Staff Retirement Plan Annual Report 2013 - World...

54

Financial Management of the Plan Staff Retirement Plan Annual Report 2013

Transcript of Staff Retirement Plan Annual Report 2013 - World...

Fina

ncia

l Man

agem

ent

of th

e Pl

an

Staff Retirement Plan Annual Report 2013

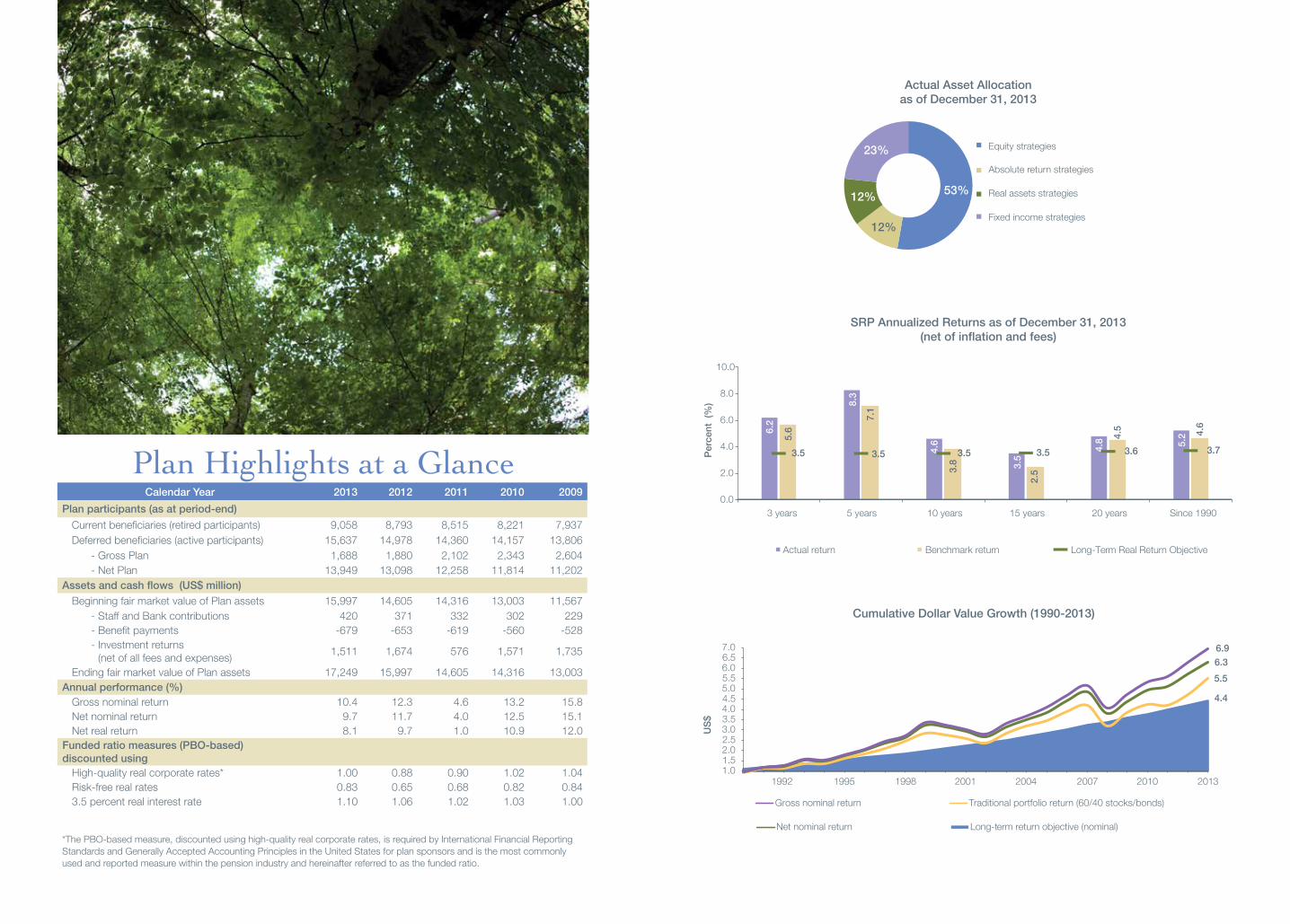

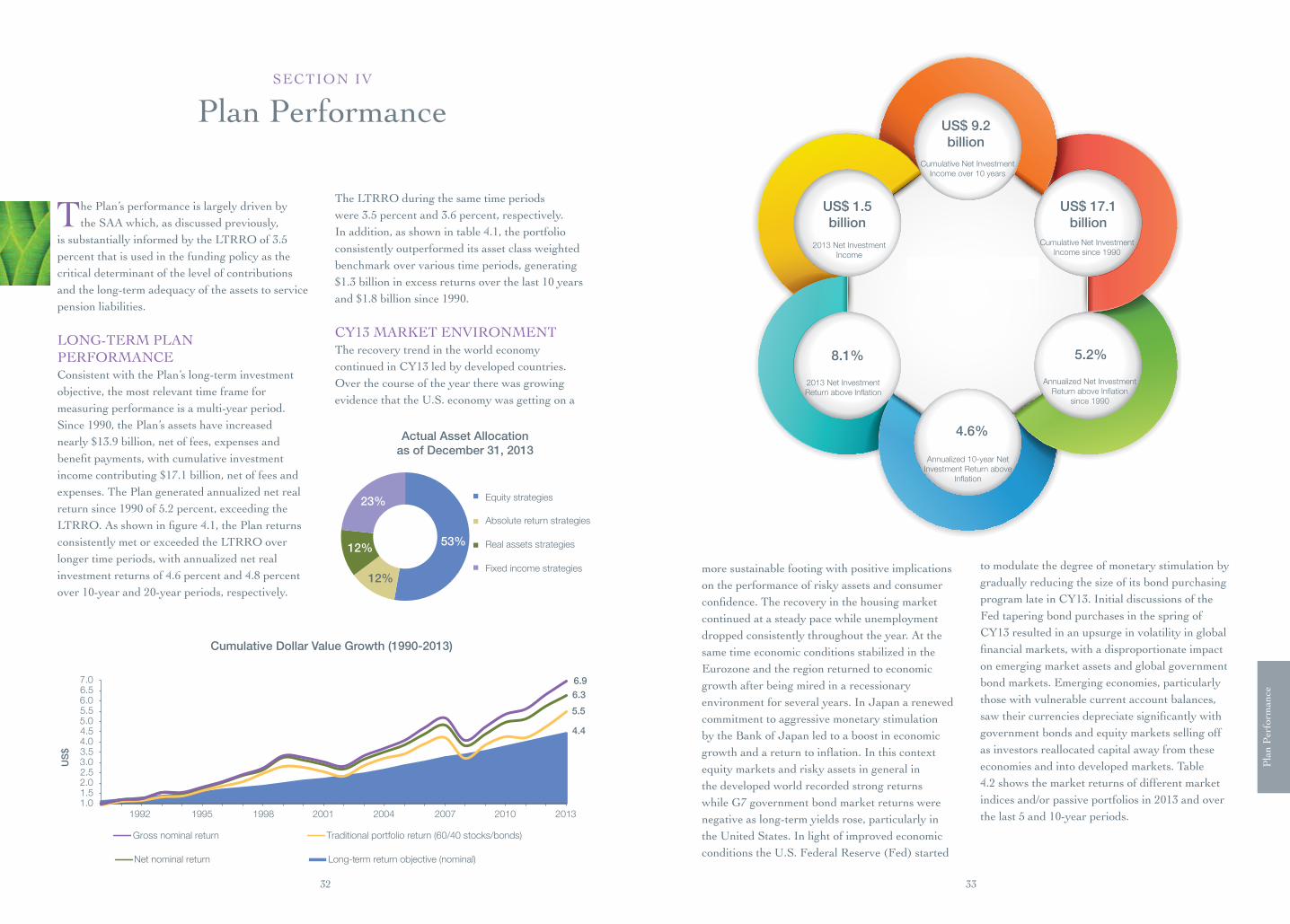

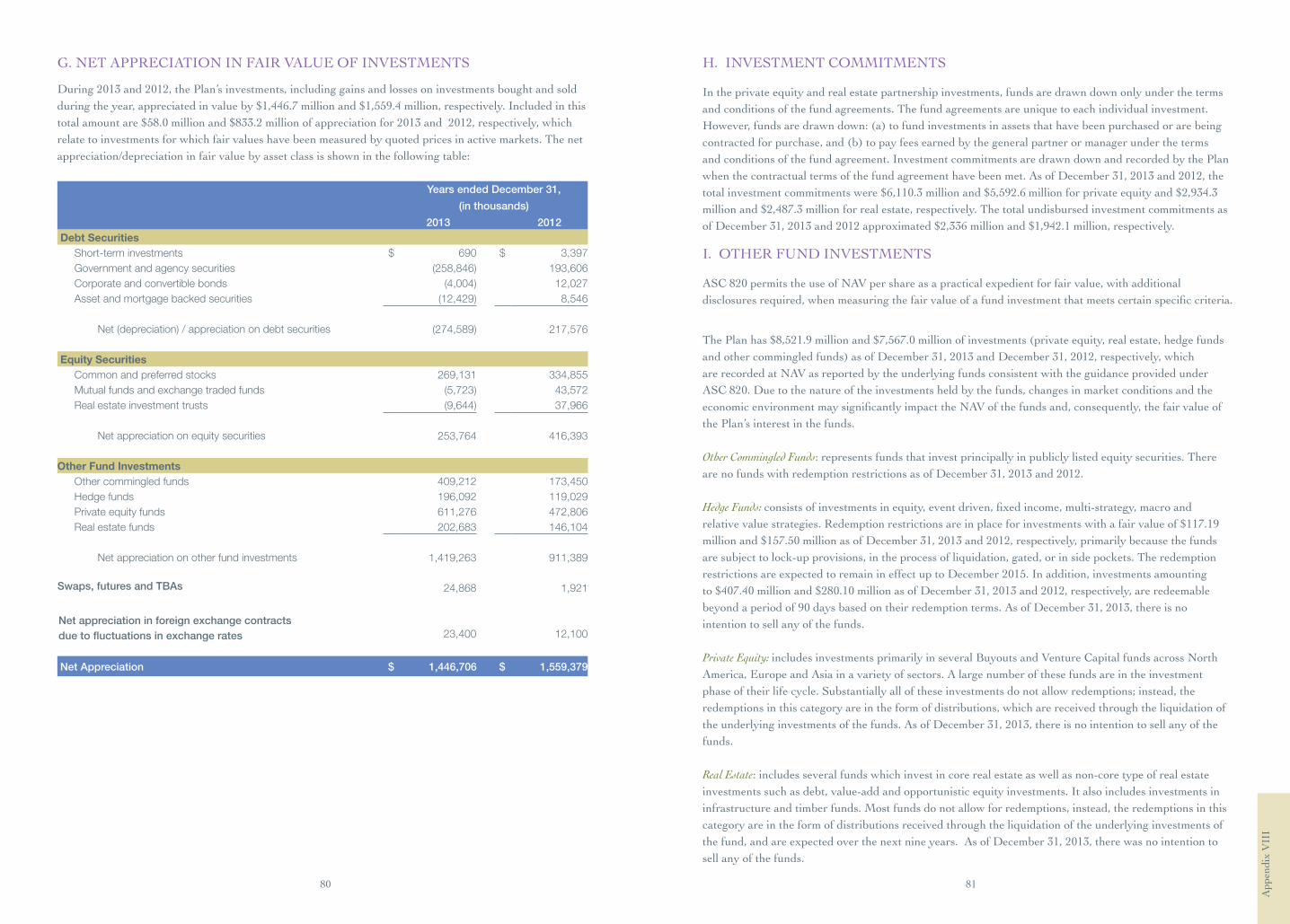

4.4

5.5 6.3 6.9

1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.0 6.5 7.0

1992 1995 1998 2001 2004 2007 2010 2013

Long-term return objective (nominal)

Traditional portfolio return (60/40 stocks/bonds)

Net nominal return

Gross nominal return

US$

Cumulative Dollar Value Growth (1990-2013)

Equity strategies

Fixed income strategies

Real assets strategies

Absolute return strategies

Actual Asset Allocation as of December 31, 2013

53%

23%

12%

12%

Plan Highlights at a GlanceCalendar Year 2013 2012 2011 2010 2009

Plan participants (as at period-end)

Current beneficiaries (retired participants) 9,058 8,793 8,515 8,221 7,937 Deferred beneficiaries (active participants) 15,637 14,978 14,360 14,157 13,806

- Gross Plan 1,688 1,880 2,102 2,343 2,604 - Net Plan 13,949 13,098 12,258 11,814 11,202 Assets and cash flows (US$ million)

Beginning fair market value of Plan assets 15,997 14,605 14,316 13,003 11,567 - Staff and Bank contributions 420 371 332 302 229 - Benefit payments -679 -653 -619 -560 -528

- Investment returns

(net of all fees and expenses)1,511 1,674 576 1,571 1,735

Ending fair market value of Plan assets 17,249 15,997 14,605 14,316 13,003 Annual performance (%)

Gross nominal return 10.4 12.3 4.6 13.2 15.8 Net nominal return 9.7 11.7 4.0 12.5 15.1 Net real return 8.1 9.7 1.0 10.9 12.0

Funded ratio measures (PBO-based) discounted using

High-quality real corporate rates* 1.00 0.88 0.90 1.02 1.04 Risk-free real rates 0.83 0.65 0.68 0.82 0.84 3.5 percent real interest rate 1.10 1.06 1.02 1.03 1.00

*The PBO-based measure, discounted using high-quality real corporate rates, is required by International Financial Reporting Standards and Generally Accepted Accounting Principles in the United States for plan sponsors and is the most commonly used and reported measure within the pension industry and hereinafter referred to as the funded ratio.

