Star Health Project

52

-

Upload

parvat-patil -

Category

Documents

-

view

224 -

download

0

Transcript of Star Health Project

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 1/52

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 2/52

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 3/52

Scope of the Study

The scope of the study for management student gets to apply all their theoreticalknowledge in the company‘s summer training. During training they solve the particular

problem given by the company and come to know the various thing practically.

The study gives the company a true and unbiased picture of its position and standing in

especially at hubli Market and also its image in the society

Type of Research – exploratory

Type of Data – Primary

Method of Data collection – Survey

Research Instrument - Structured Schedule

Sampling Method – non parametric

Sample Size – 50

Sampling Unit – consumer of star health insurance

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 4/52

Methodology

For the preparation of project report especially in case of Marketing every steps should beanticipated closely. In this anticipation of formulation there may arise some problems,

since these are two types of information.

(i) For Primary Information :

I have used personal interview method. This survey conducted on 50 consumers

across Hubli Area. I used a set questionnaire containing some questions for

consumers. These data are expensive and time consuming but these data are mostimportant and reliable.

(ii) The Secondary Information:

This secondary data were collected from the internal sources (Company‘s

Documents) of as well as some external sources (Paper & Magazines). This

collection of these data is for easier and less time consuming.

POPULATION AND SAMPLE

The sample size taken for survey includes 50 consumers. The sample takes into

consideration all the consumers consist of beneficers of star health insurance

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 5/52

SAMPLING TECHNIQUE

In this study simple random sampling is used to select the sample size.

Simple Random sampling:

Simple Random sampling is one the simplest sampling designs and can work well for

relatively small populations. Simple Random Sampling is a process which ensures that

each of the sample of size and has an equal probability of being picked up as the chosen

sample.

RESEARCH INSTRUMENTS:

The investigator has used questionnaire as the research instrument. The types of

questions used in the questionnaire are multi-ended questions. In this type of questions

the respondents will be given four choices for answer in which they have to choose one.

The questionnaire used is a structure and closed-end one. It is one on which there are

definite, concrete and predetermined question.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 6/52

L imi tation of the Study

Limitations are always accompanied with any work. I had completed his study withinshort span of 8weeks & it was not possible to understand practically all aspects of the

subjects. Each and every factor has been carried out carefully as much as possible

limitation to the study are beyond control.

As all the primary data has been collected by discussion and interviews, there is a choice

of error as people hesitate in granting correct data and sometime exaggerate theinformation. Although I tried to convince the respondents that the study is only meant for

academic purpose, some respondents were not ready to furnish other information like

competitors of Star health insurance products, how Star health insurance is better than

other products, regarding cost benefits of anlysics in the star insurance etc. The

investigator hopes that the study will yield dependable and useful results.

The successes of any research work depend on the response of the respondent.

But sometime the response is not sufficient due to these following reasons

Respondents generally have less time to respond.

Sometimes they are confusing in their response due to lack of knowledge.

Some persons are not willing to disclose the truth.

Their attitude towards people representing a company.

The time constraint faced in the project might have affected the comprehensiveness of its

findings.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 7/52

Introduction to Insurance

Definition:-

Insurance is defined as the equitable transfer of the risk of a loss, from one entity to another, inexchange for a premium, and can be thought of as a guaranteed small loss to prevent a large, possibly devastating loss.

Insurance appears simultaneously with the appearance of human society. We know of two typesof economies in human societies:

Money Economies

With markets, money, financial instruments and so on.......

Non-Money Or Natural Economies

Without money, markets, financial instruments and so on........

The second type is a more ancient form than the first. In such an economy andCommunity, we can see insurance in the form of people helping each other. For example, if ahouse burns down, the members of the community help build a new one. Should the somethinghappen to osne's neighbor, the other neighbors must help Otherwise; neighbors will not receivehelp in the future. This type of insurance has survived to the present day in some countries where

modern money economy with its financial instruments is not widespread.

For Example: - Countries in the territory of the former Soviet Union.

Turning to insurance in the modern sense (i.e., insurance in a modern money economy, inwhich insurance is part of the financial sphere), early methods of transferring or distributing risk were practiced by Chinese and Babylonian traders as long ago as the 3rd and 2ndmillennia BC,respectively. Chinese merchants travelling treacherous river rapids would redistribute their waresacross many vessels to limit the loss due to any single vessel‘s capsizing. The Babyloniansdeveloped a system which was recorded in the famous Code of Hammurabi, c. 1750 BC, and practiced by early Mediterranean sailing merchants. If a merchant received a loan to fund his

shipment, he would pay the lender an additional sum in exchange for the lender's guarantee tocancel the loan should the shipment be stolen.

Achaemenian monarchs of Iran were the first to insure their people and made it official byregistering the insuring process in governmental notary offices.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 8/52

The Greeks and Romans introduced the origins of health and life insurance in 600 AD whenthey organized guilds called "benevolent societies" which cared for the families and paid funeralexpenses of members upon death.

Insurance as we know it today can be traced to the Great Fire of London, which in

1666devoured 13,200 houses. In the aftermath of this disaster, Nicholas Barbon opened an officetonsure buildings. In 1680, he established England's first fire insurance company, "The FireOffice," to insure brick and frame homes

Insurance, in law and economics, is a form of risk management primarily used to hedgeagainst the risk of a contingent loss. An Insurer is a company selling the insurance; an Insured

is the person or entity buying the insurance.

Premium:-

The insurance rate is a factor used to determine the amount to be charged for certainAmount of insurance coverage, called the premium.

Indemnity:-

The technical definition of "indemnity" means to make whole again. There are two types of insurance contracts;

1. an "indemnity" policy and

2. A "pay on behalf" or "on behalf of‖ policy.

The difference is significant on paper, but rarely material in practice. An "indemnity" policy willnever pay claims until the insured has paid out of pocket to some third party. Under the samesituation, a "pay on behalf" policy, the insurance carrier would pay the claim and the insured both. Most modern liability insurance is written on the basis of "pay on behalf" language.

Insurers make money in two ways:

(1) through Underwriting, the process by which insurers select the risks to insure and decidehow much in premiums to charge for accepting those risks and

(2) by investing the premiums they collect from insured parties.

Claims: - Finally, claims and loss handling is the materialized utility of insurance; it is the actual"product" paid for, though one hopes it will never need to be used.

Commercially insurable risks typically share seven commonCharacteristics:-

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 9/52

Limited risk of catastrophically large losses.

Calculable Loss

Affordable Premium

Large Loss

Accidental Loss

Definite Loss

A large number of homogeneous exposure units

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 10/52

CHAPTER 2

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 11/52

Health Care Insurance

Definition:-

The term health insurance is generally used to describe a form of insurance that paysFor medical expenses.

A health insurance policy is a contract between an insurance company and anIndividual, By estimating the overall risk of healthcare expenses, a routine finance structure(such as a monthly premium or annual tax) is developed, ensuring that money is available to payfor the healthcare benefits specified in the insurance agreement. The type and amount of healthcare costs that will be covered by the health plan are specified in advance, in the member contract or Evidence of Coverage booklet.

The concept of health insurance was proposed in 1694 by Hugh the Elder Chamberlainfrom the Peter Chamberlain family. Accident insurance was first offered in the United States bythe Franklin Health Assurance Company of Massachusetts. This firm, founded in 1850, offeredinsurance against injuries arising from railroad and steamboat accidents. Before the developmentof medical expense insurance, patients were expected to pay all other health care costs out of their own pockets, under what is known as the fee-for-service business model. During the middleto late 20th century, traditional disability insurance evolved into modern health insurance programs.

Today, most comprehensive private health insurance programs cover the cost of routine, preventive, and emergency health care procedures, and also most prescription drugs, butthis is not always the case.

The basic concept of health insurance is population solidarity. There are inherent risksin a population but the population absorbs the cost of risks to an individual by spreading theimpact of incurred costs amongst the insured population. However, if the population is split intoinsured and uninsured groups, or into selectively groups (as with private insurance with pre-insurance selection either by the insurance company or the insured) the concept of populationsolidarity breaks down. The insurance balances costs across a large, random sample of individuals. For instance, an insurance company has a pool of 1000 randomly selected

subscribers, each paying Rs.100 per month. One person becomes very ill while the others stayhealthy, allowing the insurance company to use the money paid by the healthy people to pay for the treatment costs of the sick person. However, when the pool is self-selecting rather thanrandom, as is the case with individuals seeking to purchase health insurance directly, adverseselection is a greater concern. Insurance systems must then typically deal with two inherentchallenges: adverse selection and ex-post moral hazard.

