St. Clair County IL v MERS

26

IN THE CIRCUIT COURT OF THE TWENTIETH JUDICIAL CIRCUIT ST. CLAIR COUNTY, ILLINOIS ST. CLAIR COUNTY, ILLINOIS, BY AND THROUGH ITS STATE'S ATTORNEY, BRENDAN KELLY, AND ITS RECORDER OF DEEDS, MIKE COSTELLO, Plaintiff, vs. ) ) ) ) ) ) ) ) ) MORTGAGE ELECTRONIC REGISTRATION ) SYSTEMS, INC.; MERSCORP, INC.; ) BANK OF AMERICA, N.A.; CCO MORTGAGE ) CORPORATION; CITIMORTGAGE, INC.; ) CORINTHIAN MORTGAGE CORPORATION; ) EVERHOME MORTGAGE COMPANY; GMAC ) RESIDENTIAL FUNDING CORPORATION; ) GUARANTY BANK; HSBC FINANCE ) CORPORATION; SUNTRUST MORTGAGE, ) INC.; WELLS FARGO BANK, N.A.; WMC ) MORTGAGE CORPORATION; BANK OF O'FALLON; ) COMPASS MORTGAGE, INC.; FIRST COLLINSVILLE) BANK; FIRSTCO MORTGAGE CORPORATION; ) FIRST COUNTY BANK; MID AMERICA MORTGAGE ) SERVICES OF ILINOIS, INC.; MORTGAGE ) SERVICES III, LLC; MIDLAND STATES BANK ) PEOPLES NATIONAL BANK N.A., ) COMMERCE BANK, REGIONS BANK, AND ) UMB BANK N.A., ) Defendants. COMPLAINT ) ) Case No. COMES NOW the Plaintiff, by and through the St. Clair County State's Attorney, and for this cause of action against Defendants, states as follows: 1

-

Upload

wonderland-explorer -

Category

Documents

-

view

820 -

download

0

description

St. Clair County, iL State’s Attorney Brendan Kelly’s office sued the banks in May for allegedly engaging in fraud and deception by evading requirements to file documents with the county’s recorder of deeds when home loans were bought and sold by lending institutions. Banks and lending institutions created Mortgage Electronic Registration Systems (MERS), a holding company, which according to the lawsuit, resulted in a shadow recording system. St. Clair County case number 12-L-267

Transcript of St. Clair County IL v MERS

IN THE CIRCUIT COURT OF THE TWENTIETH JUDICIAL CIRCUIT

ST. CLAIR COUNTY, ILLINOIS

ST. CLAIR COUNTY, ILLINOIS, BY AND THROUGH ITS STATE'S ATTORNEY, BRENDAN KELLY, AND ITS RECORDER OF DEEDS, MIKE COSTELLO,

Plaintiff,

vs.

) ) ) ) ) ) ) ) )

MORTGAGE ELECTRONIC REGISTRATION ) SYSTEMS, INC.; MERSCORP, INC.; ) BANK OF AMERICA, N.A.; CCO MORTGAGE ) CORPORATION; CITIMORTGAGE, INC.; ) CORINTHIAN MORTGAGE CORPORATION; ) EVERHOME MORTGAGE COMPANY; GMAC ) RESIDENTIAL FUNDING CORPORATION; ) GUARANTY BANK; HSBC FINANCE ) CORPORATION; SUNTRUST MORTGAGE, ) INC.; WELLS FARGO BANK, N.A.; WMC ) MORTGAGE CORPORATION; BANK OF O'FALLON; ) COMPASS MORTGAGE, INC.; FIRST COLLINSVILLE) BANK; FIRSTCO MORTGAGE CORPORATION; ) FIRST COUNTY BANK; MID AMERICA MORTGAGE ) SERVICES OF ILINOIS, INC.; MORTGAGE ) SERVICES III, LLC; MIDLAND STATES BANK ) PEOPLES NATIONAL BANK N.A., ) COMMERCE BANK, REGIONS BANK, AND ) UMB BANK N.A., )

Defendants.

COMPLAINT

) )

Case No.

COMES NOW the Plaintiff, by and through the St. Clair County State's Attorney,

and for this cause of action against Defendants, states as follows:

1

PARTIES

PLAINTIFF

1. Plaintiff, St. Clair County, Illinois, by and through its State's Attorney

("State's Attorney"), Brendan Kelly, and its Recorder of Deeds ("Recorder of Deeds"),

Mike Costello, has its govennnental headquatters in the City of Belleville, County of St.

Clair, State of Illinois.

2. The Recorder of Deeds is the duly elected officer charged with the duties

outlined in 55 ILCS 5/3-5001, et seq., which includes the collection of all fees due

pursuant to 55 ILCS 5/3-5018 and 765 ILCS 5/28. A portion ofthe fees collected by the

Recorder of Deeds office are used by the Plaintiffto maintain a publicly accessible

repository of public land records reflecting those who assert an ownership interest in

lands within St. Clair County, Illinois and the remaining portion of the fees are

transferred to the Comity's General Revenue Fund to provide essential public services.

3. The Recorder of Deeds is also charged with promoting the public policy of

transparency in public records and promoting the central common law tenants of property

ownership law that has been in place for 1 OOs of years, namely a recording system that

(a) gives persons the opportunity to review the public records to ascertain the status of

title to pro petty, (b) provides an impottant check and balance in the preservation of

property rights, and (c) provides a public, enduring, authoritative and transparent record

of all land ownership.

2

4. The State's Attorney is authorized to prosecute civil claims of unfair and

deceptive practices such as those alleged herein pursuant to 815 ILCS 505/7(a) and 815

ILCS 510/1(5).

