Startnowhow - Financial Planning for STARTUPS

21

FINANCIAL PLANNING FOR STARTUPS Ebru Gürses / Dr. Joachim Behrendt

Transcript of Startnowhow - Financial Planning for STARTUPS

FINANCIAL PLANNING FOR STARTUPS Ebru Gürses / Dr. Joachim Behrendt

INTR

OD

UC

TION

StartNowHow

• Open seminar series for active and prospective entrepreneurs

• 10 sessions on monthly basis until summer 2015

• Covers relevant theoretical and practical aspects of entrepreneurship

• Based on lecture „entrepreneurship“ @Bogazici University

• Based on experiences of entrepreneurs, investors, mentors and consultants

• Each session with guest speaker (entrepreneurs, investors, mentors, etc.)

• Seminar materials can be downloaded after the event

• Thursdays 17.15h – 19.30h

• Next session: Thu, May 14th, 2015

• TOPIC: Marketing planning and control – the role of key performance indicators

• SPEAKER: tbd

• Certificate provided for participants joining at least 7/10 sessions

• Early registration for each session required (eventbrite), capacity 50 people!

• Priority for regular participants

Startnowhow – Seminar 5 16.04.2015 2

INTR

OD

UC

TION

StartNowHow - Seminar Topics (preliminary)