Because of adverse selection, insurance companies employ medical underwriting, using

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 12/52

a patient's medical history to screen out those whose pre-existing medical conditions pose toogreat a risk for the risk pool. Before buying health insurance, a person typically fills out acomprehensive medical history form that asks whether the person smokes, how much the personweighs, whether the person has been treated for any of a long list of diseases and so on. Ingeneral, those who present large financial burdens are denied coverage or charged high

premiums to compensate.

Moral hazard occurs when an insurer and a consumer enter into a contract under symmetricinformation, but one party takes action, not taken into account in the contract, which changes thevalue of the insurance. A common example of moral hazard is third-party payment — when the parties involved in making a decision are not responsible for bearing costs arising from thedecision. An example is where doctors and insured patients agree to extra tests which may or may not be necessary. Doctors benefit by avoiding possible malpractice suits, and patients benefit by gaining increased certainty of their medical condition. The cost of these extra tests is borne by the insurance company, which may have had little say in the decision. Co-payments,deductibles, and less generous insurance for services with more elastic demand attempt to

combat moral hazard, as they hold the consumer responsible.

Insurance companies like to compare buying health insurance after being diagnosedwith a serious medical condition like HCV to trying to buy fire insurance on a burning house.That sounds really logical….except….most fire insurance policies are never used as most housesdon‘t burn down. Everyone has medical problems, however, at one time or another.

To prevent a person from buying health insurance only when they need it, the insuranceIndustry uses a procedure called ―medical underwriting.‖ Loosely translated into plain English, itmeans ―discriminating against anyone we feel may cost us money.‖ And this type of discrimination against people with health problems is perfectly legal.

The French model of health insurance has been ranked by the World Health Organization as the best in the world, because it permits a high quality of care and nearly total patient freedom. . Itwas a compromise between Gaullist and Communist representatives in the French parliament.The Conservative Gaullists were opposed to a state-run healthcare system, while theCommunists were supportive of a complete nationalization of health care along a BritishBeverage model. The resulting programme was profession-based. All people working wererequired to pay a portion of their income to a health insurance fund, which mutualised the risk of illness, and which reimbursed medical expenses at varying rates. Children and spouses of insured people were eligible for benefits, as well. Each fund was free to manage its own budget andreimburse medical expenses at the rate it saw fit.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 13/52

Health Care Insurance Scenario In India

The health care system in India is characterized by multiple systems of medicine, mixedownership patterns and different kinds of delivery structures. During the last 50 years India hasdeveloped a large government health infrastructure with more than 150 medical colleges, 450district hospitals, 3000 Community Health Centers, 20,000 Primary Health Care centers and130,000 Sub-Health Centers. On top of this there are large number of private and NGO healthfacilities and practitioners scatters though out the country. Over the past 50 years India has madeconsiderable progress in improving its health status.

Public sector ownership is divided between central and state governments, municipaland Panchayat local governments. Public health facilities include teaching hospitals,Secondary level hospitals, first-level referral hospitals (CHCs or rural hospitals), dispensaries; primary health centres (PHCs), sub-centres, and health posts. Also included are public facilitiesfor selected occupational groups like organized work force (ESI), defense, governmentemployees (CGHS), railways, post and telegraph and mines among others.

The private sector (for profit and not for profit) is the dominant sector with 50 per cent of people seeking indoor care and around 60 to 70 per cent of those seeking ambulatory care (or outpatient care) from private health facilities.

India spends about 6% of GDP on health expenditure. Private health care expenditureis 75% or 4.25% of GDP and most of the rest (1.75%) is government funding. At present, theinsurance coverage is negligible. Most of the public funding is for preventive, promotive and primary care programes while private expenditure is largely for curative care. Over the periodthe private health care expenditure has grown at the rate of 12.84% per annum and for each one percent increase in per capital income the private health care expenditure has increased by1.47%. Number of private doctors and private clinical facilities are also expanding exponentially.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 14/52

Indian health financing scene raises number of challenges, which are:

1) I ncreasing health care costs,

2) High financial burden on poor eroding their incomes,

3) I ncreasing bur den of new diseases and health r isks and

4) Neglect of preventi ve and primary care and publi c health

functions due to under funding of the government health

care.

Around 24% of all people hospitalized in India in a single year fall below the poverty line

due to hospitalization (World Bank, 2002). An analysis of financing of hospitalization shows thatlarge proportion of people; especially those in the bottom fourincome quintiles borrow money or sell assets to pay for hospitalization (World Bank, 2002).

Given the above scenario exploring health-financing options becomes critical. In light of the fiscal crisis facing the government at both central and state levels, in the form of shrinking public health budgets, escalating health care costs coupled with demand for health-care services,and lack of easy access of people from the low-income group to quality health care, healthinsurance is emerging as an alternative mechanism for financing of health care.

Health insurance is very well established in many countries. As global insurance premiums grew by or 5% in real terms to reach $3.7 trillion due to improved profitability and a benign economicenvironment characterized by solid economic growth, moderate inflation and strong equitymarkets. Advanced economies account for the bulk of global insurance. The top four countriesaccounted for nearly two-thirds of premiums in 2006. The U.S. and Japan alone accounted for 43% of world insurance, much higher than their 7% share of the global population. Emergingmarkets accounted for over 85% of the wor ld‘s population but generated only around 10% of premiums. But in India the health insurance market is very limited covering about 10% of thetotal population. It is a new concept except for the organized sector employees. In India onlyabout 2 per cent of total health expenditure is funded by public/social health insurance while 18

per cent is funded by government budget. In many other low and middle income countriescontribution of social health insurance is much higher.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 15/52

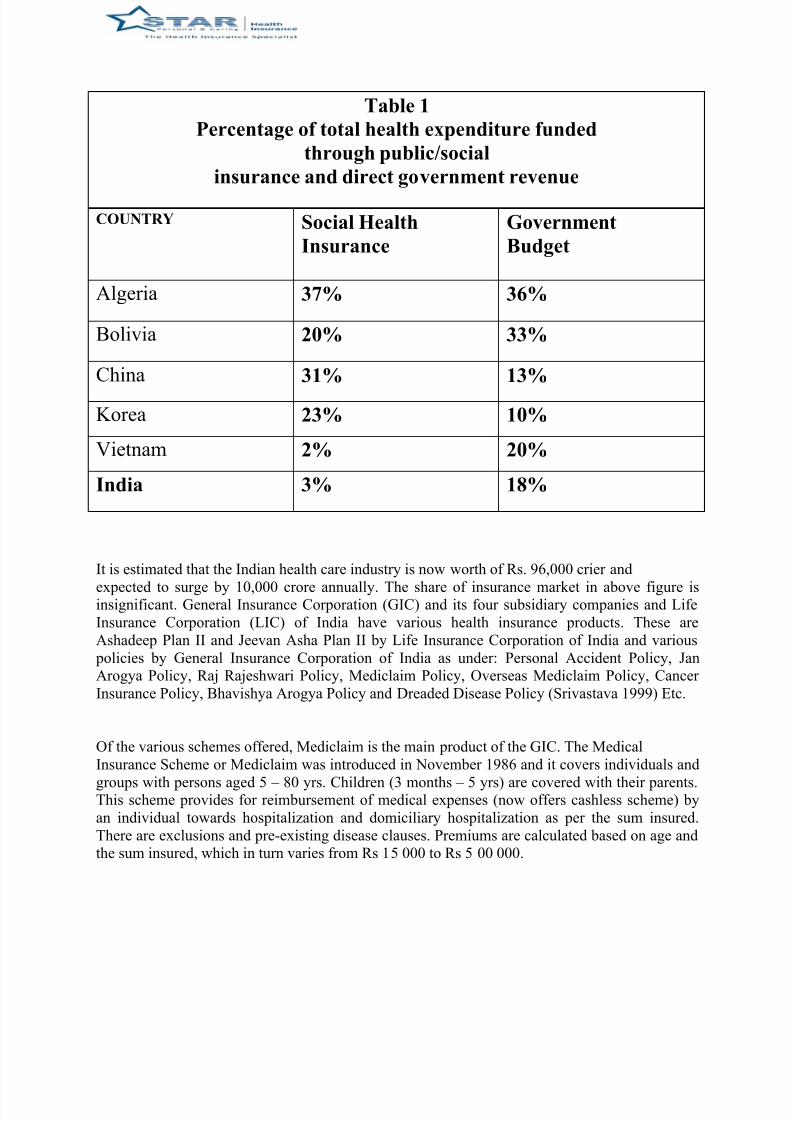

Table 1

Percentage of total health expenditure funded

through public/social

insurance and direct government revenue

It is estimated that the Indian health care industry is now worth of Rs. 96,000 crier and

expected to surge by 10,000 crore annually. The share of insurance market in above figure isinsignificant. General Insurance Corporation (GIC) and its four subsidiary companies and LifeInsurance Corporation (LIC) of India have various health insurance products. These areAshadeep Plan II and Jeevan Asha Plan II by Life Insurance Corporation of India and various policies by General Insurance Corporation of India as under: Personal Accident Policy, JanArogya Policy, Raj Rajeshwari Policy, Mediclaim Policy, Overseas Mediclaim Policy, Cancer Insurance Policy, Bhavishya Arogya Policy and Dreaded Disease Policy (Srivastava 1999) Etc.