5. State's Attorney is also authorized to commence this civil action pursuant 55

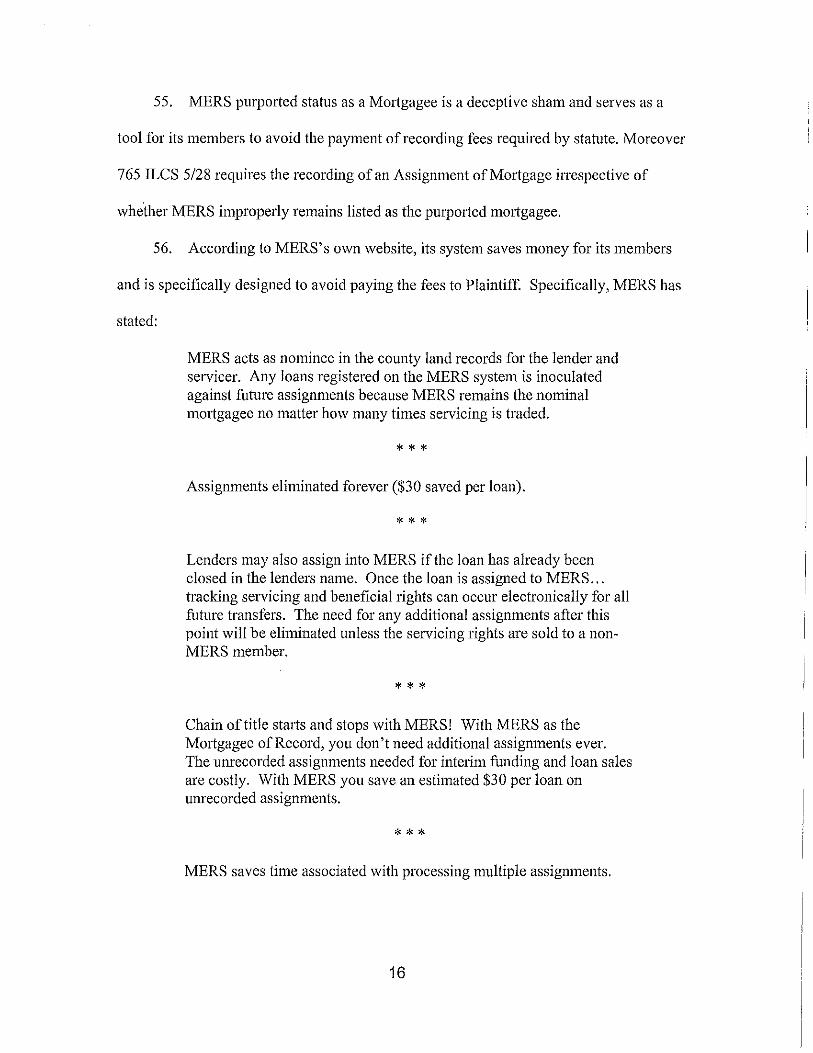

ILCS 5/3-9005.

MERS

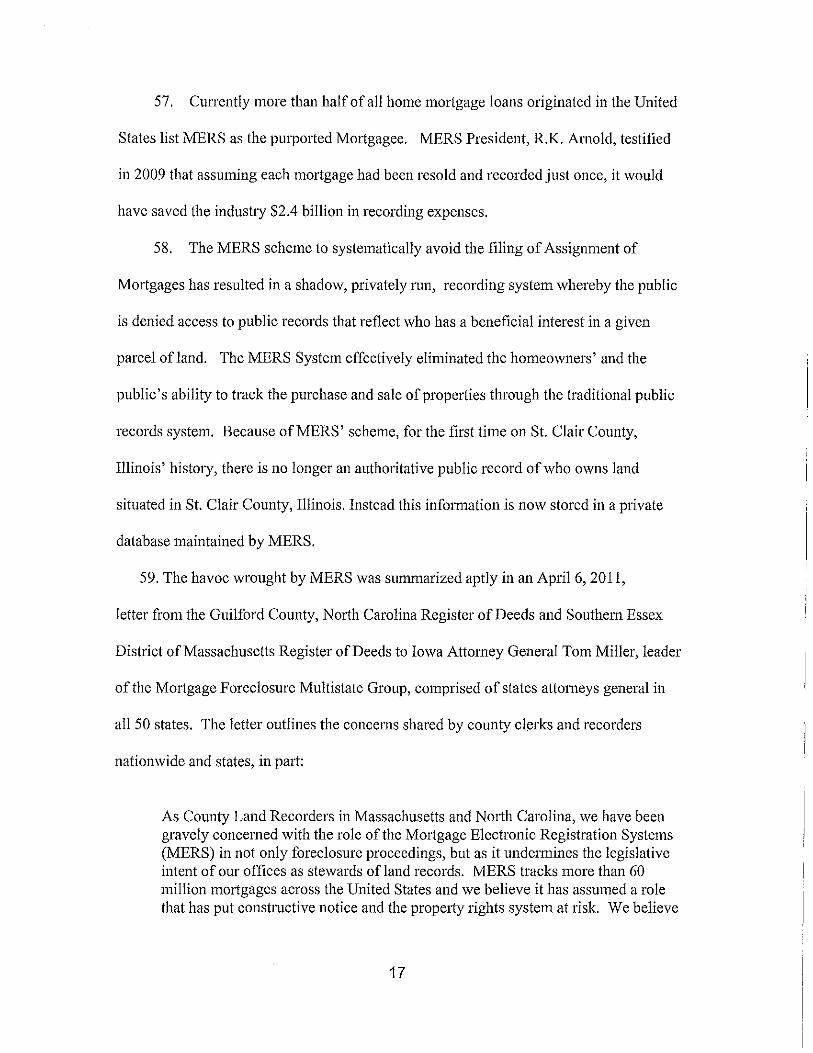

6. Defendant, Mmtgage Electronic Registration Systems, Inc. ("MERS"), is a

foreign corporate entity created in or about 1988, set up under the laws of Delaware, and