1. Mon, 20.10.: The entrepreneurial ecosystem in Turkey

2. Mon, 10.11.: Entrepreneurship as a profession

3. Mon, 8.12.: Opportunity recognition and evaluation

4. Mon, 12.1.: Planning, testing and developing a business model

5. Thu, 19.2. – lot of snow but no seminar -

6. Thu, 19.3.: Market and competitor research

7. Thu, 16.4.: Financial planning for startups

8. Thu, 14.5.: Marketing planning and control – the role of key performance indicators

9. Thu, 11.6.: Funding the startup – stage financing for ventures

10. Thu, 9.7.: The investment process – pitching, negotiations and termsheet

11. tbd: Success and failure as an entrepreneur

Startnowhow – Seminar 5 16.04.2015 3

FIN

AN

CIA

L PLA

NN

ING

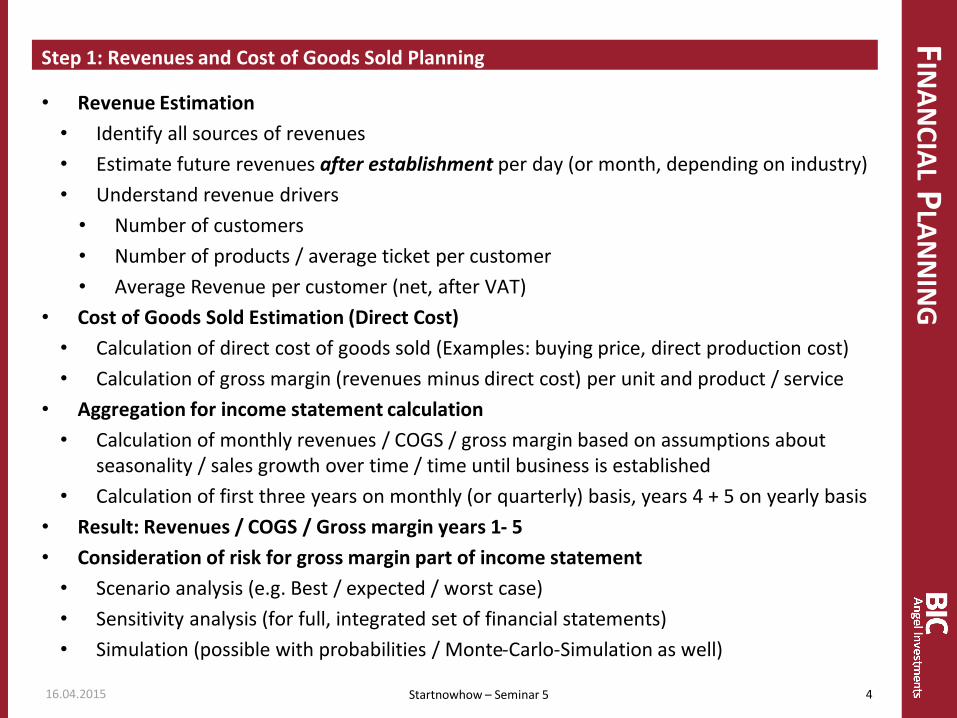

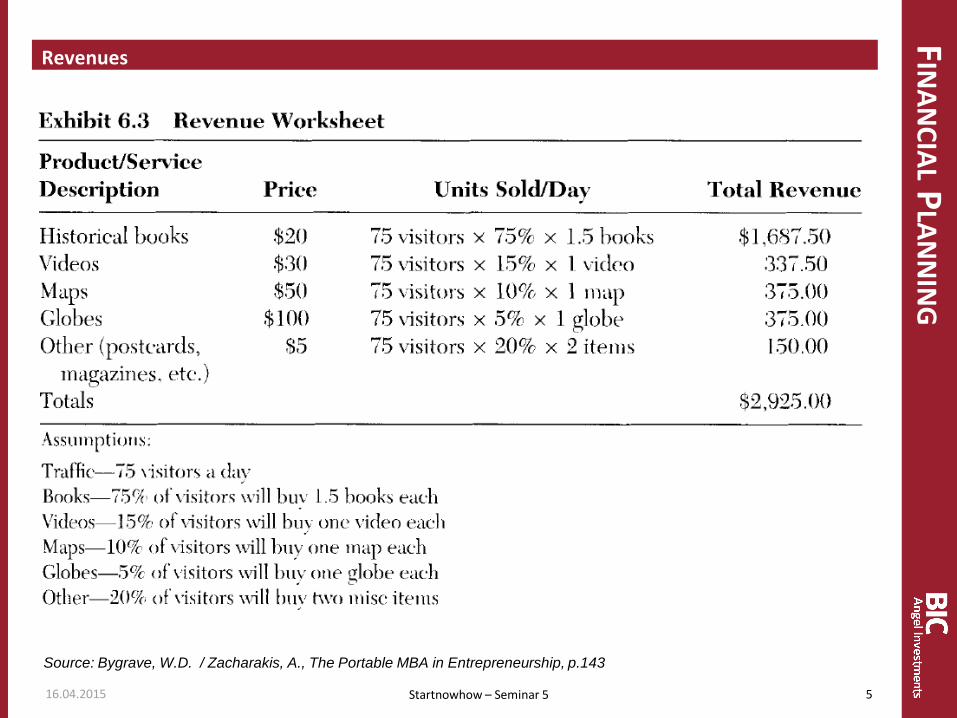

Step 1: Revenues and Cost of Goods Sold Planning

16.04.2015 4 Startnowhow – Seminar 5

• Revenue Estimation

• Identify all sources of revenues

• Estimate future revenues after establishment per day (or month, depending on industry)

• Understand revenue drivers

• Number of customers

• Number of products / average ticket per customer

• Average Revenue per customer (net, after VAT)

• Cost of Goods Sold Estimation (Direct Cost)

• Calculation of direct cost of goods sold (Examples: buying price, direct production cost)

• Calculation of gross margin (revenues minus direct cost) per unit and product / service

• Aggregation for income statement calculation

• Calculation of monthly revenues / COGS / gross margin based on assumptions about seasonality / sales growth over time / time until business is established

• Calculation of first three years on monthly (or quarterly) basis, years 4 + 5 on yearly basis

• Result: Revenues / COGS / Gross margin years 1- 5

• Consideration of risk for gross margin part of income statement

• Scenario analysis (e.g. Best / expected / worst case)

• Sensitivity analysis (for full, integrated set of financial statements)

• Simulation (possible with probabilities / Monte-Carlo-Simulation as well)

