Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies...

35

Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies COPYRIGHT ©2007 Thomson South-Western, a part of the Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under license. Chapter 12

-

date post

21-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies...

Special Industries:Banks, Utilities, Oil and Gas,

Transportation, Insurance,Real Estate Companies

COPYRIGHT ©2007 Thomson South-Western, a part of the Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under license.

Chapter 12

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #2

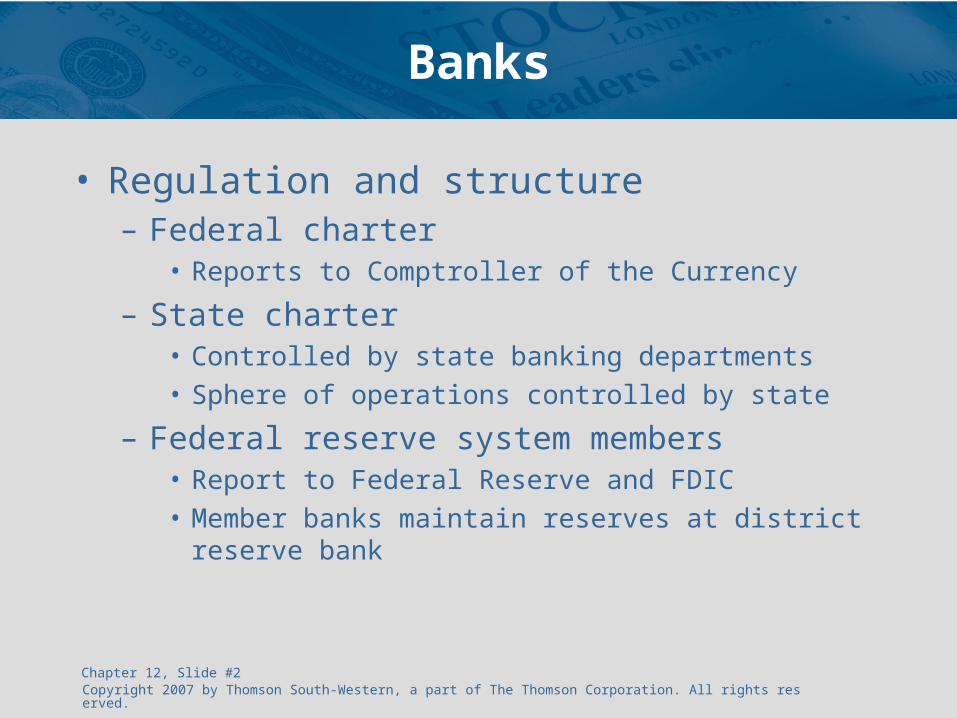

Banks

• Regulation and structure– Federal charter

• Reports to Comptroller of the Currency

– State charter• Controlled by state banking departments• Sphere of operations controlled by state

– Federal reserve system members• Report to Federal Reserve and FDIC• Member banks maintain reserves at district reserve bank

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #3

Banks (cont’d)

• Balance Sheet – Assets

• Loans to customers are assets (receivables)• Assets are not subdivided into current and noncurrent• Typical assets

– Cash on hand or due from other banks, investment securities, loans, bank premises, and equipment

• Fixed-rate assets expose bank to risk if rates rise– The receivable itself decreases in value

• LDC (less-developed countries) loans more risky than domestic

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #4

Banks (cont’d)

• Balance Sheet– Assets

• Review for related-party loans• Allowance for loan loss account• Other real estate – property taken during foreclosure;

holding for probable resale

– Liabilities• Current: savings, time/demand deposits

– Reduction in this liability also indicates the loss of an inexpensive source of lendable funds