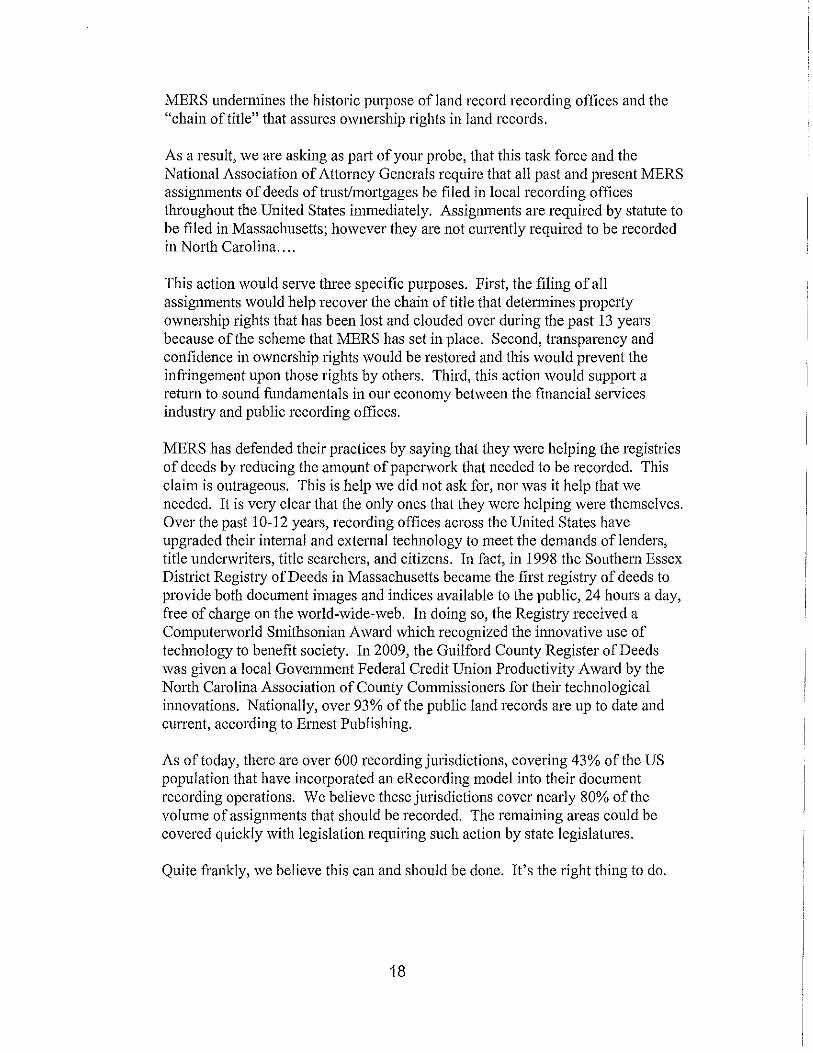

is a national organization that conducts business in the State of Illinois. MERS has its

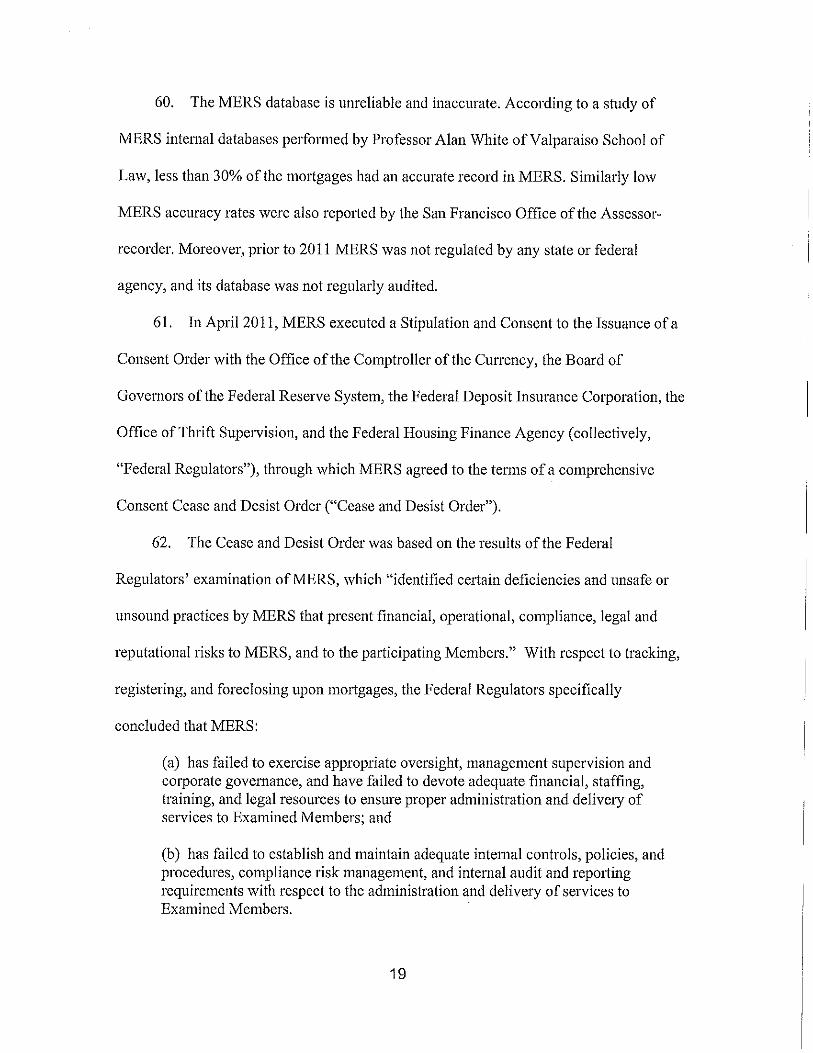

principal place of business located at 1818 Librmy Street, Reston, VA, 20191. The

designated registered agent is Genpact Registered Agent, Inc., 1901 E. Voorhees St., Ste

C, Danville, FL, 61834. Defendant, Merscorp, Inc., claims to be the operating company

that owns and operates the MERS System, and has its principal place of business located

at the same address, 1818 Librmy Street, Reston, VA, 20191.

MERSSHAREHOLDERS

7. Defendant, Bank of America, N.A., is a foreign corporate entity which,

according to www.mersinc.org. is a shareholder in MERS. As a national organization, it

conducts business in the State of Illinois, and it is therefore appropriate that it be required

to defend this suit in this Court. Defendant is a foreign corporation that is set up under

the laws ofDe1aware, with its principal place ofbusiness located at 100 Nmth T1yon

Street, Charlotte, North Carolina 28255.

3

8. Defendant, CCO Mortgage Corporation, is a foreign corporate entity which,

according to www.mersinc.org, is a shareholder in MERS. As a national organization, it

conducts business in the State of Illinois, and it is therefore appropriate that it be required

to defend this suit in this Court. Defendant is a foreign corporation that is set up under

the laws of Ohio, with its principal place of business located at 10561 Telegraph Road,

Glen Allen, Virginia 23059.

9. Defendant, CitiMortgage, Inc., is a foreign corporate entity which, according

to www.mersinc.org, is a shareholder in MERS. As a national organization, it conducts

business in the State of Illinois, and it is therefore appropriate that it be required to defend

this suit in this Comi. The designated registered agent is CT Corporation System which

is located at 208 S. LaSalle Street, Ste 814, Chicago IL 60604. Defendant is a foreign

corporation that is set up under the laws of New York, with its principal place of business

located at 1000 Technology Drive, MS 140, O'Fallon, Missouri 63304.

10. Defendant, Corinthian Mortgage Corporation, is a foreign corporate entity

which, according to www.mersinc.org, is a shareholder in MERS. As a national

organization, it conducts business in the State of Illinois, and it is therefore appropriate

that it be required to defend this suit in this Comi. The designated registered agent is CT

Corporation System which is located at 208 S. LaSalle Street, Ste 814, Chicago IL

60604. Defendant is a foreign corporation that is set up under the laws of Mississippi,

with its principal place of business located at 5700 Broadmoor, Ste 500, Mission, Kansas

66202.