Of the various schemes offered, Mediclaim is the main product of the GIC. The MedicalInsurance Scheme or Mediclaim was introduced in November 1986 and it covers individuals and

groups with persons aged 5 – 80 yrs. Children (3 months – 5 yrs) are covered with their parents.This scheme provides for reimbursement of medical expenses (now offers cashless scheme) byan individual towards hospitalization and domiciliary hospitalization as per the sum insured.There are exclusions and pre-existing disease clauses. Premiums are calculated based on age andthe sum insured, which in turn varies from Rs 15 000 to Rs 5 00 000.

COUNTRY Social Health

Insurance

Government

Budget

Algeria 37% 36%

Bolivia 20% 33%

China 31% 13%

Korea 23% 10%

Vietnam 2% 20%

India 3% 18%

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 16/52

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 17/52

Star Health & Allied Insurance Company

Star Health and Allied Insurance Co. is a joint venture between Oman Insurance Company, Mr.Syed Mohamed Salahuddin, Mr. Essa Abdullah Al Ghurair,leading Indian industrialists and

business houses. It is thier endeavor to provide dedicated, affordable and quality health insurancethat preserves and values human lives. This company aim to be the most favored brand in thehealth insurance segment. We offer a wide range of health insurance services and related products at affordable prices. Our prime objective is to offer services in the health segment thatenable you to manage stressful situations.

Star Health and Allied Insurance Company Limited (Star Health) has a capital base of Rs.108crores, more than what is adequate to form a General Insurance Company. However, Star Healthhas chosen to be in the field of Health and was the First stand-alone Health Insurance

Company in India and deals in Personal Accident, Mediclaim and Overseas Travel Insurance.

Mr. V. Jagannathan, Chairman cum Managing Director. He is a doyen of the Insuranceindustry with over 40 years of experience in Insurance. He has held various positions of authority, including that of CMD of one of India's largest Public Sector insurance companies.

BOARD OF DIRECTORS

Mr. Syed Mohamed Salahuddin - Chairman - Emeritus. Managing Director of ETA ASCONand ETA STAR group of Companies in Dubai, U.A.E

Mr. Essa Abdullah Al Ghurair was educated in San Diego, USA. The Al Ghurair family has business interests in Banking, Food & Beverages and Real estates.

Dr. M. Y. Khan is currently the Chairman of the Banking and Advisory council of YES Bank Ltd.

Mr. D. R. Kaarthikeyan is currently a visiting professor in many prestigious institutions.

Mr. V.P. Nagarajan is the Executive Director of ETA ASCON and ETA STAR group of Companies headquartered in Dubai, UAE.

Mr. Mohammed Hassan is a prominent educationalist and industrialist and has wideknowledge in the respective fields for over three decades.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 18/52

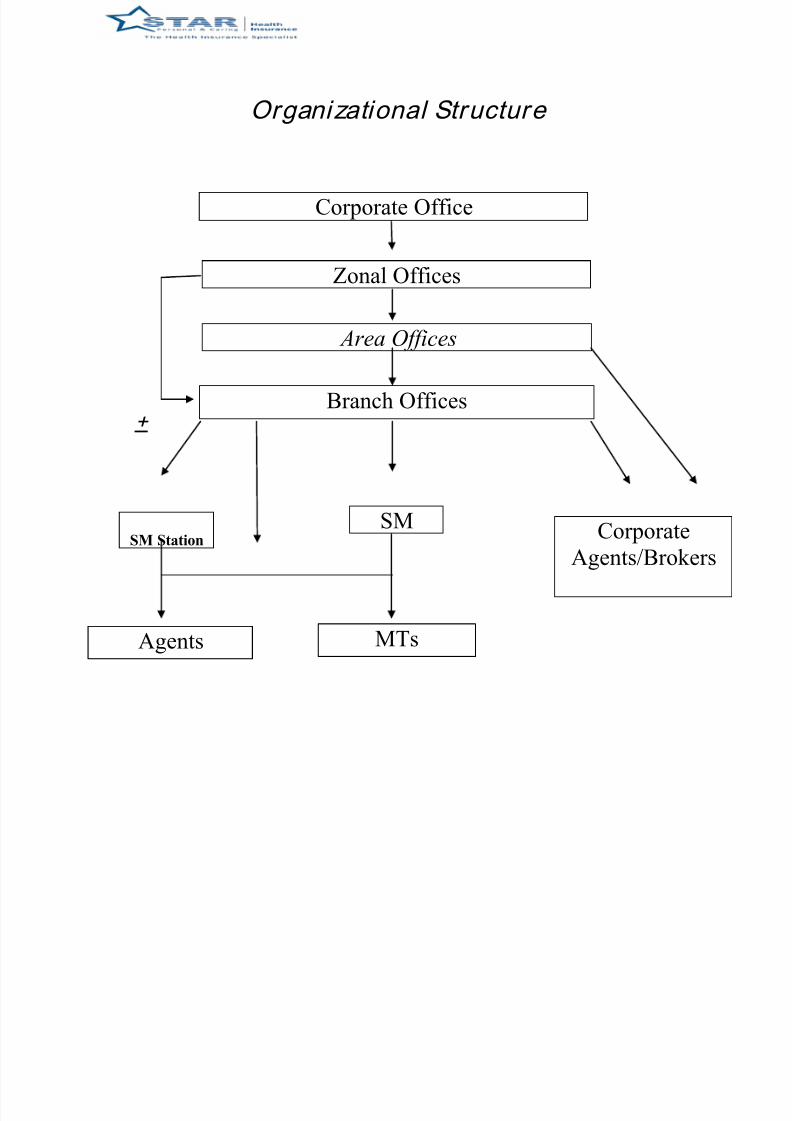

Organizational Structure

Corporate Office

+

Zonal Offices

Area Offices

Branch Offices

SMSM Station

CorporateAgents/Brokers

MTsAgents

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 19/52

Star Health & Al l ied Insurance Company

Is the first stand alone health insurance Company in India. It specializes in

Health Insurance, provides quality service at the best rates, and commitsitself to the service of the insured.

Offers hassle free cashless settlement to the insured. There is no Third Party

Administrator involved, which means better service, in shorter time and no

hassles... at all!

Provides a No Claim Discount - one that has never been offered before in

the country.

Has a round-the-clock GP service, which provides counseling and advice.

When necessary the insured will be guided to the Company's large network

of doctors in different localities.

Provides periodic health check up for the clients. Has a range of policies

suited to every age group, different health aspects and concerns.

. # And last but not the least, STAR HEALTH is first and foremost, a dedicated insurer who cares for your health...in every way!

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 20/52

Exclusive Features

Cashless service without TPA intervention the USP of the Company

Direct tie-up with hospitals on all India basis

24 hours General Practitioner's advice and medical counseling

24x7 in-house Call Center

Toll free telephone assistance

Complete knowledge backed website to offer medical information, including healthtips.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 21/52

Our VisionProtecting Health Promoting Health

Our MissionUltimate Customer Satisfaction

Trust and EthicsWe believe honesty and integrity

are essential to our success.

Conducive work environmentTo create an environment that is conducive

to Customer Satisfaction, Innovation and

Belongingness.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 22/52

CommitmentWe are committed to become a STAR in

health and related insurance.

