SSW Presentation: Loan Repayment for Federal Loans 2015

32

Student Loan Repayment and other exciting activities after GRADUATION! 1

-

Upload

lilly-hall -

Category

Education

-

view

287 -

download

0

Transcript of SSW Presentation: Loan Repayment for Federal Loans 2015

Student Loan Repaymentand other exciting activities after

GRADUATION!

1

Agenda

■ Loan types & interest rate■ The grace period■ Repayment plans■ Loan Forgiveness■ Avoiding delinquency & default■ Financial Planning

2

Key Players■ Federal government www.studentaid.ed.gov

■ Lenders – of private loans

■ Direct Loan Servicers ■ NSLDS

www.nslds.ed.gov

■ Credit Reportingwww.annualcreditreport.com

♦ Experian♦ Equifax♦ TransUnion

■ Ombudsman http://studentaid.ed.gov/repay-

loans/disputes1.877.557.2575

3

Types of Loans

■ Federal Stafford Direct – Subsidized■ Federal Stafford Direct – Unsubsidized■ Alternative – Private lenders■ Federal Graduate PLUS Loan

4

National Student Loan Data System

■ Central database for student aid records♦ Track loans from disbursement to payoff

♦ Total student loan indebtedness

♦ Loan status & interest rate

♦ Loan Servicer information

♦ www.nslds.ed.gov

5

Stafford Loan Interest Rates

Disbursed Stafford Subsidized

Stafford Unsubsidized

7.1.2006 – 6.30.2008 6.8% 6.8%

7.1.2008 – 6.30.2009 6.0% 6.8%

7.1.2009 – 6.30.2010 5.6% 6.8%

7.1.2010 – 6.30.2011 4.5% 6.8%

7.1.2011 – 6.30.2012 3.4% 6.8%

7.1.2012 – 6.30.2013 3.4% 6.8%

7.1.2013 – 6.30.2014 n/a 5.41%

7.1.2014 – 6.30.2015 n/a 6.21%

6

The Grace Period■ One-time grace period

♦ Begins after you graduate, leave school or drop below half time (caution if you took a break from school)

♦ Monthly payments begin after grace period ends■ Direct Loans – 6 months■ Perkins Loans – 9 months■ Graduate PLUS Loans – 6 months (if disbursed after

7/1/2008)■ Private Loans – Varies

7

Direct Loan Repayment Options

■ Standard Repayment■ Graduated Repayment■ Extended Repayment■ Income-Contingent Repayment■ Income-Based Repayment■ Pay as You Earn Repayment Plan

8

Standard Repayment Chart

■ Fixed monthly payment■ $50 minimum payment■ 10-year repayment schedule

Loan Amount

Monthly Payment

Total Paid* (Loan + Interest)

$10,000 $115 $13,810

$50,000 $575 $69,048

*A subsidized Stafford loan repaid at 6.80 percent interest, assuming the standard repayment plan of 10 years.

9

Graduated Repayment Plan

■ Payment gradually increases over time■ Payment must cover interest due ■ 10-year repayment schedule

Loan Amount

Beginning Monthly Payment

Ending Monthly Payment

Total Paid* (Loan + Interest)

$10,000 $57 $135 $14,353

$50,000 $283 $677 $71,765

*A subsidized Stafford loan repaid at 6.80 percent interest, assuming the graduated repayment plan of 10 years.

10

Extended Repayment Plan

■ Loans greater than $30,000■ Standard or graduated repayment plans■ Repayment term not to exceed 25 years

Loan Amount

Monthly Payment

Years in Repayment

Total Paid* (Loan + Interest

$50,000 $347 25 $104,111

*A subsidized Stafford loan repaid at 6.80 percent interest, assuming an extended standard repayment plan of 25 years.

11

Income-Contingent Repayment Plan

■ Payment based on income, household size and state of residence (often 20% of income)

■ Forgiveness after 25 years (tax consequences)

12

Loan Amount

Gross Monthly Income

Family Size

Monthly Payment

Total Paid* (Loan + Interest)

$10,000 $1,500 1 $63 $20,743

$50,000 $4,000 3 $495 $73,475*A Stafford loan repaid at 6.80 percent interest based on borrower living in the continental U.S. This is an estimated repayment amount for the first year and total loan payment.

