Sri Lanka: Improving the Rural and Urban Investment Climate · PDF fileIMPROVING THE RURAL AND...

115

-

Upload

duongkhuong -

Category

Documents

-

view

219 -

download

2

Transcript of Sri Lanka: Improving the Rural and Urban Investment Climate · PDF fileIMPROVING THE RURAL AND...

SRI LANKA:IMPROVING THE RURAL AND URBAN

INVESTMENT CLIMATE

An Investment Climate Assessment

Based on an Urban and Rural Enterprise Survey

Carried Out by the Asian Development Bank and

The World Bank with Support from Sri Lanka’s

Department of Census and Statistics and

ACNielsen Lanka (Pvt.) Ltd.

January, 2005

ii

2004 The International Bank for Reconstruction and Development/The World Bank1818 H StreetWashington DC 20433Telephone: 202-473-1000Internet: www.worldbank.orgE-Mail: [email protected]

Published by

This volume is a product of the staff of the Asian Development Bank and the International Bank forReconstruction and Development/The World Bank. The findings, interpretations, and conclusions expressed inthis paper do not necessarily reflect the views of the Board of Directors of the Asian Development Bank andthe Executive Directors of The World Bank or the governments they represent.

The Asian Development Bank and The World Bank do not guarantee the accuracy of the data included in thiswork. The boundaries, colors, denominations, and other information shown on any map in this work do not implyany judgement on the part of the Asian Development Bank and The World Bank concerning the legal status ofany territory or the endorsement or acceptance of such boundaries.

Rights and PermissionsThe material in this publication is copyrighted. Copying and/or transmitting portions or all of this work withoutpermission may be a violation of applicable law. The Asian Development Bank and the International Bank forReconstruction and Development/The World Bank encourage dissemination of this work and will normally grantpermission to reproduce portions of the work.

For permission to photocopy or reprint any part of this work, please send a request with complete informationto the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USATelephone 978-750-8400, Fax 978-750-4470, www.copyright.com

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of thePublisher,The World Bank, 1818 H Street NW, Washington DC 20433, USA,Fax: 202-522-2422, E-mail: [email protected]

ISBN : 955-8908-12-6

Publication Designed byAri Investments Limited19, St. Joseph RoadNugegodaSri Lanka

The World Bank Colombo Office73/5, Galle RoadColombo 03Sri LankaInternet: www.worldbank.org/lk

Asian Development Bank6, ADB Avenue, Mandaluyong City0401 Metro Manila, PhilippinesP.O. Box 789, 0980 Manila, PhilippinesInternet: www.adb.org

TABLE OF CONTENTSAcronyms and Abbreviations iv

Acknowledgments v

Executive Summary - English E I- Sinhala S I- Tamil T I

I. Investment Climate Matters 11.1 What is the Investment Climate and Why Does it Matter? 11.2 Overview of the Economy: Achievements and Challenges 2

II. The Different Profiles of Urban and Rural Enterprises 82.1 Great Diversity in the Enterprise Landscape 82.2 Greater Stability and Longevity among Urban Enterprises 102.3 More Assets and Higher Productivity in Urban Enterprises 112.4 Registration among Rural Firms Surprisingly High 112.5 Weak Links between Rural and Urban Firms 132.6 Strong Links with Agriculture 13

III. The Investment Climate and Its Impact on Enterprise Performance 153.1 Sri Lanka’s Investment Climate: Strong on Governance,

Weak on Infrastructure and Finance 153.2 Good Governance: Sri Lanka’s Success Story 163.3 Infrastructure: The Weakest Part of the Investment Climate 193.4 Access to Finance Costly and Limited 233.5 Growing Regional Differences across the Country 273.6 How the Investment Climate Affects Firms' Performance 29

IV. International Competitiveness: Challenges and Opportunities 324.1 Unlocking the Potential of Foreign Direct Investment 324.2 Restoring Stability 344.3 Easing Difficult Labor Market Conditions 354.4 Increasing the Efficiency of Ports and Customs to Facilitate Trade 384.5 Performance and Challenges of Key Export Sectors 40

V. Conclusions and Policy Recommendations 485.1 A Policy Strategy Recognizing the Sharp Rural-Urban Differences 485.2 Policy Recommendations 49

AppendixesAppendix 1: Urban Manufacturing Survey: Sampling Methodology 55Appendix 2: Urban Services Survey (Tourism and Information Technology):

Sampling Methodology 59Appendix 3: Rural Survey: Instrument and Sampling Methodology 61Appendix 4: Urban Manufacturing Survey: Technical Appendix on

Investment Climate and Firm Performance 69Appendix 5: Rural Survey: Technical Appendix on Investment Climate,

Firm Performance and Start Up 80Appendix 6: Rural Summary Tables 92

References 99

iii

iv

ACRONYMS ANDABBREVIATIONS

ASYCUDA - Automated System for Customs DataBOI - Board of InvestmentCEB - Ceylon Electricity BoardEPZ - Export Processing ZoneERA - Electricity Reform ActEU - European UnionFDI - Foreign Direct Investment FMRA - Fiscal Management (Responsibility) ActFTA - Free Trade AgreementGDP - Gross Domestic ProductGN - Grama NiladhariGNI - Gross National IncomeGoSL - Government of Sri LankaIC - Investment ClimateICA - Investment Climate AssessmentICT - Information and Communication TechnologyIT - Information TechnologyITU - International Telecommunications UnionLECO - Lanka Electricity CompanyLG - Local GovernmentMFA - Multi- Fibre ArrangementMFI - Microfinance InstitutionsNGO - Non Government Organization NWSDB - National Water Supply Development BoardOECD - Organization for Economic Cooperation and

DevelopmentPS - Pradeshiya SabhaPUCSL - Public Utilities Commission of Sri LankaRDA - Road Development AuthorityR&D - Research and DevelopmentSAGT - South Asia Gateway Terminals Ltd.SLPA - Sri Lanka Port AuthoritySLR - Sri Lankan RupeeTEWA - Termination of Employment of Workers ActTFP - Total Factor ProductivityUBS - Unemployment Benefit SystemUI - Unemployment InsuranceUSA - United States of AmericaUK - United KIngdomWB - World BankWDI - World Development Indicators

v

ACKNOWLEDGEMENTSTHE AUTHORS GRATEFULLY ACKNOWLEDGE the support received and the collaborationwith Sri Lanka's Department of Census and Statistics and ACNielsen Lanka (Pvt.) Ltd. This reportwas prepared by a joint Asian Development Bank (ADB) - World Bank team led by Abuzar Asra,Rana Hasan and Ernesto Pernia from the ADB and Esperanza Lasagabaster, Mona Sur and IsmailRadwan from the World Bank. Other staff contributing to the report include Gemma Estrada,Dalisay Maligalig and Georgina Nepomuceno from the ADB, and Terrence Abeysekera, KareemAziz, Uwe Deichmann, Klaus Deininger, Naresha Duraiswamy, Marjorie Espiritu, Sriyani Hulugalle,Giuseppe Iarossi, Songqin Jin, Radha Singla, Giovanni Tanzillo and Dina Umali-Deininger from theWorld Bank.

Financial support from the Bank Netherlands Partnership Program for the Rural Investment ClimateSurvey is gratefully acknowledged. The team thanks Mr. Selvin Ireneuss and staff from the Secretaryfor Immediate Humanitarian and Rehabilitation Need (SIHRN) for their support and assistance infacilitating the rural survey in the North and East. Thanks are also extended to the various DivisionalSecretary and Grama Niladhari officers for their support.

vi

EXECUTIVE SUMMARYOver the past 25 years Sri Lanka has seen steady economic growth accompanied by a profound transformation of itstrade and industrial structure. Led by the garment sector, manufacturing exports took off in the late1970s, growing by 32 percent a year between 1978-95. Spurring this remarkable transformation werethe opening of trade and liberalization of some sectors in the late 1970s. Also contributing, thanksto an early commitment to human development, was the country’s skilled and literate labor force, afeature distinguishing Sri Lanka from other lower-middle-income countries.

While this progress is heartening, Sri Lanka has failed to keep pace with East Asian countries in economic growthand poverty reduction. In the 1960s Sri Lanka had a per capita income comparable to those of theRepublic of Korea, Malaysia, and Thailand. Today its per capita income is less than half of Thailand’sand an even smaller share of Malaysia’s and Korea’s. Not surprisingly, Sri Lanka has made limitedgains in poverty reduction. The share of the population in poverty remains comparatively high, atabout 22.7 percent. Of most concern is the skewed distribution of growth. Economic activity hasbeen strongly concentrated in Western Province while growth in rural areas has lagged far behind.As a result, poverty in Sri Lanka today is primarily a rural phenomenon.

Sri Lanka’s slower growth and poverty reduction can be attributed, in part, to its civil conflict of 1983-2001, but ahost of other institutional, macroeconomic, and microeconomic factors have also held the country back. Thisinvestment climate assessment is aimed at understanding which factors have made it difficult forfirms to do business in Sri Lanka and how these obstacles have affected their productivity.

