ST. MARY’S UNIVERSITY SCHOOL OF LAW - Sarita...

33

ST. MARY’S UNIVERSITY SCHOOL OF LAW ESTATE AND GIFT TAX, LW~ FINAL EXAMINATION Professor Cochran Fall Semester 1993 Instructions 1. This examination consists of three pages, pIus this cover sheet. Please check to be sure you have all pages. 2. Your bluebooks and your copy of the exam are due four hours after you pick up the exam. 3. You may use your copy of the Internal Revenue Code and Regulations, the required course materials, and your own class notes and study notes. You may also use a pocket calculator, You may not use other materials, such as library materials or commercial outlines. 4. Please write your exam number on your copy of the exam and on all bluebooks. St. Mary’s University School of Law prohibits the disclosure of information that might aid a professor in identifying the author of an examination. Any attempt by a student to identify himself or herself in an examination is a violation of this policy and of the Code of Student Conduct. 5. You are not to discuss this exam with any person, Doing so is a violation of the Code of Student Conduct. 6. After reading the oath, place your exam number in the space below. I HAVE NEITHER GIVEN NOR RECEIVED UNAUTHORIZED ASSISTANCE IN TAKING THIS EXAMINATION, NOR HAVE I OBSERVED ANYONE ELSE DOING SO. EXAM NUMBER

Transcript of ST. MARY’S UNIVERSITY SCHOOL OF LAW - Sarita...

ST. MARY’S UNIVERSITY SCHOOL OF LAW

ESTATE AND GIFT TAX, LW~ FINAL EXAMINATION

ProfessorCochran Fall Semester1993

Instructions

1. This examinationconsistsof threepages, pIus this coversheet. Pleasecheckto be sureyou haveall pages.

2. Your bluebooksandyour copy of theexamare due four hoursafteryou pick up theexam.

3. You may useyour copy of the Internal RevenueCodeand Regulations,the requiredcoursematerials,andyour own classnotesandstudy notes. You may also useapocketcalculator, You may not useother materials,suchaslibrary materialsor commercialoutlines.

4. Pleasewrite your examnumberon your copy of the examand on all bluebooks.St. Mary’s University Schoolof Law prohibits the disclosureof informationthat might aid aprofessorin identifying the authorof an examination. Any attemptby a studentto identifyhimself or herselfin an examinationis aviolation of this policy andof the Code of StudentConduct.

5. You arenot to discussthis examwith any person, Doing so is a violation of the CodeofStudentConduct.

6. After readingthe oath,placeyour examnumberin the spacebelow.

I HAVE NEITHER GIVEN NOR RECEIVED UNAUTHORIZED ASSISTANCE INTAKING THIS EXAMINATION, NOR HAVE I OBSERVED ANYONE ELSEDOING SO.

EXAM NUMBER

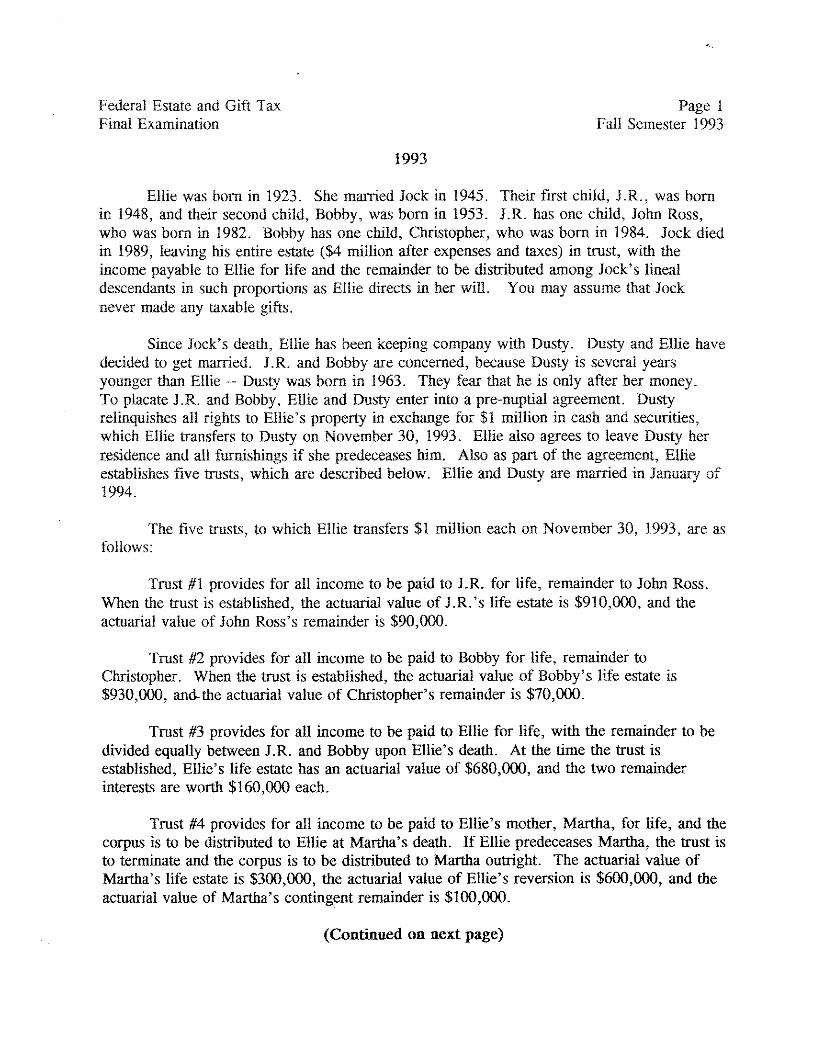

FederalEstateand Gift Tax Page1

Final Examination Fall Semester1993

1993

Ellie wasbornin 1923. She marriedJock in 1945. Their first child, J.R., wasbornin 1948, and their secondchild, Bobby, was born in 1953. J.R. hasone child, JohnRoss,who was born in 1982. Bobby hasone child, Christopher,who wasborn in 1984. Jockdiedin 1989, leaving his entire estate($4 million afterexpensesand taxes)in trust, with theincomepayableto Ellie for life and the remainderto be distributedamongJock’s linealdescendantsin suchproportionsasEllie directsin her will. You may assumethat Jocknevermadeany taxablegifts.

SinceJock’sdeath,Ellie hasbeenkeepingcompanywith Dusty. Dusty and Ellie havedecidedto get married, J. R. and Bobby areconcerned,becauseDusty is severalyearsyoungerthanEllie Dusty wasborn in 1963. They fear that he is only after hermoney.To placateJ.R. and Bobby, Ellie and Dusty enterinto a pre~nuptialagreement.Dustyrelinquishesall rights to Ellie’s propertyin exchangefor $1 million in cashand securities,which Ellie transfersto Dusty on November30, 1993. Ellie also agreesto leave Dusty herresidenceand all furnishingsif shepredeceaseshim, Also aspartof the agreement,Ellieestablishesfive trusts,which aredescribedbelow. Ellie and Dusty aremarried in Januaryof1994.

The five trusts, to which Ellie transfers$1 million eachon November30, 1993, areasfollows:

Trust #1 providesfor all incometo be paid to J.R. for life, remainderto JohnRoss.When thetrust is established,the actuarialvalueof J,R.’slife estateis $910,000,and theactuarialvalue of JohnRoss’sremainderis $90,000.

Trust #2 providesfor all incometo be paidto Bobby for life, remaindertoChristopher. When thetrust is established,the actuarialvalueof Bobby’s life estateis$930,000,and~theactuarialvalueof Christopher’sremainderis $70,000.

Trust #3 providesfor all incometo bepaid to Ellie for life, with theremainderto bedivided equally betweenJ.R. andBobby upon Ellie’s death. At the time the trust isestablished,Ellie’s life estatehasan actuarialvalueof $680,000,andthe two remainderinterestsareworth $160,000each.

Trust #4 providesfor all incometo bepaid to Ellie’s mother,Martha, for life, andthecorpusis to be distributedto Ellie at Martha’sdeath. If Ellie predeceasesMartha,the trustisto terminateand the corpusis to be distributedto Marthaoutright. The actuarialvalueofMartha’s life estateis $300,000,the actuarialvalueof Ellie’s reversionis $600,000,andtheactuarialvalue of Martha’s contingentremainderis $100,000.

