STATISTICAL REPORT - Fuels Europe · Statistical Report 2015 55 ... ril anging from transportatoni...

60

STATISTICAL REPORT

Transcript of STATISTICAL REPORT - Fuels Europe · Statistical Report 2015 55 ... ril anging from transportatoni...

STATISTICAL REPORT

Editor: John Cooper Copyright © FuelsEurope

Printed in Belgium - Designed by www.morris-chapman.com

STATISTICAL REPORT

#FuelsEurope

www.fuelseurope.eu

FuelsEurope

5Statistical Report 2015 5

Welcome to the FuelsEurope’s Statistical Report 2015, our second such report.

While the statistics were originally included in Annual Reports, the 2015 Statistical Report follows the same structure as 2014 edition thus ensuring a consistent historical overview for our readers.

The Report aims to provide high-quality data on energy markets in general but also on refining industry specific issues. Selected charts give readers a broad overview of energy and environment related data and trends over recent years.

FuelsEurope’s Statistical Report 2015 uses the following colour coding to help navigation easily through the document. Each colour corresponds to a specific oil-related theme making browsing between subsections user-friendly. We hope that you find this Report useful.

• Oil & Energy

• Oil Products

• Prices and Margins

• Refining

• Marketing Infrastructures

Foreword

John CooperDirector General

Statistical Report 20156

World

European Union33%

24%

30%

4%

7% 2%

Mtoe

36%

24%

17%

12%

5% 7%

:Uni

t: M

toe

5 000

4 500

4 000

3 500

3 000

2 500

2 000

1 500

1 000

500

0

Oil

4 185

605394 285 199 82 111

3 020

3 827

563856

279

Natural gas

Coal Nuclear energy

Hydro electricity

Renewables

Oil consumption is measured inmillion tonnes; other fuels inmillion tonnes of oil equivalent (Mtoe).

EU1 676 Mtoe

WORLD:12 730 Mtoe

Note: Please note that due to rounding, figures may not add up exactly to 100%

FIG.1 WORLDWIDE ENERGY CONSUMPTION BY FUEL TYPE IN 2013

Oil, natural gas and coal currently meet the world’s energy needs (together 86.8%). The overall share for renewables remains very small (8.5%). The EU, unlike other major economies, has a

higher share of nuclear (12%) and renewables & hydro (12%) in its energy mix.

Source: BP Statistical Review of World Energy 2014

7Statistical Report 2015 7

20% USA 12% USA

14% EU-28

7% EU-28

5% JAPAN

3% JAPAN

4% RUSSIA

12% RUSSIA

2% RUSSIA

12% CHINA 50% CHINA

4% INDIA

8% INDIA

41% OTHERS

43% OTHERS

16% OTHERS

OIL COAL

NATURAL GAS

Total energy3 020 Mtoe

Uni

t: M

toe

Total energy4 185 Mtoe 3 827 Mtoe

Total energy

22% USA

2% INDIA

5% CHINA

3% JAPAN

13% EU-28

World

European Union33%

24%

30%

4%

7% 2%

Mtoe

36%

24%

17%

12%

5% 7%

:Uni

t: M

toe

5 000

4 500

4 000

3 500

3 000

2 500

2 000

1 500

1 000

500

0

Oil

4 185

605394 285 199 82 111

3 020

3 827

563856

279

Natural gas

Coal Nuclear energy

Hydro electricity

Renewables

Oil consumption is measured inmillion tonnes; other fuels inmillion tonnes of oil equivalent (Mtoe).

EU1 676 Mtoe

WORLD:12 730 Mtoe

Note: Please note that due to rounding, figures may not add up exactly to 100%

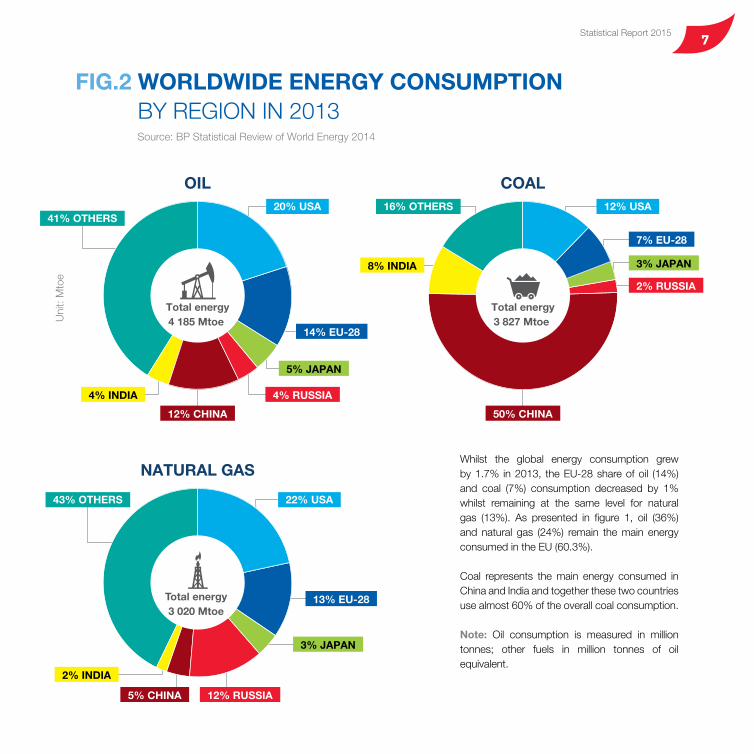

Whilst the global energy consumption grew by 1.7% in 2013, the EU-28 share of oil (14%) and coal (7%) consumption decreased by 1% whilst remaining at the same level for natural gas (13%). As presented in figure 1, oil (36%) and natural gas (24%) remain the main energy consumed in the EU (60.3%).

Coal represents the main energy consumed in China and India and together these two countries use almost 60% of the overall coal consumption.

Note: Oil consumption is measured in million tonnes; other fuels in million tonnes of oil equivalent.

Source: BP Statistical Review of World Energy 2014

FIG.2 WORLDWIDE ENERGY CONSUMPTION BY REGION IN 2013

Statistical Report 20158

Uni

t: M

illion

tonn

es p

er y

ear

32.3

23.8

25.0

154.5

24.7

45.6

52.6

30.631.5

53.026.8

18.2

16.5

227.2

83.8

USA

SOUTH AND CENTRAL AMERICA

CANADA

EUROPE & EURASIA

AFRICA

ASIA PACIFIC

TRADE FLOWS IN 2013

MEXICO

MIDDLE EAST

100.1

74.1

72.9

28.7

102.6164.2

153.9

53.0124.6

24.4

295.0 19.1

43.4

31.5

25.3

56.9

38.5

19.5

16.7

17.4

Crude oil is an internationally traded commodity with flows moving all over the world.

There are two open and transparent markets – crude oil and refined products- within which the European refining industry operates. The products are freely traded.

Source: BP Statistical Review of World Energy 2014

FIG.3 WORLDWIDE CRUDE OIL MOVEMENT IN 2013

9Statistical Report 2015 9

26% NORTH AMERICA

7% SOUTH AND CENTRAL AMERICA

4% RUSSIA

MIDDLE EAST 9%

AFRICA 4%

CHINA 12%

OTHER ASIA PACIFIC 13%

EURASIA 1%

JAPAN 5%

INDIA 4%

15% EUROPEof which EU: 13.6% and Non EU: 1.4%

Total91.34 Mbd

Uni

t: M

illion

tonn

es p

er y

ear

32.3

23.8

25.0

154.5

24.7

45.6

52.6

30.631.5

53.026.8

18.2

16.5

227.2

83.8

USA

SOUTH AND CENTRAL AMERICA

CANADA

EUROPE & EURASIA

AFRICA

ASIA PACIFIC

TRADE FLOWS IN 2013

MEXICO

MIDDLE EAST

100.1

74.1

72.9

28.7

102.6164.2

153.9

53.0124.6

24.4

295.0 19.1

43.4

31.5

25.3

56.9

38.5

19.5

16.7

17.4

FIG.4 WORLDWIDE REFINED PRODUCT DEMAND AVERAGED 91.34 MILLION BARRELS PER DAY IN 2013, WITH EUROPE ACCOUNTING FOR 15%Source: BP Statistical Review of World Energy 2014

Global demand for oil refined products continues to grow from 86.77 million barrels per day in 2012 to 91.34 in 2013. Although the European market is declining it still remains

the second largest in the world (15%) behind North-America (26%), but with China, Middle East and the rest of Asia catching rapidly.

