Stability-Liquidity Tradeoffs in Post-Crisis Bond Markets · Stability-Liquidity Tradeoffs in...

26

Stability-Liquidity Tradeoffs in Post-Crisis Bond Markets Darrell Duffie Graduate School of Business, Stanford University Brookings, November 17, 2015 PRE - SET TEMPLATES & USAGE TIPS

Transcript of Stability-Liquidity Tradeoffs in Post-Crisis Bond Markets · Stability-Liquidity Tradeoffs in...

Stability-Liquidity Tradeoffs in Post-Crisis Bond Markets

Darrell Duffie

Graduate School of Business, Stanford University

Brookings, November 17, 2015

P R E - S E T T E M P L AT E S & U S A G E T I P S

A stability-‐liquidity tradeoff

• Capital and ac6vity rules have improved bank stability and reduced commitments of bank-‐affiliated balance sheets to financial market intermedia6on.

• This raises incen6ves for agency intermedia6on, CCPs, all-‐to-‐all trade, shadow-‐bank intermedia6on, and a shiD by banks away from low-‐risk standardized (low-‐margin) products.

• The net impacts on market efficiency are s6ll playing out, and depend on other factors, including monetary policy.

Treasuries bid-‐ask spreads are stable

0

1

2

3

4

5

6

7

8

9

1/1/2005 1/1/2007 1/1/2009 1/1/2011 1/1/2013 1/1/2015

256ths

2-‐year 5-‐year 10-‐year

Source: Adrian, Fleming, Stackman, and Vogt (2015) (BrokerTec data)

Treasury note trade price impacts

Source: Adrian, Fleming, Stackman, and Vogt (2015) (from BrokerTec data)

0

3

6

9

12

15

18

1/1/2005 1/1/2007 1/1/2009 1/1/2011 1/1/2013 1/1/2015

256ths per $100 million

2-‐year 5-‐year 10-‐year

Symptoms of changing liquidity • Tradi6onal liquidity measures such as price impact and bid-‐

ask spread look fine.

• Turnover and trade sizes are generally down.

• Single-‐name CDS and matched-‐book repo markets are withering.

• The 10-‐year Treasury note “yield crash” of October 15, 2014 is a symptom of changes in the mix of intermediaries, including HFT.

Trade size has declined

Source: Adrian, Fleming, Stackman, and Vogt (2015) (BrokerTec data)

0

5

10

15

20

25

1/1/2005 1/1/2007 1/1/2009 1/1/2011 1/1/2013 1/1/2015

Millions of D

ollars

2-‐year 5-‐year 10-‐year

Treasury market turnover

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Data source: SIFMA

Daily volum

e/ou

tstand

ing

Figure 4.13: Benchmark Price Impact (Cash) Figure 4.14: Benchmark Trade Size (Cash)

Figure 4.15: Treasury Active Contract Trade Size

(Futures)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2004 2006 2008 2010 2012 2014

32nds per $100

million

2 Year 5 Year 10 Year

Note: Slope coefficients from weekly regressions of 5” price changes on 5” net order flow for the on-the-run notesSource: Staff calculations, based on data from BrokerTec.

0

5

10

15

20

25

30

2004 2006 2008 2010 2012 2014

$ millions 2 Year 5 Year 10 Year

Note: 21-day moving average; Average trade size; On-the-run notesSource: Staff calculations, based on data from BrokerTec.

0

1

2

3

4

5

6

7

8

9

2004 2006 2008 2010 2012 2014

$ millions 2 Year 5 Year 10 Year

Note: 21-day moving average; 8:20 - 15:00 ETSource: Staff calculations, based on data from CME Group.

69

duffie

Typewritten Text

Treasury futures average trade size

duffie

Typewritten Text

Source: Joint Staff Report, The U.S. Treasury Market (2015)

21

Decline in GCF net lending volume

-100

-80

-60

-40

-20

0

20

40

60

80

100

$ bi

llion

s

Mar 11 Sep 11 Mar 12 Sep 12 Mar 13 Sep 13 Mar 14 Sep 14 Mar 15 Sep 15month

Non-BHC Dealers Small BHC dealers Large BHC Dealers

Monthly AverageDaily Net Cash Positions by Dealer Group

duffie

Typewritten Text

Source: Martin (2015), FRBNY.