(Continued on next page)

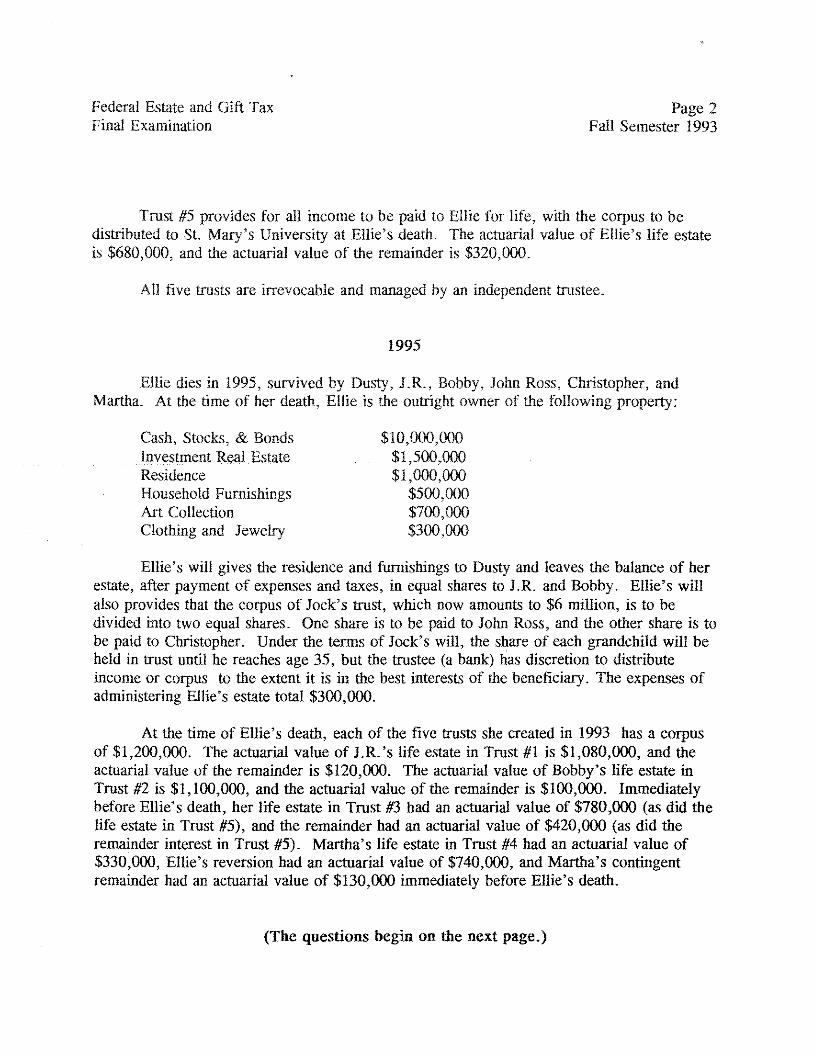

FederalEstateand Gift Tax Page2Final Examination Fail Semester1993

Trust #5 providesfor all incometo be paid to Ellie for life, with thecorpusto bedistributed to St. Mary’s University at Ellie’s death. The actuarialvalueof Ellie’s life estateis $680,000,and the actuarialvalueof the remainderis $320,000.

All five trusts are irrevocableand managedby an independenttrustee.

1995

Ellie dies in 1995, survivedby Dusty, J.R.,Bobby, JohnRoss, Christopher,andMartha. At the time of her death,Ellie is theoutright ownerof the following property:

Cash, Stocks,& Bonds $10,000,000InvestmentRealEstate $1,500,000Residence $1,000,000HouseholdFurnishings $500,000Art Collection $700,000Clothing and Jewelry $300,000

Ellie’s will gives the residenceand furnishingsto Dusty and leavesthe balanceof herestate,afterpaymentof expensesand taxes,in equal sharesto J. R. and Bobby. Ellie’ s willalso providesthat the corpusof Jock’s trust, which now amountsto $6 million, is to bedivided into two equalshares.Oneshareis to be paid to JohnRoss,and the other shareis tobepaid to Christopher. Under the termsof Jock’swill, the shareof eachgrandchildwill beheld in trust until he reachesage35, but the trustee(a bank) hasdiscretionto distributeincomeor corpus to the extentit is in thebest interestsof thebeneficiary.The expensesofadministeringEllie’s estatetotal $300,000.

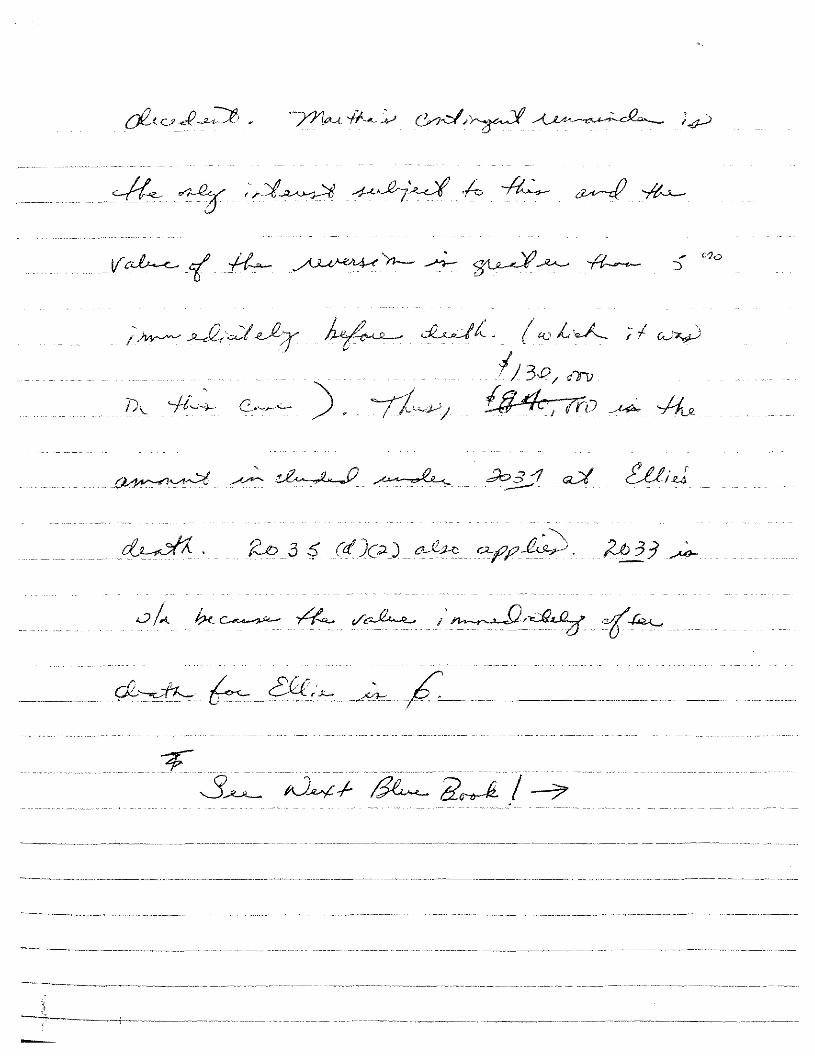

At the time of Ellie’s death,eachof the five trusts shecreatedin 1993 hasa corpusof $1,200,000. The actuarialvalueof J.R.’slife estatein Trust #1 is $1,080,000,and theactuarialvalueof theremainderis $120,000. The actuarialvalueof Bobby’s life estateinTrust #2 is $1,100,000,and the actuarialvalueof the remainderis $100,000. ImmediatelybeforeEllie’s death,herlife estatein Trust #3 had an actuarialvalueof $780,000(asdid thelife estatein Trust #5), and the remainderhad an actuarialvalueof $420,000(asdid theremainderinterestin Trust #5). Martha’slife estatein Trust #4 had an actuarialvalueof$330,000,Ellie’ s reversionhadanactuarial valueof $740,000,and Martha’s contingentremainderhad an actuarialvalueof $130,000immediatelybeforeEllie’s death.

(The questions begin on the next page.)