FIN

AN

CIA

L PLA

NN

ING

Revenues

16.04.2015 5 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.143

FIN

AN

CIA

L PLA

NN

ING

Cost of Goods Sold

16.04.2015 6 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.145

FIN

AN

CIA

L PLA

NN

ING

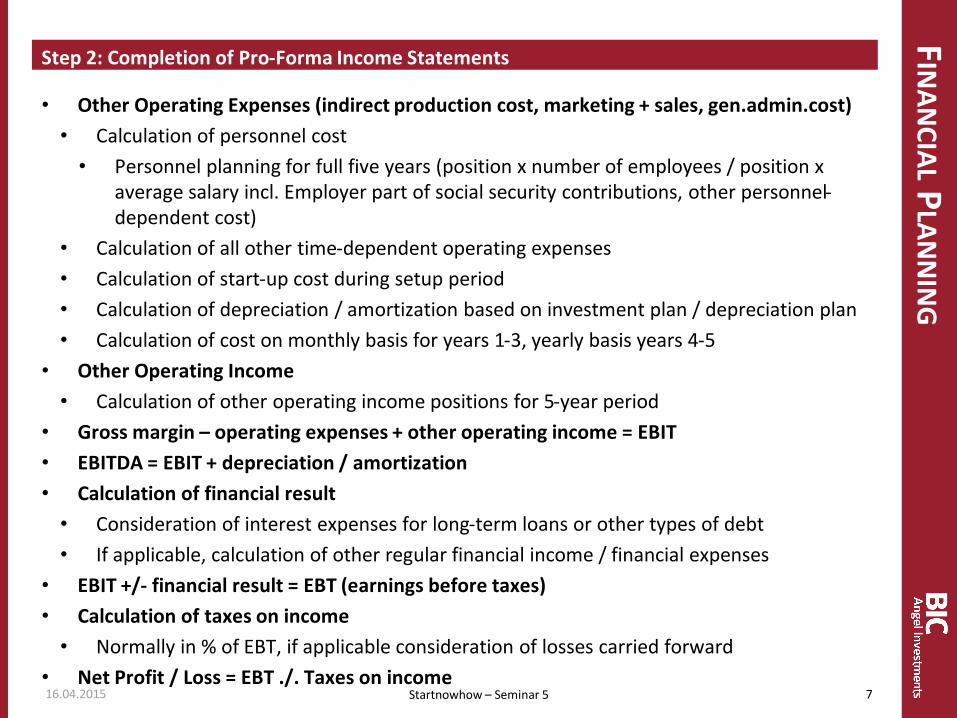

Step 2: Completion of Pro-Forma Income Statements

16.04.2015 7 Startnowhow – Seminar 5

• Other Operating Expenses (indirect production cost, marketing + sales, gen.admin.cost)

• Calculation of personnel cost

• Personnel planning for full five years (position x number of employees / position x average salary incl. Employer part of social security contributions, other personnel-dependent cost)

• Calculation of all other time-dependent operating expenses

• Calculation of start-up cost during setup period

• Calculation of depreciation / amortization based on investment plan / depreciation plan

• Calculation of cost on monthly basis for years 1-3, yearly basis years 4-5

• Other Operating Income

• Calculation of other operating income positions for 5-year period

• Gross margin – operating expenses + other operating income = EBIT

• EBITDA = EBIT + depreciation / amortization

• Calculation of financial result

• Consideration of interest expenses for long-term loans or other types of debt

• If applicable, calculation of other regular financial income / financial expenses

• EBIT +/- financial result = EBT (earnings before taxes)