11. Defendant, EverHome Mortgage Company, is a foreign corporate entity

which, according to www.mersinc.org, is a shareholder in MERS. As a national

4

organization, it conducts business in the State oflllinois, and it is therefore appropriate

that it be required to defend this suit in this Court. The designated registered agent is CT

Corporation System which is located at 208 S. LaSalle Street, Ste 814, Chicago IL

60604. Defendant is a foreign corporation that is set up under the laws of Florida, with

its principal place ofbusiness located at 8100 Nations Way, Jacksonville, Florida 32256.

12. Defendant, GMAC Residential Funding Corporation, is a foreign corporate

entity which, according to www.mersinc.org, is a shareholder in MERS. As a national

organization, it conducts business in the State oflllinois, and it is therefore appropriate

that it be required to defend this suit in this Court. Defendant is a foreign corporation that

is set up under the laws of Delaware, with its principal place of business located at 8400

Normandale Lake Blvd., Minneapolis, Minnesota 55437.

13. Defendant, Guaranty Bank, is a foreign corporate entity which, according to

www.mersinc.org, is a shareholder in MERS. As a national organization, it conducts

business in the State of Illinois, and it is therefore appropriate that it be required to defend

this suit in this Comi. Defendant is a foreign corporation that is set up under the laws of

Delaware, with its principal place of business located at 4000 West Brown Deer Rd,

Brown Deer, Wisconsin 53209.

14. Defendant, HSBC Finance Corporation, is a foreign corporate entity which,

according to www.mersinc.org, is a shareholder in MERS. As a national organization, it

conducts business in the State of Illinois, and it is therefore appropriate that it be required

to defend this suit in this Court. The designated registered agent is CT Corporation

System which is located at 208 S. LaSalle Street, Ste 814, Chicago IL 60604.

Defendant is a foreign corporation that is set up under the laws of Delaware, with its

5

principal place of business located at 26525 N. Riverwoods Blvd., Mettawa, Illinois

60045.

15. Defendant, Sun Trust Mortgage, Inc., is a foreign corporate entity which,

according to www.mersinc.org, is a shareholder in MERS. As a national organization, it

conducts business in the State of Illinois, and it is therefore appropriate that it be required

to defend this suit in this Comt. The designated registered agent is Illinois Corporation

Service, which is located at 801 Adlai Stevenson Dr., Springfield IL 62703. Defendant

is a foreign corporation that is set up under the laws of Virginia, with its principal place

of business located at 901 Semmes Avenue, Richmond, Virginia 23224.

16. Defendant, Wells Fargo Bank, N.A., is a foreign corporate entity which,

according to www.mersinc.org, is a shareholder in MERS. As a national organization, it

conducts business in the State of Illinois, and it is therefore appropriate that it be required

to defend this suit in this Court. Defendant is a foreign national bank that is set up under

the laws of the United States, with its principal place of business located at 464 California

Street, San Francisco, California 94104.

17. Defendant, WMC Mmtgage Corporation, is a foreign corporate entity which,

according to www.mersinc.org, is a shareholder in MERS. As a national organization, it

conducts business in the State of Illinois, and it is therefore appropriate that it be required

to defend this suit in this Coutt. The designated registered agent is Prentice Hall Corp.

which is located at 33 N. LaSalle Street, Chicago IL 60602. Defendant is a foreign

corporation that is set up under the laws ofCalifomia, with its principal place of business

located at 3100 Thomton Avenue, Burbank, Califomia 91504.

6

18. In addition to the direct liability of the Defendants listed in paragraphs 2-17

for their conduct alleged herein, Plaintiff seeks a determination of the court that it is

appropriate to pierce the MERSCORP and MERS cotporate veils in this instance and

hold the Defendant shareholders ofMERSCORP liable for the conduct ofMERSCORP

and its subsidiaty, MERS. Recognizing the corporate existence ofMERSCORP and

MERS separate from their shareholders, including the Defendants listed in paragraphs 2-

17, would bring about an inequitable result or injustice, or would be a cloak for fraud or

illegality. MERSCORP and MERS were undercapitalized in light of the nature and risk

of their business. The cotporate fictions is being used to justifY wrongs; as a means of

perpetrating fraud; as a mere tool or business conduit for others; as a means of evading

existing legal obligations; to petpetuate monopoly and unlawfully gain monopolistic

control over the real property recording system in the State of Illinois; and to circumvent

statutmy obligations.

MERS MEMBERS

19. Defendant Bank of O'Fallon is an Illinois Cotporation with its principal place

of business in O'Fallon, Illinois. This Defendant is a Member ofMERS that participates

in its programs to avoid recording and filing fees. This Defendant conducts substantial

business in St. Clair County, Illinois.

20. Defendant Compass Motigage, Inc. is an Illinois Cotporation with its

principal place of business in Warrensville, Illinois. This Defendant is a Member of

MERS that participates in its programs to avoid recording and filing fees. This Defendant

conducts substantial business in St. Clair County, Illinois.

7

21. Defendant First Collinsville Bank is an Illinois Corporation with its principal

place of business in Collinsville, Illinois, which, according to www.mersinc.org, is a

Member ofMERS that participates in its programs to avoid recording and filing fees.

This Defendant conducts substantial business in St. Clair County, Illinois.

22. Defendant FirstCo Mortgage Corporation is an Illinois Corporation with its

principal place of business in O'Fallon, Illinois, which is a Member of MERS that

participates in its programs to avoid recording and filing fees. This Defendant conducts

substantial business in St. Clair County, Illinois.

23. Defendant First County Bank is an Illinois Corporation with its principal place

of business in Swansea, Illinois. This Defendant is a Member ofMERS that participates

in its programs to avoid recording and filing fees. This Defendant conducts substantial

business in St. Clair County, Illinois.

24. Defendant Midland States Bank is an Illinois Corporation with its principal

place of business in Effingham, Illinois. This Defendant is a Member ofMERS that

participates in its programs to avoid recording and filing fees. This Defendant conducts

substantial business in St. Clair County, Illinois.

25. Defendant Mid America Mortgage Services of Illinois, Inc. is an Illinois

Corporation with its principal place of business in Columbia, Illinois. This Defendant is a

Member of MERS that participates in its programs to avoid recording and filing fees.

This Defendant conducts substantial business in St. Clair County, Illinois.

26. Defendant Mmigage Services III, LLC is an Illinois Corporation with its

principal place of business in Columbia, Illinois. This Defendant is a Member ofMERS

8

that participates in its programs to avoid recording and filing fees. This Defendant

conducts substantial business in St. Clair County, Illinois.

