Starting the Eighth Step in the Accounting Cycle: Journalizing the Closing Entries Closing entries...

16

Starting the Eighth Step in the Accounting Cycle: Journalizing the Closing Entries Closing entries are journal entries made to close, or reduce to zero, the balances in the temporary capital accounts and to transfer the net income or net loss for the period to the capital account. These entries prepare the financial records for the next fiscal year. Section 1 Preparing Closing Entries (cont'd.)

-

Upload

gonzalo-madkins -

Category

Documents

-

view

235 -

download

1

Transcript of Starting the Eighth Step in the Accounting Cycle: Journalizing the Closing Entries Closing entries...

Starting the Eighth Step in the Accounting Cycle: Journalizing the Closing Entries

Closing entries are journal entries made

to close, or reduce to zero, the balances in

the temporary capital accounts and to

transfer the net income or net loss for the

period to the capital account. These entries

prepare the financial records for the next

fiscal year.

Starting the Eighth Step in the Accounting Cycle: Journalizing the Closing Entries

Closing entries are journal entries made

to close, or reduce to zero, the balances in

the temporary capital accounts and to

transfer the net income or net loss for the

period to the capital account. These entries

prepare the financial records for the next

fiscal year.

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

The Income Summary Account

The Income Summary account is

used to accumulate and summarize the

revenue and expenses for the period.

The Income Summary Account

The Income Summary account is

used to accumulate and summarize the

revenue and expenses for the period.

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Income Summary

Debit Credit

Expenses Revenue

If Revenue > Expenses Balance is net income

If Revenue < Expenses Balance is net loss

The Work SheetThe Work Sheet

All temporary accounts are closed

Preparing Closing Entries

1. The balance of the revenue

account is transferred to the

credit side of the Income

Summary account.

2. The expense account balances

are transferred to the debit side

of the Income Summary account.

Preparing Closing Entries

1. The balance of the revenue

account is transferred to the

credit side of the Income

Summary account.

2. The expense account balances

are transferred to the debit side

of the Income Summary account.

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Preparing Closing Entries (cont'd.)

3. The balance of the Income

Summary account is transferred to

the capital account (net income to

the credit side; net loss to the debit

side).

4. The balance of the withdrawals

account is transferred to the debit

side of the capital account.

Preparing Closing Entries (cont'd.)

3. The balance of the Income

Summary account is transferred to

the capital account (net income to

the credit side; net loss to the debit

side).

4. The balance of the withdrawals

account is transferred to the debit

side of the capital account.

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

T ACCOUNTS 6. Delivery Income

Equipment Summary

Debit

–

Closing 2,650

Credit

Closing 2,650

Debit

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

First Closing Entry (cont'd.)First Closing Entry (cont'd.)

First Closing Entry—Close Revenue to Income Summary

Closing Entry (cont'd.)

Credit

+

Balance 2,650

Closing Entry (cont'd.)

JOURNAL ENTRY

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

First Closing Entry (cont'd.)First Closing Entry (cont'd.)

