Startup Company Valuation: The State of Art and Future Trends

Upload

i5investCategory

view

1.704download

0

2 | 12/02/2015

Experience of the founder team Product with a

Unique Selling Proposition

Traction / Momentum

Consistence / completeness of business model

Scalability of business model

Market potential and competition

Business Plan and capital

required

External proof of concept

What can you contribute in addition to

capital?

Fair valuation (for the region) with

reasonable stake

Working together over the

investment period

Exit / liquidation event

Issues from the perspective of Angel Investor

12/02/2015

Traffic

Engagement

Registered users

Active users

Revenues

Profitability

3 | 12/02/2015

What drives returns?

The following factors are positively correlated with higher returns on the investment

12/02/2015

Source: Wiltbank/Boeker, Returns to Angel Investors, 2007

Hours of due diligence

Angel investor’s expertise in the industry

Active participation at least several times per month

Market for seed funding is becoming more efficient

Proprietary deal flow is declining as a driver of returns

Advisory support is becoming more important (than connective support)

0%

10%

20%

30%

40%

50%

60%

<1X 1X to 5X 5X to 10X 10X to 30X >30XPe

rcen

t of T

otal

Exi

tsExit Multiples

Distribution of Returns by Venture Investment

Overall Multiple: 2.6xAverage Holding Period: 3.5 years

3 years

3.3 years

4.6 years 4.9 years 6 years

4 | 12/02/2015

Venture Capital Method

The VC approach reflects the business model of invest, hold and exit

Pre-money value

Post-money value

Capital raised

Exit Value

Discount Rate = Expected IRR

Exit Value drivers

Revenue potential

Profitability: e.g. EBITDA

Multiple based on revenues / EBITDA

Competitivebidding process

Consider Dilution based on next funding rounds or option poolsThey reduce value / share and pre-money valuation

Investment horizon: 5 – 8 years

Terminal Value (EUR in m) 20,0 IRR 65%Investment Horizon (yrs) 6Post-money value 1,0 Capital raised 0,3 Pre-money value 0,7

Share in the Company 30%

Cash on Cash Multiple 20

Efficient exit process

5 | 12/02/2015

Asset-based valuation

The Asset-based valuation reflects the business model, the status quo and a make/buy decision by a strategic investor

2/12/2015

Total asset value

Other Assets?

CustomersConsider traction and quality of existing customersReplacement costs based on Customer Acquisition costs / Future value based on Customer Lifecycle Value

WorkforceExisting workforce in placeReplacement costs / multiples

Software, Know How

Software and DatabasesRelief from royalty / Replacement costs

Intellectual Property

Patents, trademarks, etc.Relief from royalty / Replacement costs

Fixed & current assets

Office equipment and Net Working CapitalReplacement Costs

6 | 12/02/2015

Valuation based on Scoring Method

Step 1: Determine the average pre-money valuation of pre-revenue companies in theregion and business sector of the target company.

Step 2: Set weighting for each category and benchmark the target company withaverage pre-revenue companies

2/12/2015

Category Weighting Benchmarking Factor

Strength of Entrepreneur and Team 50% 125% 0.6250

Size of the Opportunity 15% 150% 0.2250

Product/Technology – USP 15% 100% 0.1500

Competitive Environment 5% 75% 0.0375

Marketing/Sales/Partnerships 5% 80% 0.0400

Need for Additional Investment 5% 100% 0.0500

Other factors (e.g. grants received) 5% 100% 0.0500

Total 100% 1.1775

Average pre-revenue valuation EUR 1.5 m

Valuation of Target (pre-revenue) EUR 1.8 m

7 | 12/02/2015

All approaches provide a great framework…

…in the end supply and demand for investment opportunities drive the valuation

Star

tup

inve

stm

ent

oppo

rtun

ities

Angel investors

(Deals) experience and points of reference for

valuation

Industry knowledge

Angel network

Supply Demand

8 | 12/02/2015

What is happening in startup markets?

The world talks about the big ones as this is more exciting

Source: Statista, Capital IQ & i5invest Analysis

USD in bn0 10 20 30 40 50

UBERAirbnb

DropboxXiaomi

SnapchatPalantir

JingdongRocket Internet

PinterestZalando

Overview of most valuable start ups above USD 1 billion

02468

Latest pre-money

valuation

Market Cap(Jan 2015)

USD

in b

n

Rocket Internet

02468

Latest pre-money

valuation

Market Cap(Jan 2015)

USD

in b

n

Zalando

0

10

20

30

40

Feb 2011 Aug 2013 Jun 2014 Dec 2014 Jan 2015

Pre-

mon

ey (U

SD in

bn)

UBER

….and their development over time

+141%

9 | 12/02/2015

What is happening in transaction markets?