Statistical Report 201510

Uni

t: M

illion

tonn

es p

er y

ear

162 209

651 701

501 520

343 396

286143

117 175

703 731

269 340

993 1 030

REFINERY THROUGHPUT REFINED PETROLEUM PRODUCTS DEMAND

NORTHAMERICA

AFRICA

RUSSIA

ASIA &OCEANIA

CHINAJAPAN

EUROPE

LATINAMERICA

MIDDLE EAST

The refining supply/market demand balance shows that most of the regions are dependent on imports to meet market demand. Russia and at a lesser extent China has a positive trade balance which provides Russia in particular a key role in supplying demand from other regions.

Apparently balanced product demand and refinery throughput in the EU hide a large surplus of EU gasoline production and a shortage of diesel and jet production.

Source: Wood Mackenzie

FIG.5 WORLDWIDE REFINING SUPPLY/MARKET DEMAND BALANCES IN 2014

11Statistical Report 2015 11

Uni

t: M

illion

tonn

es p

er y

ear

NON EU

EU

Austria

Belgium

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Latvia

Lithuania

Luxembourg

Malta

Netherlands

Poland

Portugal

Romania

Slovakia

Slovenia

Spain

Sweden

United Kingdom

12.6

COUNTRY Mt/y COUNTRY Mt/y

28.9

4.5

3.3

2.7

9.1

7.3

1.5

9.3

81.2

115.1

13.2

6.3

6.6

60.8

1.7

2.5

2.7

2.6

47.2

23.9

10.9

9.7

3.6

2.4

60.0

13.3

68.6

Norway

EU TOTAL 611.4

TOTAL NO + CH + TR 57.3

TOTAL 668.7

Switzerland

Turkey

10.3

11.1

35.9

Uni

t: M

illion

tonn

es p

er y

ear

162 209

651 701

501 520

343 396

286143

117 175

703 731

269 340

993 1 030

REFINERY THROUGHPUT REFINED PETROLEUM PRODUCTS DEMAND

NORTHAMERICA

AFRICA

RUSSIA

ASIA &OCEANIA

CHINAJAPAN

EUROPE

LATINAMERICA

MIDDLE EAST

FIG.6 EU TOTAL OIL DEMAND AMOUNTED TO 611 MILLION TONNES IN 2014Source: Wood Mackenzie

EU-28 total oil amounted to 611 MT for 2014, representing a decrease of 3.3% compared to 2013.

While the bigger Member States such as Germany (-1.6%), France (-1.1%), UK (-2.4%) witnessed a decrease close to the European average, the Member States hit by the Eurozone crisis recorded a more significant decrease - Greece (-13.6%); Italy (-6.5%); Spain (-5.2%).

Statistical Report 201512

LPG

GASOLINE

OTHER PRODUCTS

REFINERY FUEL & LOSS

JET/KEROSENE

NAPHTHA

DIESEL/GASOIL

FUEL OIL

Uni

t: M

illion

tonn

es p

er y

ear

800

700

600

500

400

300

200

100

0

2013 2014

53.3

270.3

53.7

48.7

80.426.7

50.128.2

201220112010200920082007200620052004

FIG.7 DEMAND HISTORY OF OIL PRODUCTS IN THE EUSource: Wood Mackenzie

Since 2009, we can observe a downward trend for oil products demand. Over the past 5 years, the overall demand has declined by 8%. The downward trend is mainly driven by the decrease in gasoline (-17%) whilst gasoil and kerosene only decreased by 3%.

13Statistical Report 2015 13

1.3% LUBRICANTS

0.2% WHITE SPIRITS

REFINERY GAS AND ETHANE 3.4%

LPG 2.5%

5.7% NAPHTHA

GASOLINE 19.2%

39% DIESEL/GASOIL

13.0% FUEL OIL

BITUMEN 3.4%

1.4% PETROLEUM COKE

OTHER PRODUCTS 4%

6.8% KEROSENE

0.1% PARAFFIN WAXES

LPG

GASOLINE

OTHER PRODUCTS

REFINERY FUEL & LOSS

JET/KEROSENE

NAPHTHA

DIESEL/GASOIL

FUEL OIL

Uni

t: M

illion

tonn

es p

er y

ear

800

700

600

500

400

300

200

100

0

2013 2014

53.3

270.3

53.7

48.7

80.426.7

50.128.2

201220112010200920082007200620052004

FIG.8 AVERAGE REFINERY OUTPUT BY PRODUCT TYPE IN OECD EUROPESource: OECD

A wide range of products are produced from crude oil, ranging from transportation and industrial fuels to chemical feedstock. EU refineries produce also many specialty products such as bitumen for road construction and roofing, lubricants

for transport and industry, petroleum coke for the metal industry as well as waxes, solvents and other specialised products. Fuels for transport represent the biggest share of the production.

Statistical Report 201514

GASOLINE DIESEL RATIO

Uni

t: M

illion

tonn

es p

er y

ear

Die

sel/G

asol

ine

ratio

0,5

1,0

1,5

2,0

2,5

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

FIG.9 ROAD FUEL DEMAND IN THE EUSource: Wood Mackenzie

The tax-incentivised dieselisation trend has significantly contributed to a fundamental change in the EU road fuel demand structure. The shift from gasoline to diesel began some 25 years ago and led to major gasoline demand decline as well as a shortage of diesel production in the EU.

Gasoline demand continue to decline while diesel demand is on the rise, currently reaching a 2.5 demand ratio in 2014.

15Statistical Report 2015 15

GASOLINE DIESELUnit: Million tonnes per year

- - 5 10 15 20 25 30 35 5 10 15 20

France17.4% 82.6%63.5%36.5% Germany

64.4%35.6% United Kingdom73.7%26.3% Italy

81.1%18.9% Spain73.6%26.4% Poland

63.1%36.9% Netherlands83.8%16.2% Belgium

78.2%21.8% Austria32.1% 67.9%Sweden

21.3% 78.7%Portugal30.2% 69.8%Czech Republic

27.3% 72.7%Romania36.5% 63.5%Finland34.2% 65.8%Hungary

32.8% 67.2%Ireland37.3% 62.7%Denmark

55.6% 44.4%Greece

15.0% 85.0%Luxembourg22.4% 77.6%Bulgaria

26.1% 73.9%Slovakia25.9% 74.1%Slovenia35.4% 64.6%Croatia17.2% 82.8%Lithuania26.8% 73.2%Latvia30.5% 69.5%Estonia48.8% 51.2%Cyprus44.8% 55.2%Malta

GASOLINE DIESEL RATIO

Uni

t: M

illion

tonn

es p

er y

ear

Die

sel/G

asol

ine

ratio

0,5

1,0

1,5

2,0

2,5

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: Wood Mackenzie

FIG.10 ROAD FUEL DEMAND IN THE EU BY COUNTRY IN 2014

Spurred on by favourable excise taxes on diesel, the shift from gasoline to diesel over past two decades led to a higher demand for diesel than gasoline as a road fuel in the vast majority of EU Member States.

