SPRING ACCELERATING TRENDS - PREA

6

SPRING 2020 ACCELERATING TRENDS IN THE POST–COVID-19 INDUSTRIAL AND RETAIL REAL ESTATE SECTORS 56 PREA Quarterly, Spring 2020

Transcript of SPRING ACCELERATING TRENDS - PREA

56 PREA Quarterly, Spring 2020

S P R I N G2 0 2 0

ACCELERATINGTRENDS

IN THE POST–COVID-19 INDUSTRIAL AND RETAIL REAL ESTATE SECTORS

56 PREA Quarterly, Spring 2020

PREA Quarterly, Spring 2020 57

accounts for about 20% of all retail spending;

CenterSquare believes this market share could reach

as high as 50% based on analysis of product types

that have reached peak penetration, such as books

and music, where e-commerce accounts for more

than 60% of all sales. Further, e-commerce represents

an efficiency gain—it is generally cheaper for retailers

to distribute online, and consumers gravitate toward

this lower cost and convenience. Given these factors,

many other goods, such as general merchandise,

fashion, and jewelry, are likely to see significant

e-commerce penetration (Exhibit 1).

Even before the COVID-19 pandemic struck, a significant change in consumer demand patterns

had occurred over the past decade, driven by

demographics, technology, and evolving consumer

preferences. In the first quarter of 2020, the

environment rapidly evolved to accelerate these

dynamics, creating investment megatrends that are

critical to optimizing a real estate investment strategy.

One of the most notable megatrends is the

emergence of e-commerce. For those paying attention

to pricing in the REIT market, the shift away from

retail toward industrial was apparent years before it

played out in the private markets. The COVID-19

crisis is poised to push this trend over the tipping

point, impacting both the retail and the industrial

sectors in meaningful ways. Additionally, the crisis

is creating a more immediate need for the build-out

of a sophisticated supply chain of modern logistics

facilities and an opportunity for real estate investors.

The fallout from this trend is also impacting brick-

and-mortar retail—most acutely, malls.

Investors who rotated their private real estate

exposure to focus on sectors and properties poised to

benefit from these trends in recent years have likely

already seen outperformance relative to traditional

portfolios. As the market absorbs the impact of

COVID-19 and values adjust accordingly, these

secular externalities are expected to continue to

provide ongoing support for pricing. When assessing

additional capital deployment in real estate in 2020,

CenterSquare believes that allocating to specific

industrial and retail properties positioned to benefit

from these dynamics and serve this demand should

be a key consideration for institutional investors.

Accelerating the Shift to E-CommerceThe shift of goods consumption from retail storefronts

to the internet is well known. Today, e-commerce

Scott CroweCenterSquare Investment

Management

QQuarterlyQQuarterly

Exhibit 1: E-Commerce Penetration by Product Type

Sources: US Census Bureau, CenterSquare Investment Management; as of January 2020