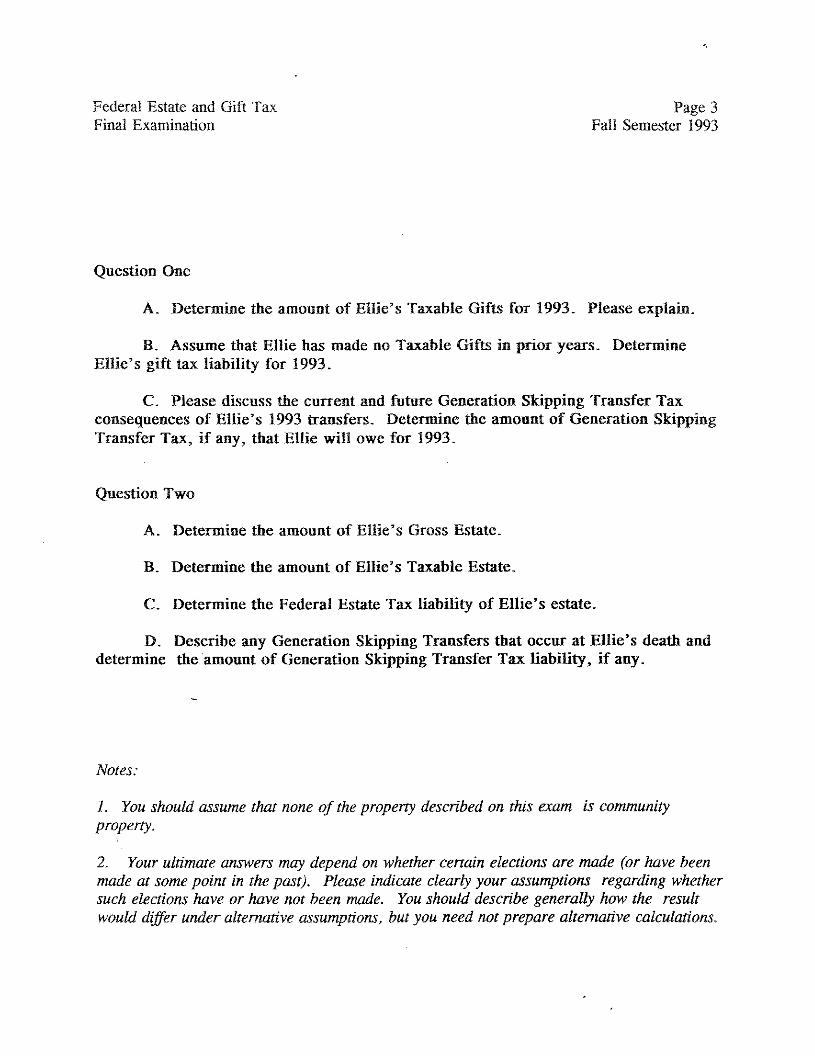

FederalEstateand Gift Tax Page3Final Examination Fall Semester1993

Question One

A. Determine the amount of Ellie’s Taxable Gifts for 1993. Pleaseexplain.

B. Assumethat Ellie has made no Taxable Gifts in prior years. DetermineEllie’s gift tax liability for 1993.

C. Pleasediscussthe current and futureGeneration Skipping Transfer Taxconsequencesof Ellie’s 1993transfers. Determine the amount of Generation SkippingTransfer Tax, if any, that Ellie will owefor 1993.

Question Two

A. Determine the amount of Ellie’s Gross Estate.

B. Determine the amount of Ellie’s Taxable Estate.

C. Determine the Federal Estate Tax liability of Ellie’ s estate.

D. Describe any Generation Skipping Transfers that occur at Ellie’s death and

determine the amount of GenerationSkipping Transfer Tax liability, if any.

Notes:

1. Youshouldassumethat noneof thepropertydescribedon this exam is communityproperty.

2. Your ultimateanswersmaydependon whethercertain electionsare made (or havebeenmadeat somepoint in thepast). Pleaseindicateclearlyyourassumptionsregarding whethersuchelectionshave or havenotbeenmade. Youshoulddescribegenerallyhowthe resultwould differ underalternativeassumptions,butyou neednotpreparealternative calculations.

Federal Estate& Gift Tax, LW8379ProfessorCochranFinal ExaminationFall 1993

Question 1

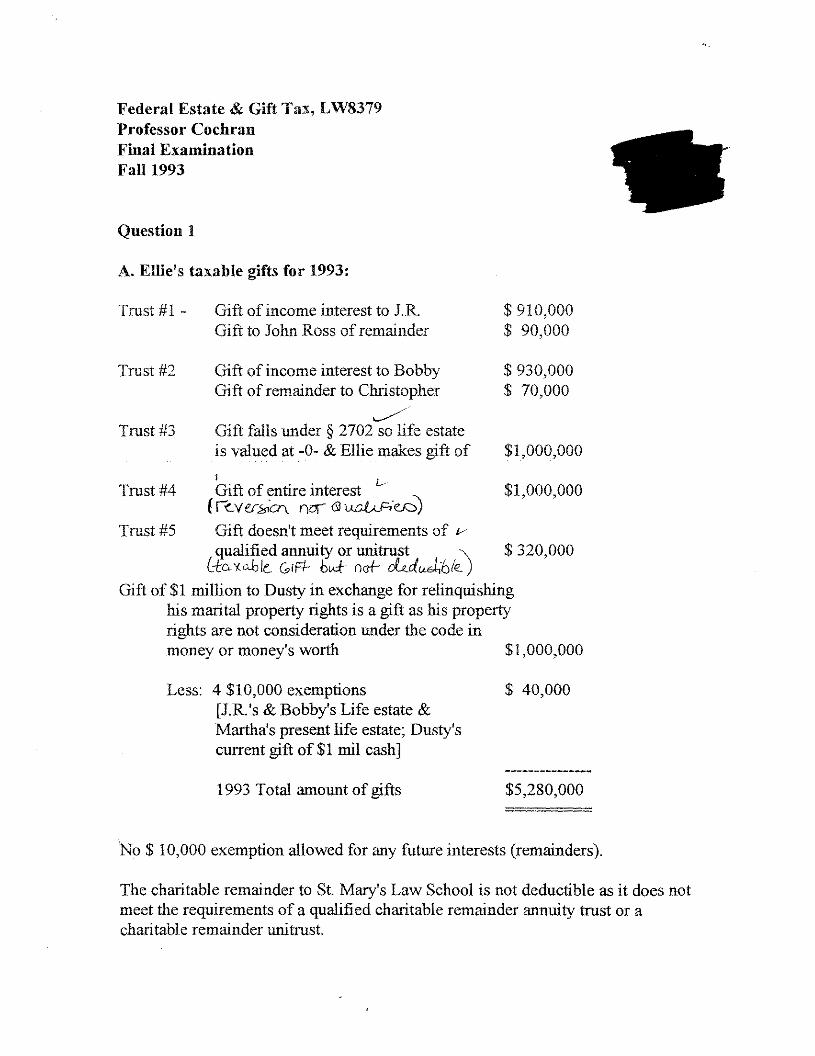

A. Effie’s taxable gifts for 1993:

Trust#1

Trust#2

GiftGift

GiftGift

of incomeinterestto J.R.to JohnRossofremainder

of incomeinterestto Bobbyof remainderto Christopher

Trust#3 Gift falls under§ 2702 so life estateis valuedat -0- & Ellie makesgift of

Trust#4 Gift of entireinterest(rcyt-~-~,~or&

Trust#5 Gift doesn’tmeetrequirementsof ‘—

qualifiedannuityor unitrust(~a~c~GIF~b~naF

Gift of $1 million to Dustyin exchangefor relinquishinghis maritalpropertyrightsis agift ashis propertyrights arenot considerationunderthecodeinmoneyor money’sworth

Less: 4 $10,000exemptions[J.R.‘s & Bobby’sLife estate&Martha’spresentlife estate;Dusty’scurrentgift of $1 mu cash]

1993 Total amountof gifts

$ 910,000$ 90,000

$ 930,000$ 70,000

$1,000,000

$1,000,000

$ 320,000

$1,000,000

$ 40,000

$5,280,000

No $ 10,000exemptionallowedfor anyfuture interests(remainders).

The charitableremainderto St. Man~sLaw School is not deductibleasit doesnotmeettherequirementsof aqualifiedcharitableremainderannuitytrustor acharitableremainderunitrust.