27. Defendant Peoples National Bank N.A. is an Illinois Corporation with its

principal place of business in Mount Vernon, Illinois, which, according to

www.mersinc.org, is a Member ofMERS that participates in its programs to avoid

recording and filing fees. This Defendant conducts substantial business in St. Clair

County, Illinois.

28. Defendant Commerce Bank is a Domestic Corporation with its principal place

of business in Kansas City, Missouri, which is a Member of MERS that patiicipates in its

programs to avoid recording and filing fees. This Defendant conducts substantial business

in St. Clair County, Illinois.

29. Defendant Regions Bank is a Domestic Corporation with its principal place of

business in Birmingham, Alabama, which is a Member of MERS that participates in its

programs to avoid recording and filing fees. This Defendant conducts substantial business

in St. Clair County, Illinois.

30. Defendant UMB Bank N.A. is a Domestic Corporation with its principal place

of business in Kansas City, Missouri, which is a Member ofMERS that pmiicipates in its

programs to avoid recording and filing fees. This Defendant conducts substantial business

in St. Clair County, Illinois.

JURISDICTION AND VENUE

31. This Court has jurisdiction over this action because the acts complained of

violate Illinois statutmy law and Illinois common law as alleged herein.

9

32. This Court has proper venue over this action because the acts and omissions

giving rise to the claims asserted herein occurred in St. Clair County, Illinois.

ASSIGNMENT OF MORTGAGES ARE REQUIRED TO BE RECORDED UNDER ILLINOIS LAW

33. The origins and reasons for public recordation of mortgage interests in the

U.S. dates back to at least the middle of the 17'h Century. According to one col1ll1lentator:

One of the most striking features of Anglo-American law is the requirement to file notice in public files of a nonpossessmy secured transaction in order to enforce the transaction in the comi against third parties. The transaction of interest first developed during the early seventeenth century. English mortgage law developed for real estate. Originally, the parties structured mmigages with the secured-mortgagee in possession ofthe landed collateral, not the debtormortgagor. But by the early seventeenth centmy, the English had developed the technique of leaving the debtor-mmigagor in possession of the land to work off the loan.

*** Not all legal systems have the filing requirement. Roman law recognized the transaction, but did not require a filing. The Napoleonic Code banned the transaction. The modern explanation of these three different legal rules involves the secret lien. When debtors retain possession ofthe personalty serving as collateral under the nonpossessory secured transaction, subsequent lenders and purchasers have no way of discovering the prior ownership interest of the earlier secured creditors unless the debtor's honesty forces disclosure. Without that disclosure, the debtor could borrow excessively offering the same collateral as security several times, possibly leaving some of the debtor's creditors without collateral sufficient to cover their loan upon the debtor's financial demise. Roman law solved the problem by providing a fraud remedy against the debtor. The Napoleonic Code solved the problem by banning the transactions. AngloAmerican law solved the problem by requiring a filing. Potential subsequent lenders and purchasers could then become aware of the debtor's prior obligation by examining the public files and protect themselves by taking the action they deemed appropriate ....

George Lee Flint, Jr. and Marie Juliet Alfaro, Secured Transactions Histol)': The First Chattel Mortgage Act in the Anglo-American World, 30:4 William Mitchell Law Review 1403' 1404-05.

10

34. 765 ILCS 5/28 provides in relevant part: Deeds, mortgages, powers of

attorney, and other instmments relating to or affecting the title to real estate in this state,

shall be recorded in the county in which such real estate is situated. No deed, mortgage,

assignment of mortgage, or other instrument relating to or affecting the title to real estate

in this State may include a provision prohibiting the recording of that instmment, and any

such provision in an instrument signed after the effective date of this amendatory Act

shall be void and of no force and effect.

35. The purpose of765 ILCS 5/28 is to give third patties the opportunity to

asce1tain the status of title to property.

36. An Assignment ofMmigage is an "instrument relating to or affecting the title

to real estate" under 765 ILCS 5/28 because an "Assignment", under Illinois Law, is the

transfer of some identifiable property, claim or right from the assignor to the assignee.

37. The Recorder of Deeds is entitled to and does charge a fee for the recording of

Assignment of Mortgages pursuant to the statutory authority found in 55 ILCS 5/3-5018.

38. The two primmy documents involved in a residential home loan are the

"Mortgage" and the "Note". The Note is the promise to pay. The Mortgage is a

conveyance of an interest in the real estate as security for the loan.

39. Under long standing Illinois Real Prope1iy Law, the Mmigage is said to

"follow the Note." In other words, the Mortgage itself is a mere incident to the debt

which is reflected in the Note. It is the debt as reflected in the Note that is assigned or

transfel1'ed and the Mmtgage is merely "carried with it." An Assignment of the Note

operates as a matter of law to transfer the Mortgage.

11

40. Prior to the advent of the MERS system in the mid 1990s if a Note was

transferred from one bank to another, the banks would arrange to file an Assignment of

Mmtgage in the Recorder of Deeds office and would pay the requisite statutory recording

fee.

MERS AND THE CREATION OF A SHADOW RECORDING SYSTEM

41. Most mortgage loans made in the United States between the mid 1990s and

2010 were sold on the secondaty market, and then ultimately resold to securities investors

through a process known as securitization. As a result, the bank or mortgage company to

whom the homeowner originally promised to make payments had to assign its right in the

Note, and the Mmtgage. This process resulted (or would have resulted if not for

Defendants actions as alleged herein) in additional recording fees in that a loan could be

sold and assigned numerous times.

42. Several large participants in the mortgage industry established MERS and

most U.S. lenders are MERS "Members", including all of the Defendants, in order to

conspire to avoid the requisite payment of recording fees to Recorder of Deeds for

assignments of mmtgages.

43. MERS's Members subscribe to the MERS system and pay annual fees for the

electronic processing and private tracking of ownership and transfer of mortgages. MERS

members pay fees to MERS on both an annual and transactional basis, in exchange for

MERS' maintenance of a national electronic database of members' mortgage

transactions. Depending on their size and level of membership, MERS members may

pay up to approximately $7,500 per year as a membership fee. In addition, MERS

12

charges modest fees to register a new mortgage in the MERS System, and to register

transactional changes associated with that mortgage.

