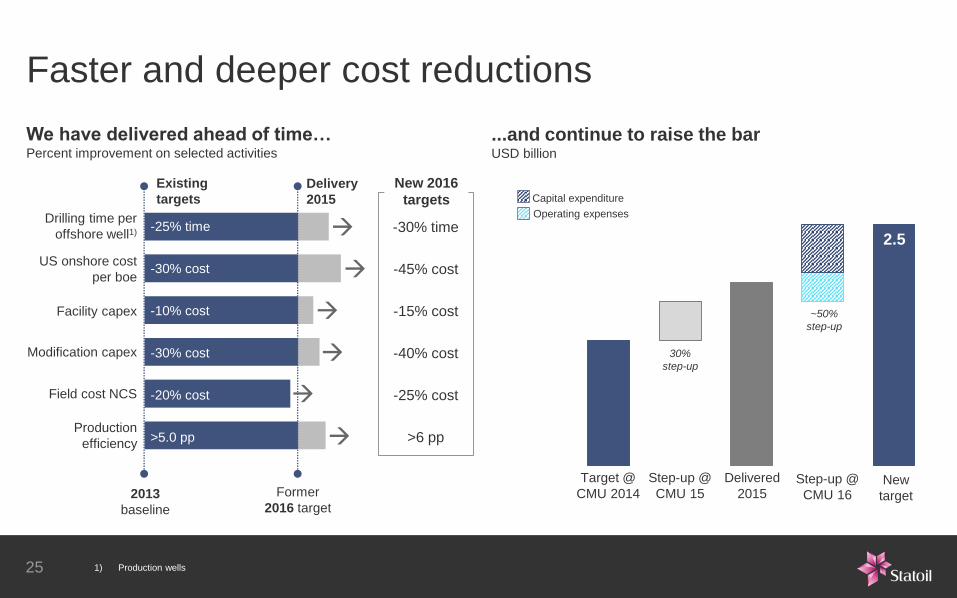

Faster and deeper cost reductions

...and continue to raise the barUSD billion

We have delivered ahead of time…Percent improvement on selected activities

-25% time

-30% cost

-10% cost

-30% cost

-20% cost

>5.0 pp

Drilling time per

offshore well1)

US onshore cost

per boe

Facility capex

Modification capex

Field cost NCS

Production

efficiency

Existing

targets

Delivery

2015

2013

baseline

Former

2016 target

-30% time

-45% cost

-15% cost

-40% cost

-25% cost

>6 pp

New 2016

targets

2.51.9

Capital expenditure

Operating expenses

1.3

Target @

CMU 2014

Step-up @

CMU 15

Delivered

2015New

target

~50%

step-up

Step-up @

CMU 16

30%

step-up

25 1) Production wells

Capitalising on market opportunities

Examples of achieved

rate reductions in contracts 1)

Expected reduction in capex and opex

due to market effects 2) (USD billion)

0% 10% 20% 30%

Equipment

Subsea

Marine installation

Engineering

Steel/Raw materials

Operations & maintenance

Drilling & well services

0.0

0.5

1.0

2015 2016 2017

26 1) Reduction measured in USD (includes currency effects)

2) Excludes currency impact. Statoil share, Statoil operated spend only.