• Calculation of taxes on income

• Normally in % of EBT, if applicable consideration of losses carried forward

• Net Profit / Loss = EBT ./. Taxes on income

FIN

AN

CIA

L PLA

NN

ING

Personnel Cost

16.04.2015 8 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.147

FIN

AN

CIA

L PLA

NN

ING

Operating Expenses

16.04.2015 9 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.146

FIN

AN

CIA

L PLA

NN

ING

Income Statement

16.04.2015 10 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.148

FIN

AN

CIA

L PLA

NN

ING

Step 3: Comparison

16.04.2015 11 Startnowhow – Seminar 5

• Recommended step, not always done: Comparision with „industry standards“

• Comparison of COGS %,

• Comparison of gross margins %

• Comparison of operating expenses %

• Comparison of operting results %

• Sources

• Published financial statements from public companies

• Associations

• Published statistical information

• Result: Confirmation / Modification of estimated income statements

FIN

AN

CIA

L PLA

NN

ING

Comparison

16.04.2015 12 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.151

FIN

AN

CIA

L PLA

NN

ING

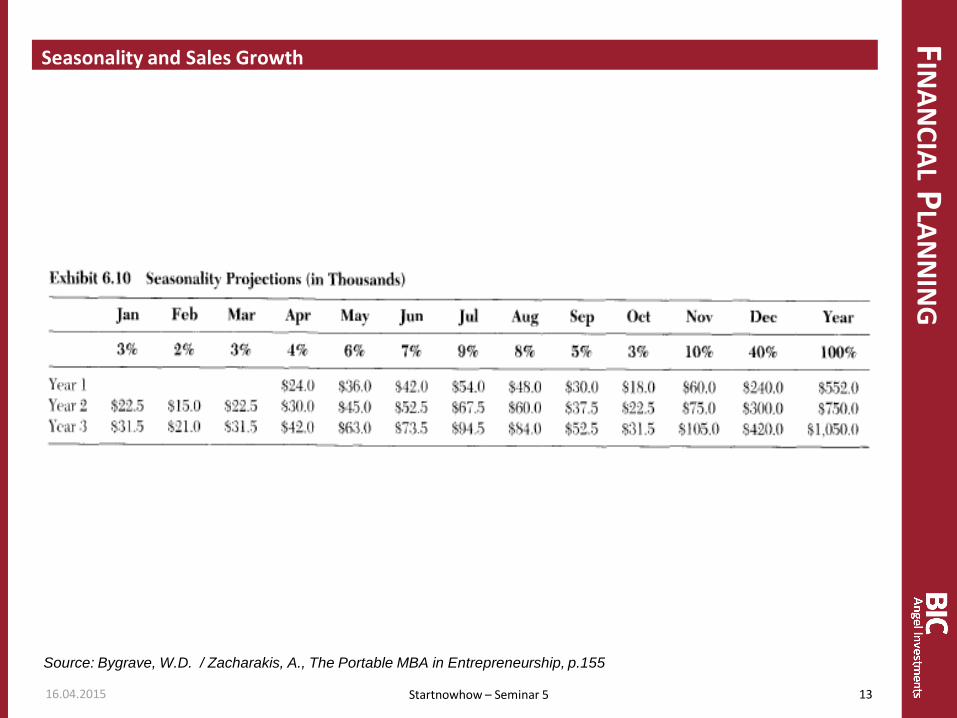

Seasonality and Sales Growth

16.04.2015 13 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.155

FIN

AN

CIA

L PLA

NN

ING

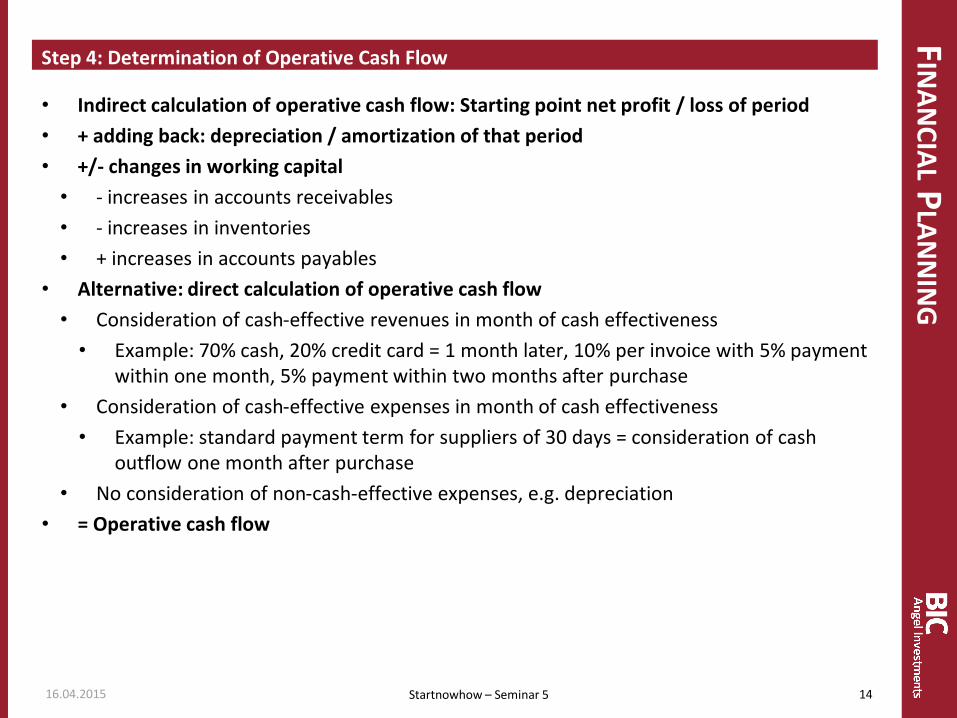

Step 4: Determination of Operative Cash Flow

16.04.2015 14 Startnowhow – Seminar 5

• Indirect calculation of operative cash flow: Starting point net profit / loss of period

• + adding back: depreciation / amortization of that period

• +/- changes in working capital

• - increases in accounts receivables

• - increases in inventories

• + increases in accounts payables

• Alternative: direct calculation of operative cash flow

• Consideration of cash-effective revenues in month of cash effectiveness

• Example: 70% cash, 20% credit card = 1 month later, 10% per invoice with 5% payment within one month, 5% payment within two months after purchase

• Consideration of cash-effective expenses in month of cash effectiveness

• Example: standard payment term for suppliers of 30 days = consideration of cash outflow one month after purchase