6.2

8.3

4.6

3.5

4.8 5.2 5.

6

7.1

3.8

2.5

4.5 4.6

3.5 3.5 3.5 3.5 3.6 3.7

0.0

2.0

4.0

6.0

8.0

10.0

3 years 5 years 10 years 15 years 20 years Since 1990

Perc

ent

(%)

Actual return Benchmark return Long-Term Real Return Objective

SRP Annualized Returns as of December 31, 2013(net of inflation and fees)

AcronymsALM asset liability managementABO accumulatedbenefitobligationASC AccountingStandardsCodificationASU Accounting Standards Updatesbps basis pointsBofA ML Bank of America Merrill Lynch BNY Mellon Bank of New York MellonCY calendar yearCPI consumer price indexEM emerging markets EURIBOR Euro Interbank Offered RateFoF fund of fundsFASB Financial Accounting Standards

BoardFY fiscalyearG7 Group of 7 industrialized countriesHAGS highest three years’ average

pensionable gross salary HANS highest three years’ average net salaryHFRI Hedge Fund Research Performance

IndexHR human resourcesIASB International Accounting Standards

BoardIBRD International Bank for

Reconstruction and DevelopmentIFC International Finance CorporationIFRS International Financial Reporting

StandardsIRS Internal Revenue ServiceISDA International Swaps and Derivatives

AssociationLEG Legal Vice PresidencyLIBOR London Interbank Offered RateL-T long-termLTRRO Long-Term Real Return ObjectiveM&A mergers and acquisitionsMIGA Multilateral Investment Guarantee

AgencyML Merrill LynchMRA mandatory retirement ageMSCI Morgan Stanley Capital International

NAV net asset valueNCREIF National Council of Real Estate

Investment Fiduciaries NRA net retirement agePBAC PensionBenefitsAdministration

CommitteePBO projectedbenefitobligationPEBP Post-EmploymentBenefitsPlanPEN Pension and Endowments

Department PENAD Pension Administration DivisionPFC Pension Finance CommitteePV present valuePVAB present value of accumulated plan

benefitsREITs Real Estate Investment TrustsSAA strategic asset allocationSRP Staff Retirement Plan and TrustSSRP Supplemental Staff Retirement PlanS&P Standard and Poor’sTBA to be announcedTIPS TreasuryInflationProtected

SecuritiesTRO Treasury Operations DepartmentTSA Tax Supplement AccountTUCS Trust Universe Comparison ServiceU.S. GAAP United States Generally Accepted

Accounting PrinciplesUST United States TreasuryVaR value at riskVSC voluntary savings componentWBG The World Bank Group

List of Boxes, Figures and Tables

BOXES Box1.1: WhoisResponsibleforBenefitPayments? 14Box 1.2: Facts about Plan Participants 16Box 3.1: A Snapshot of Plan Governance and Funding 23Box3.2: RelationshipbetweenInvestmentPerformance,FundedRatioandContributions 24Box 3.3: External Manager Selection Process 28Box4.1: NetPlanOptions 35BoxA2.1: DiscussiononLongevityAssumptions 44BoxA2.2: TheFeaturesofDifferentLiabilityMeasures 45BoxA2.3: UsageofDiscountRates 45BoxA2.4: AssessingtheFinancialPositionversusFundingaPlan 46

FIGURES FigureES.1:PlanParticipants(2004–2013) 6Figure ES.2: Increase in Plan Assets from Investment Returns and Net Contributions 7Figure ES.3: Plan Assets, Liabilities and Funded Ratios 8FigureES.4:StrategicAssetAllocationasofDecember31,2013 9Figure1.1: PlanParticipants(2004–2013) 15Figure2.1: PlanAssets,LiabilitiesandFundedRatios 19Figure2.2: RealAADiscountRates(singleequivalent) 19Figure2.3: AnnualContributions,NetInvestmentIncomeandBenefitPayments(2004–2013) 20Figure2.4: DollarImpactonPlanAssetsfromInvestmentReturnsandNetContributions 21Figure3.1: BankSRPContributionRatessinceFiscalYear1994 25Figure4.1: SRPAnnualizedReturnsasofDecember31,2013(netofinflationandfees) 34Figure4.2: FixedIncomeStrategiesbyGeography 36Figure4.3: NetInvestmentPerformance-FixedIncomeStrategies 36Figure4.4: PublicEquitiesPortfoliobyGeography 38Figure4.5: PrivateEquityPortfoliobyGeography 38Figure4.6: 1-year,5-year,10-yearNetInvestmentPerformance-EquityStrategies 39Figure4.7: PrivateRealEstatePortfoliobyGeography 39Figure4.8: NetInvestmentPerformance-RealAssetsStrategies 39Figure4.9: HedgeFundsPortfoliobyGeography 41Figure4.10:NetInvestmentPerformance-HedgeFundsPortfolio 41

TABLES Table ES.1: SRP Performance as of December 31, 2013 10Table 3.1: Asset Allocation as of December 31, 2012 27Table3.2: AssetAllocationeffectiveasofDecember31,2013 29Table4.1: SRPPerformanceasofDecember31,2013 34Table4.2: MarketEnvironmentasofDecember31,2013 35

TheSRPAnnualReportcontainsforward-lookingstatementsthatmaybeidentifiedbysuchtermsas“anticipates”,“believes”,“expects”,“intends”,orwordsofsimilarmeaning.Suchstatementsinvolveassumptionsandestimatesbasedoncurrentexpectations,which are subject to risks and uncertainties beyond control. Consequently, actual results could differ from those anticipated. This report may also contain information originating with third parties, information which is in public domain and other information providedtoorobtainedfromthirdparties(“ThirdPartyInformation”).StaffofIBRDdidnotindependentlyverifyaccuracyorcompleteness of Third Party Information and does not guarantee the same, to the extent Third Party Information has been used in, or relied upon, in preparation of this report.

Letter from the Pension Finance Administrator

Appendix I: CommitteeMembership 42Appendix II: APrimeronValuingPensionPlanLiabilities 43Appendix III: CharacteristicsofDifferentAssetClasses 47Appendix IV: Historical Performance of Cash Balance and Voluntary

Savings Component—Investment Options as of December31,201349Appendix V: GlossaryofTerms 50Appendix VI: ActuarialValuationResultsLetter 53Appendix VII: Independent Auditors’ Report 63Appendix VIII:FinancialStatements 65

Executive Summary

I. Overview of the Plan

II. Financial Health of the Plan

III. Financial Management of the Plan

IV. Plan Performance

Table of Contents

2

6

14

18

22

32

3

Let

ter

from

the

Pens

ion

Fina

nce

Adm

inis

trat

or

LETTER FROM THE

Pension Finance Administrator

2

On behalf of the Pension Finance Committee (PFC),Iampleasedtopresentthe64th

Annual Report of the World Bank Group Staff RetirementPlan(SRP,orthe“Plan”).

Calendar year 2013 was another strong year fortheSRP.Servingnearly24,700currentanddeferredbeneficiaries,theassetsofthePlanwere$17.3 billion at the end of the year, with investment returnscontributingmorethan$1.5billiontothe growth of the assets over the year. The SRP continues to be well funded and have a strong governance structure in which the assets of the Plan are held in trust, separate from the assets of the sponsor.

In 2013, the SRP assets again earned a return in excess of the Long-Term Real Return Objective (LTRRO)of3.5percentandthePBOfundedpositionoftheSRPincreased–endingtheyearat1.00–onthebackofstronginvestmentreturnsand a rise in U.S. interest rates. The year also saw somechangestotheWorldBank’spensionbenefitsthat apply only to current World Bank Group staff prospectively and not to retirees and others alreadyreceivingbenefits.Thesebenefitdesignchanges have been fully incorporated into the actuarial valuations of the Plan liabilities and are reflectedinthecontributionratesforfiscalyear(FY)2015.

RESULTSIn 2013 the world economy advanced further on its recovery path led primarily by developed economies although the journey continued to be a bumpy one. Towards the middle of 2013, with the outlook for economic growth improving in developed markets, the U.S. Federal Reserve signaled to the markets that it would begin to pare down its purchases of government and mortgage

backed securities. Concerns about stimulus withdrawal caused bond markets to sell-off, pushing up the yield on the U.S. Treasury 10-year note by more than 100 basis points and prompting investors to scale down emerging market positions. Consequently, the emerging market assets significantlyunderperformeddevelopedmarkets.

Inthisenvironment,financialmarketsdeliveredvaried results in 2013, in stark contrast to 2012. Highqualityfixedincomeassetsexperiencednegative returns and so did emerging market equities and most commodities. On the other hand, favored by the renewed growth momentum and improved expectations, developed market equities and private equity had a very strong performance with the MSCI World Index returning more than 27 percent and the private equity index returning about 20 percent. Developed markets real estate fundamentals also continued to improve over the course of 2013 resulting in a return of 11 percent for the NCREIF index. In2013,theSRP’sdiversifiedassetallocationreturned10.4percentgrossoffees(9.7percentnetoffees)andanetrealreturnoverinflationof 8.1 percent for the year. The SRP’s net real return was in excess of the LTRRO, currently at3.5percent.ActivemanagementofthePlancontributedtoanexcessreturnof48basispointsover the asset class weighted benchmark during the year, with most asset classes and strategies contributing to this excess return. In April of 2013,staffalsotookactionstosignificantlyreduce the interest rate risk of the SRP which contributed meaningfully to the total return of the Plan over the remainder of the year.

PensionbenefitsarefundedbyacombinationofPlan assets, investment income and contributions.

When real returns exceed the LTRRO, future contributionswillbelower(allelsebeingequal),andviceversa.Overthe5-year,10-yearandlonger time periods, the Plan’s net real returns of 8.3percent,4.6percentand5.2percent(since1990)respectivelyhavebeenwellinexcessoftheLTRRO. As a result, the investments have played a strongroleinthefundingofPlanbenefits,resultingin contribution rates being lower than they would have been had the assets returned the LTRRO.

The Plan’s PBO funded ratio increased to 1.00 at the end of December 2013 as a result of the combination of strong investment returns and theriseininterestrates.InMay2014,thePFCapprovedaBankcontributionrateof18.98percentofnetsalariesforFY15.Thisrateislowerthan what was expected last year primarily due to investment returns being higher than the LTRRO.

The external actuaries undertook a periodic experience study for the SRP designed to ensure that the demographic assumptions used in the actuarial valuation models provide the best estimate of future experience. They furtherreviewedtheLTRROandtheinflationassumption.TheLTRROwasreconfirmedandtheassumedinflationratewasrecalibratedto2.5percenttoreflectmoreaccuratelylongerterminflationexpectations.Inaddition,thePFC

approvedcertainmodificationstotheactuarialassumptionsandthesetooarereflectedinthecontributionrateforFY15.

STRATEGY AND OUTLOOKGoing into 2013, we expected continued strengthening of the growth trajectory, particularly in developed countries. We were concerned about the level of interest rates and, consequently, took actions during the year to reduce the interest rate sensitivity of the Plan and increase the overall exposure to growth assets while maintaining a cautious stance on emerging markets. We also continued to experience strong distributions from private equity and, to some extent, private real estate investments which we strove to reinvest in order to maintain the allocations close to the policy.Thistrendisexpectedtopersistin2014andrepresentsanareaofsignificantfocusfortheinvestment team.

Looking forward, current market expectations point towards further gradual improvement in economic conditions with developed countries stillexpectedtoleadtheway,althoughsignificantchallenges remain. Improved growth expectations in the United States reinforce the concerns for the outlook for interest rates with negative implicationsforfixedincomereturns.Atthesame time, equity and credit markets have had

54

Let

ter

from

the

Pens

ion

Fina

nce

Adm

inis

trat

or

an extraordinary run since 2008 fueled by the excessliquidityinthefinancialsystem,leavinglessroom for outsized returns going forward. Against thisbackgroundwemaintainourdiversifiedapproach seeking to strike the appropriate balance of generating strong investment returns without taking excessive risks. One of the ways we seek to achieve this is by identifying and exploiting selective investment opportunities where we can effectively use our long investment horizon and access to top external managers as a competitive advantage. For example, we have been analyzing the ongoing changes in different parts of the financialmarketssincethefinancialcrisisin2008that have altered the structure and participants primarily through the re-regulation of the banking system. We have been focusing on this as a theme and investing opportunistically to take advantage of this, whenever possible.

In December 2013, the PFC reviewed the asset allocation of the Plan and decided to make some changes to the investment framework that are designed to further streamline the asset allocation, increaseimplementationflexibilityandfocusthe asset allocation on achieving the LTRRO going forward. Supported by engagements with other major institutional investors, the PFC has been focused on the key investment objective as encapsulated by the LTRRO. Furthermore, the assetallocationofthePlanwasmodifiedslightlyto reduce the granularity of the allocation in some areas. In addition, the changes increase the flexibilityfortheimplementationofinvestmentopportunities that are outside of the streamlined policy allocation.

OUTREACH AND COMMUNICATIONRecently, we launched the Pension website. The website is an important part of the continuation of our work to enhance communication with Plan beneficiariesandstakeholders.Aspreviouslyannounced, the functionality of the website isbeingrolledoutinphases.Thefirstreleaseprovides key information about the pension plan, including plan governance and funding, pension benefits,investmentmanagementandperformance

reporting. With the recent launch by the Bank of thenewhumanresources(HR)system,ourfocusis now on the development of the second phase of the website that will provide retirees and current staff with a self-service interface to the new HR system in a secure environment. Information provided on the website is for information purposes only.

In addition to the website, we continue to engage extensively with active participants through seminars, video conferences, and one-on-one counseling services. The pension kiosk on the groundfloorofthemaincomplex,openedin2011,has assisted over 2,000 participants so far.