Exhibit 2: Amazon Daily iOS Active User Growth, Year Over Year

Source: Evercore ISI; Dec. 2019–March 23, 2020

ACCELERATINGTRENDS

IN THE POST–COVID-19 INDUSTRIAL AND RETAIL REAL ESTATE SECTORS

58 PREA Quarterly, Spring 2020

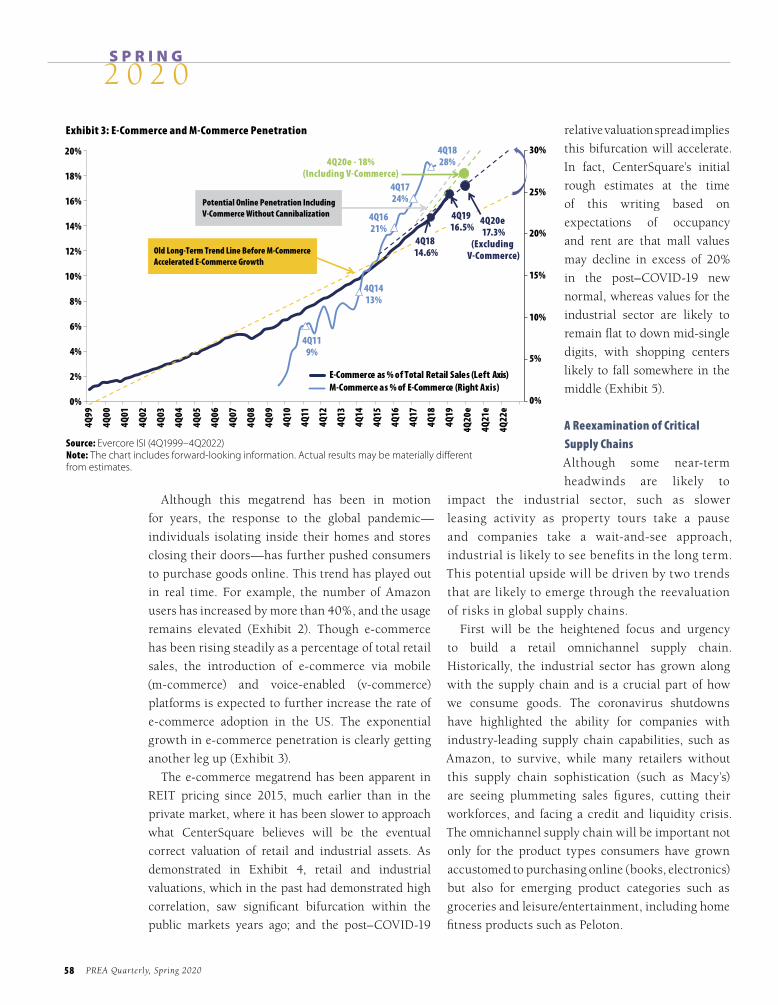

Although this megatrend has been in motion

for years, the response to the global pandemic—

individuals isolating inside their homes and stores

closing their doors—has further pushed consumers

to purchase goods online. This trend has played out

in real time. For example, the number of Amazon

users has increased by more than 40%, and the usage

remains elevated (Exhibit 2). Though e-commerce

has been rising steadily as a percentage of total retail

sales, the introduction of e-commerce via mobile

(m-commerce) and voice-enabled (v-commerce)

platforms is expected to further increase the rate of

e-commerce adoption in the US. The exponential

growth in e-commerce penetration is clearly getting

another leg up (Exhibit 3).

The e-commerce megatrend has been apparent in

REIT pricing since 2015, much earlier than in the

private market, where it has been slower to approach

what CenterSquare believes will be the eventual

correct valuation of retail and industrial assets. As

demonstrated in Exhibit 4, retail and industrial

valuations, which in the past had demonstrated high

correlation, saw significant bifurcation within the

public markets years ago; and the post–COVID-19

relative valuation spread implies

this bifurcation will accelerate.