44. When a MERS member makes a home loan to a bon·ower, the MERS member

obtains from the borrower a promissmy Note and a Mmigage instrument naming MERS

as the mmigagee (as nominee for the lender and its successors and assigns). In the

Mortgage, the bonower assigns his right, title, and interest in the propetty to MERS, and

the mortgage instrument is then recorded in the local land records with MERS as the

named mmigagee. When the promissmy Note is sold (and possibly re-sold) in the

secondaty mortgage market, the MERS database purports to track that transfer. As long

as the patiies involved in the sale are MERS members, MERS remains the mortgagee of

record. Designating MERS as the mortgagee of records purportedly excuses MERS

Members from publicly recording mmigage assignments between themselves and, thus,

from paying recording fees. Through this device, MERS Members, including

Defendants, have avoided publicly recording mmigage assignments between each other,

under the rationale that the recorded title holder of the mmigage (i.e. MERS) has not

changed, even though the holder of the mortgage's beneficial interest has changed.

45. MERS only files an Assignment ofMmigage at the local Recorder of Deeds

office when a mmigage is sold to a non-MERS member or, in some circumstances,

before foreclosure proceedings are initiated.

46. MERS, nor its members, file an Assignment ofMmigage and pay the requisite

fee to the Recorder of Deeds when the debt as reflected in the Note is transfened from

one MERS entity to another.

13

47. Rather than recording information in the Recorder of Deeds' offices, MERS

Members, including Defendants, are instead supposed to register transactional and other

information about MERS mortgages in the MERS System itself. Under MERS' Rules of

Membership, Members "shall promptly, or as soon as practicable, register on the MERS

System ... the transfer of beneficial ownership of a mortgage loan."

48. Each time the beneficial interest in the Note was sold, transferred or otherwise

assigned on the MERS System between MERS Members, the Mortgage, as a matter of

Illinois law, was transferred as well, triggering the Defendants obligations under 765

ILCS 5/28 to record an Assignment of Mmtgage and pay the recording fee. Each time the

Defendants assigned its beneficial interest in the note but failed to record an Assignment

ofMmtgage constitutes a violation of765 ILCS 5/28.

49. The MERS Rules of Membership specifically prohibit the filing of any

Assignment of Mortgage other than when a Note is transferred from a MERS Member to

a non-Member:

At the request of the beneficial owner of a mortgage loan, or any designee thereof as shown on the MERS System, MERS shall provide to such beneficial owner or designee a recordable assignment for such mmtgage loan to another patty designated by the beneficial owner or designee; provided however, that such beneficial owner or designee shall warrant to MERS that such assignment shall be promptly recorded. Requests for recordable assignments may be made only for purposes of deactivating a mortgage loan from the MERS System.

50. This prohibition against filing (or even requesting) an Assignment of

Mmtgage violates 765 ILCS 5/28.

51. According to data from Laredo, the online software contractor used by the St.

Clair County Recorder of Deeds to make its records available to the public on a remote

access 24/7 basis, the phrase "MERS" in conjunction with the filing of a "Mortgage"

14

occmTed on 49,951 occasions between January I, 2000 and May 6, 2012 in St. Clair

County, Illinois alone. However, the phrase "MERS" in conjunction with the filing of an

"Assignment of Mortgage" occurred only 3,831 times during the same time frame.

52. MERS Members are required to use MERS' approved Mortgage Form for

loans that are to be tracked on MERS system. That form reads in pati:

that

(C) "MERS" is Mortgage Electronic Registration Systems, Inc. MERS is a separate corporation that is acting solely as a nominee for Lender and Lender's successors and assigns. MERS is the mortgagee under this Security Instrument. MERS is organized and existing under the laws of Delaware, and has an address and telephone number of P.O. Box 2026, Flint, MI 48501-2026, tel (888) 679-MERS.

20. Sale ofNote; Change ofLoan Servicer; Notice of Grievance. The note or a partial interest in the Note (together with this Security Instrument) can be sold one or more times without prior notice to Borrower. A sale might result in a change in the entity (known as the "Loan Servicer") that collects periodic payments due under the Note and this Security Instrument and performs other mortgage loan servicing obligations under the Note this Security Instrument and Applicable Law .....

53. The MERS contractual Terms and Conditions with its MERS Members state

MERS shall serve as mmigagee of record with respect to all such mmigage loans solely as a nominee in an administrative capacity, for the beneficial owner or owners thereof from time to time. MERS shall have no rights whatsoever to any payments made on account of such mortgage loans, to any servicing rights related to such mortgage loans, or to any mmigaged properties securing such mmigage loans. MERS agrees not to asseti any rights (other than rights specified in the Governing Documents) with respect to such motigage loans or mortgaged propetiies.

54. MERS does not have any beneficial interest in the Note or Mortgage that are

registered on the MERS system. MERS does not have any financial interest in the loans,

MERS was not involved in the origination of the loans, MERS does not have the right to

any payment on the loans, and does not service the loans. In fact MERS relies upon the

officers, agents and employees of the MERS members to sign documents on behalf of

MERS.

15

55. MERS purported status as a Mortgagee is a deceptive sham and serves as a

tool for its members to avoid the payment of recording fees required by statute. Moreover

765 ILCS 5/28 requires the recording of an Assignment of Mortgage irrespective of

whether MERS improperly remains listed as the purported mmigagee.

56. According to MERS's own website, its system saves money for its members

and is specifically designed to avoid paying the fees to Plaintiff. Specifically, MERS has

stated:

MERS acts as nominee in the county land records for the lender and servicer. Any loans registered on the MERS system is inoculated against future assignments because MERS remains the nominal mortgagee no matter how many times servicing is traded.

* * * Assignments eliminated forever ($30 saved per loan).

* * *

Lenders may also assign into MERS if the loan has already been closed in the lenders name. Once the loan is assigned to MERS ... tracking servicing and beneficial rights can occur electronically for all future transfers. The need for any additional assignments after this point will be eliminated unless the servicing rights are sold to a nonMERS member.

* * *

Chain of title starts and stops with MERS! With MERS as the Mortgagee of Record, you don't need additional assignments ever. The umecorded assignments needed for interim funding and loan sales are costly. With MERS you save an estimated $30 per loan on unrecorded assignments.

* * *

MERS saves time associated with processing multiple assignments.

16

57. Currently more than half of all home mortgage loans originated in the United

States list MERS as the purported Mortgagee. MERS President, R.K. Arnold, testified

in 2009 that assuming each mortgage had been resold and recorded just once, it would

have saved the industry $2.4 billion in recording expenses.