What are the most severe obstacles in Sri Lanka’s investment climate? To help answer that question,the assessment uses micro-level data from a survey of the urban and rural investment climatesconducted in 2004. The urban survey covered 449 formal establishments in manufacturing (textiles,garments, food and beverages, rubber products, and industrial equipment) and 94 firms in thetourism and information technology sectors. The rural survey covered 1,327 nonfarm enterprises and555 households not participating in rural nonfarm activities.1 Sri Lanka’s rural enterprises are largelybased outside the home. Most are engaged in manufacturing or trading, with a far smaller shareinvolved in services. These enterprises are small, employing an average of 2.4 workers, includingfamily members.

This investment climate assessment is the first to include an analysis of entrepreneurship in ruralareas, allowing a more comprehensive look at the business environment. Fostering the growth of therural nonfarm sector is critical to reducing poverty in Sri Lanka, still largely a rural society. Some 85percent of the population lives in rural areas and rural nonfarm enterprises contribute significantlyto GDP. The survey findings suggest that the total value added by all rural nonfarm enterprises in2003 was SL Rs 185 billion-equivalent to 12 percent of GDP or 78 percent of agricultural GDP in2003.

Strong on Governance, Weak on Infrastructure and FinanceSri Lanka stands out among developing countries for its good governance, and firms benefit fromthe low levels of red tape and corruption. But despite differences between the urban and rural

E I

investment climates, urban manufacturing and rural enterprises alike suffer from poor-qualityinfrastructure (especially energy and transport) and costly and limited access to finance (see figures 1and 2).

Success in GovernanceIn sharp contrast with neighboringcountries, Sri Lanka has made bigstrides in reducing red tape, and ithas improved the governanceframework to the point where it nolonger poses a significant obstacle todoing business. Procedures forregistering a new firm aresimple-and, unusually, morethan half of rural enterprisesare registered. The oneexception to the success storyin governance is the continuingneed to achieve peace andpolitical stability.

Weaknesses inInfrastructureElectricity, cited as a top constraintby Sri Lankan enterprises,represents an entry barrier and asignificant operational cost for bothrural and urban firms. Access toelectricity is heavilyconcentrated in urban areassuch as Western Province,leaving rural areas such as UvaProvince grossly underserved.Less than 70 percent of ruralenterprises use electricity fromthe national grid.

Where electricity is available, the costis high and supply unreliable,exposing firms to frequent outagesand raising their production costs.Unreliable supply, leads nearly 75 percent of urban manufacturing firms in Sri Lanka to own agenerator, a significantly higher proportion than competitor countries such as China (27 percent). Forthese Sri Lankan firms, generators cost the equivalent of 12 percent of their fixed assets on average-absorbing resources that could otherwise be invested productively in their core business. Not only isowning a generator costly, operating it is also expensive. It can cost 3 to 4 times as much to generateelectricity with a generator. Lack of reliable electricity reduces the productivity of urban

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

E II

0

10

20

30

40

50 Urban

Rural

Electricity Policyuncertainty

Macroinstability

Finance(cost)

Laborregulations

N/A10 th5thUrban rank

15 th2nd

3 rd2nd1st

Rural rank

5 th4th

Per

cent

age

of fi

rms

citin

gco

nstr

aint

as

maj

or o

r se

vere

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004.

FIGURE 1

Top Five Urban Constraints and Their Rural Ratings

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004.

FIGURE 2

Top Five Rural Constraints and Their Urban Ratings

Per

cent

age

of fi

rms

citin

gco

nstr

aint

as

maj

or o

r se

vere

10

20

30

40

50

Transport Finance(cost)

Finance(access)

Demand Electricity

Rural

Urban

12 thth9 thUrban rank 1stN/A

3rd2nd1stRural rank 5 th4 th4

manufacturing firms by almost half, while among rural firms the productivity of those withoutconnections to the grid is 25 percent lower than those with connections. Moreover, lack ofelectrification lessens the probability that rural households will set up a new enterprise.

Transport is the biggest constraint for rural firms. It also poses an important obstacle to urbanmanufacturing firms and the expansion of tourism. Nearly a third of rural enterprises cited transportas a major or severe obstacle to starting or operating a business. While Sri Lanka has a dense roadnetwork by regional standards, it performs poorly in road quality relative to its Asian competitors. Asmuch as 90 percent of the country’s paved road network is in poor condition because of lack ofmaintenance.

As with electricity, transport conditions vary markedly across regions, with the inhabitants ofWestern Province enjoying the greatest mobility. For rural firms the poor quality of roads and lackof transport compound marketing problems and raise transport costs, reducing productivity. Abouta quarter of urban firms also suffer transport problems, resulting in losses equivalent to 7 percent ofsales.

The telecommunications sector, an early reformer, performs much better than electricity andtransport. Even so, waiting times for new lines remain substantially longer than those in China andMalaysia.

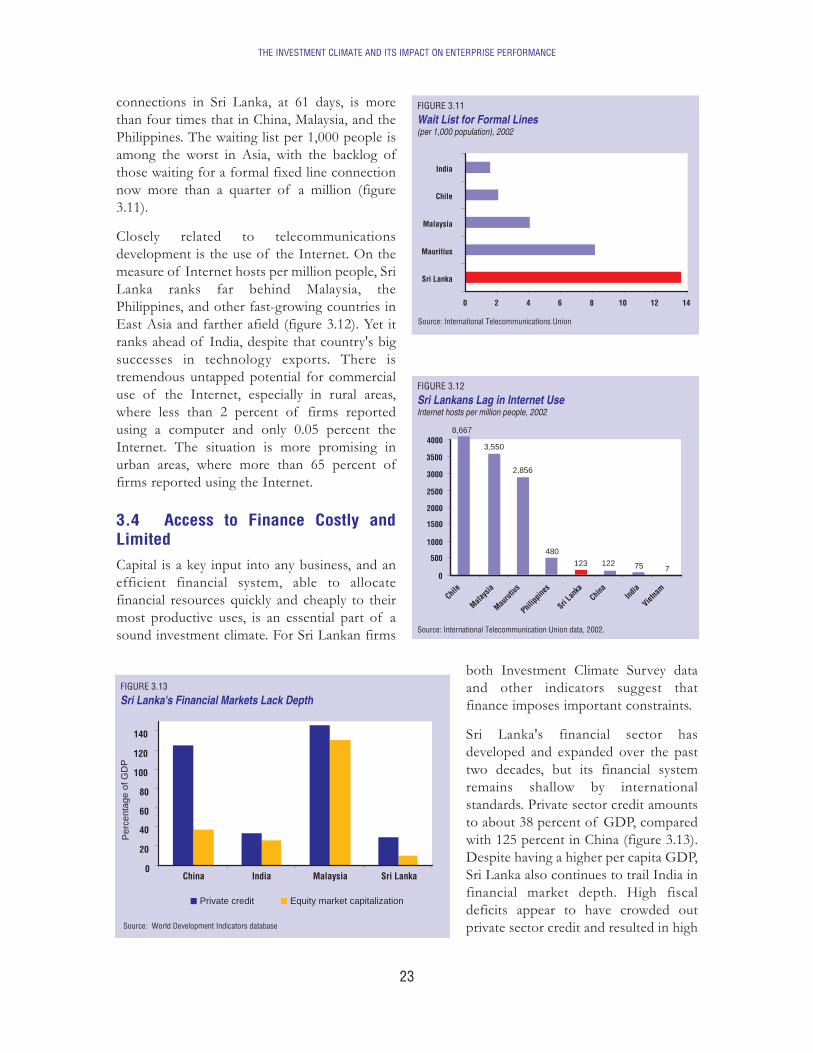

Costly and Limited Access to FinanceThe cost of finance hampers urban and rural firms alike, with almost a third of urban firms and ruralbusinesses citing it as a major constraint. Rural entrepreneurs are also constrained by limited accessto finance.

Small urban manufacturing firms pay significantly higher average interest rates (18 percent) than largeones (12 percent). They also pay higher rates than rural enterprises (14.5 percent), which benefit fromsubsidies from some state financial institutions, especially Samurdhi banks and microfinanceinstitutions. (These subsidies, however, threaten the viability of these institutions.) With supportfrom international donors, commercial banks have also started to enter the market for small andmedium-size enterprise finance, though their lending remains concentrated in Colombo. Because ofthese distortions, interest rates in rural areas vary widely. Moreover, high and persistent budgetdeficits add to the cost of finance as government crowds out the private sector to meet its borrowingrequirements.