In fact, CenterSquare’s initial

rough estimates at the time

of this writing based on

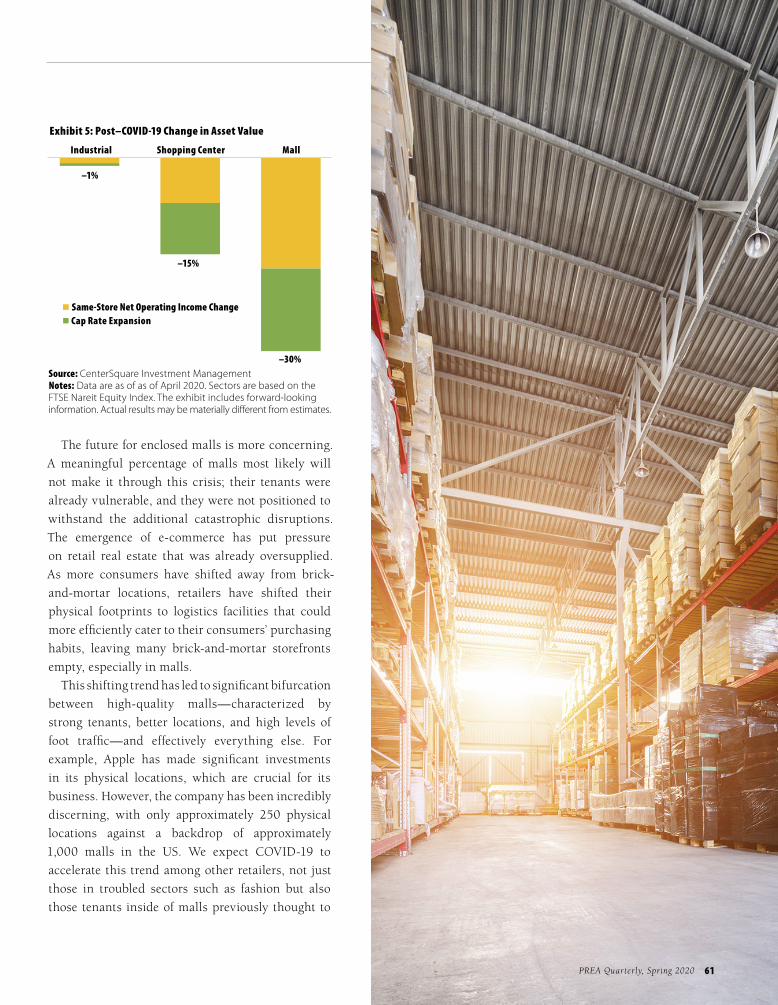

expectations of occupancy

and rent are that mall values

may decline in excess of 20%

in the post–COVID-19 new

normal, whereas values for the

industrial sector are likely to

remain flat to down mid-single

digits, with shopping centers

likely to fall somewhere in the

middle (Exhibit 5).

A Reexamination of Critical Supply ChainsAlthough some near-term

headwinds are likely to

impact the industrial sector, such as slower

leasing activity as property tours take a pause

and companies take a wait-and-see approach,

industrial is likely to see benefits in the long term.

This potential upside will be driven by two trends

that are likely to emerge through the reevaluation

of risks in global supply chains.

First will be the heightened focus and urgency

to build a retail omnichannel supply chain.

Historically, the industrial sector has grown along

with the supply chain and is a crucial part of how

we consume goods. The coronavirus shutdowns

have highlighted the ability for companies with

industry-leading supply chain capabilities, such as

Amazon, to survive, while many retailers without

this supply chain sophistication (such as Macy’s)

are seeing plummeting sales figures, cutting their

workforces, and facing a credit and liquidity crisis.

The omnichannel supply chain will be important not

only for the product types consumers have grown

accustomed to purchasing online (books, electronics)

but also for emerging product categories such as

groceries and leisure/entertainment, including home

fitness products such as Peloton.

S P R I N G2 0 2 0

Exhibit 3: E-Commerce and M-Commerce Penetration

Source: Evercore ISI (4Q1999–4Q2022)Note: The chart includes forward-looking information. Actual results may be materially different from estimates.

60 PREA Quarterly, Spring 2020

The second emerging trend is the potential

diversification of manufacturing locations to

create resiliency in supply chains. The market is

already seeing signs of deglobalization, and that

means more demand for domestic warehouses

and logistics facilities. The US-China trade war

first highlighted the need for redundant supply

chains when many manufacturers and retailers

saw complete disruption as tariffs and restrictions

severely hindered the movement of goods to and

from China. The COVID-19 shutdown was another

reminder. To put this into context, consider the

US pharmaceutical supply chain, where 97%

of all antibiotics come from China.1 Over the

past decade, China’s integration into the supply

chain was driven by lower labor costs, but tariffs,

technological efficiencies, and consumers’ demand

for faster delivery effectively bridged that labor-cost

gap. In the post–COVID-19 new normal, corporate

America may well focus on ensuring these critical

aspects of our lives can be satisfied via a domestic

supply chain.

