State of the airline industry - IATA · Airline Industry Economics Advisory Workshop 2016 1 State...

31

Airline Industry Economics Advisory Workshop 2016 1 State of the airline industry April 2017 Brian Pearce, Chief Economist, IATA www.iata.org/economics

Transcript of State of the airline industry - IATA · Airline Industry Economics Advisory Workshop 2016 1 State...

Airline Industry Economics Advisory Workshop 2016 1

State of the airline

industry

April 2017

Brian Pearce,

Chief Economist,

IATA

www.iata.org/economics

Airline Industry Economics Advisory Workshop 2016 2

Industry profitability peaked a year ago

Source: IATA Economic Performance of the Airline Industry – end year 2016 report IATA Economics www.iata.org/economics

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2011 2012 2013 2014 2015 2016 2017

EBIT

as

% r

even

ues

Quarterly profile for airline industry operating profits (EBIT)

Operating margin 8.3% => 6.6%Net profits$39.6bn => $29.8bn

Airline Industry Economics Advisory Workshop 2016 3

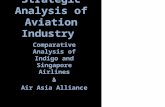

Profit margins are now being squeezed

Source: IATA using data from The Airline Analyst IATA Economics www.iata.org/economics

60

65

70

75

80

85

90

95

100

105

110

0

20

40

60

80

100

120

140

2011 2012 2013 2014 2015 2016 2017

Ind

exed

to

eq

ual

l 1

00

in J

nau

ary

20

11

US$

per

bar

rel

Airline passenger yield (constant fx) and crude oil prices, indexed

Oil price 44.6 => 55 $/b

Pax yield-8% => 0%

Return on capital is likely to be lower this year

Source: IATA Economic Performance of the Airline Industry, End-Year 2016 report

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

% o

f in

vest

ed c

apit

al

Return on capital invested in airlines

Cost of capital (WACC)

Return on capital (ROIC)

IATA Economics www.iata.org/economics

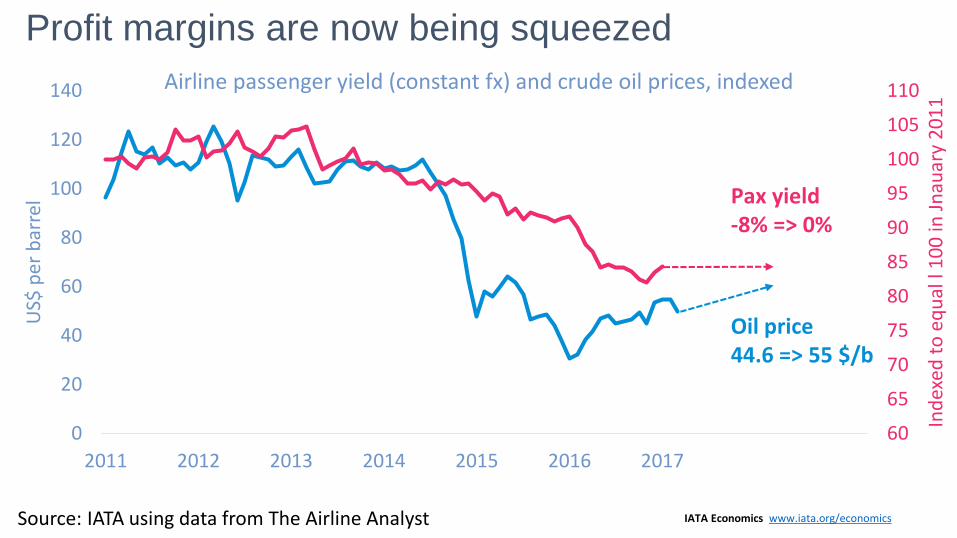

But investors should still see value created

Source: McKinsey, IATA

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

US$

bill

ion

Difference between investing in airlines and investing in similar assets elsewhere