The study will have following types of insurance policies :-

1. Mediclaim Policy

2. Family health optima insurance plan

3. Senior citizens red carpet

4. Personal accident insurance

Objectives

1. To study the underwriting Guidelines/procedure of selected policies which are being practiced in the insurance company.

2. To calculate & suggest possible ways to decrease the turn around time in theunderwriting procedure for each policy.

3. To do a SWOT analysis for the purpose of comparison.

5. To study the existing web services & alerts for the purpose of policy underwriting & post policy services.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 23/52

UNDERWRITTING

The most complicated aspect of the insurance business is the underwriting of policies. There are 2different methods of application that anyone looking for personal health insurance must be awareof. These are

1. Full Medical Underwriting (FMU)

2.

Moratorium (MOR).

Underwriting in relation to health insurance basically involves the disclosure of certaininformation to an insurance company which they can then access to decide when pre-existingconditions should be excluded from cover. With some policies one will be required to completean application form that details full medical history where as with a moratorium policy your medical history will only become an issue at the point you need to make a claim.

Policies requiring a medical history declaration, or full medical underwriting, require the

applicant to complete an application form that details the full medical history for each applicant.Private health insurance companies consult an applicant's GP in order to verify conditions or toinvestigate an applicant's medical history further. Having submitted medical history a decisionwill be made by the health insurance company as to whether or not they will cover any previousmedical conditions.

The rules surrounding ‗Duty of Disclosure' when applying for personal health insurance

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 24/52

are quite strict. It is one‘s duty to disclose any fact or circumstance about your health that isknown to you at your time of application. The main reason behind this disclosure is to identify if you have any pre-existing conditions that will be excluded from treatment from your healthinsurance policy.

Most health insurance providers will not pay benefits for any conditions that you have beentreated for in the past or have arranged treatment for prior to taking out your medical insurance policy. This also includes any chronic conditions that have been diagnosed before the healthinsurance policy was granted. If you fail to disclose details of any illness at the start of your health insurance application then you could be denied a future claim or your personal healthinsurance could be deemed invalid.

Some health insurance providers may agree to cover pre-existing conditions in exchange for additional premiums, but this will depend entirely upon the condition in question and its severity,how long you have had it and what treatment you have had or are still having for that condition.Again, each health insurance company is different with different policies so make sure youalways do your homework with regards to what is and what is not included.

If you opt for a policy that requires full medical underwriting then all your medical historywill be available to your insurers up front enabling them to make an informed judgement beforeconfirming your policy. A moratorium policy is however a little bit different as this type of application process does not require disclosure of medical history when joining. Instead anyillness is assessed at the point of making a claim.

With moratorium you do not need to fill in a health questionnaire. Instead, pre-existingconditions for which you (and any dependant included in your application) have receivedtreatment and/or medication, or asked advice on, or had symptoms of (whether or notdiagnosed), during the four years immediately before your private health insurance cover startedwill automatically be excluded from cover.

However, if you do not have any symptoms, treatment, medication, or advice for those pre-existing conditions, and any directly related conditions, for two continuous years after your policy starts, then insurers may reinstate cover for those conditions.

When choosing a personal health insurance provider it is vital that you understand thedifferences between policies and which one is best suited. With any insurance companythough it is always better to be honest from the outset to avoid any disappointment or heftymedical bills further down the line. With Full Medical Underwriting the boundaries are perhapsclearer as everything will be documented from the outset and assessed by your insurer before the policy is approved leaving you with a clear understanding of exactly what your personal healthinsurance covers you for. Using a wide assortment of data, insurers predict the likelihood that a

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 25/52

claim will be made against their policies and price products accordingly. To this end, insurersuse actuarial science to quantify the risks they are willing to assume and the premium they willcharge to assume them. Data is analyzed to fairly accurately project the rate of future claims based on a given risk. Actuarial science uses statistics and probability to analyze the risksassociated with the

range of perils covered, and these scientific principles are used to determine an insurer's overallexposure. Upon termination of a given policy, the amount of premium collected and theinvestment gains thereon minus the amount paid out in claims is the insurer's underwriting profiton that policy. Of course, from the insurer's perspective, some policies are winners (i.e., theinsurer pays out less in claims and expenses than it receives in premiums and investmentincome) and some are losers (i.e., the insurer pays out more in claims and expenses than itreceives in premiums and investment income).

- incurred loss - underwriting expenses.

ways:

underwriting, the process by which insurers select the risks to insure and

decide how much in premiums to charge for accepting those risks.

investing the premiums they collect from insured parties.

Insurance companies also earn investment profits on ―float‖. ―Float‖ or available reserve is the

amount of money, at hand at any given moment, that an insurer has collected in insurance premiums but has not been paid out in claims. Insurers start investing insurance premiums assoon as they are collected and continue to earn interest on them until claims are paid out.

Some insurance industry insiders, most notably Hank Greenberg, do not believe that it is forever possible to sustain a profit from float without an underwriting profit as well, but this opinion isnot universally held. Naturally, the ―float‖ method is difficult to carry out in an economicallydepressed period. Bear markets do cause insurers to shift away from investments and to toughenup their underwriting standards. So a poor economy generally means high insurance premiums.This tendency to swing between profitable and unprofitable periods over time is commonly

known as the "underwriting" or ―insurance cycle‖

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 26/52

Medial Underwr iting:-

On receiving an application from an individual for health insurance, the insurance companycarefully scrutinizes the applicant's medical history and other factors to decide whether to offer

coverage or not and if yes, then on what rate and on what conditions. Each insurance companydevelops its own underwriting guidelines to outline the characteristics the company considersdesirable and those that make an applicant ineligible for coverage. Health insurers avoidindividuals or groups that they think may be likely to make claims, either because of poor healthor because the person or company is financially unstable. Insurance companies use the term"adverse selection" to describe the tendency for only those who will benefit from insurance to buy it. Specifically when talking about health insurance, unhealthy people are more likely to purchase health insurance because they anticipate large medical bills. On the other side, peoplewho consider themselves to be reasonably healthy may decide that medical insurance is anunnecessary expense; if they see the doctor once a year and it costs Rs.250/-, that's much better than making monthly insurance payments of Rs.40/- (example figures).

Because of adverse selection, insurance companies employ medical underwriting, using a patient's medical history to screen out those whose pre-existing medical conditions pose too greata risk for the risk pool. Before buying health insurance, a person typically fills out acomprehensive medical history form that asks whether the person smokes, how much the personweighs, whether the person has been treated for any of a long list of diseases and so on. One

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 27/52

large industry survey found that roughly 13 percent of applicants for comprehensive,individually purchased health insurance who went through the medical underwriting in 2004were denied coverage. Declination rates increased significantly with age, rising from 5 percentfor individuals 18 and under to just under a third for individuals aged 60 to 64. Among thosewho were offered coverage, the study found that 76% received offers at standard premium rates,

and 22% were offered higher rates.

The premium structure is not designed for the extra risk assumed by insuring persons who drink intoxicants to excess, who are victims of drug habits, who are reckless in their manner of livingor choice of associates or who have questionable reputations. Such persons are not eligible for health insurance." All companies selling individual major medical insurance policies examinethe medical history of every applicant, using questions on the application, follow-up phone calls,Medical Information Bureau reports, paramedical exams, and blood and urine samples. Medicalunderwriting manuals are extensive and include detailed discussions of known illness for each of

the body's systems (circulatory, nervous, reproductive, etc.)Moral hazard occurs when an insurer and a consumer enter into a contract under symmetricinformation, but one party takes action, not taken into account in the contract, which changes thevalue of the insurance. A common example of moral hazard is third-party payment — when the parties involved in making a decision are not responsible for bearing costs arising from thedecision. An example is where doctors and insured patients agree to extra tests which may or may not be necessary. Doctors benefit by avoiding possible malpractice suits, and patients benefit by gaining increased certainty of their medical condition. The cost of these extra tests is borne by the insurance company, which may have had little say in the decision. Co-payments,deductibles, and less generous insurance for services with more elastic demand attempt tocombat moral hazard, as they hold the consumer responsible.

Underwriting is a way of determining the insurability of the client by reviewing his/her medicaland financial details using various risk classification models. This practice can be dated back to1800 B.C, when undertaking risk, or underwriting risk, of ships with goods was done. Fromthose days, underwriting has evolved greatly and is presently categorized into life and non-lifeunderwriting, both including financial underwriting. Life underwriting can be further dividedtechnically into medical and non-medical underwriting.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 28/52

Here are a few tips for prudent medical underwriting:

1. Use your analytical mind - Ask, “Does it make sense” Always ask yourself whether the data given makes sense. In most of the cases the data presentedcan be manipulated or it can be false positives. For example, a client can take a hypoglycemic

drug and go for a fasting blood glucose test or the value of nine given can be HbA1, when aHbA1c test was to be performed.

