Spurious regressions with variables possessing deterministic trends Regresson Regress Y t on X t and...

79

Spurious regressions with variables possessing deterministic trends Regress on Regress Y t on X t and t SPURIOUS REGRESSIONS 1 To motivate the discussion that will consume the rest of this chapter, we now turn to the problem of spurious regressions. There are actually two literatures on spurious regressions. t t u t Y 2 1 t b b Y t 2 1 ˆ t b b Y Y Y Y t t t t 2 1 ˆ ~ t t v t X 2 1 t a a X t 2 1 ˆ t a a X X X X t t t t 2 1 ˆ ~ t Y ~ t X ~

-

Upload

felicity-morris -

Category

Documents

-

view

224 -

download

0

description

Spurious regressions with variables possessing deterministic trends Regresson Regress Y t on X t and t SPURIOUS REGRESSIONS 3 Suppose you have two unrelated variables Y t and X t, both generated by deterministic trends as shown above. What happens if Y t is regressed on X t ?

Transcript of Spurious regressions with variables possessing deterministic trends Regresson Regress Y t on X t and...

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

1

To motivate the discussion that will consume the rest of this chapter, we now turn to the problem of spurious regressions. There are actually two literatures on spurious regressions.

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

2

The first, which dates back to the beginning of econometrics as a formal discipline, concerns regressions involving variables with deterministic trends. The other involves regressions with random walks.

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

3

Suppose you have two unrelated variables Yt and Xt, both generated by deterministic trends as shown above. What happens if Yt is regressed on Xt?

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

4

The answer is obvious. The common dependence on t will cause the variables to be correlated, and hence a regression of one on the other will yield ‘significant’ coefficients, provided that the sample is large enough.

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

5

This problem was recognised very early in the history of econometrics. A popular response was to detrend the variables before performing the regression. Yt and Xt would separately be regressed on time and the residuals saved, say as Yt and Xt.

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

~ ~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

6

Eventually it was pointed out (Frisch and Waugh, 1933) that one did not actually need to go to the trouble of detrending Yt and Xt before performing the regression.

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

7

Exactly the same results would be obtained by including a time trend in a multiple regression of (unadjusted) Yt on (unadjusted) Xt. (This was the origin of the Frisch–Waugh–Lovell theorem discussed in Section 3.2. Lovell (1963) generalized the result.)

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

8

The inclusion of a time trend in a regression of Yt on Xt makes it relatively difficult to obtain significant results. Since it possesses a trend, the series for Xt will be correlated with t, and hence the problem of multicollinearity inevitably arises to some extent.

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables possessing deterministic trends

Regress on

Regress Yt on Xt and t

SPURIOUS REGRESSIONS

9

However, performing the regression with the detrended versions of Yt and Xt does not lead to any better results because they must be exactly the same.

tt utY 21

tbbYt 21ˆ

tbbYYYY tttt 21ˆ~

tt vtX 21

taaX t 21ˆ

taaXXXX tttt 21ˆ~

tY~

tX~

Spurious regressions with variables that are random walks

SPURIOUS REGRESSIONS

10

The problem of spurious regressions caused by deterministic trends is easy to understand and easy to treat. Much more dramatic, and ultimately important, were the findings of a celebrated simulation undertaken by Granger and Newbold (1974).

Yttt YY 1

Xttt XX 1

Spurious regressions with variables that are random walks

SPURIOUS REGRESSIONS

11

They found that, if they generated two independent random walks and regressed one on the other, the slope coefficient was likely to have a significant t statistic, despite the fact that the series were unrelated.

Yttt YY 1

Xttt XX 1

Spurious regressions with variables that are random walks

SPURIOUS REGRESSIONS

12

They generated 100 pairs of random walks, with sample size 50 time periods. In 77 , the slope coefficient was significant at the 5 percent level.

Yttt YY 1

Xttt XX 1

Spurious regressions with variables that are random walks

SPURIOUS REGRESSIONS

13

This means that there were 77 instances of Type I error in the 100 regressions. With a 5 percent significance test, there ought to have been about 5. The incidence of Type I error when performing a 1 percent significance test was not much lower.

Yttt YY 1

Xttt XX 1

Spurious regressions with variables that are random walks

SPURIOUS REGRESSIONS

14

The study made an immediate impact because there was a growing consensus that many economic time series are plausibly characterized as being random walks, possibly with drift.

