Staff Audit Report of - Oregon Public Utility Commission NWN Final 3-7...OPUC Staff Audit Report...

66

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017 1 Staff Audit Report of Northwest Natural Audit Number: 17-001 Audit team: Marianne Gardner (Lead Auditor) Scott Gibbens Lisa Gorsuch Judy Johnson Mitch Moore Matthew Muldoon Prepared by: Marianne Gardner

Transcript of Staff Audit Report of - Oregon Public Utility Commission NWN Final 3-7...OPUC Staff Audit Report...

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

1

Staff Audit Report of Northwest Natural Audit Number: 17-001

Audit team: Marianne Gardner (Lead Auditor) Scott Gibbens Lisa Gorsuch Judy Johnson Mitch Moore Matthew Muldoon Prepared by: Marianne Gardner

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

2

Staff Audit Report of Northwest Natural

Table of Contents

Executive Summary ............................................................................................ 4 Audit Objectives and Scope .............................................................................. 4 Audit Areas ........................................................................................................ 4 Audit Results ..................................................................................................... 5 Other Comments ............................................................................................... 5

Summary of Recommendations ........................................................................ 6 Company Background and Organization ....................................................... 14 Affiliated Interest and Cost Allocations .......................................................... 14

Affiliated Interests ............................................................................................ 14 Affiliate Transactions ....................................................................................... 16

Capital Projects ................................................................................................. 18 Oregon Situs Utility Plant ................................................................................ 18 System Integrity Programs .............................................................................. 21 Storage ............................................................................................................ 21

Schedule 90 Conditions of Approval ............................................................ 22 WARM & Decoupling ....................................................................................... 24 Pipeline Capital Costs ..................................................................................... 25 Accounting ...................................................................................................... 25 Competitive Bidding ........................................................................................ 26 Information Technology Capital Projects ......................................................... 26

I-Series Recovery Project ............................................................................ 26 Technology Refresh-Desktops/Laptops and Peripherals ............................. 27 Technology Refresh-Large Servers/SANs ................................................... 27 GMAC Upgrade ........................................................................................... 28 Customer Order Management ..................................................................... 29 Enterprise Content Management ................................................................. 30 PCAD Upgrade ............................................................................................ 31 SAP Upgrade – Phase II .............................................................................. 31 J5 Implementation ....................................................................................... 32 Voice Radio Operations Improvement (VROI) – Phase II ............................ 32 Sherwood Microwave Tower........................................................................ 33 Eagle Wireless ............................................................................................. 34 Unified Communications – Phase 2 ............................................................. 35 ICS Network Segmentation – Cybersecurity Program ................................. 36 RLMAN Replacement .................................................................................. 36

Allowance for Funds Used During Construction (AFUDC) .............................. 37 Actual Financial Performance.......................................................................... 37

Actual Returns ................................................................................................. 37 Budget Versus Actual ...................................................................................... 39

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

3

Comparison to Other Natural Gas Utilities in Oregon ...................................... 40 Administrative and General (A&G) Expenses ................................................ 42

Cost Comparisons ........................................................................................... 42 Advertising ...................................................................................................... 43 Uncollectible Expenses ................................................................................... 43 Insurance Services, Injuries, and Damages .................................................... 45 Other Administrative & General Expense Adjustments ................................... 46 Legal Fees ...................................................................................................... 46

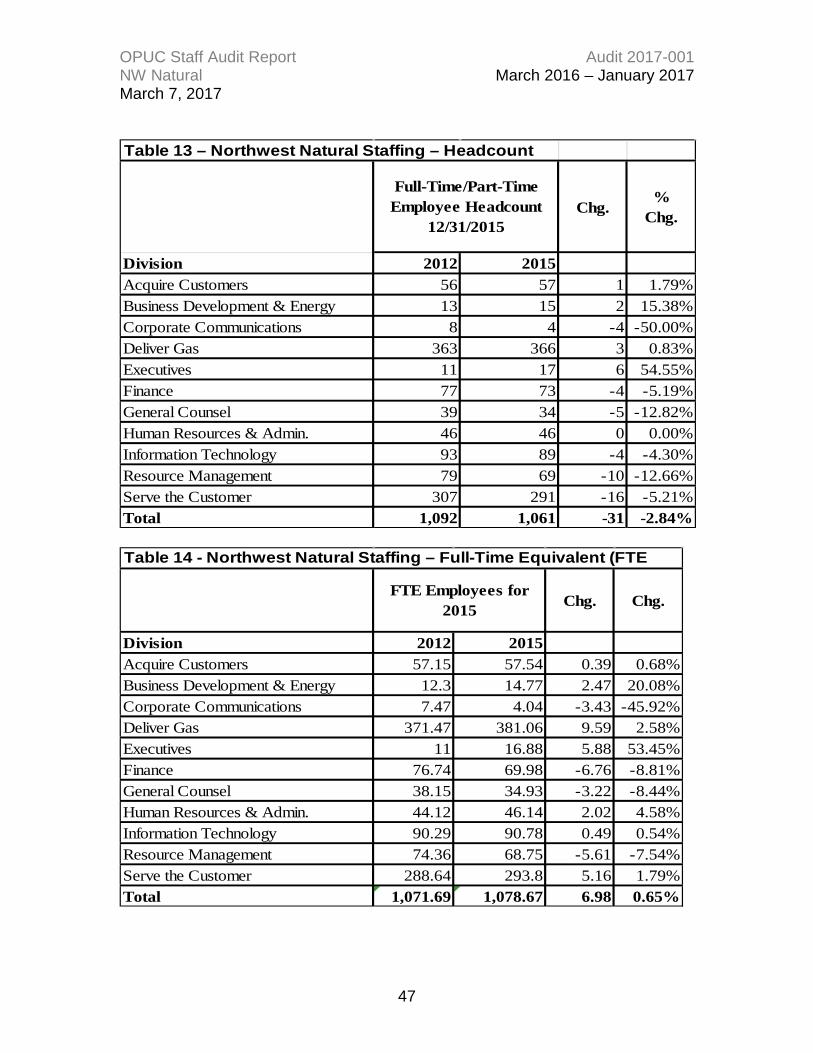

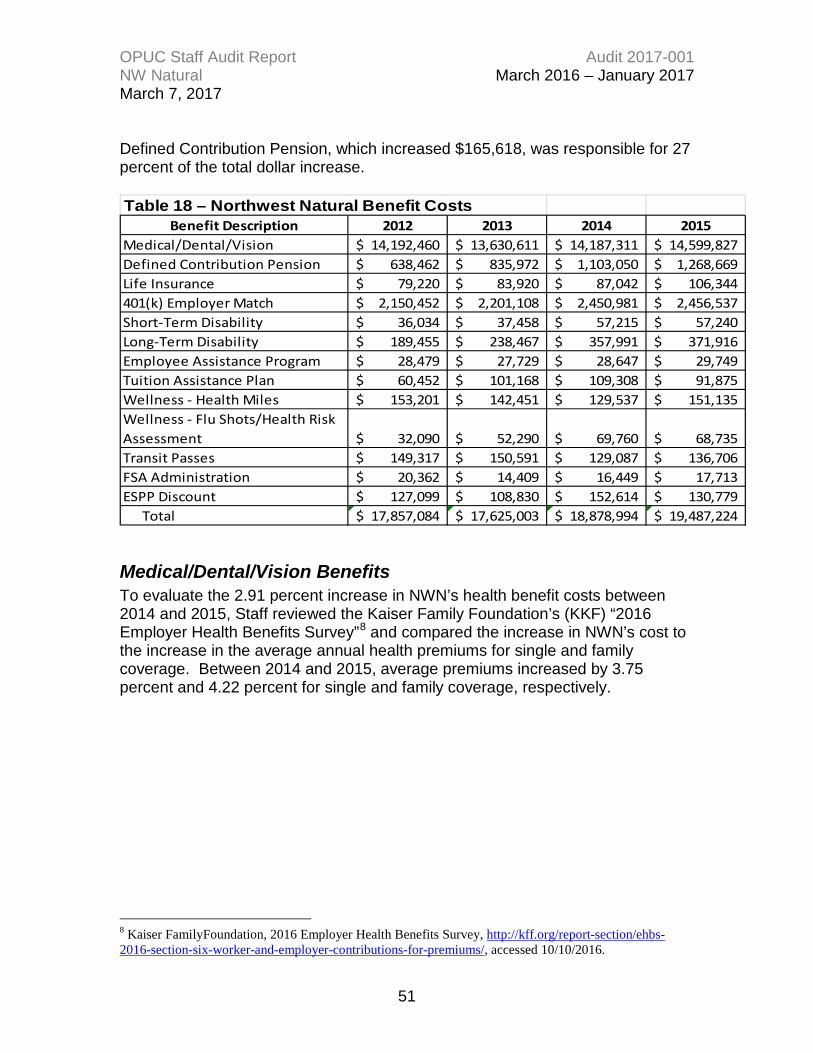

Labor Costs ....................................................................................................... 46 Staffing ............................................................................................................ 46 Severance Costs ............................................................................................. 48 Incentive Costs ................................................................................................ 48 Labor Loadings................................................................................................ 49 Benefits ........................................................................................................... 50 Medical/Dental/Vision Benefits ........................................................................ 51 Pension and Postretirement Costs .................................................................. 53

Operations and Maintenance Expenses ......................................................... 55 Taxes .................................................................................................................. 56

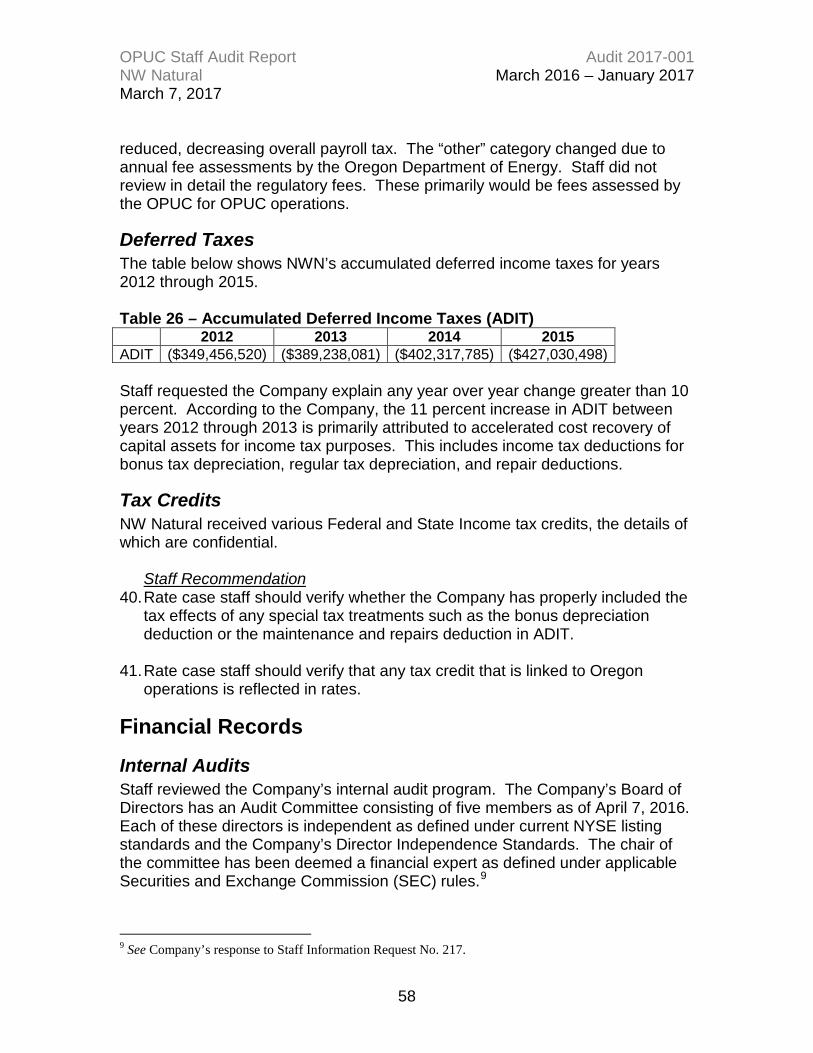

Income Taxes .................................................................................................. 56 Other Taxes..................................................................................................... 57 Deferred Taxes ................................................................................................ 58 Tax Credits ...................................................................................................... 58

Financial Records ............................................................................................. 58 Internal Audits ................................................................................................. 58 FAS 133 Mark-to-Market Accounting .............................................................. 59 Property Sales ................................................................................................. 59

Cost of Capital................................................................................................... 59 Securities Issuance ......................................................................................... 59 Long-Term Debt .............................................................................................. 60 Snapshot ......................................................................................................... 61

Cash Flows .................................................................................................. 61 Credit Facilities ............................................................................................ 62 Dividends ..................................................................................................... 62

Advice by Investment Banks to Northwest Natural .......................................... 63 Customer Service ............................................................................................. 63

Customer Count, Complaints, and Service Levels ....................................... 63

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

4

Executive Summary Audit Staff (Staff) conducted an Operational Audit of Northwest Natural (NW Natural, NWN, or Company) during the March 2016 through January 2017 timeframe. As part of the audit, Staff submitted 257 data requests to NW Natural. Although Staff focused on operations from fiscal years 2012 through 2015, Staff examined additional data for consistency and that can be reviewed as historical information in a future regulatory proceeding. In addition to NW Natural's responses to Staff's data requests, Staff relied on the following resources: 1. NW Natural Reports Results for the Quarter Ending March 31, 2016,

Company Release May 3, 2016; 2. NW Natural Form 8-K Current Reports filed with the U.S. Securities and

Exchange Commission (SEC); 3. Thompson Reuters Street-Events Edited Transcript of NWN – Q1 2016

Earnings Call of May 3, 2016; 4. NW Natural Form 10-Q filed with the SEC for the quarterly period ended

March 31, 2016; 5. “Lead, Innovate, Grow,” NW Natural Investor Presentation of June 2016 and

updated for September 2016; 6. NW Natural's Fiscal Year 2015 Results of Operations Report; 7. NW Natural's Fiscal Year 2015 Affiliated Interest Annual Report; 8. NW Natural’s calendar year 2015 FORM 10-K Annual Report filed with the

SEC; 9. NW Natural's 2015 FERC Form 2 report; 10. An analysis of NW Natural’s historic and outstanding debt securities utilizing

Bloomberg and SNL Financial, LLC; and 11. NW Natural 2016 annual shareholder meeting presentation, “Building with

foresight.”