In some countries, such as France and Spain the imbalance is far more pronounced as a result of very favourable tax policies for diesel.

The continued growth in truck transport in the EU, driven by internal market and external trade, has further contributed to spurring diesel demand.

Statistical Report 201516

GASOLINE

DIESEL/GASOIL

JET FUEL

Uni

t: pe

rcen

tage

impo

rts

/ pe

rcen

tage

exp

orts

Net gasoline exports:45 796 ktonnes

Net gasoil imports:22 672 ktonnes

Net jet fuel imports:15 218 ktonnes-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: Eurostat

FIG.11 NET TRADE FLOWS FOR REFINED PRODUCTS DEMONSTRATE THE TREND OF GROWING GASOLINE SURPLUS AND DIESEL / GASOIL / JET FUEL DEFICITS

The EU has significant excess gasoline production capacity, but is however unable to meet regional demand for diesel and jet fuel.

17Statistical Report 2015 17

18.6

14.7

18.0

5.9

6.011.2

NORTHAMERICA

AFRICA

RUSSIA

ASIA

ASIA

Uni

t: M

illion

tonn

es p

er y

ear

GASOLINE DEMAND IN 2013

DIESEL/GASOIL DEMAND IN 2013

MAIN GASOLINE TRADE FLOWS IN 2013

MAIN DIESEL/GASOIL TRADE FLOWS IN 2013

77.8 253.7

EU

Source: Eurostat

FIG.12 MAJOR GASOLINE AND DIESEL/GASOIL TRADE FLOWS TO AND FROM THE EU IN 2013

As a result of the gasoline/diesel imbalance demand Europe has significant excess gasoline production capacity that need to be exported, while to meet regional demand for diesel and jet fuel, Europe became heavily reliant on other countries for import, especially from Russia, Middle East & USA.

North America was the traditional market for exporting gasoline surplus but the recent shale oil revolution, cheap energy and reducing demand have enabled US refiners to increase their supplies for the internal market and to compete on other export markets with EU refiners.

Statistical Report 201518

EUROPE NON EU

REST OF THE WORLD

USA

Note: Please note that due to rounding, figures may not add up exactly to 100%

Unit: Million tonnes per year

500 10 155 20 25 30 35 40 45

EXPORT

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2013

17%

14%

11%

10%

9%

13%

10%

9%

7%

10%

11%

21%

22%

32%

34%

42%

44%

51%

57%

61%

56%

58% 32%

33%

33%

33%

39%

43%

49%

56%

57%

64%

62%

Source: Eurostat

FIG.13 EU GASOLINE TRADING BALANCE: USA IS A KEY EXPORT MARKET FOR THE EU

The US was the traditional export market for the structural EU gasoline surplus. The recent shale oil boom has decreased export opportunities to the US and forced EU refiners to find other markets.

The EU gasoline surplus in 2013 decreased by 8% compared to 2012. Comparatively the share of the US has decreased from 43% in 2008 to 32% in 2013 of the total exports.

19Statistical Report 2015 19

EUROPE NON EU

REST OF THE WORLD

USA

Note: Please note that due to rounding, figures may not add up exactly to 100%

Unit: Million tonnes per year

500 10 155 20 25 30 35 40 45

EXPORT

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2013

17%

14%

11%

10%

9%

13%

10%

9%

7%

10%

11%

21%

22%

32%

34%

42%

44%

51%

57%

61%

56%

58% 32%

33%

33%

33%

39%

43%

49%

56%

57%

64%

62%

Unit: Million tonnes per year

EXPORTIMPORT

NORTH AMERICA

RUSSIA

REST OF THE WORLD

40 30 20 10 0 10 20

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

201344%

48.8%

43.6%

27.1%

35.1%

35.9%

56%

51.2%

56.4%

72.9%

64.9%

64.1%

94%6%

91.5%8.5%

88.3%1.5%10.3%

90.2%9.8%

100%

Note: Please note that due to rounding, figures may not add up exactly to 100%

Source: Eurostat

FIG.14 EU GASOIL TRADING BALANCE: RUSSIA IS A LEADING EXPORTER OF GASOIL TO THE EU

Major growth of US diesel exports to EU. EU increasingly dependent upon imported diesel, exporting lower quality gasoil.

Statistical Report 201520

Unit: Million tonnes per year

EXPORTIMPORT

REST OF THE WORLD

MIDDLE EAST

EUROPE NON EU

20 15 10 5 0 5

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

201339% 61%

38% 62%

38% 62%

36% 64%

51% 49%

51% 49%

27% 73%

35% 65%

37% 63%

26%

23%

74%

77%

Source: Eurostat

FIG.15 EU JET FUEL TRADING BALANCE: MIDDLE EAST REMAINS MAIN JET FUEL SUPPLIER FOR THE EU

Growing EU dependence on jet fuel imported mainly from Middle East.

21Statistical Report 2015 21

FUEL OIL

GASOIL

FUEL OIL

GASOILUni

t: C

onsu

mpt

ion

(1,0

00 to

nnes

)U

nit:

Con

sum

ptio

n (1

,000

tonn

es)

2004 2006 2008 2010 2012 2014

2004 2006 2008 2010 2012 2014

0

10 000

20 000

30 000

40 000

50 000

60 000

0

50 000

100 000

150 000

200 000

250 000

Unit: Million tonnes per year

EXPORTIMPORT

REST OF THE WORLD

MIDDLE EAST

EUROPE NON EU

20 15 10 5 0 5

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

201339% 61%

38% 62%

38% 62%

36% 64%

51% 49%

51% 49%

27% 73%

35% 65%

37% 63%

26%

23%

74%

77%

Source: Wood MackenzieFIG.16b MARINE FUEL CONSUMPTION IN THE EU

Switch to LNG or the use of scrubbers are alternatives to new IMO emissions limits in 2020 or 2025.

Source: Wood MackenzieFIG.16a GLOBAL MARINE FUEL CONSUMPTION

The global demand for marine fuel is mainly met by fuel oil (85%) while gasoil only represents 15% of the market.

The new limits for sulphur content of marine fuels could drastically change the market with a massive demand for low sulphur distillates, requiring major refinery investments.

Statistical Report 201522

max

. sul

phur

con

tent

(ppm

)m

ax. s

ulph

ur c

onte

nt (p

pm)

6000

5000

4000

3000

2000

1000

01975 1980 1985 1990 1995 2000 2005 20142010

6000

5000

4000

3000

2000

1000

01975 1980 1985 1990 1995 2000 2005 20142010

The sulphur content of road fuels has been reduced from 5500 ppm in 1975 to sulphur free in 2010 allowing use of sophisticated emissions control by vehicles.

In addition to the environmental benefits arising from reduced sulphur dioxide (SO2), the use of 10ppm sulphur gas oil is also essential for the effective working of abatement technology in engines fitted in newer non-road mobile machinery, including tractors, which are manufactured to meet stringent new EU emission standards for oxides of nitrogen (NOX).

Source: PFC Energy

Source: PFC Energy

FIG.17a EU ROAD DIESEL SULPHUR SPECIFICATIONS

FIG.17b EU OFF-ROAD DIESEL SULPHUR SPECIFICATIONS

23Statistical Report 2015 23

max

. sul

phur

con

tent

(ppm

)m

ax. s

ulph

ur c

onte

nt (p

pm)

6000

5000

4000

3000

2000

1000

01975 1980 1985 1990 1995 2000 2005 20142010

6000

5000

4000

3000

2000

1000

01975 1980 1985 1990 1995 2000 2005 20142010

The following areas impose limits on the sulphur level of fuel in ships travelling within them.

Changes in shipping fuel specifications require large-scale industry investment, by shipping and fuels supply industries.