Yttt YY 1

Xttt XX 1

Spurious regressions with variables that are random walks

SPURIOUS REGRESSIONS

15

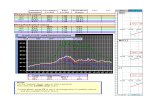

Drift would of course aggravate the problem of spurious association. The findings of Granger and Newbold are all the more remarkable because their series were pure random walks.

Yttt YY 1

Xttt XX 1

16

Here is a typical example of what they found. The series in the figure are independent random walks. Obviously, a regression of one on the other ought not to yield significant results, except as a matter of Type I error.

-25

-20

-15

-10

-5

0

5

10

1

SPURIOUS REGRESSIONS

Independent random walks

=============================================================Dependent Variable: YMethod: Least Squares Sample: 1 100 Included observations: 100 ============================================================= Variable Coefficient Std. Error t-Statistic Prob.============================================================= C 2.445060 0.369960 6.608987 0.0000 X 0.150445 0.037953 3.963954 0.0001 =============================================================R-squared 0.138181 Mean dependent var 1.223467 Adjusted R-squared 0.129387 S.D. dependent var 2.193741 S.E. of regression 2.046907 Akaike info criteri 4.290334 Sum squared resid 410.6032 Schwarz criterion 4.342437 Log likelihood -212.5167 F-statistic 15.71293 Durbin-Watson stat 0.270222 Prob(F-statistic) 0.000140 =============================================================

17

Here is the output obtained when the upper random walk in the figure is regressed on the lower one.

SPURIOUS REGRESSIONS

Regression of one random walk on another

=============================================================Dependent Variable: YMethod: Least Squares Sample: 1 100 Included observations: 100 ============================================================= Variable Coefficient Std. Error t-Statistic Prob.============================================================= C 2.445060 0.369960 6.608987 0.0000 X 0.150445 0.037953 3.963954 0.0001 =============================================================R-squared 0.138181 Mean dependent var 1.223467 Adjusted R-squared 0.129387 S.D. dependent var 2.193741 S.E. of regression 2.046907 Akaike info criteri 4.290334 Sum squared resid 410.6032 Schwarz criterion 4.342437 Log likelihood -212.5167 F-statistic 15.71293 Durbin-Watson stat 0.270222 Prob(F-statistic) 0.000140 =============================================================

18

The true slope coefficient is 0, because Y was generated independently of X. And yet the estimate of the slope coefficient appears to be significantly different from 0 at the 1% level and above.

SPURIOUS REGRESSIONS

Regression of one random walk on another

19

We will now undertake a proper simulation. Our model will be that Yt is related to Xt and we will regress Yt on Xt where Yt and Xt are generated as independent random walks.

ttt uXY 21

0: 20 H

SPURIOUS REGRESSIONS

Regression of one random walk on another

20

We will examine the distribution of b2 and see what happens when we test the null hypothesis H0: 2 = 0, knowing that it is true because the series have been generated independently.

ttt uXY 21

SPURIOUS REGRESSIONS

Regression of one random walk on another

0: 20 H

21

For comparison, we will also regress Yt on Xt where Yt and Xt are generated as independent white noise processes. In both cases we generate 10 million samples for four sample sizes: 25, 50, 100, and 200.

ttt uXY 21

SPURIOUS REGRESSIONS

Regression of one random walk on another

0: 20 H

22

The figure shows the distribution of b2 for the regression where Yt and Xt were white noise processes drawn independently from a normal distribution with zero mean and unit variance.

SPURIOUS REGRESSIONS

0

1

2

3

4

5

6

7

-1 -0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1

T = 200

T = 50

T = 25

T = 100

tt XbbY 21ˆ

Distribution of b2

Yt, Xt both iid N(0,1): illustration of standard theory

b2 is √T consistent

23

According to theory, the distribution of b2 should have mean zero and standard deviation inversely proportional to √T, where T is the sample size.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yt, Xt both iid N(0,1): illustration of standard theory

b2 is √T consistent

0

1

2

3

4

5

6

7

-1 -0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1

T = 200

T = 50

T = 25

T = 100

Distribution of b2

24

The height of the distribution should therefore be proportional to √T since the total area must remain constant at unity.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yt, Xt both iid N(0,1): illustration of standard theory

b2 is √T consistent

0

1

2

3

4

5

6

7

-1 -0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1

T = 200

T = 50

T = 25

T = 100

Distribution of b2

25

Thus one would expect the distribution for 100 to be twice as tall as that for 25, and that for 200 to be twice at tall as that for 50. This is easy to check visually. The figure confirms the theory.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yt, Xt both iid N(0,1): illustration of standard theory

b2 is √T consistent

0

1

2

3

4

5

6

7

-1 -0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1

T = 200

T = 50

T = 25

T = 100

Distribution of b2

26

Standard theory tells us that the distribution of the t statistic should have mean zero irrespective of the sample size and that it should converge to a normal distribution with zero mean and unit variance as the sample size becomes large.