Audit Objectives and Scope 1. Review and provide information that will assist Staff in the next NW

Natural rate case. 2. Provide an information base for future regulatory proceedings and other

inquiries into the operations of NW Natural.

3. Develop suggestions for further investigation during a rate case.

Audit Areas Staff audited the following areas and topics:

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

5

1. Company Background 2. Affiliated Interest 3. Capital Projects 4. Information Technology (IT) Capital Projects 5. Allowance for Funds Used During Construction (AFUDC) 6. Actual Financial Performance 7. Administrative and General Costs 8. Labor Costs 9. Operations and Maintenance (O&M) 10. Taxes 11. Financial Records 12. Securities Issuances 13. Customer Service

Audit Results Staff’s audit led to several recommendations to staff assigned to NW Natural’s next general rate case (rate case staff) regarding topics for examination and to a few recommendations that are pertinent to staff’s review of other types of filings.1 It is important to note that the audit was performed on a sample basis. Staff involved in the Company’s next rate case may discover issues and concerns that were not encountered during the audit process or may not align with the Audit Staff's findings. Additionally, these recommendations should not be construed as final rate case adjustments, as each subject area will undergo further review by staff during NW Natural's rate case.

Other Comments Staff appreciates NW Natural's responsiveness and cooperation during the audit process.

1 The latter issues are identified as “general issues” in the Audit Report.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

6

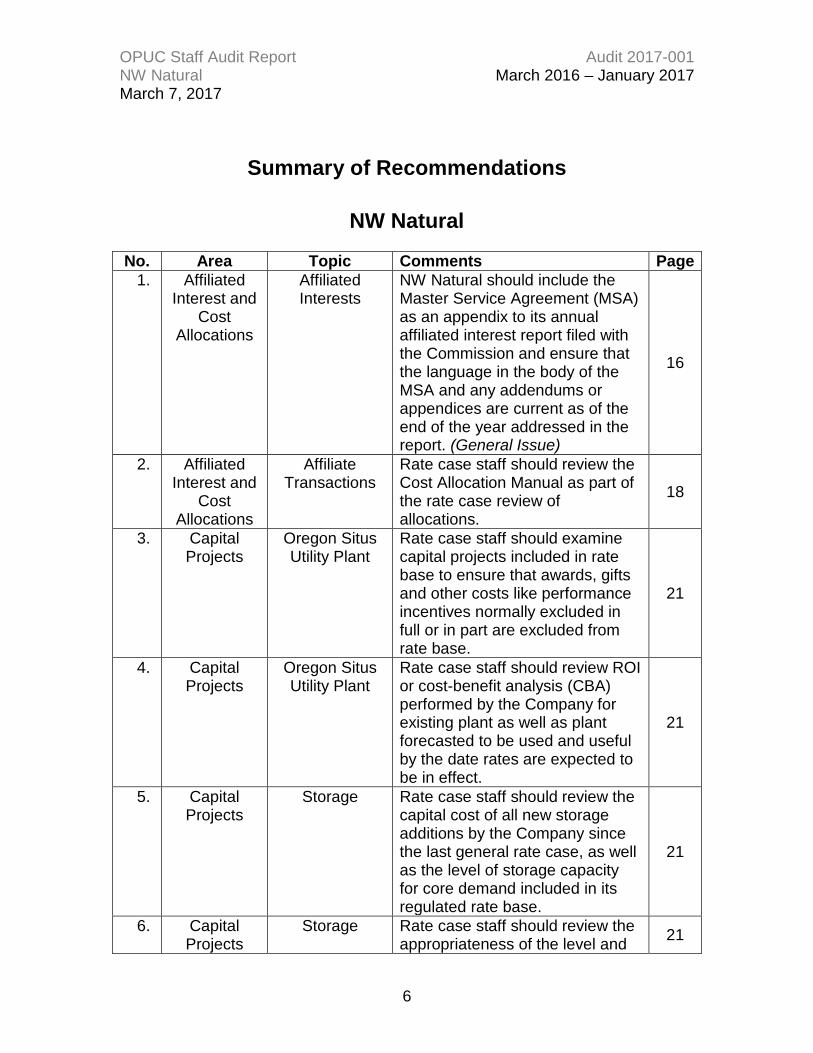

Summary of Recommendations

NW Natural

No. Area Topic Comments Page 1. Affiliated

Interest and Cost

Allocations

Affiliated Interests

NW Natural should include the Master Service Agreement (MSA) as an appendix to its annual affiliated interest report filed with the Commission and ensure that the language in the body of the MSA and any addendums or appendices are current as of the end of the year addressed in the report. (General Issue)

16

2. Affiliated Interest and

Cost Allocations

Affiliate Transactions

Rate case staff should review the Cost Allocation Manual as part of the rate case review of allocations.

18

3. Capital Projects

Oregon Situs Utility Plant

Rate case staff should examine capital projects included in rate base to ensure that awards, gifts and other costs like performance incentives normally excluded in full or in part are excluded from rate base.

21

4. Capital Projects

Oregon Situs Utility Plant

Rate case staff should review ROI or cost-benefit analysis (CBA) performed by the Company for existing plant as well as plant forecasted to be used and useful by the date rates are expected to be in effect.

21

5. Capital Projects

Storage Rate case staff should review the capital cost of all new storage additions by the Company since the last general rate case, as well as the level of storage capacity for core demand included in its regulated rate base.

21

6. Capital Projects

Storage Rate case staff should review the appropriateness of the level and 21

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

7

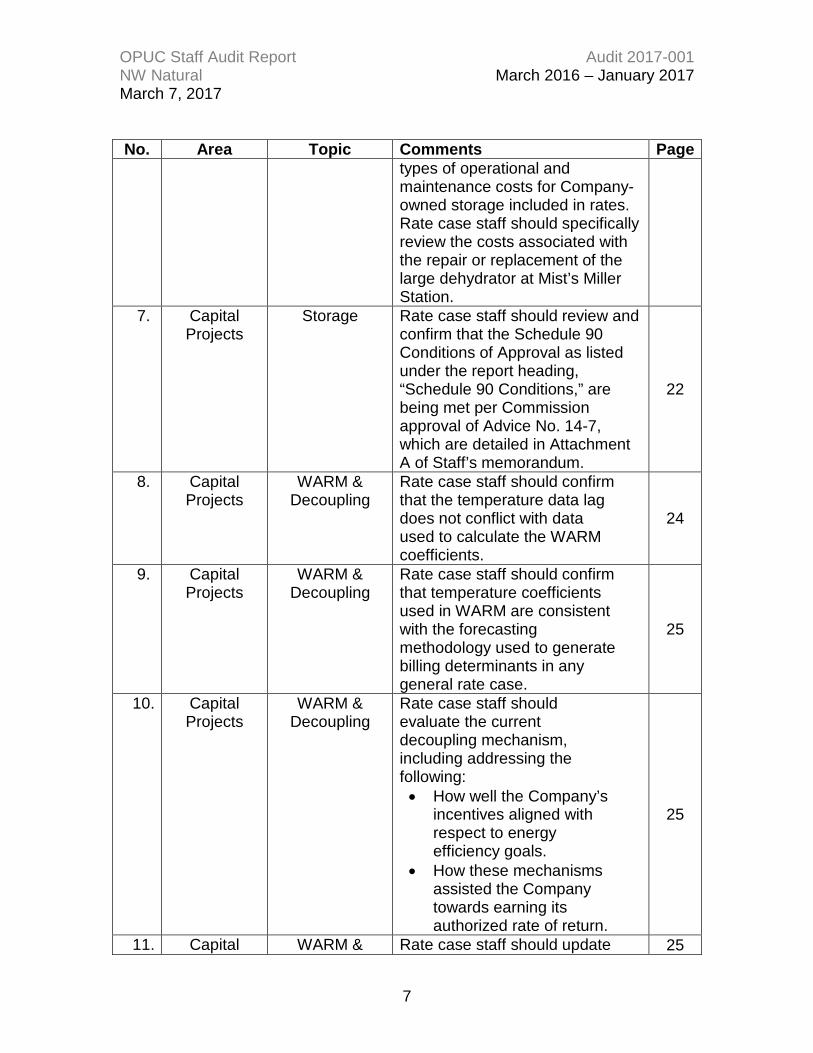

No. Area Topic Comments Page types of operational and maintenance costs for Company-owned storage included in rates. Rate case staff should specifically review the costs associated with the repair or replacement of the large dehydrator at Mist’s Miller Station.

7. Capital Projects

Storage Rate case staff should review and confirm that the Schedule 90 Conditions of Approval as listed under the report heading, “Schedule 90 Conditions,” are being met per Commission approval of Advice No. 14-7, which are detailed in Attachment A of Staff’s memorandum.

22

8. Capital Projects

WARM & Decoupling

Rate case staff should confirm that the temperature data lag does not conflict with data used to calculate the WARM coefficients.

24

9. Capital Projects

WARM & Decoupling

Rate case staff should confirm that temperature coefficients used in WARM are consistent with the forecasting methodology used to generate billing determinants in any general rate case.

25

10. Capital Projects

WARM & Decoupling

Rate case staff should evaluate the current decoupling mechanism, including addressing the following: • How well the Company’s

incentives aligned with respect to energy efficiency goals.

• How these mechanisms assisted the Company towards earning its authorized rate of return.

25

11. Capital WARM & Rate case staff should update 25

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

8

No. Area Topic Comments Page Projects Decoupling the calculation of the baseline

margin used for comparison to arrive at the decoupling adjustment.

12. Capital Projects

WARM & Decoupling

Rate case staff should review the normal weather assumptions used for the test year normalization.

25

13. Capital Projects

WARM & Decoupling

Rate case staff should evaluate all trackers adopted since UG 152, as well as the shifting of risk associated with volatility in sales volumes from NW Natural to its customers.

25

14. Capital Projects

WARM & Decoupling

Rate case staff should evaluate the decoupling status of comparison firms in any cost of capital study.

25

15. Capital Projects

Pipeline Capital Costs

Rate case staff should review all construction and capital costs for current and past proposed pipeline distribution projects.

25

16. Capital Projects

Pipeline Capital Costs

Rate case staff should review all construction and capital costs for current and past proposed low and high pressure pipeline transportation projects.

25

17. Capital Projects

Accounting Rate case staff should audit and review entries made to FERC account 380.

25

18. Capital Projects

Accounting Rate case staff should verify the mapping of SAP accounting entries to ensure they are correct and appropriate.

25

19. Capital Projects

Competitive Bidding

Rate case staff should verify that all pipeline and mains project costs are reasonable, and where competitive bidding processes are used, that the results of bidding are appropriate.

