St Vincent and the Grenadines Market Guide - October 2014

33

-

Upload

exporttltd -

Category

Documents

-

view

244 -

download

1

description

Want to export to St Vincent and the Grenadines?

Transcript of St Vincent and the Grenadines Market Guide - October 2014

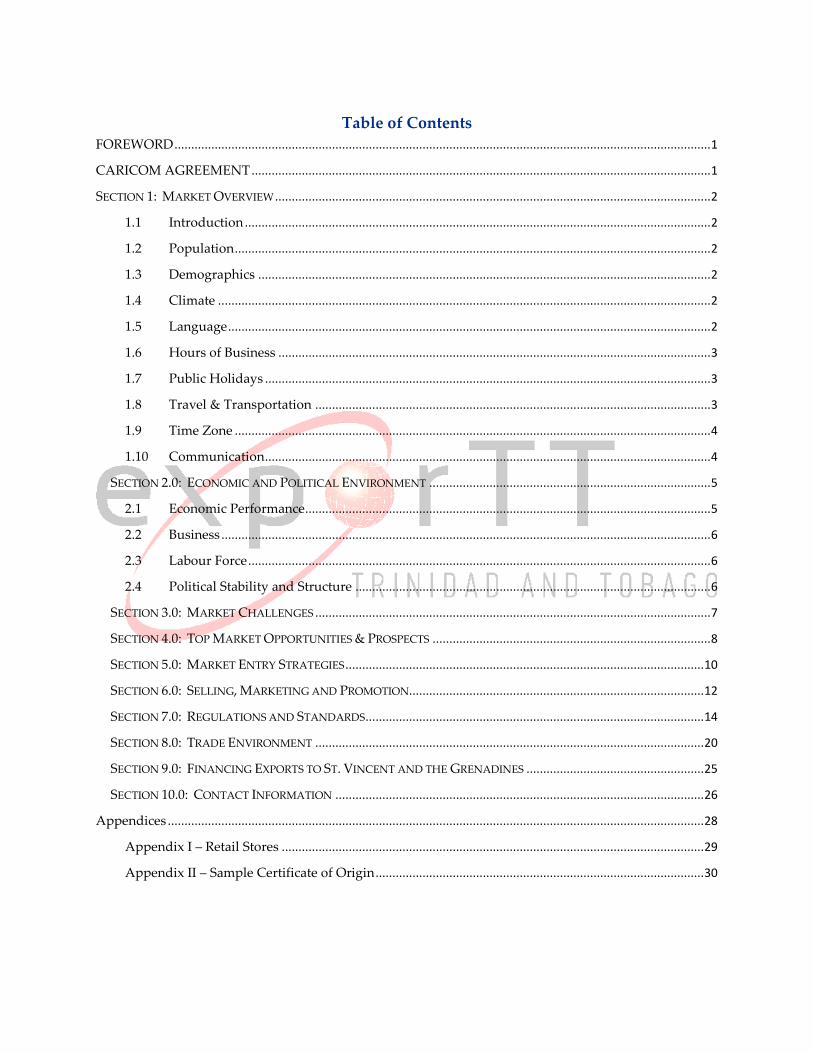

Table of Contents

FOREWORD ................................................................................................................................................................ 1

CARICOM AGREEMENT ......................................................................................................................................... 1

SECTION 1: MARKET OVERVIEW .................................................................................................................................. 2

1.1 Introduction ........................................................................................................................................... 2

1.2 Population .............................................................................................................................................. 2

1.3 Demographics ....................................................................................................................................... 2

1.4 Climate ................................................................................................................................................... 2

1.5 Language ................................................................................................................................................ 2

1.6 Hours of Business ................................................................................................................................. 3

1.7 Public Holidays ..................................................................................................................................... 3

1.8 Travel & Transportation ...................................................................................................................... 3

1.9 Time Zone .............................................................................................................................................. 4

1.10 Communication ..................................................................................................................................... 4

SECTION 2.0: ECONOMIC AND POLITICAL ENVIRONMENT .................................................................................... 5

2.1 Economic Performance......................................................................................................................... 5

2.2 Business .................................................................................................................................................. 6

2.3 Labour Force .......................................................................................................................................... 6

2.4 Political Stability and Structure .......................................................................................................... 6

SECTION 3.0: MARKET CHALLENGES ...................................................................................................................... 7

SECTION 4.0: TOP MARKET OPPORTUNITIES & PROSPECTS ................................................................................... 8

SECTION 5.0: MARKET ENTRY STRATEGIES ........................................................................................................... 10

SECTION 6.0: SELLING, MARKETING AND PROMOTION........................................................................................ 12

SECTION 7.0: REGULATIONS AND STANDARDS ..................................................................................................... 14

SECTION 8.0: TRADE ENVIRONMENT .................................................................................................................... 20

SECTION 9.0: FINANCING EXPORTS TO ST. VINCENT AND THE GRENADINES ..................................................... 25

SECTION 10.0: CONTACT INFORMATION .............................................................................................................. 26

Appendices ................................................................................................................................................................ 28

Appendix I – Retail Stores .............................................................................................................................. 29

Appendix II – Sample Certificate of Origin .................................................................................................. 30

Page 1 of 26

FOREWORD

This Market Guide is intended to give Trinidad & Tobago exporters relevant, accurate and valuable

information for successfully exporting their goods to St. Vincent and the Grenadines. The information

contained therein is based on exporTT’s visits to the market, in-market consultant information, and desk

research. Feel free to contact us at 1.868.623.5507 to discuss your exporting needs.

**********

CARICOM AGREEMENT

The Caribbean Community (CARICOM), originally the Caribbean Community and Common

Market, was established by the Treaty of Chaguaramas which came into effect on 1 August 1973.

CARICOM is an organization of 15 Caribbean nations: Antigua & Barbuda, The Bahamas,

Barbados, Belize, Dominica, Grenada, Guyana, Haiti, Jamaica, Montserrat, Saint Lucia, St. Kitts

and Nevis, St. Vincent and the Grenadines, Suriname and Trinidad and Tobago. There are also

five (5) Associate members as follows: Anguilla, Bermuda, British Virgin Islands, Cayman

Islands, and Turks and Caicos Islands.

CARICOM's main purposes are to promote economic integration and cooperation among its

members, to ensure that the benefits of integration are equitably shared, and to coordinate foreign

policy. Its major activities involve coordinating economic policies and development planning;

devising and instituting special projects for the less-developed countries within its jurisdiction;

operating as a regional single market for many of its members (CARICOM Single Market); and

handling regional trade disputes. The secretariat headquarters is based in Georgetown, Guyana.

St. Vincent and the Grenadines became a member of CARICOM on May 01, 1974.

Page 2 of 26

SECTION 1: MARKET OVERVIEW

1.1 Introduction

St. Vincent and the Grenadines is an archipelago comprising over 30 islands and cays situated at

the southern end of the Caribbean island chain. It is located between St. Lucia to the north and

Grenada to the south. The main island, St. Vincent, has an area of approximately 133 square miles

(332.5 square kilometres) while the Grenadines have an area of 17 square miles. (56.5 square

kilometres). The main islands in the Grenadines are Bequia, Balliceau, Canouan, Mayreau,

Mustique, Isle D'Quatre, Petit Saint Vincent, and Union Island. The capital is Kingstown.

1.2 Population

Source: CIA World Factbook

1.3 Demographics

St Vincent- Facts

Status Independent- 27th October 1979

Ethnic Groups black 66%, mixed 19%, East Indian 6%, European 4%, Carib

Amerindian 2%, other 3%

Religions Protestant 75% (Anglican 47%, Methodist 28%), Roman Catholic

13%, other (includes Hindu, Seventh-Day Adventist, other

Protestant) 12% Source: Caribbean Community Secretariat

1.4 Climate

Because the islands lie close to the equator, they enjoy a steady tropical temperature almost year-

round. Temperatures range from 18° to 32°C. The dry season is from December to June, and the

rainy season from July to November.

1.5 Language

The official language of St Vincent and the Grenadines is English, however, French patois is also

commonly used in the island.

St Vincent- Population

Population: Total

: Kingstown

102,918 (July 2014 est.)

28,000 (2009 est)

Population Growth -0.29% (2014 est.)

Median Age Total: 31.9 years

Male: 32 years

Female: 31.7 years (2014 est.)

Life Expectancy 74.86 years

Page 3 of 26

1.6 Hours of Business

Commercial: 8:00 a.m.-12:00 noon; 1:00-4:00 p.m. Monday to Friday

Government: 8:30 a.m.-12:00 noon, 1:00-4:00 p.m. Monday to Friday

Bank hours are from 8:00 am to 3:00 pm Mondays to Thursdays; up to 5:00 pm on Fridays.

Many shops are opened from 8:00 am to 12:00 noon on Saturdays however, most supermarkets

and shopping centres stay open later.

1.7 Public Holidays

1.8 Travel & Transportation

1.8.1 Airline Travel

There are no direct flights to SVG from outside the Caribbean, as the runway is too small to land

jet aircraft. International passengers first fly into a neighbouring island and then switch to a prop

plane for the final leg of their journey. St. Vincent & The Grenadines has five major airports. Most

visitors fly into ET Joshua Airport (SVD), but you can also opt to fly into the small airstrips found

on Canouan (CIW), Bequia (BQU), Mustique (MQS), or Union Islands (UNI).

The following airlines fly to and from SVG from within the Caribbean and also offer interisland

flights in the Grenadines:

American Eagle

LIAT

Mustique Airways

SVG Air

MONTH DAY OBSERVANCE

January 1 New Year's Day

March 14 National Hero's Day

April 18 Good Friday

21 Easter Monday

May 1 Labour Day

June 9 Whit Monday

July 7 Carnival Monday

8 Carnival Tuesday

August 4 Emancipation Day

October 27 Independence Day

December 25 Christmas Day

26 Boxing Day

Page 4 of 26

Individual Entry Requirements

In order to enter St Vincent and/or the Grenadines a person must present a valid passport and an

airline ticket.

Individual Exit Requirements

In addition to a valid passport and a return ticket, there is a $40 XCD (about $15 USD) departure

tax from the islands that applies to travellers above the age of 12 which can be included in the

ticket prices. You can pay the tax in either Eastern Caribbean dollars or U.S. dollars at the airport

prior to departure. However, this does not apply to CARICOM nationals.

1.8.2 Sea Transport

Due to the uniqueness and relationship of St Vincent with the Grenadines, sea transportation is a

major mode of transport that is utilized on a daily basis. The Bequia Express and Admiralty

Transport offer round-trip service from St. Vincent to Bequia every day. One-way fares aboard

the Bequia Express cost around $20 XCD (about $7.50 USD) to Bequia; round-trip tickets cost

around $35 XCD (about $13 USD). Meanwhile, the Barracuda makes trips between St. Vincent,

Bequia, Mayreau, and Union Island five times a week. Ferry schedules are flexible depending on

season, so it's best to check timetables in advance.

