STANDARDIZING A CHART OF ACCOUNTS AND AN ANNUAL REPORT · · 2004-07-19STANDARDIZING A CHART OF...

46

STANDARDIZING A CHART OF ACCOUNTS AND AN ANNUAL REPORT

Transcript of STANDARDIZING A CHART OF ACCOUNTS AND AN ANNUAL REPORT · · 2004-07-19STANDARDIZING A CHART OF...

STANDARDIZING A CHART OF ACCOUNTS AND AN ANNUAL REPORT

2

WHAT IS A UNIFORM SYSTEM OF ACCOUNTS?n It is an accounting system that standardizes the

accounting classifications to achieve uniform accounting records

n Allows one to maintain consistent application among companies

n Used to report financial information to the regulatory agency and generally consistent with Generally Accepted Accounting Principles

3

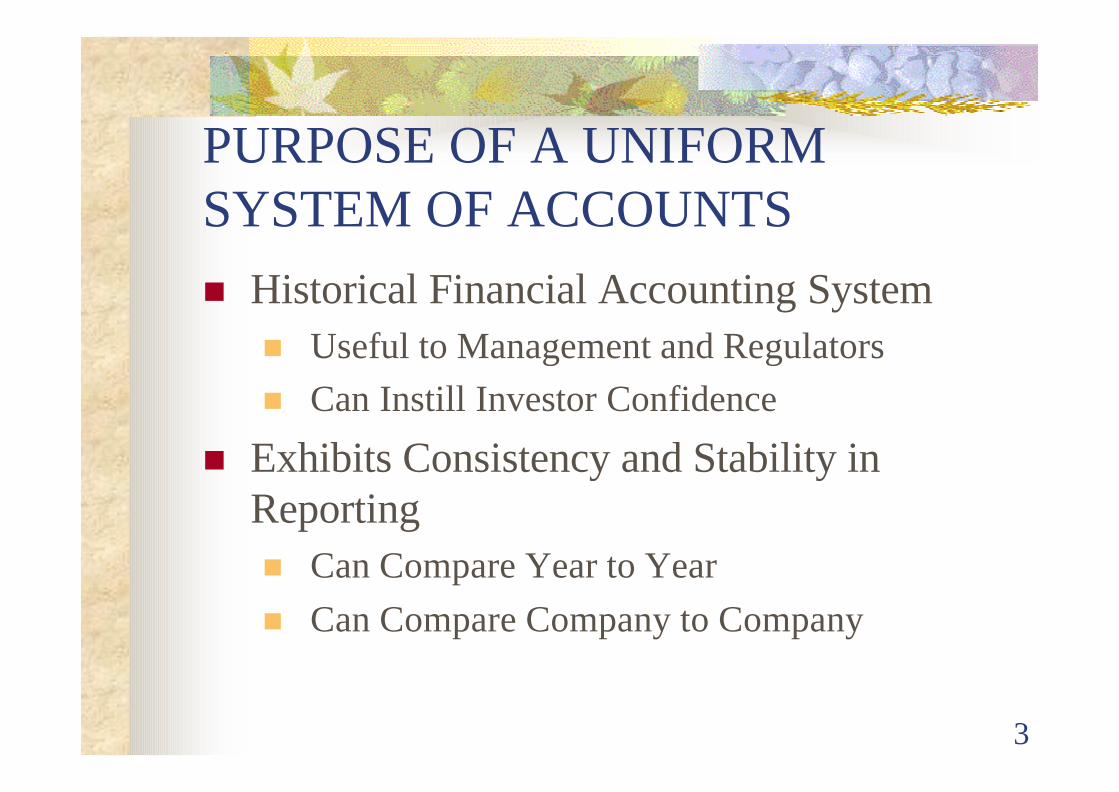

PURPOSE OF A UNIFORM SYSTEM OF ACCOUNTSn Historical Financial Accounting System

n Useful to Management and Regulatorsn Can Instill Investor Confidence

n Exhibits Consistency and Stability in Reportingn Can Compare Year to Yearn Can Compare Company to Company

4

PURPOSE OF UNIFORM SYSTEM OF ACCOUNTSn Meant to reflect stable, recurring financial data, to

extent regulatory considerations permitn Changes may be made for new accounting standardsn Changes may be made to reflect changes in

telecommunications environment

n For the most part, reflects the generally accepted accounting principles

n Reflects natural groupings of transactions

5

WHAT IS CONTAINED IN A UNIFORM SYSTEM OF ACCOUNTS?

n General Accounting Instructionsn Listing of Accounts

n Account Numbersn Account Titlesn Sample lists of types of transactions to be

recorded in the accountn Instructions on recording the transaction in

the account

6

GENERAL INSTRUCTION EXAMPLE(a) The company’s financial records shall be kept in accordance with

generally accepted accounting principles to the extent permitted by this system of accounts.