26

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

9

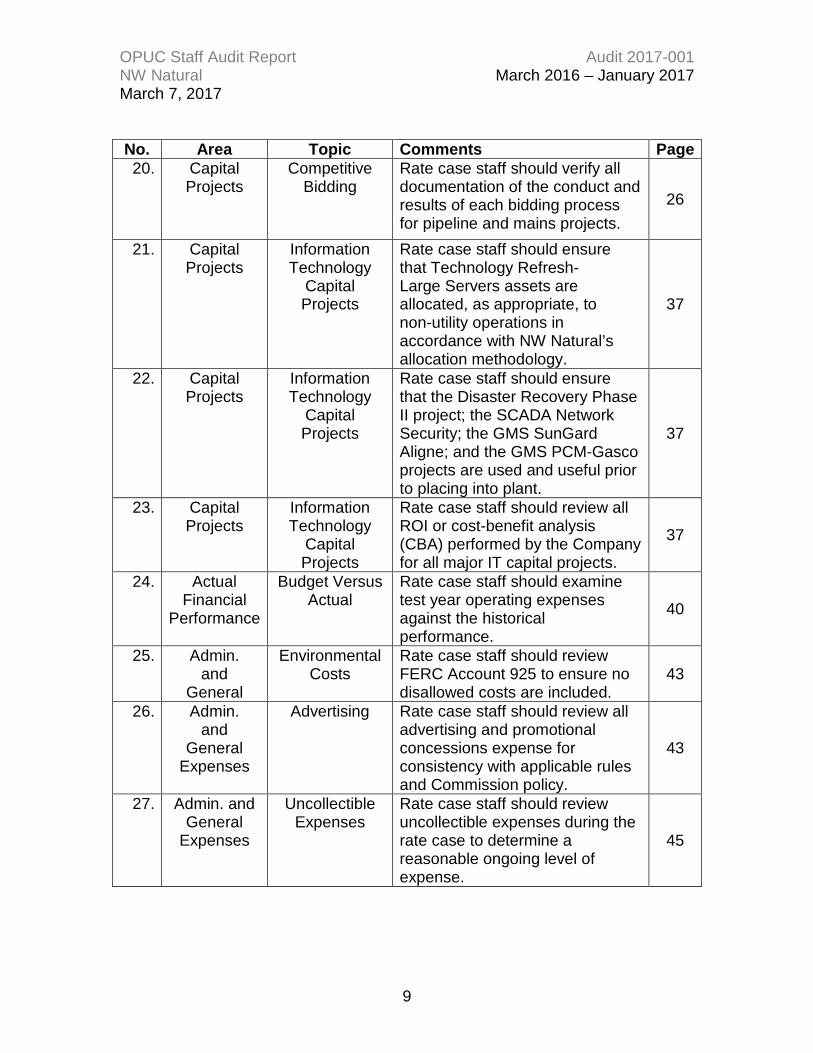

No. Area Topic Comments Page 20. Capital

Projects Competitive

Bidding Rate case staff should verify all documentation of the conduct and results of each bidding process for pipeline and mains projects.

26

21. Capital Projects

Information Technology

Capital Projects

Rate case staff should ensure that Technology Refresh-Large Servers assets are allocated, as appropriate, to non-utility operations in accordance with NW Natural’s allocation methodology.

37

22. Capital Projects

Information Technology

Capital Projects

Rate case staff should ensure that the Disaster Recovery Phase II project; the SCADA Network Security; the GMS SunGard Aligne; and the GMS PCM-Gasco projects are used and useful prior to placing into plant.

37

23. Capital Projects

Information Technology

Capital Projects

Rate case staff should review all ROI or cost-benefit analysis (CBA) performed by the Company for all major IT capital projects.

37

24. Actual Financial

Performance

Budget Versus Actual

Rate case staff should examine test year operating expenses against the historical performance.

40

25. Admin. and

General

Environmental Costs

Rate case staff should review FERC Account 925 to ensure no disallowed costs are included.

43

26. Admin. and

General Expenses

Advertising Rate case staff should review all advertising and promotional concessions expense for consistency with applicable rules and Commission policy.

43

27. Admin. and General

Expenses

Uncollectible Expenses

Rate case staff should review uncollectible expenses during the rate case to determine a reasonable ongoing level of expense.

45

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

10

No. Area Topic Comments Page 28. Admin. and

General Expenses

Insurance Services,

Injuries, and Damages

Rate case staff should review individual insurance policies to determine an appropriate level of insurance expense that should be borne by customers.

46

29. Admin. and General

Expenses

Other A&G Expenses

Rate case staff should review in detail other administrative and general expense to identify non-utility office expenses, meals/travel/entertainment expenses, spousal expenses, political contributions, gifts, catering, etc. that should be removed as rate case adjustments.

46

30. Labor Costs Staffing Rate case staff should review wages and salaries and compare the historical trend in base rates, incentives, and FTE to the test year amounts and determine causal drivers that appear to influence changes in the year over year trend.

48

31. Labor Costs Staffing Rate case staff should review salary studies or labor benchmarking conducted internally by NWN or outside consultants.

48

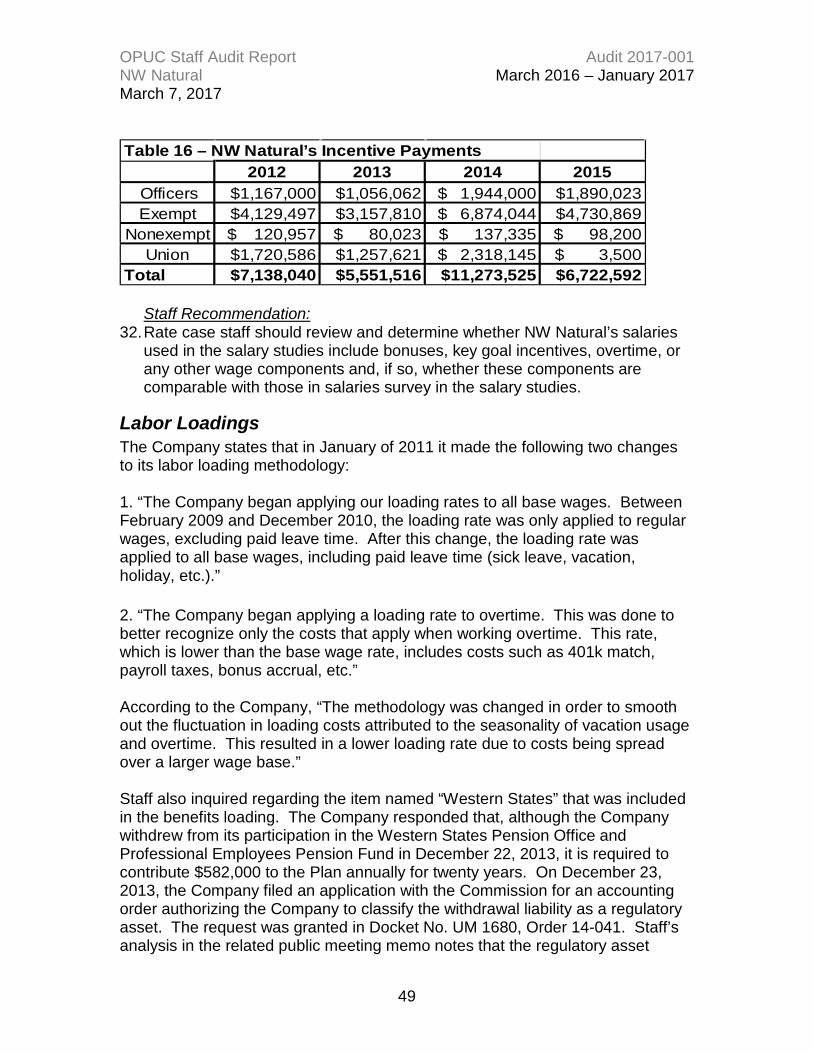

32. Labor Costs Incentive Costs Rate case staff should review and determine whether NWN’s salaries used in the salary studies included bonuses, key goal incentives, overtime or any other wage components, and, if so, whether the components are comparable with the surveys provided in the salary studies.

49

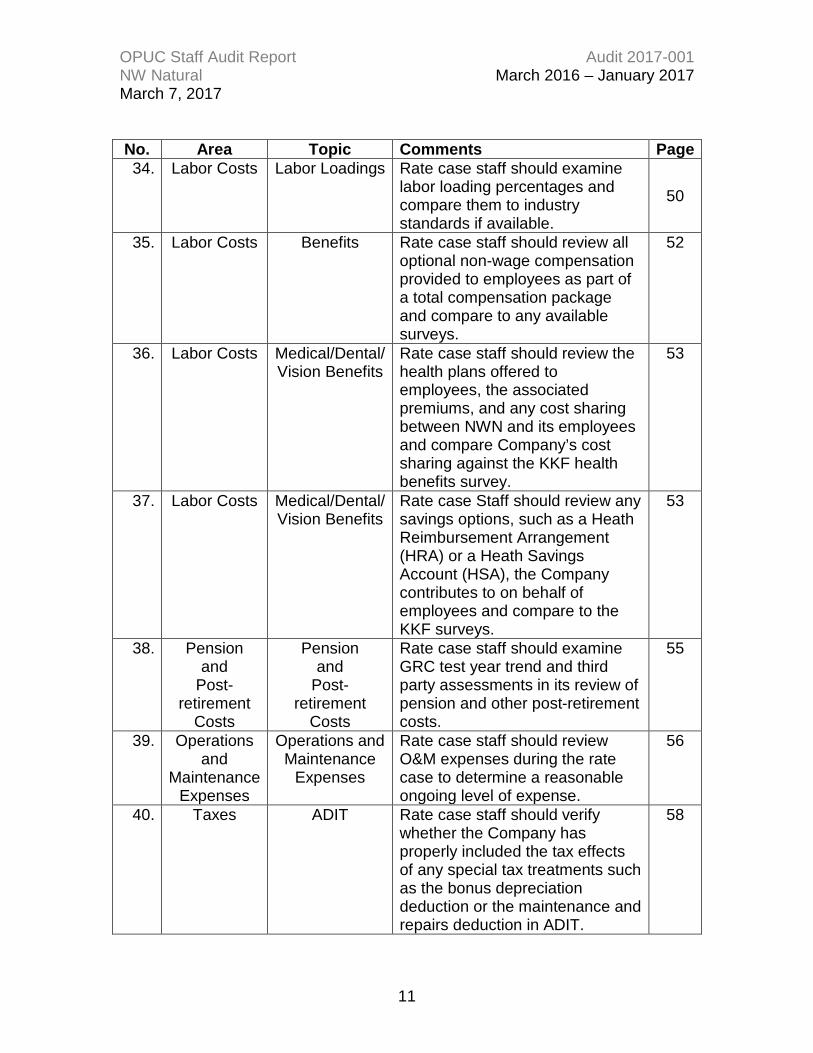

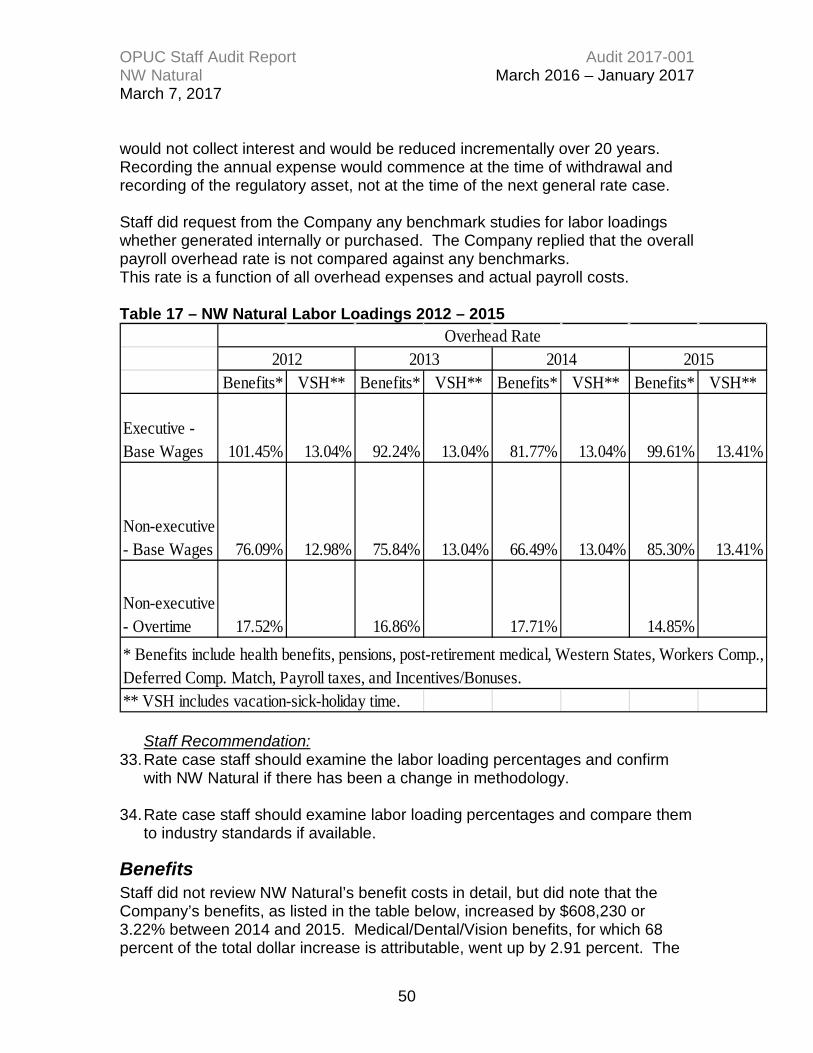

33. Labor Costs Labor Loadings Rate case staff should examine the labor loading percentages and confirm with NWN if there has been a change in methodology.