2/12/2015

Development of transaction multiples in Internet Software

Source: Capital IQ & i5invest Analysis

0,0

5,0

10,0

15,0

0,0

20,0

40,0

60,0

80,0

100,0

Q1-2/FY2013 Q3-4/FY2013 Q1-2/FY2014 Q3-4/FY2014

Transactions in Europe - Internet Software

Average transaction value (EUR in m)

Transaction Value / EBITDA

0 1 000,0 2 000,0 3 000,0

Scout24 Holding GmbH - 2013Host Europe WVS Limited - 2013

Civica plc - 2013Nets Holding A/S - 2014

VKontakte Ltd. - 2014Viber Media Inc. - 2014

Enterprise Value (USD in m)

Biggest Transactions

(USD in m)

Enterprise Value / EBITDA

Development of private placements in Internet Software

0,0

100,0

200,0

300,0

400,0

500,0

0,0

2,0

4,0

6,0

8,0

10,0

Aug 2014 Sept 2014 Oct 2014 Nov 2014 Dec 2014

Private Placements - Internet Software

Average money raised (EUR in m)

Number of transactions

012345678

Europe and USA USA Europe

Private Placements per region - Internet Software (money raised)

Q3 2014 Q4 2014

+20% +38%-30%

(USD in m)

(USD in m)

10 | 12/02/2015

What is happening in capital markets?

2/12/2015

66%

0,00

0,50

1,00

1,50

2,00

2,50

3,00

Europe USA

Enterprise Value / Sales - Jan 2015

Enterprise Value / Sales

How do capital markets look at Internet Companies?

Source: Capital IQ & i5invest Analysis

US-based companies trade at a 66% premium above their peers in Europe.

Companies in the Anglo-Saxon Regiontrade at higher multiples in general.

Does being in the US add value for the sake of being in the US?

0,00

1,00

2,00

3,00

4,00

5,00

6,00

-

2 000,0

4 000,0

6 000,0

8 000,0

10 000,0

United Internet AG(DB:UTDI)

Yandex N.V.(NasdaqGS:YNDX)

Telecity Group plc(LSE:TCY)

Top 3 "European"

Enterprise Value EV / Revenues

0,00

5,00

10,00

15,00

20,00

-

50 000,0

100 000,0

150 000,0

200 000,0

250 000,0

300 000,0

350 000,0

Google Inc.(NasdaqGS:GOOGL)

Facebook, Inc.(NasdaqGS:FB)

eBay Inc.(NasdaqGS:EBAY)

Top 3 American

Enterprise Value EV / Revenues

What are the big players and their valuations?

USD in bn

11 | 12/02/2015

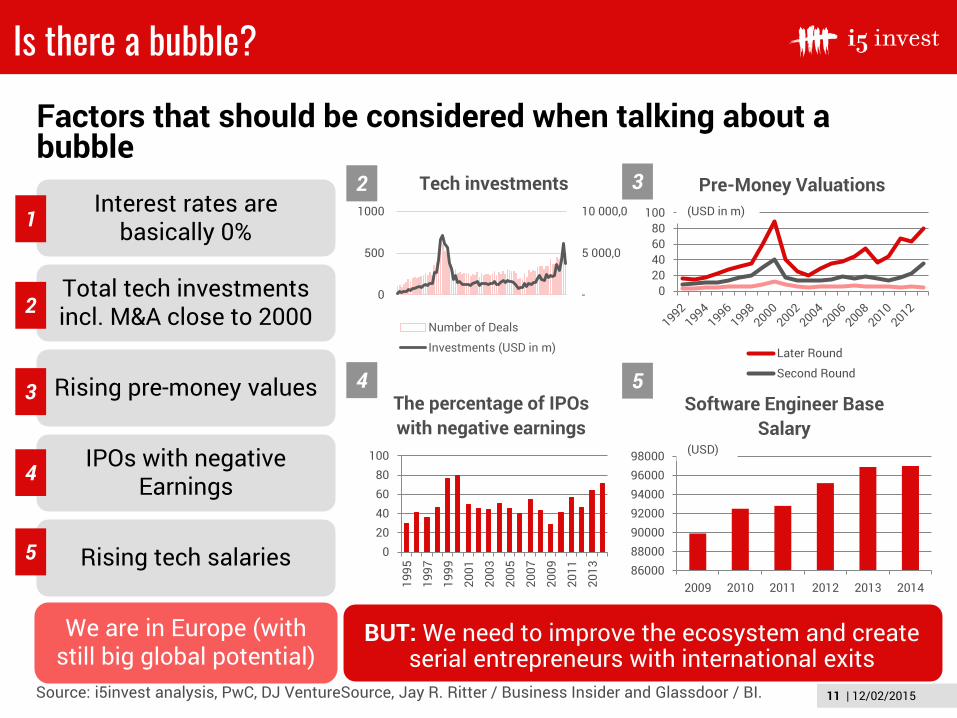

Is there a bubble?