(b) The company’s financial records shall be kept with sufficient particularity to show fully the facts pertaining to all entries in these accounts. The detail records shall be filed in such manner as to be readily accessible for examination by representatives of this Commission.

(c) The Commission shall require a company to maintain financial andsubsidiary records in such manner that specific information, of a type not warranting disclosure as an account or subaccount, will be readily available. When this occurs, or where the full information is not otherwise recorded in the general books, the subsidiary records shall be maintained in sufficient detail to facilitate the reporting of the required specific information. The subsidiary records, in which the full details are shown, shall be sufficiently referenced to permit ready identification and examination by representatives of this Commission.

7

EXAMPLE OF AN ACCOUNT DESCRIPTION

32.2423 Buried Cable(a) This account shall include the original cost of buried cable as well as the

cost of other material used in the construction of such plant. This account shall also include the cost of trenching for and burying cable run in conduit not classifiable to Account 2441, Conduit Systems. Subsidiary record categories, as defined below, are to be maintained for nonmetallic buried cable and metallic buried cable.(1) Nonmetallic cable. This subsidiary record category shall include the original

cost of optical fiber cable and other associated material used in constructing a physical path for the transmission of telecommunications signals.

(2) Metallic cable. This subsidiary record category shall include the original cost of single or paired conductor cable, wire and other associated material used in constructing a physical path for the transmissin of telecommunications signals.

(b) The cost of pumping water out of manholes and of cleaning manholes and ducts in connection with construction work and the cost of permits and privileges for the construction of of cable and wire facilities shall be included in the account chargeable with such construction.

8

HOW IS UNIFORM SYSTEM OF ACCOUNTS USED?n To determine the reasonableness of chargesn Basis from which to then allocate costsn Collection and distribution of universal

service fundsn Monitor continued financial viabilityn Monitor new investments (impacting

quality of service)n Look at competitiveness of the market

9

U.S. ENERGY ACCOUNT NUMBERINGn 100 Assetsn 200 Liabilities and Capitaln 300 Detailed Plant Accountsn 400 Operating Revenues, Other

Income, and Income Deductionsn 500 Operation and Maintenance

Expense Accountsn 900 Administrative and General Expense

Accounts

10

U.S. TELECOMMUNICATIONS ACCOUNT NUMBERINGn 1000 Assetsn 2000 Detail Plant Accountsn 3000 Depreciation and Amortizationn 4000 Liabilities and Equityn 5000 Revenuesn 6000 Expense Accountsn 7000 Other Operating Income and Expenses

11

ACCOUNT NUMBERING DETAILn Balance Sheet Accounts (1120 – 1500)n Plant Accounts (2001 – 2690)n Accumulated Depreciation and Amortization (3100 –

3410)n Liabilities and Shareholders’ Equity (4000 – 4550)n Revenues (5000 – 5300)n Plant Specific Operations (6110 – 6410)n Plant Non-Specific Operations Expense (6510 – 6560)

12

ACCOUNT NUMBERING DETAILn Customer Operations Expense (6610 – 6620)n Corporate Operations Expense (6720 – 6790)n Other Operating Income and Expense (7100)n Operating Taxes (7200)n Non-operating Income and Expense (7300)n Non-operating Taxes (7400)n Interest and Related Items (7500 – 7600)n Jurisdictional Differences and Non-Regulated Income

Items (7910 – 7990)

13

MISCELLANEOUS BALANCE SHEET ACCOUNTSn Current Assets

n Cash and Equivalentsn Receivablesn Allowance for Doubtful Accountsn Materials and Suppliesn Prepaymentsn Other Current Assets

14

MISCELLANEOUS BALANCE SHEET ACCOUNTSn Non-Current Assets

n Non-regulated Investmentsn Other Non-current Assetsn Deferred Chargesn Other

15

PLANT ACCOUNTSn Telecommunications Plant in Service (Summary

Account)n Property Held for Future Telecommunications

Usen Telecommunications Plant Under Constructionn Telecommunications Plant Adjustmentn Non-Operating Plant (Example: Plant Held for

Sale)n Goodwill

16

PLANT IN SERVICE (DETAIL)n General Support Assets

n Landn Motor Vehiclesn Aircraftn Tools and Other Work Equipmentn Buildingsn Furnituren Office Equipmentn General Purpose Computers