SPURIOUS REGRESSIONS

0.00

0.10

0.20

0.30

0.40

0.50

-5 -4 -3 -2 -1 0 1 2 3 4 5

T = 25

T = 200tt XbbY 21

ˆ

Yt, Xt both iid N(0,1): illustration of standard theory

t distribution converges to a normal distribution

Distribution of t statistic for b2

27

The figure confirms this. It shows only the distributions for T = 25 and T = 200. Those for T = 50 and T = 100 are not shown because they are virtually coincidental with the other two.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yt, Xt both iid N(0,1): illustration of standard theory

t distribution converges to a normal distribution

0.00

0.10

0.20

0.30

0.40

0.50

-5 -4 -3 -2 -1 0 1 2 3 4 5

T = 25

T = 200

Distribution of t statistic for b2

28

The distribution for T = 200 is the one with the very slightly higher mode and the thinner tails. It has converged on the normal distribution.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yt, Xt both iid N(0,1): illustration of standard theory

t distribution converges to a normal distribution

0.00

0.10

0.20

0.30

0.40

0.50

-5 -4 -3 -2 -1 0 1 2 3 4 5

T = 25

T = 200

Distribution of t statistic for b2

29

The distribution for T = 25 is very similar. The body of the distribution has also almost converged on the normal distribution. It is only in the tails, which are marginally fatter than those for a normal distribution, that the distribution has not fully converged.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yt, Xt both iid N(0,1): illustration of standard theory

t distribution converges to a normal distribution

0.00

0.10

0.20

0.30

0.40

0.50

-5 -4 -3 -2 -1 0 1 2 3 4 5

T = 25

T = 200

Distribution of t statistic for b2

0.0

0.2

0.4

0.6

0.8

-3 -2 -1 0 1 2 3

30

We will now present the results of a parallel simulation for the random walk regressions. This figure demonstrates a truly remarkable result. If you regress one random walk on another, the slope coefficient does not tend to zero, no matter how large is the same size.

SPURIOUS REGRESSIONS

T = 25, 50, 100, 200

Yt, Xt independent random walks

tt XbbY 21ˆ

b2 is inconsistent. Its distribution quickly converges on a limiting distribution and fails to collapse.

Distribution of b2

31

It tends to a limiting distribution. This is a complete break from what we have seen so far. It is the first time that we have come across an estimator that is inconsistent because its distribution fails to collapse to a spike.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

tt XbbY 21ˆ

T = 25, 50, 100, 200

b2 is inconsistent. Its distribution quickly converges on a limiting distribution and fails to collapse.

0.0

0.2

0.4

0.6

0.8

-3 -2 -1 0 1 2 3

Distribution of b2

32

The two requirements of a consistent estimator are:1. Its distribution should collapse to a spike.2. The spike should be at the true value of the parameter being estimated.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

tt XbbY 21ˆ

T = 25, 50, 100, 200

b2 is inconsistent. Its distribution quickly converges on a limiting distribution and fails to collapse.

0.0

0.2

0.4

0.6

0.8

-3 -2 -1 0 1 2 3

Distribution of b2

33

In previous encounters with inconsistent estimators, for example, OLS estimators in the presence of measurement error or simultaneity, the distributions did collapse to a spike, but the spike was at the wrong place.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

tt XbbY 21ˆ

T = 25, 50, 100, 200

b2 is inconsistent. Its distribution quickly converges on a limiting distribution and fails to collapse.

0.0

0.2

0.4

0.6

0.8

-3 -2 -1 0 1 2 3

Distribution of b2

34

In this case, there is no bias, so if the distribution had collapsed, the estimator would have been consistent. But it refuses to collapse.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

tt XbbY 21ˆ

T = 25, 50, 100, 200

b2 is inconsistent. Its distribution quickly converges on a limiting distribution and fails to collapse.

