Spun Yarns and Threads - InfoHouseinfohouse.p2ric.org/ref/39/38011.pdf · Spun Yarns and Threads...

6

Spun Yarns and Threads SIC 228 The spun yams and thread industry consists of establishments primarily engaged in producing natural or manmade fiber yarns and threads. The industry is composed of three 4-digit SICS. Yam spinning estab- lishments (SIC 2281) spin yams for several end uses, including woven and knit fabrics and carpets. SIC 2282 (the texturizing sector) consists of establishments that texturize, throw, twist, wind, or spool pur- chased yarns or manmade fiber filaments. Thread mills (SIC 2284) manufacture thread used for sewing, daming, hand knitting, embroidery, handicrafts and industrial applications. Threads are also used in bookbindings, dental floss, tea bag strings and shoelaces. The basic statistics for these three sectors are provided in Table 1. The value of spun yam shipments (SIC 2281) totaled $7.6 billion in 1989, a 4.2 percent increase over the 1988 level. This was the fourth consecutive annual increase in shipments. The strong demand conditions of late 1986 and 1987, when capacity was stretched to the limit and shortages developed for some types of yarns, moderated in 1988. The softening in demand is not fully reflected in the value of shipments because generally higher fiber prices contributed significantly to a rise in yarn prices. Shipments by the texturizing and thread producing sectors have also contin- ued to show increases after down- tums i.n the mid 1980s. Demand in the knitting and carpet industries have also spurred growth in yams and threads. Imports are still one of the biggest problems facing the U. S. textile industry. U. S. Department of Commerce data indicate that textile and apparel imports for 1989 may be 13 percent above the record- breaking level of 1987. Foreign trade, however, remains a relatively small portion of activity in the spun yams and thread industry. Foreign producers continue to focus on the higher value-added items such as fabrics and apparel. Thus, although the import value in this industry rose by over 7 percent in 1988, this was largely due to higher foreign prices. Very few U.S. companies import much yarn or thread. market forces have caused recent structural changes in the yam and thread mill industry. Vertical and horizontal integration as well as Technological developments and

Transcript of Spun Yarns and Threads - InfoHouseinfohouse.p2ric.org/ref/39/38011.pdf · Spun Yarns and Threads...

Spun Yarns and Threads SIC 228

The spun yams and thread industry consists of establishments primarily engaged in producing natural or manmade fiber yarns and threads. The industry is composed of three 4-digit SICS. Yam spinning estab- lishments (SIC 2281) spin yams for several end uses, including woven and knit fabrics and carpets. SIC 2282 (the texturizing sector) consists of establishments that texturize, throw, twist, wind, or spool pur- chased yarns or manmade fiber filaments. Thread mills (SIC 2284) manufacture thread used for sewing, daming, hand knitting, embroidery, handicrafts and industrial applications. Threads are also used in bookbindings, dental floss, tea bag strings and shoelaces. The basic statistics for these three sectors are provided in Table 1.

The value of spun yam shipments (SIC 2281) totaled $7.6 billion in 1989, a 4.2 percent increase over the 1988 level. This was the fourth consecutive annual increase in shipments. The strong demand conditions of late 1986 and 1987, when capacity was stretched to the limit and shortages developed for

some types of yarns, moderated in 1988. The softening in demand is not fully reflected in the value of shipments because generally higher fiber prices contributed significantly to a rise in yarn prices. Shipments by the texturizing and thread producing sectors have also contin- ued to show increases after down- tums i.n the mid 1980s. Demand in the knitting and carpet industries have also spurred growth in yams and threads.