58. The MERS scheme to systematically avoid the filing of Assignment of

Mortgages has resulted in a shadow, privately nm, recording system whereby the public

is denied access to public records that reflect who has a beneficial interest in a given

parcel ofland. The MERS System effectively eliminated the homeowners' and the

public's ability to track the purchase and sale ofpropetiies through the traditional public

records system. Because ofMERS' scheme, for the first time on St. Clair County,

Illinois' histmy, there is no longer an authoritative public record of who owns land

situated in St. Clair County, Illinois. Instead this information is now stored in a private

database maintained by MERS.

59. The havoc wrought by MERS was summarized aptly in an April6, 2011,

letter from the Guilford County, Nmih Carolina Register of Deeds and Southem Essex

District of Massachusetts Register of Deeds to Iowa Attomey General Tom Miller, leader

of the Mmigage Foreclosure Multistate Group, comprised of states attomeys general in

all 50 states. The letter outlines the concems shared by county clerks and recorders

nationwide and states, in part:

As County Land Recorders in Massachusetts and Nmih Carolina, we have been gravely concerned with the role of the Mmigage Electronic Registration Systems (MERS) in not only foreclosure proceedings, but as it undennines the legislative intent of our offices as stewards of land records. MERS tracks more than 60 million mmigages across the United States and we believe it has assumed a role that has put constmctive notice and the propetiy rights system at risk. We believe

17

MERS undermines the historic purpose of land record recording offices and the "chain of title" that assures ownership rights in land records.

As a result, we are asking as part of your probe, that this task force and the National Association of Attorney Generals require that all past and present MERS assignments of deeds of trust/mortgages be filed in local recording offices throughout the United States immediately. Assignments are required by statute to be filed in Massachusetts; however they are not currently required to be recorded in Nmih Carolina ....

This action would serve tlu·ee specific purposes. First, the filing of all assignments would help recover the chain of title that detennines property ownership rights that has been lost and clouded over during the past 13 years because ofthe scheme that MERS has set in place. Second, transparency and confidence in ownership rights would be restored and this would prevent the infringement upon those rights by others. Third, this action would support a retum to sound fundamentals in our economy between the financial services industry and public recording offices.

MERS has defended their practices by saying that they were helping the registries of deeds by reducing the amount of paperwork that needed to be recorded. This claim is outrageous. This is help we did not ask for, nor was it help that we needed. It is vety clear that the only ones that they were helping were themselves. Over the past 10-12 years, recording offices across the United States have upgraded their intema1 and external teclu10logy to meet the demands of lenders, title underwriters, title searchers, and citizens. In fact, in 1998 the Southem Essex District Registry of Deeds in Massachusetts became the first registry of deeds to provide both document images and indices available to the public, 24 hours a day, free of charge on the world-wide-web. In doing so, the Registly received a Computerworld Smithsonian A ward which recognized the innovative use of technology to benefit society. In 2009, the Guilford County Register of Deeds was given a local Govennnent Federal Credit Union Productivity Award by the North Carolina Association of County Commissioners for their technological innovations. Nationally, over 93% of the public land records are up to date and current, according to Emest Publishing.

As of today, there are over 600 recording jurisdictions, covering 43% of the US population that have incorporated an eRecording model into their document recording operations. We believe these jurisdictions cover nearly 80% of the volume of assignments that should be recorded. The remaining areas could be covered quickly with legislation requiring such action by state legislatures.

Quite frankly, we believe this can and should be done. It's the right thing to do.

18

60. The MERS database is unreliable and inaccurate. According to a shtdy of

MERS internal databases performed by Professor Alan White of Valparaiso School of

Law, less than 30% of the mortgages had an accurate record in MERS. Similarly low

MERS accuracy rates were also repotted by the San Francisco Office of the Assessor-

recorder. Moreover, prior to 2011 MERS was not regulated by any state or federal

agency, and its database was not regularly audited.

61. In April2011, MERS executed a Stipulation and Consent to the Issuance of a

Consent Order with the Office of the Comptroller of the Currency, the Board of

Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the

Office of Thrift Supervision, and the Federal Housing Finance Agency (collectively,

"Federal Regulators"), through which MERS agreed to the tem1s of a comprehensive

Consent Cease and Desist Order ("Cease and Desist Order").

62. The Cease and Desist Order was based on the results of the Federal

Regulators' examination ofMERS, which "identified cettain deficiencies and unsafe or

unsound practices by MERS that present financial, operational, compliance, legal and

reputational risks to MERS, and to the participating Members." With respect to tracking,

registering, and foreclosing upon mottgages, the Federal Regulators specifically

concluded that MERS:

(a) has failed to exercise appropriate oversight, management supervision and corporate govemance, and have failed to devote adequate financial, staffing, training, and legal resources to ensure proper administration and delivety of services to Examined Members; and

(b) has failed to establish and maintain adequate intemal controls, policies, and procedures, compliance risk management, and internal audit and repotting requirements with respect to the administration and delivety of services to Examined Members.

19

63. In a recent interview, the current MERSCORP CEO openly acknowledged

that the company "did not have a robust process to make sure that all the date on our

system was accurate, timely and reliable. Our view was that is the servicer's data and

they're relying on it for their own transactions, they're using their own systems, so we

don't have to double check."

64. Additionally, since the MERS System has effectively replaced the Recorder of

Deeds' offices as the repositmy of records reflecting transfers of beneficial interests in

MERS registered loans, the failure to ensure the accuracy of the database makes it

difficult to verify the chain oftitle for a loan.

65. MERS has few or no employees but serves as the mortgagee for tens of

millions of mortgages throughout the county, it has indiscriminately designated over

20,000 MERS member employees as MERS "certifying officers" to act on the company's

behalf, expressly authorizing these individuals to assign MERS mmigages, to execute

paperwork necessmy to foreclose on propeziies secured by MERS mmigages, and to

submit proofs of claims and affidavits on behalf ofMERS in bankruptcy proceedings.

MERS has failed to adequately screen, train, or monitor the activities ofthese certifying

officers, who have executed millions of important legal documents on MERS' behalf.

66. Homeowners, as well as the general public and the comis, do not have access

to the vast majority of information maintained on the MERS System, including records

reflecting the sale of mortgage loans from one financial institution to another.

67. Thus, as a result ofthe creation ofMERS, one can no longer look to the public

recording system as a reliable source for tracking the chain of title for a loan or for

identifying the current beneficial owner of the mortgage. Although MERS Members are

20

supposed to update the MERS System to reflect this information, MERS relied on its

Members to voluntarily register transactions and did not take sufficient steps to ensure

that is members did so or that MERS System date was current and accurate.

68. It is important for homeowners to know who owns their loans because this

may be the only entity with the authority to modify the tetms or reduce the principal of

their mortgage. Investor-specific restrictions may also impact the types of loan

modification options available.