50

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

11

No. Area Topic Comments Page 34. Labor Costs Labor Loadings Rate case staff should examine

labor loading percentages and compare them to industry standards if available.

50

35. Labor Costs Benefits Rate case staff should review all optional non-wage compensation provided to employees as part of a total compensation package and compare to any available surveys.

52

36. Labor Costs Medical/Dental/ Vision Benefits

Rate case staff should review the health plans offered to employees, the associated premiums, and any cost sharing between NWN and its employees and compare Company’s cost sharing against the KKF health benefits survey.

53

37. Labor Costs Medical/Dental/ Vision Benefits

Rate case Staff should review any savings options, such as a Heath Reimbursement Arrangement (HRA) or a Heath Savings Account (HSA), the Company contributes to on behalf of employees and compare to the KKF surveys.

53

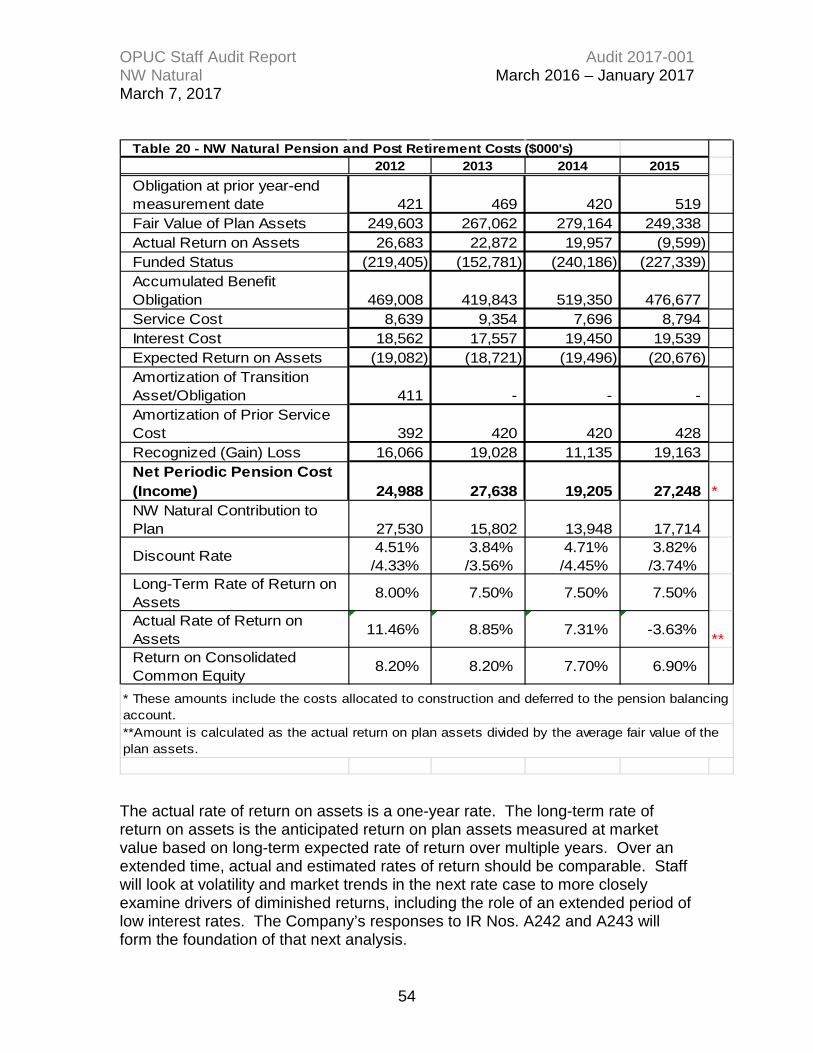

38. Pension and

Post- retirement

Costs

Pension and

Post- retirement

Costs

Rate case staff should examine GRC test year trend and third party assessments in its review of pension and other post-retirement costs.

55

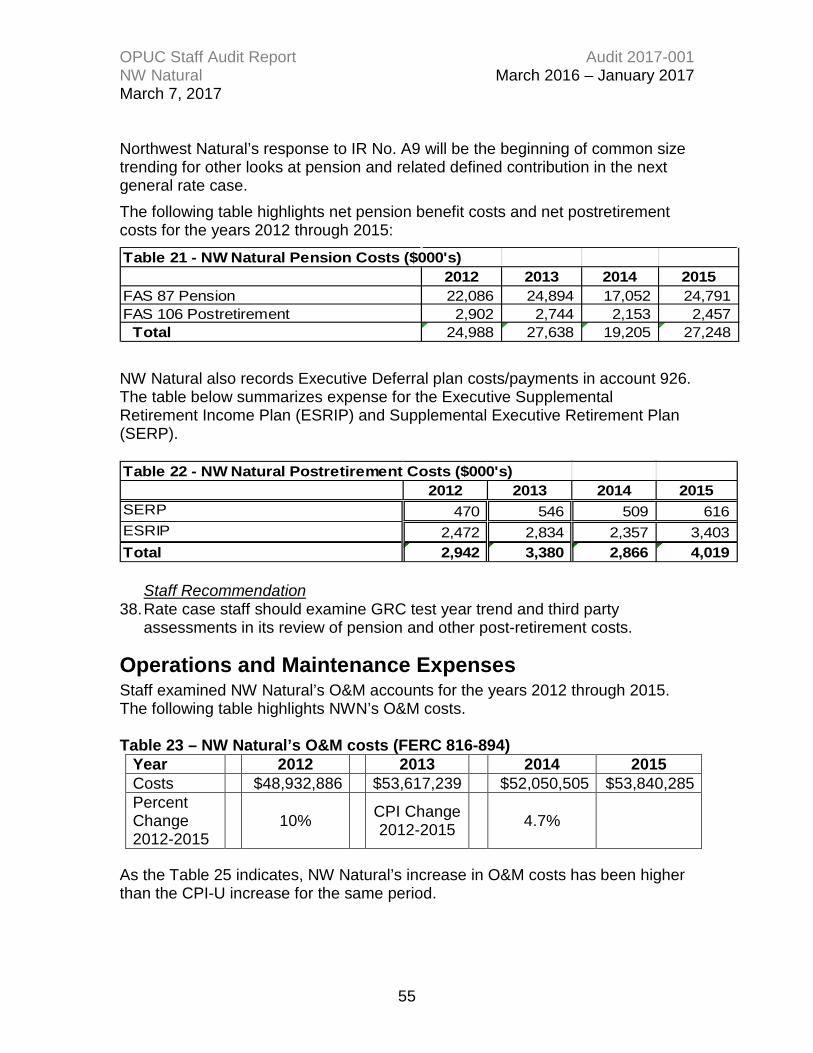

39. Operations and

Maintenance Expenses

Operations and Maintenance

Expenses

Rate case staff should review O&M expenses during the rate case to determine a reasonable ongoing level of expense.

56

40. Taxes ADIT Rate case staff should verify whether the Company has properly included the tax effects of any special tax treatments such as the bonus depreciation deduction or the maintenance and repairs deduction in ADIT.

58

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

12

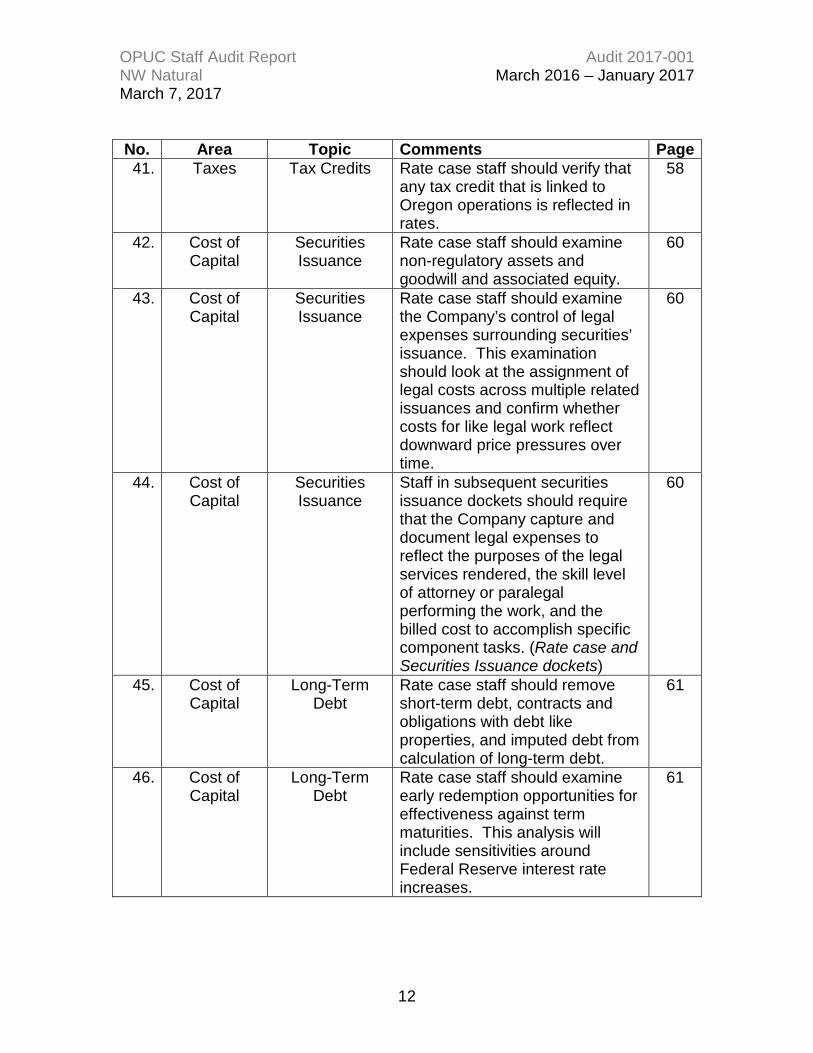

No. Area Topic Comments Page 41. Taxes Tax Credits Rate case staff should verify that

any tax credit that is linked to Oregon operations is reflected in rates.

58

42. Cost of Capital

Securities Issuance

Rate case staff should examine non-regulatory assets and goodwill and associated equity.

60

43. Cost of Capital

Securities Issuance

Rate case staff should examine the Company’s control of legal expenses surrounding securities’ issuance. This examination should look at the assignment of legal costs across multiple related issuances and confirm whether costs for like legal work reflect downward price pressures over time.

60

44. Cost of Capital

Securities Issuance

Staff in subsequent securities issuance dockets should require that the Company capture and document legal expenses to reflect the purposes of the legal services rendered, the skill level of attorney or paralegal performing the work, and the billed cost to accomplish specific component tasks. (Rate case and Securities Issuance dockets)

60

45. Cost of Capital

Long-Term Debt

Rate case staff should remove short-term debt, contracts and obligations with debt like properties, and imputed debt from calculation of long-term debt.

61

46. Cost of Capital

Long-Term Debt

Rate case staff should examine early redemption opportunities for effectiveness against term maturities. This analysis will include sensitivities around Federal Reserve interest rate increases.

61

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

13

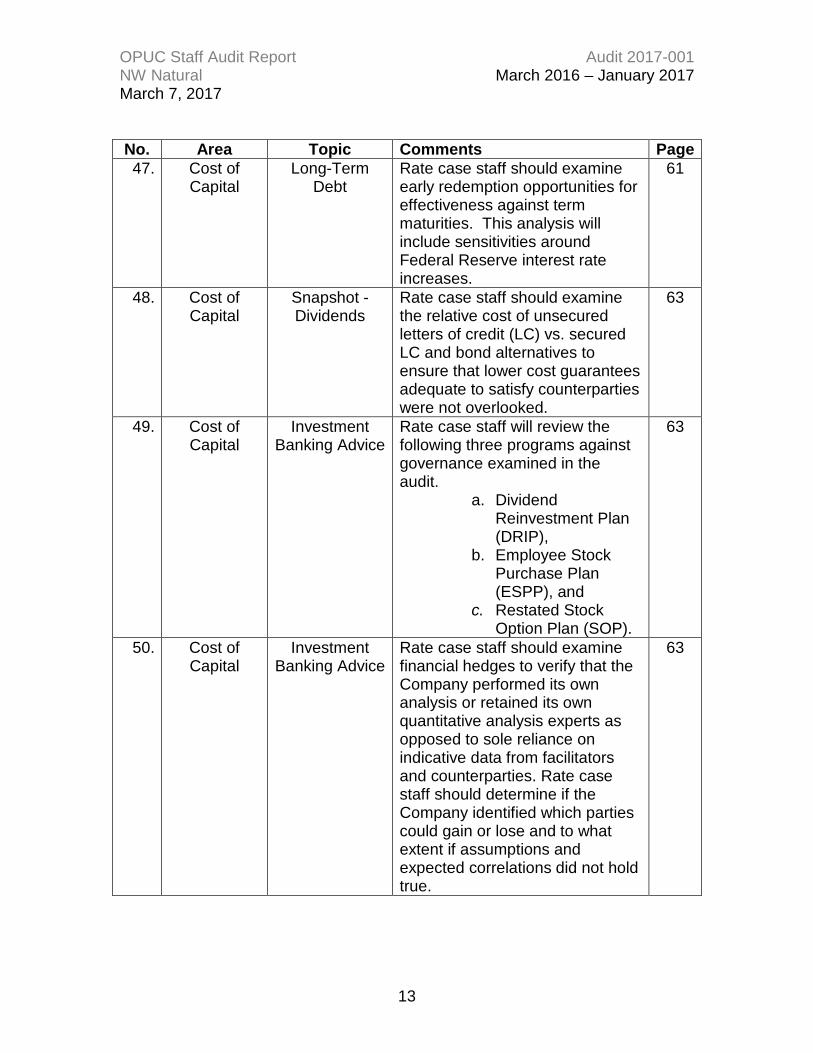

No. Area Topic Comments Page 47. Cost of

Capital Long-Term

Debt Rate case staff should examine early redemption opportunities for effectiveness against term maturities. This analysis will include sensitivities around Federal Reserve interest rate increases.

