S.P. Singh 26 June 2013€¢ Questions & Answers 2 . ... Intra- Group Management Charges ... •...

60

India - Circulars on R&D Demystifying or Mystifying? S.P. Singh 26 June 2013

Transcript of S.P. Singh 26 June 2013€¢ Questions & Answers 2 . ... Intra- Group Management Charges ... •...

India - Circulars on R&D

Demystifying or Mystifying?

S.P. Singh

26 June 2013

©2013 Deloitte Haskins & Sells

Agenda

• Introduction

• Dispute Resolution

• Circulars on R&D

• An update on the Indian Advance Pricing Agreement (APA) program

• Software Industry- Corporate Tax Implications

‒ Section 10 A- Provisions in Brief

‒ Section 10AA-Provisions in Brief

‒ Recent Controversies

‒ Direct Tax Code

• Questions & Answers

2

Introduction

©2013 Deloitte Haskins & Sells

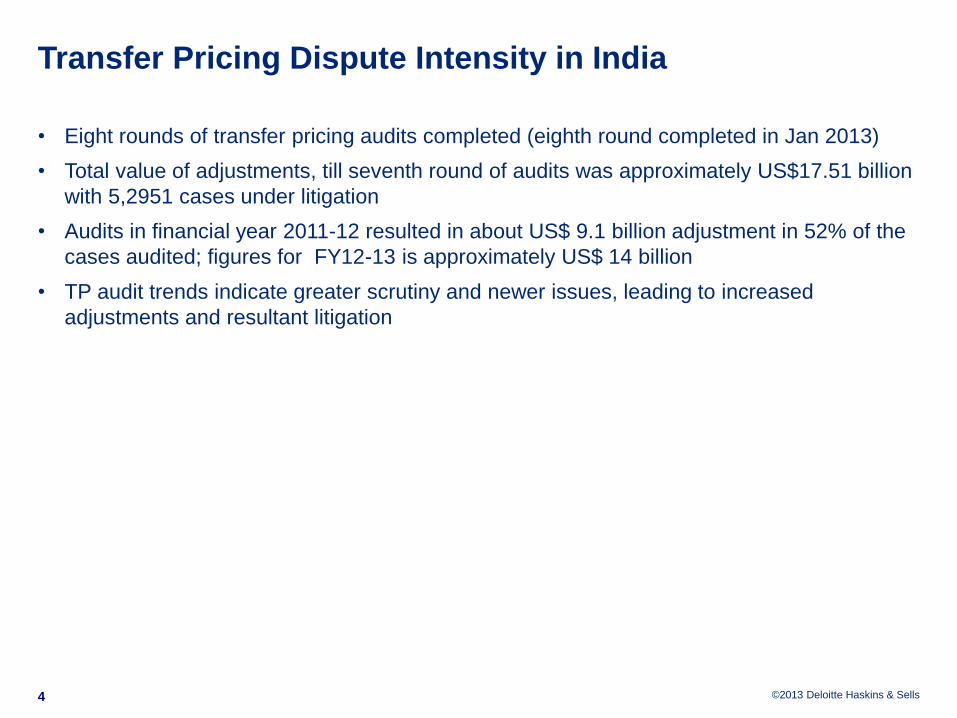

Transfer Pricing Dispute Intensity in India

• Eight rounds of transfer pricing audits completed (eighth round completed in Jan 2013)

• Total value of adjustments, till seventh round of audits was approximately US$17.51 billion

with 5,2951 cases under litigation

• Audits in financial year 2011-12 resulted in about US$ 9.1 billion adjustment in 52% of the

cases audited; figures for FY12-13 is approximately US$ 14 billion

• TP audit trends indicate greater scrutiny and newer issues, leading to increased