The new 0.10% marine fuel will be difficult to produce from fuel oil and be met by marine diesel, a lighter product or potentially by LNG.

Secondary technology such as scrubbers can also be used to meet these sulphur levels but this technology is not suitable for our ships.

FIG.18 MARINE FUEL SULPHUR SPECIFICATIONS SO2 EMISSION CONTROL AREAS (SECAs)Source: European Commission

SECAs cover the Baltic and North Seas and the English Channel

Limits for the sulphur content of marine fuels in SECAs: 1% until 31 December 20140.10% as from 1 January 2015

Limits for the sulphur content of marine fuels outside SECAs in the EU waters: 0.50% by 2020

Statistical Report 201524

PM2.5 Overall transport emissions

PM2.5 Exhaust emissions

PM10 Overall transport emissions

PM2.5 PM10

PM10 Exhaust emissions

0

50

100

150

200

250

300

350

400

1990 1996 2002 2008 20120

50

100

150

200

250

300

350

400

1990 1996 2002 2008 2012

Uni

t: G

igag

ram

s (G

g)

FIG.19a PM EMISSIONS FROM EXHAUST IN THE EU REDUCED BY OVER 50%Source: European Environment Agency

PM emissions are continuously decreasing as the result of cleaner diesel fuel, advanced engines and effective emissions control technology.

With the EURO6 standard, modern road vehicles with diesel engines are using highly efficient filters that remove over 99.9% of the number of PMs.

25Statistical Report 2015 25

0

1000

2000

3000

4000

5000

6000

1990 2000 2012

NMVOC

0

5000

10000

15000

20000

25000

30000

35000

1990 2000 2012

CO

0

1000

2000

3000

4000

5000

6000

7000

8000

1990 2000 2012

NOx

SOx

0

100

200

300

400

500

600

700

1990 2000 2012

Uni

t: G

igag

ram

s (G

g)

PM2.5 Overall transport emissions

PM2.5 Exhaust emissions

PM10 Overall transport emissions

PM2.5 PM10

PM10 Exhaust emissions

0

50

100

150

200

250

300

350

400

1990 1996 2002 2008 20120

50

100

150

200

250

300

350

400

1990 1996 2002 2008 2012

Uni

t: G

igag

ram

s (G

g)

FIG.19b SINCE 1990 FUELS ARE GETTING PROGRESSIVELY CLEANER RESULTING IN SIGNIFICANT EMISSIONS REDUCTIONSSource: European Environment Agency

NOx - Nitrogen OxidesSOx - Sulphur Oxides NMVOC - Non Methane Volatile Organic CompoundsCO - Carbon Monoxide

Since 1990 the refining industry has contributed to cleaner exhausts by containing today over 80% lower SOx, NMVOC & CO, while NOx emissions decreased by over 50%. These significant improvements are the result of the partnerships with the automotive industry aiming at improving the fuel-engine efficiency and leading to multiple environmental benefits.

Statistical Report 201526

10 - 15 PPM 16 - 50 PPM 51 - 350 PPM

351 - 500 PPM 501 - 2000 PPM >2000 PPM

FIG.20 MAXIMUM ON-ROAD DIESEL SULPHUR LIMITSSource: Hart Energy Research and Consulting, 2014

Europe together with USA, Canada, Japan, Australia and Chile apply the lowest (10-15 ppm) on-road diesel sulphur limits in the world.

Countries may apply lower limits for different grades, regions/cities, or based on average content. Detailed information on limits and regulations can be found at www.ifqc.org

27Statistical Report 2015 27

10 PPM 11 - 99 PPM 100 - 150 PPM

151 - 600 PPM 601 - 2500 PPM

10 - 15 PPM 16 - 50 PPM 51 - 350 PPM

351 - 500 PPM 501 - 2000 PPM >2000 PPM

FIG.21 MAXIMUM GASOLINE SULPHUR LIMITSource: Hart Energy Research and Consulting, 2014

The EU has set the most stringent environmental specifications for sulphur in gasoline worldwide with a maximum level of 10 PPM.

Countries may apply lower limits for different grades, regions/cities, or based on average content. Detailed information on limits and regulations can be found at www.ifqc.org

Statistical Report 201528

Uni

t: U

S D

olla

r pe

r ba

rrel

Eur

ope

Bre

nt s

pot p

rice

per

barr

el in

mon

thly

ave

rage

0

20

40

60

80

100

120

140

160

Jan-

1989

Jan-

1990

Jan-

1991

Jan-

1992

Jan-

1993

Jan-

1994

Jan-

1995

Jan-

1996

Jan-

1997

Jan-

1998

Jan-

1999

Jan-

2000

Jan-

2001

Jan-

2002

Jan-

2003

Jan-

2004

Jan-

2005

Jan-

2006

Jan-

2007

Jan-

2008

Jan-

2009

Jan-

2010

Jan-

2011

Jan-

2012

Jan-

2013

Jan-

2014

REAL PRICE (2014$)

NOMINAL PRICE

The EU Refining industry operates between two global, open and transparent markets: the market of crude oil and the market of refined products. The main benchmarks are priced in dollars.

The price of crude oil is set on international spot markets and reported by designated agencies. The price of oil is an important marker for the global economy and is closely watched by businesses and policy-makers.

After a decade of relatively low prices, oil started rising last decade, leading to peaks just before the financial crisis in 2008. In the summer of 2014, oil prices started to fall, reaching daily closing prices of below 50 $.

FIG.22 CRUDE OIL PRICE EVOLUTIONSource: Energy Information Administration

29Statistical Report 2015 29

Net Cash Margin in US $/bbl for all regions indexed relative to 100 in Year 2000

Inde

xed

Net

Cas

h M

argi

n U

SD

/bbl

700

600

500

400

300

200

100

0

-100

2000 2002 2004 2006 2008 2010 2012

US Gulf Coast

Middle East

Korea/Singapore

EU - 28

Uni

t: U

S D

olla

r pe

r ba

rrel

Eur

ope

Bre

nt s

pot p

rice

per

barr

el in

mon

thly

ave

rage

0

20

40

60

80

100

120

140

160

Jan-

1989

Jan-

1990

Jan-

1991

Jan-

1992

Jan-

1993

Jan-

1994

Jan-

1995

Jan-

1996

Jan-

1997

Jan-

1998

Jan-

1999

Jan-

2000

Jan-

2001

Jan-

2002

Jan-

2003

Jan-

2004

Jan-

2005

Jan-

2006

Jan-

2007

Jan-

2008

Jan-

2009

Jan-

2010

Jan-

2011

Jan-

2012

Jan-

2013

Jan-

2014

REAL PRICE (2014$)

NOMINAL PRICE

FIG.23 REFINERS’ NET CASH MARGIN ACROSS REGIONSSource: Concawe

Statistical Report 201530

Uni

t: U

S D

olla

r pe

r ba

rrel

(Nom

inal

)

GASOLINE PRICE (NW EUROPE, 95R)

CRUDE OIL PRICE (BRENT)

0

20

40

60

80

100

120

140

1998 2000 2002 2004 2006 2008 2010 2012 2014

FIG.24 REFINERS OPERATE BETWEEN TWO GLOBAL COMMODITY MARKETSSource: Wood Mackenzie & Argus Media

EU refining operates between two global commodity markets, the crude market and the refined products market. The ‘crack spread’ represents the difference between the cost of crude oil and the market sales price for refined products.

Generally product prices rise with crude prices but the drivers of the difference are many.

In historic terms, the profitability has started to decline in a context of falling demand (2008). Whilst 2012 saw a small improvement for refiners, the spread is generally tight- margins are low and the industry is highly vulnerable to the operating costs that must be deducted from the spread before profitability can be considered.