Copyright 2014 FINRA

Corporate bond – average bid-ask spreads

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

2002 2004 2006 2008 2010 2012 2014 2016

$ pe

r uni

t par

Investment Grade

High Yield

Copyright 2014 FINRA

Corporate bond – average trade size

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2002 2004 2006 2008 2010 2012 2014 2016

$ mill

ion

1,000 Most Active BondsLess Active Bonds

Turnover of corporate and municipal bonds

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008

Municipal bonds Corporate bonds

Daily volum

e/ou

tstand

ing

Data source: SIFMA

When more dealers compete, corporate bond trade costs go down

-‐10

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Cost in Basis Points

Number of dealers responding

Investment Grade

High Yield

Source: Hendersho` and Madhavan (2014)

Number of CDS trades per quarter

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000 Single-‐Name Index

Data source: DTCC

Who handles U.S. bonds?

0

500

1000

1500

2000

2500

3000

3500

4000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Bond Fund+ETF Dealer Bonds Financed

Data sources. ICI: AUM, bond mutual funds + ETFs. FRBNY: primary dealer daily financing (securi6es out) of UST + agencies + MBS + corporate bonds.

Assets (b

illion USD

)

Net monthly cash inflows to bond funds

-‐80

-‐60

-‐40

-‐20

0

20

40 1/1/13

3/1/13

5/1/13

7/1/13

9/1/13

11/1/13

1/1/14

3/1/14

5/1/14

7/1/14

9/1/14

11/1/14

1/1/15

3/1/15

5/1/15

7/1/15

9/1/15

Billion

s of d

ollars

Data source: Investment Company Ins6tute

Section 4 Figures

Figure 4.1: Financial Assets of Security Brokers and Dealers

Figure 4.2: Net Treasury Positions of Primary Dealers

Figure 4.3: Gross Treasury Positions of Primary

Dealers Figure 4.4: Estimated Treasury Market-Making

Positions of Primary Dealers

Figure 4.5: Ownership of Treasury Debt by Investor

Group

Figure 4.6: Government Bond Fund Flows

0

1

2

3

4

5

6

1990 1994 1998 2002 2006 2010 2014

$ trillions

Note: Quarterly observations; Total financial assets of security brokers and dealers as reported in the financial accounts of the United StatesSource: Staff calculations, based on data from Federal Reserve Board.

-200

-150

-100

-50

0

50

100

150

2002 2004 2006 2008 2010 2012 2014

$ billions

Note: 4-week moving averageSource: Staff calculations, based on data from FRBNY.

0

1

2

3

4

5

6

7

8

9

0

100

200

300

400

500

600

2002 2004 2006 2008 2010 2012 2014

%$ billions

Position

Position as % of Debt Outstanding,ex-Fed (RHS)

Note: 4-week moving average; Sum of dealers’ short and long positions Source: Staff calculations, based on data from FRBNY.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

50

100

150

200

250

2002 2004 2006 2008 2010 2012 2014

%$ billions

Position

Position as % of Debt Outstanding, ex-Fed (RHS)

Note: 4-week moving average; Smaller of each dealer’s short and long position in each reporting bucket, aggregated across dealers and buckets Source: Staff calculations, based on data from FRBNY.

0

10

20

30

40

50

60

2004 2006 2008 2010 2012 2014

%

Mutual funds Pension fundsHouseholds State and local governmentsDepository institutions Money market fundsInsurance companies Other financial institutionsNonfinancial businesses Federal Reserve

Note: Mutual funds includes closed-end funds and exchange-traded funds; Pension funds includes government retirement fundsSource: Staff calculations, based on data from Federal Reserve Board.

-10-8-6-4-202468

10

2004 2006 2008 2010 2012 2014

$ billions

Note: Total net monthly flows; Some funds own agency debt securities and MBS in addition to Treasury securitiesSource: Staff calculations, based on data from Morningstar.

67

duffie

Typewritten Text

Government bond fund flows

duffie

Typewritten Text

Source: Joint Staff Report: The U.S. Treasury Market

Asset management stability issues • Comments on the risk of a crisis arising from sudden bond

fund redemp6ons seem exaggerated. • A rush for the exits would impact prices, but bids will likely

arrive before a crisis is triggered. Who exactly would “fail”? • Large hedge funds present a poten6al for unwind risk, given

their reliance on leverage and expert porkolio managers. • Large agency-‐based managers seem more benign, and have

not been designated as SIFIs. • Regulators also focus on insurance firms that are ac6ve in

financial markets. Some have been designated. • Money-‐market funds are migra6ng to government securi6es

Supplementary content

Depth has declined from recent highs

Source: Adrian, Fleming, Stackman, and Vogt (2015) (from BrokerTec data)