Imports are still one of the biggest problems facing the U. S. textile industry. U. S. Department of Commerce data indicate that textile and apparel imports for 1989

may be 13 percent above the record- breaking level of 1987. Foreign trade, however, remains a relatively small portion of activity in the spun yams and thread industry. Foreign producers continue to focus on the higher value-added items such as fabrics and apparel. Thus, although the import value in this industry rose by over 7 percent in 1988, this was largely due to higher foreign prices. Very few U.S. companies import much yarn or thread.

market forces have caused recent structural changes in the yam and thread mill industry. Vertical and horizontal integration as well as

Technological developments and

Table 1 _ _ ~ ~

Spun Yams and Threads Industry: Basic Statistics (1987)

EMPLOYMENT DATA (1,000) OPERATING STATISTICS (MILLION DOLLARS)

Prod. Ship- New Cap. Cost of SIC Industry Employees Wkers. ments Expend. Materials Payroll

2281 Yarn Spinning 85.8 78.1 7,094.0 315.2 4,206.5 1,399.6

2284 Thread Mills 6.6 5.7 644.7 14.3 404.3 107.4

Total 114.2 103.2 10,1%.6 396.0 6,410.6 1,854.4

2282 Texturizing 21.8 19.4 2,457.9 66.5 1,799.8 347.3

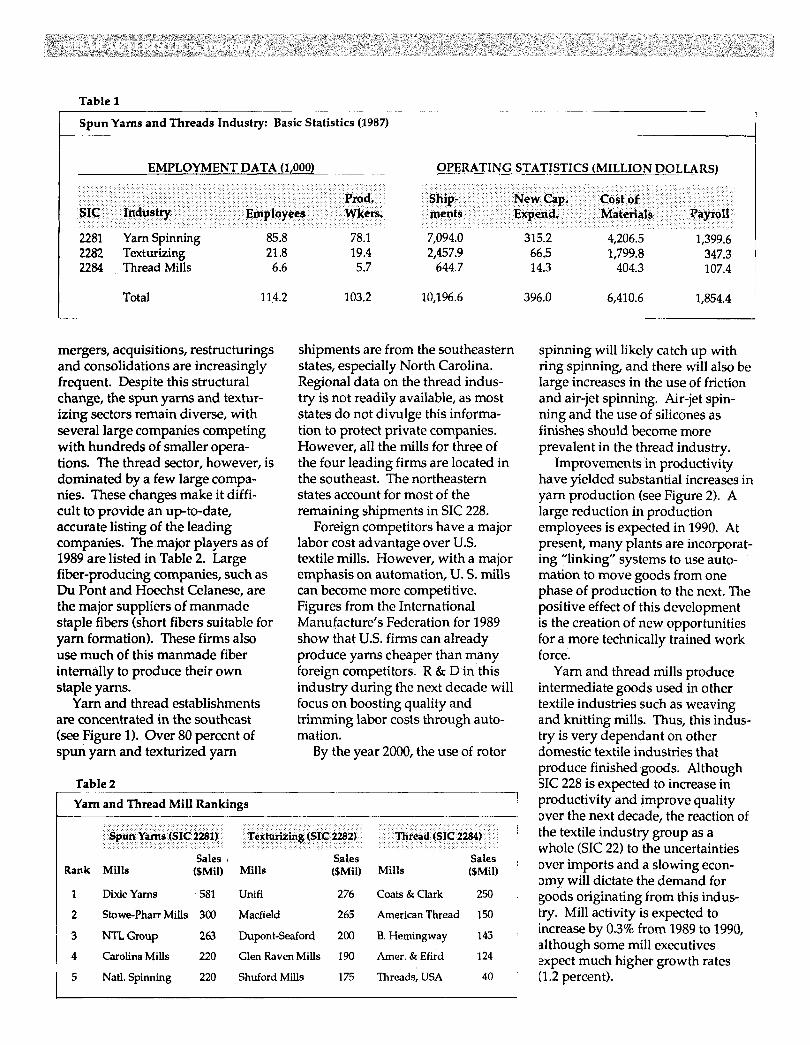

mergers, acquisitions, restructurings and consolidations are increasingly frequent. Despite this structural change, the spun yarns and textur- izing sectors remain diverse, with several large companies competing with hundreds of smaller opera- tions. The thread sector, however, is dominated by a few large compa- nies. These changes make it diffi- cult to provide an up-to-date, accurate listing of the leading companies. The major players as of 1989 are listed in Table 2. Large fiber-producing companies, such as Du Pont and Hoechst Celanese, are the major suppliers of manmade staple fibers (short fibers sui table for yam formation). These firms also use much of this manmade fiber internally to produce their own staple yams.