17

PLANT IN SERVICE (DETAIL)n Central Office Assets

n Central Office Switchingn Non-digital Switchingn Digital Electronic Switchingn Operator Systemsn Central Office Transmissionn Radio Systemsn Circuit Equipment

18

PLANT IN SERVICE (DETAIL)n Information Origination / Termination

Assetsn Station Apparatusn Customer Premises Wiringn Large Private Branch Exchangesn Public Telephone Terminal Equipmentn Other Terminal Equipment

19

PLANT IN SERVICE (DETAIL)n Cable and Wire Facilities Asset

n Polesn Aerial Cablen Underground Cablen Buried Cablen Submarine and Deep Sea Cablen Intrabuilding Network Cablen Aerial Wiren Conduit Systems

20

PLANT IN SERVICE (DETAIL)n Amortizable Assets

n Capital Leasesn Leasehold Improvementsn Intangibles

21

PLANT ACCOUNT INSTRUCTIONS

n Do not include the cost of plant contributed to the company

n Plant is recorded at original costn Plant cost includes allowance for funds

used during construction which provides for the cost of financing the plant construction.

22

ACCUMULATED DEPRECIATION AND AMORTIZATIONn Accumulated Depreciationn Accumulated Depreciation – Held for

Future Telecommunications Usen Accumulated Depreciation – Non-

Operatingn Accumulated Depreciation – Tangiblen Accumulated Amortization – Capitalized

Leases

23

LIABILITIES AND STOCKHOLDERS’S EQUITYn Current Liabilities

n Current Accounts and Notes Payablen Customers’ Depositsn Income Taxes – Accruedn Other Taxes – Accruedn Net Current Deferred Operating Income Taxesn Net Current Deferred Non-operating Income Taxesn Other Current Liabilities

24

LIABILITIES AND STOCKHOLDERS’S EQUITY

n Long Term and Funded Debtn Other Liabilities and Deferred Credits

n Other Liabilities and Deferred Creditsn Unamortized Operating Investment Tax Creditsn Unamortized Non-Operating Investment Tax Credits n Net Non-Current Deferred Operating Taxesn Net Deferred Tax Liability Adjustmentsn Net Non-=Current Deferred Non-Operating Income

Taxesn Deferred Tax Regulatory Adjustmentsn Other Jurisdictional Liabilities and Deferred Credits

25

LIABILITIES AND STOCKHOLDERS’S EQUITYn Stockholders’ Equity

n Capital Stockn Additional Paid-in Capitaln Treasury Stockn Other Capitaln Retained Earnings

26

REVENUESn Local Network Service Revenues

n Basic Area Revenuen Private Line Revenuesn Other Basic Area Revenue

n Network Access Services Revenuesn End User Revenuen Switched Access Revenuen Special Access Revenue

27

REVENUESn Long Distance Network Services Revenuesn Miscellaneous Revenuesn Non-Regulated Revenuesn Uncollectible Revenues

28

PLANT SPECIFIC OPERATIONS EXPENSEn Network Support Expense

n Motor Vehicle Expensen Aircraft Expensen Tools and Other Work Equipment Expense

n General Support Expensen Land and Building Expensesn Furniture and Artwork Expensesn Office Equipment Expensesn General Purpose Computer Expense

29

PLANT SPECIFIC OPERATIONS EXPENSEn Central Office Switching Expense

n Non-digital Switching Expensen Digital Electronic Switching Expense

n Operators System Expensen Central Office Transmission Expense

n Radio Systems Expensen Circuit Equipment Expense

30

PLANT SPECIFIC OPERATIONS EXPENSEn Information Origination / Termination

Expensen Station Apparatus Expensen Large Private Branch Exchange Expensen Public Telephone Terminal Equipment

Expensen Other Terminal Equipment Expense

31

PLANT SPECIFICOPERATIONS EXPENSEn Cable and Wire Facilities Expense

n Poles Expensen Aerial Cable Expensen Underground Cable Expensen Buried Cable Expensen Submarine and Deep Sea Cable Expensen Intrabuilding Network Cable Expensen Aerial Wire Expensen Conduit Systems Expense

32

PLANT NON-SPECIFICOPERATIONS EXPENSEn Other property, plant and equipment

expensesn Property held for future telecommunications

use expensen Provisioning expense

33

PLANT NON-SPECIFIC OPERATIONS EXPENSEn Network Operations Expense

n Power Expensen Network Administration Expensen Testing Expensen Plant Operations Administration Expensen Engineering Expense

n Access Expensen Depreciation and Amortization Expense

34

CUSTOMER OPERATIONS EXPENSEn Marketing

n Product Management and Salesn Product Advertising

n Services

35

CORPORATE OPERATIONS EXPENSEn General and Administrativen Provision for Uncollectible Notes