IATA Economics www.iata.org/economics

Airline Industry Economics Advisory Workshop 2016 6

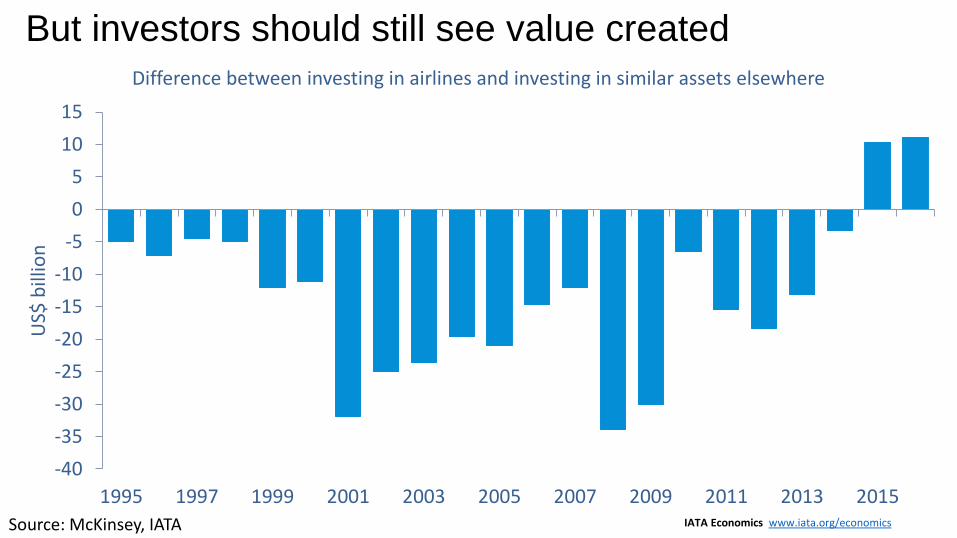

Fuel prices were low but no simple impact on ROIC

Source: IATA, Platts IATA Economics www.iata.org/economics

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2000 2002 2004 2006 2008 2010 2012 2014 2016