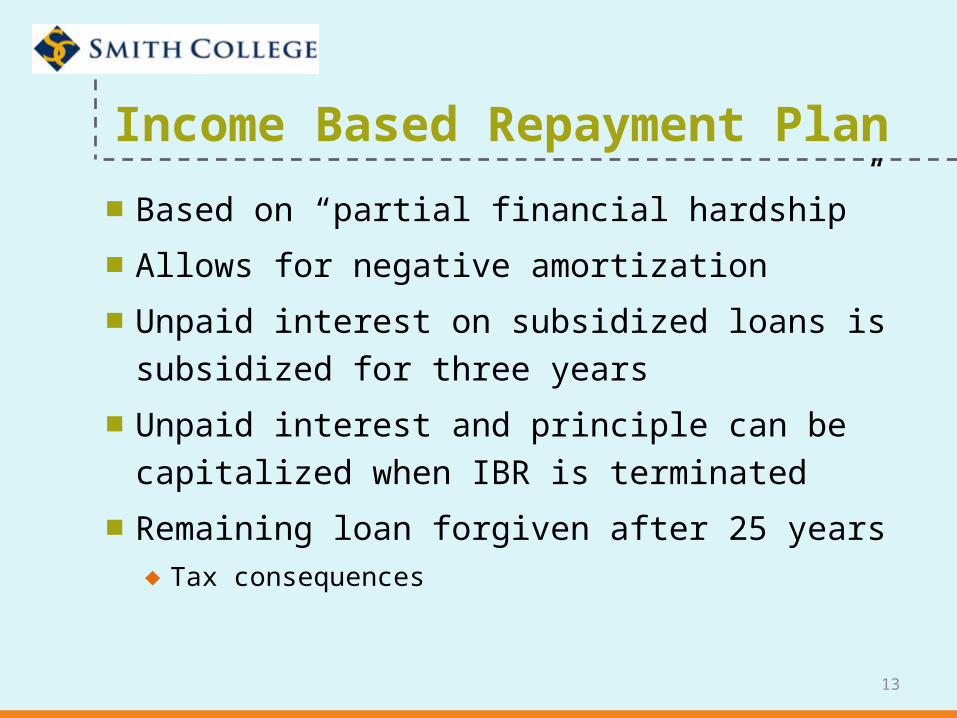

Income Based Repayment Plan■ Based on “partial financial hardship”

■ Allows for negative amortization

■ Unpaid interest on subsidized loans is subsidized for three years

■ Unpaid interest and principle can be capitalized when IBR is terminated

■ Remaining loan forgiven after 25 years♦ Tax consequences

13

Income Based Repayment Plan

■ Payment based on percentage of total income

Loan Amount AGI* 150% of

Poverty LineDisposable

IncomeCurrent Monthly

Payment*New Monthly

Payment**

$12,500 $25,000 $17,560 $7,440 $144 $94

$50,000 $25,000 $17,560 $7,440 $576 $94

*A subsidized Stafford loan repaid at 6.80 percent interest, assuming the standard repayment plan of 10 years.

**Assumed AGI with one person in the household.

See if you qualify at the following site:studentaid.ed.gov – select “repaying your loans”

14

Pay As You Earn Repayment Plan

■ Base on “partial financial hardship”■ Maximum payment is 10% of

discretionary income, the difference between your AGI and 150% of poverty.

■ Remaining loan forgiven after 20 years♦ Tax consequences

15

Pay As You Earn Repayment Plan

■ Payment based on percentage of total income

Loan Amount AGI* 150% of

Poverty LineDisposable

IncomeCurrent Monthly

Payment*New Monthly

Payment**

$12,500 $25,000 $17,560 $7,440 $144 $62

$50,000 $25,000 $17,560 $7,440 $576 $62

*A subsidized Stafford loan repaid at 6.80 percent interest, assuming the standard repayment plan of 10 years.