Receivable

36

OTHER INCOME ACCOUNTSn Other Operating Income and Expensen Operating Taxesn Non-Operating Income and Expensen Non-Operating Taxesn Interest and Related Items

n Interest and Related Itemsn Extraordinary Items

n Jurisdictional Differences and Non-Regulated Income Items

37

AFFILIATE TRANSACTIONSn Unless Done Pursuant to Tariff or Other Exception:

n Assets sold by or transferred by a carrier to its affiliate shall be recorded at no less than the higher of fair market value and net book cost

n Exception:n Assets sold by or transferred to a carrier from its affiliate

shall be recorded at no more than the lower of fair market value and net book cost

n If sale of a particular asset or service to third parties encompass greater than 25% of the total sales quantity

38

OTHER ACCOUNTING CONSIDERATIONS n Record Retention Requirements

n How long should supporting documents be held and available to auditors / regulators?

n Level of Detail in Main Accounts and Subsidiary Records to be Requiredn What degree of supporting documentation should be

mandated (e.e., continuting property records)?n Cost/Benefit of Implementation

n What is the cost of implementation to operators versus need for information by regulators?

39

ANNUAL REPORTn An annual report filed with a regulatory agency

can be more tailored for regulatory needs rather than simply duplicating the public financial reports.

n Can contain more than just financial informationn Can format to make useful for on-going

comparisons n Paper or electronic filing (or both)?

40

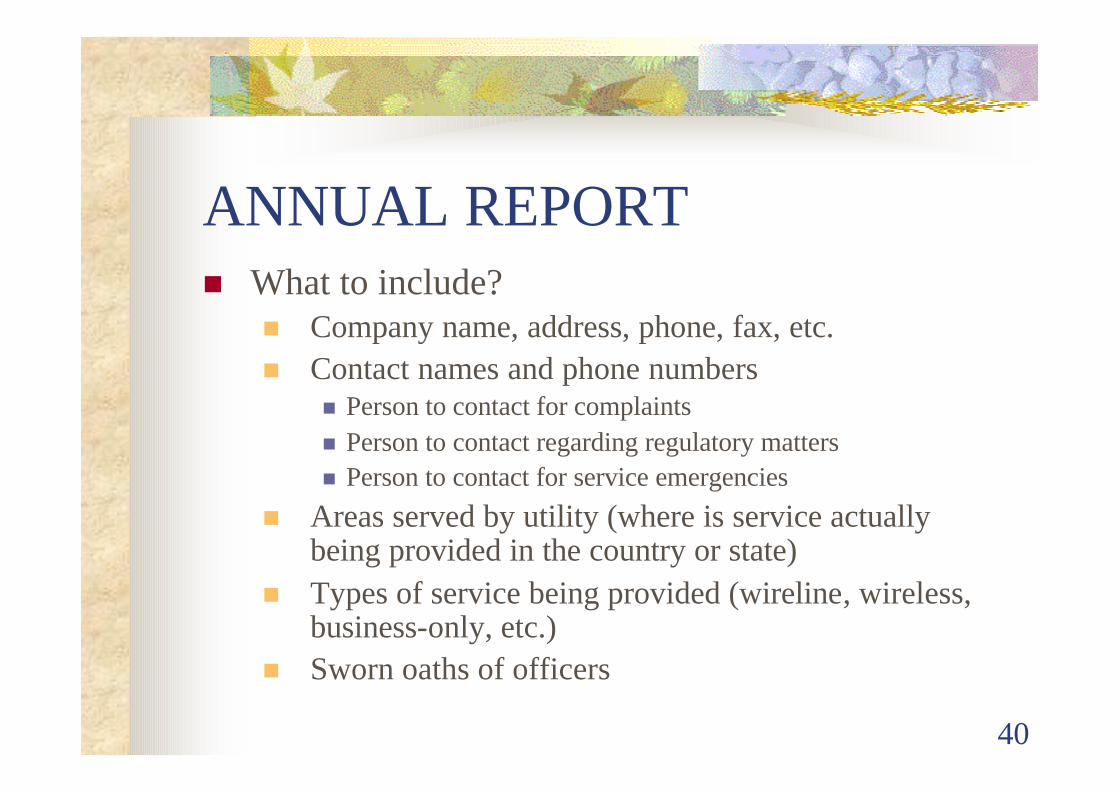

ANNUAL REPORTn What to include?