PENSION FINANCE COMMITTEEThis year, I would like to welcome Frank Heemskerk and Javed Hamid to the PFC. Mr. Heemskerk is a World Bank executive director. Mr. Hamid, is the retiree alternate to Jeff Katz who serves as a nominee of the 1818 Society. We are looking forward to working with Mr. Heemskerk and Mr. Hamid. Also, at this time, I would like to thank Piero Cipollone for his service and contributions to the Committee.

COMMITMENT TO RESULTSThe pension team is committed to working with thePFCandthePensionBenefitsAdministrationCommittee to ensure that the investment, financialandadministrationfunctionsareperformed with integrity and with the ultimate goal of serving well the World Bank Staff RetirementPlanandallofthePlanbeneficiaries.The team will continue to work to employ strategies and practices that we believe are in the best interest of the Plan and that best enable us to accomplish the mission entrusted to us.

John F. GandolfoPension Finance Administrator and Chief Investment Officer

7

Exe

cutiv

e Su

mm

ary

6

Executive Summary

12,1

03

12,3

03

12,6

71

12,9

07

13,5

06

13,8

06

14,1

57

14,3

60

14,9

78

15,6

37

6,67

8

6,95

1

7,17

3

7,44

0

7,70

6

7,93

7

8,22

1

8,51

5

8,79

3

9,05

8

55 56 57 58 57 57 58 59 59 58

0

15

30

45

60

75

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2004

2005

2006

20

07

2008

20

09

2010

2011

20

12

2013

Active participants (includes those not in contributory service) (left scale)

Retired participants and beneficiaries (left scale)

Retired as a percentage of active participants (right scale)

Parti

cipa

nts

Perc

ent (

%)

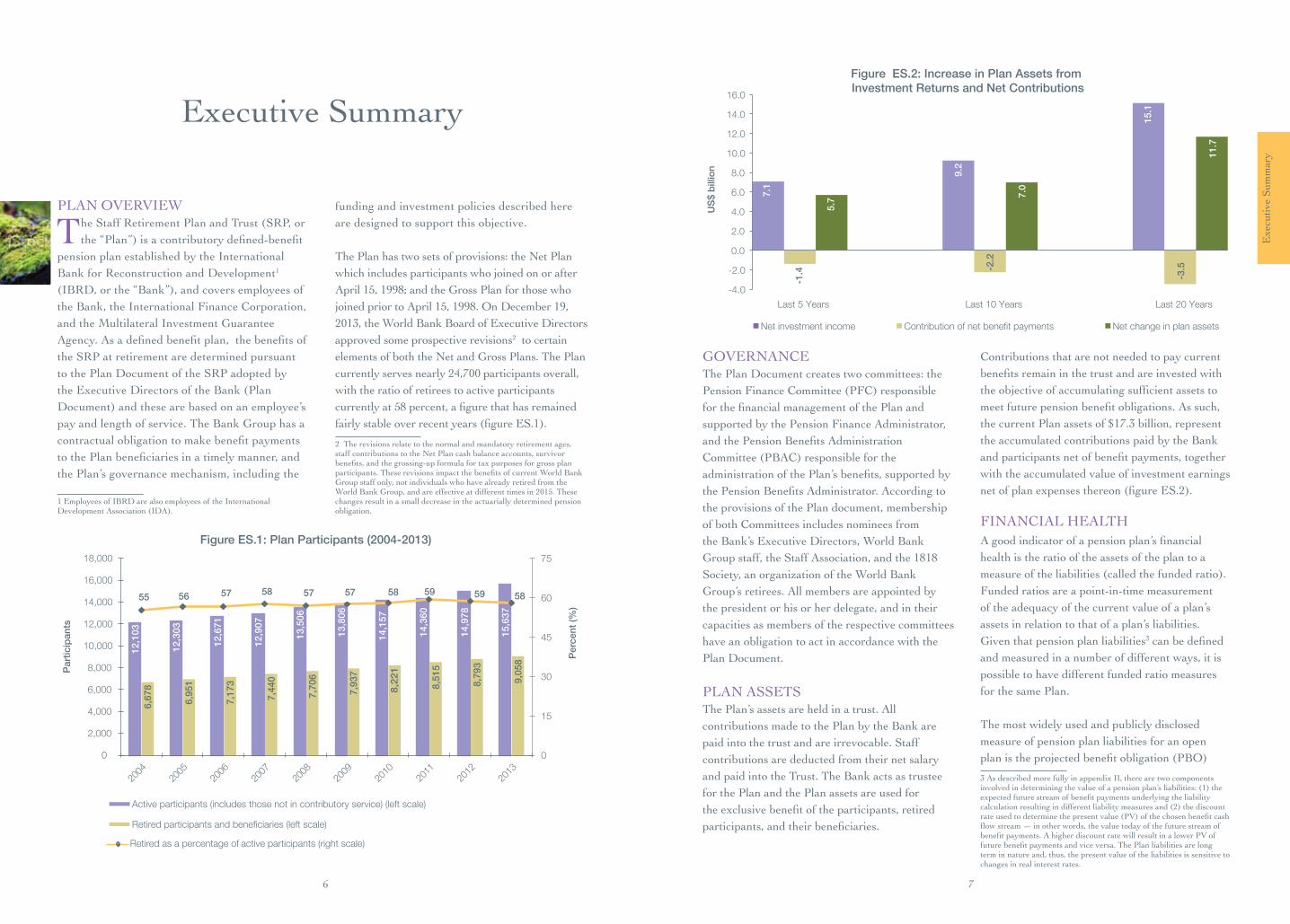

Figure ES.1: Plan Participants (2004-2013)

PLAN OVERVIEW

The Staff Retirement Plan and Trust (SRP, or the“Plan”)isacontributorydefined-benefit

pension plan established by the International Bank for Reconstruction and Development1 (IBRD,orthe“Bank”),andcoversemployeesofthe Bank, the International Finance Corporation, and the Multilateral Investment Guarantee Agency.Asadefinedbenefitplan,thebenefitsofthe SRP at retirement are determined pursuant to the Plan Document of the SRP adopted by the Executive Directors of the Bank (Plan Document)andthesearebasedonanemployee’spay and length of service. The Bank Group has a contractualobligationtomakebenefitpaymentstothePlanbeneficiariesinatimelymanner,andthe Plan’s governance mechanism, including the

1 Employees of IBRD are also employees of the International DevelopmentAssociation(IDA).

funding and investment policies described here are designed to support this objective.

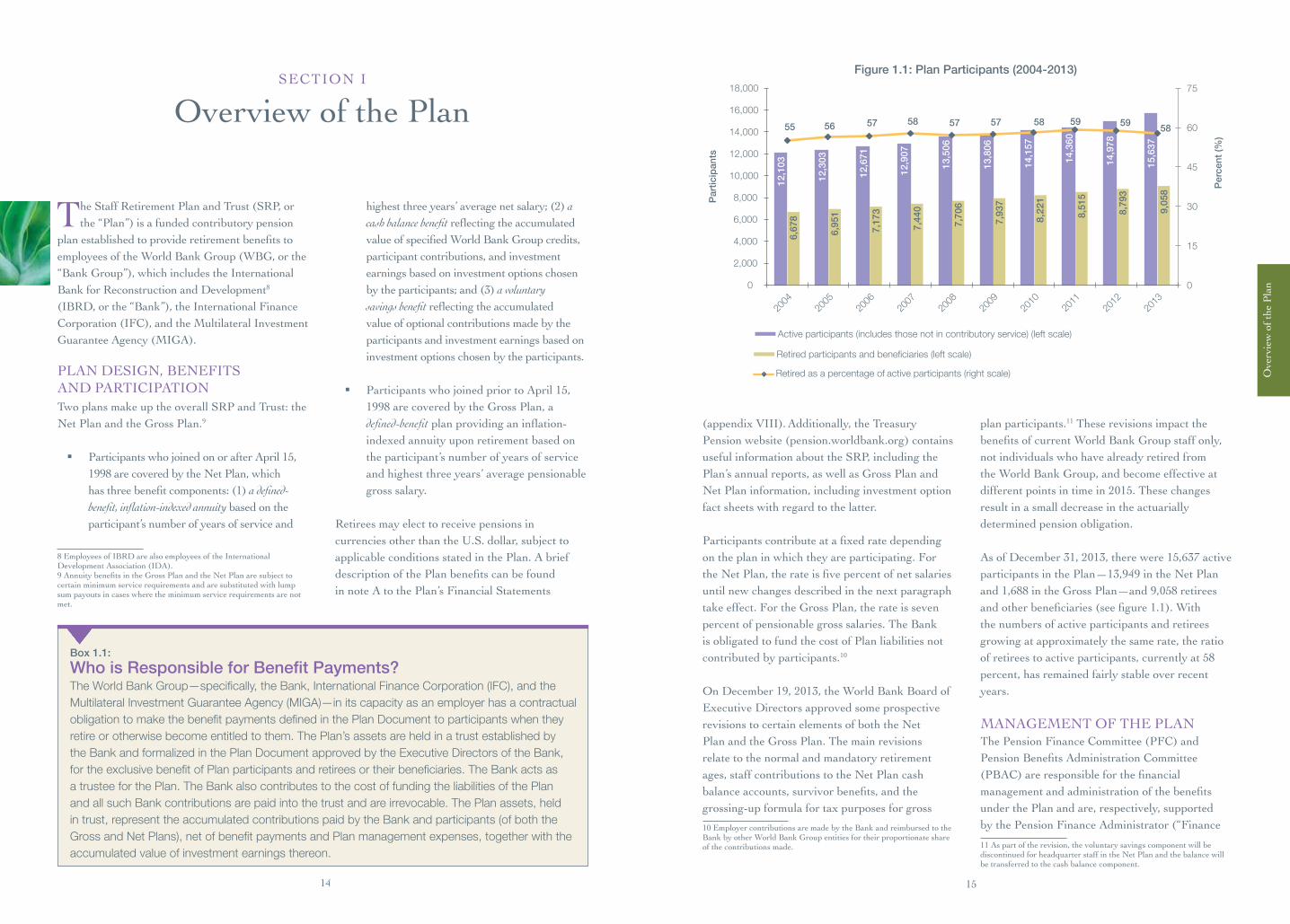

The Plan has two sets of provisions: the Net Plan which includes participants who joined on or after April15,1998;andtheGrossPlanforthosewhojoinedpriortoApril15,1998.OnDecember19,2013, the World Bank Board of Executive Directors approved some prospective revisions2 to certain elements of both the Net and Gross Plans. The Plan currentlyservesnearly24,700participantsoverall,with the ratio of retirees to active participants currentlyat58percent,afigurethathasremainedfairlystableoverrecentyears(figureES.1).

2 The revisions relate to the normal and mandatory retirement ages, staff contributions to the Net Plan cash balance accounts, survivor benefits,andthegrossing-upformulafortaxpurposesforgrossplanparticipants.TheserevisionsimpactthebenefitsofcurrentWorldBankGroup staff only, not individuals who have already retired from the WorldBankGroup,andareeffectiveatdifferenttimesin2015.Thesechanges result in a small decrease in the actuarially determined pension obligation.

GOVERNANCEThe Plan Document creates two committees: the PensionFinanceCommittee(PFC)responsibleforthefinancialmanagementofthePlanandsupported by the Pension Finance Administrator, andthePensionBenefitsAdministrationCommittee(PBAC)responsiblefortheadministrationofthePlan’sbenefits,supportedbythePensionBenefitsAdministrator.Accordingtothe provisions of the Plan document, membership of both Committees includes nominees from the Bank’s Executive Directors, World Bank Group staff, the Staff Association, and the 1818 Society, an organization of the World Bank Group’s retirees. All members are appointed by the president or his or her delegate, and in their capacities as members of the respective committees have an obligation to act in accordance with the Plan Document.

PLAN ASSETSThe Plan’s assets are held in a trust. All contributions made to the Plan by the Bank are paid into the trust and are irrevocable. Staff contributions are deducted from their net salary and paid into the Trust. The Bank acts as trustee for the Plan and the Plan assets are used for theexclusivebenefitoftheparticipants,retiredparticipants,andtheirbeneficiaries.

Contributions that are not needed to pay current benefitsremaininthetrustandareinvestedwiththeobjectiveofaccumulatingsufficientassetstomeetfuturepensionbenefitobligations.Assuch,the current Plan assets of $17.3 billion, represent the accumulated contributions paid by the Bank andparticipantsnetofbenefitpayments,togetherwith the accumulated value of investment earnings netofplanexpensesthereon(figureES.2).