0

500

1000

1500

2000

2500

1/1/2005 1/1/2007 1/1/2009 1/1/2011 1/1/2013 1/1/2015

Millions of D

ollars

2-‐year 5-‐year 10-‐year

T-‐note mul6lateral plakorm volumes

0

10

20

30

40

50

60

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

10-‐year 5-‐year 2-‐year

Source: Fleming (2014) (BrokerTec data)

Daily volum

e (billions of d

ollars)

FX dealer versus non-‐dealer volumes

0

500

1000

1500

2000

2500

3000

3500

1995 1998 2001 2004 2007 2010 2013

Dealers Non-‐dealers

Source: Rime and Schrimpf (2014) (BIS data)

Daily trade volume (billions of U

SD)

Some remaining system vulnerabili6es

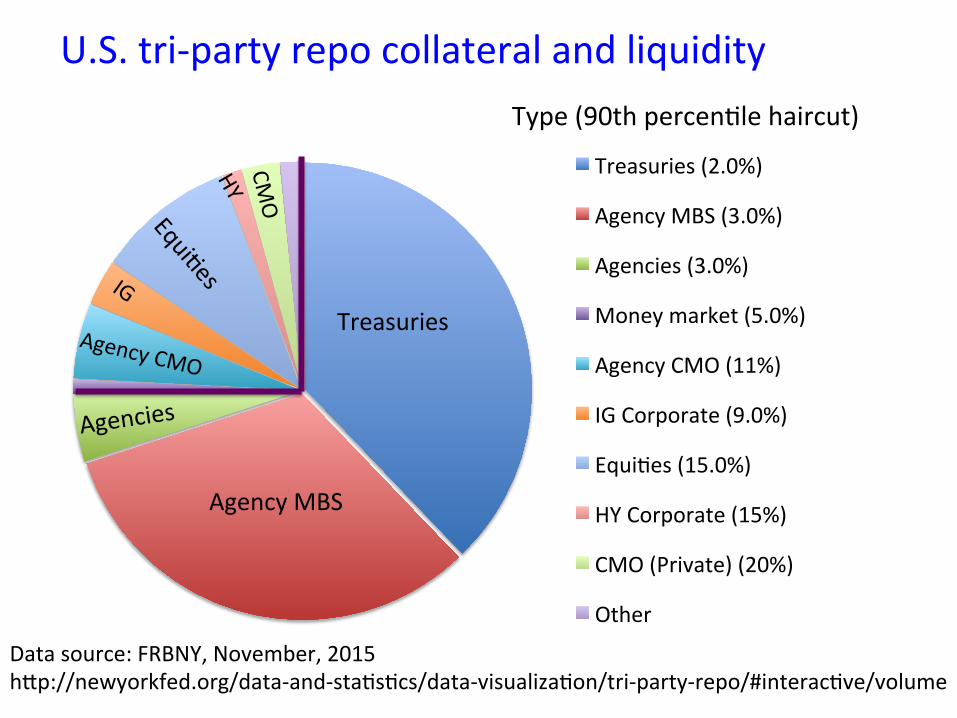

• Improving but s6ll fragile design of tri-‐party repo leaves the poten6al for repo fire sales.

• Lending of last resort is overly limited by Dodd-‐Frank.

• Poten6al for pro-‐cyclical margins, pending new FSB standards (more research needed).

Type (90th percen6le haircut)

Treasuries (2.0%)

Agency MBS (3.0%)

Agencies (3.0%)

Money market (5.0%)

Agency CMO (11%)

IG Corporate (9.0%)

Equi6es (15.0%)

HY Corporate (15%)

CMO (Private) (20%)

Other

Treasuries

Agency MBS

Agencies

Agency CMO

CMO

U.S. tri-‐party repo collateral and liquidity

Data source: FRBNY, November, 2015 h`p://newyorkfed.org/data-‐and-‐sta6s6cs/data-‐visualiza6on/tri-‐party-‐repo/#interac6ve/volume

US GSIFI FHC

U.S. Bank U.S. Broker Dealer

Counterparty

U.K. Broker Dealer

Zone of stays on failure terminaNon of swaps, repos, sec-‐lending

Daily average volume of interest rate deriva6ves

0

200

400

600

800

1000

1200

1400

1600

1995 1998 2001 2004 2007 2010 2013

US-‐OTC US-‐EXCH UK-‐OTC

Daily average volum

e ( $

billions)

Data sources. BIS: OTC Triennial (April), U.S. exchanges Table 23A (March).