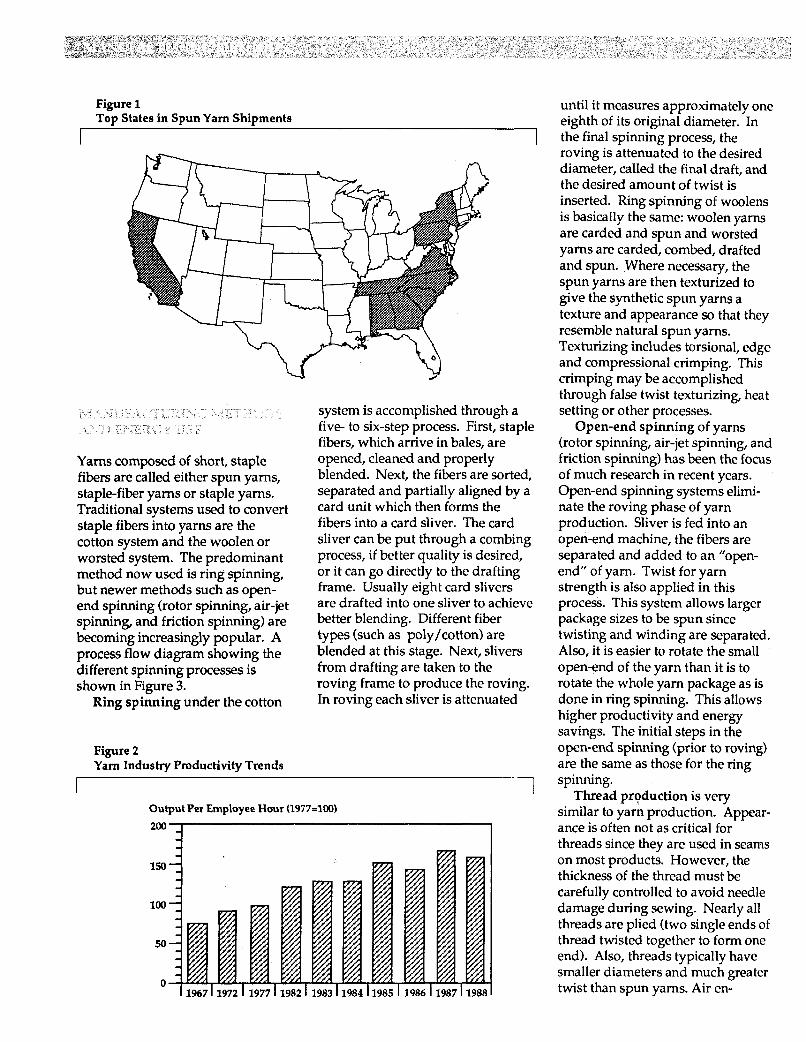

are concentrated in the southeast (see Figure 1). Over 80 percent of spun yarn and texturized yam

Yam and thread establishments

Table 2

shipments are from the southeastern states, especially North Carolina. Regional data on the thread indus- try is not readily available, as most states do not divulge this informa- tion to protect private companies. However, all the mills for three of the four leading firms are located in the southeast. The northeastern states account for most of the remaining shipments in SIC 228.

Foreign competitors have a major labor cost advantage over US. textile mills. However, with a major emphasis on automation, U. S. mills can become more competitive. Figures from the International Manufacture’s Federation for 1989 show that U.S. firms can already produce yams cheaper than many foreign competitors. R & D in this industry during the next decade will focus on boosting quality and trimming labor costs through auto- mation.

By the year 2000, the use of rotor

Yam and Thread Mill Rankings

Spun Yams (SIC 2281) Texturizing (SIC 2282) Thread (SIC 2284)

Sales Sales Sales Rank Mills ($Mil) Mills ($Mil) Mills ($Mil)

1 DixieYams 581 Unifi 276 Coats & Clark 250

2 Stowe-Pharr Mills 300 Macfield 265 AmericanThread 150

3 NTLGroup 263 Dupont-Seaford 200 8. Hemingway 145

4 Carolina Mills 220 Glen Raven Mills 190 Amer. & Efird 124

5 Natl. Spinning 220 Shuford Mills 175 Threads, USA 40

I

spinning will likely catch up with ring spinning, and there will also be large increases in the use of friction and air-jet spinning. Air-jet spin- ning and the use of silicones as finishes should become more prevalent in the thread industry.