Jet

fuel

pri

ce, U

S$/b

arre

l

RO

IC, %

of

inve

sted

cap

ital

Airline industry ROIC and jet fuel prices

ROIC

Jet fuel price

Airline Industry Economics Advisory Workshop 2016 7

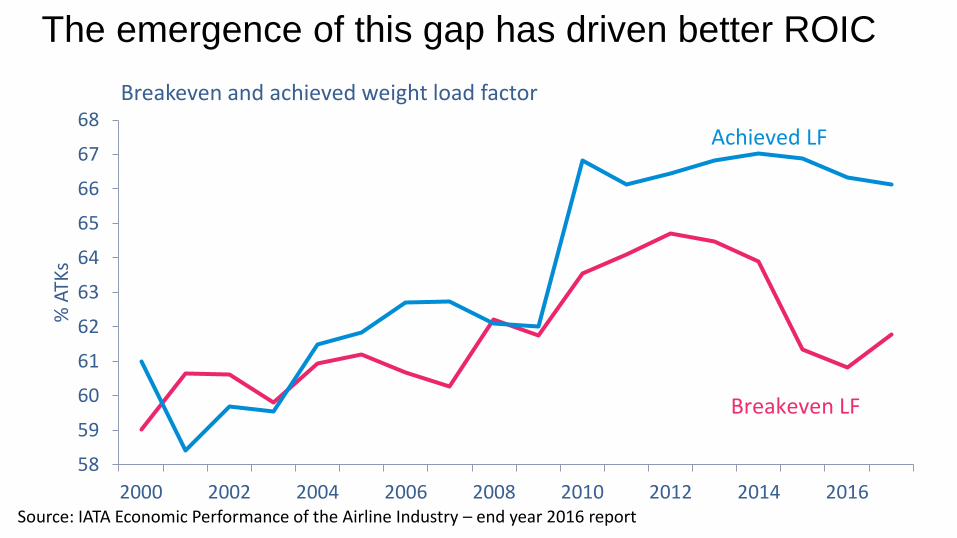

The emergence of this gap has driven better ROIC

58

59

60

61

62

63

64

65

66

67

68

2000 2002 2004 2006 2008 2010 2012 2014 2016

% A

TKs

Breakeven and achieved weight load factor

Achieved LF

Breakeven LF

Source: IATA Economic Performance of the Airline Industry – end year 2016 report

Airline Industry Economics Advisory Workshop 2016 8

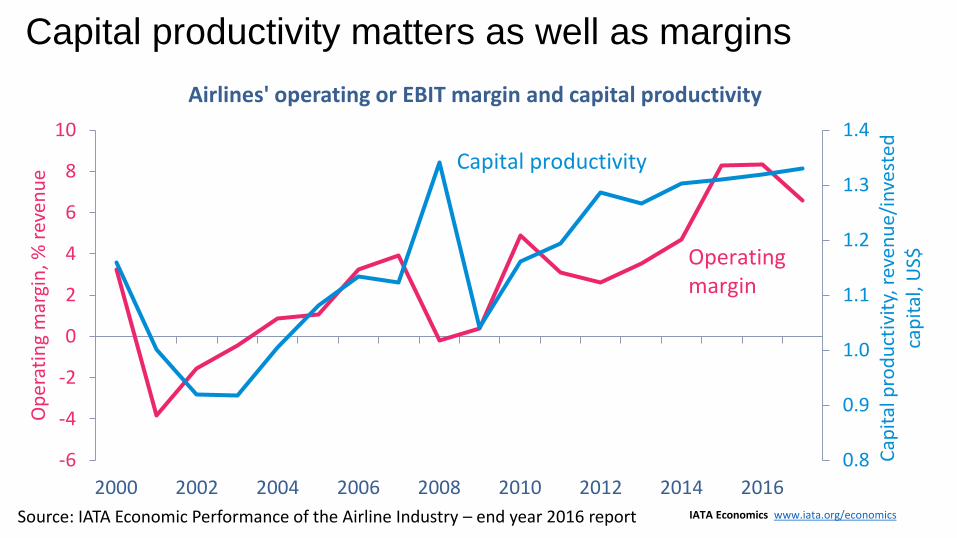

Capital productivity matters as well as margins

0.8

0.9

1.0

1.1

1.2

1.3

1.4

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014 2016

Cap

ital

pro

du

ctiv

ity,

rev

enu

e/in

vest

ed

cap

ital

, US$

Op

erat

ing

mar

gin

, % r

even

ue

Airlines' operating or EBIT margin and capital productivity

Capital productivity

Operating margin

Source: IATA Economic Performance of the Airline Industry – end year 2016 report IATA Economics www.iata.org/economics

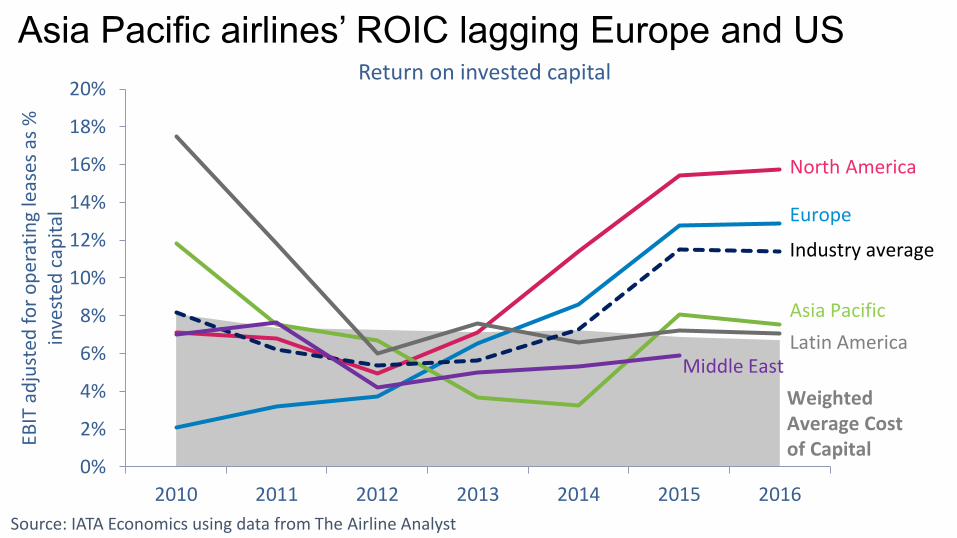

Asia Pacific airlines’ ROIC lagging Europe and US

Source: IATA Economics using data from The Airline Analyst

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011 2012 2013 2014 2015 2016