n Company name, address, phone, fax, etc.n Contact names and phone numbers

n Person to contact for complaintsn Person to contact regarding regulatory mattersn Person to contact for service emergencies

n Areas served by utility (where is service actually being provided in the country or state)

n Types of service being provided (wireline, wireless, business-only, etc.)

n Sworn oaths of officers

41

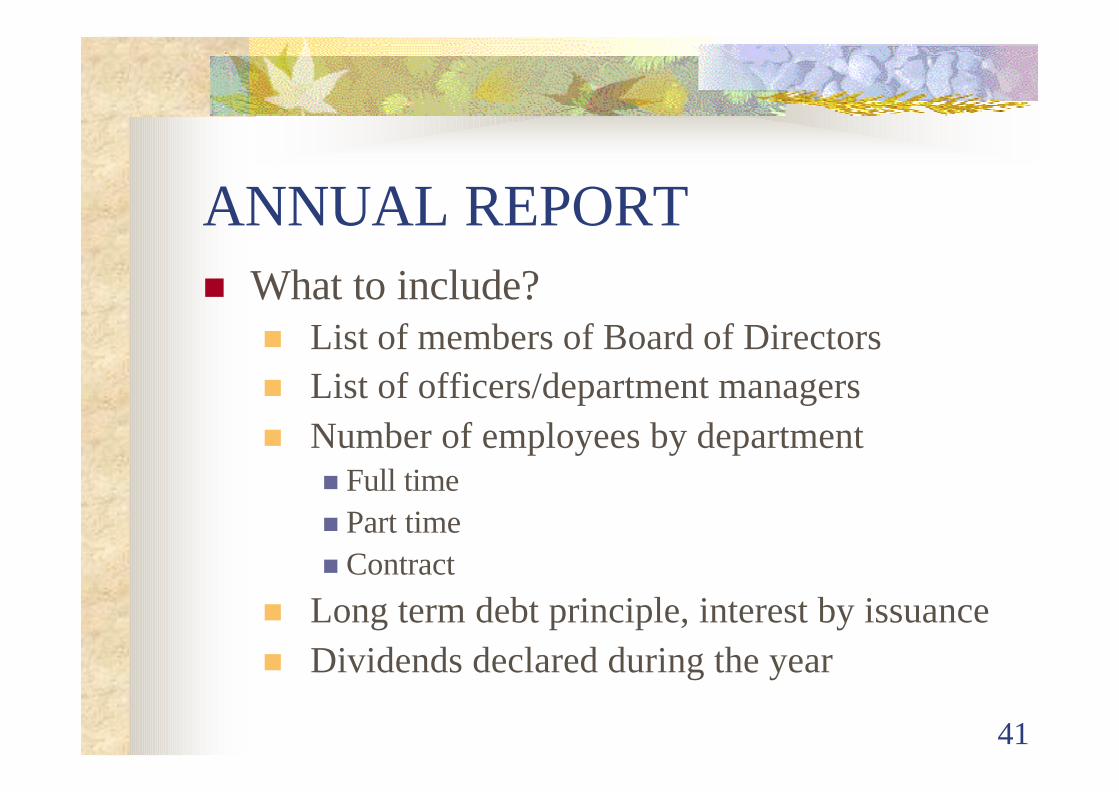

ANNUAL REPORTn What to include?

n List of members of Board of Directorsn List of officers/department managersn Number of employees by department

n Full timen Part time n Contract

n Long term debt principle, interest by issuancen Dividends declared during the year

42

ANNUAL REPORTn What to include

n Balance Sheetn Beginning and end of year, so can see changesn Total company versus for your jurisdiction onlyn Separate schedules detailing major items like plant (by

account), accumulated depreciation (by account) with specified additions and retirement totals throughout the year (by account)

n Revenuesn Total company versus for your jurisdiction onlyn By subcategory (international, local, interconnection, etc.)

43

ANNUAL REPORTn What to include?

n Operating Expensesn By account or major category breakdownn Total company versus your jurisdiction only

n Other Operating Income and Expensesn By your desired level of detail

n Taxesn By desired level of detail

44

ANNUAL REPORTn What to include?

n Non-financial datanNumber of central offices (switches)nMiles of linenNumber of minutes soldnNumber of customers by type

n Total at end of year versus monthly customer countsnDescription of Important Changes during the

reporting yearnMajor Facilities Construction Forecast

45

ANNUAL REPORTn What to include?

n Quality of Service data n Example: Average per customer outage time

n Established Performance IndicesnAverage Call Center Answer timen Response time for answering customer complaints

n Other