1.8.3 Ground Transportation

Taxis services are available on more populated islands like St. Vincent, Bequia, Mustique, and

Union Islands, as well as some of the smaller isles. Taxis are not metered, therefore, the skill of

negotiating a price before hitting the road will be valuable. The average cost from ET Joshua

Airport (SVD) to downtown Kingstown may cost roughly $30 XCD (about $12 USD).

An alternative for travellers is the use of a rental car, temporary drivers' permits cost $65 XCD

(about $24 USD). Recommended car agencies include Avis and Ben's Auto Rental (784-456-2907).

1.9 Time Zone

1.10 Communication

Calls to Trinidad and Tobago to St. Vincent and the Grenadines = 1-(784)-XXX-XXXX

Calls from St. Vincent and the Grenadines to Trinidad and Tobago = 1-(868)-XXX-XXXX

Time Zone AST- Atlantic Standard Time

Time Difference No Time Difference with Trinidad and Tobago

Page 5 of 26

SECTION 2.0: ECONOMIC AND POLITICAL ENVIRONMENT

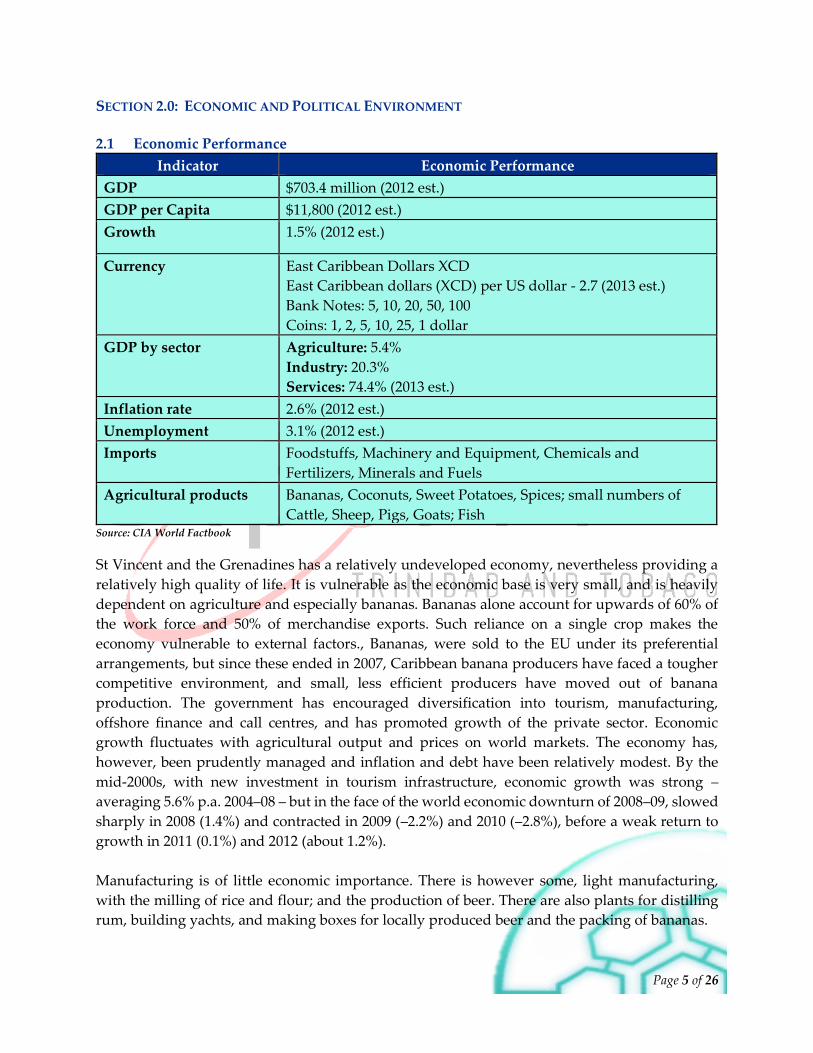

2.1 Economic Performance

Indicator Economic Performance

GDP $703.4 million (2012 est.)

GDP per Capita $11,800 (2012 est.)

Growth 1.5% (2012 est.)

Currency East Caribbean Dollars XCD

East Caribbean dollars (XCD) per US dollar - 2.7 (2013 est.)

Bank Notes: 5, 10, 20, 50, 100

Coins: 1, 2, 5, 10, 25, 1 dollar

GDP by sector Agriculture: 5.4%

Industry: 20.3%

Services: 74.4% (2013 est.)

Inflation rate 2.6% (2012 est.)

Unemployment 3.1% (2012 est.)

Imports Foodstuffs, Machinery and Equipment, Chemicals and

Fertilizers, Minerals and Fuels

Agricultural products Bananas, Coconuts, Sweet Potatoes, Spices; small numbers of

Cattle, Sheep, Pigs, Goats; Fish Source: CIA World Factbook

St Vincent and the Grenadines has a relatively undeveloped economy, nevertheless providing a

relatively high quality of life. It is vulnerable as the economic base is very small, and is heavily

dependent on agriculture and especially bananas. Bananas alone account for upwards of 60% of

the work force and 50% of merchandise exports. Such reliance on a single crop makes the

economy vulnerable to external factors., Bananas, were sold to the EU under its preferential

arrangements, but since these ended in 2007, Caribbean banana producers have faced a tougher

competitive environment, and small, less efficient producers have moved out of banana

production. The government has encouraged diversification into tourism, manufacturing,

offshore finance and call centres, and has promoted growth of the private sector. Economic

growth fluctuates with agricultural output and prices on world markets. The economy has,

however, been prudently managed and inflation and debt have been relatively modest. By the

mid-2000s, with new investment in tourism infrastructure, economic growth was strong –

averaging 5.6% p.a. 2004–08 – but in the face of the world economic downturn of 2008–09, slowed

sharply in 2008 (1.4%) and contracted in 2009 (–2.2%) and 2010 (–2.8%), before a weak return to

growth in 2011 (0.1%) and 2012 (about 1.2%).

Manufacturing is of little economic importance. There is however some, light manufacturing,

with the milling of rice and flour; and the production of beer. There are also plants for distilling

rum, building yachts, and making boxes for locally produced beer and the packing of bananas.

Page 6 of 26

The major imports are machinery and transport equipment, food and beverages, chemicals, and

fuels, coming primarily from the United States and the Caribbean Community and Common

Market (CARICOM) countries, especially Trinidad and Tobago and Barbados. The main exports

are bananas, packaged flour and rice, and root crops such as dasheens and eddoes. The country’s

main export destinations are the CARICOM countries particularly Barbados, Saint Lucia, and

Trinidad and Tobago, the United Kingdom, and the United States.

Tourism has grown to become a very important part of the economy. The Grenadines have

become a favourite of the up-market yachting crowd. The trend toward increasing tourism

revenues will likely continue.

The main projects currently taking place in St. Vincent are as follows:

The Argyle International Airport

The upgrade of the Buccament Bay Resort

EC $44MM Leeward Highway Rehabilitation project. Though work is set to begin in

January 2014, the project was launched over five years ago and is just now being tendered.

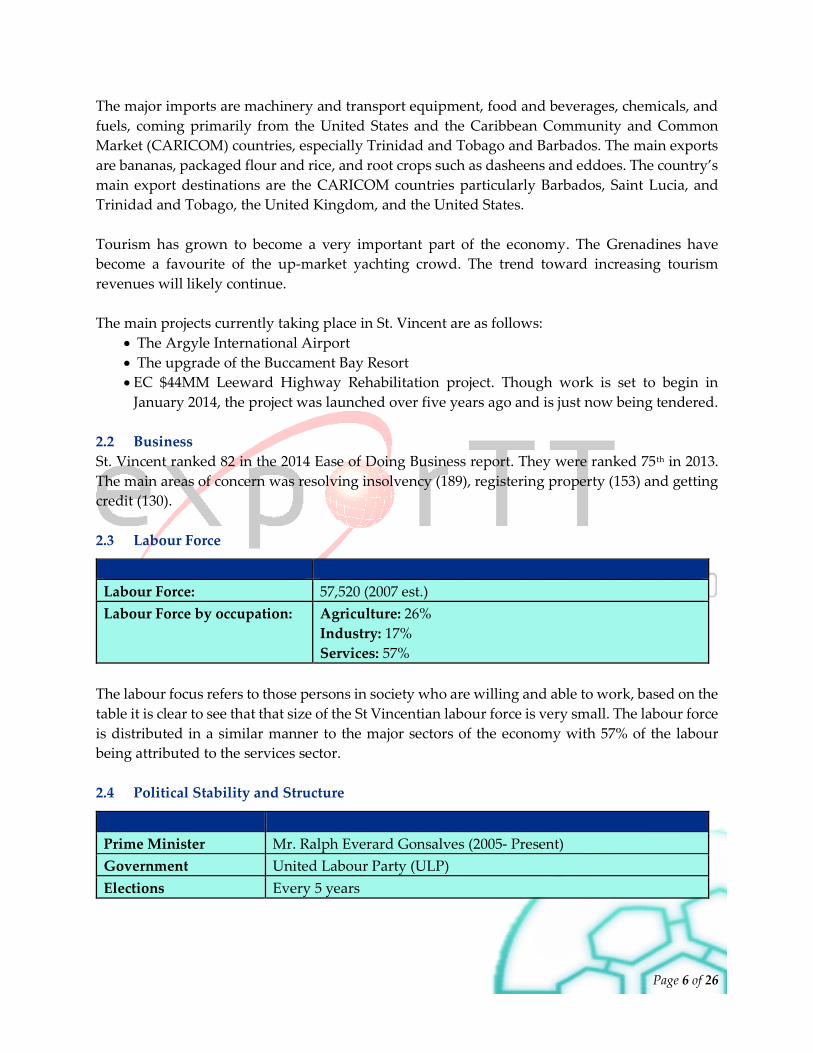

2.2 Business

St. Vincent ranked 82 in the 2014 Ease of Doing Business report. They were ranked 75th in 2013.

The main areas of concern was resolving insolvency (189), registering property (153) and getting

credit (130).

2.3 Labour Force

The labour focus refers to those persons in society who are willing and able to work, based on the

table it is clear to see that that size of the St Vincentian labour force is very small. The labour force

is distributed in a similar manner to the major sectors of the economy with 57% of the labour

being attributed to the services sector.

2.4 Political Stability and Structure

Labour Force: 57,520 (2007 est.)

Labour Force by occupation: Agriculture: 26%

Industry: 17%

Services: 57%

Prime Minister Mr. Ralph Everard Gonsalves (2005- Present)

Government United Labour Party (ULP)

Elections Every 5 years

Page 7 of 26

Political Stability and Absence of Violence/Terrorism captures perceptions of the likelihood that

the government will be destabilized or overthrown by unconstitutional or violent means,

including politically-motivated violence and terrorism. Based on World Bank statistics the latest

value for St. Vincent and the Grenadines Political Stability and Absence of Violence/Terrorism is

0.87 in 2011. The all-time low was 0.25 on 2002-12-31, while the all-time high was 1.18 on 2005.