adjustments and resultant litigation

4

©2013 Deloitte Haskins & Sells

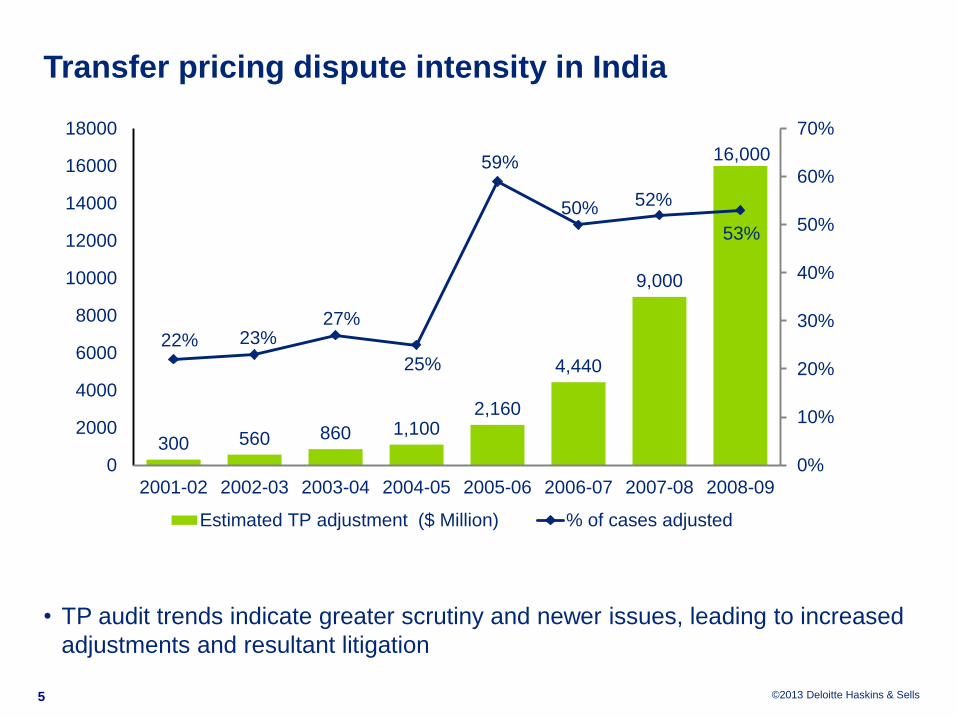

Transfer pricing dispute intensity in India

• TP audit trends indicate greater scrutiny and newer issues, leading to increased