Rural enterprises avail themselves of external finance but have extremely limited access to formal finance. Theyobtain most of their financing for new investments from internal sources (43 percent) and family andfriends (35 percent). Public financial institutions, despite a widespread presence in rural areas,account for a far smaller share of rural investment finance, while private commercial banks providea minimal share (2 percent), mostly to larger enterprises. In the urban manufacturing sector, smallfirms have less access to bank finance than large ones, forcing them to rely more on internalfinancing, leasing, and informal and family sources. For firms with inadequate external finance, theconsequence is limited opportunities for growth.

Collateral plays a vital role in the availability of finance. Results from the urban manufacturing survey showthat greater productivity does not translate into easier access to bank loans. Apparently unable todiscriminate on the basis of performance, banks instead rely heavily on the value of collateral whenconsidering a loan application. Collateral in the form of land is especially important for rural

EXECUTIVE SUMMARY

E III

enterprises. For many rural entrepreneurs, however, high levels of public landownership, unclearownership records, and widespread restrictions on the use and transfer of land make it difficult touse land as collateral, limiting access to external finance.

The Investment Climate and the External EconomySri Lanka has benefited greatly from opening its economy in the late 1970s, as evidenced by its powerful export growth.Yet it has failed to attract significant foreign direct investment. Maintaining its export growth andattracting greater foreign direct investment depend most importantly on achieving political stabilityOther factors in the country’s investment climate also affect its ability to compete internationally.

Critical Factors in International CompetitivenessSri Lankan firms have gained from international integration, as results from the Investment Climate Surveyconfirm. Exporting firms enjoy faster sales and investment growth-and the longer they have beenexporting, the higher their productivity, offering support for the "learning by exporting" hypothesis.For Sri Lankan manufacturers the two most important sources of the technological innovationcritical to this growth and productivity are acquiring new machinery and hiring key personnel-bothclosely tied to Sri Lanka’s openness. The acquisition of new machinery has been facilitated by theopen trade regime. And firms with foreign personnel-even firms with no foreign direct investment-perform better.

Despite generous fiscal incentives, flows of foreign direct investment to Sri Lanka trail behind those to other fast-growing Asian economies. In China, Malaysia, and Thailand annual investment inflows have reached orsurpassed 3 percent of GDP, while in Sri Lanka inflows averaged 1.3 percent of GDP in 1990-2002.When looking for a new facility, global corporations consider a broad set of factors that will affectproductivity and growth opportunities. Sri Lanka fares well on many of these indicators, such as askilled labor force and low levels of red tape and corruption compared with other developingcountries. Moreover, its ports and customs are more efficient than those of competitors such asChina and India, though there is scope for greater improvement. Sri Lanka performs poorly in manyother aspects of the investment climate, however, particularly political stability, economic certainty,quality of infrastructure, and predictability of labor regulations. While the Board of Investment seeksto facilitate each stage of the investment process, survey findings suggest that it has been unable toisolate firms from most problems in the investment climate. Manufacturing firms benefiting from itsregime are no more productive than others.

Political stability is a critical factor in the business environment. Sri Lanka remains among the world’s mostunstable countries, though it has made great strides since reaching a cease-fire in 2001. Although thenortheast is likely to gain most from the eventual peace settlement, the overall economy will benefitfrom greater ability to attract foreign direct investment and lower insurance costs for enterprises.

The civil war fought between 1983 and 2001 has not been the only source of instability; in the past four years SriLanka has had three different governments. The frequent changes in government have disruptedpolicymaking and slowed reform. Not surprisingly, economic and regulatory policy uncertainty ranksas the second most important constraint for urban manufacturing firms, with more than a third ofthese firms (though less than 5 percent of rural firms) citing it as a major or severe obstacle to doingbusiness (see figure 1). Nearly a third of urban manufacturing firms regard macroeconomicinstability as a major or severe constraint. Such perceptions also hold among foreign investors: whenpolitical uncertainties resurfaced in late 2003, foreign investors considering Sri Lanka as a locationput their plans on hold.

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

E IV

Also an important constraint are Sri Lanka’s labor regulations, ranked among the top five obstacles in theinvestment climate by urban manufacturing firms. Rigid, inflexible, and arbitrary, these regulationsoffer no certainty to investors and discourage increased employment. Payments mandated forredundancy in Sri Lanka are many times those legislated in other Asian countries. Perhaps mostrestrictive is the Termination of Employment of Workers Act of 1971, which makes it very difficultfor firms to fire or lay off workers. Firms can try to avoid restrictive labor regulations by hiringtemporary workers, but this too has costs: survey results show that the larger the share of temporaryworkers in a firm’s employment, the lower its productivity.

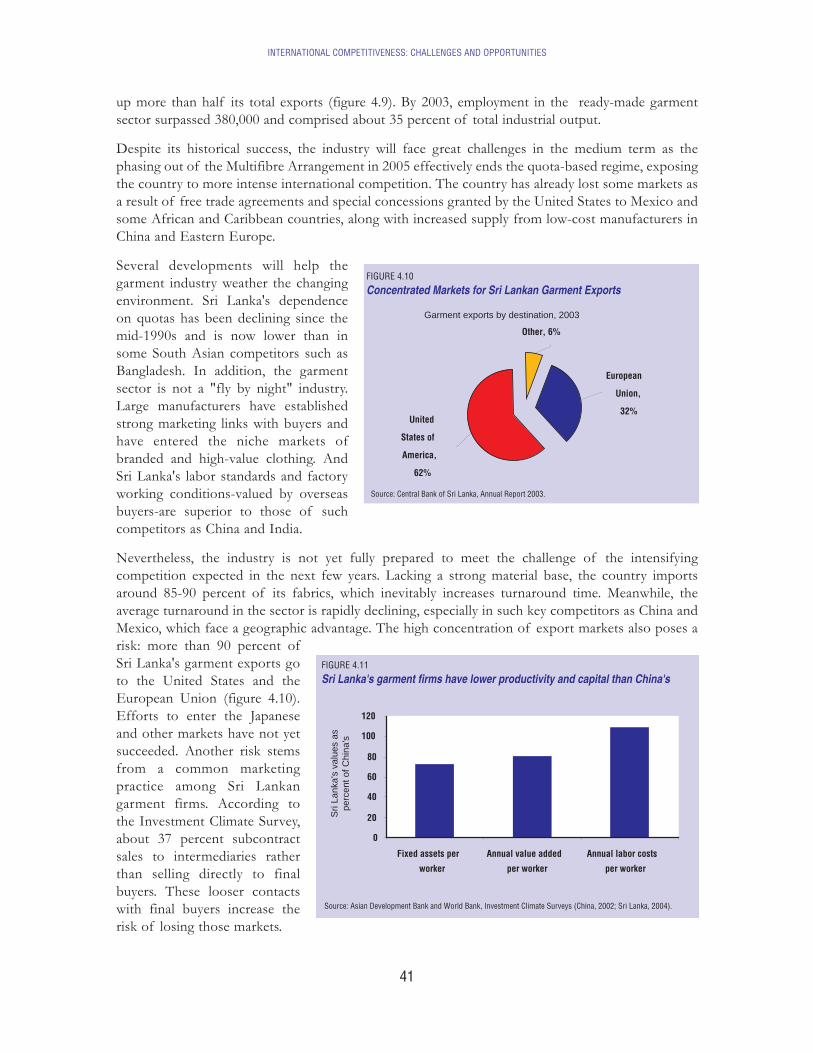

Performance and Challenges of Key Export SectorsThe economic prospects of Sri Lanka, as a small, open economy, depend on maintaining robust export growth. Oneof its biggest economic success stories is the development of the garment sector, which accounts formore than half the country’s exports. This concentration of exports, however, means that thephasing out of the Multifibre Agreement poses new challenges. This situation highlights the need fora better investment climate to maintain the competitiveness of the garment sector and support thediversification of exports.

Recent developments will help the garment industry weather the change in the international environment. Sri Lanka’sdependence on quotas has been declining since the mid-1990s, and large manufacturers have enteredthe niche market of branded and high-value clothing. Nevertheless, competition in the sector willintensify in the next few years, and the industry will have to prepare itself to meet this challenge.Lacking a strong material base, the country imports around 85-90 percent of its fabrics, whichinevitably increases turnaround time. Meanwhile, the average turnaround in the sector is rapidlydeclining, especially in key competitors such as China. The high concentration of export markets forthe garment sector also poses a risk.

How competitive are Sri Lankan garment firms today? A comparison with Chinese garment firms, based onInvestment Climate Survey data, shows that Sri Lankan firms have lower value added per worker.This difference can be attributed in part to higher capital investment by Chinese firms. Otherinvestment climate indicators also seem to favor Chinese firms, including access to more reliableenergy, lower inventories, lower subcontracting of sales to clients, and greater investment in formaltraining.

Sri Lanka’s tourism industry stands to benefit greatly from a sustained peace and could become an important newsource of foreign exchange and rural and urban employment. After facing bright prospects in the 1970s,tourism collapsed with the onset of the civil conflict. While the sector struggled to survive in SriLanka, it expanded rapidly in neighboring destinations. Today tourism accounts for less than 5percent of Sri Lanka’s export revenue, while it contributes nearly 10 percent in Thailand and 25percent in Mauritius.