EBIT

ad

just

ed f

or

op

erat

ing

leas

es a

s %

in

vest

ed c

apit

alReturn on invested capital

Industry average

North America

Europe

Asia Pacific

Latin AmericaMiddle East

Weighted Average Cost of Capital

Free Cash Flow yield just positive in Asia Pacific

Source: IATA Economics using data from The Airline Analyst

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2010 2011 2012 2013 2014 2015 2016

FCF

as %

inve

sted

cap

ital

Free cash flow yield

North America

Industry average

Asia Pacific

Latin America

Europe

Middle East

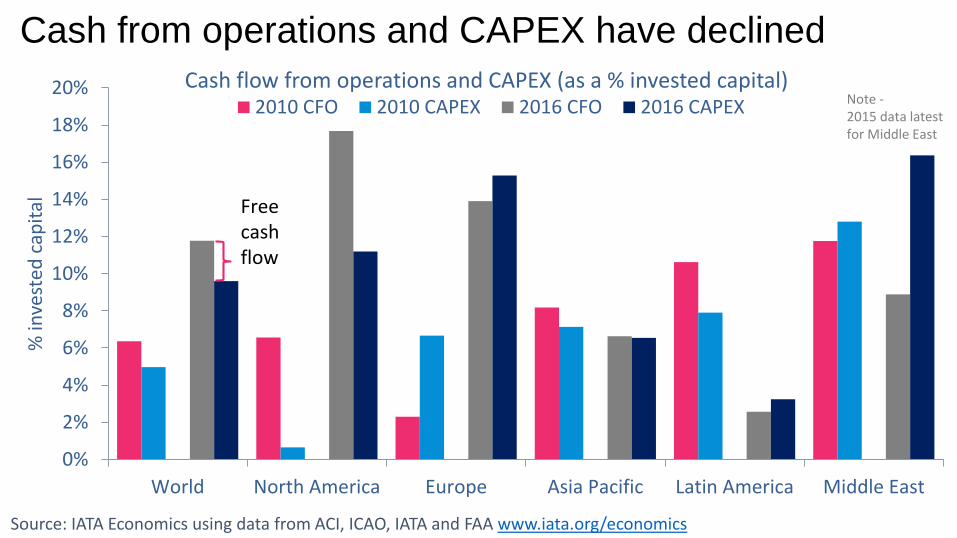

Cash from operations and CAPEX have declined

Source: IATA Economics using data from ACI, ICAO, IATA and FAA www.iata.org/economics

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

World North America Europe Asia Pacific Latin America Middle East

% in

vest

ed c

apit

al

Cash flow from operations and CAPEX (as a % invested capital)2010 CFO 2010 CAPEX 2016 CFO 2016 CAPEX