31Statistical Report 2015 31

Uni

t: U

S D

olla

r pe

r ba

rrel

(Nom

inal

)

GASOLINE PRICE (NW EUROPE, 95R)

CRUDE OIL PRICE (BRENT)

0

20

40

60

80

100

120

140

1998 2000 2002 2004 2006 2008 2010 2012 2014

US Gulf Coast

Middle East

Korea/Singapore

EU - 28

0

100

200

300

400

2000 2002 2004 2006 2008 2010 2012

Inde

xed

Cas

h O

PEX

FIG.25 EU CASH OPEX OPERATING YEARS 2000–2012Source: Concawe

Cash OPEX in US $/bbl for all regions indexed relative to 100 in Year 2000

Since 2000, the EU has seen greater operating cost increases than rival areas, leaving them at a competitive disadvantage. In recent years the US Gulf Coast has seen operating costs fall, due largely to cheaper gas from unconventionals.

Statistical Report 201532

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

Baselineopex

ETS IED REACH RED SLFD(MFD)

Estim

ated

cos

t to

EU r

efine

rs ($

/bbl

)

2020 Low costscenario

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

Estim

ated

cos

t to

EU r

efine

rs ($

/bbl

)

Baselineopex

ETS IED REACH RED SLFD(MFD)

2020 High costscenario

FIG.26 ESTIMATED CUMULATIVE COST IMPACT OF EU LEGISLATION IN 2020 ON EU REFININGSource: Concawe

ETS - Emission Trading Scheme (2009/29/EC)IED - Industrial Emission Directive (2010/75/EC)REACH - Registration, Evaluation, Authorisation & Restriction of Chemicals (Regulation 1907/2006)RED - Renewable Energy Directive (2009/28/EC)SLFD - The Sulphur in Liquid Fuels Directive (1999/32/EC)OPEX - Operating Expense

For EU ETS, ‘low cost scenario assumes 16.5 €/t CO2, high cost scenario 30 €/t CO2

This chart provides an estimation of the cost burden imposed on EU refineries over the period from 2010 to 2020 by a number of EU legislative and implementing acts. It shows the cumulative impact in a low and high cost scenario, expressed in dollars per barrel of refinery intake. These estimated costs impacts should be seen in the context of the EU refining net margin which was less than 3 $/bbl in several of the recent years (source: IEA Oil Market Report).

The legislation under consideration has the potential to significantly increase the operating costs of the EU refining industry, thereby impairing its competitive position relative to other world regions where similar legislation is not enacted or is enforced at later dates.

33Statistical Report 2015 33

CH4%

10%8%

4%

7%

3%

5%

3% 3%7%

7%

8%

4%

4%

9%

7%

8%

6%

12%

6%

9%

7%

4%6%

6%6%

3%

COUNTRY SHARE

AT Austria 4%

BE Belgium 3%

BG Bulgaria 12%

HR Croatia 8%

CY Cyprus 7%

CZ Czech Republic 7%

DK Denmark 3%

EE Estonia 9%

FI Finland 4%

FR France 3%

DE Germany 3%

EL Greece 6%

HU Hungary 6%

IE Ireland 6%

IT Italy 4%

LV Latvia 7%

LT Lithuania 8%

LU Luxembourg 7%

MT Malta 5%

NL Netherlands 4%

PL Poland 8%

PT Portugal 6%

RO Romania 9%

SK Slovakia 7%

SI Slovenia 10%

ES Spain 6%

SE Sweden 4%

UK United Kingdom 5%

5%

6% - 10%

HIGHER THAN 10%

EUROPE NON EU

LESS THAN 6%

FIG.27 FUEL TAXES MAKE A SIGNIFICANT CONTRIBUTION TO MEMBER STATE TAX REVENUESource: Eurostat and Wood Mackenzie

Taxes on fuels contribute on average to 7% of Member State tax revenue.

Many competing products are subsidised. Replacing economically viable petroleum products with such alternatives would have large fiscal consequences.

Figures are based on 2012 revenues.

Statistical Report 201534

EU28 + Norway Net Government Revenues and Mandated Transfers

400

350

300

250

200

150

100

50

0

-50

€bn

OIL GAS COAL WIND SOLAR

Government Revenues

Government Expenditure + Mandated Transfers

Total

FIG.28 OIL IS THE LARGEST CONTRIBUTOR TO GOVERNMENT REVENUES, WHILE WIND AND SOLAR POWER ARE NET RECIPIENTS OF TRANSFERS AS A RESULT OF GOVERNMENT POLICIESSource: NERA

Note: Upstream oil and gas revenues allocated in proportion to production value, resulting in slightly higher allocation to oil.

Oil and gas contribute hundreds of billions of euros to European government revenues every year. Far from being subsidised, the oil and gas industry is one of the largest contributors to government revenues in the energy sector.

In 2011 oil and gas contributed €433 billion to the EU and Norwegian government treasuries.

35Statistical Report 2015 35

EU28 + Norway Net Government Revenues and Mandated Transfers

400

350

300

250

200

150

100

50

0

-50

€bn

OIL GAS COAL WIND SOLAR

Government Revenues

Government Expenditure + Mandated Transfers

Total

EU28 + Norway Net Government Revenues and Mandated Transfers per boe (2011):

$ /b

oe

OIL GAS COAL WIND SOLAR

Government Revenues

Government Expenditure + Mandated Transfers

Total

200

0

-200

-400

-600

-800

-1000

FIG.29 PER UNIT OF PRIMARY ENERGY CONSUMPTION OIL, GAS AND COAL ARE NET CONTRIBUTORS TO GOVERNMENT REVENUESSource: NERA

Note: Upstream oil and gas revenues allocated in proportion to production value, resulting in slightly higher allocation to oil.

The consumption of one barrel of oil generates $124 (around €90) in government revenue. This contrasts with the consumption of an equivalent amount of energy generated by renewables, which in some cases can cost tax payers over $700 (or more than €500).

Statistical Report 201536

4954

5058

4959

5559

4756

5157

5357

525756655464

5769

5865

54615364

53575359

5362

5564

6871

6165

6367

5764

5364

4967

4953 5559

PTES

FR

UKNL

BEDE

DK

SE

FI

EE

LV

LT

PL

CZ SK

HUHR

RO

BGIT

GR

MT CY

AT

LU

IE

6267

5461

SI

Euro-Super 95COUNTRY %

United Kingdom 71

Netherlands 69

Italy 67

Greece 67

Slovenia 67

Germany 65

Ireland 65

France 65

Sweden 64

Finland 64

Belgium 64

Portugal 64

64Slovakia

Denmark 62

Czech Republic 61

Croatia 61

Austria 59

Cyprus 59

Lithuania 59

Latvia 58

Hungary 57

Spain 57

Poland 57

Estonia 57

Luxembourg 56

Bulgaria 54

Malta

Romania

53

59

EURO-SUPER 95 ROAD DIESEL OIL

<50%

50-55%

55-60%

>60%

ROAD DIESEL OILCOUNTRY %

United Kingdom 68

Finland

55

Italy 63

Slovenia 62

Ireland 61

France 58

Netherlands 57

Sweden 57

Germany 56

Cyprus 55

Belgium 54

Czech Republic 54

54Croatia

Denmark 53

Portugal 53

Slovakia 53

Hungary 53

Austria 53

Estonia 53

Poland 52

Spain 51

Latvia 50

Greece 49

49Malta

Lithuania 49

Bulgaria 49

Luxembourg

Romania

47

55

FIG.30 TOTAL TAXATION SHARE IN THE END CONSUMER PRICESource: European Commission

The price at the pump is driven to a large degree by taxes and over half the cost of fuel represents taxes. The taxes on gasoline are generally higher than for diesel. This differential tax treatment has driven a demand shift over the past 10 years.

Fuels Taxes contribute substantially to Member State revenues.