The sector rebounded after the cease-fire, and the country offers a range of attractions catering to alarge tourism market. Yet it continues to face important constraints on its ability to compete withother destinations in the region. Many of these constraints are shared with urban manufacturingfirms, including macroeconomic instability, economic policy uncertainty, and the poor quality ofinfrastructure. Tapping tourism’s potential will require substantially upgrading basic infrastructure, tointegrate rural areas and spread the benefits to a larger number of provinces. Tourism so far has beenconcentrated in the South Coast while the potential of other provinces-such as North Central, Uva,and Sabaragamuwa-has been neglected.

EXECUTIVE SUMMARY

E V

Though still in a nascent stage, the information technology industry in Sri Lanka is growing rapidly. Most of itsrevenue still comes from the domestic market, but firms continue to expand their services to foreignmarkets, indicating that the industry has the potential to compete internationally. Survey resultssuggest that 60 percent of information technology firms are exporters and about 30 percent receiveforeign investment.

Before the industry can fully exploit the opportunities in the international market, however, it mustfirst overcome obstacles to business development. Some of these cut across sectors, such asmacroeconomic instability. Sri Lankan software companies also identified skills, education, andtelecommunications as among their most important constraints-unsurprising, given the sector’s heavyreliance on skilled labor and telecommunications. The government has already recognized theimportance of training and plans a comprehensive program to promote training in informationtechnology skills throughout the country. In telecommunications, further reforms and privatizationare needed to promote expansion and competitiveness and provide a stronger development platformfor the software industry.

The Investment Climate for Rural FirmsFor rural entrepreneurs a big constraint is limited access to regional markets (see figure 2). These entrepreneurscite marketing problems, particularly lack of demand, as a major obstacle. The problems stem froma range of factors. Rural entrepreneurs have few contacts or links with larger firms or buyers thatcould increase their exposure to bigger and more diverse markets. Most are unable to realizeeconomies of scale and face high marketing costs. The goods they produce are often of low qualityand have limited appeal in larger markets. Poor transport and telecommunications restrict their accessto information.

Moreover, the voices of rural entrepreneurs have not been heard. Evidence suggests that rural enterprises arenot yet effectively integrated into the policymaking process. Less than 10 percent of enterprises withmore than three workers believe that they can influence the content of existing or proposed lawsrelating to their business. The government could do more to strengthen mechanisms ensuring greatervoice for rural entrepreneurs.

The Investment Climate in Disadvantaged RegionsTwo regions of Sri Lanka are particularly disadvantaged: the northeast, which has suffereddisproportionately from the conflict, and the south, which suffers disproportionately from poverty.

The Northeast: An Investment Climate Constrained by Conflict In the Northeast Province, the site of most of the fighting during the conflict, businesses appear to have been establishedas part of household coping strategies and have been unable to grow in the difficult circumstances. Enterprises in theregion are typically smaller and much more likely to engage in household-based production thanenterprises in other areas. Production enterprises account for 60 percent of firms in the northeast,compared with 36 percent elsewhere. This structure suggests that entrepreneurs were unwilling toinvest in alternative premises for their business that might be destroyed in the fighting or that mighthave to be evacuated.

The insecurity has imposed a high cost. As many as 20 percent of firms in the northeast haveincurred losses as a result of crime and violence in the past year, compared with just 1-2 percent inthe rest of the country. In addition, much of the local infrastructure was destroyed during the

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

E VI

conflict. Not surprisingly, a larger share of rural firms in the northeast than in the rest of the countryconsider public infrastructure to be a constraint.

The South: Poverty and Poor Service DeliveryExcluding the northeast, where poverty data are not yet available, the southern provinces of Uva andSabaragamuwa have the country’s highest poverty rates. In Uva Province one symptom of poverty isthe small manufacturing base in rural areas: half its rural enterprises are trading firms, which requirefewer assets than production firms. Given the lower incomes in Uva, it is unsurprising thathouseholds resort to small services and trading businesses to smooth their incomes during the slackagricultural periods. Uva also stands out for its greater problems in access to services. Only 62percent of its enterprises use electricity, compared with an average of 69 percent in the rest of thecountry. Its rural firms also are physically isolated, limiting their access to markets.

RecommendationsAchieving a permanent peace is undoubtedly the most important step Sri Lanka can take toward improving itsinvestment climate. The survey results highlight other areas warranting urgent consideration. Policiespaying greater attention to the differences between the urban and rural investment climates could domuch to increase rural employment and incomes and reduce the tremendous disparities betweenregions. Among the five most important issues in the investment climate, however, some arecommon to both urban and rural firms.

Improving Access to and the Quality of Energy and Transport (Urban and RuralFirms)Sri Lanka is already undertaking several important energy reforms, including restructuring the CeylonElectricity Board under the Electricity Reform Act of 2002 and establishing the Public UtilitiesCommission of Sri Lanka. Continuing to implement the regulatory framework is also a priority forthe energy sector. In the medium term essential reforms include introducing competition andcommercial relationships within the industry to drive improvements in performance. They alsoinclude establishing transparent and efficient subsidy mechanisms to help expand access to electricityin rural areas.

In the road sector the main policy priorities are driven by lack of access to good-quality roads, a keyimpediment to existing businesses and a severe barrier to starting or participating in rural nonfarmenterprises. Priority actions include providing adequate funding for maintaining and rehabilitatingroads, selecting a core network of roads to be maintained, developing an overall pricing policy forthe sector, and strengthening the capacity of agencies responsible for formulating and implementingsector policies.

Reducing the Cost of Finance and Improving Access to It (Urban and Rural Firms)Reducing the cost of finance in Sri Lanka will require stabilizing the macroeconomic situation, reducing the deficit,and reforming the two state-owned commercial banks, the Bank of Ceylon and the People’s Bank. Other key policypriorities in the finance sector include enhancing debt recovery mechanisms, expanding andupgrading the capacity of the Credit Information Bureau, improving the regulatory framework formicrofinance institutions, and reforming the contractual savings system.

EXECUTIVE SUMMARY

E VII

Improving Labor Market Flexibility (Urban Firms)In 2003 the government moved to reform labor regulations. While the details of the proposedreforms remain under discussion, they include introducing a formula for employee severancepayments, imposing strict limits on the duration of labor tribunal cases, and establishing anunemployment benefit system. To encourage foreign direct investment, foster efficient reallocationof labor, and promote employment in the formal sector, Sri Lanka also needs to transform itsdiscretionary and costly severance payment into modern, affordable, and equitable income supportfor the unemployed. This support need not take the form of unemployment insurance, however,since current conditions may not favor the effective operation of such a system.

Improving Access to Major Markets (Rural Firms)Beyond enhancing the coverage and quality of rural infrastructure, several other initiatives would also help improveaccess to markets for rural firms. Business organizations and local chambers of commerce couldstrengthen marketing channels for rural enterprises by holding product fairs to expose localproducers to buying habits and consumer behavior in different markets, helping to develop businessdirectories, and sharing information on prices, quality standards, and ways to obtain technical andfinancial services for greater value addition. In addition, supporting group marketing (for example,through associations and cooperatives) and business clusters would help rural firms take advantageof scale economies.

Improving Policy Certainty and Macroeconomic Stability (Urban Firms)As the survey revealed, policy uncertainty and macroeconomic instability have a tremendously adverse effect on urbanenterprises. A policy framework geared to improving policy certainty and macroeconomic stabilitywould include reducing the deficit and public debt, strengthening revenue collection through bettertax administration, reforming the civil service and reducing the wage bill, and decreasing the lossesof state-owned enterprises.

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

E VIII

Notes

1. For the purposes of the survey, rural nonfarm enterprises were defined as any income-generating activity(trade, production, or services) not related to primary production (crops, livestock, or fisheries)undertaken within the household or in any nonhousing unit. Any value addition to primary production(processing) was considered to be a rural nonfarm activity.

INVESTMENT CLIMATEMATTERS

1.1 What is the Investment Climate and Why Does it Matter?There is growing recognition around the world of the importance of a sound investment climate forgenerating economic growth and poverty reduction. Few now accept the simplistic view that greaterinvestment alone will lead to higher growth. Instead, the prevailing view emphasizes building aproductive environment in which private businesses can flourish. Although the term investment climateis used broadly, here it is taken to mean the policy, regulatory, institutional, and governanceenvironment that supports (or fails to support) entrepreneurship and efficient markets.

Despite the greater awareness of the importance of the investment climate, until recently little workhad been done to systematically gather objective measures of the investment climate or to link thesemeasures directly to the performance of firms. In Asia such work is being undertaken by the WorldBank and the Asian Development Bank, together with Asian governments and other developmentpartners, through a series of investment climate assessments, each based on a representative nationalsurvey of enterprises.1 The assessments measure how conducive a country’s investment climate is tocreating economic growth and benchmark the country against its neighbors and competitors. Thisassessment of Sri Lanka is based on an Investment Climate Survey conducted in 2004 (box 1.1).