61

48. Cost of Capital

Snapshot - Dividends

Rate case staff should examine the relative cost of unsecured letters of credit (LC) vs. secured LC and bond alternatives to ensure that lower cost guarantees adequate to satisfy counterparties were not overlooked.

63

49. Cost of Capital

Investment Banking Advice

Rate case staff will review the following three programs against governance examined in the audit.

a. Dividend Reinvestment Plan (DRIP),

b. Employee Stock Purchase Plan (ESPP), and

c. Restated Stock Option Plan (SOP).

63

50. Cost of Capital

Investment Banking Advice

Rate case staff should examine financial hedges to verify that the Company performed its own analysis or retained its own quantitative analysis experts as opposed to sole reliance on indicative data from facilitators and counterparties. Rate case staff should determine if the Company identified which parties could gain or lose and to what extent if assumptions and expected correlations did not hold true.

63

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

14

Company Background and Organization Founded in 1859, Northwest Natural Gas Company, dba NW Natural, is a local gas distribution company based in Oregon and Washington. NW Natural is headquartered in Portland, Oregon. At year-end 2015, NW Natural had approximately 714,000 utility customers in Oregon and southwest Washington, including the Portland-Vancouver metropolitan area, the Willamette Valley, the Oregon coast, and the Columbia River Gorge. NW Natural serves a wide array of industries including but not limited to, pulp, paper, and other forest products processors; food processors; agriculture; government and educational institutions; and electric generation. NW Natural meets the expected needs of its core utility customers through natural gas purchases from a variety of suppliers in the western United States and Canada. The Company also operates an underground storage facility and contracts for additional gas storage outside its service territory. NW Natural operates two liquefied natural gas plants in its service area. The Company also provides gas storage services to other energy companies in the Northwest interstate market. In addition, NW Natural has contracts with an electric generator and two industrial customers that provide recallable capacity transportation.

Affiliated Interest and Cost Allocations

Affiliated Interests The following is a brief description of NW Natural’s affiliated entities based on the Company’s 2015 Annual Affiliated Interests Report filed with the Commission. These entities are affiliated interests of the Company, as defined by ORS 757.015, because each has two or more officers or directors in common with the Company, or they meet the ownership requirements of 5 percent direct or indirect ownership. NNG Financial Corporation (NNGFC) is a wholly owned subsidiary of NW Natural created in 1984. NNGFC owns 100 percent of the stock of KB Pipeline Company. NNGFC is also a limited partner in a low-income housing project located in Portland, Oregon. NNGFC’s ownership interest in this project is 49.5 percent. KB Pipeline Company (KBPC) is a wholly owned subsidiary of NNGFC created in 1991. KBPC owns a 10 percent interest in, and is the former operator of, an interstate natural gas pipeline known as the Kelso-Beaver Pipeline. KBPC has

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

15

no separate employees of its own; it uses employees shared with Northwest Natural, as approved by FERC in July 2004. Northwest Energy Corporation (NWEC) is a wholly owned subsidiary of NW Natural created in 2001. It was formed to serve as the holding company for Northwest Natural and PGE in the event NWN’s proposed acquisition of PGE had been completed. NWN terminated the acquisition process in May 2002 and the corporation remained dormant until 2013. Since 2013, NW Energy Corp has served as the holding company for NWN Gas Reserves LLC. Northwest Energy Sub Corporation (NWESC) is a wholly owned subsidiary of NWEC created in 2001. It was formed to effect the corporate reorganization of the proposed acquisition mentioned in the preceding paragraph. The corporation has remained dormant since its foundation. There were no affiliated transactions between NW Natural and NWESC in 2015. NWN Gas Reserves LLC (NWN Gas Reserves) is a wholly owned subsidiary of Northwest Energy Corporation formed in December 2012. In March 2013, NWN's transferred its working interest in the Jonah Field to this entity.

The agreements related to the working interest were amended in 2014 to facilitate Encana Oil & Gas (USA) Inc.'s sale of its interest in the Jonah Field to an affiliate of TPG Capital. The agreements related to the working interest were again amended in 2016 to further clarify the terms related to additional well development and capital expenditures. Northwest Biogas, LLC (NWB) is partly owned by NWN. NWN owns a 50 percent membership interest in NW Biogas and serves as the Managing Member. The other 50 percent membership interest is owned by BEF Renewable Incorporated. NW Biogas developed and operates a demonstration biodigester located at Three Mile Canyon Farms in Boardman, Oregon. NW Natural Gas Storage, LLC (NWN Gas Storage) is a wholly owned subsidiary of NW Natural formed in 2009. NWN Gas Storage owns and manages non-utility gas storage interests. BL Credit Holdings, LLC (BLCH) is a wholly owned subsidiary of TWP. There were no affiliated transactions between the Company and BLCH in 2015. Gill Ranch Storage, LLC (GRS) is a wholly owned subsidiary of NW Natural created in 2007. Effective March 7, 2007, the Company assigned all of its membership interest in GRS to NW Natural Energy, LLC. NW Natural Energy,

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

16

LLC, subsequently assigned all of its membership interest in GRS to NW Natural Gas Storage, LLC. GRS entered into a Joint Project Agreement with Pacific Gas & Electric Company (PG&E) in 2007 for the co-development of an underground natural gas storage facility near Fresno, California. GRS has a 75 percent undivided ownership interest in the project and is the project operator. NW Natural Energy, LLC (NWNE) is a wholly owned subsidiary of Northwest Natural Gas Company created in 2009. It was formed to own NW Natural Gas Storage, LLC, and other non-utility businesses. Trail West Holdings, LLC (TWH) is owned by NW Natural Energy, LLC ("NWN Energy") and TransCanada American Investment Ltd. ("TAIL"), with each owning a 50 percent membership interest. TWH wholly owns Trail West Pipeline, LLC (TWP), which is developing the cross-Cascades natural gas pipeline. See below for description of TWP. Trail West Pipeline (TWP) is a wholly owned subsidiary of TWH, and has been pursuing the development of a proposed FERC-regulated cross-Cascades natural gas pipeline.

Affiliate Transactions Staff reviewed the Company’s 2015 Annual Affiliated Interest Report and comments on the following: Money Pooling The Company does not maintain a cash management (money pooling) arrangement with subsidiaries and affiliates. Master Services Agreement NW Natural’s most recent Affiliated Master Services Agreement (MSA) was approved on February 6, 2009, in OPUC Order No. 09-051. At this time, however, the MSA does not accurately reflect NW Natural’s current affiliates. Staff noted the same in the prior audit and recommended the Company file an addendum to update the list of current affiliates in its MSA within 120 days of this report. During the course of this audit, Staff asked the Company whether it had updated the MSA since February 6, 2009. The Company replied that the MSA remains unchanged since that date.

Staff Recommendation 1. NW Natural should include the MSA as an appendix to its Annual Affiliated

Interest report filed with the Commission and ensure that the language in the body of the MSA and any addendums or appendices are current as of the end of the year addressed in the Report. (General Issue)

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

17

Transactions NW Natural made payments to KB Pipeline Company in 2015 for pipeline demand charges of $224,258 and $12,359 on a total Company and total Oregon basis, respectively. These payments are pursuant to certain FERC regulations and do not require an affiliated interest filing pursuant to OAR 860-027-0040(3)(b)(A). Services rendered by NNG Financial Corporation (NNGFC) Affiliate services payments to the utility in 2015 for insurance, overhead, property taxes, and other administrative expenses totaled $1,289,367. Services provided by NW Natural employees to affiliates or non-utility are direct charged and based on individual time cards with an administrative overhead allocation of 27.5 percent of the direct labor in addition to vacation and holiday overhead and benefits overhead. An administrative overhead charge is likewise added to labor charges from an affiliate to the parent. Affiliates or non-public utility activities are charged directly for materials, supplies, and services purchased by NW Natural on behalf of the affiliate. Intercompany balances between NW Natural and its affiliates are generally paid on a monthly basis. Staff did not note any issues concerning the services payments. Other Payments Tax benefits (Oregon) used by NW Natural from NNG Financial Corporation in 2015 equaled ($16,327). Tax benefits (Oregon) paid by NW Natural to GRS in 2015 equaled $11,291,482. Tax benefits (Oregon) paid by NW Natural to NWN Gas Storage in 2015 equaled $405,792. Tax benefits (Oregon) paid by NW Natural to NWN Energy in 2010 equaled $264,656. Salaries and overhead paid by NW Natural to NWN Gas Storage equaled $180,526. NW Natural files both federal and state income taxes on a consolidated basis and allocates income tax expense or benefit to each affiliate or activity based on the taxable income or loss of the affiliate or activity. Staff did not note any issues concerning the other payments. Cost Allocation Manual The Cost Allocation Manual attached to the 2015 Affiliated Interest Report notes that nine percent of total assets and three percent of gross operating revenues were attributable to non-regulated/non-utility activities. A section-by-section comparison to the Cost Allocation Manual template indicates compliance with the Commission’s requirements concerning the Cost Allocation Manual. Staff also performed a cursory review of the Cost Allocation Manuals included with the 2013 and 2014 Affiliated Interest Reports and noted no extraordinary or unexpected items.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