Note: Share at February 2015

37Statistical Report 2015 37

Unit: Price in Euro per litrePRODUCT TARIFFS VAT

PRODUCT TARIFFS VAT

0.000 0.200 0.400 0.600 0.800 1.000 1.200 1.400 1.600 1.800

United Kingdom 0.538 0.794 0.267 1.599

Italy 0.580 0.617 0.263 1.460

Sweden 0.627 0.519 0.286 1.432

Finland 0.606 0.463 0.256 1.325

Denmark 0.648 0.419 0.267 1.333

Ireland 0.533 0.499 0.237 1.269

Cyprus 0.603 0.461 0.202 1.265

Netherlands 0.579 0.490 0.224 1.293

Germany 0.564 0.470 0.197 1.231

Greece 0.634 0.341 0.224 1.199

Belgium 0.585 0.429 0.213 1.227

Bulgaria 0.631 0.330 0.192 1.153

Malta 0.642 0.442 0.195 1.280

Slovenia 0.507 0.493 0.220 1.220

Slovakia 0.533 0.406 0.188 1.127

Hungary 0.598 0.368 0.261 1.228

Portugal 0.594 0.402 0.229 1.225

Spain 0.600 0.368 0.203 1.171

Czech Republic 0.549 0.398 0.199 1.146

Austria 0.574 0.410 0.197 1.180

France 0.527 0.481 0.202 1.210

Estonia 0.569 0.393 0.192 1.154

Romania 0.581 0.427 0.242 1.250

Lithuania 0.566 0.330 0.188 1.085

Latvia 0.532 0.346 0.184 1.063

Croatia 0.566 0.373 0.235 1.173

Poland 0.550 0.351 0.207 1.108

Luxembourg 0.584 0.335 0.156 1.075

COUNTRY% of taxes

United Kingdom 66.35%

Italy 60.31%Slovenia 58.47%Ireland 58.02%France 56.41%Sweden 56.22%Netherlands 55.26%Finland 54.28%Germany 54.18%Romania 53.52%Slovakia 52.70%Cyprus 52.37%Belgium 52.30%Czech Republic 52.10%Croatia 51.76%Portugal 51.52%Denmark 51.43%Austria 51.38%Hungary 51.25%Estonia 50.72%Poland 50.38%Latvia 49.92%Malta 49.82%Spain 48.77%Lithuania 47.80%Greece 47.13%Luxembourg 45.68%Bulgaria 45.26%

FIG.31 BREAKDOWN OF AUTOMOTIVE DIESEL PRICES ACROSS EU (DECEMBER 2014)Source: European Commission

Diesel prices are generally lower than gasoline prices due to the lower tax element, with the notable exception of the United Kingdom.

Only a fraction of the price paid at the pump contributes to the refiners’ income, the remainder gain to Member States and to buy the crude oil.

Statistical Report 201538

Unit: Price in Euro per litrePRODUCT TARIFFS VAT

0.000 0.200 0.400 0.600 0.800 1.000 1.200 1.400 1.600

% of taxes

United KingdomNetherlandsItalyGreeceIrelandSloveniaSlovakiaFinlandGermanyFranceSwedenPortugalBelgiumDenmarkCzech RepublicCroatiaAustriaRomaniaLatviaCyprusLithuaniaPolandHungaryEstoniaSpainLuxembourgMaltaBulgaria

COUNTRY

66.98%65.12%64.93%64.43%63.50%63.29%63.28%63.15%63.05%62.57%62.40%61.92%60.93%59.30%58.69%57.92%57.18%56.72%56.26%55.75%55.64%55.53%54.93%54.69%54.48%53.73%50.07%

69.73%

Latvia

Bulgaria

Poland

Estonia

Czech Republic

Lithuania

Luxembourg

Hungary

Austria

Romania

Cyprus

Slovakia

Croatia

Spain

Slovenia

Ireland

Malta

France

Belgium

Germany

Portugal

Sweden

Finland

Greece

Denmark

United Kingdom

Italy

Netherlands 0.515 0.774 0.271 1.560

0.539 0.728 0.279 1.547

0.453 0.794 0.250 1.497

0.584 0.612 0.299 1.495

0.517 0.681 0.275 1.473

0.521 0.624 0.275 1.420

0.530 0.603 0.283 1.415

0.531 0.618 0.264 1.413

0.511 0.655 0.221 1.387

0.526 0.615 0.240 1.381

0.502 0.631 0.227 1.359

0.625 0.519 0.206 1.350

0.473 0.608 0.249 1.329

0.477 0.595 0.236 1.308

0.561 0.462 0.215 1.237

0.509 0.477 0.247 1.233

0.449 0.570 0.204 1.223

0.532 0.490 0.194 1.215

0.519 0.458 0.234 1.212

0.503 0.493 0.199 1.196

0.519 0.400 0.248 1.168

0.527 0.462 0.168 1.157

0.501 0.434 0.196 1.131

0.453 0.467 0.193 1.114

0.498 0.423 0.184 1.105

0.482 0.402 0.203 1.087

0.543 0.363 0.181 1.087

0.465 0.423 0.187 1.075

PRODUCT TARIFFS VAT

FIG.32 BREAKDOWN OF AUTOMOTIVE GASOLINE PRICES ACROSS EU (DECEMBER 2014)Source: European Commission

Gasoline prices are generally higher than diesel prices due to the higher tax element.

Only a fraction of the price paid at the pump contributes to the refiners’ income, the remainder going to Member States and to buy the crude oil.

39Statistical Report 2015 39

Uni

t: th

ousa

nd b

arre

ls d

aily

21 389

6 029 3 517 8 822 31 284

17 861 6 027

e

22.5%North

America

19%Europe +Eurasia

6%Russia

6.5%Latin

America

9%MiddleEast

4%Africa

33%Asia

Pacific

FIG.33 GLOBAL REFINING CAPACITY AS OF 2013Source: BP Statistical Review of World Energy 2014

Refining is spread around the world and is a truly global business. The share of Europe & Eurasia refining has decreased from over

20% in 2012 to 19% in 2013 but still remains the third largest refining region.

Statistical Report 201540

REFINERY LOCATION

STEAM CRACKER LOCATION

INTEGRATED REFINERY / STEAM CRACKER LOCATION

4

3

FIG.34 REFINERY/STEAM CRACKER SITES IN EUROPESource: Concawe

A large number of refineries are integrated with or located very close to steam crackers that produce products for the petrochemicals industry.

Such interconnections show how refining is an intrinsic part of the industrial value chain and provides the basis for highly advance, high value products.

41Statistical Report 2015 41

REFINERY LOCATION

STEAM CRACKER LOCATION

INTEGRATED REFINERY / STEAM CRACKER LOCATION

4

3

EFTAEU

Threshold >50 kbbl/d or 2.5Mt/a

10.2

39.2

5.0

6.7

8.4

8.8

13.2

70.5

102.3

24.0

8.1

Number of refineries

Refining capacity

Refining capacity

Number of refineries

Austria

Belgium

Bulgaria

Croatia

Czech Republic

Denmark

Finland

France

Germany

Greece

Hungary

1

COUNTRY COUNTRY

3

1

2

2

2

2

8

11

4

1

84

10.0

66.0

24.7

16.0

15.0

5.6

70.5

21.6

65.6

Italy

Lithuania

Netherlands

Poland

Portugal

Romania

Slovakia

Spain

Sweden

United Kingdom

10

1

6

2

2

3

1

9

3

6

Norway

EU TOTAL: Refineries = 81 | Refining capacity = 679

TOTAL NO + CH: Refineries = 3 | Refining capacity = 20.7

TOTAL: Refineries = 84 | Refining capacity = 699.7

Switzerland

2

1

17.3

3.4

3.6Ireland 1

FIG.35 84 MAINSTREAM REFINERIES WERE OPERATING IN THE EU, NORWAY AND SWITZERLAND AT END 2014Source: Concawe

At the end of 2014, there are 84 `mainstream` refineries in the EU & EFTA. In addition there were 22 small or speciality sites.