Diverse Recoveries Across RetailIn contrast to the opportunities in the industrial

sector, CenterSquare believes certain areas of the

retail sector will be permanently impaired by the

COVID-19 crisis in the form of lost occupancy and a

liquidity crunch. Yet each type of retail property will

recover differently.

Within the open-air shopping center space,

service-based retail will likely experience the

greatest recovery when consumers return to gyms,

hair salons, cafés, and breweries once government-

mandated shutdowns are lifted; these services cannot

be accessed online. Grocery-anchored shopping

centers should also recover as grocery-driven foot

traffic brings consumers back to the other retailers

in the shopping centers. However, grocery could

see an acceleration in e-commerce adoption among

consumers who shifted to online delivery during

the shutdown. Through the pandemic, the online

traffic for Walmart’s groceries has jumped 55%.

With 40 million new online grocery users in the

US, this adoption is expected to continue, according

to CBRE. On the other side of the shopping center

spectrum, the lowest-quality shopping centers likely

will not survive this crisis, as this virus rationalizes

the oversupply of retailers.

Exhibit 4: Historical Industrial Versus Retail REIT Implied Cap Rates

Source: CenterSquare Investment Management; 1Q1999–1Q2020

S P R I N G2 0 2 0

1. Yanzhong Huang, “U.S. Dependence on Pharmaceutical Products from China,” Council on Foreign Relations blog, Aug. 14, 2019, https://www.cfr.org/blog/us-dependence-pharmaceutical-products-china.

PREA Quarterly, Spring 2020 61

The future for enclosed malls is more concerning.

A meaningful percentage of malls most likely will

not make it through this crisis; their tenants were

already vulnerable, and they were not positioned to

withstand the additional catastrophic disruptions.

The emergence of e-commerce has put pressure

on retail real estate that was already oversupplied.

As more consumers have shifted away from brick-

and-mortar locations, retailers have shifted their

physical footprints to logistics facilities that could

more efficiently cater to their consumers’ purchasing

habits, leaving many brick-and-mortar storefronts

empty, especially in malls.

This shifting trend has led to significant bifurcation

between high-quality malls—characterized by

strong tenants, better locations, and high levels of

foot traffic—and effectively everything else. For

example, Apple has made significant investments

in its physical locations, which are crucial for its

business. However, the company has been incredibly

discerning, with only approximately 250 physical

locations against a backdrop of approximately

1,000 malls in the US. We expect COVID-19 to

accelerate this trend among other retailers, not just

those in troubled sectors such as fashion but also

those tenants inside of malls previously thought to

Exhibit 5: Post–COVID-19 Change in Asset Value

Source: CenterSquare Investment ManagementNotes: Data are as of as of April 2020. Sectors are based on the FTSE Nareit Equity Index. The exhibit includes forward-looking information. Actual results may be materially different from estimates.

PREA Quarterly, Spring 2020 61

62 PREA Quarterly, Spring 2020

S P R I N G2 0 2 0

be more resilient, such as experiential and movie

theaters. Even after mandated shutdowns are lifted,

consumers will be slow to return to enclosed, high-

foot-traffic areas, CenterSquare believes, further

dragging out the recovery for many mall tenants.

The silver lining to the COVID-19 crisis, however,

is the supply-side rationalization of retail real estate.