First Closing Entry—Close Revenue to Income Summary

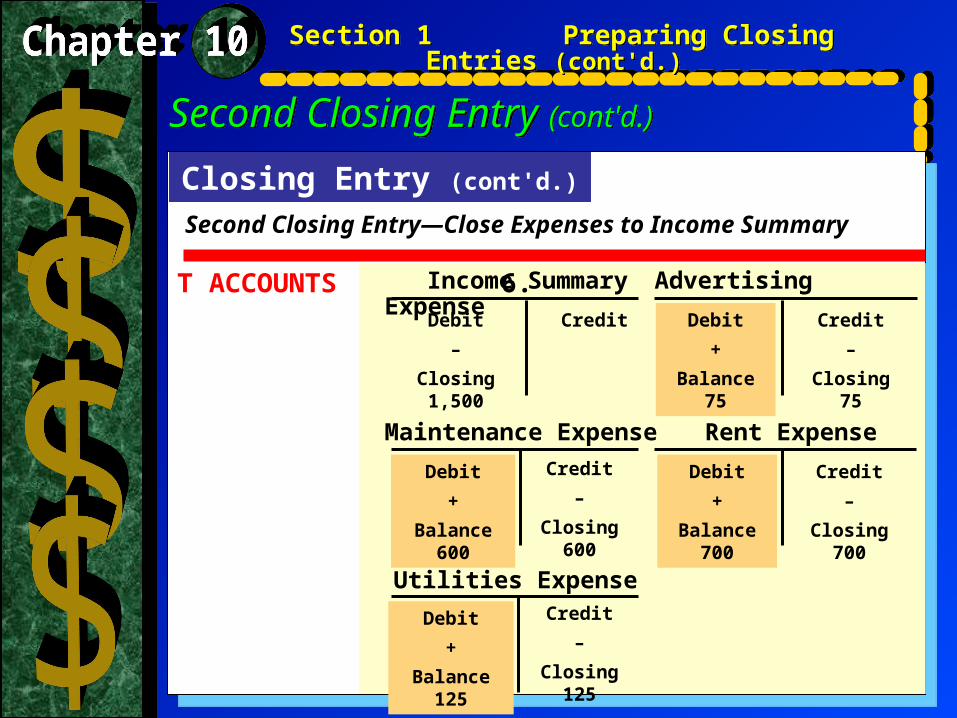

T ACCOUNTS 6.Income Summary Advertising Expense

Debit

–

Closing 1,500

Credit

–

Closing 75

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Second Closing Entry (cont'd.)Second Closing Entry (cont'd.)

Closing Entry (cont'd.)

Credit

Second Closing Entry—Close Expenses to Income Summary

Debit

+

Balance 75

Maintenance Expense Rent Expense

Debit

+

Balance 125

Credit

–

Closing 600

Debit

+

Balance 700

Credit

–

Closing 700

Utilities ExpenseCredit

–

Closing 125

Debit

+

Balance 600

Closing Entry (cont'd.)

JOURNAL ENTRY 7.

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Second Closing Entry (cont'd.)Second Closing Entry (cont'd.)

Second Closing Entry—Close Expenses to Income Summary

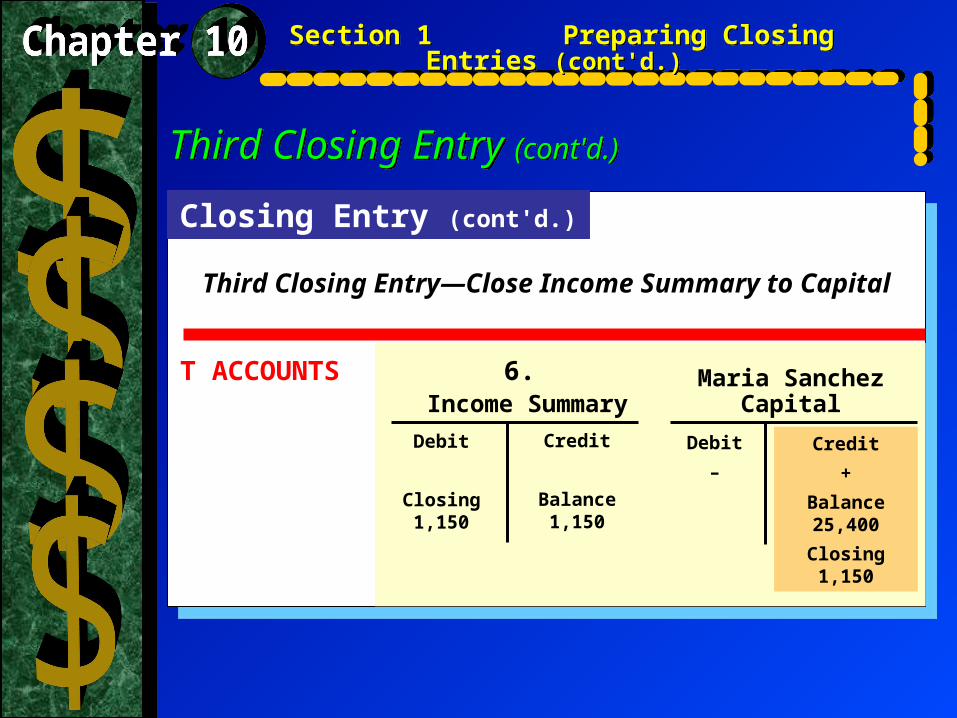

T ACCOUNTS 6. Maria SanchezIncome Summary Capital

Debit

Closing 1,150

Debit

–

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Third Closing Entry (cont'd.)Third Closing Entry (cont'd.)

Closing Entry (cont'd.)

Credit

Balance 1,150

Credit

+

Balance 25,400

Closing 1,150

Third Closing Entry—Close Income Summary to Capital

Closing Entry (cont'd.)

JOURNAL ENTRY 7.

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Third Closing Entry (cont'd.)Third Closing Entry (cont'd.)