• No consideration of non-cash-effective expenses, e.g. depreciation

• = Operative cash flow

FIN

AN

CIA

L PLA

NN

ING

Operative Cash Flow Months 1-6

16.04.2015 15 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.157

FIN

AN

CIA

L PLA

NN

ING

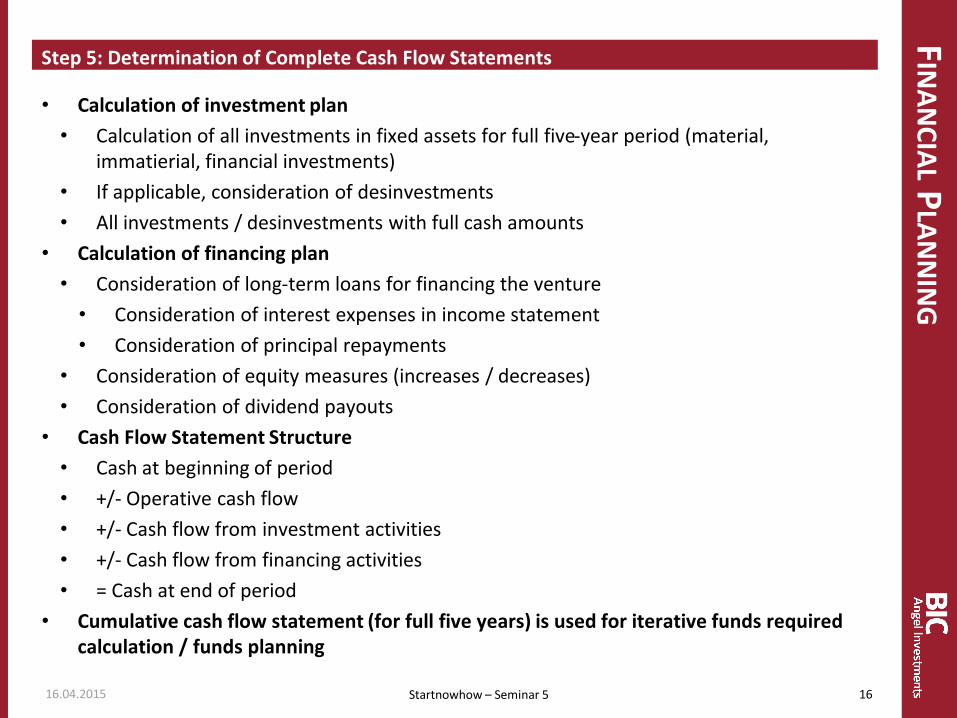

Step 5: Determination of Complete Cash Flow Statements

16.04.2015 16 Startnowhow – Seminar 5

• Calculation of investment plan

• Calculation of all investments in fixed assets for full five-year period (material, immatierial, financial investments)

• If applicable, consideration of desinvestments

• All investments / desinvestments with full cash amounts

• Calculation of financing plan

• Consideration of long-term loans for financing the venture

• Consideration of interest expenses in income statement

• Consideration of principal repayments

• Consideration of equity measures (increases / decreases)

• Consideration of dividend payouts

• Cash Flow Statement Structure

• Cash at beginning of period

• +/- Operative cash flow

• +/- Cash flow from investment activities

• +/- Cash flow from financing activities

• = Cash at end of period

• Cumulative cash flow statement (for full five years) is used for iterative funds required calculation / funds planning

FIN

AN

CIA

L PLA

NN

ING

Total Cash Flow / Funds Needed

16.04.2015 17 Startnowhow – Seminar 5

Source: Bygrave, W.D. / Zacharakis, A., The Portable MBA in Entrepreneurship, p.158

FIN

AN

CIA

L PLA

NN

ING

Step 6: Completion of Pro-Forma Financial Statements

16.04.2015 18 Startnowhow – Seminar 5

• Balance sheet at beginning of venture

• Normally only initial equity + cash

• Balance sheet at end of each period

• Consideration of income statement for period

• Consideration of changes in working capital (accounts receivables, inventories, accounts payables) in balance sheet at end of period

• Consideration of investments and depreciation in balance sheet at end of period

• Consideration of loan repayments / additional loans in balance sheet at end of period

• Consideration of equity measures / dividend payouts in balance sheet at end of period

• Result: Full set of integrated pro-forma financial statements

• Balance sheets for t = 0 to t = 6

• Income statements for periods t0-1 to t4-5

• Cash flow statements for periods t0-1 to t4-5

• Investment plans for periods t0-1 to t4-5

• Financing plans for periods t0-1 to t4-5

OU

TLOO

K StartNowHow - Outlook

• Today‘s materials will be made available to participants for downloading

• Next Seminar: „Marketing planning and control – the role of key performance indicators”

• Guest Speaker: tbd

• Thursday, 14.5.2015, 17.15 – 19.30h

• Don‘t forget to register early (eventbrite) - capacity 50 people!

• Priority for participants / registrants from today‘s session

• General rule: Allocation of seats according to participation

• Regular participation = certificate (70% participation)

Startnowhow – Seminar 5 16.04.2015 19

STA

RTN

OW

10

1

StartNow101 - Preseed program

Startnowhow – Seminar 5 16.04.2015 20

BIC ANGEL INVESTMENTS Dr. Joachim Behrendt

Phone: +90 212 328 1939 Fax: +90 212 328 1933

www.bicangels.com http:/twitter.com/joachimbehrendt http://tr.linkedin.com/pub/joachim-behrendt/18/706/a7a

Email: [email protected]