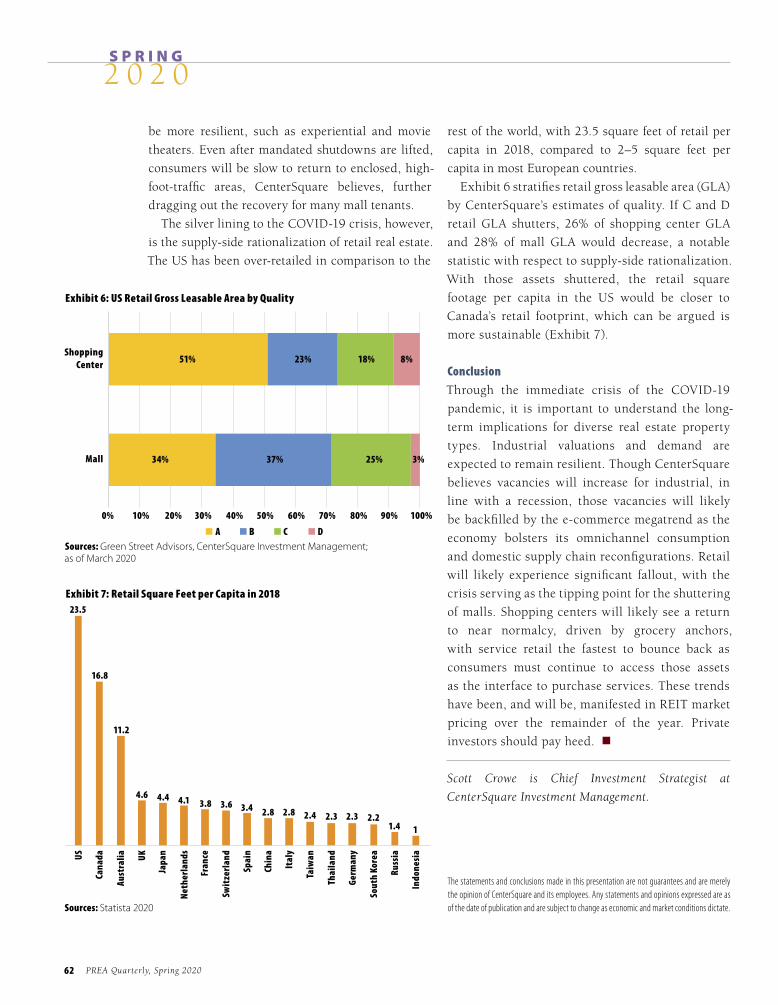

The US has been over-retailed in comparison to the

rest of the world, with 23.5 square feet of retail per

capita in 2018, compared to 2–5 square feet per

capita in most European countries.

Exhibit 6 stratifies retail gross leasable area (GLA)

by CenterSquare’s estimates of quality. If C and D

retail GLA shutters, 26% of shopping center GLA

and 28% of mall GLA would decrease, a notable

statistic with respect to supply-side rationalization.

With those assets shuttered, the retail square

footage per capita in the US would be closer to

Canada’s retail footprint, which can be argued is

more sustainable (Exhibit 7).

ConclusionThrough the immediate crisis of the COVID-19

pandemic, it is important to understand the long-

term implications for diverse real estate property

types. Industrial valuations and demand are

expected to remain resilient. Though CenterSquare

believes vacancies will increase for industrial, in

line with a recession, those vacancies will likely

be backfilled by the e-commerce megatrend as the

economy bolsters its omnichannel consumption

and domestic supply chain reconfigurations. Retail

will likely experience significant fallout, with the

crisis serving as the tipping point for the shuttering

of malls. Shopping centers will likely see a return

to near normalcy, driven by grocery anchors,

with service retail the fastest to bounce back as

consumers must continue to access those assets

as the interface to purchase services. These trends

have been, and will be, manifested in REIT market

pricing over the remainder of the year. Private

investors should pay heed. n

Scott Crowe is Chief Investment Strategist at

CenterSquare Investment Management.

Exhibit 6: US Retail Gross Leasable Area by Quality

Exhibit 7: Retail Square Feet per Capita in 2018

Sources: Green Street Advisors, CenterSquare Investment Management; as of March 2020

Sources: Statista 2020

The statements and conclusions made in this presentation are not guarantees and are merely the opinion of CenterSquare and its employees. Any statements and opinions expressed are as of the date of publication and are subject to change as economic and market conditions dictate.