69. Moreover, in the absence of a public record, homeowners in foreclosure

proceedings cannot reliably verify that the purpmied plaintiff is the successor to the

original lender and thus a proper plaintiff. As the Kansas Supreme Comi noted when

discussing the problems associated with MERS, "having a single front man, or nominee,

for various financial institutions makes it difficult for mortgagors and other in~titutions to

detem1ine the identity of the cun-ent note holder." A Bankruptcy Court in Massachusetts

noted "[I]t is not uncommon for notes and mmigages to be assigned, often more than

once. When the role of a servicing agent acting on behalf of a mortgagee is thrown into

the mix, it is no wonder that it is often difficult for unsophisticated borrowers to be

certain of the identity of their lenders and mortgagees." A New York Court of Appeals

Comi noted "[T]he practices of the various MERS members, including both [the original

lender] and [the mmigage purchaser], in obscuring from the public the actual ownership

of a mmigage, thereby creating the opportunity for substantial abuses and prejudice to

mortgagors ... ". The Arkansas Supreme Court has noted: "The only recorded document

provides notice that [the original lender] is the lender and, therefore, MERS 's principal.

MERS assetts [the original lender] is not its principal. Yet no other lender recorded its

21

interest as an assignee of [the original lender]. Permitting an agent such as MERS

purports to be to step in and act without a recorded lender directing its action would

wreak havoc on notice in this state."

70. Fmthetmore, the failure to register propetty transfers in publicly available

records deprives potential future purchasers and other lien holders of imp01tant chain of

title information.

71. MERS' scheme frustrates the purpose of 55 ILCS 5/3-5036 and interferes

with the Recorder of Deeds' duties under 55 ILCS 5/3-5036 to provide public access to

land records.

72. MERS's scheme fmstrates the purpose of 55 ILCS 5/3-5025 and interferes

with the Recorder of Deeds' duties under 55 ILCS 5/3-5025 to provide and maintain

accurate Grantor and Grantee books.

73. As a proximate result of the Defendants' actions, Plaintiff has suffered

damages.

FIRST CLAIM- NEGLIGENT VIOLATION OF 765 ILCS 5/28 AND 55 ILCS 5/3-5018

74. The allegations of paragraphs 1-73 above are re-alleged and incorporated

herein by reference.

75. The conduct of the Defendants as alleged herein has repeatedly violated 765

ILCS 5/28 and 55 ILCS 5/3-5018 and has caused Plaintiff a loss of substantial fees that

would have been collected had the statutes not been violated.

76. As a proximate result of the Defendants' negligent violations of765 ILCS

5/28 and 55 ILCS 5/3-5018 Plaintiff has been damaged.

22

SECOND CLAIM- UNJUST ENRICHMENT

77. The allegations of paragraphs 1-73 above are re-alleged and incorporated

herein by reference.

78. Defendants' actions were perfotmed with the specific purpose of avoidance of

recording assignments of mortgages and avoiding the expenses associated with same, in

violation of765 ILCS 5/28 and 55 ILCS 5/3-5018.

79. As a proximate result, Defendants have been unjustly enriched by this

violation of the 765 ILCS 5/28 and 55 ILCS 5/3-5018.

80. As a proximate result of the unjust enrichment, Plaintiff has been injured.

Defendants' conduct confetTed a benefit upon themselves at the expense of Plaintiff.

Defendants were fully aware of this benefit to themselves at the expense of Plaintiff.

Finally, Defendants have retained the benefit (namely, the fees saved by circumventing

the recordation of assignments of mottgages when transferred) without compensating

Plaintiff.

THIRD CLAIM- CIVIL CONSPIRACY TO VIOLATE 765 ILCS 5/28 and 55 ILCS 5/3-5018

81. The allegations of paragraphs 1-73 above are re-alleged and incmporated

herein by reference.

82. Defendants in this action have conspired in concert with one another to thwart

the provisions of765 ILCS 5/28 and 55 ILCS 5/3-5018.

83. Defendants' actions were done with the specific purpose avoiding the

recording of assignments of mortgages and payment of associated expenses.

23

84. As a proximate result, Plaintiff has been damaged.

FOURTH CLAIM- VIOLATION OF THE DECEPTIVE TRADE PRACTICES ACT (815 ILCS 510/2)

85. The allegations of paragraphs 1-73 above are re-alleged and incorporated herein

by reference.

86. Defendants' actions as alleged herein constitute violations of815 ILCS

510/2(a)(2-3).

87. Defendants' actions were done with the specific purpose of causing likelihood of

confusion and misunderstanding as to MERS status as a motigagee, its affiliation with the

other Defendants named herein and the identity of the beneficial owner of the Note

associated with the Mortgage.

88. As a proximate result, Plaintiff has been damaged.

FIFTH CLAIM- VIOLATION OF THE CONSUMER FRAUD AND DECEPTIVE PRACTICES ACT (815 ILCS 505/2)

89. The allegations of paragraphs l-73 above are re-alleged and incorporated herein

by reference.

90. Defendants' actions as alleged herein constitute violations of815 ILCS 505/2.

91. Defendants' actions were done with the specific purpose of causing likelihood of

confusion or misunderstanding as to MERS status as a mortgagee, its affiliation with the

other Defendants named herein, and the identity of the beneficial owner of the Note

associated with the Mortgage.

92. As a proximate result, Plaintiff has been damaged.

24

PRAYER FOR RELIEF

WHEREFORE, Plaintiff has suffered damages due to Defendants' conduct

and as such requests the court enter judgment against Defendants, and award relief to

Plaintiff as follows:

a. Enter an injunction ordering Defendants, Defendants' agents and

employees and all other person in active concert and pmiicipation with Defendants to

immediately cease the practice of non recording of assignments of mortgages pursuant to

815 ILCS 505/7;

b. Order an Accounting, at Defendants' expense, of all Assignment of

Motigages that should have been recorded but were not as a result of MERS' scheme and

then Order Defendants' to record same and tender to Plaintiff the Fees owed for said

recordings;

c. Find for the Plaintiff and award compensatory and consequential damages

for the Defendants' conduct;

c. Award actual damages and relief to Plaintiff;

d. Award costs and reasonable attorneys' fees to Plaintiff;

e. Award interest on the amounts improperly withheld by the Defendants;

and,

f. Order such other and fmiher relief as may be just including all relief

available under 815 ILCS 505/2 et seq.

25

26

Respectfully Submitted,

BRENDANKE~

For:~· Paul Slocomb, #6226129 Special Assistant States Attorney 10 Public square Belleville, II 62220