Therefore, based on the graph the St Vincentian market is generally a stable market

Source: World Bank

SECTION 3.0: MARKET CHALLENGES

The following challenges were identified in the market:

3.1 Logistics

One of the major challenges identified in the market was the lack of cold storage shipping facilities

from Trinidad and Tobago to St Vincent. Currently none of the shipping lines that carry

refrigerated or reefer containers service the island. Hence temperature sensitive cargo are not

easily accessible to the customers. This can be seen as a barrier to trade as Trinidad and Tobago

exporters are unable to export products such as deli meats to the island. St Vincent buyers are

therefore forced to look at other supplying markets such as the United States and Canada for

these products.

Inconsistencies in the delivery of products from Trinidad and Tobago was sighted as another

major obstacle. Buyers within the market stated that shipments from Trinidad and Tobago are

usually delayed and takes an unwarranted period of time to arrive. This leads to buyers switching

suppliers to other CARICOM Member States or the United States of America.

3.2 Suitcase Traders “Traffickers”

This term refers to individuals who travels back and forth between Trinidad and Tobago and St

Vincent on a regular basis mainly to sell their agricultural produce. These traders usually

purchase Trinidad & Tobago products to trade on their return to St Vincent. A majority of these

products qualify for duty free access and as such a Certificate of Origin is issued to facilitate the

preferential access to the country.

0

2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Political Stability and absence of violence/terrorism 2002 -2011

Page 8 of 26

This trade has been sighted as a major challenge for established Vincentian companies who

currently have sole distributorship of a product or product line or even attempting to source new

products.

3.3 Taste and Preference

While there is a heavy presence of Trinidad & Tobago products in the supermarkets and retail

stores, there is also solid competition from products from the United States of America. The

presence of US products therefore has the potential to shift the taste and preference profile of the

local consumers thereby resulting in Trinidad and Tobago exporters losing market share.

Therefore Trinidad and Tobago exporters will need to modify their products to match the taste

profile of the market. In addition, there should be innovation in packaging and labelling to

compete with the international brands.

SECTION 4.0: TOP MARKET OPPORTUNITIES & PROSPECTS

The trade in goods between St Vincent and Trinidad and Tobago is skewed in favour of Trinidad

and Tobago. Therefore, despite the market challenges highlighted above, there is still major

potential for doing business with this country. Some market opportunities and prospects are as

follows:

4.1 Aerated Beverages

These were identified by buyers in the market as a potential product of interest. Based on line

graph below it is evident that the imports of soft drink to St Vincent have been increasing over

the 7 year period under review. This can be seen by the upward slope of the line and 63.5% change

from 2006.

The supplying markets of aerated beverages to St. Vincent and the Grenadines based on the data

from ITC Trademap shows that Trinidad and Tobago controls the largest share of the market and

represents 41%. This was then closely followed by St. Lucia and the US with 26% and 13%

respectively. Observations in the supermarkets confirmed the presence of soft drinks and juices

similar to Trinidad and Tobago manufactured products from the US.

0

2000

4000

6000

2006 2007 2008 2009 2010 2011 2012

St Vincent's Import of Aerated Beverages

Page 9 of 26

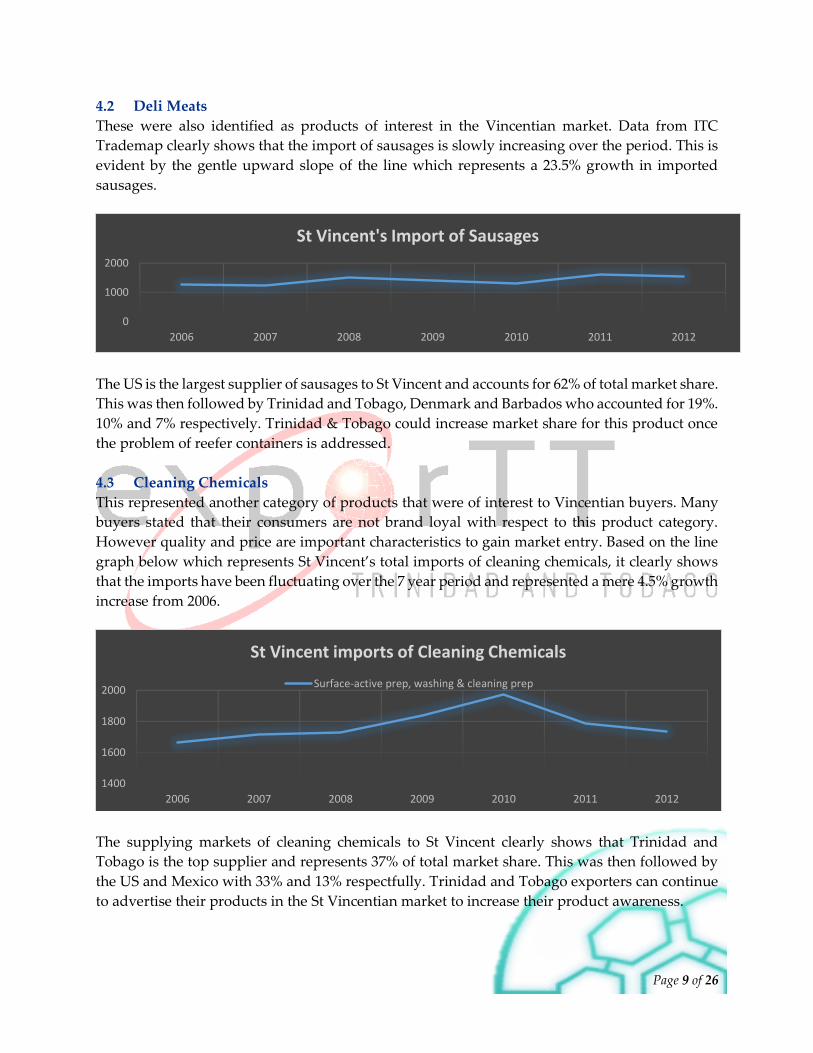

4.2 Deli Meats

These were also identified as products of interest in the Vincentian market. Data from ITC

Trademap clearly shows that the import of sausages is slowly increasing over the period. This is

evident by the gentle upward slope of the line which represents a 23.5% growth in imported

sausages.

The US is the largest supplier of sausages to St Vincent and accounts for 62% of total market share.

This was then followed by Trinidad and Tobago, Denmark and Barbados who accounted for 19%.

10% and 7% respectively. Trinidad & Tobago could increase market share for this product once

the problem of reefer containers is addressed.

4.3 Cleaning Chemicals

This represented another category of products that were of interest to Vincentian buyers. Many

buyers stated that their consumers are not brand loyal with respect to this product category.

However quality and price are important characteristics to gain market entry. Based on the line

graph below which represents St Vincent’s total imports of cleaning chemicals, it clearly shows

that the imports have been fluctuating over the 7 year period and represented a mere 4.5% growth

increase from 2006.

The supplying markets of cleaning chemicals to St Vincent clearly shows that Trinidad and

Tobago is the top supplier and represents 37% of total market share. This was then followed by

the US and Mexico with 33% and 13% respectfully. Trinidad and Tobago exporters can continue

to advertise their products in the St Vincentian market to increase their product awareness.

0

1000

2000

2006 2007 2008 2009 2010 2011 2012

St Vincent's Import of Sausages

1400

1600

1800

2000

2006 2007 2008 2009 2010 2011 2012

St Vincent imports of Cleaning Chemicals

Surface-active prep, washing & cleaning prep

Page 10 of 26

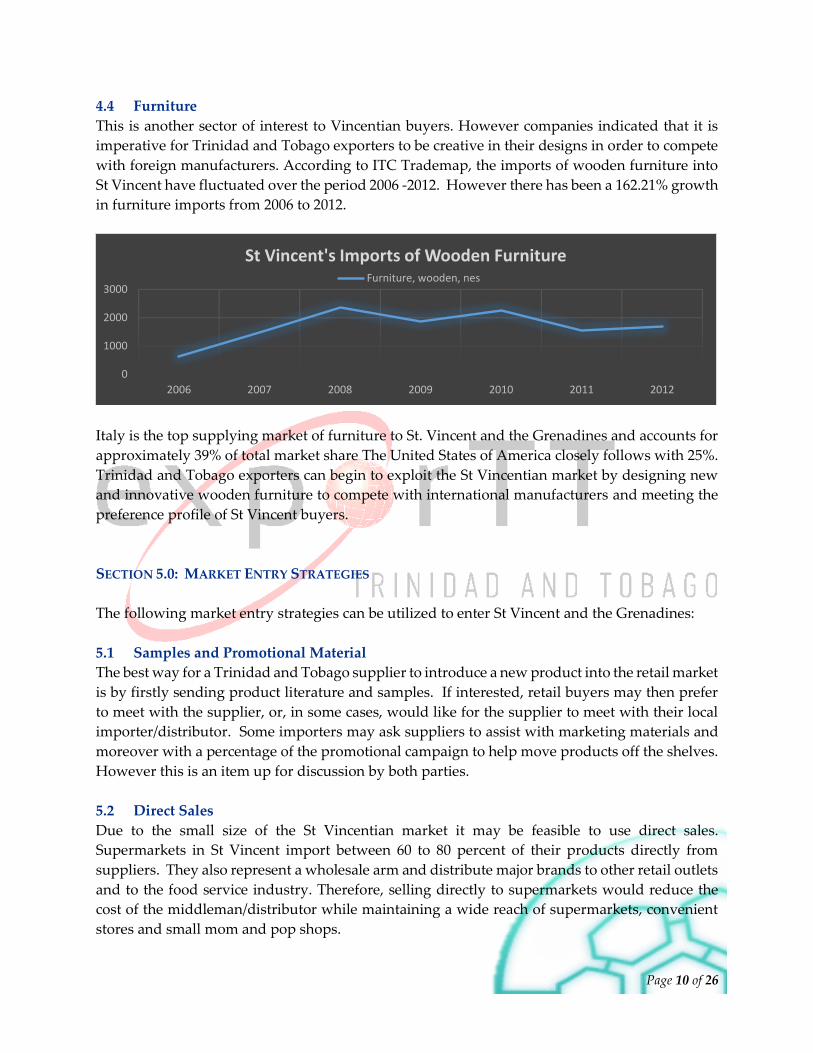

4.4 Furniture

This is another sector of interest to Vincentian buyers. However companies indicated that it is

imperative for Trinidad and Tobago exporters to be creative in their designs in order to compete

with foreign manufacturers. According to ITC Trademap, the imports of wooden furniture into

St Vincent have fluctuated over the period 2006 -2012. However there has been a 162.21% growth

in furniture imports from 2006 to 2012.

Italy is the top supplying market of furniture to St. Vincent and the Grenadines and accounts for

approximately 39% of total market share The United States of America closely follows with 25%.

Trinidad and Tobago exporters can begin to exploit the St Vincentian market by designing new

and innovative wooden furniture to compete with international manufacturers and meeting the

preference profile of St Vincent buyers.