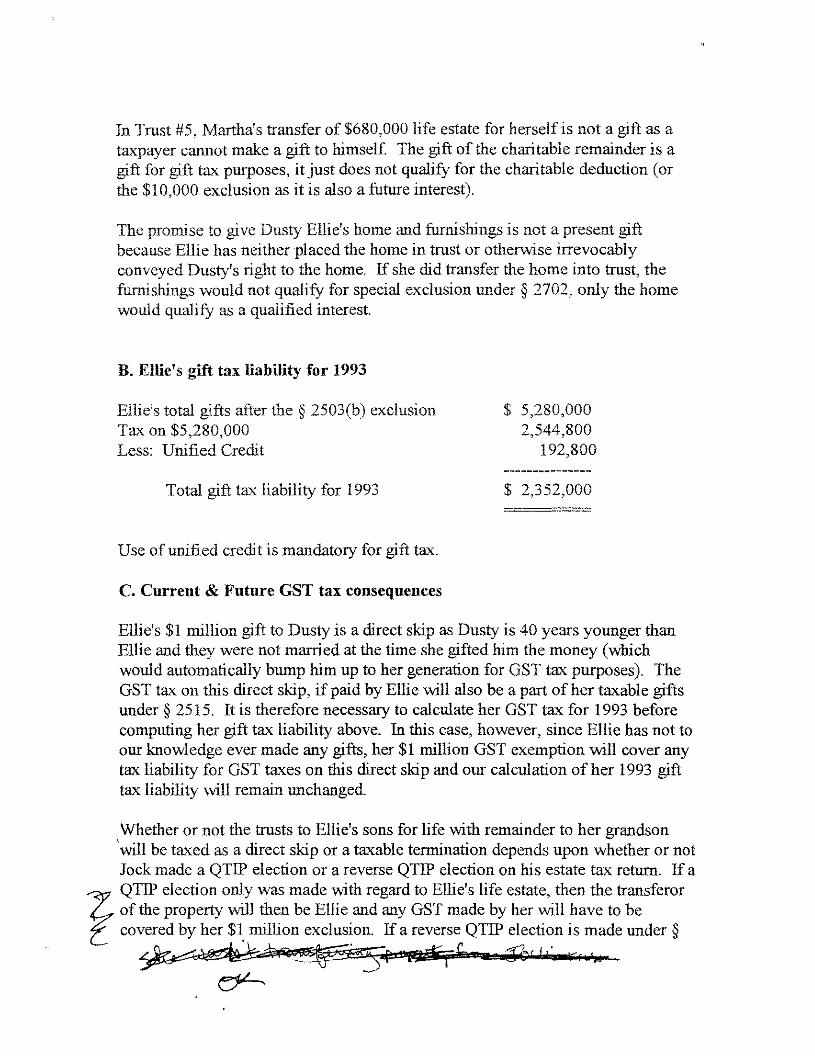

In Trust #5, Martha’stransferof $680,000life estatefor herselfis nota gift as ataxpayercannotmakeagift to himself. Thegift of thecharitableremainderis agift for gift taxpurposes,it justdoesnot qualify for thecharitablededuction(orthe$10,000exclusionasit is alsoa future interest).

Thepromiseto give DustyEllie’s homeandfurnishingsis notapresentgiftbecauseEllie hasneitherplacedthehomein trust or otherwiseirrevocablyconveyedDusty’s right to thehome. If shedid transferthehomeinto trust, thefurnishingswouldnot qualifyfor specialexclusionunder§ 2702,only thehomewould qualify asaqualified interest.

B. Ellie’s gift tax liability for 1993

Ellie’s total gifts afterthe § 2503(b)exclusion $ 5,280,000Tax on $5,280,000 2,544,800Less: Unified Credit 192,800

Total gift tax liability for 1993 $ 2,352,000

Useof unified creditis mandatoryfor gift tax.

C. Current & Future GST tax consequences

Ellie’s $1 million gift to Dusty is adirect skip asDusty is 40 yearsyoungerthanEllie andtheywerenot marriedat thetime shegiftedhim themoney(whichwouldautomaticallybumphim up to hergenerationfor GSTtaxpurposes).TheGSTtaxon this directskip, if paidby Ellie will alsobeapartofhertaxablegiftsunder§ 2515. It is thereforenecessaryto calculateher GSTtax for 1993 beforecomputinghergift taxliability above. In this case,however,sinceEllie hasnottoourknowledgeevermadeanygifts, her$1 million GSTexemptionwill coveranytax liability for GSTtaxeson this directskip andour calculationof her 1993 gifttax liability will remainunchanged.

Whetheror not thetrusts to Ellie’s sonsfor life with remainderto hergrandsonwill be taxedasadirectskip or a taxabletenninationdependsuponwhetheror notJockmadea QTIPelectionor a reverseQTIP electionon his estatetaxreturn, If aQT1P electiononly wasmadewith regardto Ellie’s life estate,thenthetransferorof the propertywill thenbeEllie andanyGSTmadeby herwill haveto becoveredby her$1 million exclusion, If a reverseQTIPelectionis madeunder§

i.:~4h”~ ~II-f .~(Lai~q~~~

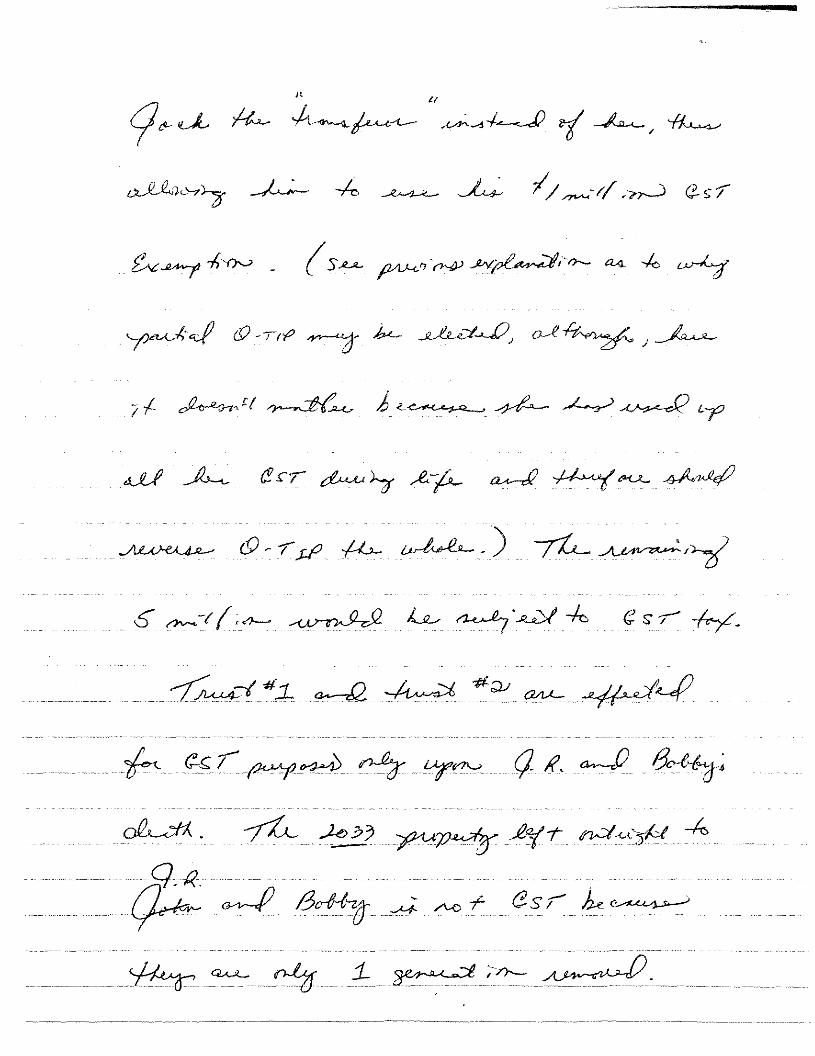

2652(a)(3),Jockwill beconsideredthetransferorfor the portionof his estatewhich heelectedthereverseQTIP, thusenablinghis $1 million exemptionto beutilized to transferwealthto generationsbelow.

At thetime thetrustsarecreated,thetrust isnot consideredaskip personbecauseno personwith a currentinterestis a skip person. WhenJ.R. andBobbythe, therewill bea taxableterminationbecauseall of theremainingtrustcorpuswill bedistributedto skip persons.

BecauseEllie’s only 1993 GST wasthe directskip to Dusty, shewill not owe anyGSTtax for 1993. Shecould, however,allocateaportionof her$1 millionexemptionto thefixture GSTtaxableterminationswhich will ariseoutof thetrustsshehascreatedfor her2 grandchildren.This woulddependuponwhetherornotsomeoftheGSTtaxmight becoveredif JockelectedreverseQTIP for partofhisestateandtherewasactually$2 million of exemptionto be spreadthroughoutthesetransfers.

Onereasonshemight want to allocateherexemptionto otherthanthedirect skip wouldbe to freezethevalueof theGSTat thepresentvalueofwhatassetswereplacedin trustandnot eventuallyincur GSTtaxeson anappreciatedvalueoftheremainderinterest.