2. Read between the linesAnalyze what is not given in the data provided or find the potential risks the medical reports point to. For example, a 44-year-old female undergoing tooth extraction was also asked toundergo an electrocardiogram and fasting blood sugar test. This data created a doubt and whenfurther investigated revealed diabetes mellitus.

3. Study medical history and genetic susceptibilityCarefully analyze the medical history as it can give you a lot of information about the client‘s current health status and possible endothelial damage, which must have occurred in their body.For example, in the case of diabetes, hypertension along with the date of diagnosis can provide aclear idea on the risks involved. Also some disorders are genetically manifested, for examplearthritis, thallassemia, diabetes, arthritis and obesity to name a few. Hence understanding themedical history of the client and his first line relatives can provide substantial data for classifyingthe risk to him.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 29/52

4. Do not look from a clinical point of viewRemember insurance medicine is different from clinical medicine. You as medical underwriter are not required to identify the root cause of the disease, but to identify the pathology andanalyze how much risk it presents to the life of the client and also within how much time theclient is going to suffer from that expected disease.

5. Use probability principlesUse probability principles to evaluate the chances of death or susceptibility to critical illnessescovered by the health insurance product proposed within that span of the coverage by thecompany.

6. Do not think long termA medical underwriter should not think from a long-term point of view. Remember you shouldonly be interested up to the extent of the duration of the plan proposed. In addition, you need toevaluate if the risk cover age money (premium) is recovered within the first few years of the plan. Then you should evaluate the risk and underwrite, taking into consideration only that

duration of time.

7. Correlate all findingsHuman body mechanisms are complex and interrelated processes. Try to find the correlation between the different pathologies and sum them up to find the total risk presented by the client.For example, a person with diabetes mellitus and smoking presents a higher risk than that presented by the person with only diabetes mellitus.

8. Apply Cost Benefit analysisA medical underwriter is also required to have an understanding of financial terms like cost benefit analysis and use them prudently to evaluate the risk.

Key Findings in Star Health & Allied

Insurance Company Ltd

It is the first stand alone health insurance company in India. It specializes in Health Insurance, provides quality service at the best rates, and commits itself to the service of the insured.TheCompany is led by a group of leading industrialists and business houses in the subcontinent.

Oman Insurance Company is one of the leading Insurance Companies in the MiddleEast. Mr. Essa Abdullah Al Ghurair hails fssrom the prominent Al Ghurair family in the 0U.A.E.With a net worth of USD 3.7 billion, the family has been ranked as one of the world's richest byForbes magazine...

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 30/52

The company has it‘s Head Office in Chennai, Corporate Office in Mumbai & Regional Office

in Pune from last three years. Looking at the potential of vidarbha region the company started its branch office in nagpur in october 2008.

The organisational structure for this branch is as follows:

PolicyUnderwrite

The company has very strong financial backup & very good leadership which two arethe most important factors for any company to become successful. The company has recordeditself as the fastest growing company with 400% of growth rate.

Looking at the indian scenario of Health insurance, which remained highly underdeveloped anda less significant segment of the product portfolios of the nationalized insurance companies inIndia, There was need of such type of company dealing only in health insurance. Therefore thereis overwhelming response from the consumers. Only in Nagpur from last 3 – 4 months over 400 policies are sold which comes around 4 – 5 policies per day.

Here comes the role of an underwriter as Health sector policy formulation, assessment andimplementation is an extremely complex task especially in a changing epidemiological,institutional, technological, and political scenario. Further, given the institutional complexity of

our health sector programmes and the pluralistic character of health care providers.\

Though policy underwriting is done in the branch office for those not requiring medicalexamination as they are below 50 years of age, those proposers who are above 50 years of age,their medical underwriting is done at regional office pune.

The work load here is though not much as the company is in its cradle phase still the underwriter confirms the policy underwriting in minimum time which varies from half hour to 4 hours for policies not requiring medical underwriting, & those requiring medical underwriting may varyfrom 24 hours to 15 days. The major factor here of concern is delay from the proposer in

submitting medical documents. If time phase is considered from the submission of medicalreports to the issuing of policy it comes to around 12 hours to 48 hours.

UNDERWRITTING GUIDELINES FOR VARIOUS

PRODUCTS

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 31/52

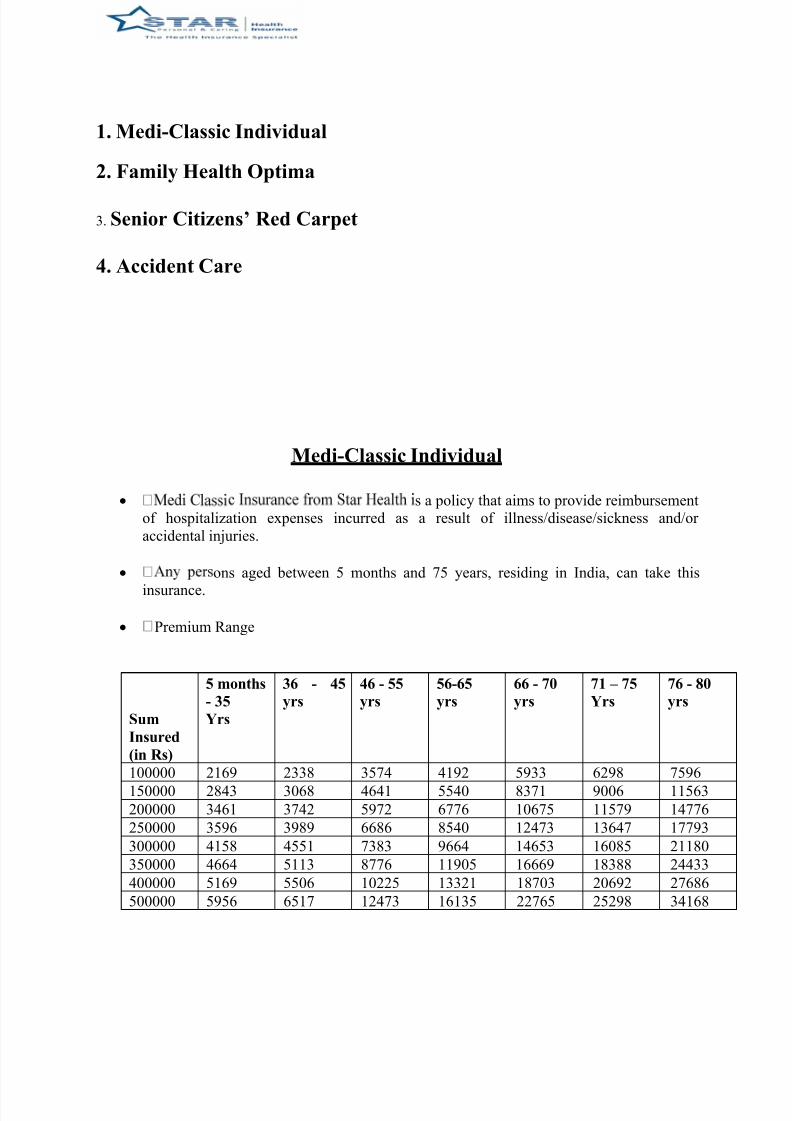

1. Medi-Classic Individual

2. Family Health Optima

3. Senior Citizens’ Red Carpet

4. Accident Care

Medi-Classic Individual

s a policy that aims to provide reimbursementof hospitalization expenses incurred as a result of illness/disease/sickness and/or accidental injuries.

ons aged between 5 months and 75 years, residing in India, can take this

insurance.