• Long-term: loan obligations, long-term debt

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #5

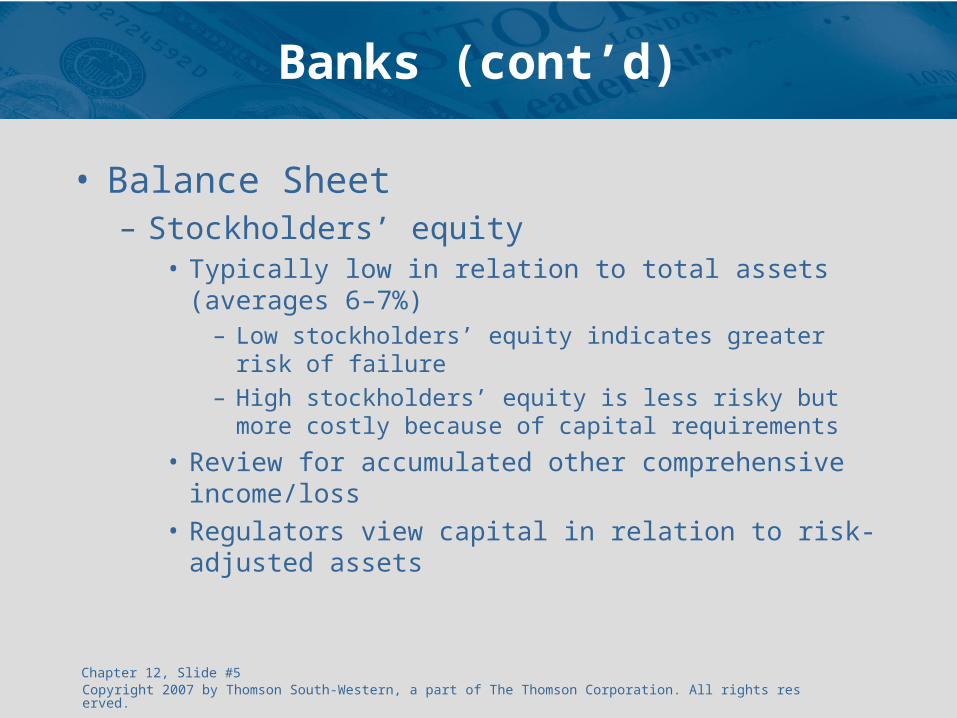

Banks (cont’d)

• Balance Sheet– Stockholders’ equity

• Typically low in relation to total assets (averages 6–7%)– Low stockholders’ equity indicates greater risk of failure

– High stockholders’ equity is less risky but more costly because of capital requirements

• Review for accumulated other comprehensive income/loss• Regulators view capital in relation to risk-adjusted assets

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #6

Banks (cont’d)

• Balance Sheet– Read notes and Management’s Discussion and

Analysis for indication of• Nonperforming assets: assets no longer producing income

or producing reduced income– Nonaccrual loans: payments are past due; interest no longer

being accrued– Renegotiated loans: modified as part of a restructured

agreement– Watch carefully; these may indicate potential future

difficulties

• Commitments and contingencies

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #7

Banks (cont’d)

• Income Statement– Interest

• Principal revenue is interest earned on loans and investment securities

• Principal expense is interest on deposits and other debt• Excess of interest revenue over interest expense is net

interest income (margin)• Interest rates

– Falling: reduces expense (interest paid on deposits)

– Increasing: increases expense

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #8

Banks (cont’d)