18

Staff Recommendation

2. Rate case staff should review the Cost Allocation Manual as part of the rate case review of allocations.

Capital Projects

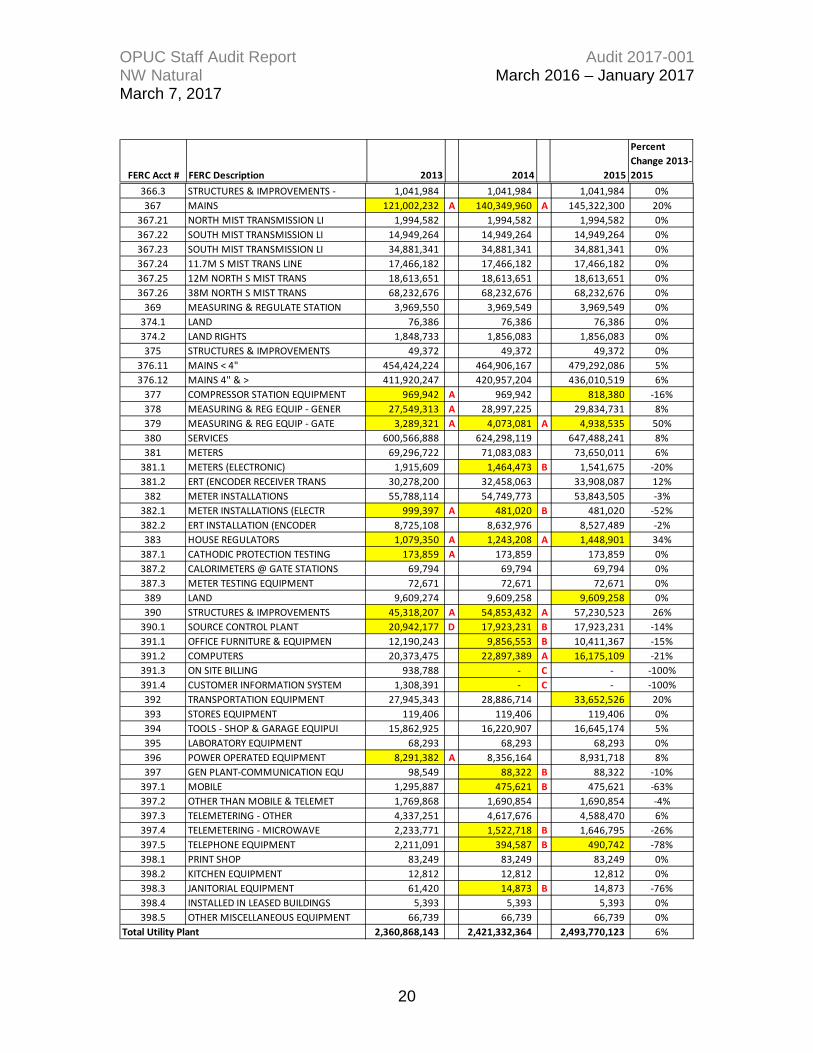

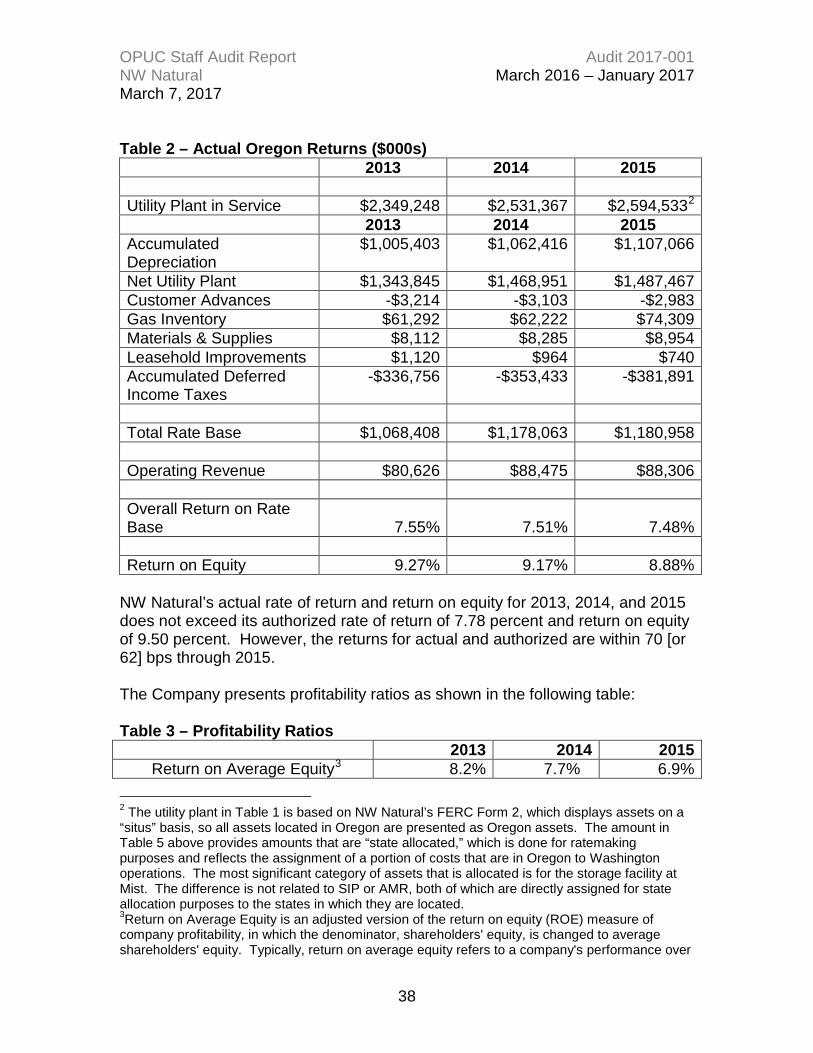

Oregon Allocated and Situs Utility Plant The following table presents the depreciated changes in asset accounts 301 through 399 from 2012 through 2015. Table 1 – Oregon Allocated and Situs Utility Plant Note: Year-to-year account differences over 10 percent are highlighted and are explained below. See notes A, B, and C.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

19

FERC Acct # FERC Description 2013 2014 2015

Percent Change 2013-

2015301 ORGANIZATION 852 852 852 0%302 FRANCHISES & CONSENTS 83,496 83,496 83,496 0%

303.1 COMPUTER SOFTWARE 64,579,309 A 53,335,387 B 56,947,460 -12%303.2 CUSTOMER INFORMATION SYSTEM 30,488,305 30,488,305 30,488,305 0%303.3 INDUSTRIAL & COMMERCIAL BIL 4,146,951 4,146,951 4,146,951 0%303.4 CRMS 2,049,451 A 682,893 B 682,893 -67%304.1 LAND 24,998 24,998 24,998 0%305.5 P P O G STRU & IMPR-OTHER Y 13,156 13,156 13,156 0%318.3 P P O G LIGHT OIL REFINING 144,896 144,896 144,896 0%318.5 P P O G TAR PROCESSING 243,551 243,551 243,551 0%

305.11 GAS PRODUCTION - COTTAGE G 8,320 8,320 8,320 0%305.17 STRUCTURES MIXING STATION 46,587 46,587 46,587 0%311.7 LIQUIFIED GAS EQUIPMENT COO 4,033 4,033 4,033 0%311.8 LIQUIFIED GAS EQUIPMENT LIN 4,209 4,209 4,209 0%319 GAS MIXING EQUIPMENT GASCO 185,448 185,448 185,448 0%

350.1 LAND 106,549 106,549 106,549 0%350.2 RIGHTS-OF-WAY 109,625 109,625 109,625 0%351 STRUCTURES AND IMPROVEMENTS 6,715,064 7,139,428 7,208,245 7%352 WELLS 20,047,076 20,047,076 20,047,076 0%

352.1 STORAGE LEASEHOLD & RIGHTS 3,538,491 3,938,491 A 3,938,491 11%352.2 RESERVOIRS 5,844,618 5,844,618 7,272,553 24%352.3 NON-RECOVERABLE NATURAL GAS 6,440,890 6,440,890 6,440,890 0%353 LINES 6,552,220 6,552,220 6,552,220 0%354 COMPRESSOR STATION EQUIPMENT 29,528,531 29,528,531 31,351,812 6%355 MEASURING / REGULATING EQUIPM 6,700,892 6,700,892 7,159,406 7%356 PURIFICATION EQUIPMENT 297,363 297,363 297,363 0%357 OTHER EQUIPMENT 1,331,924 1,331,924 1,332,029 0%

360.11 LAND - LNG LINNTON 83,598 83,598 83,598 0%360.12 LAND - LNG NEWPORT 536,675 536,675 536,675 0%360.2 LAND - OTHER 106,557 B 106,557 106,557 0%

361.11 STRUCTURES & IMPROVEMENTS 4,540,966 4,540,966 4,594,791 1%361.12 STRUCTURES & IMPROVEMENTS 4,603,395 4,659,407 4,656,739 1%361.2 STRUCTURES & IMPROVEMENTS - 26,757 26,757 26,757 0%

362.11 GAS HOLDERS - LNG LINNTON 2,690,579 2,690,579 2,744,404 2%362.12 GAS HOLDERS - LNG NEWPORT 5,791,956 5,791,956 5,791,956 0%362.2 GAS HOLDERS - LNG OTHER 1,600 1,600 1,600 0%

363.11 LIQUEFACTION EQUIP. - LINN 2,921,964 2,921,686 2,975,510 2%363.12 LIQUEFACTION EQUIP - NEWPO 7,308,111 7,308,111 7,308,111 0%363.21 VAPORIZING EQUIP - LINNTON 2,629,836 2,629,836 2,683,660 2%363.22 VAPORIZING EQUIP - NEWPORT 3,594,015 3,594,015 3,664,362 2%363.31 COMPRESSOR EQUIP - LINNTON 180,903 180,903 180,903 0%363.32 COMPRESSOR EQUIPMENT - NE 300,951 1,390,926 A 1,390,926 362%363.41 MEASURING & REGULATING EQU 737,149 1,091,077 A 1,247,665 69%363.42 MEASURING & REGULATING EQU 113,414 113,414 113,414 0%363.5 CNG REFUELING FACILITIES 1,787,828 3,051,295 A 3,051,295 71%363.6 LNG REFUELING FACILITIES 739,473 739,473 739,473 0%365.1 LAND 89,772 89,772 89,772 0%365.2 LAND RIGHTS 6,455,177 6,455,177 6,455,177 0%

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

20

FERC Acct # FERC Description 2013 2014 2015

Percent Change 2013-2015

366.3 STRUCTURES & IMPROVEMENTS - 1,041,984 1,041,984 1,041,984 0%367 MAINS 121,002,232 A 140,349,960 A 145,322,300 20%

367.21 NORTH MIST TRANSMISSION LI 1,994,582 1,994,582 1,994,582 0%367.22 SOUTH MIST TRANSMISSION LI 14,949,264 14,949,264 14,949,264 0%367.23 SOUTH MIST TRANSMISSION LI 34,881,341 34,881,341 34,881,341 0%367.24 11.7M S MIST TRANS LINE 17,466,182 17,466,182 17,466,182 0%367.25 12M NORTH S MIST TRANS 18,613,651 18,613,651 18,613,651 0%367.26 38M NORTH S MIST TRANS 68,232,676 68,232,676 68,232,676 0%

369 MEASURING & REGULATE STATION 3,969,550 3,969,549 3,969,549 0%374.1 LAND 76,386 76,386 76,386 0%374.2 LAND RIGHTS 1,848,733 1,856,083 1,856,083 0%375 STRUCTURES & IMPROVEMENTS 49,372 49,372 49,372 0%

376.11 MAINS < 4" 454,424,224 464,906,167 479,292,086 5%376.12 MAINS 4" & > 411,920,247 420,957,204 436,010,519 6%

377 COMPRESSOR STATION EQUIPMENT 969,942 A 969,942 818,380 -16%378 MEASURING & REG EQUIP - GENER 27,549,313 A 28,997,225 29,834,731 8%379 MEASURING & REG EQUIP - GATE 3,289,321 A 4,073,081 A 4,938,535 50%380 SERVICES 600,566,888 624,298,119 647,488,241 8%381 METERS 69,296,722 71,083,083 73,650,011 6%

381.1 METERS (ELECTRONIC) 1,915,609 1,464,473 B 1,541,675 -20%381.2 ERT (ENCODER RECEIVER TRANS 30,278,200 32,458,063 33,908,087 12%382 METER INSTALLATIONS 55,788,114 54,749,773 53,843,505 -3%

382.1 METER INSTALLATIONS (ELECTR 999,397 A 481,020 B 481,020 -52%382.2 ERT INSTALLATION (ENCODER 8,725,108 8,632,976 8,527,489 -2%383 HOUSE REGULATORS 1,079,350 A 1,243,208 A 1,448,901 34%

387.1 CATHODIC PROTECTION TESTING 173,859 A 173,859 173,859 0%387.2 CALORIMETERS @ GATE STATIONS 69,794 69,794 69,794 0%387.3 METER TESTING EQUIPMENT 72,671 72,671 72,671 0%389 LAND 9,609,274 9,609,258 9,609,258 0%390 STRUCTURES & IMPROVEMENTS 45,318,207 A 54,853,432 A 57,230,523 26%

390.1 SOURCE CONTROL PLANT 20,942,177 D 17,923,231 B 17,923,231 -14%391.1 OFFICE FURNITURE & EQUIPMEN 12,190,243 9,856,553 B 10,411,367 -15%391.2 COMPUTERS 20,373,475 22,897,389 A 16,175,109 -21%391.3 ON SITE BILLING 938,788 - C - -100%391.4 CUSTOMER INFORMATION SYSTEM 1,308,391 - C - -100%392 TRANSPORTATION EQUIPMENT 27,945,343 28,886,714 33,652,526 20%393 STORES EQUIPMENT 119,406 119,406 119,406 0%394 TOOLS - SHOP & GARAGE EQUIPUI 15,862,925 16,220,907 16,645,174 5%395 LABORATORY EQUIPMENT 68,293 68,293 68,293 0%396 POWER OPERATED EQUIPMENT 8,291,382 A 8,356,164 8,931,718 8%397 GEN PLANT-COMMUNICATION EQU 98,549 88,322 B 88,322 -10%

397.1 MOBILE 1,295,887 475,621 B 475,621 -63%397.2 OTHER THAN MOBILE & TELEMET 1,769,868 1,690,854 1,690,854 -4%397.3 TELEMETERING - OTHER 4,337,251 4,617,676 4,588,470 6%397.4 TELEMETERING - MICROWAVE 2,233,771 1,522,718 B 1,646,795 -26%397.5 TELEPHONE EQUIPMENT 2,211,091 394,587 B 490,742 -78%398.1 PRINT SHOP 83,249 83,249 83,249 0%398.2 KITCHEN EQUIPMENT 12,812 12,812 12,812 0%398.3 JANITORIAL EQUIPMENT 61,420 14,873 B 14,873 -76%398.4 INSTALLED IN LEASED BUILDINGS 5,393 5,393 5,393 0%398.5 OTHER MISCELLANEOUS EQUIPMENT 66,739 66,739 66,739 0%

Total Utility Plant 2,360,868,143 2,421,332,364 2,493,770,123 6%

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

21

Notes: A Plant additions to FERC Account B Plant retirements in FERC Account C Assets in FERC Account were fully retired As noted from the table above, plant in service has increased at an average rate of three percent a year over the past two years. Staff reviewed the Company’s Capital Asset Policy and did not have any concerns on how the Company capitalizes assets.