Why Undertake an Investment Climate Assessment in Sri Lanka? In Sri Lanka, despite an open trade and foreign investment regime and recent steps toward peace,considerable barriers to investment remain. Indeed, Sri Lanka attracts significantly lower levels ofdomestic and foreign investment than countries with similar incomes. The host of institutional,macroeconomic, and micro-economic factors that hamper investment inhibit the country’s potentialfor growth and poverty reduction.

Boosting investment and its productivity requires a concerted effort by the government to improvethe investment climate. The government has initiated reforms in the financial, labor, and land sectorsto address some of the barriers. To build on these initial efforts, a better understanding is needed ofthe microeconomic constraints facing firms and the effects of these constraints on productivity. Byquantifying the costs associated with barriers to investment, this study can help policymakers identifythe areas most in need of reform and monitor improvements in the investment climate over time.

Why Undertake an Assessment of the Rural Investment Climate?The vast majority of investment climate assessments around the world have focused on factorsinfluencing entrepreneurial initiative and performance in the urban formal sector, most often inmanufacturing. This assessment of Sri Lanka is among the first to take a more comprehensive lookat the business environment by extending beyond major urban centers to analyze entrepreneurshipin rural areas as well.

CHAPTER ONE

1

Enterprises in the urban formal sector can generally be easily identified through a company register.By contrast, identifying rural enterprises, many of which operate informally, can be difficult, time-consuming, and costly. Yet understanding the rural investment climate can be essential in efforts toengender pro-poor growth. In Sri Lanka the rural nonfarm sector is critical to growth and povertyreduction. Still a rural society, the country has 85 percent of its population in rural areas, but only 32percent of its labor force in agriculture.2 A recent World Bank study of Sri Lanka (2002a) revealedthat a large share of rural households and rural poor depend on the rural nonfarm sector foremployment and income.

The findings of this investment climate assessment confirm that rural households with nonfarmenterprises are significantly better off than those relying solely on agricultural income. The results alsoconfirm that the investment climate has important effects on the performance of rural nonfarmenterprises-and thus on overall employment growth, poverty reduction, and development in rural areas.

1.2 Overview of the Economy: Achievements and ChallengesDespite a civil conflict extending over the past two decades, Sri Lanka has achieved a socioeconomicperformance quite remarkable in the developing world. Yet challenges remain. Sri Lanka has fallenshort of its growth potential for a host of reasons, the most important being the prolonged civilconflict. Structural rigidities in the economy also continue to constrain its growth. Sharpeningregional disparities in growth and poverty reduction are another cause for concern.

Social and Economic Progress in the Midst of Civil WarSri Lanka began liberalizing its economy in the late 1970s, much earlier than other South Asiancountries. By the 1980s, thanks to privatization, trade liberalization, and financial sector reform, thecountry could provide a more favorable investment climate for foreign investors. Continuing itsreforms over the past decade, Sri Lanka privatized many public entities, including its plantations,national airline, and telecommunications corporation. These policy changes, together with thecountry’s strong human resource base, have fostered healthy export performance, especially in teaand garments. The services sector has also grown steadily, benefiting from greater banking activity,the liberalization of telecommunications services, and expanding tourism and regional containertraffic. Today Sri Lanka ranks among the most open economies in South Asia, with exports andimports amounting to 78 percent of GDP and a foreign investment regime that is among the mostliberal in the developing world (Central Bank of Sri Lanka, Annual Report 2003).

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

2

BOX 1.1

The Investment Climate Survey in Sri Lanka: Coverage and Methodology

What are the most severe obstacles in Sri Lanka’s investment climate? To help answer that question, the Asian Development Bank andthe World Bank-together with Sri Lanka’s Department of Census and Statistics and A. C. Nielsen-conducted a survey of the urban andrural investment climates in 2004. The urban survey covered 449 formal establishments in five key manufacturing sectors (textiles,garments, food and beverages, rubber products, and industrial equipment) and 94 firms in tourism and information technology, allsectors important to the external economy. The sample covers both Western Province and districts outside it.

The rural survey had four parts: an enterprise survey, a survey of households not engaged in nonfarm activities, a community survey,and a price module. Designed to be as comparable as possible to the urban survey, the rural enterprise survey covered 1,327 nonfarmenterprises operated within a household or as a stand-alone establishment. An additional 555 randomly selected households notparticipating in rural nonfarm activities were surveyed to capture factors influencing the decisions of households on whether to engagein such activities. Households and enterprises were selected from 147 rural communities (grama niladharis) spread across all provinces.For the purposes of the survey, rural nonfarm enterprises were defined as any income-generating activity (trade, production, orservices) not related to primary production (crops, livestock, or fisheries) undertaken within the household or in any nonhousing unit.Any value addition to primary production (processing) was considered to be a rural nonfarm activity.

For more detail on the methodologies used to define the sample design of the urban and rural surveys, see appendixes 1-3.

Investments in human developmenthave produced remarkableoutcomes in health and education,where indicators have reached levelsclose to those of industrialcountries (table 1.1). Free anduniversal health and educationservices, a focus on gender equality,and extensive social welfareprograms have been core featuresof the country’s social policies forseveral decades. Sri Lanka hasalready achieved many of theMillennium Development Goals.

By contrast with its impressive human development record, Sri Lanka’s economic growth and povertyreduction have been less noteworthy, especially when compared with achievements in East Asia. Inthe 1960s Sri Lanka had a per capita income comparable to those in the Republic of Korea, Malaysia,and Thailand (figure 1.1). Today its per capita income is less than a tenth of Korea’s, less than afourth of Malaysia’s, and less than half of Thailand’s. Not surprisingly, Sri Lanka has also madesmaller gains in poverty reduction. The share of the population in poverty (poverty headcount)remains comparatively high, at about 23 percent-a rate similar to Indonesia’s 27 percent but higherthan Malaysia’s 15 percent and Thailand’s 13 percent.3

The slow pace of growth and poverty reduction in the past two decades can be attributed in part tothe civil conflict, estimated to have cost the country 2-3 percentage points of GDP growth a year(Central Bank of Sri Lanka, Annual Report 1998). A host of other factors have also held Sri Lankaback. One such factor has been a reluctance to continue progressive social and economic policies inthe past decade-policies that might have helped reorient the role of the state toward improving

opportunities for privatesector-led growth andproviding better public servicesto the population. The policyshift stems in part from lack ofstrong political leadership andthe accommodation ofminority interests by successivegovernments. Also slowingreform have been a lack ofconsensus on vital developmentissues among the major politicalparties and frequent changes ofleadership, with Sri Lankaholding three general electionsin the past four years.

INVESTMENT CLIMATE MATTERS

3

Source: World Bank, World Development Indicators database.

FIGURE 1.1

Missed Opportunities for Economic Growth in Sri Lanka

0

2000

4000

6000

8000

10000

12000

1962

1967

1972

1977

1982

1987

1992

1997

2002

GN

I per

cap

ita (

U.S

. dol

lars

)

Korea, Rep. of

Sri Lanka

Thailand

Malaysia

TABLE 1.1

Selected Human Development Indicators, Sri Lanka, 2002

Life expectancy (years) 74

Maternal mortality ratio (per 100,000 live births) 23

Child mortality rate (per 1,000) 16

Net enrollment at first grade (percent) 106

Literacy rate (percent) 92

Net primary completion rate (percentage of age group) 95

Source: World Bank, World Development Indicators database.

A Decline in Agriculture, a Rise in IndustryThe reform efforts of the late 1970s transformed the structure of the Sri Lankan economy. Althoughthe services sector continues to dominate the economy, accounting for more than 50 percent ofGDP, in the early 1990s industry overtook agriculture to become the second largest sector (figure1.2). It now contributes about 27 percent of GDP, compared with agriculture’s 20 percent. Duringthe 1990s, boosted by liberalization, industry grew by 6.8 percent a year and services by 5.7 percent-compared with only 1.9 percent for agriculture, still heavily constrained by interventionistgovernment policies. Nevertheless, agriculture continues to employ 32 percent of the labor force,while industry provides employment for only 24 percent.4

With the liberalization of the economyand the establishment of exportprocessing zones, manufacturing beganto cater to the international market,strengthening its competitiveness,especially in apparel. The gradualrelaxation of tariffs-from a prohibitiveand distortionary system in the 1970s toa three-band system with a maximumtariff of 25 percent-also fosteredgreater competitiveness in industrywhile agriculture, continuouslyprotected, lagged behind. To helpcounter initial obstacles faced byindustrial exporters, the governmentprovided an extensive package ofincentives-duty rebates, concessionaryexport financing, cash grants forexporters, and tax holidays-starting inthe 1970s and 1980s. (These incentivesremain in place, though some weremeant to be temporary measures tostimulate production.) Manufacturingexports took off, growing by 32 percenta year (in U.S. dollars) between 1978 and1995. As a result, the industrial exportshare increased markedly-from 14percent in 1977 to 72 percent in 1992and 78 percent in 2000 (figure 1.3).Reflecting this rapid growth inmanufacturing and exports, privateinvestment rose from the low levels ofthe 1960s and early 1970s (table 1.2).