adjustments and resultant litigation

5

300 560 860 1,100 2,160

4,440

9,000

16,000

22% 23% 27%

25%

59%

50% 52%

53%

0%

10%

20%

30%

40%

50%

60%

70%

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

Estimated TP adjustment ($ Million) % of cases adjusted

©2013 Deloitte Haskins & Sells

Transfer Pricing- Recurrent Issues

6

Mark-up for service providers

Comparable and Adjustments

Intra- Group Management Charges

Intercompany Financial Transactions

Royalties

©2013 Deloitte Haskins & Sells

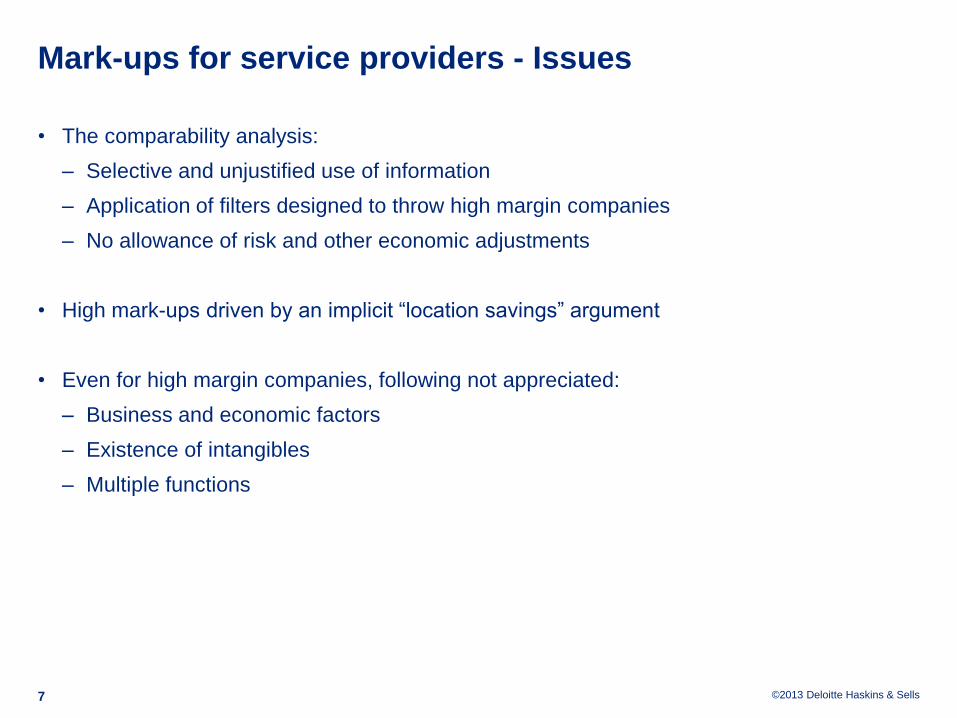

Mark-ups for service providers - Issues

• The comparability analysis:

‒ Selective and unjustified use of information

‒ Application of filters designed to throw high margin companies

‒ No allowance of risk and other economic adjustments

• High mark-ups driven by an implicit “location savings” argument

• Even for high margin companies, following not appreciated:

‒ Business and economic factors

‒ Existence of intangibles

‒ Multiple functions

7

©2013 Deloitte Haskins & Sells

Location Savings Why is it being discussed?

• India’s tax authority has highlighted India’s cost advantage as the primary reason for

multinationals transferring services and manufacturing to India:

‒ In service companies, salaries are the main cost for companies, varying from 40

percent to 50 percent of total cost. This cost can also be significant for labor-intensive

manufacturing companies; and

‒ Typically, Indian salaries can be as low as 25% of those in the United States.

• The tax authority has not quantified location savings yet, and has reached out to

economists in other government departments to understand the quantitative impact

• In the meanwhile, Indian tax authority has relied on this as a qualitative argument to

support a higher return for the local entity

• It is only a matter of time before Indian tax authority comes up with an approach to

calculate the quantitative impact of location savings

8

©2013 Deloitte Haskins & Sells

Location saving approach outside India

• Indian tax authority and the ITAT often refer to judgments of foreign courts and views

expressed by tax authorities. Following are some of the US cases, where location savings

was at issue:

‒ Sundstrand: US parent established a subsidiary in Singapore, provided it exclusive

rights to intangibles for a royalty, and then left the location savings in Singapore. Tax

authority argued that the Singapore entity is a mere contract manufacturer. The court

decided in the favor of the taxpayer;

‒ Compaq: In this case again, the court ruled that the savings could stay in Singapore,

especially in light of the CUP prices produced by the company, and strong quality

standard of the Singapore entity. This case was not well accepted within the tax

community because it ignored the role of unique intangibles that were owned by the US

company.

• Indian tax authority is likely to interpret these cases in a superficial manner and argue that

the savings should stay in the country where they arise;

• In anticipation of such arguments, it is important to develop facts to show the strong

bargaining position of US affiliate, originating from unique intangibles, customer

relationships, and access to multiple suppliers. Investment in project management and

other minor tools should be funded by the US parent.