NLf~0

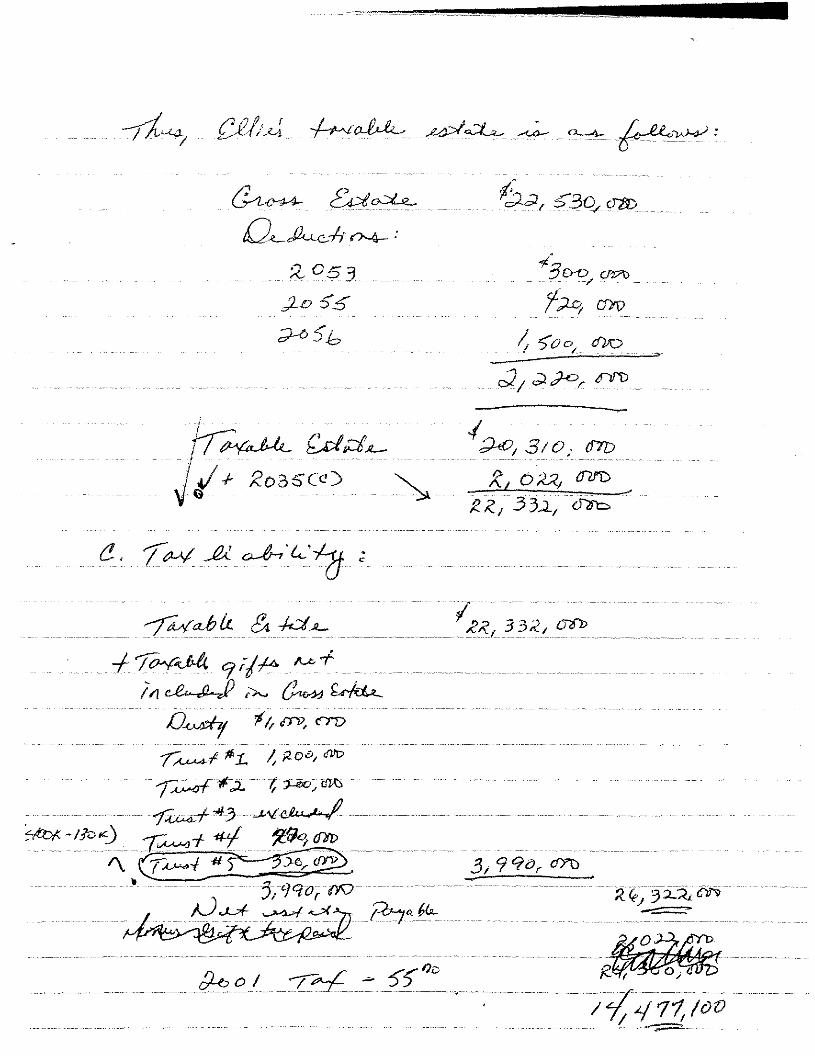

Question2

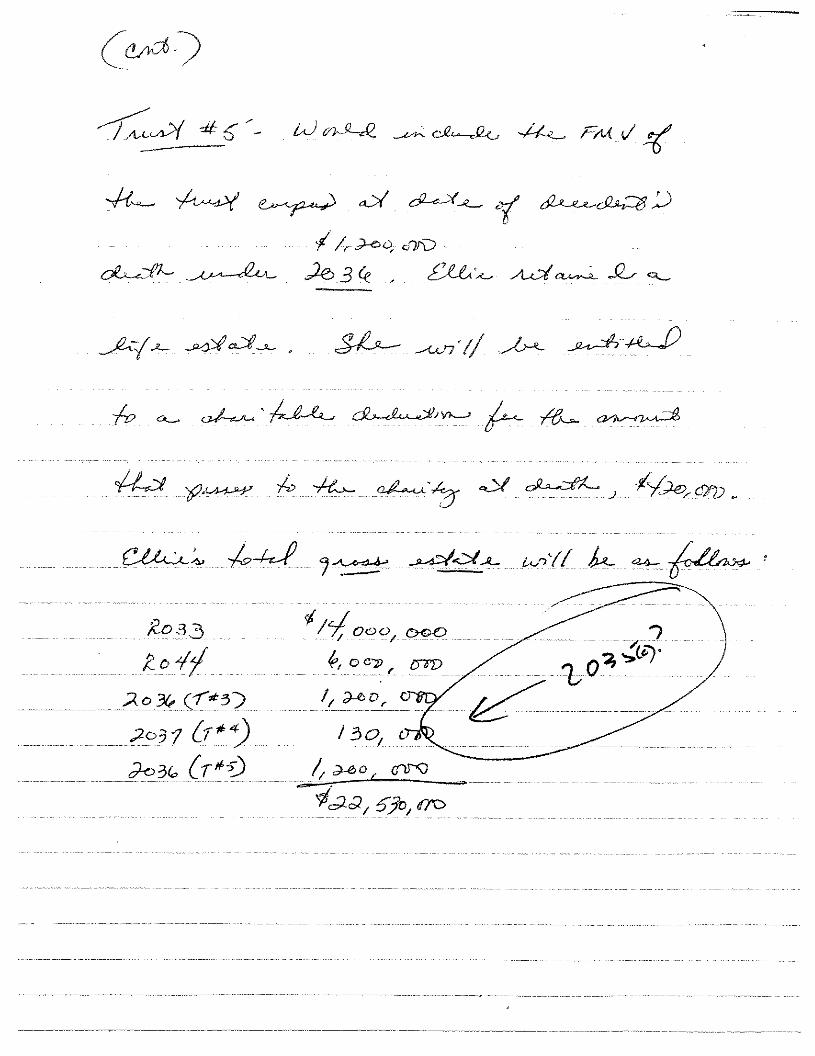

A. Ellie’s GrossEstate

Everythingownedat death $ 14,000,000Corpusof trustfrom Jock’swill

(assuminghe electedQTIP) 6,000,000

Gift taxpaidon gifts within 3 years

of deathunder§ 2035 2,352,000

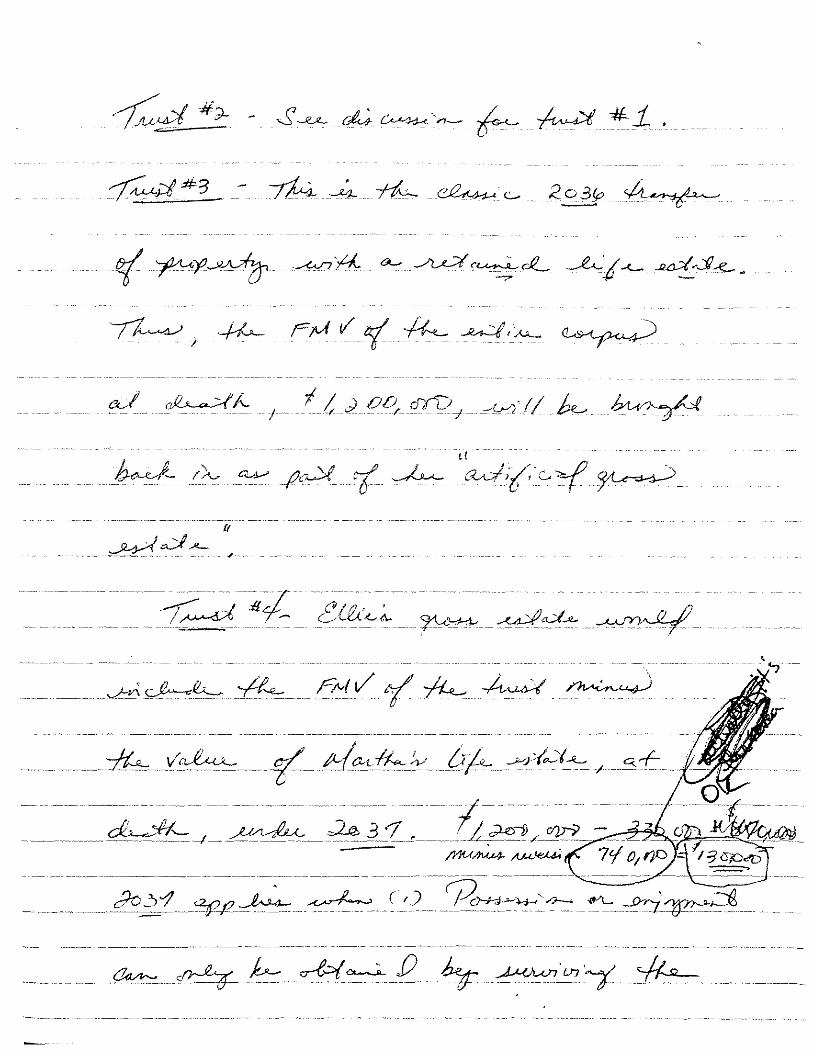

Trust#3 includedunder§ 2036 1,200,000

Trust#4 Ellie’s reversioninterest 740,000 ~ Ztn- ~naub4PA &~~4’&sce4.w~~.tAn

Trust#5 ~2O3G 1 200 000

Total grossestate $ 25,492,000

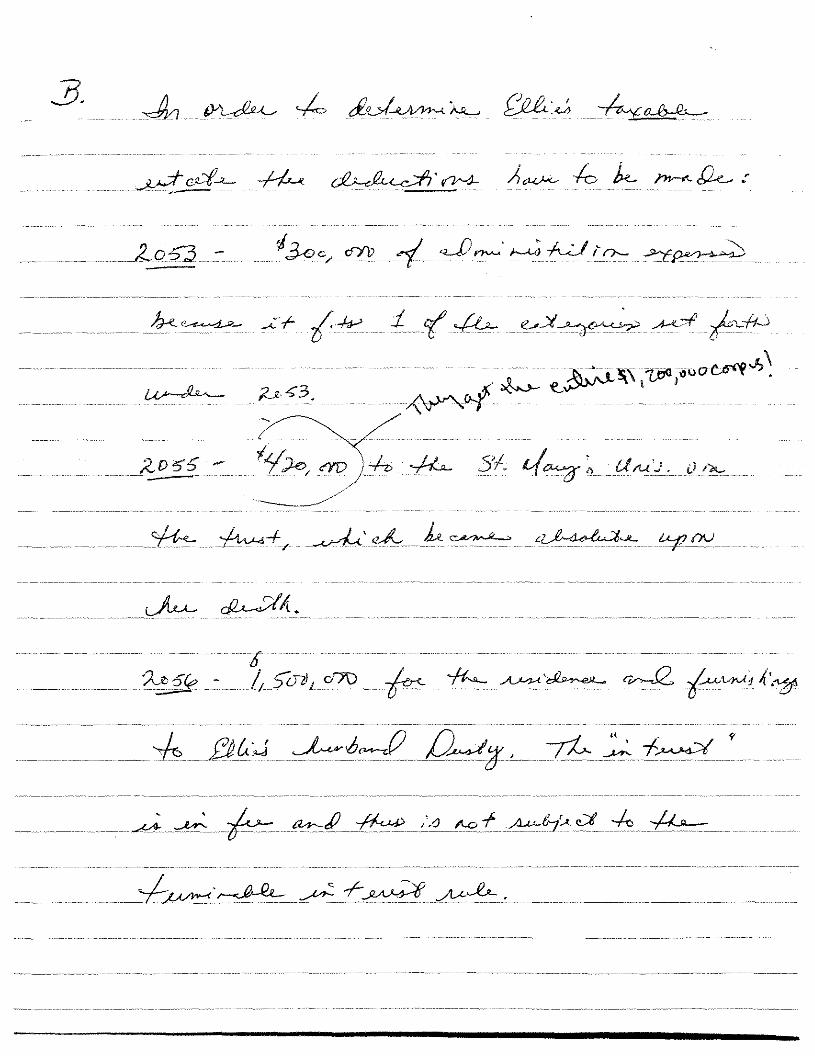

B & C . Ellie’s taxableestate& tax

Grossestate $ 25,492,000Less: Expensesofadministration 300,000

Charity deduction 42%8’Otr l1tco,~o~.iRn.. e4~Cat?!)Marital deduction 1,500,000

TaxableEstate $ 23,272,000

Plus: post-1976taxablegifts not

includedin grossestate:Trust#1 ‘¼c0Trust#2 F0vUOöö ~GifttoDusty i,.oeotnt tkSoTrust#4 gift of $1 million less