• Income Statement– Other income

• Fees, service charges, trading securities gain/loss, securities transactions

• Of increasing importance to banks

• Ratios– Many ‘traditional’ ratios do not work for banks– Workable ratios

• Return on assets• Return on equity• Most investment-related ratios

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #9

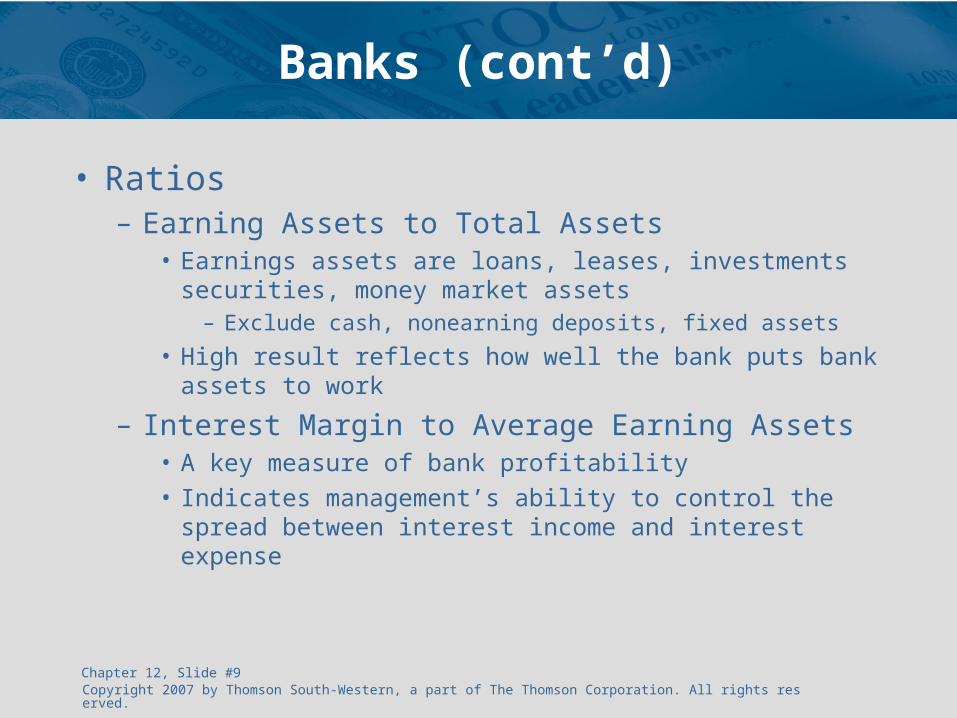

Banks (cont’d)

• Ratios– Earning Assets to Total Assets

• Earnings assets are loans, leases, investments securities, money market assets

– Exclude cash, nonearning deposits, fixed assets

• High result reflects how well the bank puts bank assets to work

– Interest Margin to Average Earning Assets• A key measure of bank profitability• Indicates management’s ability to control the spread

between interest income and interest expense

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #10

Banks (cont’d)

• Ratios– Loan Loss Coverage Ratio

• (Pretax income + provision for loan losses) ÷ net charge-offs

• Measures– Asset quality

– The level of protection of loans

– Equity Capital to Total Assets• Measures the extent of equity ownership in the bank

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #11

Banks (cont’d)

• Ratios– Deposits Times Capital

• Average deposits ÷ average stockholders’ equity• A type of debt-to-equity ratio• Concerns both depositors and stockholders• Indicators

– More capital implies greater margin of safety

– More deposits indicate investment potential

– Loans to Deposits• A type of asset to liability or debt coverage ratio

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #12

Regulated Utilities

• Regulation and structure– Subject to government regulation and rate

regulation– Accounting procedures prescribed by

• Federal Energy Regulatory Commission• Federal Communications Commission• State regulatory agencies

– Regulated utilities have added nonregulated businesses

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #13

Regulated Utilities (cont’d)

• Financial Statements– Balance sheet

• Plant, property, and equipment is listed first• Capitalization section includes sources of financing

– Long-term capital

– Long-term debt

• Current liabilities and deferred charges

– Income statement• Operating income• Other income• Interest charges

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #14

Regulated Utilities (cont’d)

• Financial Statements– Construction work in progress [balance sheet asset]

• Substantial construction work in progress should be viewed as more risky

• Rate base determination will not normally consider construction work in progress

• Disallowed costs provide no return

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #15

Regulated Utilities (cont’d)

• Financial Statements– Allowance for funds used during construction

[income statement]• Allowance for equity funds [other income]

– An assumed rate of return on equity funds

• Allowance for borrowed funds [interest charges]

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #16

Regulated Utilities (cont’d)

• Ratios– Few of the traditional ratios are appropriate for

regulated utilities

– Operating Ratio• Measures efficiency

• Operating expenses ÷ operating revenue

– Funded Debt to Operating Property• Operating (net) property is plant and equipment less

accumulated depreciation

• Include construction in progress

• Measures debt coverage

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #17

Regulated Utilities (cont’d)

• Ratios– Percent Earned on Operating Property

• Relates net earnings to the assets primarily intended to generate earnings

– Operating Revenue to Operating Property• A type of operating asset turnover ratio• Fixed plant is often much larger than revenue

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #18

Oil and Gas

• General background– Major impact on financial statements from method

of accounting for exploration and production– Specific required supplemental disclosures– Traditional ratios apply

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #19

Oil and Gas (cont’d)

• Successful-Efforts versus Full-Costing Methods– Successful-efforts

• Theory: unsuccessful efforts are costs of the current period

• Capitalize costs of successful efforts• Immediately expense costs of unsuccessful efforts • More conservative approach yielding lower net income

due to immediate expensing of unsuccessful efforts

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #20

Oil and Gas (cont’d)

• Successful-Efforts versus Full-Costing Methods– Full-costing

• Theory: all costs are part of eventually finding successful wells

• Capitalize all costs of exploration• Items capitalized are subject to depletion

– In total, the same amount is expensed under either method, but the timing of expense recognition varies dramatically

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #21

Oil and Gas (cont’d)

• Successful-Efforts versus Full-Costing Methods– Practical application

• Smaller companies choose full-costing method• Larger balance sheet due to full capitalization• Short-run higher profit (expense is periodic depletion, not full

cost)• Presents more favorable picture to creditors and investors• Larger companies use variation of successful-efforts method• Smaller balance sheet with only successful efforts capitalized• Short-run lower profit due to immediate expensing of

unsuccessful efforts

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #22

Oil and Gas (cont’d)