Premium Range

Sum

Insured

(in Rs)

5 months

- 35

Yrs

36 - 45

yrs 46 - 55

yrs

56-65

yrs

66 - 70

yrs

71 – 75

Yrs

76 - 80

yrs

100000 2169 2338 3574 4192 5933 6298 7596

150000 2843 3068 4641 5540 8371 9006 11563200000 3461 3742 5972 6776 10675 11579 14776

250000 3596 3989 6686 8540 12473 13647 17793

300000 4158 4551 7383 9664 14653 16085 21180

350000 4664 5113 8776 11905 16669 18388 24433

400000 5169 5506 10225 13321 18703 20692 27686

500000 5956 6517 12473 16135 22765 25298 34168

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 32/52

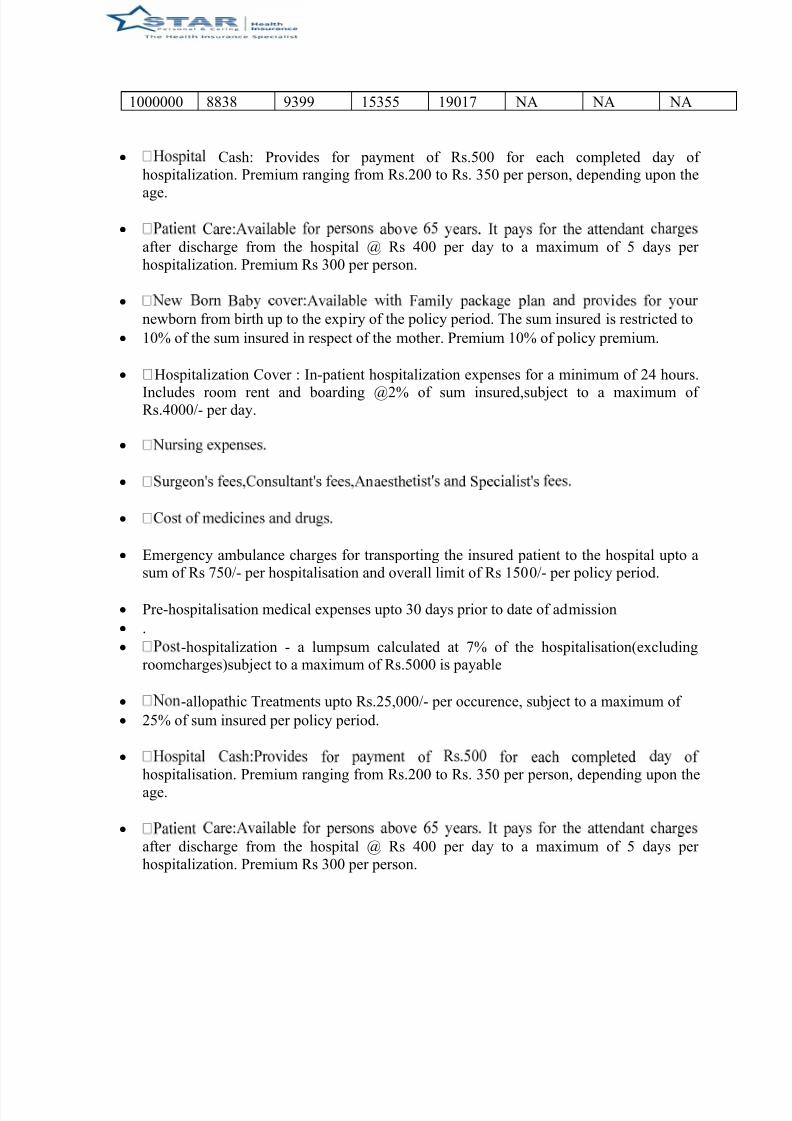

1000000 8838 9399 15355 19017 NA NA NA

Cash: Provides for payment of Rs.500 for each completed day of hospitalization. Premium ranging from Rs.200 to Rs. 350 per person, depending upon the

age.

after discharge from the hospital @ Rs 400 per day to a maximum of 5 days per hospitalization. Premium Rs 300 per person.

newborn from birth up to the expiry of the policy period. The sum insured is restricted to

10% of the sum insured in respect of the mother. Premium 10% of policy premium.

Hospitalization Cover : In-patient hospitalization expenses for a minimum of 24 hours.

Includes room rent and boarding @2% of sum insured,subject to a maximum of Rs.4000/- per day.

Emergency ambulance charges for transporting the insured patient to the hospital upto a

sum of Rs 750/- per hospitalisation and overall limit of Rs 1500/- per policy period.

Pre-hospitalisation medical expenses upto 30 days prior to date of admission

.

-hospitalization - a lumpsum calculated at 7% of the hospitalisation(excludingroomcharges)subject to a maximum of Rs.5000 is payable

-allopathic Treatments upto Rs.25,000/- per occurence, subject to a maximum of

25% of sum insured per policy period.

hospitalisation. Premium ranging from Rs.200 to Rs. 350 per person, depending upon theage.

after discharge from the hospital @ Rs 400 per day to a maximum of 5 days per hospitalization. Premium Rs 300 per person.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 33/52

newbornfrom birth up to the expiry of the policy period. The sum insured is restricted to

10% of the sum insured in respect of the mother. Premium 10% of policy premium.

Sectin 80D of the Income Tax Act.

Exclusions :-

Expenses for the treatment of any illness/disease/condition,which is pre-existing

Treatment of illness/disease/sickness contracted by the insured person during the first30 days from the commencement date of this policy

First Two Years Exclusions: Cataract,Hysterectomy for Menorrhagia or Fibromyoma,Replacement surgery for knee and/or joint(other than caused by anaccident),Prolapse of intervertibral disc (other than caused by accident), Varicose Veinsand Varicose Ulcers

FirstYearExclusions:Benign Prostate Hypertrophy,Hernia,Hydrocele,Fistula in

anus,Piles,Sinusitis and related disorders,Congenital internal disease/defect,removal of gallstones and renal stone

Naturopathy treatment

Expenses which are purely diagnostic in nature with no positive existence of anydisease

Treatment of Cogential external disease/defects/anomalies

Expenses which are mainly cosmetic in nature

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 34/52

Family Health Optima

Family Health Optima from Star Health is a health insurance plan that gives protectionfor the entire family on the payment of a single premium under a single sum insured.

The sum insured floats among the family members insured. It‘s just one more way to tighten the family bonds.

Any person aged between 5 months and 65 years residing in India can take this insurance