**Assumed AGI with one person in the household.

See if you qualify at the following site:studentaid.ed.gov – select “repaying your loans”

16

Loan Consolidation

■ Combine loans into one single new loan ♦ You agree to new terms and conditions

■ One monthly payment♦ Lower payment/longer repayment period

■ Payments begin at consolidation■ Caution with Perkins Loans■ Be informed

♦ www.studentloans.gov♦ www.studentaid.ed.gov

17

Loan Forgiveness

■ Explore all options – do more research■ Review Websites – regulations change!■ Call to describe your individual situation■ Call to confirm your understanding of

their information■ You are your own advocate

18

Loan Forgiveness

■ Work in public service profession■ Volunteer work■ Military service ■ Teach or practice medicine in certain

communities – National Health Service Corps

■ Loan forgiveness resources♦ www.studentaid.ed.gov♦ www.nhsc.hrsa.gov/loanrepayment/♦ http://www.hesc.ny.gov/

19

Public Service Loan Forgiveness (PSLF)■ Full-time eligible public service job■ Non-defaulted Direct Loans

♦ Other federal student loans consolidated into Direct Consolidation Loan

■ Payments beginning October 1, 2007♦ 120 qualifying payments♦ IBR, ICR, PAYE and Standard Repayment

plans■ Forgiven amount not taxable 20

Apply for PSLF

■ Track your employment record!♦ Clearly identify your employer(s)♦ Position/title♦ Supervisor’s name/telephone number♦ Show employer meets the definition♦ Dates of employment♦ Full-time employee

■ Keep complete loan payment records

21

Loan Cancellation In extreme circumstances:

♦ Total and permanent disability♦ Inability to complete course of

study due to school closure♦ False certification by school♦ Death

22

Avoid Delinquency & Default

■ Pay on time■ A payment received one day late is

considered delinquent■ Must pay, even if you don’t get a bill■ Delinquent payments are reported to

the credit bureaus■ Always call your servicer for help

23

Deferment■ Postponement of payments

♦ Not automatic♦ You must apply & receive approval from

lender ■ Primary reasons

♦ In-school ♦ Unemployment♦ Economic hardship♦ Military service

24

Forbearance■ Temporary reduction or postponement of

payments■ Not automatic

♦ You must apply and receive approval from lender■ Primary reasons

♦ Poor health♦ Residency program♦ Financial hardship

■ Interest will continue to accrue

25

Consequences of Default■ Full amount of loan is due

♦ Including collection costs■ Subject to federal and state offsets

♦ Wages and tax refund may be garnished■ Credit will be tarnished■ Loss of deferment and forbearance options■ Loss of eligibility for future financial aid■ May lose eligibility for certain federal or state

jobs■ May lose professional license

26

Your Rights

■ Receive a copy of your signed MPN■ Receive a disclosure statement■ Prepay all or part of your loan without penalty■ Deferments & forbearance, if eligible ■ Written notice if your loan is sold■ Proof of discharge after repaying loan in full

27

Your Responsibilities

■ Repay your loan(s)