• Required supplementary disclosure: SFAS 69– Proved oil and gas reserve quantities– Results of operations for oil- and gas-producing

activities– Costs incurred in oil and gas property acquisition,

exploration, and development activities– Capitalized costs relating to oil- and gas-producing

activities– A standardized measure of discounted future net cash

flows relating to proved oil and gas reserve quantities

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #23

Transportation

• Regulation and oversight– Civil Aeronautics Board

• Commercial aviation• Uniform system of accounts and reporting

– Interstate Commerce Commission• Interstate railroads• Interstate motor carriers• Uniform system of accounts and reporting

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #24

Transportation (cont’d)

• Financial Statements– Balance sheet

• Similar to manufacturing and retailing reporting• Plant, property, and equipment makes up large portion of

assets

– Income statement• Similar to utility reporting• Revenues and expenses grouped by natural objectives and

functional activities• Reports operating income (operating revenues minus operating

expenses)• Presented in single-step fashion

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #25

Transportation (cont’d)

• Ratios– Sources of comparable data

• Interstate Commerce Commission’s Annual Report on transport statistics

• American Trucking Association’s Financial Analysis of the Motor Carrier Industry

– Operating Ratio• Operating expenses ÷ operating revenue

• External forces will impact the ratio

– Long-Term Debt to Operating Property• Operating property: long-term property and equipment

• Measures the sources of funds with which property has been obtained

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #26

Transportation (cont’d)

• Ratios– Operating Revenue to Operating Property

• Measures turnover of operating assets• Operating objective is to generate as many dollars in

revenue per dollar of property

– Per-Mile, Per-Person, and Per-Ton Passenger Load Factors

• Not required but often presented in the financial statement notes or highlights

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #27

Insurance

• Types of service– Identified contract service (mortality or loss)– Investment management service

• Types of insurance organizations– Stock companies: organized to return a profit to stockholders– Mutual companies: incorporated without private ownership

interest– Fraternal benefit societies: similar to a mutual insurance

company– Assessment companies: organized group with a similar

interest

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #28

Insurance (cont’d)

• Primary regulation is at the state level• Accounting

– Uniform SAP (statutory accounting practices) reporting under auspices of the National Association of Insurance Commissioners

• Balance sheet is emphasized; focus is on solvency• Ratio analysis conducted by the NAIC

– GAAP exists for public (SEC) filings

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #29

Insurance (cont’d)

• Sources of comparative data– Best’s Insurance Reports

• Separate ratings for life-health and property-casualty companies

• Ratings range from A+ (Superior) to C– (Fair); also a “Not Assigned” category

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #30

Insurance (cont’d)

• Balance Sheet Under GAAP– Investments

• High liquidity, typically bonds• Review spread between cost or amortized cost and fair value• Review stockholders’ equity for unrealized gains and losses

on investments

– Assets Other than Investments• Operating (plant) assets• Policy acquisition costs are deferred and matched to

premium-earning period for GAAP; expensed for SAP• Goodwill and other intangibles

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #31

Insurance (cont’d)

• Balance Sheet Under GAAP– Liabilities

• Loss reserves: commitments reported at present value• Policy and contract claims: claims accrued net of

recoverable portion

– Stockholders’ equity• Resembles other industry stockholders’ equity• Review for unrealized gains and losses on investments

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #32

Insurance (cont’d)

• Income Statement Under GAAP– Duration of contract governs revenue

• Short-duration: revenue recognized over period of the contract in proportion to protection provided

• Long-duration: revenue recognized when premium is due– Low-risk contracts are “investment contracts” and accounted

for as liabilities

– Realized gains/losses from investments

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #33

Insurance (cont’d)

• Ratios– Industry-specific based on SAP reporting to states– Ratios based on GAAP data

• Profitability• Investor-related

– Confusion surrounding insurance industry reporting• Two accounting standards: SAP and GAAP• Insurance stock typically carries discount to the average

market price

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #34

Insurance (cont’d)

• Federal oversight and enforcement– Limited by McCarran-Ferguson Act of 1945– SEC has jurisdiction only over publicly-traded

companies– Nationwide review of insurance practices by FBI

Copyright 2007 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 12, Slide #35

Real Estate Companies

• Construct and operate income-producing real properties

• Contend that conventional accounting misleads investors

• Real estate companies supplement historical cost information with current value– Current value is based on future income potential