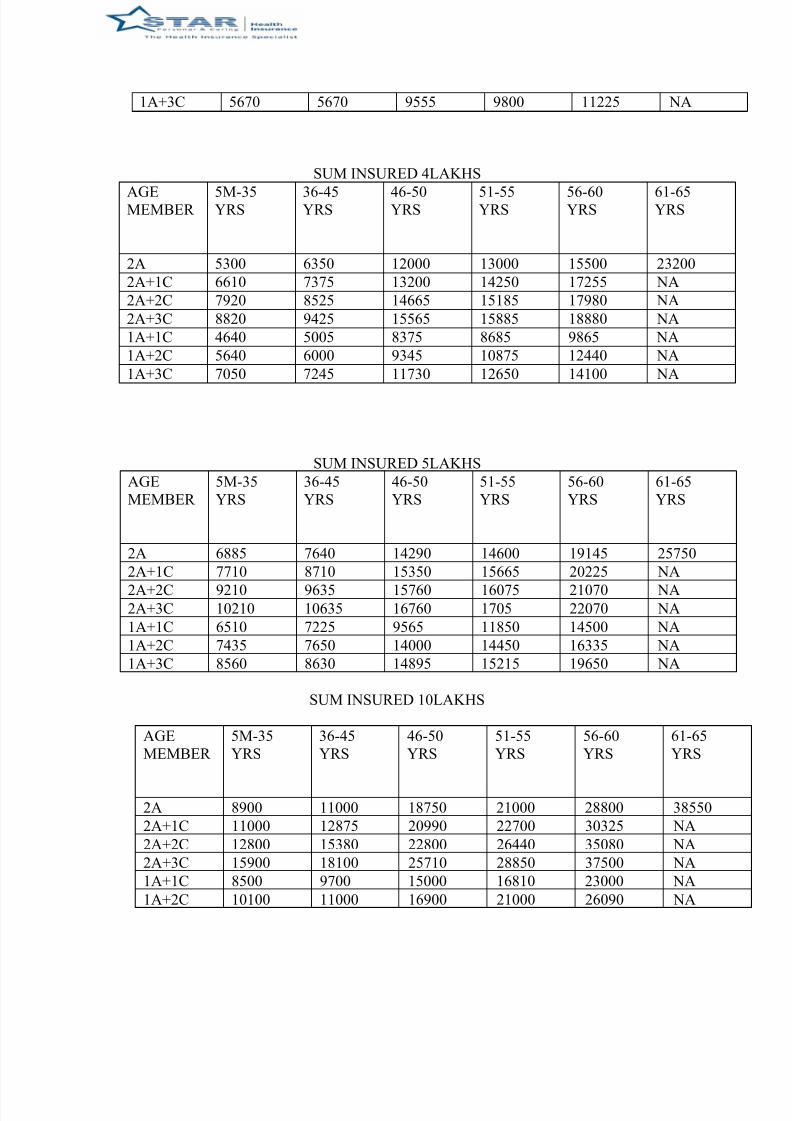

SUM INSURED 3LAKHS

AGEMEMBERS

5M-35YRS

36-45YRS

46-50YRS

51-55YRS

56-60YRS

61-65YRS

2A 4200 5170 9085 9345 12090 18750

2A+1C 5300 5555 10565 10830 12830 NA

2A+2C 6565 6775 11340 11605 13390 NA

2A+3C 7465 7675 12240 12505 14290 NA

1A+2C 3875 4275 7010 7335 8645 NA

1A+1C 4910 5100 7810 8770

9510 NA

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 35/52

1A+3C 5670 5670 9555 9800 11225 NA

SUM INSURED 4LAKHS

AGEMEMBER 5M-35YRS 36-45YRS 46-50YRS 51-55YRS 56-60YRS 61-65YRS

2A 5300 6350 12000 13000 15500 23200

2A+1C 6610 7375 13200 14250 17255 NA

2A+2C 7920 8525 14665 15185 17980 NA

2A+3C 8820 9425 15565 15885 18880 NA

1A+1C 4640 5005 8375 8685 9865 NA

1A+2C 5640 6000 9345 10875 12440 NA

1A+3C 7050 7245 11730 12650 14100 NA

SUM INSURED 5LAKHS

AGEMEMBER

5M-35YRS

36-45YRS

46-50YRS

51-55YRS

56-60YRS

61-65YRS

2A 6885 7640 14290 14600 19145 25750

2A+1C 7710 8710 15350 15665 20225 NA

2A+2C 9210 9635 15760 16075 21070 NA2A+3C 10210 10635 16760 1705 22070 NA

1A+1C 6510 7225 9565 11850 14500 NA

1A+2C 7435 7650 14000 14450 16335 NA

1A+3C 8560 8630 14895 15215 19650 NA

SUM INSURED 10LAKHS

AGEMEMBER

5M-35YRS

36-45YRS

46-50YRS

51-55YRS

56-60YRS

61-65YRS

2A 8900 11000 18750 21000 28800 38550

2A+1C 11000 12875 20990 22700 30325 NA

2A+2C 12800 15380 22800 26440 35080 NA

2A+3C 15900 18100 25710 28850 37500 NA

1A+1C 8500 9700 15000 16810 23000 NA

1A+2C 10100 11000 16900 21000 26090 NA

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 36/52

1A+3C 12575 13895 20100 25660 27775 NA

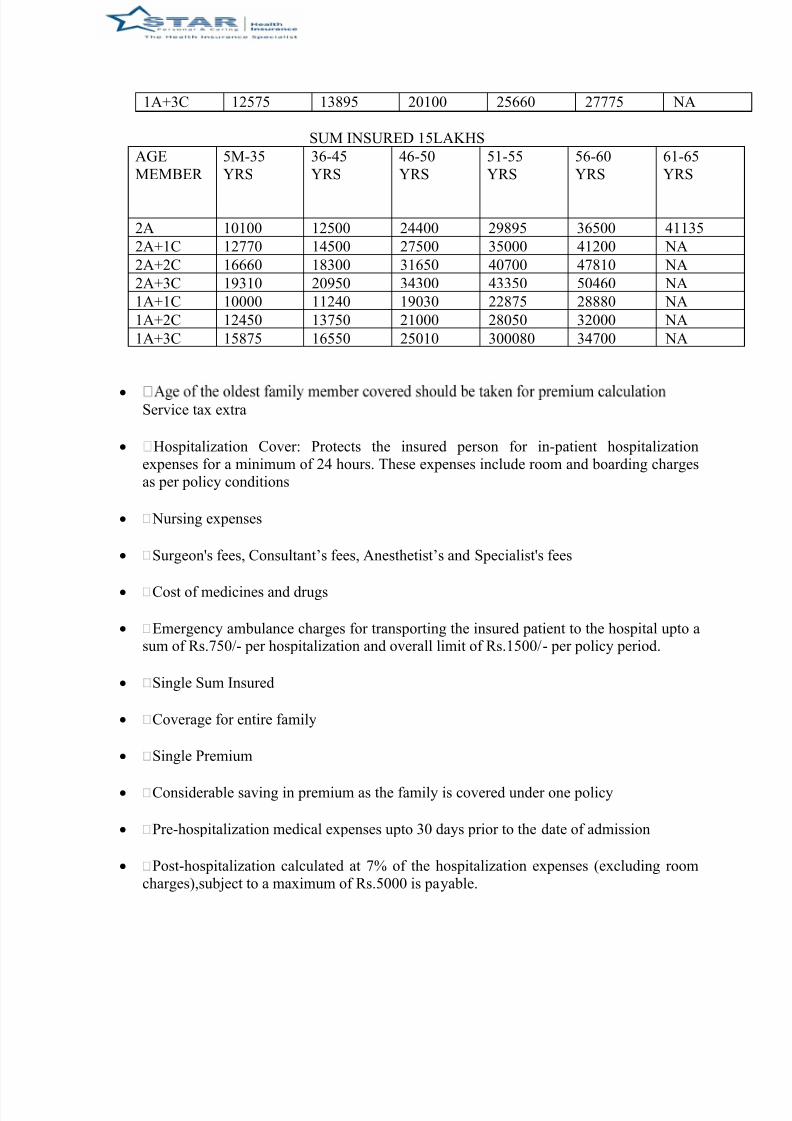

SUM INSURED 15LAKHS

AGEMEMBER

5M-35YRS

36-45YRS

46-50YRS

51-55YRS

56-60YRS

61-65YRS

2A 10100 12500 24400 29895 36500 41135

2A+1C 12770 14500 27500 35000 41200 NA

2A+2C 16660 18300 31650 40700 47810 NA

2A+3C 19310 20950 34300 43350 50460 NA

1A+1C 10000 11240 19030 22875 28880 NA

1A+2C 12450 13750 21000 28050 32000 NA

1A+3C 15875 16550 25010 300080 34700 NA

Service tax extra

Hospitalization Cover: Protects the insured person for in-patient hospitalizationexpenses for a minimum of 24 hours. These expenses include room and boarding chargesas per policy conditions

Nursing expenses

Surgeon's fees, Consultant‘s fees, Anesthetist‘s and Specialist's fees

Cost of medicines and drugs

Emergency ambulance charges for transporting the insured patient to the hospital upto asum of Rs.750/- per hospitalization and overall limit of Rs.1500/- per policy period.

Single Sum Insured

Coverage for entire family

Single Premium

Considerable saving in premium as the family is covered under one policy

Pre-hospitalization medical expenses upto 30 days prior to the date of admission

Post-hospitalization calculated at 7% of the hospitalization expenses (excluding roomcharges),subject to a maximum of Rs.5000 is payable.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 37/52

Proposer, spouse, dependent children upto 25 years those who are economicallydependent on their parents.

A discount of 10% on Premium is allowed on renewal of the policy if there is no claimin the immediately preceding year of the policy. This discount is not cumulative.

Payment by cheque for this insurance is eligible for relief under Section 80D of theIncome Tax Act.

Exclusions:-

Expenses for the treatment of any illness/ disease/condition which is pre-existing

Treatment of illness/disease/sickness contracted by the insured person during the first

30 days from the commencement date of the policy

First four Years Exclusions:Cataract,Hysterectomy for Menorrhagia or Fibromyoma,Replacement surgery for knee and/or joint (other than caused by anaccident),Prolepses of intervertebral disc(other than caused by accident),varicose veinsand varicose ulcers

First Year Exclusions:Benign Prostate Hypertrophy,Hernia,Hydrocele,Fistula inanus,Piles,Sinusitis and related disorders,congenital internal disease/defects, removalof gallstones and renal stone

Naturopathy treatment

Expenses which are purely diagnostic in nature with no positive existence of anyDisease

Expenses incurred for non-allopathic treatment

Treatment of external Congential disease/defects/anomalies

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 38/52

Expenses which are mainly cosmetic in nature

Senior Citizens’ Red Carpet

Turning sixty is a major milestone and for people,a time to start being more careful about their health.It is a matter of concern that insurance policies are hardly available to address this criticalrequirement.STAR Health is proud to introduce India's first health insurance policy aimedspecifically at senior citizens.It provides cover for anyone over the age of 60 and permits entryright up to the age of 69 with continuing cover after that.It is our way of caring for a generation that has done so much to build the country.