Domestic Policy Challenges While international trade has beensubstantially liberalized, domestic

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

4

0

10

20

30

40

50

60

1971 1981 1990 1995 2000 2003

Source: Central Bank of Sri Lanka, Annual Report, various years.

FIGURE 1.2

Industry Overtakes Agriculture in Sri Lanka

Services

Industry

Agriculture

Sha

re o

f val

ue a

dded

in G

DP

(pe

rcen

t)

0

10

20

30

40

50

60

70

80

90

1972 1977 1982 1987 1992 1997 2002

Industrial exports as percentage of total

Exports as percentage of GDP

Source: Central Bank of Sri Lanka, Annual Report 2003.

FIGURE 1.3

Industrial Exports Lead the Way for Sri Lanka

Per

cent

structural rigidities continue to constrain economic growth. Factor markets in labor, finance, and, toa lesser extent, land are neither sufficiently well developed nor flexible enough for Sri Lanka to beinternationally competitive. Besides reforming its factor markets, Sri Lanka also needs to limit itsfiscal deficit and maintain macroeconomic stability-severe challenges made all the more difficult bythe size of the civil service and the public sector’s continuing intervention in the economy.

Labor regulations have been designed to protect the few who are employed in the formal sector-apolicy that has restricted labor mobility, limited productivity improvements, increasedunemployment, and hindered investment. Indeed, Sri Lanka’s labor policies offset the benefits of awell-educated labor force. Despite having eight years of schooling on average, workers in Sri Lankaearn wages no higher than those in neighboring countries, where workers have much less schooling.Unemployment, especially among educated youth, has risen as a result.

Sri Lanka’s financial sector, benefiting from liberalization, has grown and become more dynamic overthe past two decades. Nevertheless, banks continue to dominate the landscape, intermediating nearly55 percent of assets. State participation in banking has declined significantly since 1980, when the

two state-owned banks controlled 74 percent ofassets. Public financial institutions remain themost important players, however, with the twostate-owned banks still holding 46 percent ofbanking assets today. Financial intermediation isinefficient, as evidenced by large intermediationspreads and a narrow range of financialinstruments.

Slow and insufficient adjustment of the publicsector, together with the civil conflict, has led topersistent budget deficits, averaging 10 percentof GDP since the 1980s and resulting in highlevels of public indebtedness. At the end of2003 public debt reached 105.9 percent of GDP.In the past the government managed to financehigh deficits and maintain growth by relying onsignificant concessional foreign borrowing and

INVESTMENT CLIMATE MATTERS

5

Functional classification of spending, 2003

Interest 29%

Other 6% Civil Service 7%

Defense 14%

Education 9%

Health 7%

Welfare and Housing 12%Energy 6%

Transport 6%

Agriculture andFisheries 4%

Note: Defense includes public order.Source: Sri Lanka, Ministry of Finance data.

FIGURE 1.4

Interest Payments a Heavy Burden in Sri Lanka

TABLE 1.2

Investment and Savings as a Share of GDP, Sri Lanka, Selected Years, 1960-2003 (percent)

Indicator 1960 1975 1980 1985 1990 1995 2000 2003

Investment 15 16 34 24 22 26 28 22

Private 10 10 25 19 18 22 25 17

Public 5 6 9 5 4 4 3 5

Gross domestic savings 12 8 11 12 14 15 17 16

Gross national savings 11 7 14 14 17 19 21 21

Source: Central Bank of Sri Lanka, Annual Report, various years.

by engaging in financial repression-that is, by borrowing at below-market rates, especially through thecontractual savings system. Government borrowing continues to crowd out the private sector andkeeps interest rates high. Without a strong adjustment, fiscal policy will not be sustainable.

Despite the high fiscal deficits, Sri Lanka’s budget does little to promote good public services andeconomic growth. An oversized public sector and burdensome interest payments on domestic debt-payments that consume almost a third of the budget-make it difficult to reallocate spending (figure1.4). Sri Lanka has the largest bureaucracy per capita in Asia, with one million employed in the civilservice and semigovernment institutions (Central Bank of Sri Lanka, Annual Report 2003). Inaddition, defense constitutes the second largest spending category in the budget. Decisively endingthe civil conflict is therefore the most important step toward both reducing the fiscal deficit andgreatly improving the investment climate.

The high deficits have squeezed critical spending on social services and infrastructure. There aresigns that the quality of social services is suffering, which is bound to undercut Sri Lanka’s greatprogress in human development over the past few decades (World Bank 2002b). Capital spending hasbeen drastically cut back. Public investment in infrastructure fell from around 7 percent of GDP in1990 to half that level by 2000, contributing to a sharp deterioration in physical infrastructure andundermining Sri Lanka’s competitiveness. Although road density is relatively high by regionalstandards, the condition of the road network has markedly declined. Similarly, while access toelectricity expanded significantly in the past two decades, Sri Lanka has experienced chronic powershortages since the mid-1990s as a result of droughts and a failure of supply to keep up with demand.The effect of this situation on the investment climate shows up clearly in the survey results (seechapter 3).

Growing Regional DisparitiesGrowth and poverty reduction have been heavily skewed toward Western Province, with rural areaslagging behind (figure 1.5). In the 1990s economic activity became even more concentrated aroundWestern Province, whose share of GDP rose from 40 percent in 1990 to nearly 50 percent by theend of the decade. Meanwhile the combined share of Uva, North Central, and the former Easternand Northern Provinces fellfrom 22 percent to 15 percent,with the former NorthernProvince recording the worstperformance because of thecivil conflict.5 These regionaleconomic differences havetranslated into growing regionaldisparities in the incidence andseverity of poverty. While theincidence of poverty hasdeclined substantially inWestern Province, dropping toaround 11 percent by 2002, itremains above 20 percent in therest of the country and as highas 37 percent in Uva (figure1.6).

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

6

North

Cen

tral

Saba

raga

muw

a

Cent

ral

Uva

East

ernC

ontr

ibut

ion

to G

DP

by

prov

ince

(per

cent

), 2

002

0

10

20

30

40

50

Wes

tern

Sout

hern

North

Wes

tern

North

ern

Source: Central Bank of Sri Lanka, Annual Report, 2003.

FIGURE 1.5

Sri Lanka's Growth Concentrated in Western Province

One reason for the sharpening disparities is the concentration of export processing zones in WesternProvince. Another is the sluggish growth in agriculture, which has contributed to slower economicgrowth and poverty reduction in other provinces. The meager growth in agriculture compared withmanufacturing and services reflects in part the sector’s low productivity, which stagnated in the 1990s.It also stems from the failure of economic liberalization to reach agriculture, which remains highly

protected. Public interventionsin agricultural commodity andfactor markets haveunintentionally createdobstacles and disincentives thathave hindered productivitygrowth and discourageddiversification, bindingagricultural households to low-value activities such as paddyproduction. The findings of theinvestment climate assessmentalso point to obstacleshampering the growth andproductivity of ruralenterprises and to opportunitiesfor reducing rural poverty.

INVESTMENT CLIMATE MATTERS

7

Pov

erty

rat

e by

pro

vinc

e (

perc

ent)

, 200

2

11

2125

27 28

3437

0

10

20

30

40

Wester

n

North C

entra

l

Centra

l

North W

ester

n

Southe

rn

Sabara

gamuw

aUva

Source: World Bank staff estimates.

FIGURE 1.6

Poverty Still High Outside Sri Lanka's Western Province

Notes

1. The World Bank is conducting similar studies in other regions.2. Data are from the 2001 Census and 2003 Labor Force Survey (fourth quarter), conducted by the Sri Lanka

Department of Census and Statistics.3. These estimates are based on comparable national poverty lines. Based on internationally comparable

poverty lines, Sri Lanka also has higher poverty than Thailand and Korea. See World Bank (2003b; 2004b,table 1).

4. Data are from the 2003 Labor Force Survey (fourth quarter), conducted by the Sri Lanka Department ofCensus and Statistics.

5. Although Northern and Eastern Provinces were provisionally merged in 1987, data continue to becollected at the district level, making it possible to present data separately for the districts in the formerNorthern Province and those in the former Eastern Province. The report presents disaggregated datawhere warranted by differences between the two areas, using the former provincial names in figures andtables showing such data. This should not be taken to imply any judgment on the legal status of districtsor provinces in Sri Lanka or the endorsement or acceptance of such boundaries.