9

©2013 Deloitte Haskins & Sells

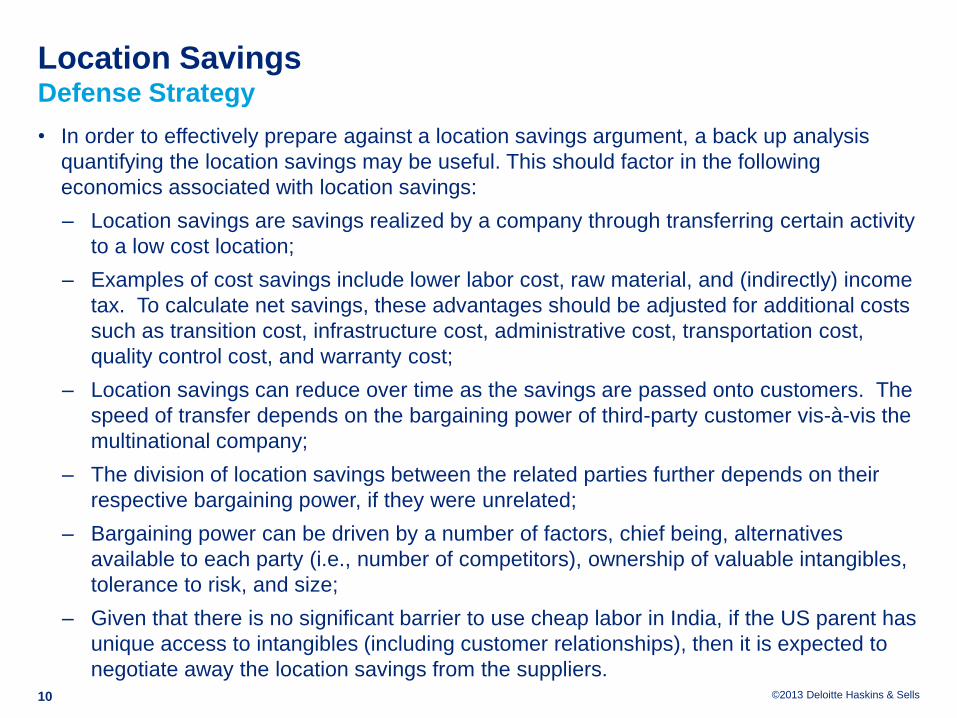

Location Savings Defense Strategy

• In order to effectively prepare against a location savings argument, a back up analysis

quantifying the location savings may be useful. This should factor in the following

economics associated with location savings:

‒ Location savings are savings realized by a company through transferring certain activity

to a low cost location;

‒ Examples of cost savings include lower labor cost, raw material, and (indirectly) income

tax. To calculate net savings, these advantages should be adjusted for additional costs

such as transition cost, infrastructure cost, administrative cost, transportation cost,

quality control cost, and warranty cost;

‒ Location savings can reduce over time as the savings are passed onto customers. The

speed of transfer depends on the bargaining power of third-party customer vis-à-vis the

multinational company;

‒ The division of location savings between the related parties further depends on their

respective bargaining power, if they were unrelated;

‒ Bargaining power can be driven by a number of factors, chief being, alternatives

available to each party (i.e., number of competitors), ownership of valuable intangibles,

tolerance to risk, and size;

‒ Given that there is no significant barrier to use cheap labor in India, if the US parent has

unique access to intangibles (including customer relationships), then it is expected to

negotiate away the location savings from the suppliers. 10

Dispute Resolution

©2013 Deloitte Haskins & Sells

TP Issues - ITAT’s Observation

• Functions, Assets and Risk profile of companies are of utmost importance for selecting

appropriate comparable companies –Logica Private Limited (Bangalore Tribunal)

• Significance of high turnover filter while making the final selection of comparable

companies –Trilogy E-Business Software India Private Limited (Bangalore Tribunal) *

• Companies making super normal profits can only be excluded if there are abnormal factors

- Adobe Systems India Private (Delhi Tribunal)

• Giant companies like Infosys, Wipro can not be taken as comparable companies as they

are engaged in diversified activities and development of products - Intoto Software India

Private Limited (Hyderabad Tribunal)

* Special Bench has been constituted to decide whether high/ low turnover filter should be applied for making selection of

comparable companies.

12

©2013 Deloitte Haskins & Sells

TP Issues - ITAT’s Observation ….(Contd.)

• Related Party Transactions (“RPT”) – No uniform view among Tribunals:

‒ Philips Software Centre Private Limited (Bangalore Tribunal) - even with a single rupee

of transaction with related parties should not be considered as comparable

‒ Sony India Private Limited (Delhi Tribunal) - RPT threshold limit 10%-15%

‒ Actis Advisers Private Limited (Delhi Bench) - not exceed 25% of total revenue

13

©2013 Deloitte Haskins & Sells

Recent Trends in US-India MAP Process

• Several taxpayers filed for Mutual Agreement Procedure (MAP) with the US and India

competent authorities

• Till last year, some resolutions for software and business support services at cost plus

markups ranging from 17.5% to 24%

• However, contract R&D markups are being proposed at cost plus 30%

• Last meeting in June 2012 – no resolution

• Currently meetings on hold

• Further developments awaited

14

©2013 Deloitte Haskins & Sells

Safe Harbour Rules

Safe Harbour provisions in India introduced in 2009

• Rangachary Committee was to submit its report on Safe Harbour rules by 31 March 2013

‒ Rules under deliberation e.g. sector specific, service specific, mark-up etc.