Improvements in productivity have yielded substantial increases in yarn production (see Figure 2). A large reduction in production employees is expected in 1990. At present, many plants are incorporat- ing “linking” systems to use auto- mation to move goods from one phase of production to the next. The positive effect of this development is the creation of new opportunities for a more technically trained work force.

Yam and thread mills produce intermediate goods used in other textile industries such as weaving and knitting mills. Thus, this indus- try is very dependant on other domestic textile industries that produce finished goods. Although SIC 228 is expected to increase in productivity and improve quality over the next decade, the reaction of the textile industry group as a whole (SIC 22) to the uncertainties over imports and a slowing econ- omy will dictate the demand for goods originating from this indus- try. Mill activity is expected to increase by 0.3% from 1989 to 1990, although some mill executives expect much higher growth rates (1.2 percent).

c , .. I... . >

Figure 1 Top States in Spun Yam Shipments

U

Yams composed of short, staple fibers are called either spun yams, staple-fiber yams or staple yams. Traditional systems used to convert staple fibers into yarns are the cotton system and the woolen or worsted system. The predominant method now used is ring spinning, but newer methods such as open- end spinning (rotor spinning, air-jet spinning, and friction spinning) are becoming increasingly popular. A process flow diagram showing the different spinning processes is shown in Figure 3.

Ring spinning under the cotton

Figure 2 Yam Industry Productivity Trends

Y system is accomplished through a five- to six-step process. First, staple fibers, which arrive in bales, are opened, cleaned and properly blended. Next, the fibers are sorted, separated and partially aligned by a card unit which then forms the fibers into a card sliver. The card sliver can be put through a combing process, if better quality is desired, or it can go directly to the drafting frame. Usually eight card slivers are drafted into one sliver to achieve better blending. Different fiber types (such as poIy/cotton) are blended at this stage. Next, slivers from drafting are taken to the roving frame to produce the roving. In roving each sliver is attenuated

Output Per Employee Hour (1977=100)

*” 150

100

50

1987 1988 I

until it measures approximately one eighth of its original diameter. In the final spinning process, the roving is attenuated to the desired diameter, called the final draft, and the desired amount of twist is inserted. Ring spinning of woolens is basically the same: woolen yarns are carded and spun and worsted yams are carded, combed, drafted and spun. Where necessary, the spun yarns are then texturized to give the synthetic spun yarns a texture and appearance so that they resemble natural spun yarns. Texturizing includes torsional, edge and compressional crimping. This crimping may be accomplished through false twist texturizing, heat setting or other processes.

Open-end spinning of yarns (rotor spinning, air-jet spinning, and friction spinning) has been the focus of much research in recent years. Open-end spinning systems elimi- nate the roving phase of yarn production. Sliver is fed into an open-end machine, the fibers are separated and added to an ”open- end” of yam. Twist for yarn strength is also applied in this process. This system allows larger package sizes to be spun since twisting and winding are separated. Also, it is easier to rotate the small open-end of the yarn than it is to rotate the whole yam package as is done in ring spinning. This allows higher productivity and energy savings. The initial steps in the open-end spinning (prior to roving) are the same as those for the ring spinning.

Thread production is very similar to yarn production. Appear- ance is often not as critical for threads since they are used in seams on most products. However, the thickness of the thread must be carefully controlled to avoid needle damage during sewing. Nearly all threads are plied (two single ends of thread twisted together to form one end). Also, threads typically have smaller diameters and much greater twist than spun yarns. Air en-

Yarn Spinning: Process Flow Chart

Spinning 1 System

Carding tl - - - - -

Drafting

Roving

Spinning

System

Opening

Carding

Drafting 3 Spinning

Open-end Spinning

Opening i Carding tl Drafting

fl Rotor, Air-jet

Friction

I 1

tangled threads are made from continuous filaments of yarn that are entangled as they pass through a high pressure jet. This, along with the use of silicones as finish applica- tions, has been the focus of R & D efforts recently in the thread indus- try.