SECTION 5.0: MARKET ENTRY STRATEGIES

The following market entry strategies can be utilized to enter St Vincent and the Grenadines:

5.1 Samples and Promotional Material

The best way for a Trinidad and Tobago supplier to introduce a new product into the retail market

is by firstly sending product literature and samples. If interested, retail buyers may then prefer

to meet with the supplier, or, in some cases, would like for the supplier to meet with their local

importer/distributor. Some importers may ask suppliers to assist with marketing materials and

moreover with a percentage of the promotional campaign to help move products off the shelves.

However this is an item up for discussion by both parties.

5.2 Direct Sales

Due to the small size of the St Vincentian market it may be feasible to use direct sales.

Supermarkets in St Vincent import between 60 to 80 percent of their products directly from

suppliers. They also represent a wholesale arm and distribute major brands to other retail outlets

and to the food service industry. Therefore, selling directly to supermarkets would reduce the

cost of the middleman/distributor while maintaining a wide reach of supermarkets, convenient

stores and small mom and pop shops.

0

1000

2000

3000

2006 2007 2008 2009 2010 2011 2012

St Vincent's Imports of Wooden FurnitureFurniture, wooden, nes

Page 11 of 26

Product Flow for Imported Products:

This method of market entry creates an opportunity to establish a closer relationship with the

overseas market and buyers.

5.3 Use of a Distributor

Although direct sales can have its benefits, exporters can decide to use a distributor in the market.

Foreign distributors purchase the product and are always responsible for payment of the goods.

They assume financial risk and generally provide support and customer service. They often buy

to fill their own inventories and typically carry a range of non-competitive, but complementary

products. The benefit of carrying non-competitive products allows the distributor to focus

primarily on a specific type of product without sacrificing similar or competing brands at the

same time. Distributors usually have a much wider reach when compared to direct sales.

Product Flow for Imported Products:

5.4 Private Labelling

In St Vincent there are some locally manufactured products such as toilet paper and pasta, among

others. However, due to financial and other constraints companies are unable to produce in large

quantities to supply both local and foreign markets. Trinidad and Tobago manufacturers can

enter into an agreement with St Vincentian manufacturers to supply finished but unbranded

products which can then be repackaged under the St Vincentian company’s own brand.

5.5 Establishing an Office

This is an alternative route that companies can utilize to enter into the St Vincentian market. The

registration of an external company creates a legal presence within St Vincent and the Grenadines,

Trinidad and Tobago

Supplier

Supermarket/ Grocery Store

Trinidad and Tobago

Supplier

Importer/Distributor

Supermarket/Grocery

Store

Page 12 of 26

validates all legitimate operations of the company within the State and subjects the company to

certain regulatory requirements of the Companies Act.

In order to become registered as an external company in St Vincent and the Grenadines an

Application for Registration in Form 21 must be filed with the Registrar. The application must be

accompanied by the following:

Request of Name Search and Reservation in Form 26

Statutory Declaration of a Director of the company verifying the particular set out in the

application form

Statutory Declaration of an Attorney-at-law confirming compliance with section 344.

Power of Attorney and Consent to act as Attorney in Form 23 empowering some person

resident in St Vincent and the Grenadines act as attorney of the company for the purpose

of receiving service of process in all suits and proceedings in St Vincent and the

Grenadines and all lawful notices.

A notarised copy of each of the corporate instruments of the company

The prescribed fees

For further information please contact the Commerce and Intellectual Property Office. See Section 10.0

for contact information.

SECTION 6.0: SELLING, MARKETING AND PROMOTION

6.1 Selling Factors/Techniques

Selling factors and techniques are described in the following five steps to master the selling

process.

Steps Description

1. Greeting

You need to ‘arrest’ the buyer:

Pay attention to dress, hygiene, grooming, handshake,

etc.

Treat the buyer’s business card with respect and present

your business card in a professional manner.

Speak clearly, paying attention to voice, tone, eye

contact, etc.

Use correct titles and surnames.

Have a positive body language.

2. Ask questions to

understand the prospect

Don’t ask direct questions but ask leading questions in a

conversation type manner to find out the buyer’s need and

what he/she is looking for.

3. Present Benefits Present the benefits of your product/s or service/s in a

manner that aligns them to the need of the buyer.

Page 13 of 26

6.2 Retail Market Composition

The retail market of St Vincent and the Grenadines is composed of over 30 supermarkets, grocery

stores, convenience stores, and gas marts. Only six are large supermarkets and all six are located

in St. Vincent. They import most of their food products from overseas suppliers and also

purchase a small percentage of food products from other local importers or distributors. About

12 smaller grocery stores offer a smaller selection of food products.

In addition, there are approximately seven convenience stores on the island. Both grocery stores

and convenience stores occasionally import directly but purchase most of their food supplies

from local distributors. Gas marts also compete for convenience in the St Vincent and the

Grenadines retail food market. They rarely, if ever, import food products directly from supplier.

Additionally, roughly 400 mom & pop shops are currently in business as well and local

wholesalers supply their food needs (Source: USDA Foreign Agricultural Information Network).

On the construction and industrial materials side of the retail chain there are approximately 18

hardware’s located throughout St Vincent and the Grenadines. The larger hardware stores such

as Coreas Hazells Inc., Ace Hardware and General Hardware Supplier among others, purchase

directly from foreign suppliers.

4. Handle Objections

If the buyer is not interested in your product/s or service/s,

don’t end the meeting in despair, remain calm. Instead,

take the opportunity to find out more about the market and

their needs so that you can possibly make adjustments to

your product to suit their needs.

5. Close

It is very important to know and agree on the next steps

which should include a thank you email which captures the

essence of the conversation and the activities that would

follow.

Other Tips

Be prepared

Know your business and your products

Be confident

Be a persuasive negotiator

Confirm appointments at least 24 hours in advance and

be on time.

Prepare your marketing tools e.g. brochures, samples,

PowerPoint presentations, etc. and make them come

alive with images.

Take notes and bring a notetaker.

When using an interpreter, do not speak directly to the

interpreter as if the buyer is absent, however keep the

conversation focused on the buyer and allow the

interpreter to interpret accordingly.

Page 14 of 26

Retail stores in St. Vincent target the local population. In contrast, those in the Grenadines are

more geared toward tourists. Every inhabited island in the nation has at least one reasonably

well-stocked retail store for the purchase of foodstuffs.

6.3 Distribution Channel

Due to the small size of the St Vincentian market, the distribution channels as mentioned above

can be either direct since supermarkets carry a distributive, wholesale and retail arm of business.

The distributive trade is cross-sectorial and is dominated by the informal distributors (Suitcase

traders) and a few large organization such as Coreas & Hazells Ltd, C K. Graves & Co, E.D.,

Laynes & Co and SMBs such as Randy’s Supermarket Ltd, Bonnadies Supermarket among others.

Also a distributor can be utilized in the help promote the product in the market. Some distributors

in St Vincent are interested in carrying new products but having exclusivity for products is of

utmost importance. Distributors indicated that they would be unwilling to carry products that

are currently being sold by the suitcase traders. However, using a distributor will ensure that

products are given the necessary attention in the market and can allow for wider reach than

selling directly to a supermarket.

6.4 Pricing Information

Pricing information is available for following products and is available upon request:

Toilet paper

Napkins

Paper Towels

Bleach

Liquid Laundry Detergents

Cleaning Chemicals

Jams and Jellies

Pepper Sauce

SECTION 7.0: REGULATIONS AND STANDARDS

7.1 Import Requirements and Documentation

The following list of documents are required when exporting to St Vincent and the Grenadines

Commercial Invoice

Packing List

Transport Document

Certificate of Origin

Cargo Insurance (optional)

Certificate of Value

7.1.1 Commercial Invoice

A Commercial Invoice is required for commercial shipments. Use the special CARICOM

Invoice format, also known as the U.N. Layout Key format, available at commercial

stationers. CARICOM provides a CARICOM Specimen Invoice in the recommended

format, which lists all the information required on the invoice along with explanatory

information on how to complete the form. Shipments not covered by a CARICOM invoice

may be subject to delay. CARICOM countries generally require the following information

to be included:

Page 15 of 26

Seller and consignee name and

address

Buyer name and address if

different from consignee

Name of bank handling

transaction (if applicable)

Invoice number and date

Customer order and other

reference numbers

Country of origin

Destination country

Mode of transportation

Transportation details

Port of lading

Marks and numbers

Number and type of packages

Quantity

Gross weight

Net weight

Cubic meters

Description (a general description

for all the goods, and also a specific

per-item description by code or in

full to allow for proper

classification)

Unit price

Total price

Freight, insurance, packing, and

other costs in detail

Total invoice value

Certification

Signature

For airfreight shipments, documents in most cases should accompany cargo such as an

Airway bill (AWB).

For non-commercial shipments, prepare a Pro-forma Invoice.

7.1.2 Packing list

An original packing list is required, signed in blue ink and stamped with a company seal.

At least three (3) copies of the packing list should be included. Net weight and gross weight

must match weights on commercial invoice and bill of lading.

In general, even when it is not required regulation, it is recommended that a packing list be

used with all shipments containing more than one shipping unit of packaged cargo. Most

countries require a packing list be provided together with the commercial invoice. The

required information must be consistent with all information shown on the commercial

invoice.

At least three (3) copies of the packing list should be included as part of the shipping

documents sent to the consignee or the agent thereof. The exact contents of each package

should be clearly identified. This should include each item's gross weight and net weight

and each package's marks and numbers.

7.1.3 Transport document

A properly prepared transport document is required. For ocean cargo, two (2) copies of an

ocean bill of lading are required.