• Safe Harbour still awaited

International Safe Harbour experience

• Existing safe harbor rules in countries e.g. US, Australia, New Zealand, Brazil and Mexico

• Challenges

‒ Potential risk of double taxation

‒ Implementation might be a challenge

Awaiting Safe Harbour Margins

15

©2013 Deloitte Haskins & Sells

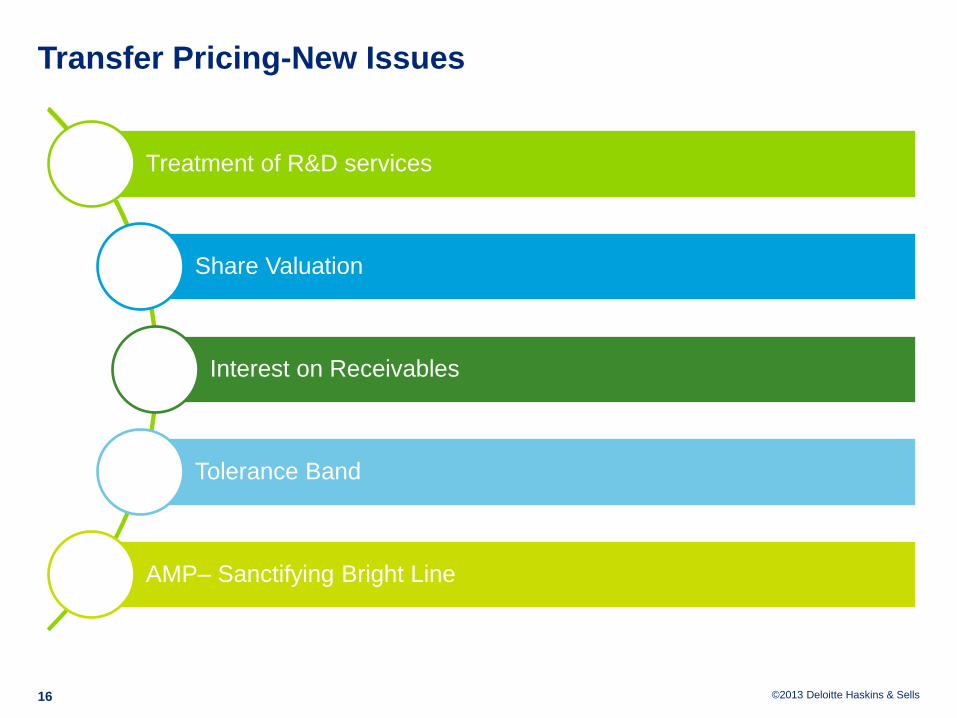

Transfer Pricing-New Issues

16

Treatment of R&D services

Share Valuation

Interest on Receivables

Tolerance Band

AMP– Sanctifying Bright Line

©2013 Deloitte Haskins & Sells

Interest on Receivables

• Finance Act 2012 extended meaning of the term “international transaction” to include,

apart from others:

‒ capital financing, lending or guarantee, any type of advance, receivables, etc.

• Experience from the last round of TP audit:

‒ Only receivables pertaining to AEs considered

‒ Regardless of business activity- manufacturing, trading, services etc.