Note: Refining capacity is expressed in million tonnes per year.

Statistical Report 201542

REFINERY THROUGHPUT UTILISATION RATEIDLE CAPACITY

Cap

acity

(milli

on to

nnes

)

Util

isat

ion

rate

2012 2013201120102009200820072006200520042003

600

700

800

62%

74.6%

87.3%

100%

FIG.36 CAPACITY AND UTILISATION OF EUROPEAN REFINERIESSource: BP Statistical Review of World Energy 2014

The utilisation rate of EU refineries dropped from the 2012 levels to about 80%. The continued decrease of demand and evolution

of market demand (increasing diesel/gasoline imbalance) forces European refiners to adapt these market forces.

43Statistical Report 2015 43

REFINERY THROUGHPUT UTILISATION RATEIDLE CAPACITY

Cap

acity

(milli

on to

nnes

)

Util

isat

ion

rate

2012 2013201120102009200820072006200520042003

600

700

800

62%

74.6%

87.3%

100%

31% ENERGY INDUSTRIES

OTHER SECTORS 15%

TRANSPORT 20%

FUGITIVE EMISSIONS 2%FROM FUELS

INDUSTRIAL PROCESSES* 7%

WASTE 3%

AGRICULTURE 10%

12% MANUFACTURINGINDUSTRIES & CONSTRUCTION

FIG.37 GHG EMISSIONS BY SECTOR IN THE EU IN 2012Source: European Environmental Agency

*NOTE: This sector includes by-product or fugitive emissions of greenhouse gases from industrial processes. Emissions from fuel combustion in industry are reported under Energy.

Energy and manufacturing industries accounts for 43% of GHG emissions in the EU. Transport, supplied around 90% by oil refined products, generates 20% of EU GHG emissions.

Statistical Report 201544

ENERGY INDUSTRIES MANUFACTURING, INDUSTRIES & CONSTRUCTIONTRANSPORTRESIDENTIAL

FUGITIVE EMISSIONS FROM FUELS

AGRICULTURE

TOTAL (EXCLUDING LULUCF)

INDUSTRIAL PROCESSES

WASTE

Em

issi

ons

(% o

f 199

0 le

vel)

40

50

60

70

80

90

100

110

120

130

140

1990

(1990=100%)

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

FIG.38 CO2 EMISSIONS TREND BY SECTORSource: European Commission

CO2 emissions per sector are generally all declining since 2007. Industry (processes and manufacturing) CO2 emissions reduced sharply over the period 2007-2012 and are now between 30% and 38% lower than 1990 level.

CO2 emissions from transport are also steadily decreasing since 2007.

45Statistical Report 2015 45

ENERGY INDUSTRIES MANUFACTURING, INDUSTRIES & CONSTRUCTIONTRANSPORTRESIDENTIAL

FUGITIVE EMISSIONS FROM FUELS

AGRICULTURE

TOTAL (EXCLUDING LULUCF)

INDUSTRIAL PROCESSES

WASTE

Em

issi

ons

(% o

f 199

0 le

vel)

40

50

60

70

80

90

100

110

120

130

140

1990

(1990=100%)

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

CO

2 e

mis

sion

s (%

of w

orld

tota

l)

2012

2040

AFRICA

RUSSIA

CHINA

INDIA

LATINAMERICA

REST OFTHE WORLD

MIDDLE EAST

USA

16%11%

EUROPEAN UNION

6%11%

4.5%5%

12%6.5%

5% 6%

5%

3.5%

4%4%

24.5%23.5%

26.5%26%

FIG.39 DECLINING EU SHARE IN GLOBAL CO2 EMISSIONSSource: IEA, WEO 2014

In 2012 the EU accounted for 11% of global CO2 emissions and is expected to account for only 6% by 2040.

Statistical Report 201546

Ene

rgy

cost

as

% o

f tot

al o

pera

ting

cost

Cash operating costs

Trendline

0%

10%

20%

30%

40%

50%

60%

70%

1998 2000 2002 2004 2006 2008 2010 2012

FIG.40 EU REFINERIES’ ENERGY COST AS PERCENTAGE OF TOTAL OPERATING COSTSSource: Concawe

The share of energy costs has continuously increased over the past 20 years to reach in 2012 over 60% of total operating costs.Despite strong records in energy efficiency gains and a leading

position in this field, European refiners suffer a strong competitive disadvantage from these high energy costs.

47Statistical Report 2015 47

Ene

rgy

cost

as

% o

f tot

al o

pera

ting

cost

Cash operating costs

Trendline

0%

10%

20%

30%

40%

50%

60%

70%

1998 2000 2002 2004 2006 2008 2010 2012

1979 1982 1985 1989 1992 1995 1998 2002 2006 2010

1.8

1.6

1.4

1.2

1

0.8

0.6

0.4

0.2

0

SULPHUR EMISSIONS IN RELATION TO REFINERIES’ THROUGHPUT

Uni

t: K

ilo-t

onne

Sul

phur

per

milli

on to

nne

of re

fi ner

y th

roug

hput

Source: Concawe

FIG.41 REFINERY SULPHUR EMISSIONS HAVE BEEN DECLINING OVER THE YEARS

The sulphur emissions from refinery operations decreased by 75% over the past 30 years.

Statistical Report 201548

50

45

40

35

30

25

20

15

10

5

0

140

120

100

80

60

40

20

01969 1974 1978 1981 1984 1987 1990 1993 1997 2000 2005 2008 2010 2012

OIL DISCHARGED WITH AQUEOUS EFFLUENTS (KTONNES/YR)

OIL DISCHARGED PER REPORTED THROUGHPUT (G/TONNE)

Uni

t: O

il in

wat

er d

isch

arge

(kto

nnes

/yr)

Uni

t: O

il di

scha

rged

per

rep

orte

d th

roug

hput

(g/t

onne

)

Over the years the EU Refineries have significantly improved the quality of refinery water effluent.

The amount of oil discharged in effluents from reporting installations continued to decrease to extremely low levels - both in terms of the absolute amount discharged and the amount expressed relative to the volume of feedstock processed (throughput) and the refining capacity of the installations.

FIG.42 QUALITY OF REFINERY WATER EFFLUENT: OIL DISCHARGED IN WATERSource: Concawe

49Statistical Report 2015 49

Total Energy Consumption per tonne (Net input)

Energy intensity index (EII)

Note: the lower the Ell®, the higher the energy efficiency of a refinery

Tota

l Ene

rgy

Con

sum

ptio

n pe

r to

nne

net i

nput

and

Ell

rela

tive

to 1

992

85

90

95

100

105

110

115

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

FIG.43 EU REFINERIES’ ENERGY CONSUMPTION AND EFFICIENCY TRENDS RELATIVE TO 1992Source: Solomon Associates

The index shows that EU refineries have improved their energy efficiency by about 10% over the past 20 years. This improvement was achieved despite more energy intensive refinery operations to produce cleaner fuels and meet shifts

in market demand. The corresponding annual energy saving is roughly equivalent to the total annual average energy consumption of four large EU refineries.

Statistical Report 201550

60%

55%

50%

45%

40%

35%

30%2010200820062004200220001998199619941992

Cogeneration

Overall

EU conventional thermal plants

Ele

ctric

ity g

ener

atio

n ef

ficie

ncy

perc

enta

geFIG.44 ELECTRICITY GENERATION EFFICIENCY

Source: Concawe

Refineries have long recognised the considerable efficiency gains offered by cogeneration, which now accounts for more than 90% of the electricity produced in EU refineries.