Page 16 of 26

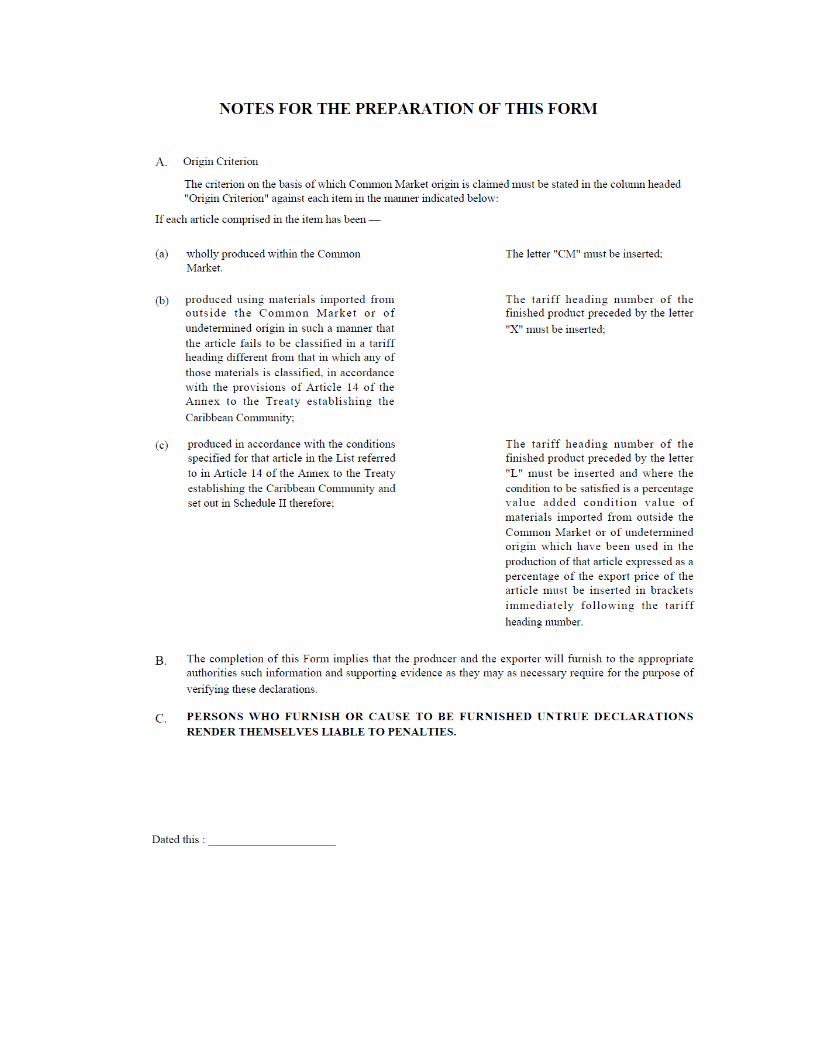

7.1.4 Certificate of Origin

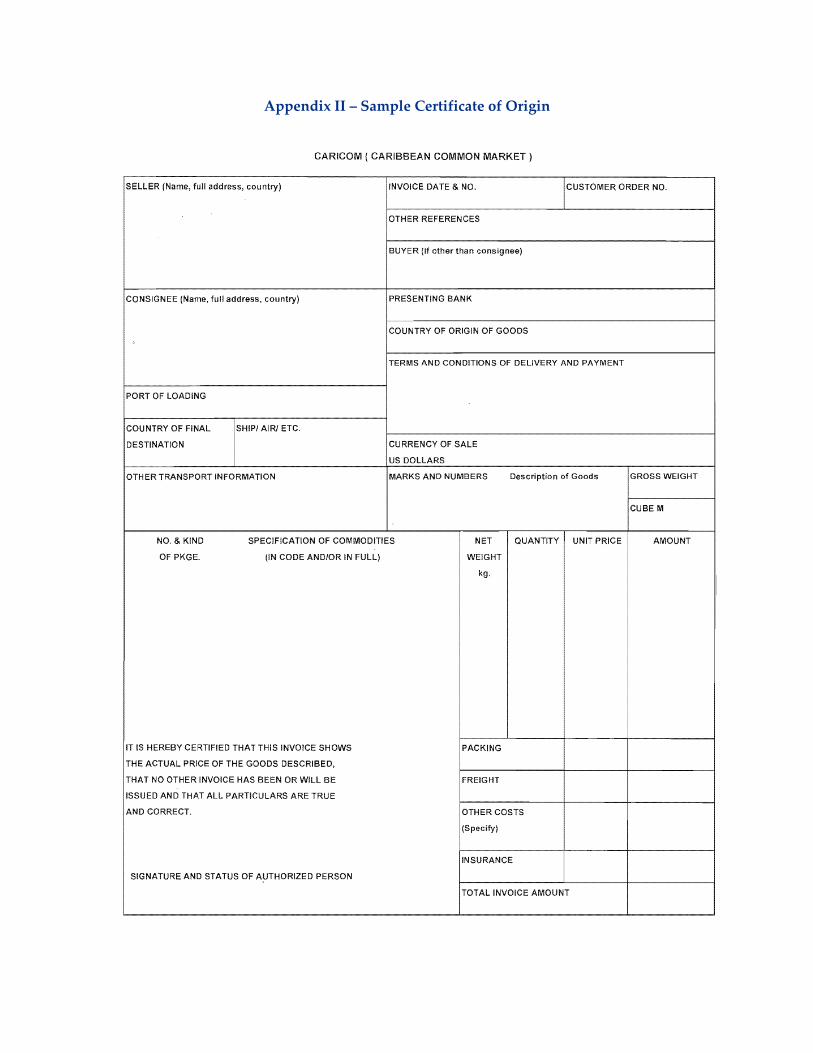

A Certificate of Origin is required when goods are eligible for preferential treatment. The

Certificate of Origin is to be prepared in two (2) copies using the general Certificate of

Origin form, certified by a legal chamber of commerce.

7.2 How to get Certified

exporTT’s Trade Facilitation Office is charged with the responsibility of certifying all products

and determining their eligibility for preferential treatment into trade agreement countries. In the

regard, exporters should complete the following steps to determine their eligibility for

preferential access:

• Completion of Factory Visit Form (Information Furnished in Support of Declaration of

Origin

• Payment ($400.00)

• Visit by a Certification Officer

• Inspection on process of production, raw material and relevant documentation

Please see Appendix 1 for a sample Certificate of Origin

7.3 Official Cargo Insurance Requirements

Shippers who wish to protect their interests in the cargo in the event of loss or damage prior to

delivery to the ultimate consignee should obtain cargo insurance, depending on terms of delivery

with either an FOB/FAS clause or, a CIF+10% value coverage. It is more advisable, however, to

obtain contingency insurance clause coverage.

Having obtained that insurance coverage for the shipment, a copy of the insurance certificate or

the insurance policy should be included in the shipping documents sent to the consignee or the

agent/transportation intermediary thereof.

7.4 Other general import document requirements

Two (2) copies of a certificate of value must be included with each shipment.

7.5 TTBizLink and Single Electronic Window (SEW)

TTBizLink is a Single Electronic Window (SEW) that is a secure user-friendly online platform

which gives real time approvals to more than twenty five different e-government business and

trade related services. It allows individuals to complete application forms online and includes the

upload of supporting documentation. Once submitted, these documents are automatically routed

to various agencies responsible for processing and approvals. Notifications on the status of

applications are sent to applicants via email and if requested via mobile text.

Please visit the link below for TTBizlink Certificate of Origin Training Manual Video

https://www.youtube.com/watch?v=OMLRApTwEL0

Page 17 of 26

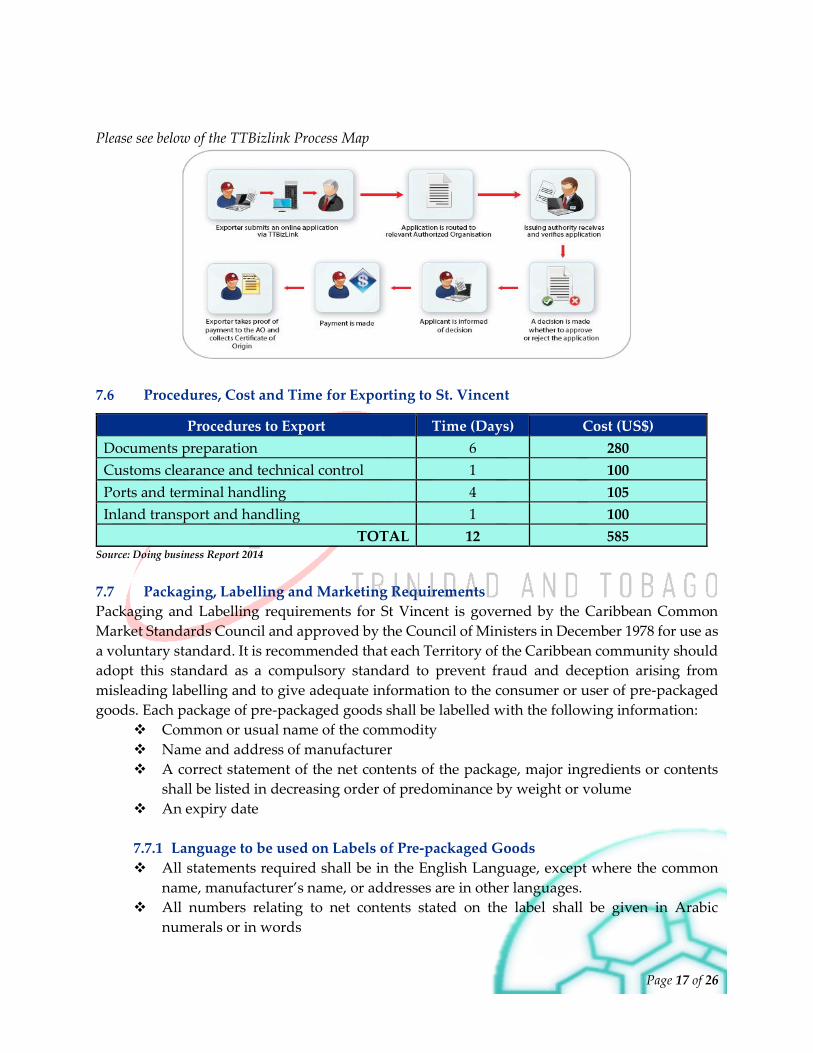

Please see below of the TTBizlink Process Map

7.6 Procedures, Cost and Time for Exporting to St. Vincent

Source: Doing business Report 2014

7.7 Packaging, Labelling and Marketing Requirements

Packaging and Labelling requirements for St Vincent is governed by the Caribbean Common

Market Standards Council and approved by the Council of Ministers in December 1978 for use as

a voluntary standard. It is recommended that each Territory of the Caribbean community should

adopt this standard as a compulsory standard to prevent fraud and deception arising from

misleading labelling and to give adequate information to the consumer or user of pre-packaged

goods. Each package of pre-packaged goods shall be labelled with the following information:

Common or usual name of the commodity

Name and address of manufacturer

A correct statement of the net contents of the package, major ingredients or contents

shall be listed in decreasing order of predominance by weight or volume

An expiry date

7.7.1 Language to be used on Labels of Pre-packaged Goods

All statements required shall be in the English Language, except where the common

name, manufacturer’s name, or addresses are in other languages.

All numbers relating to net contents stated on the label shall be given in Arabic

numerals or in words

Procedures to Export Time (Days) Cost (US$)

Documents preparation 6 280

Customs clearance and technical control 1 100

Ports and terminal handling 4 105

Inland transport and handling 1 100

TOTAL 12 585

Page 18 of 26

Page 19 of 26

7.7.2 Position of Information on Package or on the Goods

The general information required shall be placed on the principal display panel of the

package, that is, the part of the package that is displayed or visible to the purchaser or

consumer at the point of sale, which may be:

In the case of a box, the side or surface commonly displayed;

In the case of a cylindrical container, an area covering an arc of 40 percent of the

circumference of the cylindrical surface;

In the case of a bag with equal sides, one of these sides;

In the case of a bag with sides of more than one size, the size with the largest area;

In the case of a wrapper or confining band that is much narrower than the goods

contained therein, the total area of a ticket or tag attached to the container or to the

goods;

In the case of an article attached to a display card with which it is sold, the area of the

display card and of the package; and

In the case of an ornamental package, at the bottom of the package.

7.7.3 Information on Retail or Unit Price

The label on a package may include a statement of the price of the goods in the package.