THE DIFFERENTPROFILES OF URBAN ANDRURAL ENTERPRISES

The urban and rural enterprises surveyed in Sri Lanka have sharply different profiles, and thedifferences are accentuated by the coverage of the urban manufacturing survey, limited to formalfirms.1 Urban enterprises tend to be older and much larger than their rural counterparts. Large-scalemanufacturing is concentrated around Colombo-though geographic distribution differs markedlyacross sectors-and is oriented toward exporting. Rural enterprises are likely to be a soleproprietorship headed by a male, based outside the home, and established using household savings.Their managers have education levels suggesting great potential for improving productivity andintroducing new technologies in Sri Lanka’s ruralareas. Rural enterprises in North EasternProvince have very different characteristics thanthose elsewhere in the country, largely because ofthe conflict.

2.1 Great Diversity in the EnterpriseLandscapeWhat makes up the diverse landscape ofenterprises in Sri Lanka? A large part of itconsists of an estimated 16,405 manufacturingenterprises operating in urban areas, and another620,000 enterprises in rural areas. Ruralenterprises employ some 1.5 million workers,about 20 percent of the country’s labor force.Contrary to popular opinion, the majority (59percent) of rural businesses are stand-aloneenterprises-that is, have a place of business otherthan the home. Because the survey excludedinformal firms operating in urban areas, allcomparisons of urban and rural firms refer toformal firms in urban manufacturing and bothformal and informal enterprises in rural areas.

What Firms Do-and WhereIn urban areas the five most importantmanufacturing activities-accounting for nearly 50percent of all urban manufacturing enterprises-

CHAPTER TWO

8

TABLE 2.1

A Snapshot of Urban Enterprises in Key ManufacturingSectors, Sri Lanka(percent, except where otherwise indicated)

Indicator Value

Share of firms with export orientationa

Garments 94

Rubber products 75

Food and beverages 62

Industrial equipment 41

Textiles 35

Share of firms with foreign direct investment

Garments 23

Rubber products 31

Food and beverages 9

Industrial equipment 27

Textiles 16

Share of firms in Western Province 56

Median number of workers 105

Male managers as a share of total 88

Share of managers with university degree 45

Average age (years) 30

Annual value added per worker (Sri Lankan rupees) 411,257

a. Firms exporting more than 10 percent of sales.

Source: Asian Development Bank and World Bank, Sri Lanka Investment ClimateSurvey, 2004.

are ready-made garments, textiles, industrialequipment, food and beverages, and rubber.Urban manufacturing activity is largely exportoriented, especially in garments (where 93.5percent of the firms surveyed export more than10 percent of sales), rubber (75.4 percent), andfood and beverages (62.2 percent; table 2.1)).Manufacturing is heavily concentrated in theColombo metropolitan area, though geographicdistribution varies across sectors. While garmentand industrial equipment firms are limitedlargely to the Colombo area, nearly three-quarters of food and beverage firms operateoutside Colombo, probably to be closer tosupplies. Textile enterprises are divided almostequally between Colombo and other urbancenters.

Most rural nonfarm enterprises are involved inproduction (41 percent) or trading (38 percent),with a far smaller share in services (21 percent;table 2.2). Around 10 percent are engaged in themanufacture and sale of processed agriculturalgoods. Nonagricultural production focusesmainly on manufacturing such goods asgarments, nonmetallic mineral products,furniture, and wood products. Most rural trading establishments are engaged in selling processed (65percent) and unprocessed agricultural products (57 percent). As would be expected, there is muchvariation among service-related enterprises, with the largest share engaged in repair services (24percent), followed by personal services (17 percent) and hotels (14 percent).

Rural nonfarm enterprises are scattered throughout the country. Western Province has the greatestconcentration, with more than 20 percent, followed by North Eastern and Southern Provinces

(figure 2.1). The large share of nonfarmenterprises in North Eastern Provincerelative to its share of the rural populationmay reflect the conflict in the region. Manyhouseholds appear to have forgoneagricultural activities and started smallbusinesses operating in their home as aresponse to the uncertainty and thepotential for loss.

Firms’ Workers and Their Skills The split between urban and ruralenterprises is not simply one of location butalso one of size: on average, urbanenterprises are significantly larger than their

THE DIFFERENT PROFILES OF URBAN AND RURAL ENTERPRISES

9

TABLE 2.2

A Snapshot of Rural Enterprises in Sri Lanka(percent, except where otherwise indicated)

Indicator Value

Number of enterprises 620,000

Number of workers 1,500,000

Share of firms producing for domestic market 99

Sole proprietorships as a share of total 98

Share of firms headed by a male 75

Stand-alone businesses as a share of total 59

Firms by sector

Production 41

Trade 38

Services 21

Share of firms in Western Province 20

Average number of workers 2.4

Family members as a share of workforce 50

Share of managers with university degree 2

Average age (years) 9

Share of firms registered 53

Annual value added per worker (Sri Lankan rupees) 93,763

Source: Asian Development Bank and World Bank, Sri Lanka Investment ClimateSurvey, 2004.

FIGURE 2.1

Sri Lanka's Rural Enterprises are Scattered Across Provinces

0

5

10

15

20

25

30

Wes

tern

North

Eas

tern

Sout

hern

North

Wes

tern

Saba

raga

muw

a

Cent

ral

North

Cen

tral

Uva

Per

cent

Nonfarm enterprises

Rural population

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004; Sri Lanka Department of Census and Statistics data.

rural counterparts. The median number of workers employed by urban manufacturing enterprises isroughly 105, including 15 temporary workers. By contrast, rural enterprises employ 2.4 workers onaverage, including family members. Family members account for almost half the workforce in ruralnonfarm enterprises, with the largest share in trading enterprises (60 percent) and the smallest inproduction (42 percent). Production enterprises also tend to be larger, with 3 workers on average. Thelargest rural enterprise in the survey has 181 workers. Only 6 percent of rural enterprises have morethan 5 workers.2

In urban manufacturing about 45 percent of senior managers have a university degree, and more thanhalf of these also have a professional qualification. Less than 6 percent had failed to completesecondary school. In rural firms almost half the managers have completed 10 or more years ofeducation and nearly all are literate, indicating great potential to improve productivity and introducenew technologies in the country’s rural areas. Only 1 percent had no schooling at all. In Bangladesh,by contrast, a similar survey of the rural nonfarm sector found that 34 percent of owners or majoritypartners had no formal education.

Although women represent half theunskilled labor force in urbanmanufacturing, they account foronly 12 percent of seniormanagement. Their participationdiffers markedly across sectors andis highest in the textile sector. In therural nonfarm sector, by contrast,women run almost a quarter of allenterprises.

In urban manufacturing, export-oriented firms are the mostdynamic in terms of employmentgrowth. Rural enterprises appear toexperience little flux inemployment, with more than 90percent making no change in thenumber of employees during the previous year. The smallest rural firms (with less than fiveemployees) are the most stable, while larger firms tend to be growing or shrinking in response tomarket demand or seasonal fluctuations.

2.2 Greater Stability and Longevity among Urban EnterprisesUrban manufacturing enterprises tend to be older and more stable than rural enterprises (figure 2.2).The average age of urban manufacturing firms is 30 years, while for rural enterprises it is slightlymore than 9 years. Among urban enterprises, those in the garment sector are the youngest (16 yearsold on average), while those in the rubber and food and beverage sectors are the oldest (45 and 35years old).

In rural areas trading enterprises tend to be younger than others-as would be expected, since theyrequire less start-up capital. More than 85 percent of rural enterprises have always operated in thesame location. Of the few that have relocated, the vast majority have stayed in the same gramaniladhari (community).

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

10

FIGURE 2.2

Urban Firms Generally Older Than Rural Ones in Sri Lanka

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004.

0

10

20

30

40

50

60

70

80

90

Less than 2years

2-5 years 5-10 years More than 10years

Urban

Rural

Firm

s by

age

(P

erce

nt)

2.3 More Assets and Higher Productivity in Urban EnterprisesSri Lanka’s urban firms are generallymore capital intensive and moreproductive than their ruralcounterparts. Annual value addedper worker in urban manufacturingis almost eight times that in ruralmanufacturing (figure 2.3). Thelower labor costs for ruralenterprises do not fully compensatefor the difference in productivity.Productivity tends to be particularlylow-and duration short-lived-among rural nonfarm enterprisesstarted as part of a householdsurvival strategy to supplementagricultural income or tide a familythrough the lean season.

In the urban sector the industrial equipment and rubber products industries appear to be the mostproductive (table 2.3). The more labor-intensive textile and garment industries trail far behind.Indeed, rural service enterprises have value added per worker close to that of the urban textile sector,which appears to be in decline.

The productivity of rural firmsvaries markedly across regions andsectors. Rural enterprises inWestern and Central Provinces arealmost 3.5 times as productive assimilar enterprises in NorthEastern Province. Among all ruralenterprises, service firms have thehighest productivity.