Staff Recommendation: 3. Rate case Staff should examine capital projects included in rate base to

ensure entertainment, awards, and other costs such as performance incentives normally disallowed in full or in part are excluded from rate base.

4. Rate case staff should review ROI or cost-benefit analyses (CBA) performed

by the Company for existing plant as well as plant forecasted to be used and useful by the date rates are expected to be in effect.

System Integrity Programs NW Natural’s System Integrity Program (SIP) Investments last appeared in the 2014 PGA. There were no SIP investments in the 2015 PGA. Staff, NW Natural, the Citizens’ Utility Board of Oregon (CUB), and Northwest Industrial Gas Users (NWIGU) participated in Docket No. UM 1722, which investigated gas utility safety programs and how to fund them. A Stipulation resolving issues raised in Docket No. UM 1722 has been submitted to the Commission and is under advisement.

Storage Staff reviewed NW Natural’s storage. NWN utilizes four different storage facilities in its current resource stack including, Mist (underground storage), Jackson Prairie (underground storage), Gasco (Liquefied natural gas (LNG) storage), and Newport (LNG storage). Mist underground storage is the Company’s largest storage resource, and it is located on the Company’s system. Staff’s recommendations are as follows.

Staff Recommendations: 5. Rate case staff should review the capital cost of all new storage additions by

the Company since the last general rate case, as well as the level of storage capacity for core demand included in its regulated rate base.

6. Rate case staff should review the appropriateness of the level and types of operational and maintenance costs for Company-owned storage included in

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

22

rates. Rate case staff should specifically review the costs associated with the repair or replacement of the large dehydrator at Mist’s Miller Station.

7. Rate case staff should review whether the following Schedule 90 Conditions of Approval are being met per Commission approval of Advice No. 14-7, which are detailed in Attachment A of Staff’s memorandum and included below for reference.

Schedule 90 Conditions of Approval Cost Recovery 1. As an overarching principle, NWN is committed that all direct

and indirect costs incurred by the Company to provide Schedule 90 service will be allocated to and recovered from Schedule 90 customers. NWN agrees to work collaboratively with the parties and to be subject to future processes for Staff and stakeholder review of accounting entries and supporting documentation to ensure an appropriate cost allocation.

2. The costs of any utility personnel that work on the planning and

construction of the non-Core Mist Storage for the provision of RS 90 service will be charged to the RS 90 customers as provided in the customer’s agreement. (With respect to PGE, NWN and PGE have agreed to implement this commitment through allocating such costs to PGE as capital. NWN agrees that there will be a credit provided to core customers to offset the costs that would otherwise be in rates, but which are allocated to PGE. NWN will seek to pass that credit through to customers as a one-time credit when the project goes into service, subject to gaining any necessary approvals of the Commission required to affect the credit).

3. In the event that NWN and the applicable Schedule 90 customer

determine that, after Schedule 90 service is initiated, utility resources will be used in any way to provide ongoing service to that Schedule 90 customer, NWN will develop a shared services-type agreement that allocates utility costs to the Schedule 90 customer. NWN commits to providing an opportunity for stakeholders to review and comment on such agreement and raise any concerns to the Commission prior to effectiveness of such services-type agreement.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

23

4. NWN will further clarify the costs that will be recoverable from Schedule 90 customers under the general rate formula contained in the service agreement. Specifically, NWN confirms that operation and maintenance activities such as accounting, financial reporting, customer service, communications and monitoring, control room services and general management are included. NWN is currently working with PGE on an amendment to the service agreement that would capture these elements, and NWN will add them to the generic service agreement filed with the Commission as part of its original filing on Schedule 90.

Core Customer Interests in Assets Used to Provide Schedule 90 Service 5. NWN will make appropriate provisions to compensate non-

Schedule 90 customers for any use of assets for which they have paid in providing Schedule 90 service. (With respect to PGE’s Schedule 90 service, which will be provided through a development of the Adams Pool at North Mist, NWN has confirmed that all costs associated with the Adams Pool have remained in “Construction Work in Progress,” and have not affected rates, with one exception. The one exception is that recoverable gas costs associated with the pool have been included in inventories for general customers, included in rate base, and expensed over time at a calendar Weighted Average Cost of Gas or other average-cost rate as used by customers. NWN proposes to negotiate with PGE for PGE’s purchase of any remaining recoverable gas at market prices taking into account the quality and location of the gas, and credit general customers as though it was a sale of a rate base item).

6. NWN will continue, through its IRP process, to refine cost estimates, timing, and least-cost planning related to any future expansion of North Mist reservoirs, other than the Adams reservoir, for non-Schedule 90 customers. NWN recognizes that the Staff and stakeholders retain all of their rights to participate in that process and determine their positions on the issues surrounding future expansion of North Mist for non-Schedule 90 customers, and NWN commits to work collaboratively on those issues.

7. NWN commits that in any future proceeding regarding the review for prudence of any expansion or proposed expansion of Mist for non-Schedule 90 customers, it will provide access to

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

24

information that is required to perform an analysis of the costs that would have been associated with developing the Adams Pool for non-Schedule 90 customers versus the costs of any other pool that is ultimately developed for non-Schedule 90 customers.

NWN’s determinations related to the use of the Adams Pool may be raised by any party as an issue during the future prudence review related to any expansion or proposed expansion of Mist for non-Schedule 90 customers. All parties would reserve their rights to take any position in that future proceeding with respect to any such issues raised, including the relevance of the other parties’ arguments.

WARM & Decoupling During and after the 2014-2015 heating season, the OPUC experienced elevated customer complaints regarding NW Natural’s Weather Adjusted Rate Mechanism (WARM) Program. As a result, at the September 8, 2015 Public Meeting, the Commission opened an investigation into WARM, docketed as UM 1750. Parties to the docket entered into a stipulation to implement several modifications to the WARM Program that would reduce adverse customer impacts in the future. The WARM investigation was concluded on June 20, 2016, with Commission Order No. 16-223 adopting the parties’ stipulation with agreed-to WARM Program modifications. NW Natural filed an updated tariff in compliance with Order 16-223. NW Natural has also asked to defer certain WARM-related expenses as contemplated in Order No. 16-223. This request for deferral was filed on September 19, 2016, and is being addressed in Docket No. UM 1798. During the investigation into the WARM Program mentioned above, Staff noted that NW Natural’s billing system incorporates a one-day time lag when recording temperatures. Temperature data is used to estimate the heat response coefficients used in the WARM tariff and in the actual WARM adjustments made to customer bills. Staff includes recommendations in this audit report for staff to review, in the next general rate proceeding, the effect of this lag as well as other aspects of the WARM Program.

Staff Recommendations:

8. Rate case staff should confirm that the temperature data lag does not conflict with data used to calculate the WARM coefficients.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

25

9. Rate case staff should confirm that temperature coefficients used in WARM are consistent with the forecasting methodology used to generate billing determinants in any general rate case.

10. Rate case staff should evaluate the current decoupling mechanism, including

addressing the following:

• How well the Company’s incentives are aligned to energy efficiency goals.

• How these mechanisms assisted the Company with respect to earning its authorized rate of return.

11. Rate case staff should update the calculation of the baseline margin used for

comparison to arrive at the decoupling adjustment.

12. Rate case staff should review the normal weather assumptions used for the test year normalization.

13. Rate case staff should evaluate all trackers adopted since UG 152, as well as the shifting of risk associated with volatility in sales volumes from NW Natural to its customers.

14. Rate case Staff should evaluate the decoupling status of comparison firms in

any cost of capital study.

Pipeline Capital Costs Staff Recommendations:

15. Rate case staff should review all construction and capital costs for current and past proposed pipeline distribution projects.

16. Rate case staff should review all construction and capital costs for current and past proposed low and high pressure transmission pipeline projects.

Accounting Staff Recommendations:

17. Rate case staff should audit and review entries made in FERC account 380.

18. Rate case staff should verify the mapping of SAP accounting entries to ensure they are correct and appropriate.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

26

Competitive Bidding Staff Recommendations:

19. Rate case staff should verify all major pipeline and mains project costs are reasonable, and where competitive bidding processes are used, that the results of the bidding are appropriate.

20. Rate case staff should verify all documentation of the conduct and results of each bidding process for pipeline and mains projects.

Information Technology Capital Projects The following fifteen Information Technology capital projects (expected total project cost greater than $500,000) are currently being implemented by the Company. The information below was provided by NW Natural in response to Staff Information Request No. 168. In part e. of IR No. 168, Staff requested a summary of the return on investment (ROI) studies performed. The Company responded that no (ROI) studies were performed for any of the listed projects. Instead the Company provided a short explanation justifying each project.

I-Series Recovery Project a. Purpose: Purchase of a new production hardware system for CIS at

headquarters, and equivalent for our backup site in Sherwood. NWN will use its previous production system as a hot standby unit at headquarters. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed because of a need for a disaster and business continuity environment that could handle the full load of restored business operations in the event of a critical outage of the production systems.

b. Capability Gained: Increased failover capabilities and reduction of downtime.

c. System Replaced: The Power 6 system in Sherwood, which was beyond the end of life.

d. Anticipated Operational Savings: Reduced equipment maintenance expense.

e. Project required to enhance business operations resiliency and recovery capabilities.

f. Project Budget: $1,105,710.

g. Primary Customers: All users of CIS and CRMS.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

27

Technology Refresh-Desktops/Laptops and Peripherals a. Purpose: Complete Desktop/Laptop replacements per lease schedules.

Desktops are leased for 4 years and laptops for 3 years (industry standard estimated useful life).

b. Capability Gained: “Technology Refresh” means replacing existing technology assets according to a planned schedule based upon the estimated useful life of the asset and as required to support existing and new business systems. Additional areas of return include:

• Reduction in risk resulting from inability to access critical information due to failure of aging hardware

• Increased user efficiency by providing faster access to essential business information (faster processors, disk, additional bandwidth, etc.)

• Increased quality of service by implementing technologies that enable and enhance collaboration (access to and exchange of electronic information) among employees, customers, and business partners

• Reduction in capital cost and time to implement new business processes by having in place the technologies required to support the new applications

c. System Replaced: 2016 Lease Schedules include replacement of 289 desktops and 89 laptops. The project budget includes funding for refresh of other capital peripherals (monitors and/or printers) only as needed.

d. Anticipated Operational Savings: Reduced equipment maintenance expense.

e. Tech refresh required to reduce maintenance.

f. Project Budget: $696,310.

g. Primary Customers: All Company business systems users.

Technology Refresh-Large Servers/SANs a. Purpose: Acquire and implement hardware/software to expand the

Company’s virtual server farm and storage environment to accommodate the continued growth in data storage requirements of existing systems. Estimated useful life of servers is 5 years (industry standard). Typical use is 3 years as production servers and then they are repurposed as development/test servers. IT strategy continues to be virtualizing all servers when possible.

b. Capability Gained: “Tech Refresh” means replacing existing technology assets according to a planned schedule based upon the estimated useful

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

28

life of the asset and as required to support existing and new business systems. It is key to meeting the Company’s Infrastructure Strategic Objectives:

• Infrastructure is resistant to intrusion as defined by passing penetration tests.

• Processing capacity is available when needed with very few unscheduled outages.

• Critical systems are recoverable within committed business recovery windows.

• 1st Quartile infrastructure support costs – Cost effective and sustainable.

• Infrastructure is responsive to application and company process changes without significant implementation efforts, timeframes or costs.

c. System Replaced: Disk storage equipment in headquarters and our backup site in Sherwood. Also upgraded blade servers used for virtual hosts.

d. Anticipated Operational Savings: Reduced equipment maintenance expense

e. Tech refresh required to reduce maintenance.

f. Project Budget: $610,000.

g. Primary Customers: All Company Business Systems Users.

GMAC Upgrade a. Purpose: Implement new infrastructure and upgraded applications

environment for Gas Control inclusive of the upgraded version of primary SCADA control and monitoring application, upgraded associated software, communication drivers, upgraded database environments, enhanced security, and optimized architecture. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed because of the fact that our present system was approaching its end of supportability and the application ecosystem also needed cybersecurity enhancements to secure the validity of data being consumed and monitored by our gas control function.

b. Capability Gained: The current version of SCADA system runs on the operating systems that are end of support in 2015. Upgrading to the current version of system will ensure continued support from the vendor and allow NW Natural to incorporate product improvements and new capabilities. Moving to current versions of operating systems, applications, and databases will facilitate NW Natural’s SCADA security

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

29

initiatives including patching. The project will also provide greater SCADA system resilience with local high availability and significant improvements to our disaster recovery.

c. System replaced: None (product/system lifecycle upgrade).

d. Anticipated Operations Savings: Not applicable (product/system lifecycle upgrade).

e. This project is required as product/system lifecycle upgrade.

f. Project Budget: $1,620,450.

g. Primary Customers: NW Natural Gas Control and Operations.