Where the price of a package of the goods is not marked on the label or on the package,

the price shall be clearly displayed on a card or notice placed in the close proximity to

the place where the goods are displayed or exposed for sale.

For a copy of a complete packaging and labelling report, please contact us at exporTT.

7.8 Standards

The authority charged with the portfolio of standards is the St Vincent and the Grenadines Bureau

of Standards (SVGBS). The Standards Act No. 70 of 1992 which was amended by Act No. 28 in

2001 gives SVGBS the authority to prepare and promote standards relating to goods, services,

processes and practice used in St Vincent and the Grenadines.

Additionally, the SVGBS is responsible for the administration of the Weights and Measures Act

No. 16 2003. This legislation gives the SVGBS responsibility for regulating all weights and

measuring devices used for trade in St Vincent and the Grenadines.

The SVGBS operates in accordance with the:

The World Trade Organization Technical Barrier to Trade Agreement (WTO/TBT)

The CARICOM Regional Organization for Standards and Quality (CROSQ)

The SVGBS offers the following services:

Standardization

Conformity Assessment/ Compliance

Certification

Technical Assistance

Page 20 of 26

Metrology Services Weights and Measures

Laboratory Services

Please visit the link below for a complete listing of SVGBS fees:

http://www.svgbs.gov.vc/index.php?option=com_content&view=article&id=17&Itemid=3

7.9 Customs – Gold Card Programme

Members of the SVG Chamber of Industry and Commerce (CIC) doing business with the Customs

and Excise Department stand to benefit significantly with a new Gold Card Programme

arrangement between both entities.

Under the new system, goods would be released upon importation with less customs

intervention. Documentation, books and records would be checked, verified and audited

subsequently. Besides the quickest possible release of consignments, Gold Card Holders

consignments would not be routinely examined. Gold Card Holders would enjoy an improved

status when compared with other businesses.

Under the new agreement, only members of CIC or a similar organization can become Gold Card

Holders. The Chamber, which has a membership of 138 companies, is anticipating more

businesses joining the organization to share in this new measure.

Following the launching of the Gold Card programme, three business entities Pasta Enterprises

Limited, St. Vincent Brewery Limited and Coreas Hazells Inc. were awarded Gold Cards and

Certificates

SECTION 8.0: TRADE ENVIRONMENT

8.1 Import Statistics (WORLD)

Based on data from ITC Trademap St Vincent’s total imports have been increasing over the 5 year

period under review by approximately 36.39%. This is evident by the gentle upward slope of the

line graph below.

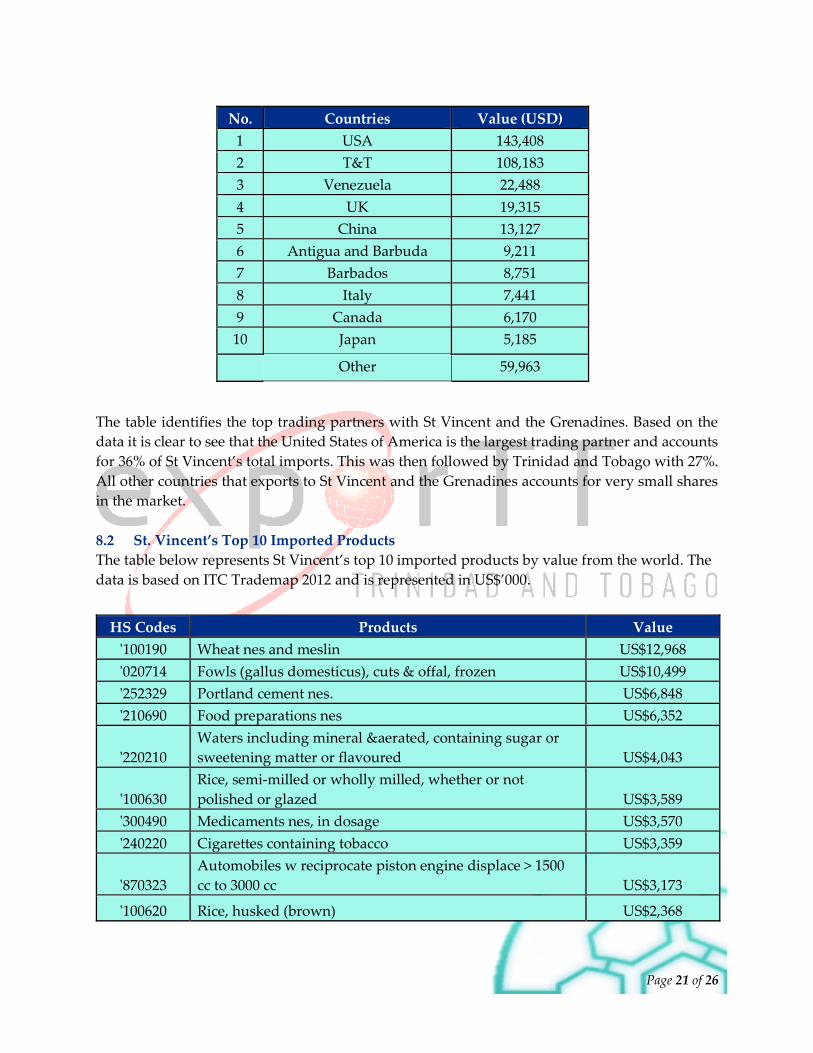

The top trading partners with St Vincent and the Grenadines based on ITC Trademap 2012 data

are as follows: Table 1- Top 10 trading partners by Value $US ‘000.

0

200000

400000

600000

2009 2010 2011 2012 2013

St Vincent Total Imports 2009-2013

Page 21 of 26

The table identifies the top trading partners with St Vincent and the Grenadines. Based on the

data it is clear to see that the United States of America is the largest trading partner and accounts

for 36% of St Vincent’s total imports. This was then followed by Trinidad and Tobago with 27%.

All other countries that exports to St Vincent and the Grenadines accounts for very small shares

in the market.

8.2 St. Vincent’s Top 10 Imported Products

The table below represents St Vincent’s top 10 imported products by value from the world. The

data is based on ITC Trademap 2012 and is represented in US$’000.

No. Countries Value (USD)

1 USA 143,408

2 T&T 108,183

3 Venezuela 22,488

4 UK 19,315

5 China 13,127

6 Antigua and Barbuda 9,211

7 Barbados 8,751

8 Italy 7,441

9 Canada 6,170

10 Japan 5,185

Other 59,963

HS Codes Products Value

'100190 Wheat nes and meslin US$12,968

'020714 Fowls (gallus domesticus), cuts & offal, frozen US$10,499

'252329 Portland cement nes. US$6,848

'210690 Food preparations nes US$6,352

'220210

Waters including mineral &aerated, containing sugar or

sweetening matter or flavoured US$4,043

'100630

Rice, semi-milled or wholly milled, whether or not

polished or glazed US$3,589

'300490 Medicaments nes, in dosage US$3,570

'240220 Cigarettes containing tobacco US$3,359

'870323

Automobiles w reciprocate piston engine displace > 1500

cc to 3000 cc US$3,173

'100620 Rice, husked (brown) US$2,368

Page 22 of 26

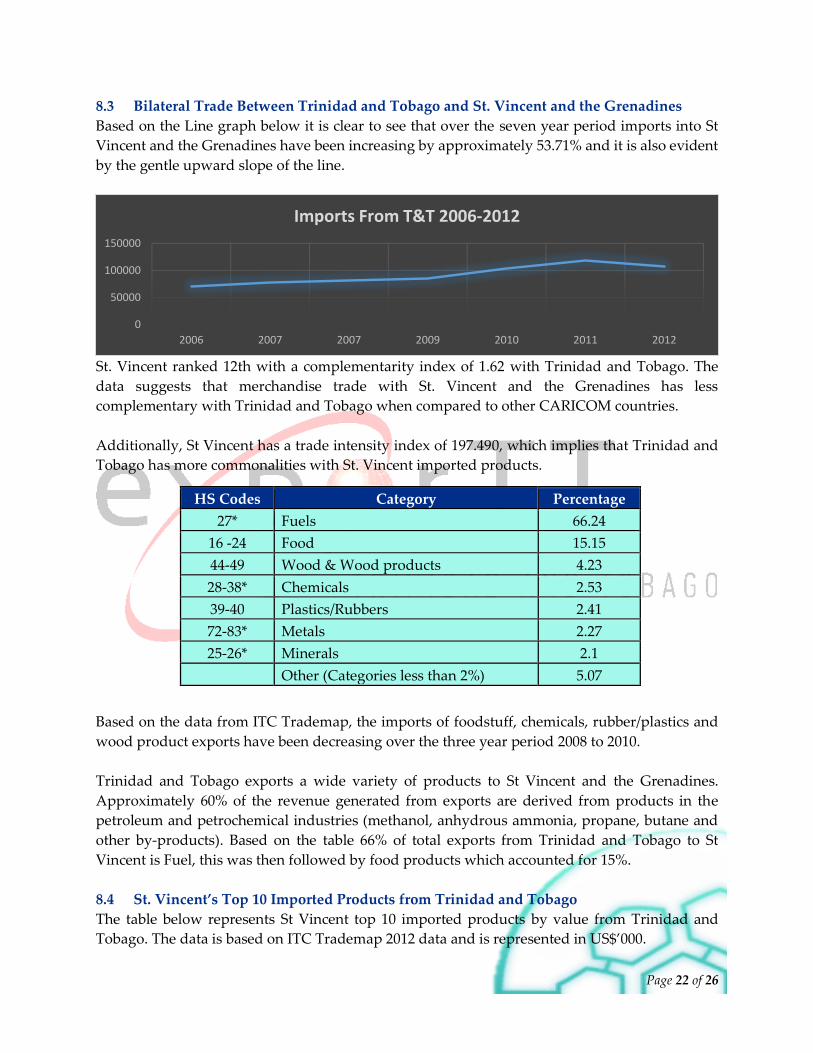

8.3 Bilateral Trade Between Trinidad and Tobago and St. Vincent and the Grenadines

Based on the Line graph below it is clear to see that over the seven year period imports into St

Vincent and the Grenadines have been increasing by approximately 53.71% and it is also evident

by the gentle upward slope of the line.

St. Vincent ranked 12th with a complementarity index of 1.62 with Trinidad and Tobago. The

data suggests that merchandise trade with St. Vincent and the Grenadines has less

complementary with Trinidad and Tobago when compared to other CARICOM countries.

Additionally, St Vincent has a trade intensity index of 197.490, which implies that Trinidad and

Tobago has more commonalities with St. Vincent imported products.

Based on the data from ITC Trademap, the imports of foodstuff, chemicals, rubber/plastics and

wood product exports have been decreasing over the three year period 2008 to 2010.

Trinidad and Tobago exports a wide variety of products to St Vincent and the Grenadines.

Approximately 60% of the revenue generated from exports are derived from products in the

petroleum and petrochemical industries (methanol, anhydrous ammonia, propane, butane and

other by-products). Based on the table 66% of total exports from Trinidad and Tobago to St

Vincent is Fuel, this was then followed by food products which accounted for 15%.