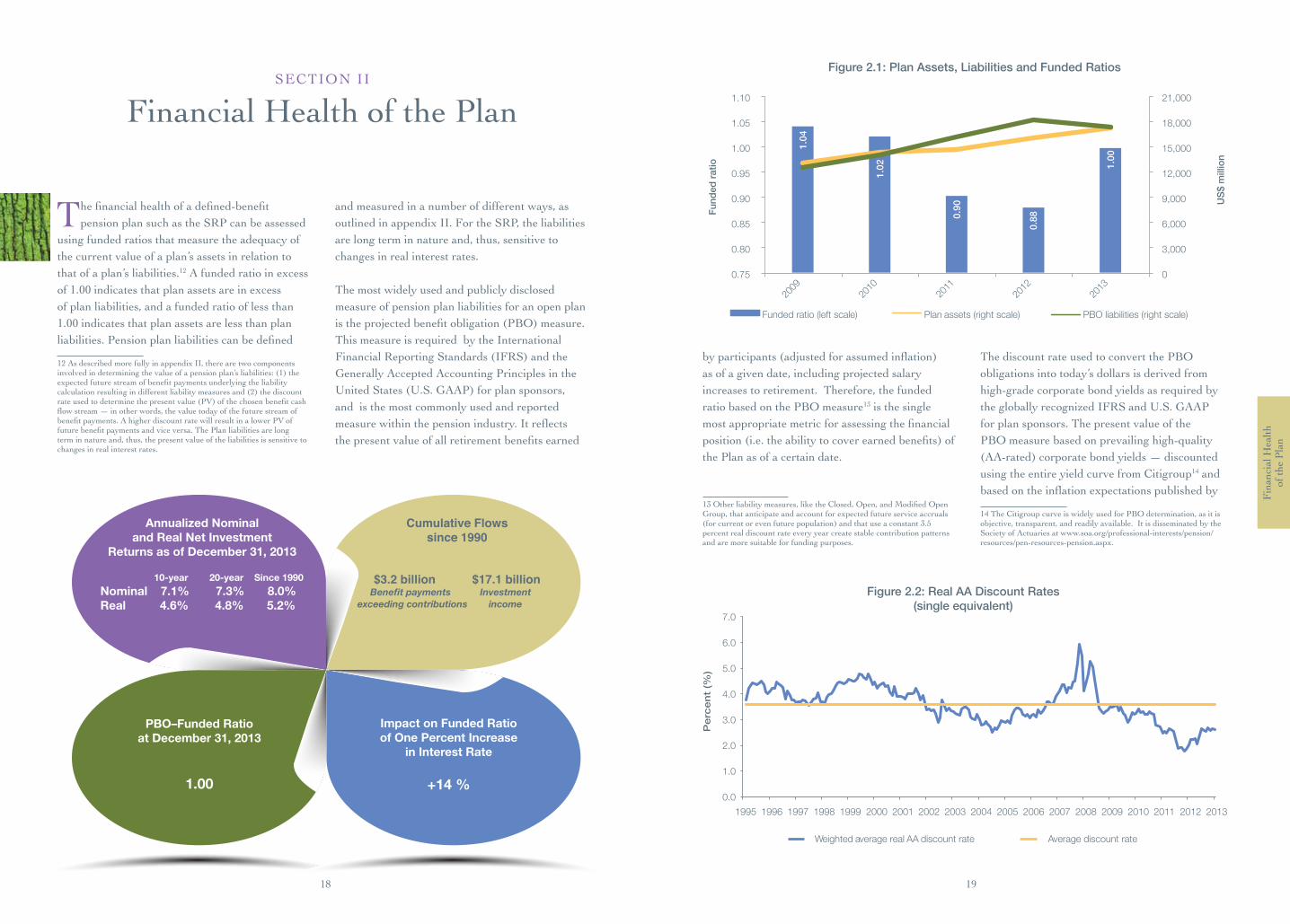

FINANCIAL HEALTHAgoodindicatorofapensionplan’sfinancialhealth is the ratio of the assets of the plan to a measureoftheliabilities(calledthefundedratio).Funded ratios are a point-in-time measurement of the adequacy of the current value of a plan’s assets in relation to that of a plan’s liabilities. Given that pension plan liabilities3canbedefinedand measured in a number of different ways, it is possible to have different funded ratio measures for the same Plan.

The most widely used and publicly disclosed measure of pension plan liabilities for an open planistheprojectedbenefitobligation(PBO)

3 As described more fully in appendix II, there are two components involvedindeterminingthevalueofapensionplan’sliabilities:(1)theexpectedfuturestreamofbenefitpaymentsunderlyingtheliabilitycalculationresultingindifferentliabilitymeasuresand(2)thediscountrateusedtodeterminethepresentvalue(PV)ofthechosenbenefitcashflowstream—inotherwords,thevaluetodayofthefuturestreamofbenefitpayments.AhigherdiscountratewillresultinalowerPVoffuturebenefitpaymentsandviceversa.ThePlanliabilitiesarelongterm in nature and, thus, the present value of the liabilities is sensitive to changes in real interest rates.

7.1

9.2

15.1

-1.4 -2

.2

-3.5

5.7 7.

0

11.7

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Last 5 Years Last 10 Years Last 20 Years

US$

bill

ion

Net investment income Contribution of net benefit payments Net change in plan assets

Figure ES.2: Increase in Plan Assets from Investment Returns and Net Contributions

9

Exe

cutiv

e Su

mm

ary

8

1.04

1.02

0.90

0.88

1.00

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

2009

2010

2011

2012

2013

US$

mill

ion

Fund

ed ra

tio

Funded ratio (left scale) Plan assets (right scale) PBO liabilities (right scale)

Figure ES.3: Plan Assets, Liabilities and Funded Ratios

measure.4Itreflectsthepresentvalueofallretirementbenefitsearnedbyparticipants(adjustedforassumedinflation)asofagivendate,including projected salary increases to retirement. Therefore, the PBO measure is the single most appropriatemetricforassessingthefinancialposition(i.e.theabilitytocoverearnedbenefits)of the Plan as of a certain date. The discount rate used to convert future obligations into today’s dollars is derived from high-grade (that is, AA-rated)corporatebondyieldsasrequiredbythe globally recognized International Financial Reporting Standards and Generally Accepted Accounting Principles in the United States for plan sponsors. The PBO-based funded ratio for SRP5 was 1.00 as of December 31, 2013 as shown infigureES.3,anincreaseof12basispointsowingto strong investment performance coupled with an increase in the real AA discount rate.

FINANCIAL MANAGEMENTIn managing the Plan, the PFC seeks to strike abalancebetweenfundingPlanbenefitsfromPlan assets and investment returns, and from

4ThismeasureisrequiredbytheInternationalFinancialReportingStandards and Generally Accepted Accounting Principles in the United States for plan sponsors, and is the most commonly used and reported measure within the pension industry.5Forreference,theaveragePBO-fundedratioforthe100largestU.S.-basedpensionplans,accordingtoMilliman,stoodat0.95asofDecember31,2013.Milliman,apensionconsultingandadvisoryfirm,conductsannualpensionfundingstudiesofthe100largestdefined-benefitpensionplanssponsoredbyU.S.publiccorporations.Thestudyisbasedonpensionplanfinancialinformationdisclosedinthefootnotesto the companies’ annual reports.

contributions. The key policies underpinning thefinancialmanagementofthePlan,includingthe determination of sponsor contributions and the investment of Plan assets are the funding and investment policies. The objective of these policies is toensurethatthePlanhassufficientassetstomeetbenefitpaymentsoverthelongterm.

The funding policy, as approved by the PFC, establishes the rules that determine sponsor contributions. The policy seeks to fund the Plan in a consistent and timely manner, while at the same time avoiding excessive volatility in Bank contributions. The funding policy, determines how much the Bank, as the Plan sponsor, must contribute annually to sustain and ensure the accumulationofsufficientPlanassetsovertimetomeettheexpectedbenefitpayments.TheBank’sannual contributions to the Plan are calculated using assumptions established under the funding policy. Asset performance is an important factor in determining the Bank’s contribution rate. The funding policy has been predicated on the achievementofa3.5percentrealreturnonPlaninvestmentssince1999,andthisrateconstitutesthelong-term(L-T)objectiveor“hurdlerate”forPlan assets, referred to as the Long-Term Real ReturnObjective(LTRRO).ThePFCbelievesthat the LTRRO is the most appropriate metric for assessing whether investment returns are meeting funding policy assumptions and the objectives of

thefinancialmanagementofthePlan.Essentially,ifPlanassetsreturn3.5percentrealandcontributionsare made at the actuarially required rates (that reflectthelong-termcostofthebenefitdesign),thebenefitswillbefullyfundedovertime.6

Infiscalyear(FY)2014,theBank’scontributionrate to the SRP was 20.88 percent of net salaries covering the period from July 2013 through June 2014.ForFY15,therateapprovedbythePFCis18.98percentofnetsalaries.In2014,basedonrecommendations from the Plan’s independent actuaries, Buck Consultants, the PFC approved reviseddemographicandfinancialassumptionsfor future valuations, effective for the most recent actuarialvaluations.Theaforementionedbenefitdesign changes as well as the actuarial assumptions have been incorporated into the actuarial valuationsandarereflectedinthecontributionsapprovedbythePFCforFY15.

The investment of Plan assets is directed by the Plan’sinvestmentpolicy.Assetdiversificationand liability-informed investment management are important considerations in the SRP’s overall investment strategy and risk management approach. A major component of the investment policyisthestrategicassetallocation(SAA)whichrepresents the asset mix that the PFC believes is best able to meet the LTRRO over a given investment horizon and within acceptable risk parameters. Volatility of returns and downside risk measures are considered key indicators of the Plan’s overall investment risk. At any point in

6TheBankcontributionsaredeterminedbasedonamodifiedopengroup approach of determining liabilities. This measure differs from thePBOliabilitymeasurealludedtoearlierinanumberofways:(i)it covers not only the existing Plan participants, but also new staff projectedtoenterthePlanoverthenext10years,(ii)itcoversnotonlybenefitsearnedandaccruedtilldate,butalsofutureaccrualsofall participants over the entire length of their future projected service, (iii)also,thePVoftheseliabilitiesaredeterminedusinga3.5percentreal discount rate, in contrast to the market-based discount rate used to calculate the PBO for accounting purposes.

time, the return assumptions underlying a given SAA are dependent on the particular market environment. These return assumptions, which have varied — and will vary — over time, guide the PFC in determining the appropriate level of risk-taking on plan assets in order to meet or exceed the LTRRO over the medium to long term.

The SAA is periodically reviewed and approved by the PFC as appropriate. Over the course of 2013, the PFC approved several changes to the asset allocationandinvestmentframeworkreflectingconcernsabouttheoutlookforfixedincomeinsome developed countries and the on-going goal of taking a more dynamic approach to the investment strategy. The asset allocation was streamlined andgreaterflexibilitywasintroducedtoenableaccessing investment opportunities that fall outside the policy portfolio. In addition, the exposure of the asset allocation to interest rates was further reduced through the sale of the U.S. Treasury InflationProtectedSecurities(TIPS)portfolioatasignificantpremiumoverthepurchaseprice.The SAA as of December 31, 2013 is presented in figureES.4.

=+ BenefitLiabilities

CurrentPlan

Assets

InvestmentReturns

Contributions+

Equity strategies

Absolute return strategies

Real assets strategies

Fixed income strategies

53%

26%

8%

13%

Figure ES.4: Strategic Asset Allocation as of December 31, 2013

11

Exe

cutiv

e Su

mm

ary

10

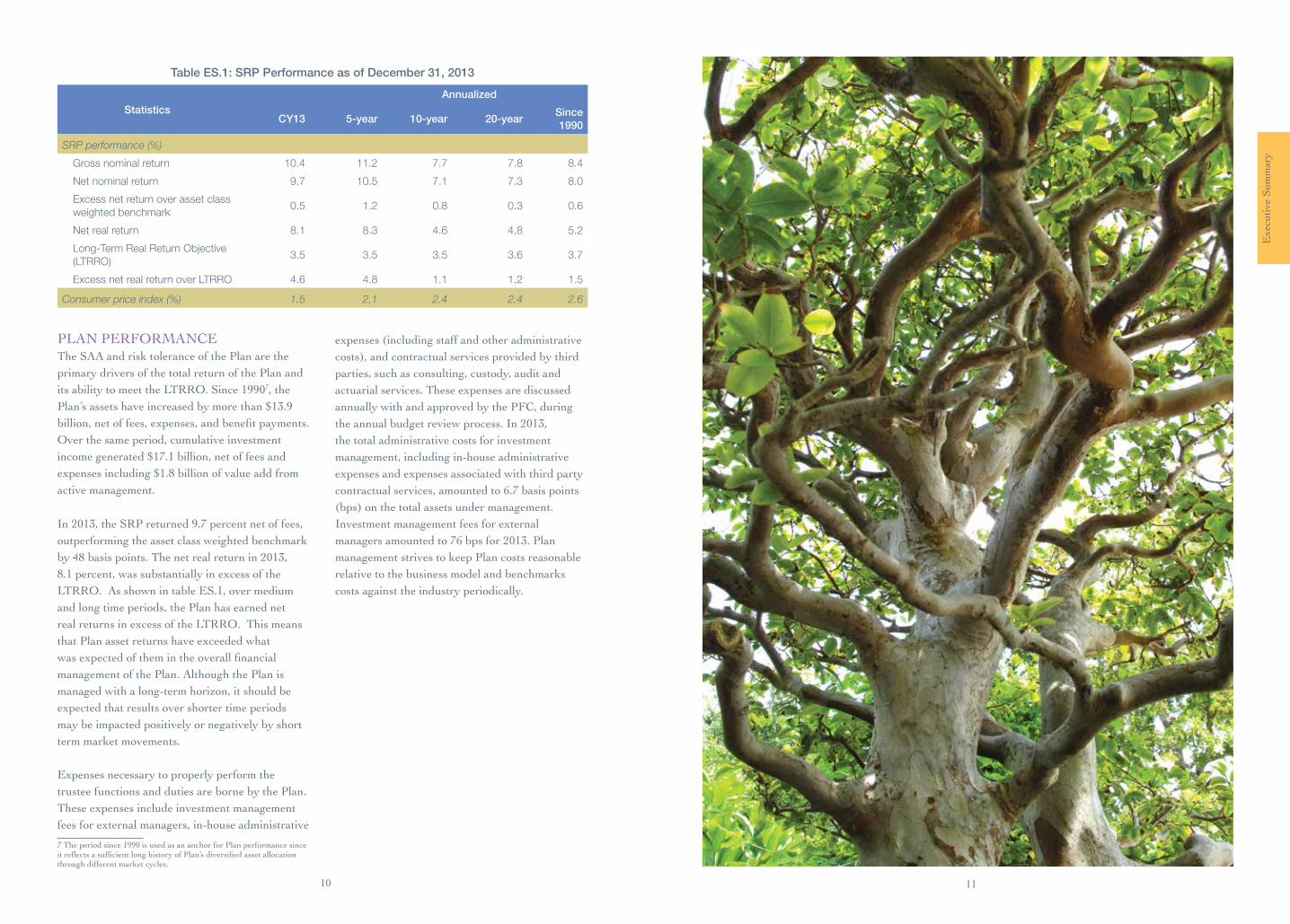

Table ES.1: SRP Performance as of December 31, 2013

Statistics Annualized

CY13 5-year 10-year 20-yearSince 1990

SRP performance (%)Gross nominal return 10.4 11.2 7.7 7.8 8.4

Net nominal return 9.7 10.5 7.1 7.3 8.0

Excess net return over asset class weighted benchmark

0.5 1.2 0.8 0.3 0.6

Net real return 8.1 8.3 4.6 4.8 5.2

Long-Term Real Return Objective (LTRRO)

3.5 3.5 3.5 3.6 3.7

Excess net real return over LTRRO 4.6 4.8 1.1 1.2 1.5

Consumer price index (%) 1.5 2.1 2.4 2.4 2.6

PLAN PERFORMANCEThe SAA and risk tolerance of the Plan are the primary drivers of the total return of the Plan and itsabilitytomeettheLTRRO.Since19907, the Plan’sassetshaveincreasedbymorethan$13.9billion,netoffees,expenses,andbenefitpayments.Over the same period, cumulative investment income generated $17.1 billion, net of fees and expenses including $1.8 billion of value add from active management.