Free cash flow

Note -2015 data latest for Middle East

Balance sheets still highly leveraged in Asia Pacific

Source: IATA Economics using data from The Airline Analyst

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015 2016

Deb

t ad

just

ed f

or

op

erat

ing

leas

es/E

BIT

DA

R

Adjusted net debt/EBITDAR

Latin America

Asia Pacific

Industry average

EuropeNorth America

Middle East

Investment grade credits

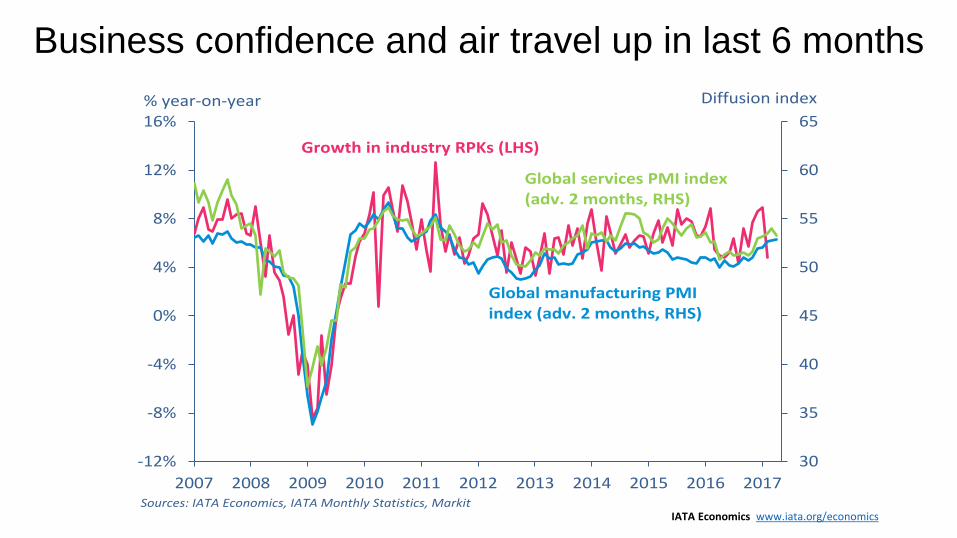

Business confidence and air travel up in last 6 months

30

35

40

45

50

55

60

65

-12%

-8%

-4%

0%

4%

8%

12%

16%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% year-on-year Diffusion index

Growth in industry RPKs (LHS)

Global manufacturing PMI index (adv. 2 months, RHS)

Sources: IATA Economics, IATA Monthly Statistics, Markit

Global services PMI index (adv. 2 months, RHS)

IATA Economics www.iata.org/economics

Though still much variation by air travel market

Africa - Europe

Europe- C. AmericaEurope - Asia

Europe - Middle East

Europe - North America

Asia - North AmericaAsia - SW Pacific

Middle East - Asia

Middle East - North America

North - South America

Within Europe

Within Asia

Domestic Australia

Domestic Brazil

Domestic China

Domestic India

Domestic Japan

Domestic Russia

Domestic US

-5%

0%

5%

10%

15%

20%

0% 2% 4% 6% 8% 10% 12% 14% 16%Share of total global RPKs (Year ended Jan 2017)

Sources: IATA Economics, IATA Monthly Statistics by Route

RPK growth by int'l route and dom. market (latest month, % year-on-year*)

*Note: int'l routes data are for January;domestic market data are for February

IATA Economics www.iata.org/economics

Growth has returned to air cargo

IATA Economics www.iata.org/economics Source: Markit, IATA Statistics

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-30%

-20%

-10%

0%

10%

20%

30%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

% year-on-year % year-on-year

Growth in industry FTKs Global PMI new export orders component (adv. 2 months)

Sources: IATA Economics, IATA Monthly Statistics, Markit

Implied PMI series if the index remains flat at its

February 2017 level over the coming months

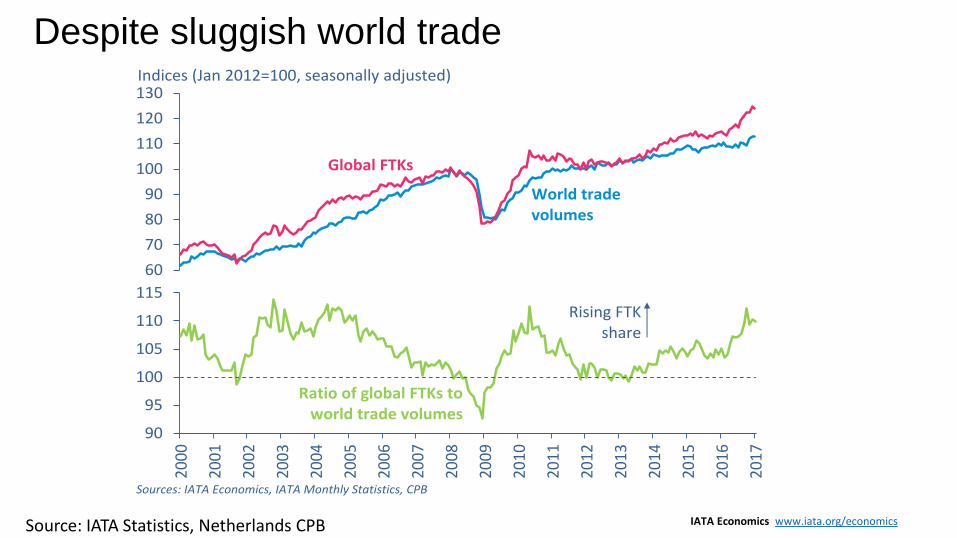

Despite sluggish world trade

IATA Economics www.iata.org/economics Source: IATA Statistics, Netherlands CPB

60

70

80

90

100

110

120

130Indices (Jan 2012=100, seasonally adjusted)