8.4 St. Vincent’s Top 10 Imported Products from Trinidad and Tobago

The table below represents St Vincent top 10 imported products by value from Trinidad and

Tobago. The data is based on ITC Trademap 2012 data and is represented in US$’000.

0

50000

100000

150000

2006 2007 2007 2009 2010 2011 2012

Imports From T&T 2006-2012

HS Codes Category Percentage

27* Fuels 66.24

16 -24 Food 15.15

44-49 Wood & Wood products 4.23

28-38* Chemicals 2.53

39-40 Plastics/Rubbers 2.41

72-83* Metals 2.27

25-26* Minerals 2.1

Other (Categories less than 2%) 5.07

Page 23 of 26

Source: ITC Trademap

8.5 Import Tariffs & Taxes

All locally manufactured products that qualifies under the Rule of Origin will qualify under

Custom’s for duty free treatment. All other products will be subject to Custom duties, and

information on these duties can be sourced at exporTT.

St. Vincent and the Grenadines apply Customs duties according to the Caribbean Community

(CARICOM) Common External Tariff (CET). Duties generally range from 0 to 20% for non-

agricultural goods; up to 40% for agricultural goods, assessed on the CIF value.

Additional taxes and surcharges which may apply:

Value added tax (15 percent; exceptions apply)

Customs service charge (4% of CIF value)

Excise tax on certain commodities are assessed on CIF

Certain products such alcoholic beverages are subject to specific duty rates based on quantity or

net weight. It should also be noted that Ad valorem duties are based on CIF value.

For items subject to ad valorem duties, the WTO Customs Valuation Agreement applies.

According to this agreement, there are six acceptable methods of determining customs value.

Typically the first method is used (unless the buyer and seller are related parties). When the value

cannot be obtained this way, or is rejected by customs, one of the other methods is to be used, in

descending order:

HS Codes Products Value

'240220 Cigarettes containing tobacco US$3,219

'252329 Portland cement nes US$1,885

'220210 Waters including mineral & aerated, containing sugar ro

sweetening matter or flavoured

US$1,668

'190590 Communion wafers, empty cachets of a kind suitable for

pharmaceutical use & similar products & bakers' wares nes

US$1,112

'190531 Sweet biscuits US$802

'190490 Cereals, exclude maize (corn),in grain form, pre-cooked or

otherwise prepared

US$673

'340220 Surface-active prep, washing & cleaning prep put up for retail

sale

US$648

'701090 Carboys, bottles, flasks, jars, pots, phials and other containers, of US$595

'481810 Toilet paper US$562

'721420 Bars & rods, containing indentation, ribs, etc., prod during the

rolling process, nes.

US$480

Page 24 of 26

1) Transaction value (the price actually paid or payable by the importer, plus certain costs

and expenses)

2) Transaction value of identical goods

3) Transaction value of similar goods

4) Deductive value (the sale or resale value, reduced by certain costs such as customs duties,

taxes, and commissions)

5) Computed value (calculated by adding together certain costs/values for production,

materials, profit and other expenses)

6) Fall-back method

8.6 Trade Barriers

As a member of the OECS St Vincent and the Grenadines is expected to implement ARTICLE 164

of the CARICOM Treaty of Chaguaramas. This is a tax on a specific list of products as a

protectionism policy to help local manufacturers. This tax will be placed on goods originating

from Developed Countries and More Developed Countries (MDC) in which Trinidad and Tobago

is classified. Products that are being targeted are: Water, flour, toilet paper, aerated beverages,

beer, pasta and furniture.

St Vincent and the Grenadines has not been able to implement any taxes as was anticipated under

the ARTICLE 164. This is due largely to the fact that small local manufacturing firms are unable

to supply the local market. The Ministry of Trade stated that they will not deny any licenses for

the above mentioned products for entry into St Vincent.

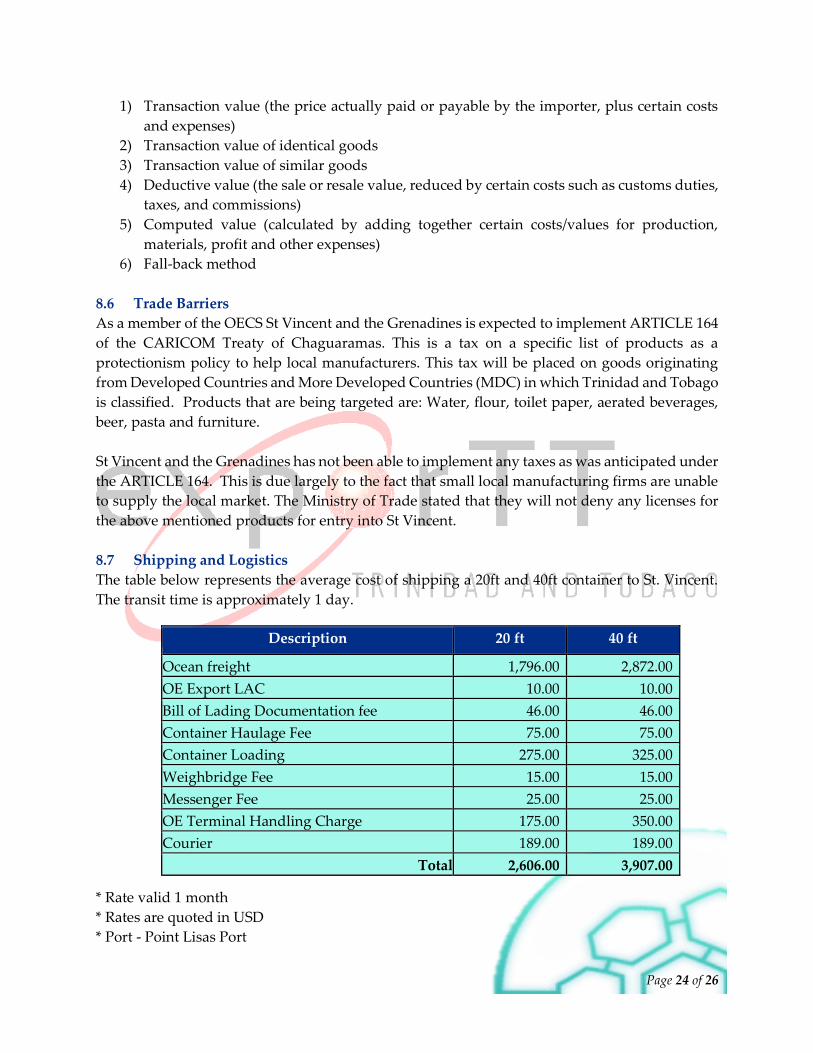

8.7 Shipping and Logistics

The table below represents the average cost of shipping a 20ft and 40ft container to St. Vincent.

The transit time is approximately 1 day.

* Rate valid 1 month

* Rates are quoted in USD

* Port - Point Lisas Port

Description 20 ft 40 ft

Ocean freight 1,796.00 2,872.00

OE Export LAC 10.00 10.00

Bill of Lading Documentation fee 46.00 46.00

Container Haulage Fee 75.00 75.00

Container Loading 275.00 325.00

Weighbridge Fee 15.00 15.00

Messenger Fee 25.00 25.00

OE Terminal Handling Charge 175.00 350.00

Courier 189.00 189.00

Total 2,606.00 3,907.00

Page 25 of 26

8.8 Trade Agreements

St Vincent and the Grenadines is a WTO Member since 01 January 1995. St Vincent and

the Grenadines is a member of one customs union, CARICOM (Caribbean Community).

St Vincent and the Grenadines also has two free trade agreements with: CARICOM-

Costa Rica and CARICOM- Dominica Republic.

St Vincent and the Grenadines also has partial scope agreements with: CARICOM-

Colombia and CARICOM- Venezuela.

St Vincent and the Grenadines is also part of an Economic Association Agreement which

is the CARIFORUM-European Community.

SECTION 9.0: FINANCING EXPORTS TO ST. VINCENT AND THE GRENADINES

exporTT Limited provides co-financing options (50% reimbursement) for the following market

access activities:

a. Product Registration

b. Trademark Registration

c. Product Testing

d. Translation & Interpretation Services

e. Legal representation for product, brand and trademark registration

f. Booth rental at trade shows

g. Business to business matchmaking services

h. Shipping of samples

i. In-store marketing and promotions

j. Booth design at trade shows

k. Ground transportation for exporTT led groups at trade missions and trade shows

l. Brand registration

m. Label modification

n. Registration at international capacity building forum/workshop

Please contact the following person or any other exporTT representative for more information on

these services:

Mr. Crisen Maharaj

Manager- Capacity Building and Programme Financing

exporTT Limited

151B Charlotte Street

Port of Spain

Tel.: (868) 623-5507 ext. 362

Fax: (868) 625-8126

Mobile: (868) 796-4276

Email: [email protected]

Website: www.exportt.co.tt

Page 26 of 26

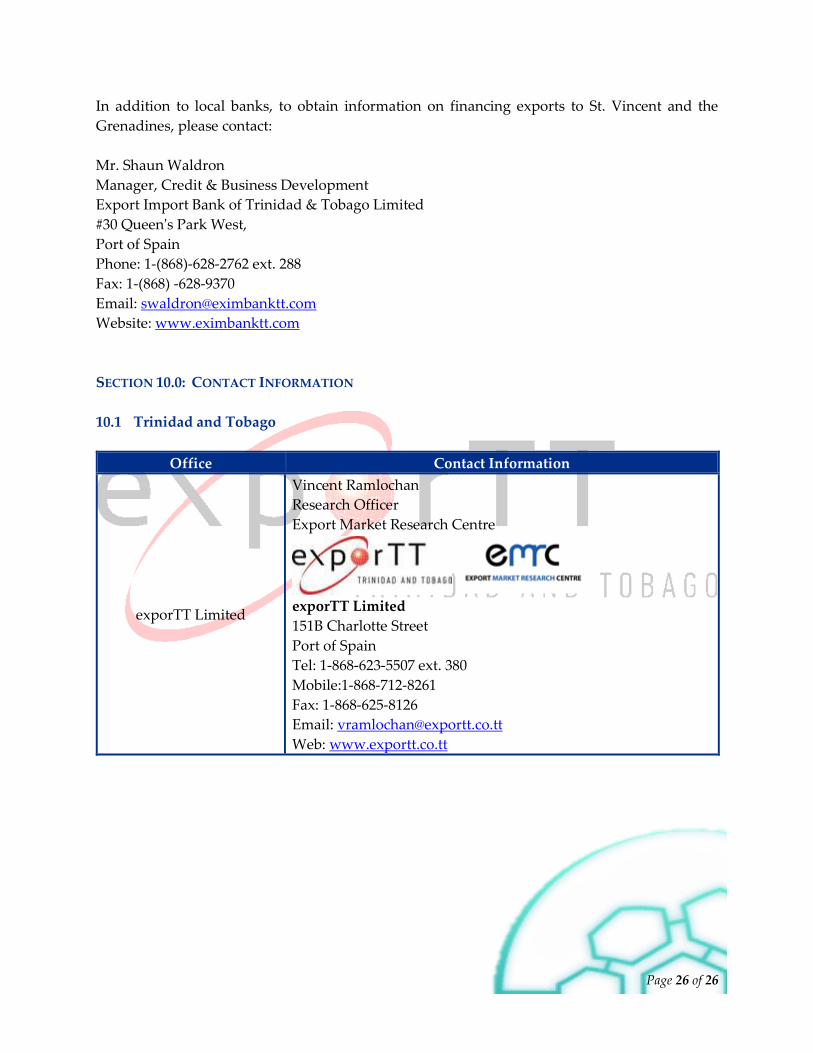

In addition to local banks, to obtain information on financing exports to St. Vincent and the