In2013,theSRPreturned9.7percentnetoffees,outperforming the asset class weighted benchmark by48 basis points. The net real return in 2013, 8.1 percent, was substantially in excess of the LTRRO. As shown in table ES.1, over medium and long time periods, the Plan has earned net real returns in excess of the LTRRO. This means that Plan asset returns have exceeded what wasexpectedofthemintheoverallfinancialmanagement of the Plan. Although the Plan is managed with a long-term horizon, it should be expected that results over shorter time periods may be impacted positively or negatively by short term market movements.

Expenses necessary to properly perform the trustee functions and duties are borne by the Plan. These expenses include investment management fees for external managers, in-house administrative

7Theperiodsince1990isusedasananchorforPlanperformancesinceitreflectsasufficientlonghistoryofPlan’sdiversifiedassetallocationthrough different market cycles.

expenses (including staff and other administrative costs),andcontractualservicesprovidedbythirdparties, such as consulting, custody, audit and actuarial services. These expenses are discussed annually with and approved by the PFC, during the annual budget review process. In 2013, the total administrative costs for investment management, including in-house administrative expenses and expenses associated with third party contractual services, amounted to 6.7 basis points (bps)onthetotalassetsundermanagement.Investment management fees for external managers amounted to 76 bps for 2013. Plan management strives to keep Plan costs reasonable relative to the business model and benchmarks costs against the industry periodically.

1312

Section IOverview of the PlancontainsabriefoverviewofthePlandesign,benefitstructure,participants’profiles,andgovernance.

Section IIFinancial Health of the PlandiscussesthePlan’sfinancialhealth.

Section IIIFinancial Management of the PlanfocusesonthefinancialmanagementofthePlan,providinggreaterdetailson the key policies, including funding, asset liability management and risk tolerance, investment management, as well as risk management.

Section IVPlan Performancecovers the 2013 market environment along with the long-term and short-term performance of the various strategies and asset classes in detail.

The following sections of the report provide a more detailed review of the SRP for the yearendedDecember31,2013,includinginformationonPlanbeneficiaries,thekeypoliciesunderpinningthefinancialmanagement,financialresults,andthefinancialhealthof the Plan. The report is organized as follows:

Ove

rvie

w o

f the

Pla

n

1514

SECTION I

Overview of the Plan

12,1

03

12,3

03

12,6

71

12,9

07

13,5

06

13,8

06

14,1

57

14,3

60

14,9

78

15,6

37

6,67

8

6,95

1

7,17

3

7,44

0

7,70

6

7,93

7

8,22

1

8,51

5

8,79

3

9,05

8

55 56 57 58 57 57 58 59 59 58

0

15

30

45

60

75

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2004

2005

2006

20

07

2008

20

09

2010

2011

20

12

2013

Active participants (includes those not in contributory service) (left scale)

Retired participants and beneficiaries (left scale)

Retired as a percentage of active participants (right scale)

Parti

cipa

nts

Perc

ent (

%)

Figure 1.1: Plan Participants (2004-2013)

Box 1.1:

Who is Responsible for Benefit Payments?The World Bank Group—specifically, the Bank, International Finance Corporation (IFC), and the Multilateral Investment Guarantee Agency (MIGA)—in its capacity as an employer has a contractual obligation to make the benefit payments defined in the Plan Document to participants when they retire or otherwise become entitled to them. The Plan’s assets are held in a trust established by the Bank and formalized in the Plan Document approved by the Executive Directors of the Bank, for the exclusive benefit of Plan participants and retirees or their beneficiaries. The Bank acts as a trustee for the Plan. The Bank also contributes to the cost of funding the liabilities of the Plan and all such Bank contributions are paid into the trust and are irrevocable. The Plan assets, held in trust, represent the accumulated contributions paid by the Bank and participants (of both the Gross and Net Plans), net of benefit payments and Plan management expenses, together with the accumulated value of investment earnings thereon.

(appendixVIII). Additionally, the Treasury Pension website (pension.worldbank.org) contains useful information about the SRP, including the Plan’s annual reports, as well as Gross Plan and Net Plan information, including investment option fact sheets with regard to the latter.

Participantscontributeatafixedratedependingon the plan in which they are participating. For theNetPlan,therateisfivepercentofnetsalariesuntil new changes described in the next paragraph take effect. For the Gross Plan, the rate is seven percent of pensionable gross salaries. The Bank is obligated to fund the cost of Plan liabilities not contributed by participants.10

OnDecember19,2013,theWorldBankBoardofExecutive Directors approved some prospective revisions to certain elements of both the Net Plan and the Gross Plan. The main revisions relate to the normal and mandatory retirement ages, staff contributions to the Net Plan cash balanceaccounts,survivorbenefits,andthegrossing-up formula for tax purposes for gross 10 Employer contributions are made by the Bank and reimbursed to the Bank by other World Bank Group entities for their proportionate share of the contributions made.

plan participants.11 These revisions impact the benefitsofcurrentWorldBankGroupstaffonly,not individuals who have already retired from the World Bank Group, and become effective at differentpointsintimein2015.Thesechangesresult in a small decrease in the actuarially determined pension obligation.

AsofDecember31,2013,therewere15,637activeparticipantsinthePlan—13,949intheNetPlanand1,688intheGrossPlan—and9,058retireesandotherbeneficiaries(seefigure1.1).Withthe numbers of active participants and retirees growing at approximately the same rate, the ratio ofretireestoactiveparticipants,currentlyat58percent, has remained fairly stable over recent years.

MANAGEMENT OF THE PLANThePensionFinanceCommittee(PFC)andPensionBenefitsAdministrationCommittee(PBAC)areresponsibleforthefinancialmanagementandadministrationofthebenefitsunder the Plan and are, respectively, supported bythePensionFinanceAdministrator(“Finance

11 As part of the revision, the voluntary savings component will be discontinued for headquarter staff in the Net Plan and the balance will be transferred to the cash balance component.

The Staff Retirement Plan and Trust (SRP, or the“Plan”)isafundedcontributorypension

planestablishedtoprovideretirementbenefitstoemployees of the World Bank Group (WBG, or the “BankGroup”),whichincludestheInternationalBank for Reconstruction and Development8 (IBRD,orthe“Bank”),theInternationalFinanceCorporation(IFC),andtheMultilateralInvestmentGuaranteeAgency(MIGA).

PLAN DESIGN, BENEFITS AND PARTICIPATIONTwo plans make up the overall SRP and Trust: the Net Plan and the Gross Plan.9

§ ParticipantswhojoinedonorafterApril15,1998arecoveredbytheNetPlan,whichhasthreebenefitcomponents:(1)a defined-benefit, inflation-indexed annuity based on the participant’s number of years of service and

8 Employees of IBRD are also employees of the International DevelopmentAssociation(IDA).9AnnuitybenefitsintheGrossPlanandtheNetPlanaresubjecttocertain minimum service requirements and are substituted with lump sum payouts in cases where the minimum service requirements are not met.

highestthreeyears’averagenetsalary;(2)a cash balance benefitreflectingtheaccumulatedvalueofspecifiedWorldBankGroupcredits,participant contributions, and investment earnings based on investment options chosen bytheparticipants;and(3)a voluntary savings benefitreflectingtheaccumulatedvalue of optional contributions made by the participants and investment earnings based on investment options chosen by the participants.

§ ParticipantswhojoinedpriortoApril15,1998arecoveredbytheGrossPlan,adefined-benefitplanprovidinganinflation-indexed annuity upon retirement based on the participant’s number of years of service and highest three years’ average pensionable gross salary.

Retirees may elect to receive pensions in currencies other than the U.S. dollar, subject to applicable conditions stated in the Plan. A brief descriptionofthePlanbenefitscanbefoundin note A to the Plan’s Financial Statements

17

Ove

rvie

w o

f the

Pla

n

16

Box 1.2:

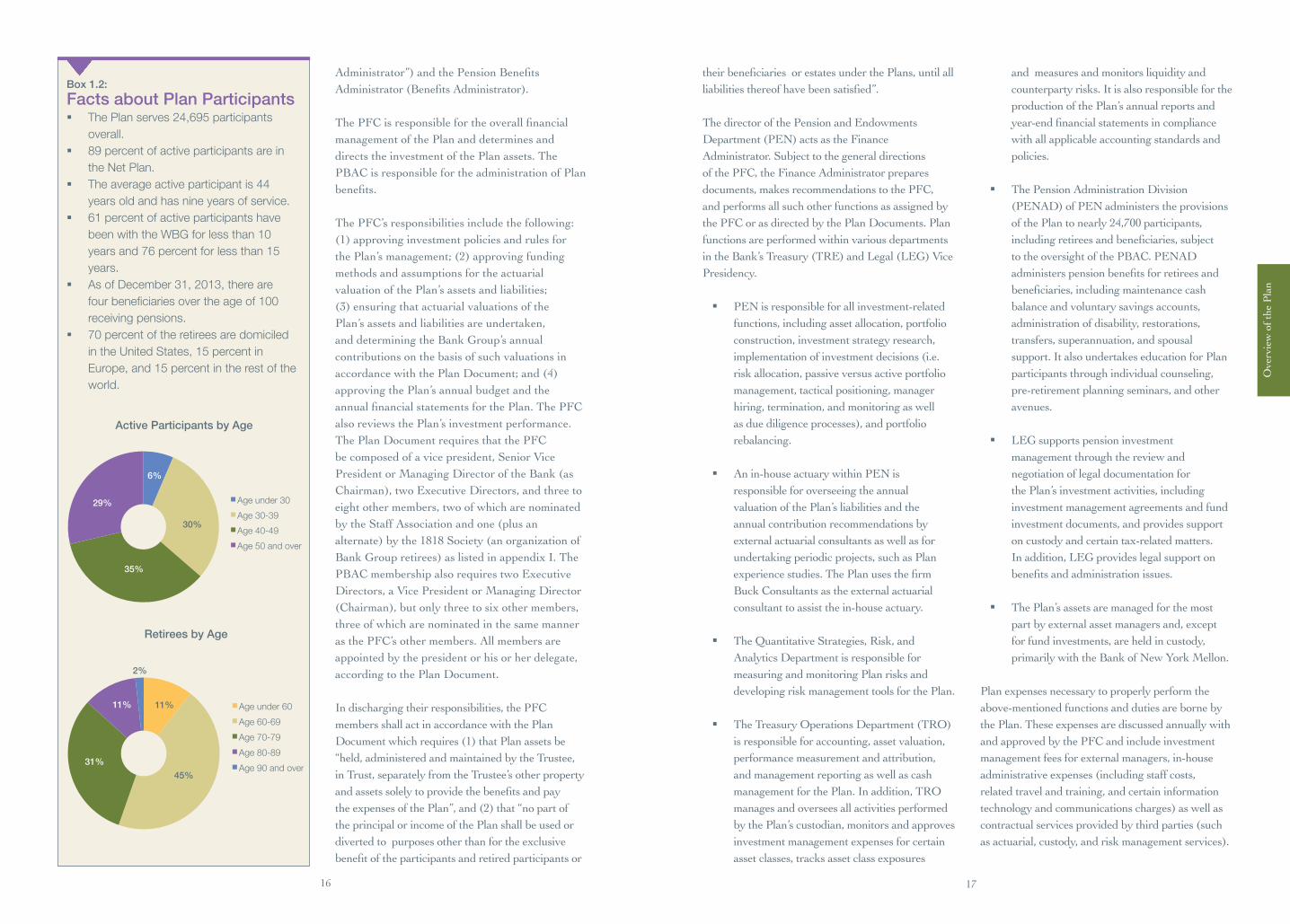

Facts about Plan Participants § The Plan serves 24,695 participants

overall. § 89 percent of active participants are in

the Net Plan. § The average active participant is 44

years old and has nine years of service. § 61 percent of active participants have

been with the WBG for less than 10 years and 76 percent for less than 15 years.

§ As of December 31, 2013, there are four beneficiaries over the age of 100 receiving pensions.

§ 70 percent of the retirees are domiciled in the United States, 15 percent in Europe, and 15 percent in the rest of the world.

6%

30%

35%

29% Age under 30 Age 30-39 Age 40-49 Age 50 and over

Active Participants by Age

11%

45% 31%

11%

2%

Age under 60 Age 60-69 Age 70-79 Age 80-89 Age 90 and over

Retirees by Age

Administrator”)andthePensionBenefitsAdministrator(BenefitsAdministrator).

ThePFCisresponsiblefortheoverallfinancialmanagement of the Plan and determines and directs the investment of the Plan assets. The PBAC is responsible for the administration of Plan benefits.