12/02/2015

Factors that should be considered when talking about a bubble

Interest rates are basically 0%

Total tech investments incl. M&A close to 2000

Rising pre-money values

IPOs with negative Earnings

Rising tech salaries

We are in Europe (with still big global potential)

BUT: We need to improve the ecosystem and create serial entrepreneurs with international exits

1

2

5

3

4

-

5 000,0

10 000,0

0

500

1000

Tech investments

Number of Deals

Investments (USD in m)

2

4

020406080

100

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

The percentage of IPOs with negative earnings

3

020406080

100

Pre-Money Valuations

Later Round

Second Round

(USD in m)

5

86000880009000092000940009600098000

2009 2010 2011 2012 2013 2014

Software Engineer Base Salary

(USD)

Source: i5invest analysis, PwC, DJ VentureSource, Jay R. Ritter / Business Insider and Glassdoor / BI.

12 | 12/02/2015

Cluster Spengergasse

Spengergasse 371050 Vienna

In the heart of Vienna‘s startup ecosystem

13 | 12/02/2015

What we do – Our Services

WE ARE LONG TERM PARTNERS (through all stages)START-UP MENTORINGSEED FUNDINGCORPORATE DEVELOPMENT / M&A ADVISORY

We focus on max 2 new companies per year – we aren’tspray & pray investors. We focus on sector expertise, mostlystrong IP/technology, international/US markets, rarelycopycat business models

14 | 12/02/2015

Who we are – Our Team

Founded 2007, Vienna - partner i5growth Inc. in Palo Alto

12/02/2015

- PARTNERS & FRIENDS – OUR ECOSYSTEM-

Herwig SpringerCEO Corp. Dev.,M&A

Patrick ProkeschDirector Corp. Dev.,M&A

Paul WeinbergerPartner

Markus WagnerChairmain of theAdvisory Board

AlexanderIgelsboeckAdvisory Board

Martin BrunthalerAdvisory Board

Georg NovakExecutive Assistant

Bernhard LehnerPartner

Vlad GozmanPartner

15 | 12/02/2015

Startup Mentoring and Seed Funding

Venture 1 Venture 2 Venture 3 Venture 4 Venture 5

Innovation Management and Product Strategy

Go-to-Market Strategy

Company Setup and Office Infrastructure

IT Dev. & Operations, Accounting, Finance

Seed Funding, Business Planning & Public Funding

HR & Recruiting

Marketing, PR & Media Planning

Social Media Marketing and SEO

Development

Project Management

Product Management

Development

Project Management

Product Management

Development

Project Management

Product Management

Development

Project Management

Product Management

Development

Project Management

Product Management

help ideas to grow

?

International Business NetworkBusiness development

16 | 12/02/2015

Startup Incubation – Top 10 learnings

1

2

6

5

3

4

7

9

8

10

Team up with the best/team members you know/complementary people/experienced pros

Better a small piece of success than a huge of a failure

Don’t wait until your product is perfect but create a Minimum Viable Product

Talk-talk-talk about your company/products, no one will steal it

Sell-sell-sell generate revenues – revenue is the best funding ever!

Don’t rely on viral effects, PR or social media (SEO, CPA, …)

Launch fast, A/B testing, try out, learn, mutate, adopt

Look for experienced investors (execs, managers, experts, …) expertise, money, network

Do it, don’t wait, don’t think about it, try it out

Build companies that earn money

17 | 12/02/2015

Corporate Development / M&A Advisory

Company and market analysis

Financial model and business plan

Indicative valuation Long- and shortlisting

of potential buyers Preparation of

transaction documents (Info Memo, Teaser & NDA)

Contacting short list with teaser and NDA

Distribution of Info Memo after receipt of signed NDAs

Preparation of management presentation

Setup of Data Room Assessment of LOIs Selection of bidders

SPA Negotiations with preferred buyer(s)

Development of final transaction structure (share/asset deal)

Signing of SPA Receipt of approvals Closing

Management presentations and site visits

Coordinating Due Diligence, expert meetings and Q&A session

Assessment of Binding Offers / Term Sheets

Selection of preferred buyer(s)

Phase 1Preparation

Phase 2Reach Out

Phase 3Due Diligence

Phase 4Negotiation

Key steps

Key success factors Understand dynamics

of transaction environment

Business Development to assure Fit for Exit

Establish the right first point of contact be it business or corporate development

Create quickly competitive process with several potential bidders

Negotiation tactics and mitigating reps & warranties

Leverage different stakeholders

Bridging the value gap

Comprehensive preparation of documents and company data

Fast, streamlined and efficient due diligencewith several bidders

Efficient sell side support to maximize returns

18 | 12/02/2015

Portfolio Overview

#inspire, #innovate, #incubate, #invest, #internationalize

Thank you!

OUR EUROPE OFFICEi5invest Beratungs GmbH

(CEO Herwig Springer)Spengergasse 37-39

A-1050 ViennaAustria/Europe

OUR US PARTNERi5growth Inc.

(CEO Markus Wagner)460 S California Ave, #304Palo Alto, California 94306

United States