Global FTKs

World trade volumes

90

95

100

105

110

115

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Sources: IATA Economics, IATA Monthly Statistics, CPB

Rising FTK share

Ratio of global FTKs to world trade volumes

Headwind – continuing debt overhang

Source: Bank for International Settlement database

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

250

260

270

280

1999 2001 2003 2005 2007 2009 2011 2013 2015

% o

f G

DP

% o

f G

DP

Outstanding debt of non-financial sector, % of GDP

Developed economies

Developing economies

Headwind – the retreat from globalization

Source: IMF World Economic Outlook and the World Trade Organization

-15

-10

-5

0

5

10

15

2000 2002 2004 2006 2008 2010 2012 2014 2016

% c

han

ge o

ver

pre

vio

us

year

World GDP and cross-border trade growth

World trade growth

World GDP growth

Headwind - poor demographics in some economies

Source: Oxford Economics

-1.0

0.0

1.0

2.0

3.0

4.0

1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

% c

han

ge o

ver

pre

vio

us

year

Labour force growth

US

ChinaJapanGermany

Note: Only+0.1% pa without net immigration

Headwind - the exhaustion of monetary policies

Source: Haver

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

0

1

2

3

4

5

6

7

8

9

10

1985 1990 1995 2000 2005 2010 2015

Bill

ion

US$

% in

tere

st r

ate

US federal funds target rate and balance sheet assets

US fed funds

US Federal Reserve Bank assets

Airline Industry Economics Advisory Workshop 2016 21

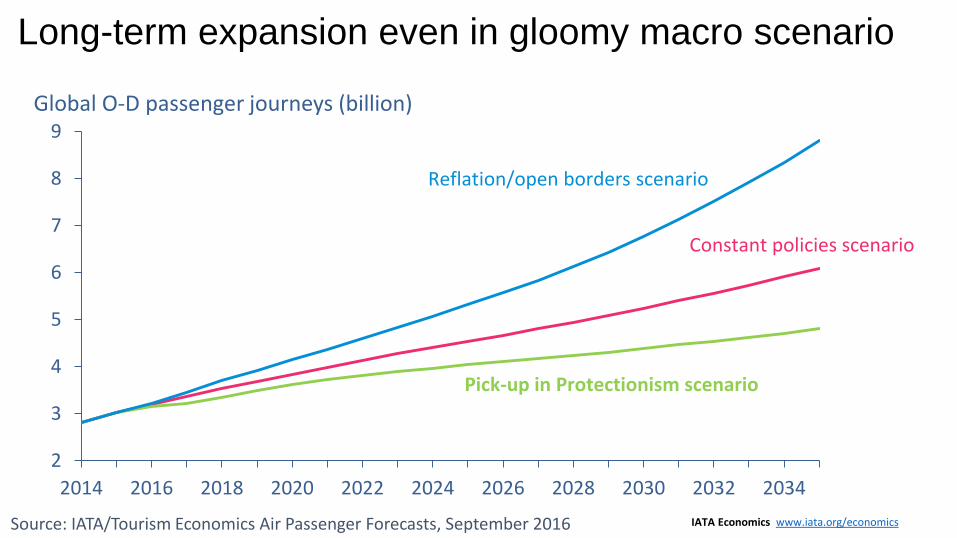

Long-term expansion even in gloomy macro scenario

2

3

4

5

6

7

8

9

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034

Global O-D passenger journeys (billion)

Constant policies scenario

Reflation/open borders scenario

Pick-up in Protectionism scenario

Source: IATA/Tourism Economics Air Passenger Forecasts, September 2016 IATA Economics www.iata.org/economics