The PFC’s responsibilities include the following: (1)approvinginvestmentpoliciesandrulesforthePlan’smanagement;(2)approvingfundingmethods and assumptions for the actuarial valuationofthePlan’sassetsandliabilities;(3)ensuringthatactuarialvaluationsofthePlan’s assets and liabilities are undertaken, and determining the Bank Group’s annual contributions on the basis of such valuations in accordancewiththePlanDocument;and(4)approving the Plan’s annual budget and the annualfinancialstatementsforthePlan.ThePFCalso reviews the Plan’s investment performance. The Plan Document requires that the PFC be composed of a vice president, Senior Vice President or Managing Director of the Bank (as Chairman),twoExecutiveDirectors,andthreetoeight other members, two of which are nominated by the Staff Association and one (plus an alternate)bythe1818Society(anorganizationofBankGroupretirees)aslistedinappendixI.ThePBAC membership also requires two Executive Directors, a Vice President or Managing Director (Chairman),butonlythreetosixothermembers,three of which are nominated in the same manner as the PFC’s other members. All members are appointed by the president or his or her delegate, according to the Plan Document.

In discharging their responsibilities, the PFC members shall act in accordance with the Plan Documentwhichrequires(1)thatPlanassetsbe“held,administeredandmaintainedbytheTrustee,in Trust, separately from the Trustee’s other property andassetssolelytoprovidethebenefitsandpaytheexpensesofthePlan”,and(2)that“nopartofthe principal or income of the Plan shall be used or diverted to purposes other than for the exclusive benefitoftheparticipantsandretiredparticipantsor

theirbeneficiariesorestatesunderthePlans,untilallliabilitiesthereofhavebeensatisfied”.

The director of the Pension and Endowments Department(PEN)actsastheFinanceAdministrator. Subject to the general directions of the PFC, the Finance Administrator prepares documents, makes recommendations to the PFC, and performs all such other functions as assigned by the PFC or as directed by the Plan Documents. Plan functions are performed within various departments intheBank’sTreasury(TRE)andLegal(LEG)VicePresidency.

§ PEN is responsible for all investment-related functions, including asset allocation, portfolio construction, investment strategy research, implementation of investment decisions (i.e. risk allocation, passive versus active portfolio management, tactical positioning, manager hiring, termination, and monitoring as well asduediligenceprocesses),andportfoliorebalancing.

§ An in-house actuary within PEN is responsible for overseeing the annual valuation of the Plan’s liabilities and the annual contribution recommendations by external actuarial consultants as well as for undertaking periodic projects, such as Plan experiencestudies.ThePlanusesthefirmBuck Consultants as the external actuarial consultant to assist the in-house actuary.

§ The Quantitative Strategies, Risk, and Analytics Department is responsible for measuring and monitoring Plan risks and developing risk management tools for the Plan.

§ TheTreasuryOperationsDepartment(TRO)is responsible for accounting, asset valuation, performance measurement and attribution, and management reporting as well as cash management for the Plan. In addition, TRO manages and oversees all activities performed by the Plan’s custodian, monitors and approves investment management expenses for certain asset classes, tracks asset class exposures

and measures and monitors liquidity and counterparty risks. It is also responsible for the production of the Plan’s annual reports and year-endfinancialstatementsincompliancewith all applicable accounting standards and policies.

§ The Pension Administration Division (PENAD)ofPENadministerstheprovisionsofthePlantonearly24,700participants,includingretireesandbeneficiaries,subjectto the oversight of the PBAC. PENAD administerspensionbenefitsforretireesandbeneficiaries,includingmaintenancecashbalance and voluntary savings accounts, administration of disability, restorations, transfers, superannuation, and spousal support. It also undertakes education for Plan participants through individual counseling, pre-retirement planning seminars, and other avenues.

§ LEG supports pension investment management through the review and negotiation of legal documentation for the Plan’s investment activities, including investment management agreements and fund investment documents, and provides support on custody and certain tax-related matters. In addition, LEG provides legal support on benefitsandadministrationissues.

§ The Plan’s assets are managed for the most part by external asset managers and, except for fund investments, are held in custody, primarily with the Bank of New York Mellon.

Plan expenses necessary to properly perform the above-mentioned functions and duties are borne by the Plan. These expenses are discussed annually with and approved by the PFC and include investment management fees for external managers, in-house administrative expenses (including staff costs, related travel and training, and certain information technologyandcommunicationscharges)aswellascontractual services provided by third parties (such asactuarial,custody,andriskmanagementservices).

19

Fina

ncia

l Hea

lth

of th

e Pl

an

18

SECTION II

Financial Health of the Plan

1.04

1.02

0.90

0.88

1.00

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

2009

2010

2011

2012

2013

US$

mill

ion

Fund

ed ra

tio

Funded ratio (left scale) Plan assets (right scale) PBO liabilities (right scale)

Figure 2.1: Plan Assets, Liabilities and Funded Ratios

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Per

cent

(%)

Weighted average real AA discount rate Average discount rate

Figure 2.2: Real AA Discount Rates(single equivalent)

Thefinancialhealthofadefined-benefitpension plan such as the SRP can be assessed

using funded ratios that measure the adequacy of the current value of a plan’s assets in relation to that of a plan’s liabilities.12 A funded ratio in excess of 1.00 indicates that plan assets are in excess of plan liabilities, and a funded ratio of less than 1.00 indicates that plan assets are less than plan liabilities.Pensionplanliabilitiescanbedefined

12 As described more fully in appendix II, there are two components involvedindeterminingthevalueofapensionplan’sliabilities:(1)theexpectedfuturestreamofbenefitpaymentsunderlyingtheliabilitycalculationresultingindifferentliabilitymeasuresand(2)thediscountrateusedtodeterminethepresentvalue(PV)ofthechosenbenefitcashflowstream—inotherwords,thevaluetodayofthefuturestreamofbenefitpayments.AhigherdiscountratewillresultinalowerPVoffuturebenefitpaymentsandviceversa.ThePlanliabilitiesarelongterm in nature and, thus, the present value of the liabilities is sensitive to changes in real interest rates.

and measured in a number of different ways, as outlined in appendix II. For the SRP, the liabilities are long term in nature and, thus, sensitive to changes in real interest rates.

The most widely used and publicly disclosed measure of pension plan liabilities for an open plan istheprojectedbenefitobligation(PBO)measure.This measure is required by the International FinancialReportingStandards(IFRS)andtheGenerally Accepted Accounting Principles in the UnitedStates(U.S.GAAP)forplansponsors,and is the most commonly used and reported measurewithinthepensionindustry.Itreflectsthepresentvalueofallretirementbenefitsearned

byparticipants(adjustedforassumedinflation)as of a given date, including projected salary increases to retirement. Therefore, the funded ratio based on the PBO measure13 is the single mostappropriatemetricforassessingthefinancialposition(i.e.theabilitytocoverearnedbenefits)ofthe Plan as of a certain date.

13Otherliabilitymeasures,liketheClosed,Open,andModifiedOpenGroup, that anticipate and account for expected future service accruals (forcurrentorevenfuturepopulation)andthatuseaconstant3.5percent real discount rate every year create stable contribution patterns and are more suitable for funding purposes.

The discount rate used to convert the PBO obligations into today’s dollars is derived from high-grade corporate bond yields as required by the globally recognized IFRS and U.S. GAAP for plan sponsors. The present value of the PBO measure based on prevailing high-quality (AA-rated)corporatebondyields—discountedusing the entire yield curve from Citigroup14 and basedontheinflationexpectationspublishedby

14TheCitigroupcurveiswidelyusedforPBOdetermination,asitisobjective, transparent, and readily available. It is disseminated by the Society of Actuaries at www.soa.org/professional-interests/pension/resources/pen-resources-pension.aspx.

10-year 20-year Since 1990

Nominal 7.1% 7.3% 8.0%Real 4.6% 4.8% 5.2%

Annualized Nominal and Real Net Investment

Returns as of December 31, 2013

PBO–Funded Ratio at December 31, 2013

1.00

$3.2 billion $17.1 billion Benefit payments Investment exceeding contributions income

Cumulative Flows since 1990

Impact on Funded Ratio of One Percent Increase

in Interest Rate

+14 %

21

Fina

ncia

l Hea

lth

of th

e Pl

an

20

the Cleveland Federal Reserve15 — was $17.3 billion16 as of December 31, 2013. The effective realdiscountrateunderlyingthisfigurewasapproximately 2.7 percent. The fair value of the Plan’s net assets were $17.3 billion, resulting in a PBO-based funded ratio of 1.0017(figure2.1)as of December 31, 2013. By way of reference, the average PBO-funded ratio for the 100 largest U.S.-based pension plans, according to Milliman18, stoodat0.95atthatdate.

The investment performance in 2013 coupled with the increase in real AA discount rate contributed to the increase of the funded ratio for the Plan, from 0.88 to 1.00. Implied real AA interest rates, which areusedtodiscountthebenefitcashflows,rosein2013bymorethan65basispoints(figure2.2).

15TheClevelandFederalReservepublishesinflationforecaststhatareconsistent with market yields, available at www.clevelandfed.org/research/data/inflation_expectations/index.cfm.16Approximately15percentoftheseobligationsarecurrentlyestimatedtobedenominatedincurrenciesotherthantheU.S.dollar,reflectingtheaggregate impact of the currency choices made thus far by individual eligible retirees.17 A PBO-based funded ratio of 1.00 indicates that all accrued rights todateareexactlycoveredbytheassets;futurecontributionswillcoverfuture rights only.18Milliman,apensionconsultingandadvisoryfirm,conductsannualpension funding studies of the 100 largest U.S. public corporations that sponsordefined-benefitpensionplans.Thestudyisbasedonpensionplan accounting information disclosed in the footnotes to the companies’ annual reports.

In order to assess the risk and return trade-offs underlying the management of the Plan, two additional approaches are used to calculate the presentvalueofthePBOmeasure.Thefirstapproach is based on the Long-Term Real Return Objective(LTRRO)of3.5percentusedinthefunding methodology. On this basis, the resulting funded ratio was 1.10 at year end 2013.

This indicates that, using the real return assumption in the funding methodology, the assets are more than keeping pace with the liabilities over time. The second approach is based on risk-free real interest rates—real interest rates derived from U.S. Government TIPS with maturitiescorrespondingtothetimeprofileofthebenefitcashflows.AsofDecember31,2013,this approach produced a funded ratio of 0.83, an increase of 18 basis points, aided by strong investment returns and a rise in real interest rate ofmorethan140basispoints.Thisapproachillustrates the extent to which the current assets, if invested to eliminate inflation and investment risk, wouldmeetbenefitspaymentsaccruedpriortoDecember 31, 2013. It is important to note that this funded ratio is not widely used, represents a much more conservative measure than just

described, and is not comparable to the funded ratios often quoted in the press for other plans. The differences between the funded ratios are discussed in detail in appendix II.

A combination of staff and Bank contributions and investmentreturns(figure2.3)augmentthePlanassetsandtogetherfundthebenefitspaidtotheretirees. The amount that the Plan pays each year inpensionbenefitsisnowgreaterthantheamountit collects in contributions.

In 2013, Bank and staff contributions were $302 million and $118 million, respectively. Net investment earnings, after all fees and administrativeexpenses,amountedto$1,511million;andpensionbenefitpaymentstotaled$679million.

Figure2.4 shows the dollar impact of investment returns and net contributions (i.e., contributions lessbenefitpayments)onthegrowthoftheassetsof the Plan over various time periods. Over the past 10-year and 20-year periods, the Plan’s assets have increased by $7.0 billion and $11.7 billion, respectively, with investment performance not only driving the growth in assets, but also contributing totheregularpensionbenefitpayments.

7.1

9.2

15.1

-1.4 -2

.2

-3.5

5.7 7.

0

11.7

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Last 5 Years Last 10 Years Last 20 Years

US$

bill

ion

Net investment income Contribution of net benefit payments Net change in plan assets

Figure 2.4: Dollar Impact on Plan Assets from Investment Returns and Net Contributions

77

77

80

87

97

98

103

108

111

118

184 24

8

224

161

101

131 19

9 224 260 30

2

-366

-397

-447

-480

-510

-528

-560

-619

-653

-679

-3,600

-2,700

-1,800

-900

0

900

1,800

2,700

-800

-600

-400

-200

0

200

400

600

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

US$

mill

ion

Staff contributions (left scale) Bank contributions (left scale)

Benefit payments (left scale) Net investment income (right scale)

US$

mill

ion

Figure 2.3: Annual Contributions, Net Investment Income and Benefit Payments (2004-2013)

2322

Fina

ncia

l Man

agem

ent

of th

e Pl

an

SECTION III

Financial Management of the Plan

=+ BenefitLiabilities

CurrentPlan

Assets

InvestmentReturns

Contributions

Actuarial Value

of Assets

PV of Staff

Contributions

PV of Required Bank

Contributions

PV of Benefits for Current

and Former Staff

PV of Benefits for Future

Staff+ + +

Box 3.1:

A Snapshot of Plan Governance and Funding

Pension Finance Committee Responsibility The PFC oversees the Plan’s financial management. The PFC is responsible for the following:

§§ Arranging regular actuarial valuations of assets and liabilities

§§ Reviewing and adopting assumptions underlying such valuations after obtaining recommendations from the Plan’s actuaries

§§ Determining the Bank’s contributions on the basis of those actuarial valuations after consulting with the Bank.

Bank Responsibility§§ The Bank’s obligations are based on the

Plan Document approved by the Board.

§§ The Plan Document provides that the Bank shall contribute to the Plan the amount determined by the PFC on the basis of actuarial valuations after consulting with the Bank.

Plan Document and Principles of Staff Employment§§ The Plan may not be amended to reduce

benefits to which Plan participants have already become entitled.

§§ The Principles of Staff Employment, approved by the Board, prohibit the retroactive reduction of compensation for services already rendered.