■ Make on-time, monthly payments

■ Read correspondence from servicer

■ Notify servicer of changes within 10 days♦ School & enrollment status

♦ Name, address & telephone number

■ Ask your servicer for help

28

Who to Pay

■ Check NSLDS to see what federal loans you have: www.nslds.ed.gov

■ Federal Direct Stafford Loans♦ One of many Federal Loan Servicers

■ Federal Perkins Loans♦ Servicer designated by college

■ Smith College Loans♦ Campus Partners

■ Private Loans – The Lender29

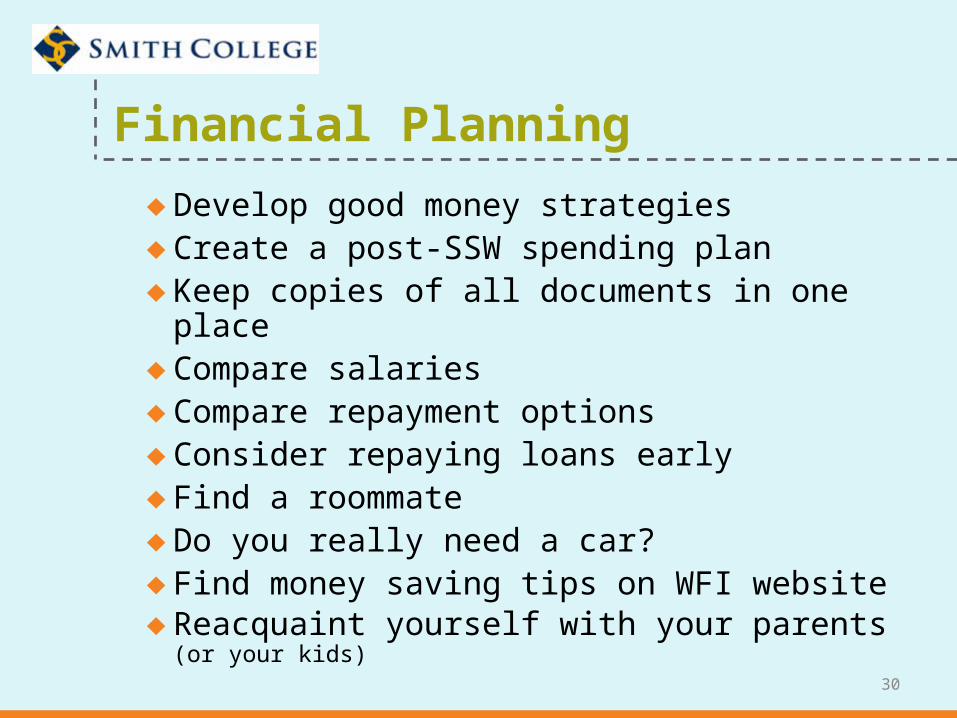

Financial Planning♦ Develop good money strategies♦ Create a post-SSW spending plan♦ Keep copies of all documents in one place♦ Compare salaries♦ Compare repayment options♦ Consider repaying loans early♦ Find a roommate♦ Do you really need a car?♦ Find money saving tips on WFI website♦ Reacquaint yourself with your parents (or your

kids)30

Executive Summary

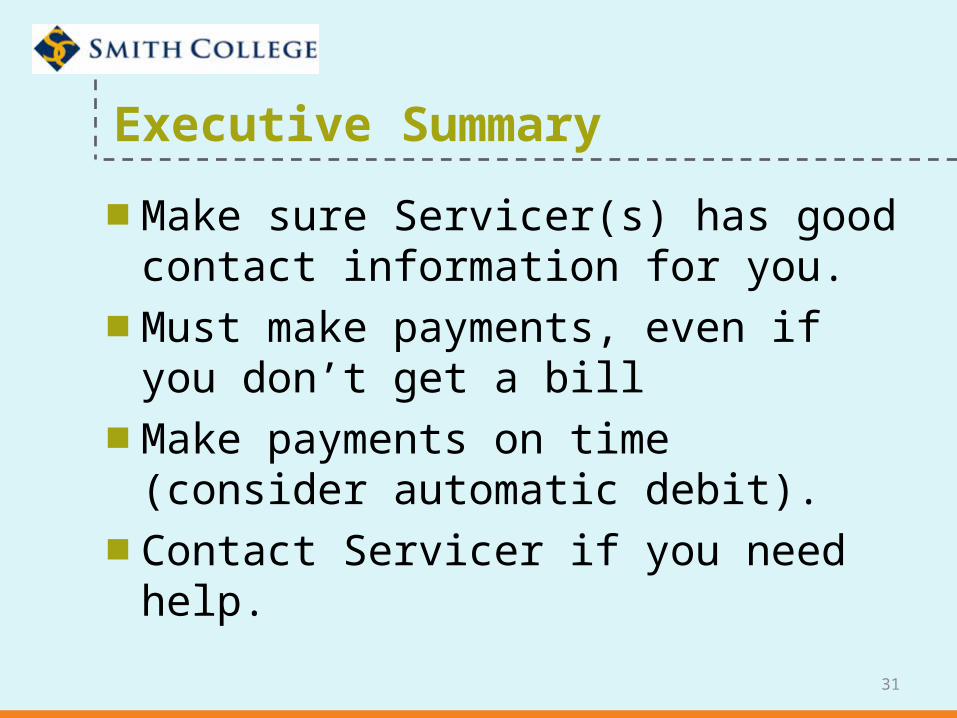

■ Make sure Servicer(s) has good contact information for you.

■ Must make payments, even if you don’t get a bill

■ Make payments on time (consider automatic debit).

■ Contact Servicer if you need help.

31

Celebrate! (Any Questions?)

32