the$740,000reversionwhichis includedin estate 260,000

Total amountto computetax $ 26,532,000

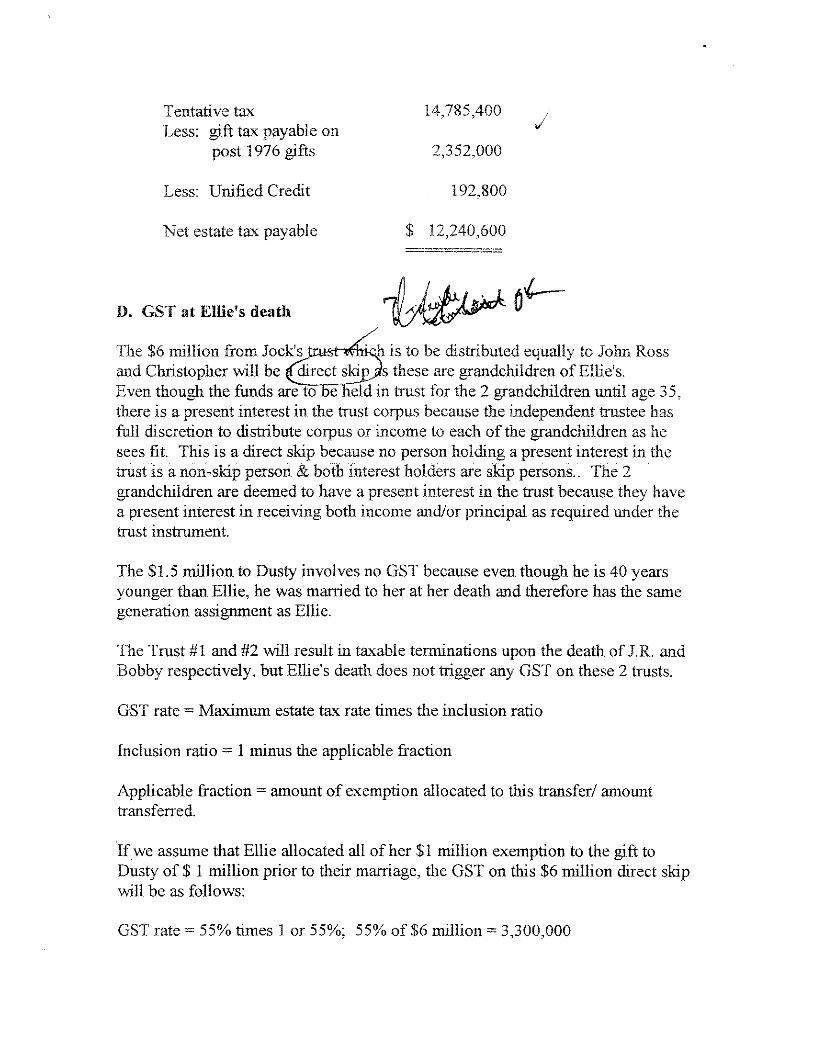

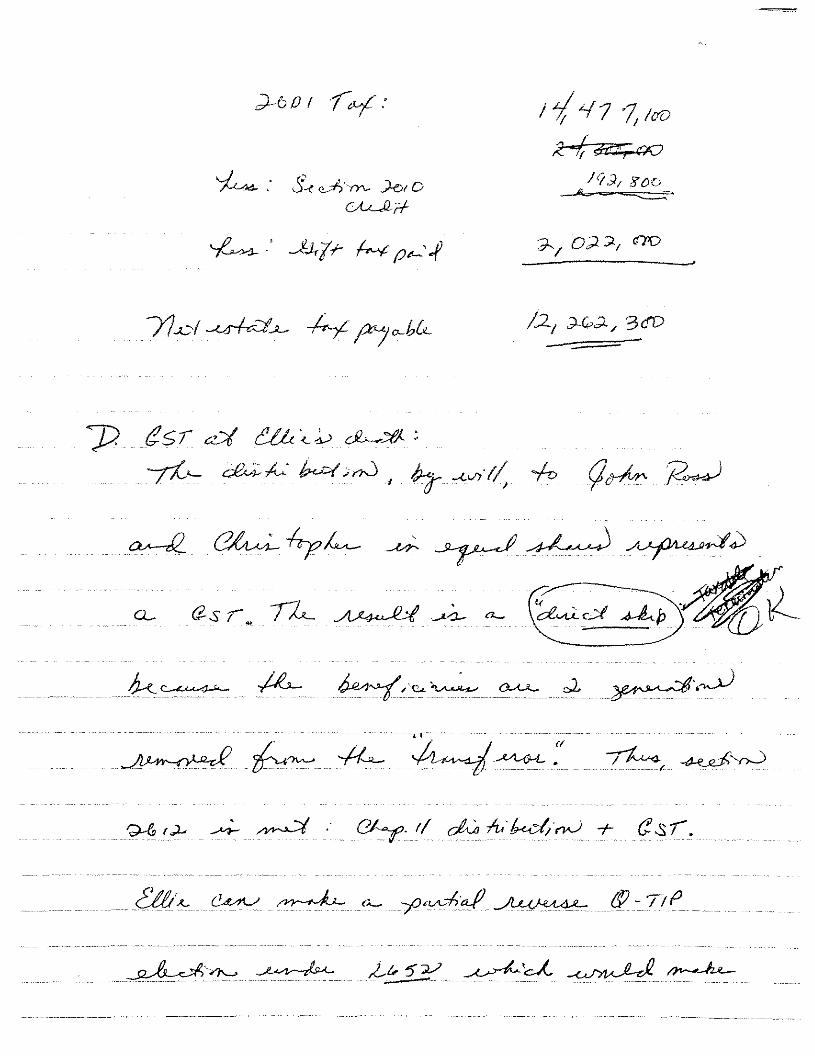

Tentativetax 14,785,400Less: gift taxpayableon V

post1976gifts 2,352,000

Less: Unified Credit 192,800

Netestatetaxpayable $ 12,240,600

~D, GST at Effi&s death ~.1

The $6 million from Jock’s is to be distributedequallyto JohnRossandChristopherwill be directski thesearegrandchildrenofEllie’s.Eventhoughthefundsareto e eldin trust for the2 grandchildrenuntil age35,thereis apresentinterestin thetrust corpusbecausethe independenttrusteehasfull discretionto distributecorpusor incometo eachofthe grandchildrenasheseesfit. This is a directskip becauseno personholdingapresentinterestin thetrustis anon-skipperson& bothinterestholdersareskip persons..The2grandchildrenaredeemedto haveapresentinterestin the trustbecausetheyhaveapresentinterestin receivingbothincome and/orprincipalasrequiredunderthetrust instrument.

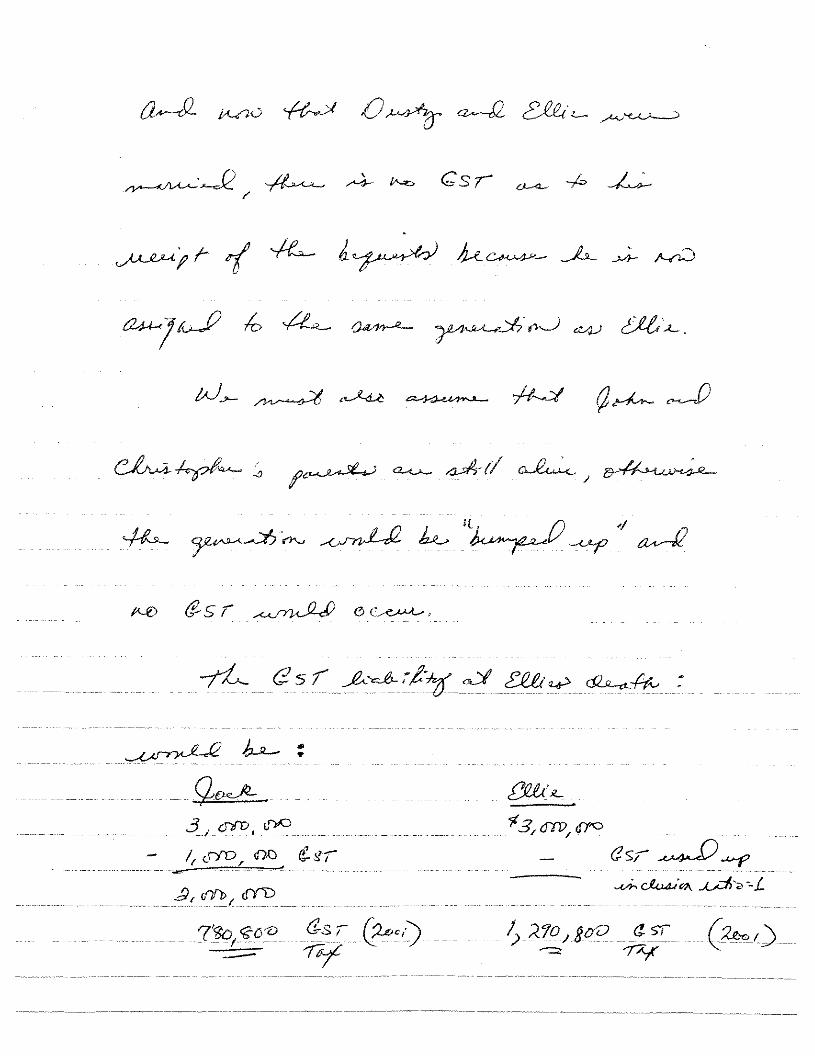

The$1.5 million to Dusty involvesno GST becauseeventhoughhe is 40 yearsyoungerthanEllie, hewasmarriedto her at herdeathandthereforehasthesamegenerationassignmentasEllie.

TheTrust#1 and#2 will resultin taxableterminationsupon thedeathof J.R. andBobbyrespectively,butEllie’s deathdoesnot triggeranyGSTon these2 trusts.

GSTrate = Maximumestatetax ratetimestheinclusionratio

Inclusionratio = 1 minustheapplicablefraction

Applicablefraction= amountof exemptionallocatedto this transfer!amount

transferred.

If we assumethatEllie allocatedall ofher$1 million exemptionto thegift toDusty of$ 1 million prior to theirmarriage,theGSTon this $6million directskipwill beasfollows:

GSTrate= 55%times I or 55%; 55%of $6 million = 3,300,000

Theapplicablefractionwouldbe zero becausethere‘would be no exemptionleft.Pleasenote,howeverthe previousdiscussionregardinga reverseQTIP electionJockcouldhavemadein orderto fully utilize bothhis $1 million exemptionandEIlie’s $1 million exclusionfor GST. Theamountof exemptionwould dependuponthis andwhetheror notEllie electedto alsoallocatesomeofher $1 millionexemptionto thefuture taxableterminationsin the2 trustsshesetup for herson’swith remaindersto her grandchildrenwhile shewasalive.

A, L t&AJ 5A/* lb a~~?dt~4~J.t ~iZ&’4 ceJUt.t~ 7’

bit ~ c~ia~ta-ct ~) Ic P-’-c4a~ XZv.

ac, 1Q93. . ,.&aw~ ~ ~ °-t

~ 4~~lf~ /e’~ ~ ~Jc~ C~4~

.~),, ~ ~ a ~

~

~ ~ ~ “~4~ 4t~4

~ J~, H~tz~-~~

~ ±P.

~ if,,,

~ ~ . -

“~ __ ~±~±

‘ • r::, :‘ ..:c, ~?C1t~$

~ 4~’~ AC’~-~

- t~j~Dr’ */ ‘~*±~:.

‘~ __ ~-~- ~aP~

- - - -:

-T2L1 rl4sL 1/4 ~ 4&~ .tLa kO~..a4y~ru?~~LP Ak_ ~._.

.Y~ ~

~‘~4t tc~Lc/L~ at~c7’

.A.4A7 .j~Ltcb&.tL ~c/A-t ~/ aé~cQ ,4cAa.. ~

c -

~ ~ .......... .

__~__~______2._s~~, A.t~j~c2~’~ ~

~ ~4~’.kco.. ~ ~

~ ~ ~

~ 7~4_~f/~Ac~

~ ~

~

r~ r~i Ce4~Cf%..t~~ ~ti~E

~ WIL i4t>c &~~r4~

-7~TZ~44J_*3T. 77~L ~ ~ z~.

cvz~. %/$- 4 ~tt.. ~ w.~.c&~-c&L4t

~ .~.. ~ 7’~ ~

.~Z/t is’. (~cL~ 547~

.~4C&/4-). ,q!w~V~, ~7O~-

7jtu~ ~ P~’O~:~i~ ~

rL ~

L~ J~A; 7 ~ra~Q

~ .214........q ~ R....~.

-~

~ .7L~ b-ce c,..-t~e2....4

C4j~Q~CAa4 vYe~~ __

~ /,f0 ~

~, ,a. ~Q 4 c,Lja~ c4~j,,,~ ~

~ ~ ~ ~7F, ~ a,

V‘‘V ‘ -

~4~t~c&. ~zZ~c/#S~

~ ~i7/,”~.t#T ~ ~

~ ~ ~.

~ ~ ..-~-‘~------ ~Ca __

~ ~

~~*~&L44. .~T’), TLa- ,.1-L_

¾-41c~~-

/ C, 73 ~ ~.