FUNDING POLICY

The funding policy for a pension plan such as the SRP seeks to determine how much a plan

sponsor must contribute annually to sustain and ensuretheaccumulationofsufficientplanassetsovertimetomeettheexpectedbenefitpayments.A funding policy often has to balance competing objectives avoiding excessive volatility in sponsor contributions and maintaining the participants’ securitybyfundingplanbenefitpaymentswithoutaccumulatingexcesssurplusesordeficits.

The SRP’s funding policy is approved by the PFC. The policy determines the Bank’s annual contributions to the Plan and incorporates the actuarial principles and assumptions used to calculate the Plan assets and liabilities. The following steps determine the Bank’s annual contributions:

1. Estimating the value of Plan assets and liabilities and the PV of projected future staff contributions, all in accordance with actuarial principles as of the end of the previouscalendaryear(CY):Theliabilitiesand the PV of projected staff contributions are calculated using the relevant population of staff and new entrants assumed in the funding methodology (refer to appendix II formoredetails).

2. Computing the difference between the actuarial value of Plan liabilities and the actuarial value of Plan assets, after accounting for the PV of projected staff contributions: The difference, if any, is the PV of contributions needed from the Bank.

+

Assets Liabilities

The SRP benefit payments are funded by plan assets, staff and Bank contributions, and investment returns. Staff contributions are fixed as a percentage of salaries, while the Bank’s contributions and the Plan’s investment returns vary. The key policies underpinning the determination of sponsor contributions and guiding the investment of Plan assets are the funding and investment policies. The objective of these policies is to ensure that the Plan has sufficient assets to meet benefit payments over the long term.

The funding policy, approved by the PFC, establishes the actuarial principles and assumptions used to determine the Bank’s annual contributions to the Plan. The funding policy effectively assumes a real return on plan investments (3.5 percent since 1999) and this rate constitutes the long-term objective or “hurdle rate” for Plan assets (referred to as the LTRRO). This is the real rate of return that the plan assets are expected to earn on average over the long term. Consequently, the PFC believes that the LTRRO is the most appropriate metric for assessing whether investment returns are meeting funding policy assumptions.

The investment of Plan assets is directed by the Plan’s investment policy. A major component of the investment policy is the strategic asset allocation (SAA) which represents the asset mix that the PFC believes is best able to meet the LTRRO over a given investment horizon and within acceptable risk parameters. At any point in time, the return assumptions underlying a given SAA are dependent on the particular market environment. These return assumptions, which have varied – and will vary - over time, guide the PFC in determining the appropriate level of risk taking on plan assets in order to meet or exceed the LTRRO. The SAA is periodically reviewed and approved by the PFC as appropriate.

=

25

Fina

ncia

l Man

agem

ent

of th

e Pl

an

24

24.8

4

23.9

4

22.3

5

20.1

1

5.00

15.0

9

25.6

2

26.7

2

18.3

5

12.2

3

5.74

15.5

5

15.3

0 17.6

4

18.9

1

20.8

8

18.9

8

0

5

10

15

20

30

1994 1997 2000 2003 2006 2009 2012 2015

Perc

ent (

%)

Fiscal year (FY) ending June 30

Note: Bank contributions were suspended from FY98 to FY02. Actual Projected FY15

25

Figure 3.1: Bank SRP Contribution Rates since Fiscal Year 1994*

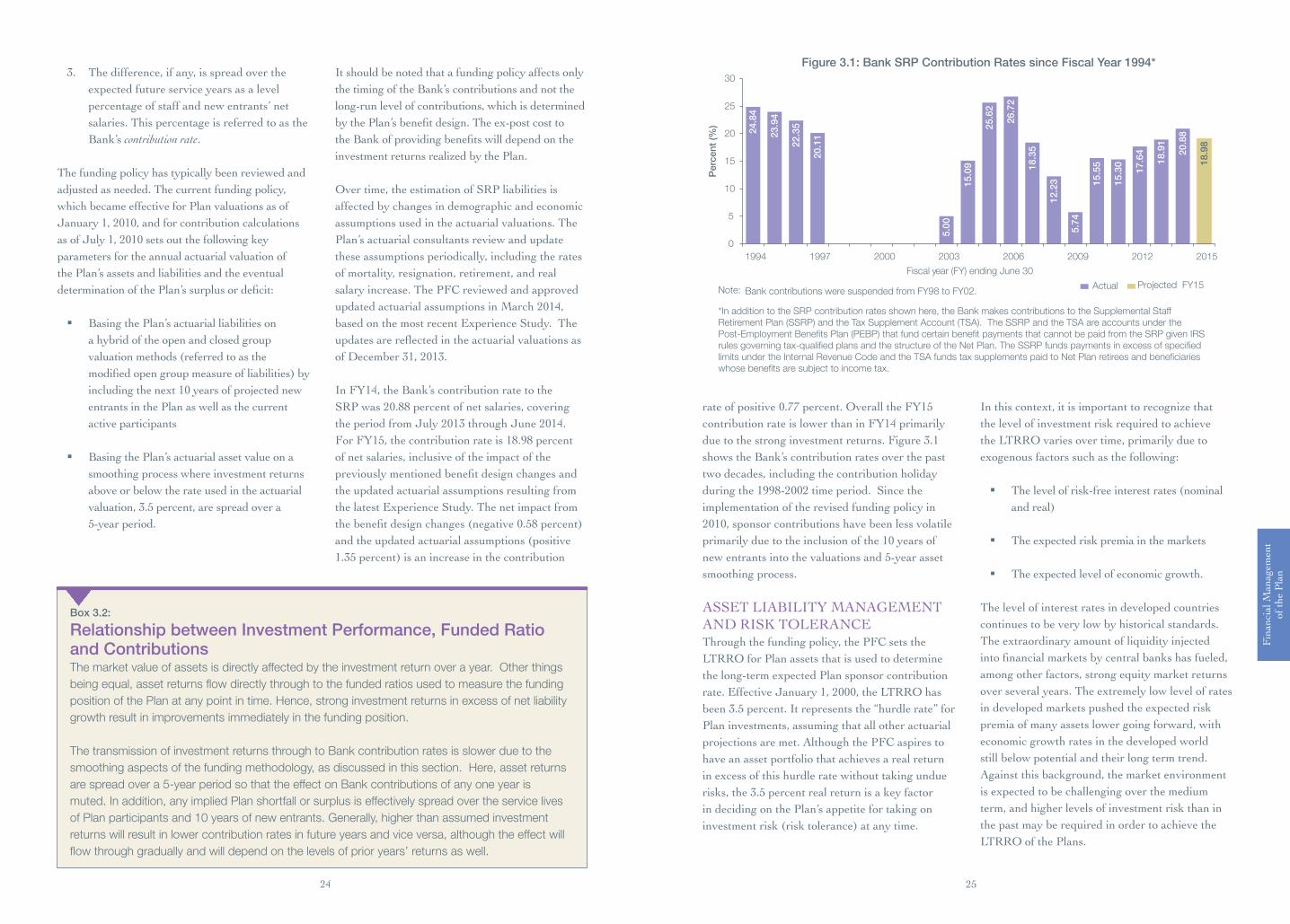

*In addition to the SRP contribution rates shown here, the Bank makes contributions to the Supplemental Staff Retirement Plan (SSRP) and the Tax Supplement Account (TSA). The SSRP and the TSA are accounts under the Post-Employment Benefits Plan (PEBP) that fund certain benefit payments that cannot be paid from the SRP given IRS rules governing tax-qualified plans and the structure of the Net Plan. The SSRP funds payments in excess of specified limits under the Internal Revenue Code and the TSA funds tax supplements paid to Net Plan retirees and beneficiaries whose benefits are subject to income tax.

Box 3.2:

Relationship between Investment Performance, Funded Ratio and ContributionsThe market value of assets is directly affected by the investment return over a year. Other things being equal, asset returns flow directly through to the funded ratios used to measure the funding position of the Plan at any point in time. Hence, strong investment returns in excess of net liability growth result in improvements immediately in the funding position.

The transmission of investment returns through to Bank contribution rates is slower due to the smoothing aspects of the funding methodology, as discussed in this section. Here, asset returns are spread over a 5-year period so that the effect on Bank contributions of any one year is muted. In addition, any implied Plan shortfall or surplus is effectively spread over the service lives of Plan participants and 10 years of new entrants. Generally, higher than assumed investment returns will result in lower contribution rates in future years and vice versa, although the effect will flow through gradually and will depend on the levels of prior years’ returns as well.

3. The difference, if any, is spread over the expected future service years as a level percentage of staff and new entrants’ net salaries. This percentage is referred to as the Bank’s contribution rate.

The funding policy has typically been reviewed and adjusted as needed. The current funding policy, which became effective for Plan valuations as of January 1, 2010, and for contribution calculations as of July 1, 2010 sets out the following key parameters for the annual actuarial valuation of the Plan’s assets and liabilities and the eventual determinationofthePlan’ssurplusordeficit:

§ Basing the Plan’s actuarial liabilities on a hybrid of the open and closed group valuation methods (referred to as the modifiedopengroupmeasureofliabilities)byincluding the next 10 years of projected new entrants in the Plan as well as the current active participants

§ Basing the Plan’s actuarial asset value on a smoothing process where investment returns above or below the rate used in the actuarial valuation,3.5percent,arespreadovera5-yearperiod.

It should be noted that a funding policy affects only the timing of the Bank’s contributions and not the long-run level of contributions, which is determined bythePlan’sbenefitdesign.Theex-postcosttotheBankofprovidingbenefitswilldependontheinvestment returns realized by the Plan.

Over time, the estimation of SRP liabilities is affected by changes in demographic and economic assumptions used in the actuarial valuations. The Plan’s actuarial consultants review and update these assumptions periodically, including the rates of mortality, resignation, retirement, and real salary increase. The PFC reviewed and approved updatedactuarialassumptionsinMarch2014,based on the most recent Experience Study. The updatesarereflectedintheactuarialvaluationsasof December 31, 2013.

InFY14,theBank’scontributionratetotheSRP was 20.88 percent of net salaries, covering theperiodfromJuly2013throughJune2014.ForFY15,thecontributionrateis18.98percentof net salaries, inclusive of the impact of the previouslymentionedbenefitdesignchangesandthe updated actuarial assumptions resulting from the latest Experience Study. The net impact from thebenefitdesignchanges(negative0.58percent)and the updated actuarial assumptions (positive 1.35percent)isanincreaseinthecontribution

rateofpositive0.77percent.OveralltheFY15contributionrateislowerthaninFY14primarilydue to the strong investment returns. Figure 3.1 shows the Bank’s contribution rates over the past two decades, including the contribution holiday duringthe1998-2002timeperiod.Sincetheimplementation of the revised funding policy in 2010, sponsor contributions have been less volatile primarily due to the inclusion of the 10 years of newentrantsintothevaluationsand5-yearassetsmoothing process.

ASSET LIABILITY MANAGEMENT AND RISK TOLERANCEThrough the funding policy, the PFC sets the LTRRO for Plan assets that is used to determine the long-term expected Plan sponsor contribution rate. Effective January 1, 2000, the LTRRO has been3.5percent.Itrepresentsthe“hurdlerate”forPlan investments, assuming that all other actuarial projections are met. Although the PFC aspires to have an asset portfolio that achieves a real return in excess of this hurdle rate without taking undue risks,the3.5percentrealreturnisakeyfactorin deciding on the Plan’s appetite for taking on investmentrisk(risktolerance)atanytime.

In this context, it is important to recognize that the level of investment risk required to achieve the LTRRO varies over time, primarily due to exogenous factors such as the following:

§ The level of risk-free interest rates (nominal andreal)

§ The expected risk premia in the markets

§ The expected level of economic growth.

The level of interest rates in developed countries continues to be very low by historical standards. The extraordinary amount of liquidity injected intofinancialmarketsbycentralbankshasfueled,among other factors, strong equity market returns over several years. The extremely low level of rates in developed markets pushed the expected risk premia of many assets lower going forward, with economic growth rates in the developed world still below potential and their long term trend. Against this background, the market environment is expected to be challenging over the medium term, and higher levels of investment risk than in the past may be required in order to achieve the LTRRO of the Plans.