Grenadines, please contact:

Mr. Shaun Waldron

Manager, Credit & Business Development

Export Import Bank of Trinidad & Tobago Limited

#30 Queen's Park West,

Port of Spain

Phone: 1-(868)-628-2762 ext. 288

Fax: 1-(868) -628-9370

Email: [email protected]

Website: www.eximbanktt.com

SECTION 10.0: CONTACT INFORMATION

10.1 Trinidad and Tobago

Office Contact Information

exporTT Limited

Vincent Ramlochan

Research Officer

Export Market Research Centre

exporTT Limited

151B Charlotte Street

Port of Spain

Tel: 1-868-623-5507 ext. 380

Mobile:1-868-712-8261

Fax: 1-868-625-8126

Email: [email protected]

Web: www.exportt.co.tt

Page 27 of 26

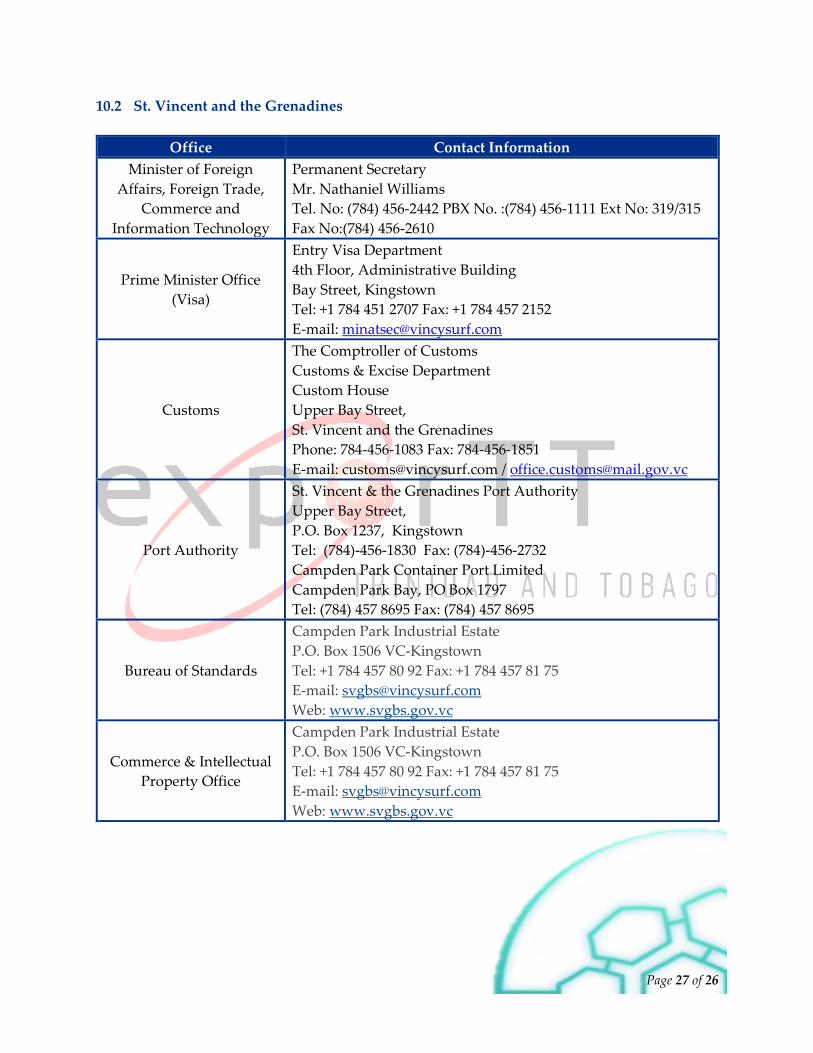

10.2 St. Vincent and the Grenadines

Office Contact Information

Minister of Foreign

Affairs, Foreign Trade,

Commerce and

Information Technology

Permanent Secretary

Mr. Nathaniel Williams

Tel. No: (784) 456-2442 PBX No. :(784) 456-1111 Ext No: 319/315

Fax No:(784) 456-2610

Prime Minister Office

(Visa)

Entry Visa Department

4th Floor, Administrative Building

Bay Street, Kingstown

Tel: +1 784 451 2707 Fax: +1 784 457 2152

E-mail: [email protected]

Customs

The Comptroller of Customs

Customs & Excise Department

Custom House

Upper Bay Street,

St. Vincent and the Grenadines

Phone: 784-456-1083 Fax: 784-456-1851

E-mail: [email protected] / [email protected]

Port Authority

St. Vincent & the Grenadines Port Authority

Upper Bay Street,

P.O. Box 1237, Kingstown

Tel: (784)-456-1830 Fax: (784)-456-2732

Campden Park Container Port Limited

Campden Park Bay, PO Box 1797

Tel: (784) 457 8695 Fax: (784) 457 8695

Bureau of Standards

Campden Park Industrial Estate

P.O. Box 1506 VC-Kingstown

Tel: +1 784 457 80 92 Fax: +1 784 457 81 75

E-mail: [email protected]

Web: www.svgbs.gov.vc

Commerce & Intellectual

Property Office

Campden Park Industrial Estate

P.O. Box 1506 VC-Kingstown

Tel: +1 784 457 80 92 Fax: +1 784 457 81 75

E-mail: [email protected]

Web: www.svgbs.gov.vc

Appendices

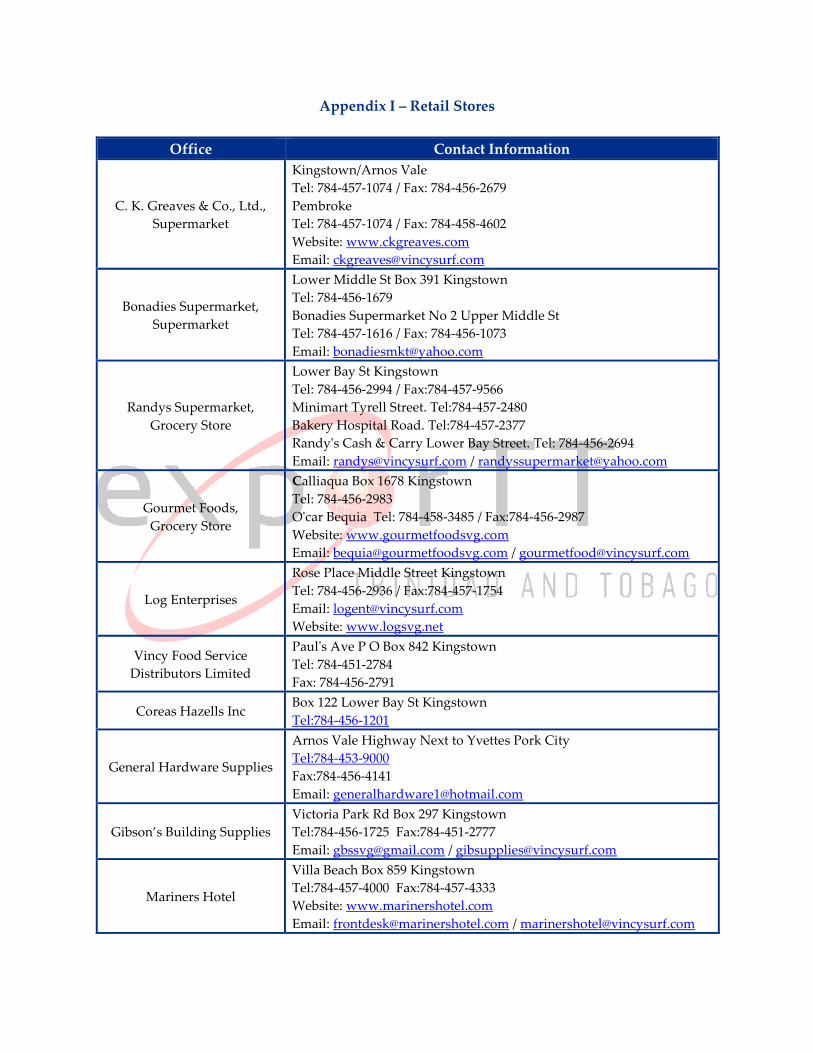

Appendix I – Retail Stores

Office Contact Information

C. K. Greaves & Co., Ltd.,

Supermarket

Kingstown/Arnos Vale

Tel: 784-457-1074 / Fax: 784-456-2679

Pembroke

Tel: 784-457-1074 / Fax: 784-458-4602

Website: www.ckgreaves.com

Email: [email protected]

Bonadies Supermarket,

Supermarket

Lower Middle St Box 391 Kingstown

Tel: 784-456-1679

Bonadies Supermarket No 2 Upper Middle St

Tel: 784-457-1616 / Fax: 784-456-1073

Email: [email protected]

Randys Supermarket,

Grocery Store

Lower Bay St Kingstown

Tel: 784-456-2994 / Fax:784-457-9566

Minimart Tyrell Street. Tel:784-457-2480

Bakery Hospital Road. Tel:784-457-2377

Randy's Cash & Carry Lower Bay Street. Tel: 784-456-2694

Email: [email protected] / [email protected]

Gourmet Foods,

Grocery Store

Calliaqua Box 1678 Kingstown

Tel: 784-456-2983

O'car Bequia Tel: 784-458-3485 / Fax:784-456-2987

Website: www.gourmetfoodsvg.com

Email: [email protected] / [email protected]

Log Enterprises

Rose Place Middle Street Kingstown

Tel: 784-456-2936 / Fax:784-457-1754

Email: [email protected]

Website: www.logsvg.net

Vincy Food Service

Distributors Limited

Paul's Ave P O Box 842 Kingstown

Tel: 784-451-2784

Fax: 784-456-2791

Coreas Hazells Inc Box 122 Lower Bay St Kingstown

Tel:784-456-1201

General Hardware Supplies

Arnos Vale Highway Next to Yvettes Pork City

Tel:784-453-9000

Fax:784-456-4141

Email: [email protected]

Gibson’s Building Supplies

Victoria Park Rd Box 297 Kingstown

Tel:784-456-1725 Fax:784-451-2777

Email: [email protected] / [email protected]

Mariners Hotel

Villa Beach Box 859 Kingstown

Tel:784-457-4000 Fax:784-457-4333

Website: www.marinershotel.com

Email: [email protected] / [email protected]

Appendix II – Sample Certificate of Origin