7>~c~v,flflD

If c~( c~ ~ . 9 £

1, cn, lit , 7~J ~ ~ 6~2IzpL~~

~ i-/c~4~

zEuS if ~,‘i’ ~ -p. ___

7” ~i/~ ,r~thZc~,CL~t4)~ ~7Z &4&*~~J~4.C

& ~ Az~

7~,g(6) - at€-ac~~d2X~a ui’b ~fi1

(Ct’.ciAr1’~*

..fl~.’, ~ ~. ~ ~‘-

j~ ~ ~4. ~

~ 9L~~ ~

t~4t~*i~&~P ce&~

~0 frt ...~

~CtkO,crfl~ ‘ “‘‘ “ ‘

~t,.(ef4~ot ~.. 7~-~ca4-& .

~3.~ —

I~ ~ caw f~ccJt 444~144~

/,a~?c’,g~

Qcfl) Ztoue) ,J~.~.720.4.jl4Qn~-7~/

Z605 u~j;~ ~

~ d.’i° ,~

-ô-~t c.4.tW~aS~ ~t44~fl4~ ~L/~€ 81&2~ .,L4Z fl~~A

‘/.-~, ~ r”~ ~__ / F

Ce.. iZ, ~.$L~Jd?s1~~ 7’ ccl c&.,sbà ~ j~~.,&M(s~c ‘Ita.,.

~ Q’S/ ~ç)~/ y~uvTX7fl~-

,_____,,_,_,,,,t/’t,_ft~&y?~ c~.-’~--.tL~fr Z~~Q..-P~e~~t~-)

~ ~ .~ ~, tJ.~jS ~‘ ~.

‘~‘ ~3~L:~& ~ ~ )L~

~ 4....’. ~ ~-.

-4.’,’-,’-’ ~ ~

~ ~~i:

~- 2 04 fl~- a

tM+~. ~tZ~)~yg1~) ~ ~

~. ~_(. ~

~ __ .. ~

f24~S~4aq.~. ~

.-.----~~-..-,---(.~- ~ ~

.

~

~ .~ ~.

p aA-t,Q ~ ~i ‘t~ I

___ ____ ~

- ~YZD7~ ~ U~ ..4&t... .4a—~-

i~cc-&~4l czc&iVt. ‘~&~ca-6.&7~&j~2tn.— /)~

~ ~ ~. i~ CC7 ~i~ç’~ ~

4~ ~tt~

~ ..A2t1 -~~Péucnt~¼&

1~cjtl tJ~ C~~sr c6~y2~’kca4aa_-

~ ~ ~ ~1jø

~, ~- -..--~-. ~ 4~ni~

.4-f .‘~ ?,}td_f~..

~ IC C1&~ /913

__ e~’ ~

iD~Jj se~

,‘ rn’1 (WI)

- ‘~ ‘~‘~9Jds&/973

~ ~

7 ~L ~

4 //,a~,c7t K ~

~ ~, A ~ ‘~ ~ ~

-Y ~ ~ __

~ ~T9) /.~ ~

&~

~4 ~

?O5~(6~) ~

~‘r ~ ___

~H: ~ ~

s r

~- 9-r~~o~ ~

±1.1’ ~ ~ ~4~r

~ ~

4et~.q ..Ac (~Lk:i ~ ~ IcOC~) 3L7

- -~ __ ‘I -

~s4ñ~- ~2

A ~ 4to~

/c/ ~ ~

~/~~jL Ze33 ~J42

-hC~.. ~ ~ .

~ei~c’~~

r�~/

v ~ ~v~w) ~ Z3 , ,aM ‘::, ~&ACfi~

~ ~ ~ •r~f’~,~

_ ~ ~ ~-.. /~)

~ ~~77

~ ~

,r~~±!2~

‘- - ~w(~2’-, ~tT ~ ‘r~~

ii :A~7~7H~

,,,,.....,9¼,,., ,~-4t~y ~cec -t~ >~~<C ‘LA’ ~

~

e~c~~, IJ.Q ~

I ~ ~

.~‘ e&~4( d2’~c~~’~~C-~4~-~ ~4~& J) i~

~

~ ji~Q 7~ L~

~ ‘~ ~

‘-l”- -‘1’I;I’7~.~

~~~u-flo14., ~

~~&~-$

711, 11~’~11‘~‘~J ‘177111117

- 1~?&A..~ JL~Q a- ~ ¼

I0~ £& ac~~1~a

- ¶~-~-~ ‘~- ~ £2 , , - -

4 ~ ~ .~ ~ . , —

~ ~ ~ ,

L~t ~, __ ~

4 Q~c2~~JoJtc. , , ‘

P’”~”~7I11~11’11I1117”7171.’1”7171I1fI

a ~ ~ r’ ~

~ n*C((~ (~tt~ i1 ____

stt~( 4j t3__txz 514ca{ttcg. tAf?VtQ c4

~ ,-~4c-~~ ~n~-~_J ~

3 .

- ~°86dYO~0

j/ ~ie~rp{9A~

J_6Es~ vt 7LC7~’ 7 c1LI.t__ )/*~

Rc9ccd)(~j ~%, ~ 2o36cc~

~ ~1~i/1 ~.

,tbI

floe,’ ~ ,J.~ ~

K.

774~/~~-SCc~’flC74A~€*j.

~

-~ -4~-t~-~%~ &~Cc. £a~i.c -

.7/,, ~“x~’-..’~’~ ~

~ ~

~L

~ ~t

~ ~‘:‘~:71”~I ‘,~‘HI~’1”~’,“

,,e(e~t~~ -

~-.‘-‘~- .~~t,___ ‘~‘-~-~ ~_,___,zz±~ ,~ -

/

-

~ ,-~±tJ ±2L. J±~±1trff i~±4T~L,,--

- ‘Tfl14t~ ~ ~‘ ~ ~

~ *-~7’~4/t //A.: cz~c~

- (~ L~ ,i ~

1/3~,c’rv

P~,H~-c~c~),~rL~ i7~7a~/J~

~ ~ ~ ,~ ~

H ~,“, .,~ ~ ~ ~ ~

2~-~/ —~

. ___

(~.)

A) ~ ~ ..A<~FM V

tt~cfa~) aJ~/ ~

~ a2SB Ce t-t&’-c~ ‘tz2jctc~ £~

~cf~ ~ - ~ ~i/ ~

~ ~ ~ ~J~, ~<, ~e ~ .f½4cn7~

CZ4~C~4-~-~-7-~c±

£o33 , ~

~9~7~ff4),,

~ -~

1c2c?/ 63o, Ct

3- ___,,,,J~ ~ ~

~‘n~

~ C~

~ ~ t ~‘q. cE~4~flo ~4y~

tt-c-- ,~&�‘3. ~ A&J.- t

~ ~ I;,.L.,11,,’~1H,It,I

~___±t ~

cul&-~uu1o

I1”1H~’1..1’~H’~1” ~ ,~J. ~ ~ ~ cHH1’H1~I~1,,;~‘,

~

ftAIOL4 ~I ~~-

6~Lc-~4- Lctct?.~ �30, cY�t

O)y

‘5oc~ d2v

~2,~1o~flrD

2o36Cc) N ~ -.2Z/ 33i, J2rt~

~

-

-- - j7~a ~7//~ ,A~

in i~

~ %II~dlv, cI~

~ /,goo,dVD -

- ~

~ i~,iH~1~i~~q7,/oV

~L4~:

~ .JJqfr

p~ /2, ~ 3eV/

72, C�r ~ ~ae~ ~

7X~-. c é~c(n3, /~o~j/ ~/v 9~

n’ ~s r ~,:; C’,’ ___

. It~ e’e~p~~1 ~

“11.H.’~’,.,..IL~ “~

~ &(ap.f/ ~

- ~ 7

~~-“- ~-‘-----

/~_ ~ ‘/ ~ q ~ / (1..’

-4 g2’-~ -~ ~/~-‘7,?~ ecr

(s~a /2’t~~“r’ j7rearli°- aAL

~ -~ ~ ~ L~~1 0e~ I

7 / ~ ft ~ A ~ ____

J~ __ ~

~AWtMLc- &-tjjO ~

6 ~t~’- ~fi~Q £~ ~~cr

~ q~c,,. ~ ...

~ ~ tc a

-‘-“--‘--‘--~“-“‘~ ‘--~- ‘~“-:-“-“— ~t,_t__,__.,____,_,_,_,,_,,,_

a &e~-

J4~ A- i~ Csr ~ ~

~ 1’ It~ trJ>&

-.3,

~ 4~4(7 ~ ~

~ ~ ~

,t.e ~cr ~ Sc~twt-~

~L8srA~’~ &at~

~

3,crn2,ut~,, ,,~zøW/d~?.. .. , ‘

—.

4,tfl,dYt

__ _ (2eoi)

-~ lv