Fina

ncia

l Man

agem

ent

of th

e Pl

an

26 27

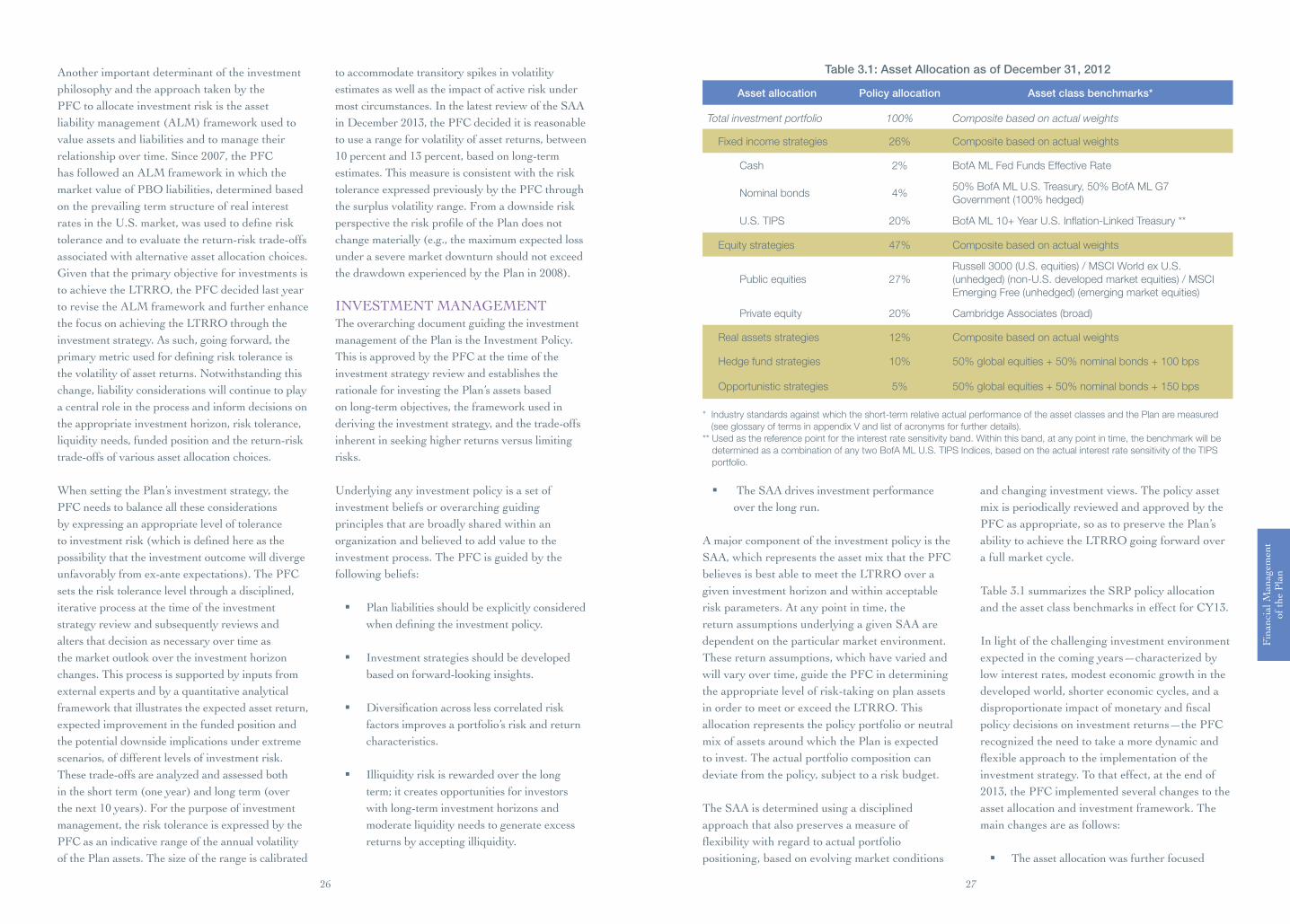

Table 3.1: Asset Allocation as of December 31, 2012

Asset allocation Policy allocation Asset class benchmarks*

Total investment portfolio 100% Composite based on actual weights

Fixed income strategies 26% Composite based on actual weights

Cash 2% BofA ML Fed Funds Effective Rate

Nominal bonds 4%50% BofA ML U.S. Treasury, 50% BofA ML G7 Government (100% hedged)

U.S. TIPS 20% BofA ML 10+ Year U.S. Inflation-Linked Treasury **

Equity strategies 47% Composite based on actual weights

Public equities 27%Russell 3000 (U.S. equities) / MSCI World ex U.S. (unhedged) (non-U.S. developed market equities) / MSCI Emerging Free (unhedged) (emerging market equities)

Private equity 20% Cambridge Associates (broad)

Real assets strategies 12% Composite based on actual weights

Hedge fund strategies 10% 50% global equities + 50% nominal bonds + 100 bps

Opportunistic strategies 5% 50% global equities + 50% nominal bonds + 150 bps

* Industry standards against which the short-term relative actual performance of the asset classes and the Plan are measured (see glossary of terms in appendix V and list of acronyms for further details).

** Used as the reference point for the interest rate sensitivity band. Within this band, at any point in time, the benchmark will be determined as a combination of any two BofA ML U.S. TIPS Indices, based on the actual interest rate sensitivity of the TIPS portfolio.

Another important determinant of the investment philosophy and the approach taken by the PFC to allocate investment risk is the asset liabilitymanagement(ALM)frameworkusedtovalue assets and liabilities and to manage their relationship over time. Since 2007, the PFC has followed an ALM framework in which the market value of PBO liabilities, determined based on the prevailing term structure of real interest ratesintheU.S.market,wasusedtodefinerisktolerance and to evaluate the return-risk trade-offs associated with alternative asset allocation choices. Given that the primary objective for investments is to achieve the LTRRO, the PFC decided last year to revise the ALM framework and further enhance the focus on achieving the LTRRO through the investment strategy. As such, going forward, the primarymetricusedfordefiningrisktoleranceisthe volatility of asset returns. Notwithstanding this change, liability considerations will continue to play a central role in the process and inform decisions on the appropriate investment horizon, risk tolerance, liquidity needs, funded position and the return-risk trade-offs of various asset allocation choices. When setting the Plan’s investment strategy, the PFC needs to balance all these considerations by expressing an appropriate level of tolerance toinvestmentrisk(whichisdefinedhereasthepossibility that the investment outcome will diverge unfavorablyfromex-anteexpectations).ThePFCsets the risk tolerance level through a disciplined, iterative process at the time of the investment strategy review and subsequently reviews and alters that decision as necessary over time as the market outlook over the investment horizon changes. This process is supported by inputs from external experts and by a quantitative analytical framework that illustrates the expected asset return, expected improvement in the funded position and the potential downside implications under extreme scenarios, of different levels of investment risk. These trade-offs are analyzed and assessed both intheshortterm(oneyear)andlongterm(overthenext10years).Forthepurposeofinvestmentmanagement, the risk tolerance is expressed by the PFC as an indicative range of the annual volatility of the Plan assets. The size of the range is calibrated

to accommodate transitory spikes in volatility estimates as well as the impact of active risk under most circumstances. In the latest review of the SAA in December 2013, the PFC decided it is reasonable to use a range for volatility of asset returns, between 10 percent and 13 percent, based on long-term estimates. This measure is consistent with the risk tolerance expressed previously by the PFC through the surplus volatility range. From a downside risk perspectivetheriskprofileofthePlandoesnotchange materially (e.g., the maximum expected loss under a severe market downturn should not exceed thedrawdownexperiencedbythePlanin2008).

INVESTMENT MANAGEMENTThe overarching document guiding the investment management of the Plan is the Investment Policy. This is approved by the PFC at the time of the investment strategy review and establishes the rationale for investing the Plan’s assets based on long-term objectives, the framework used in deriving the investment strategy, and the trade-offs inherent in seeking higher returns versus limiting risks.

Underlying any investment policy is a set of investment beliefs or overarching guiding principles that are broadly shared within an organization and believed to add value to the investment process. The PFC is guided by the following beliefs:

§ Plan liabilities should be explicitly considered whendefiningtheinvestmentpolicy.

§ Investment strategies should be developed based on forward-looking insights.

§ Diversificationacrosslesscorrelatedriskfactors improves a portfolio’s risk and return characteristics.

§ Illiquidity risk is rewarded over the long term;itcreatesopportunitiesforinvestorswith long-term investment horizons and moderate liquidity needs to generate excess returns by accepting illiquidity.

§ The SAA drives investment performance over the long run.

A major component of the investment policy is the SAA, which represents the asset mix that the PFC believes is best able to meet the LTRRO over a given investment horizon and within acceptable risk parameters. At any point in time, the return assumptions underlying a given SAA are dependent on the particular market environment. These return assumptions, which have varied and will vary over time, guide the PFC in determining the appropriate level of risk-taking on plan assets in order to meet or exceed the LTRRO. This allocation represents the policy portfolio or neutral mix of assets around which the Plan is expected to invest. The actual portfolio composition can deviate from the policy, subject to a risk budget.

The SAA is determined using a disciplined approach that also preserves a measure of flexibilitywithregardtoactualportfoliopositioning, based on evolving market conditions

and changing investment views. The policy asset mix is periodically reviewed and approved by the PFC as appropriate, so as to preserve the Plan’s ability to achieve the LTRRO going forward over a full market cycle.

Table 3.1 summarizes the SRP policy allocation and the asset class benchmarks in effect for CY13.

In light of the challenging investment environment expected in the coming years—characterized by low interest rates, modest economic growth in the developed world, shorter economic cycles, and a disproportionateimpactofmonetaryandfiscalpolicy decisions on investment returns—the PFC recognized the need to take a more dynamic and flexibleapproachtotheimplementationoftheinvestment strategy. To that effect, at the end of 2013, the PFC implemented several changes to the asset allocation and investment framework. The main changes are as follows:

§ The asset allocation was further focused

28 29

Fina

ncia

l Man

agem

ent

of th

e Pl

an

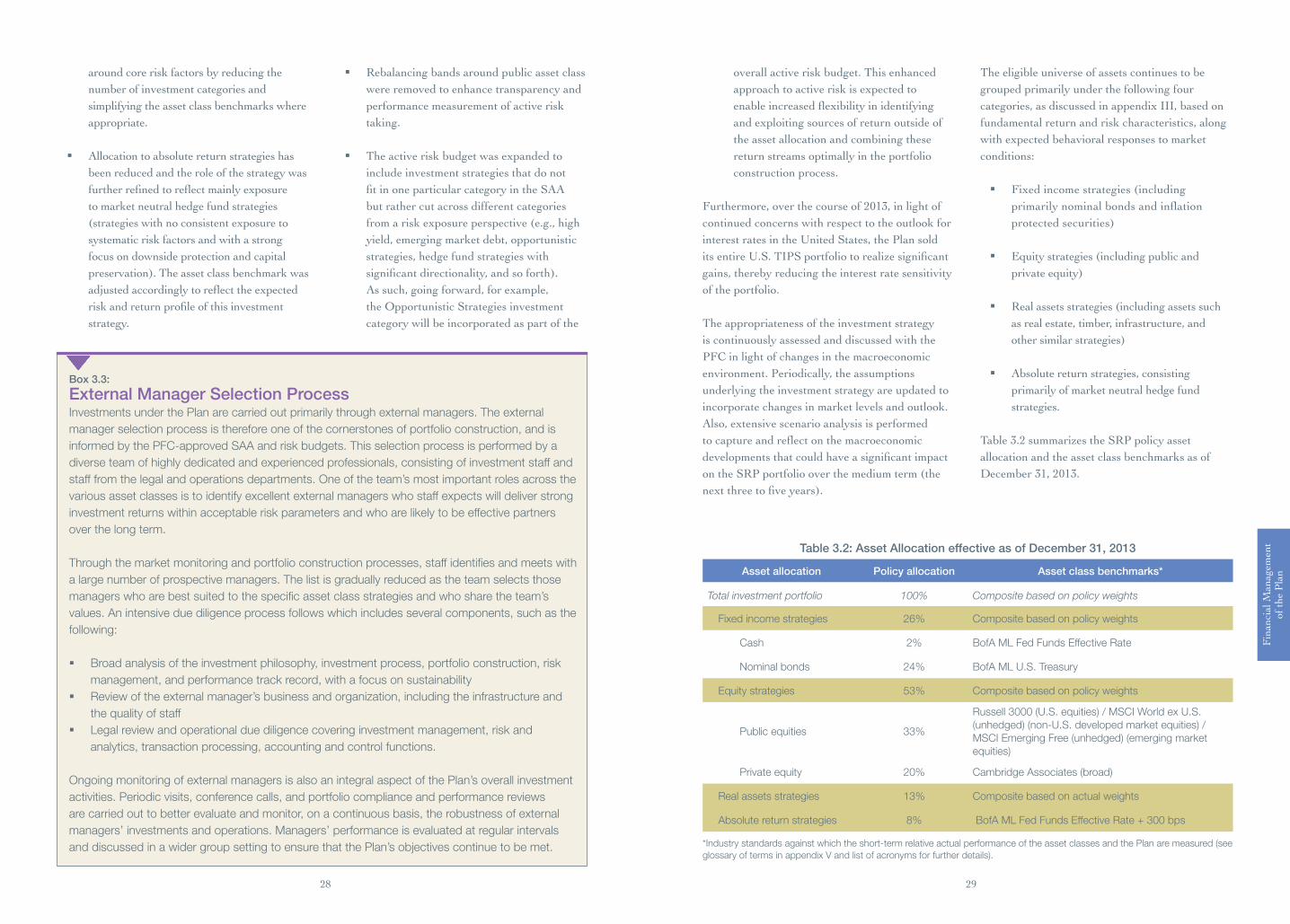

Table 3.2: Asset Allocation effective as of December 31, 2013

Asset allocation Policy allocation Asset class benchmarks*

Total investment portfolio 100% Composite based on policy weights

Fixed income strategies 26% Composite based on policy weights

Cash 2% BofA ML Fed Funds Effective Rate

Nominal bonds 24% BofA ML U.S. Treasury

Equity strategies 53% Composite based on policy weights

Public equities 33%

Russell 3000 (U.S. equities) / MSCI World ex U.S. (unhedged) (non-U.S. developed market equities) / MSCI Emerging Free (unhedged) (emerging market equities)

Private equity 20% Cambridge Associates (broad)

Real assets strategies 13% Composite based on actual weights

Absolute return strategies 8% BofA ML Fed Funds Effective Rate + 300 bps

*Industry standards against which the short-term relative actual performance of the asset classes and the Plan are measured (see glossary of terms in appendix V and list of acronyms for further details).

Box 3.3:

External Manager Selection Process Investments under the Plan are carried out primarily through external managers. The external manager selection process is therefore one of the cornerstones of portfolio construction, and is informed by the PFC-approved SAA and risk budgets. This selection process is performed by a diverse team of highly dedicated and experienced professionals, consisting of investment staff and staff from the legal and operations departments. One of the team’s most important roles across the various asset classes is to identify excellent external managers who staff expects will deliver strong investment returns within acceptable risk parameters and who are likely to be effective partners over the long term.

Through the market monitoring and portfolio construction processes, staff identifies and meets with a large number of prospective managers. The list is gradually reduced as the team selects those managers who are best suited to the specific asset class strategies and who share the team’s values. An intensive due diligence process follows which includes several components, such as the following:

§ Broad analysis of the investment philosophy, investment process, portfolio construction, risk management, and performance track record, with a focus on sustainability