Customer Order Management a. Purpose: Implement a comprehensive system that will provide end to end

functionality for customer relationship management (CRM), configuring / pricing / quoting (CPQ) and order management (OM). This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed because of the fact that it will reduce reliance on manual processing and provide system flexibility to support customer delivery process improvements

b. Capability Gained: The benefits of the project include greater effectiveness and the ability to redirect staff time to higher value work. The increases in efficiency and productivity are of prime importance given growing capacity constraints of current staff. As the market rebounds and the market demands shift to a more complex work mix, current staffing levels are not sufficient to address manual, time-intensive processes caused by system work- arounds and lack of functionality and flexibility. NWN cannot adapt fast enough to changing customer demands to effectively serve the market (e.g. multifamily, multiple segments and channels in the commercial market, and permitting and moratorium issues). Streamlining processes, adding financial analysis capabilities, automated tracking, interactivity and on-demand reporting for our work streams that involve customers, trade allies, municipalities and prospects will be necessary to achieving our goals efficiently.

c. System replaced: Existing CRMS and Prospector applications and interfaces.

d. Anticipated Operations Savings: While we have not identified specific operational savings, we anticipate efficiencies will be gained through automation of certain current manual processes.

e. Alternatives analysis was performed. Two alternatives were evaluated: 1) Do nothing alternative was evaluated but not pursued. Current

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

30

CRMS/price and quote systems are homegrown systems with many layers from continuous add-ons and updates. Do nothing alternative increases risk when changes are required and limits ability to improve and redesign existing processes without significant changes to the application. 2) Replacement of existing systems with a custom built CRMS and price/quote system was evaluated but not pursued as being more expensive than vendor provided solution.

f. Project Budget: $1,837,178 (preliminary and subject to change).

g. Primary Customers: NW Natural Customer Acquisitions, Industrial Customer Group, Government Relations, NW Natural customers, trade allies.

Enterprise Content Management a. Purpose: The Enterprise Content Management (ECM) Program will

establish the governance framework, business processes and technology platform to effectively manage NW Natural business information throughout its lifecycle in order to protect this asset, reduce the company’s risk and improve employee productivity. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed because it replaces unsupported technology and improves compliance with legal requirements related to company records.

b. Capability Gained: This project is driven by four needs: 1) To improve compliance with legal requirements related to company records including the need to access and deliver records timely to regulatory authorities; 2) To manage the protection and optimization of company assets – i.e., information in a record; 3) To replace/upgrade the company’s legacy records management application – TRIM; 4) To manage a large and growing number of records in various systems.

c. System replaced: TRIM.

d. Anticipated Operations Savings: While we have not identified specific operational savings, NWN anticipate efficiencies will be gained through automation of certain current manual processes.

e. Alternatives analysis was performed. Two alternatives were evaluated: 1) Do nothing alternative was evaluated but not pursued as viable. Current system is not supported or upgradable by the vendor. 2) Replace TRIM only alternative was evaluated but not pursued as TRIM only manages a subset of company records.

f. Project Budget: $2,250,087 (preliminary and subject to change).

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

31

g. Primary Customers: All NW Natural employees.

PCAD Upgrade a. Purpose: Upgrade NW Natural work management system to the new

version includes upgrades of operating system and database. The project also includes extensive training of all field employees on the new application. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed because of the fact that our present system has not been upgraded since it went live in 2008 and the new version provides significant supportability and business benefits.

b. Capability Gained: The upgrade will ensure that the application as well as its operating system and database remain supported by the vendors to allow for break fixes and enhancements. The upgrade will provide more flexibility for IT department to make application changes in response to business needs. New version of the application includes functionality that will create a platform to support our business needs for many years in the future. Examples of this functionality include: simplified/more initiative user interface; graphical dispatch; improvements in work levelling algorithms; and many more.

c. System replaced: None (product/system lifecycle upgrade).

d. Anticipated Operations Savings: Not applicable (product/system lifecycle upgrade).

e. This project is product/system lifecycle upgrade.

f. Project Budget: $1,581,594.

g. Primary Customers: NW Natural Resource Management Center and Operations.

SAP Upgrade – Phase II a. Purpose: Upgrade all applications in the SAP environment. This project

was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed as a product/system lifecycle upgrade.

b. Capability Gained: An SAP upgrade is needed to obtain additional functionality and keep our existing system up-to-date in terms of security and patches. We are currently three enhancement packs behind in our SAP environment and GRC and Solution manager are no longer supported by SAP. The upgrade is also a prerequisite to certain projects that NW Natural is considering for 2017 and beyond such as asset management and risk and land application replacement.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

32

c. System replaced: None (product / system lifecycle upgrade).

d. Anticipated Operations Savings: Not applicable (product / system lifecycle upgrade).

e. This project is required as product/system lifecycle upgrade.

f. Project Budget: $512,533.

g. Primary Customers: All NW Natural employees.

J5 Implementation a. Purpose: This project is the first phase of the Control Room Management

(CRM) Integration program and addresses logbook functionality, shift change process, and change management workflows for Gas Control. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed because of the fact that supports our regulatory compliance need.

b. Capability Gained: This project will greatly enhance Gas Control situational awareness and change management capabilities which will improve NW Natural CRM compliance with CRM regulations (49 CFR 192.631). Capabilities gained include:

1) Enhance situational awareness for Gas Control Operators.

2) Improve Controller’s ability to electronically record information and events.

3) Enhanced reporting on operational information involving all aspects of management of change.

4) Improved shift change process.

5) Improved work tracking and work management.

c. System replaced: None.

d. Anticipated Operations Savings: Not applicable.

e. This project supports regulatory compliance need.

f. Project Budget: $560,000 (preliminary and subject to change).

g. Primary Customers: NW Natural Gas Control and Operations.

Voice Radio Operations Improvement (VROI) – Phase II a. Purpose: Voice Radio Operations Improvement (VROI) project phase two

integrates a radio console and radio network technical refresh with business operational radio standard operating procedures (SOPs). This

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

33

phase combines system modifications with improved operational protocols for business continuity, emergency operations, incident response and routine business communications. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed to improve radio communication functionality and operations.

b. Capability gained or enhanced: Upgraded business voice radio consoles and DR radio capability supporting emergency operations and business continuity. NW Natural’s voice radio network is highly One Pacific Square (“OPS”) centric. If the connection with OPS is lost, communications to trucks, (or dispatch to field) would significantly impair radio communications. The voice radio project Phase I included design and acquisition of software to support converting our traditional single point radio console into a networked topology. In the event of a local DR (OPS is lost), implementation of Voice Radio Phase 2 will provide voice radio console (dispatch) capability at our DR facility, from key NWN business continuity sites, and mobile operation vehicles. Additional benefit of the upgrade is improved connectivity, flexible patching of frequencies, and improved normal business operational use of the voice radio system.

c. System replaced, if applicable: Radio Console technology; Radio infrastructure components.

d. Anticipated operational savings: Not applicable. This project supports a strategic business need for operational resiliency in the event of a disruption in our primary access to system networks.

e. This project replaces end-of-life radio technology to support a business need.

f. Project Budget: $898,148.00.

g. Primary customers, internal or external: All Company employees dispatched for customer support, construction, locates, and services. All Company employees responding in the event of a disaster; external customers able to continue business with Company in the event of a disaster.

Sherwood Microwave Tower a. Purpose: The two Sherwood microwave links will provide communications

resiliency between OPS and the data center and business continuity spaces at the Sherwood site. Additionally, these links will allow NWN to meet the demand for increased bandwidth requirements between OPS and Sherwood on a day-to-day basis. The Tualatin resource center move to the new Sherwood location necessitated the move of the Tualatin to

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

34

Healy Heights microwave link. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed to provide voice, data, and radio communications links with the Sherwood DR facility.

b. Capability gained or enhanced: The Sherwood to Mt Scott microwave link provides redundancy and resiliency for the Sherwood data center and business continuity spaces and supports the requirement for increased bandwidth.

c. System replaced, if applicable: The Sherwood to Healy Heights microwave link replaces the Tualatin to Healy Heights link.

d. Anticipated operational savings: Not applicable.

e. This project supports a strategic business need.

f. Project Budget: $405,689.

g. Primary customers, internal or external: All company employees utilizing applications supported by the Sherwood data center; external customers able to continue business with Company in the event of a disaster.

Eagle Wireless a. Purpose: The Eagle Wireless Upgrade project will convert current Eagle

Advance Automated Meter Reading (AAMR) devices from analog lines to wireless technology (cellular or satellite). The upgrade is necessary due to a recent FCC ruling (FCC ruling 15-14, Feb 2, 2015), allowing telecom providers to move from legacy copper services to IP based networks and services. As telecom providers begin the transition, the Eagle AAMR devices will no longer function appropriately as they are currently utilizing copper legacy phone lines. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed to continue metering service as legacy technology is phased out.

b. Capability gained or enhanced: Moving to a cellular or satellite connection will not only allow NW Natural to maintain connectivity with our customers to receive billing data required by tariff, the advanced technology will increase efficiencies and can reduce outages. Cellular technology is also more scalable, which provides NW Natural more opportunities to meet future technological demands quicker and more effectively. In the event of a local disaster, cellular technology can provide our customers with more flexibility as cellular technology is mobile and is not hardwired.

c. System replaced, if applicable: Analog Eagle AAMR devices.

d. Anticipated operational savings: Not applicable.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

35

e. This project replaces end-of-life technology.

f. Project Budget: $2.3M.

g. Primary customers, internal or external: External, Large Commercial Customers.

Unified Communications – Phase 2 a. Purpose: Technical Refresh of 20 year old Company telecommunications

system and call center technology. The NorTel telephone system was past end-of-life support by the vendor. The Unified Communications and Collaboration (UCC) – Phase 2 project completed the migration of NW Natural’s telephony to a UCC platform and was a continuation of the work completed in Phase 1. This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed to continue telecommunications services as legacy technology is phased out.

b. Capability gained or enhanced: The upgrade ensured that the telephony platform and customer contact center applications as well as operating system and databases remain supported by the vendors to allow for break fixes and enhancements. The new DR architecture and applications included new business functionality coupled with resiliency and redundancy for business and customer service emergency call services. The telephony infrastructure at OPS, NW Natural’s 14 Resource Centers and the 3 storage facilities migrated to the Avaya Voice over Internet Protocol (VoIP) platform and the NorTel switch was removed. Core infrastructure hardware was added at OPS, resource centers, Salem call center, and Sherwood data center. Additionally, the project included the implementation of an Interactive Voice Response (IVR) application development/testing environment to enable enhancements to the customer services provided by the IVR.

c. System replaced, if applicable: Tech refresh of end-of-life NorTel phone switch, over 1000 telephones, and ancillary equipment supporting call technology.

d. Anticipated operational savings: Not applicable.

e. This project replaced end-of-life technology.

f. Project Budget: $1,150,855.00.

g. Primary customers, internal or external: All NW Natural customers and all NW Natural employees.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

36

ICS Network Segmentation – Cybersecurity Program a. Purpose: This project improves the security of our industrial control

systems.

b. Capability Gained: Improve security by segmenting the industrial control network. This is a recommendation based on NIST standards.

c. System Replaced: SCADA Network at NW Natural headquarters and Sherwood

d. Anticipated Operational Savings: Not applicable.

e. This project is a critical need for the cybersecurity protection of our critical SCADA networks.

f. Project Budget: $1,020,431.

g. Primary Customers, Internal or External: NW Natural Gas Control and Operations.

RLMAN Replacement a. Purpose: Implement SAP real estate module to manage NW Natural

contracts (easements, leases, franchises, licenses, permits, railroad permits). This project was presented before the NWN Project Prioritization Steering Committee for approval and was approved to proceed because of the fact that it improves NW Natural processes for managing real estate contracts and payments.

b. Capability Gained: Consolidate risk and land department many separate data management tools into a single system integrated with NW Natural accounting system. Standardize and automate many manual departmental processes associated with tracking and managing NW Natural risk and land contracts and payments.

c. System replaced: A portion of the custom built application (RLMAN) and many spreadsheets.

d. Anticipated Operations Savings: Specific operational savings not identified yet.

e. Anticipate efficiencies will be gained through automation of current manual processes.

f. Project Budget: $540,576.

g. Primary Customers: Risk and Land group, Accounting, Legal departments.

OPUC Staff Audit Report Audit 2017-001 NW Natural March 2016 – January 2017 March 7, 2017

37

Non-utility use of assets acquired by the Technology Refresh-Large Servers project is reviewed annually in September and will be directly charged.

Staff Recommendations: 21. Rate case staff should ensure that Technology Refresh-Large Servers

assets are allocated, as appropriate, to non-utility operations in accordance with NW Natural’s allocation methodology.