0.0

0.2

0.4

0.6

0.8

-3 -2 -1 0 1 2 3

Distribution of b2

35

This figure shows the distributions of b2 for T = 25, 50, 100, and 200. They are virtually identical. For a sample size of 25, the distribution has already virtually reached its limiting distribution. To see the process of convergence, one must look at even smaller sample sizes.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

tt XbbY 21ˆ

T = 25, 50, 100, 200

b2 is inconsistent. Its distribution quickly converges on a limiting distribution and fails to collapse.

0.0

0.2

0.4

0.6

0.8

-3 -2 -1 0 1 2 3

Distribution of b2

36

In this figure T = 5, 10, 15, and 20. The variance of the distribution falls when one increases the sample size from 5 to 10, and it falls further when one increases the sample size to 15. There is hardly any further change when one increases the sample size to 20 because the distribution is already close to its limit.

SPURIOUS REGRESSIONS

0.0

0.2

0.4

0.6

0.8

-3 -2 -1 0 1 2 3

T = 5

T = 10T = 15T = 20

Yt, Xt independent random walks

tt XbbY 21ˆ

T = 5, 15, 10, 20

b2 is inconsistent. Its distribution quickly converges on a limiting distribution and fails to collapse.

Distribution of b2

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

37

This figure gives the distributions of the standard errors, as printed out in the regression results, for T equal to 25, 50, and 100, and 200.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

Distribution of standard error of b2

True DGP for Yt:

Yttt YY 1

tt XbbY 21ˆ

38

These distributions ought to be almost identical, given that the standard error provides an estimate of the standard deviation, and we have just seen that the distributions of b2 for these sample sizes are almost identical.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

Distribution of standard error of b2

True DGP for Yt:

Yttt YY 1

tt XbbY 21ˆ

39

However, the figure suggests that the standard deviation decreases with the sample size, in the usual way. This is incorrect, and the reason for the aberration is that the model is misspecified.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

Distribution of standard error of b2

True DGP for Yt:

Yttt YY 1

tt XbbY 21ˆ

40

Since Yt is a random walk, the true data generating process (DGP) is Yt = Yt–1 + Yt, where Yt is a white noise process. When we regress Yt on Xt, we commit two errors.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

Distribution of standard error of b2

True DGP for Yt:

Yttt YY 1

tt XbbY 21ˆ

41

One is that we have introduced an irrelevant explanatory variable Xt. We know that, in general, introducing irrelevant variables does not lead to serious harm.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

Distribution of standard error of b2

True DGP for Yt:

Yttt YY 1

tt XbbY 21ˆ

42

The more serious error is that, since the true DGP for Yt is Yt = Yt–1 + Yt, we have omitted Yt–1. The effects of omitted variable misspecification are complex, but in this case we can come up with an intuitive explanation of what is happening.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

True DGP for Yt:

Yttt YY 1

tt XbbY 21ˆ

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

Distribution of standard error of b2

43

By omitting Yt–1, we have forced it into the disturbance term. Since Yt is a random walk, this implies that ut is also a random walk.

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

Distribution of standard error of b2

ttt uXY 21 0: 20 H

1 tt Yu

44

This invalidates the OLS procedure for calculating standard errors, which assumes that ut is generated randomly from one observation to the next (no autocorrelation).

SPURIOUS REGRESSIONS

Yt, Xt independent random walks

0

2

4

6

8

10

12

14

16

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

T = 25

T = 50

T = 200

T = 100

Distribution of standard error of b2

ttt uXY 21 0: 20 H

1 tt Yu

45

It follows that the t statistic, as printed in the regression results, does not conform to its theoretical distribution. The apparent reduction in the reported standard error as T increases causes the distribution of the reported t statistic to widen as T increases.

SPURIOUS REGRESSIONS

0.00

0.05

0.10

0.15

-40 -30 -20 -10 0 10 20 30 40

T = 25

T = 100

T = 200

T = 50

Yt, Xt independent random walks

Distribution of t statistic for b2

tt XbbY 21ˆ

46

The t distribution ought to converge on the standardized normal distribution, as in white noise regressions.