Airline Industry Economics Advisory Workshop 2016 22

Trip frequency still low in many important markets

0 0.5 1 1.5 2 2.5 3 3.5 4

NigeriaIndia

EgyptChina

South AfricaIndonesia

BrazilMexico

Russian FederationColombia

ChileTurkey

ThailandJapan

Korea, Republic OfSaudi Arabia

GermanyFrance

ItalyUnited States

CanadaUnited Kingdom

SpainAustralia

Propensity to fly (total passengers/population)Source: IATA/Tourism Economics Air Passenger Forecasts, September 2016 IATA Economics www.iata.org/economics

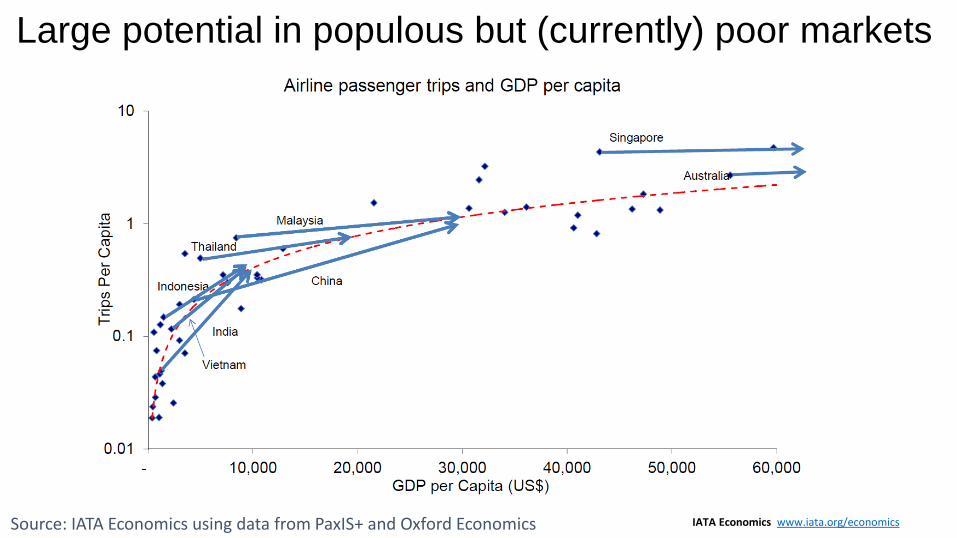

Large potential in populous but (currently) poor markets

Source: IATA Economics using data from PaxIS+ and Oxford Economics IATA Economics www.iata.org/economics

Airline Industry Economics Advisory Workshop 2016 24

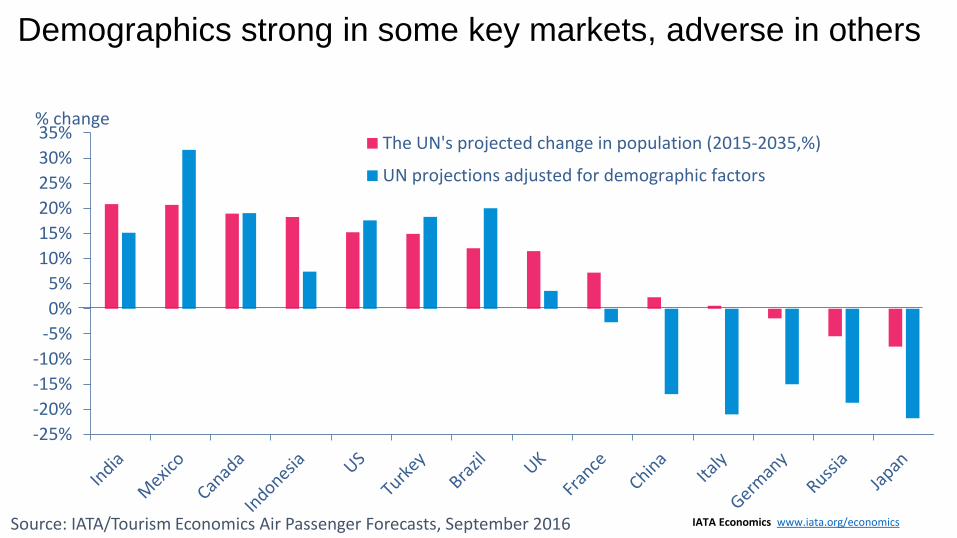

Demographics strong in some key markets, adverse in others

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%% change

The UN's projected change in population (2015-2035,%)