For people aged between 60 and 69 years

Guaranteed renewals beyond 69 years

No pre-insurance medical test required

Treatment at network hospitals only

All pre-existing diseases are covered from first year,except those for which treatment or advice was recommended by or received during the immediately preceding 12 monthsfrom the date of proposal

Disease for which treatment or advice was recommended by or received during the

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 39/52

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 40/52

A discount of 10% of the above premium will be allowed if the Proposer produces thefollowing documents to the satisfaction of the Company

Stress Thallium Report*

BP report*

Sugar (blood & urine)*

Blood urea & creatinine*

Self-declaration or certification that surgeries related to Heart / Brain / Cancer has /have not been done in the past *The tests should have been taken not before 45 days fromthe date of proposal.

Premium paid by cheque or credit card is eligible for relief as provided under Section

80 D of the Income Tax Act.

Exclusions:-

Treatments currently availed or availed during the previous 12 months from date of Proposal

Any expenses incurred for treatment of illness/disease/sickness contracted by theinsured person during the first 30 days from the commencement date of the policy

First Two-year exclusions : Hernia, Piles, Hydrocele, Congenital Internaldisease/defect, Sinusitis, Gall Stone/Renal Stone removal and Benign ProstrateHypertrophy

Two-Year Exclusions:Hysterectomy,Cataract,Joint/Knee Replacement surgery(other than caused by an accident),Prolapsed Intervertebral Discs,Varicose Veins,Ulcers

Naturopathy treatement

Expenses which are purely diagnostic in nature with no positive existence of anydisease

Expenses for treatments that are mainly cosemtic in nature

50% co-payment applicable for pre-existing diseases conditions

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 41/52

30% co-paument applicable for all other claims.

Accident Care

An accident can put anyone‘s future at risk. While an accident can be sudden, guarding againstthem can be a conscious deliberate decision. STAR Health Accident CareInsurance provides compensation in the event of death, permanent disability and injuries suffereddue to accidents

Accidental death

Permanent disability – total or partial – following an accident

Temporary total disablement – the Insured Person is eligible for a weekly benefit at 1%of Capital Sum Insured (following an accident) subject to maximum of Rs.5000/- per week for a for 100 weeks

Educational grant to children (1 Child – Rs.5000/-, 2 Children – Rs.10,000/-)

Transportation expenses of mortal remains (Rs.3000/-)

Travel expenses of one relative (Rs.1000/-)

Cumulative Bonus of 5% accrues to the Insured Person for every claim free year,subject to a maximum of 50%

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 42/52

For purpose of rating, persons proposed for insurance are classified under three risk Groups

Risk Group I – Persons engaged primarily in administrative functions

Risk Group II – Persons engaged in manual work other than what is specifically provided for under Group III

Risk Group III – Persons working in explosives industry, mines workers, high tension\electric supply, horse racing including jockeys, athletes and occupations of similar hazards

The Insurance may be renewed under mutual consent

Exclusions

Expenses incurred on events occurring before the commencement of the cover or otherwise outside the Period of Insurance

Any claim in respect of Pre-existing condition

Any claim if the insured acts against the advice of a physician

Any claim arising out of Accidents that the Insured Person has caused intentionally or by committing a crime or as a result of drunkenness or addiction (drugs, alcohol, etc)

Any claim arising out of mental disorder, suicide or attempted suicide self inflictedinjuries, or sexually transmitted conditions, anxiety, etc

Participation in Hazardous Sport/Hazardous activities

Persons who are physically and mentally challenged unless specifically agreed and

endorsed in the policy

2.Overseas Health Insurance :-

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 43/52

Star Corporate travel Protect

Star Corporate travel Protect

Globalization and business expansion have increased the need for traveling between countries.People who travel also hold positions of high responsibility in their organizations. While all riskscannot be avoided, STAR Health protects corporate executives during their travel by coveringthem against most risks arising out of travel so they can focus on the job at hand and accomplishtheir objectives.

Features

Emergency medical expenses whilst you travel/stay abroad

Emergency medical transportation to India

Repatriation of mortal remains

Any dental emergency expenses following an accident

Compensation following accidental injuries

Cost of loss of traveler's checked-in baggage

Reasonable expenses incurred for obtaining new passport

Star Family Travel Protect

Star Student Travel Protect

Star individual Travel Protect

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 44/52

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 45/52

Star Student Travel Protect

Students traveling abroad are already on their own and need help if they are ever laid low by anillness. STAR Health has a specially designed Student Travel Protect Insurance that protectsthem during a crucial phase because medical treatment abroad can be prohibitively expensive inmost cases.

Medical Benefits

Emergency medical expenses

Emergency transportation back to India

Repatriation of mortal remains

Dental emergency expenses following an accident

Travel Related Benefits

For injuries caused by accidents

For checked in baggage

Compassionate Benefits

Visit of one immediate family member, in case of hospitalization

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 46/52

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 47/52

Claims Procedure

Inform the ID number for easy referenceon toll free number

In case of planned hospitalization, it should be informed 24 hours prior to admission into

hospital

In case of emergency hospitalization,information to be given within 24 hours after

hospitalization

In non-network hospitals, payment must bemade upfront and then reimbursement will be

effected on the submission of documents.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 48/52

The Medical Officer will personally visit thehospital for overlooking & taking proper follow

up of the claim & fills the field visit report

The Medical Officer will personally visit thehospital for overlooking & taking proper follow

up of the claim & fills the field visit report

KEY INTERPRETATIONS

There is still much scope to explore the market as the city population is above30,00,000 & only 2 – 5% of population is covered under any kind of health insurancecoverage.

Various marketing activities are done to promote the company.

Underwriting procedures are done cautiously for overall risk assessment & if found outof the box full efforts are taken to cover that person under some different plan

Personal freedom is given to the Sales Managers to explore his / her talent and generate business by his / her innovative ideas.

Underwriting guidelines are user friendly and fitted into the software called PREMIA.

The software sometimes becomes trouble creator due to inefficiency of either internet

connectivity or continuous power supply.

Medical underwriting is taken care by qualified doctors at Pune due to under load of work.

Company possesses reminder software which generates alerts before expiry of the policy after one year for renewal.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 49/52

There is a fixed prototype of policy underwriting due to software in which changes canonly occur through higher centers.

Some Suggestions for considerations:-

market.

As the work load goes up unedrwritting procedures should be more cautiously done for not accepting doubtful cases so the repudiation rate of the claims can also be reducedthereby reducing disappointment for the policy holders.

d 12 15cases per day reduce the turn around time required for policy issuing.

-network hospitals should be empanelled as soon as possible after confirming their genuiness to reduce incidences of moral hazards.

The company totally depends on web services for their underwriting, there should besome backup if the system fails to continue the work.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 50/52

SWOT – Analysis

STRENGTHS WEAKNESSES

Stand alone health insurance company inthe field.Experience, expertise and support of Big financial group.Latest Technology and Infrastructure to

support & fasten the services.All the range of health products under oneroof.Cashless service without TPA interventioni.e. in-house claim settlement.24 hours General Practitioner's advice andmedical counseling24x7 in-house Call Center Toll free telephone assistanceComplete knowledge backed website tooffer medical information, including health

tips.Large range of premiums through different products for every class of people.Direct discount on premium for no claim benefitWelcome discount for the proposers shiftingfrom other company with all thecontinuation benefits.

health companiesoffering health insurance.

companies.

branch offices

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 51/52

Innovative products even for chronicnoncurablediseases like diabetes, AIDS etc.Availability of tailor made policies.

OPPORTUNITIES THREATS

services.

Non-availability of any major healthinsurance service provider.

Willingness of Corporates to have atie-up with the company.

covered under health insurance & evenis unaware of the benefits.

and hence availing Overseas policies.

accidents & increased cost of healthcarefacilities

Established general insurancecompanies having brand name.

regularly done in this form of insurance practices.

insurance thinking of wastage of money.

age group.who are in real need of health care expenses.

havemindset of availing policies from publicsector companies.

7/27/2019 Star Health Project

http://slidepdf.com/reader/full/star-health-project 52/52