Third Closing Entry—Close Income Summary to Capital

T ACCOUNTS 6.Maria Sanchez Maria Sanchez

Capital Withdrawals

Debit

–

Closing 500

Credit

–

Closing 500

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Fourth Closing Entry (cont'd.)Fourth Closing Entry (cont'd.)

Closing Entry (cont'd.)

Credit

+

Balance 26,550

Debit

+

Balance 500

Fourth Closing Entry—Close Withdrawals to Capital

Closing Entry (cont'd.)

JOURNAL ENTRY 7.

Section 1 Preparing Closing Entries (cont'd.)Section 1 Preparing Closing Entries (cont'd.)

Fourth Closing Entry (cont'd.)Fourth Closing Entry (cont'd.)

Fourth Closing Entry—Close Withdrawals to Capital

Why It’s Important

A post-closing trial balance verifies

that the closing entries are properly

recorded in the general ledger and that

you are ready to start the next

accounting period.

Why It’s Important

A post-closing trial balance verifies

that the closing entries are properly

recorded in the general ledger and that

you are ready to start the next

accounting period.

Section 2 Posting Closing Entries and Preparing a Post-Closing Trial Balance (cont'd.)

Section 2 Posting Closing Entries and Preparing a Post-Closing Trial Balance (cont'd.)

Key Terms

post-closing trial balance

Key Terms

post-closing trial balance

Completing the Eighth Step in the Accounting Cycle: Posting Closing Entries to the General Ledger

Completing the Eighth Step in the Accounting Cycle: Posting Closing Entries to the General Ledger

Section 2 Posting Closing Entries and Preparing a Post-Closing Trial Balance (cont'd.)

Section 2 Posting Closing Entries and Preparing a Post-Closing Trial Balance (cont'd.)

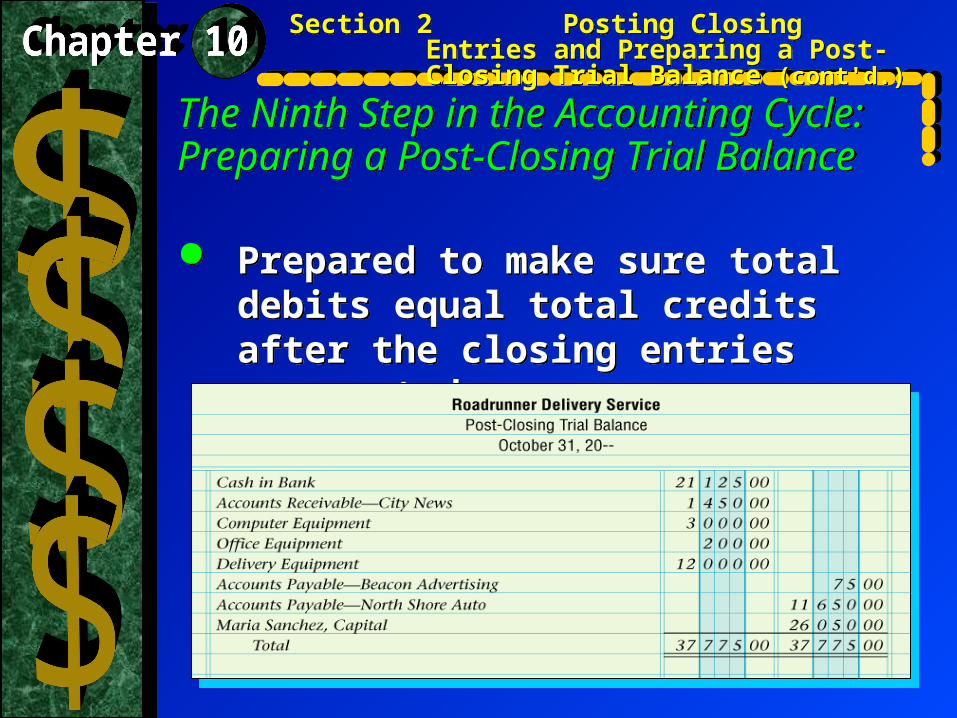

The Ninth Step in the Accounting Cycle: Preparing a Post-Closing Trial Balance

The Ninth Step in the Accounting Cycle: Preparing a Post-Closing Trial Balance

Section 2 Posting Closing Entries and Preparing a Post-Closing Trial Balance (cont'd.)

Section 2 Posting Closing Entries and Preparing a Post-Closing Trial Balance (cont'd.)

Prepared to make sure total debits equal total credits after the closing entries are posted.

Prepared to make sure total debits equal total credits after the closing entries are posted.