UN projections adjusted for demographic factors

Source: IATA/Tourism Economics Air Passenger Forecasts, September 2016 IATA Economics www.iata.org/economics

Airline Industry Economics Advisory Workshop 2016 25

Significant change in top-10 markets over next 20 years

2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035

US

China

UK

Japan

Spain

Germany

India

Italy

France

Indonesia

China

US

India

UK

Indonesia

Japan

Spain

Germany

Brazil

Turkey

Source: IATA/Tourism Economics Air Passenger Forecasts, September 2016 IATA Economics www.iata.org/economics

Centre of gravity of air travel shifting fast towards China

Source: IATA Economics using data from PaxIS+

1914 2004 2015 2035

IATA Economics www.iata.org/economics

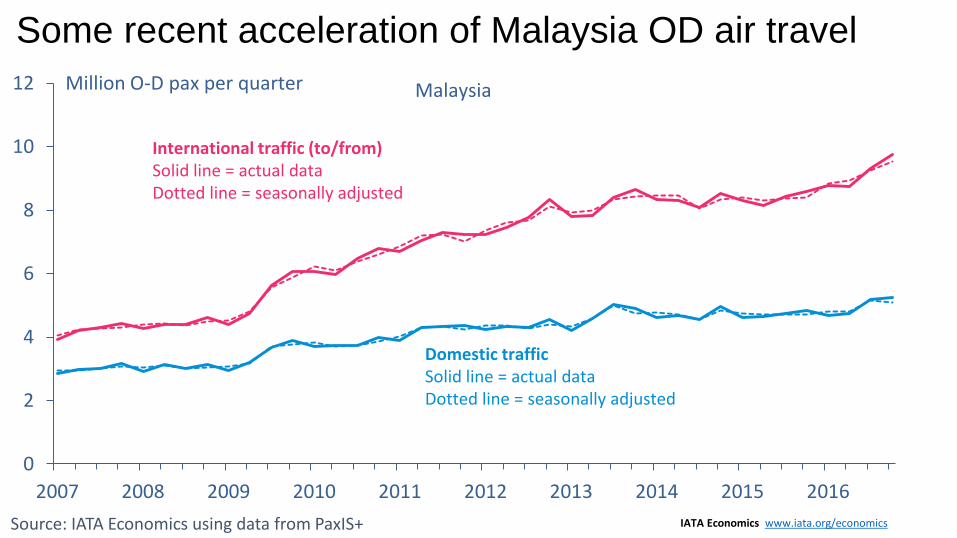

Some recent acceleration of Malaysia OD air travel

Source: IATA Economics using data from PaxIS+ IATA Economics www.iata.org/economics

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Million O-D pax per quarter

International traffic (to/from) Solid line = actual data Dotted line = seasonally adjusted

Domestic traffic Solid line = actual data Dotted line = seasonally adjusted

Malaysia

Growth rates back to double figures

Source: IATA Economics using data from PaxIS+ IATA Economics www.iata.org/economics

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total Dom Int

%yoy growth Malaysia

Middle East hubs dominating some connecting markets

Source: IATA Economics using data from PaxIS+ IATA Economics www.iata.org/economics

4.1%

10.6% 11.4%

30.3%

36.8%

8.9%

17.1% 15.1%

54.7%

41.3%

0%

10%

20%

30%

40%

50%

60%

Asia - North America Asia - Europe Asia - Middle East Europe - Australasia Asia - Africa

2010 2016

Passenger journeys connecting through the Middle East (AUH, DOH, DXB) % of total

-0.4% -2.7%

-0.7%

-0.4% -8.4% -1.3% -1.4%

6.7%

5.3%

-0.8% -0.1% -5.5% -0.6%

0.3%

-1

0

1

2

3

4

5

6

Singapore Kuala Lumpur

Passengers (millions) Change in number of connecting passengers (2010-2016)

Note: the data labels show the change in the proportion of total connecting passengers on each route passing through SIN and KUL between 2010 and 2016.

But KL has seen success in regional connecting market

Source: IATA Economics using data from PaxIS+ IATA Economics www.iata.org/economics

Airline Industry Economics Advisory Workshop 2016 31