Despite urban-rural differences inproductivity, rural nonfarmenterprises contribute significantlyto GDP. The survey findingssuggest that the total value addedby all rural nonfarm enterprises in2003 was SL Rs 185 billion-equivalent to 12 percent of GDPor 78 percent of agricultural GDPin 2002.

2.4 Registration among Rural Firms Surprisingly HighWhile rural enterprises are commonly perceived as operating in the informal sector and thus avoidingregistration and taxation, the survey findings indicate that a surprising 53 percent of those in Sri

THE DIFFERENT PROFILES OF URBAN AND RURAL ENTERPRISES

11

FIGURE 2.3

Productivity Far Higher in Urban Manufacturing Firms in Sri Lanka

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004.

Tho

usan

ds o

f Sri

Lank

an R

upee

s

0

50

100

150

200

250

300

350

400

450

Annual valueAdded per worker

Fixed assetsPer worker

Annual laborCosts per worker

Urban

Rural

TABLE 2.3

Productivity, Capital Intensity, and Labor Costs in Urban and Rural Firms,Sri Lanka(Sri Lankan Rupees)

Sector Annual valueadded per worker

Fixed assetsper worker

Annual laborcosts per worker

Urban enterprises 411,257 400,487 94,919

Industrial equipment 913,158 379,496 97,657

Rubber products 649,114 688,993 96,745

Food and beverages 495,024 509,764 90,836

Garments 275,940 232,974 97,898

Textiles 177,337 368,217 96,068

Rural enterprises 93,763 198,460 33,333

Production 54,779 203,862 27,000

Services 162,447 195,832 36,000

Trade 97,725 194,099 30,000

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004.

Lanka are registered. The rural enterprises most likely to be registered are larger and older, pay taxes,and operate as a stand-alone establishment. Trade and service enterprises are more likely thanproduction enterprises to be registered, perhaps because these types of enterprise tend to operate asstand-alone businesses and are therefore far more visible.

Among rural enterprises that have registered, the majority did so with the pradeshiya sabha, thoughalmost half are registered with the divisional secretary (there is much overlap between these twogroups).3 Most firms that have not registered explained that they had not done so because it was notrequired, and less than 2 percent because the process was too costly or time consuming or to avoidhigh taxes. As box 2.1 shows, the cost of registering a business in Sri Lanka has been declining.

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

12

BOX 2.1

The Ease of Entry

Starting a business in Sri Lanka involves relatively little red tape. Nearly 74 percent of urban manufacturing firms reported that obtaininga business license or operating permit was not a problem, compared with 37 percent in India, 41 percent in China, and 51 percent inthe Philippines. Less than 8 percent of urban manufacturing firms, and 4 percent of rural nonfarm enterprises, cited the procedure asa major or severe obstacle.

The administrative burden for start-ups in Sri Lanka has only become lighter in recent years. In 2002 entrepreneurs wishing to registera limited liability company had to undertake 8 procedures taking at least 73 days and costing $127, equivalent to 15 percent of percapita gross national income (GNI). Recently, the process was simplified reducing the number of procedures to 8, the average time to50 days, and the cost to just under 11 percent of GNI. Even so, Sri Lanka still trails behind more dynamic East Asian economies in thetime it takes to open a business (table 1). Further efficiency gains are likely, however, with the government planning to automate thecompany registry.

In rural areas registration appears to be a relatively manageable process for most enterprises (table 2), with some 94 percent reportingthat it was not a problem. Yet a significant share (47 percent) continues to operate informally. Three-quarters of these enterprisesreported that they had not registered because it was not required. Almost all rural businesses are sole proprietorships, whose ownersare simply required to register the name of their business under the Business Name Ordinance of 1918. Since responsibility forbusiness registration passed to the provincial councils in 1998, each province has established slightly different registration procedures,and registration fees range from a low of SL Rs 250 in North Western Province to SL Rs 500 in Western Province.

Once a business is registered, the owners may still have to obtain a business license, required to operate in such areas as hotels,banking, bakeries, pharmacies, meat outlets, and motor vehicles. The licensing body varies. For example, the Central Bank grantsbanking licenses, while the Ceylon Tourist Board issues licenses to operate hotels.

Trade licenses must be renewed annually. The license fees, set each year by the responsible institution (under Pradeshiya Sabha Act15 of 1987), range from SL Rs 50 to SL Rs 1,000.

TABLE 1

Administrative Burden of Starting a Business, Selected Countries (2004)

Country Number ofprocedures

Duration(days)

Cost(percentageof GNI per

capita)

Minimumcapital

(percentageof GNI per

capita)

Chile 10 28 11.6 0

China 12 46 14.3 3,855.9

India 10 88 49.8 430.4

Malaysia 8 31 27.1 0

Philippines 11 59 24.4 9.5

Sri Lanka 8 58 18.3 0

Thailand 9 42 7.3 0

Vietnam 11 63 29.9 0

Source: World Bank, Doing Business Indicators, 2004.

TABLE 2

Administrative Burden of Registeringa Rural Enterprise, Sri Lanka (2004)

Time spent on the registration process(days) 3.62

Time spent on obtaining or renewingpermits or licenses (days) 2.20

Number of government agencies visitedfor registration 1.26

Number of government agencies visitedfor licensing 1.02

Official fees paid for registering orrenewing registration (Sri Lankan Rupees)

640.29

Official fees paid for obtaining or renewinglicense or permit (Sri Lankan Rupees)

972.94

Source: Asian Development Bank and World Bank, SriLanka Investment Climate Survey, 2004

2.5 Weak Links between Rural and Urban FirmsLinks between rural nonfarm enterprises and urban firms in Sri Lanka are relatively weak. Evidencefrom the survey of rural enterprises shows that few sell their products to multinationals, parentcompanies, or larger urban firms (table 2.4). The vast majority reported selling their goods andservices directly to consumers or traders in their own district. The data may understate the linksbetween rural and urbanfirms, however, since ruralenterprises could sell theirproducts to intermediariesthat then resell them tofirms in other parts of thecountry.

Larger rural nonfarmenterprises (those with morethan five workers)-particularly largerproduction and tradingenterprises-are more likelyto have links with largerfirms and to sell in marketsoutside their province.

One way for small ruralfirms to tap into widermarkets is throughsubcontracting (Lanjouwand Lanjouw 2001). In SriLanka it is primarily largerrural firms (with more thanfive workers) that takeadvantage of sucharrangements.

2.6 Strong Links with AgricultureAgriculture is intricately linked with both the urban manufacturing and the rural nonfarm sector inSri Lanka. Agricultural products serve as inputs to key urban manufacturing sectors. The food,beverage, and tobacco industries, for example, accounted for almost 33 percent of total value addedin 2000-the single largest share of industrial value added. The processing of tea and coconuts, bigexport earners for Sri Lanka, has long been an important industry. The rubber industry has also beenprominent, though its value has declined sharply with the drop in world rubber prices.

The strong production links run backward as well as forward: agriculture not only supplies inputs,but also demands equipment and chemicals produced by industry. Agriculture, urban manufacturing,and rural nonfarm activities are also related through labor and capital markets and through strongconsumption links. Sales in all three rural nonfarm sectors peak during April (the festival season)following the main (maha) harvest and hit their lows in the middle of the slack (yala) season, when

THE DIFFERENT PROFILES OF URBAN AND RURAL ENTERPRISES

13

TABLE 2.4

Rural Firms’ Links with Buyers and Suppliers by Sector, Sri Lanka(percent)

Indicator Production Services Trade

Share of firms selling their output

To multinationals 1 0 1

To parent company or affiliatedsubsidiaries

2 0 0

To large domestic firms 0 1 0

Share of firms selling their output

Outside their grama niladhari 58 79 53

Outside their district 11 11 7

Outside their province 8 8 3

Share of firms selling undersubcontracting arrangements

8 9 8

Share of firms purchasing inputs undersubcontracting arrangements

10 N/A 15

N/A: Not available.

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004.

demand for agricultural labor is low and rural household incomes decline, reducing the demand forgoods and services (figure 2.4).4

SRI LANKA: IMPROVING THE RURAL AND URBAN INVESTMENT CLIMATE

14

Source: Asian Development Bank and World Bank, Sri Lanka Investment Climate Survey, 2004

FIGURE 2.4

Strong Links between Agriculture and Rural Nonfarm Enterprises in Sri Lanka

Volume of sales of nonfarm enterprises anddemand for male labor in agriculture

1.01.21.41.61.82.02.22.42.62.83.0

Jan

Feb

Mar Apr

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

Sal

es a

nd d

eman

d ra

nge

from

low

(1)

to h

igh

(3) Agriculture

Production

Services

Trade

Notes

1. In accordance with the sampling techniques for the Investment Climate Survey, urban firms are formalfirms located in urban areas, while rural firms are formal and informal firms located in rural areas. Thedesignations urban and rural are as defined by the Sri Lanka Department of Census and Statistics.