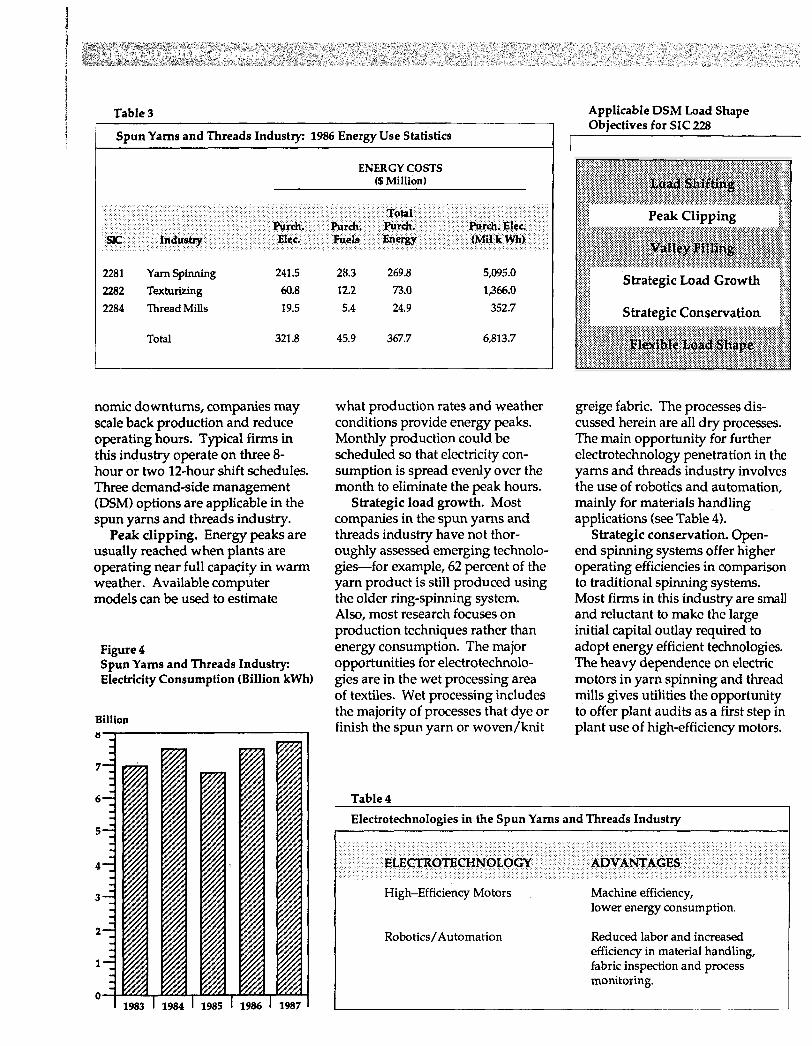

The spun yams and threads in- dustry represent approximately 26 percent of the total purchased electricity in the textile industry group. Figure 4 shows the electric-

ity consumption for years 1983-1987 for SIC 228.' The thread mill sector (SIC 2284) is much less electricity intensive than either the spun yams or texturizing sectors. Also, due to its size the thread mill sector consumes less electricity than the other two sectors. The spun yarns and texturizing sectors have virtu- ally the same electricity intensity (see Table 3).

The demand for goods produced in SIC 228 follows demand from fabric and carpet producers. Thus, the spun yarns and threads industry is very cyclical. Energy use in SIC 228 may vary with the economy and the textile industry as a whole. During prosperous times, firms in this industry may operate 24 hours a day, 7 days a week. During eco-

I

Table 3

Spun Yams and Threads Industry: 1986 Energy Use Statistics

ENERGY COSTS (S Million)

Total Pur&. Pur&. Pur&. Purch. Elec.