SPURIOUS REGRESSIONS

0.00

0.10

0.20

0.30

0.40

0.50

-5 -4 -3 -2 -1 0 1 2 3 4 5

T = 25

T = 200

Yt, Xt both iid N(0,1): illustration of standard theory

t distribution converges to a normal distribution

tt XbbY 21ˆ

Distribution of t statistic for b2

47

Instead, it widens, as shown in the present figure. This accounts for the very high incidence of Type I errors found by Granger and Newbold.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yt, Xt independent random walks

0.00

0.05

0.10

0.15

-40 -30 -20 -10 0 10 20 30 40

T = 25

T = 100

T = 200

T = 50

Distribution of t statistic for b2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-3 -2 -1 0 1 2 3

T = 200

T = 50

T = 25

T = 100

48

Before drawing the implications of these findings, we will consider one further example. Suppose that, instead of being random walks, Yt and Xt are (independent) AR(1) processes with coefficient 0.95 as shown, Yt and Xt being independent white noise processes.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Distribution of b2

Yt, Xt independent stationary autoregressive processes

49

What happens if one regresses Yt on Xt? The figure shows the distribution of b2 for sample sizes 25, 50, 100, and 200. The distribution does contract as the sample size increases, and if we continued to increase the sample size, it will progressively contract to a spike at zero.

SPURIOUS REGRESSIONS

Distribution of b2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-3 -2 -1 0 1 2 3

T = 200

T = 50

T = 25

T = 100

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

50

So, in contrast to the regressions with random walks, b2 is a consistent estimator.

SPURIOUS REGRESSIONS

Distribution of b2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-3 -2 -1 0 1 2 3

T = 200

T = 50

T = 25

T = 100

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

51

But the rate of reduction of the standard deviation (and hence the increase in height) of the distribution is less than the √T that we would expect from standard theory and that we saw in the figure for the white noise regressions. This is especially noticeable for small sample sizes.

SPURIOUS REGRESSIONS

Distribution of b2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-3 -2 -1 0 1 2 3

T = 200

T = 50

T = 25

T = 100

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

52

Here is the figure for the white noise regressions again. The standard deviation is inversely proportional to √T, and so the height is proportional to √T. You can see that the height for T = 100 is twice that for T = 25, and the height for T = 200 is twice that for T = 50.

SPURIOUS REGRESSIONS

0

1

2

3

4

5

6

7

-1 -0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1

T = 200

T = 50

T = 25

T = 100

Distribution of b2

Yt, Xt both iid N(0,1): illustration of standard theory

tt XbbY 21ˆ

white noise regressions, for comparison

53

The substandard rates of reduction of the standard deviation and increase in height of the distribution is especially noticeable for small sample sizes.

SPURIOUS REGRESSIONS

Distribution of b2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-3 -2 -1 0 1 2 3

T = 200

T = 50

T = 25

T = 100

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

54

As with the random walk case, the standard errors are computed incorrectly and the t statistics are not valid.

SPURIOUS REGRESSIONS

Distribution of b2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-3 -2 -1 0 1 2 3

T = 200

T = 50

T = 25

T = 100

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

ttt uXY 21 0: 20 H

1 tt Yu

55

When we regress Yt on Xt instead of Yt–1, we have included the redundant variable Xt, which does not matter, and have omitted Yt–1, which does. Again, Yt–1 is forced into ut and so ut is an autocorrelated process with = 0.95.

SPURIOUS REGRESSIONS

Distribution of b2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-3 -2 -1 0 1 2 3

T = 200

T = 50

T = 25

T = 100

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

ttt uXY 21 0: 20 H

1 tt Yu

0.00

0.05

0.10

0.15

-40 -30 -20 -10 0 10 20 30 40

T = 25

T = 50T = 100T = 200

56

The figure shows the t distribution for the different sample sizes. It is nonstandard, although not as distorted as that for the random walks.

SPURIOUS REGRESSIONS

tt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

Distribution of t statistic for b2

ttt uXY 21 0: 20 H

1 tt Yu

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

57

Of course, the autocorrelation should be revealed by a formal test. This is the case. For this purpose, it is sufficient to use the d statistic for the Durbin–Watson test, despite its imperfections. The figure shows the distribution of this statistic for the four sample sizes.

SPURIOUS REGRESSIONS

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

58

Even with T as small as 25, it indicates autocorrelation significant at the 1 percent level in most of the 10 million samples. For larger samples, it indicates significant autocorrelation almost all of the time.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

59

Once aware of the problem, we know how to treat it. We eliminate the autocorrelation by fitting the specification shown.

SPURIOUS REGRESSIONS

ttttt XXYY 12211 1

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

60

If we do this, we will find that the coefficients of Xt and Xt–1 are both zero and that the coefficient of Yt–1 is 0.95, subject of course to sampling error and the finite-sample bias caused by the presence of the lagged dependent variable in the specification.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

61

The fitted model then reveals the truth, that Yt depends only on Yt–1 with coefficient 0.95, and that it does not depend on Xt at all.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

62

Could we not treat the random walk case where, under the null hypothesis, the disturbance term itself is a random walk, as an extreme case of autocorrelation with = 1?