As a result the average efficiency of electricity generation in EU refineries is substantially higher than the EU average efficiency of electricity production from the average of conventional thermal plants of the electricity sector.

51Statistical Report 2015 51

60%

55%

50%

45%

40%

35%

30%2010200820062004200220001998199619941992

Cogeneration

Overall

EU conventional thermal plants

Ele

ctric

ity g

ener

atio

n ef

ficie

ncy

perc

enta

ge

Japan

US

OECD Europe

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Q2

FIG.45 EVOLUTION OF END-USER ELECTRICITY PRICES FOR INDUSTRYSource: IEA

(2005 = index 100)

Over the past few years US industry gained a significant competitive advantage as a result of low electricity prices.

While European industry faced a 80% energy price increase between 2005 and 2014, the price of electricity for US industry only increased by 20% over the same period.

Statistical Report 201552

68% Refined products

Natural gas 21%

Renewables 9%2% Coal

FIG.46 RELATIVE CHEMICAL INDUSTRY RAW MATERIAL USESource: CEFIC

The EU Refining sector is closely integrated with the Petrochemical Sector. In 2011, 68% of the petrochemical feedstock relied on refined products, such as naphtha and petroleum gases.

53Statistical Report 2015 53

68% Refined products

Natural gas 21%

Renewables 9%2% Coal

Leat

her

& fo

otw

ear

Agr

icul

ture

& fo

rest

ryC

loth

ing

Woo

d &

woo

d pr

oduc

tsTe

xtile

sFu

rnitu

reA

ccom

odat

ion

& fo

od s

ervi

ces

Food

Fabr

icat

ed m

etal

pro

duct

sC

onst

ruct

ion

Tran

spor

tatio

n &

sto

rage

Non

-met

allic

min

eral

pro

duct

sR

ubbe

r &

pla

stic

sB

asic

met

als

Pap

erW

hole

sale

& re

tail

trad

eW

ater

Min

ing

& q

uarr

ying

Prin

ting

Adm

inis

trat

ive

& s

uppo

rt s

ervi

ces

Rep

air

of m

achi

nery

Oth

er m

anuf

actu

ring

Ele

ctric

al e

quip

men

tM

otor

veh

icle

sB

ever

ages

Oth

er s

ervi

ces

Mac

hine

ry &

equ

ipm

ent n

.e.c

.To

bacc

oC

hem

ical

sO

ther

tran

spor

t equ

ipm

ent

Rea

l est

ate

activ

ities

Ele

ctric

ity &

gas

Com

pute

r, el

ectr

onic

and

opt

ical

Co

ke a

nd r

efi n

ed p

etro

leum

Art

s &

ent

erta

iinm

ent

Adm

inis

trat

ion

Hum

an h

ealth

and

soc

ial w

ork

Fina

ncia

l & in

sura

nce

activ

ities

Pha

rmac

eutic

als

Info

rmat

ion

Per

sona

l, sc

ient

ifi c

and

tech

nica

l act

iviti

esE

duca

tion

80%

60%

40%

20%

0%

HIGH SKILL

MEDIUM SKILL

LOW SKILL

FIG.47 SKILL AND KNOWLEDGE INTENSITIES (% OF TOTAL EMPLOYMENT)Source: European Competitiveness Report 2013

According to the European Commission’s Competitiveness Report for 2013, the European refining industry employs one

of the largest percentages of highly skilled workers of all manufacturing industries, just after the pharmaceutical industry.

Statistical Report 201554

Pha

rmac

eutic

als

Com

pute

rsC

hem

ical

sC

oke

and

pet

role

um p

rod

ucts

Ele

ctric

al e

q.M

achi

nery

and

eq.

n.e

.c.

Bev

erag

esIn

form

atio

n an

d co

mm

unic

atio

nTo

bacc

oO

ther

tran

spor

t eq.

Rub

ber

and

plas

tics

Mot

or v

ehic

les

Oth

er m

anuf

actu

ring

Bas

ic m

etal

sM

anuf

actu

ring

Non

-met

allic

min

eral

pro

duct

sTe

xtile

sP

aper

Furn

iture

Pro

fess

iona

l and

sci

entifi

c a

ctiv

ities

Food

and

drin

kFi

nanc

ial a

ctiv

ities

Ele

ctric

ity a

nd g

asLe

athe

rFa

bric

ated

met

al p

rodu

cts

Rep

air

and

inst

alla

tion

of m

achi

nery

Mar

ket s

ervi

ces

Prin

ting

and

publ

ishi

ngW

ood

Who

lesa

le a

nd re

tail

trad

eR

eal e

stat

e ac

tiviti

esC

loth

ing

Wat

er s

uply

Min

ing

& q

uarr

ying

Con

stru

ctio

nA

dmin

istr

ativ

e an

d su

ppor

t act

iviti

esTr

ansp

ort a

nd s

tora

geA

ccom

odat

ion

and

food

40%

35%

30%

25%

20%

15%

10%

5%

0%

PRODUCT INNOVATION

COKE AND PETROLEUM PRODUCTS

PROCESS INNOVATION

PROCESS INNOVATION

FIG.48 EU REFINING INDUSTRY # 1 PROCESS INNOVATION AND AMONG MOST INNOVATIVE INDUSTRIES FOR PRODUCTSSource: European Competitiveness Report 2013

According to data presented by the European Commission in its annual Competitiveness Report, the EU Refining industry was the leading industrial sector in process innovation and among the top 4 for product innovation.

55Statistical Report 2015 55

Uni

t: N

umbe

r of

pet

rol s

tatio

ns

NON EU

EU

Austria

Belgium

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Latvia

Lithuania

Luxembourg

Malta

Netherlands

Poland

Portugal

Romania

Slovakia

Slovenia

Spain

Sweden

United Kingdom

2 622

COUNTRY END 2014 COUNTRY END 2014

3 386

2 980 **

280 *

3 792

2 007

440 *

1 892

11 356

14 562

6 245

1 914

1 798

21 800

609

238

3 825

6 479

2 709

2 050

857

546

10 712

2 723 *

8 609

Norway

EU TOTAL 114 431

TOTAL NO + CH + TR 17 705

TOTAL 132 136

Switzerland

Turkey

1 602

3 480

12 623 *

* Numbers for 2013

** Numbers for 2012

Source: National Oil Inustry Associations + FPS Economy - DG Energy

FIG.49 NUMBER OF PETROL STATIONS IN EUROPE END OF 2014

There were over 130,000 petrol stations in the EU, Norway, Switzerland and Turkey operating in 2014, fuelling some 230 million cars and over 30 million trucks on Europe’s roads.

Statistical Report 201556

FuelsEurope is a division of the European Petroleum Refiners Association, an AISBL operating in Belgium. This association, whose members are all 42 companies that operate petroleum refineries in the European Economic Area in 2014, is comprised of FuelsEurope and Concawe divisions, each having separate and distinct roles and expertise but administratively consolidated for efficiency and cost effectiveness.

Members account for almost 100% of EU petroleum refining capacity and more than 75% of EU motor fuel retail sales.

FuelsEurope aims to inform and provide expert advice to the EU institutions and other stakeholders about European Petroleum Refining and Distribution and its products in order to:

n Contribute in a constructive way to the development of technically feasible and cost effective EU policies and legislation.

n Promote an understanding amongst the EU institutions and citizens of the contribution of European Petroleum Refining and Distribution and its value chain to European economic, technological and social progress.

About FuelsEurope

57Statistical Report 2015 57

FuelsEurope Members

FuelsEurope

Boulevard du Souverain, 165 I B-1160 Brussels I BelgiumPhone: +32 (0)2 566 9100 I Fax: +32 (0)2 566 9111

www.fuelseurope.eu