SIC Industry Elec. Fuels Energy (Mil k Wh)

2281 Yarn Spinning 241.5 28.3 269.8 5,095.0

2284 ThreadMills 19.5 5.4 24.9 352.7 2282 Texturizing 60.8 12.2 73.0 1366.0

Total 321.8 45.9 367.7 6,813.7

nomic downturns, companies may scale back production and reduce operating hours. Typical firms in this industry operate on three 8- hour or two 12-hour shift schedules. Three demand-side management (DSM) options are applicable in the spun yarns and threads industry. Peak clipping. Energy peaks are

usually reached when plants are operating near full capacity in warm weather. Available computer models can be used to estimate

Figure 4 Spun Yams and Threads Industry: Electricity Consump tion (Billion kWh)

Billion - 4

I 1983 I 1984 I 1985 1 1986 I 1987

what production rates and weather conditions provide energy peaks. Monthly production could be scheduled so that electricity con- sumption is spread evenly over the month to eliminate the peak hours.

Strategic load growth. Most companies in the spun yams and threads industry have not thor- oughly assessed emerging technolo- gies-for example, 62 percent of the yam product is still produced using the older ring-spinning system. Also, most research focuses on production techniques rather than energy consumption. The major opportunities for electrotechnolo- gies are in the wet processing area of textiles. Wet processing includes the majority of processes that dye or finish the spun yarn or woven/knit

Table 4

Applicable DSM Load Shape Objectives for SIC 228

I

Strategic Load Growth

Strategic Conservation

greige fabric. The processes dis- cussed herein are all dry processes. The main opportunity for further electrotechnology penetration in the yarns and threads industry involves the use of robotics and automation, mainly for materials handling applications (see Table 4).

Strategic conservation. Open- end spinning systems offer higher operating efficiencies in comparison to traditional spinning systems. Most firms in this industry are small and reluctant to make the large initial capital outlay required to adopt energy efficient technologies. The heavy dependence on electric motors in yarn spinning and thread mills gives utilities the opportunity to offer plant audits as a first step in plant use of high-efficiency motors.

Electrotechnologies in the Spun Yams and Threads Industry

ELECTROTECHNOLOGY ADVANTAGES

High-Efficiency Motors Machine efficiency, lower energy consumption.

Robotics/ Automation Reduced labor and increased efficiency in material handling, fabric inspection and process monitoring.

American Textile Manufacturers Institute, Inc. 1801 K Street, N.W., Suite 900 Washington, D.C. 20036 (202) 683-7520

American Yarn Spinners Association 2500 Lowell Road Gastonia, NC 28054 (704) 824-3522

. . ... .- . -. . - .- . . ~ ~" .. .. . . -. . I.. ..

. .

Davison's Textile Blue Book, 1989, Davison Publishing Co. Inc., Ridge- wood,NJ 07451

Electric Power Research Institute, Textile Industrv Scopine Studv, EPRI Report, November, 1988.

Market Outlook, Textile World, December, 1989

Textile HiOliPhts, American Textile Manufacturers Institute, Inc., December, 1989

Textile Industrv Guidebook: Profile and DSM Options, EPRI, CU-6789, March, 1990

"Textiles in the '90s: A Decade of Change," Textile World, January, 1990

U. S. Congress, Office of Technology Assessment, U. S. Textile and Apparel Industry: A Revolution in Progress, April, 1987

U.S. Dept. of Commerce, Interna- tional Trade Administration, 1989 U. S. Industrial Outlook and 1990 U. S. Industrial Outlook

U. S. Dept. of Commerce, Bureau of the Census, 1987 Census of Manu- factures

U.S. Dept. of Energy, The U. S. Textile Industrv: An Enerm Per- spective, November, 1988

Basic funding for this Brief is pro- vided by the Electric Power Re- search Institute (EPRI), a nonprofit

organization that conducts research and development on behalf of the electric utility industry. Industry Briefs are designed to provide the utility marketing representative with an overview of industry trends, manufacturing methods and energy use characteristics of each industry. Such informa tion will enable utilities to identify, evaluate and implement industrial DSM options suitable for specific process industry groups.

This Industry Brief was developed by the EPH Textile Office, the College of Textiles, North Carolina State University. The Resource Dynamics Corporation coordinated technical review.

For ordering information, call EPRI's Affiliate Member Program 1-8004320-AMP

For technical information, contact EPRI Textile Office College of Textiles North Carolina State University Box 8301 Raleigh, NC 27695

Copyright 0 1990 Industry Brief, Vol. 1, No 8 Electric Power Research Institute Palo Alto, CA

919-737-7550