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

63

In some ways, we can. As with the = 0.95 case, the Durbin–Watson d statistic almost invariably indicates severe positive autocorrelation. The distributions of the d statistic for the various sample sizes are similar to those in the figure, shifted even further to the left.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

64

What happens in this case if we fit the revised specification that eliminates the autocorrelation?

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

65

The results are much the same as for the case = 0.95. We will discover that = 1, that 2 = 0, and the relationship simplifies to the definition of the random walk that is the true relationship for Yt.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

66

This is not quite the full story because, as we will see in the next section, there are further surprises when we come to test the (true) null hypothesis that the coefficient of Yt–1 is equal to 1. However, it is a reasonable first approximation.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

67

The AR(1) regressions demonstrate that the problem of excess Type I errors arising from nonstandard t distributions found by Granger and Newbold did not depend on the nonstationarity of their processes. It occurs with any AR(1) process, being more evident, the more closely the slope coefficient approximates unity.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

68

The lesson to be learnt from the Granger–Newbold simulations is the one that motivated their article and was articulated by them at the time.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

69

This was that there is a substantial risk of apparently obtaining significant results, where no relationship exists, if you ignore evidence of autocorrelation, as was once quite common in applied work.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

70

The fact that Granger and Newbold used nonstationary processes, in the form of random walks, to make their point is not important. They could have made it just as well by using independent stationary AR(1) processes. But the effect is the more dramatic, the greater the value of , and most obvious when one goes to the extreme value of 1, the random walk.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

71

The objective of the Granger–Newbold simulations was to highlight the dangers of ignoring evidence of autocorrelation in time series models.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

72

However, their experiments also contributed to a growing awareness that standard theory did not necessarily apply to the properties of regression estimators, and associated statistical inference, for regressions using nonstationary time series data.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

73

These concerns were reinforced by the fact that the use of nonstationary variables in model-building was very common.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

74

Macroeconomic analysis, in particular, routinely used variables such as aggregate income and aggregate consumption that invariably possessed time trends when measured in levels and were unquestionably nonstationary.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

75

The only issue was whether they were better characterized as random walks with drift or as subject to deterministic trends. This stimulated a literature, now enormous and still growing, concerning the determination of the conditions under which such regressions with nonstationary time series could yield consistent estimates with valid statistical inference.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

76

The first step was to develop a means for identifying whether a time series is, or is not, nonstationary in the first place, and if it is nonstationary, whether or not it possesses a trend, and if it does, whether the trend is deterministic or is the outcome of a random walk with drift.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

77

These issues will be particularly important when we come to cointegration and explore whether there exist genuine relationships among variables characterized as nonstationary processes.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

78

Historically there have been two approaches to testing for nonstationarity, one using graphical techniques, the other using formal statistical tests. The following slideshows will consider each in turn.

SPURIOUS REGRESSIONS

Yt, Xt independent stationary autoregressive processes

Distribution of the Durbin–Watson statistic

0

1

2

3

4

5

6

7

8

0 0.5 1 1.5 2 2.5 3 3.5 4

T = 25

T = 50

T = 200

T = 100

ttt uXY 21 0: 20 H

1 tt Yutt XbbY 21ˆ

Yttt YY 195.0

Xttt XX 195.0

ttttt XXYY 12211 1

Copyright Christopher Dougherty 2011.

These slideshows may be downloaded by anyone, anywhere for personal use.Subject to respect for copyright and, where appropriate, attribution, they may be used as a resource for teaching an econometrics course. There is no need to refer to the author.

The content of this slideshow comes from Section 13.2 of C. Dougherty, Introduction to Econometrics, fourth edition 2011, Oxford University Press.Additional (free) resources for both students and instructors may be downloaded from the OUP Online Resource Centrehttp://www.oup.com/uk/orc/bin/9780199567089/.

Individuals studying econometrics on their own and who feel that they might benefit from participation in a formal course should consider the London School of Economics summer school courseEC212 Introduction to Econometrics http://www2.lse.ac.uk/study/summerSchools/summerSchool/Home.aspxor the University of London International Programmes distance learning course20 Elements of Econometricswww.londoninternational.ac.uk/lse.

11.07.25