‒ Presumptive arm’s length standard for the holding period e.g. 30 days

‒ Interest rate based on Indian long term lending rates

17

©2013 Deloitte Haskins & Sells

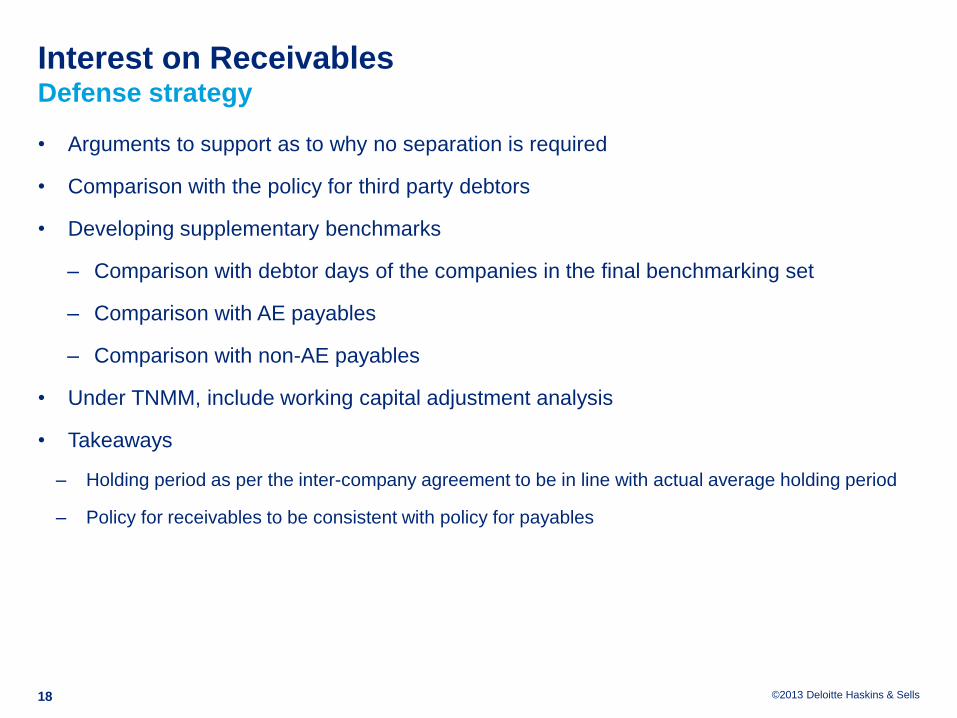

Interest on Receivables Defense strategy

• Arguments to support as to why no separation is required

• Comparison with the policy for third party debtors

• Developing supplementary benchmarks

– Comparison with debtor days of the companies in the final benchmarking set

– Comparison with AE payables

– Comparison with non-AE payables

• Under TNMM, include working capital adjustment analysis

• Takeaways

‒ Holding period as per the inter-company agreement to be in line with actual average holding period

‒ Policy for receivables to be consistent with policy for payables

18

©2013 Deloitte Haskins & Sells

Share Valuation

• Issuance of equity/preference shares to foreign group entities at the valuation undertaken

by an independent valuer

• The valuation is challenged by the transfer pricing officer and revalued based on the

discounted cash flow approach

• The conclusion drawn was that the foreign entity subscribed to the shares of its Indian sub

at a price much lower than the market price

• Shortfall treated as receivable and hence loan granted to AE

• In some cases, adjustment made for both receivable as well as interest on the receivable

19

©2013 Deloitte Haskins & Sells

Share Valuation Issues under Debate

• Whether there is a short receipt

• Does the definition of "international transaction" include equity

• Whether the alleged short receipt of equity can be considered as income

• Can the alleged differential be characterized as debt

• Whether the alleged loan can be added to income as a transfer pricing adjustment

• Whether the approach adopted by the TPO to arrive at the imputed interest rate is at arm’s

length

20

Circulars on R&D services

©2013 Deloitte Haskins & Sells

Background

• India has, in the recent times, emerged as an important location for R&D centers for

MNEs.

• The centers work as captive units for the group whereby they provide contract R&D

services to the group companies across the world.

• The services are spread across industries including telecom, pharmaceuticals,

automobiles, software, etc.

• The Transfer Pricing (‘TP’) methodology for the R&D services has been under the scanner

of the Indian tax authorities (‘ITA’).

• The approach of the ITA has not been consistent giving rise to litigation.

22

©2013 Deloitte Haskins & Sells

Global Perspective on compensation for R&D

23

• Developing countries place more emphasis on functions performed in addition to ownership

of intangibles and risks borne

• Developed countries adopt a process which takes into account (in conjunction)

Developer Owner User

• Preferable method:

Cost plus • Contract R&D

Residual profits; or

Royalty

• Funding / Ownership

• Strategy

• Technical capability

• However, OECD, in its discussion draft on Chapter VI, relating to intangibles, has

provided emphasis on substance in the principal company, for the contract R&D structure

with cost plus model.

©2013 Deloitte Haskins & Sells

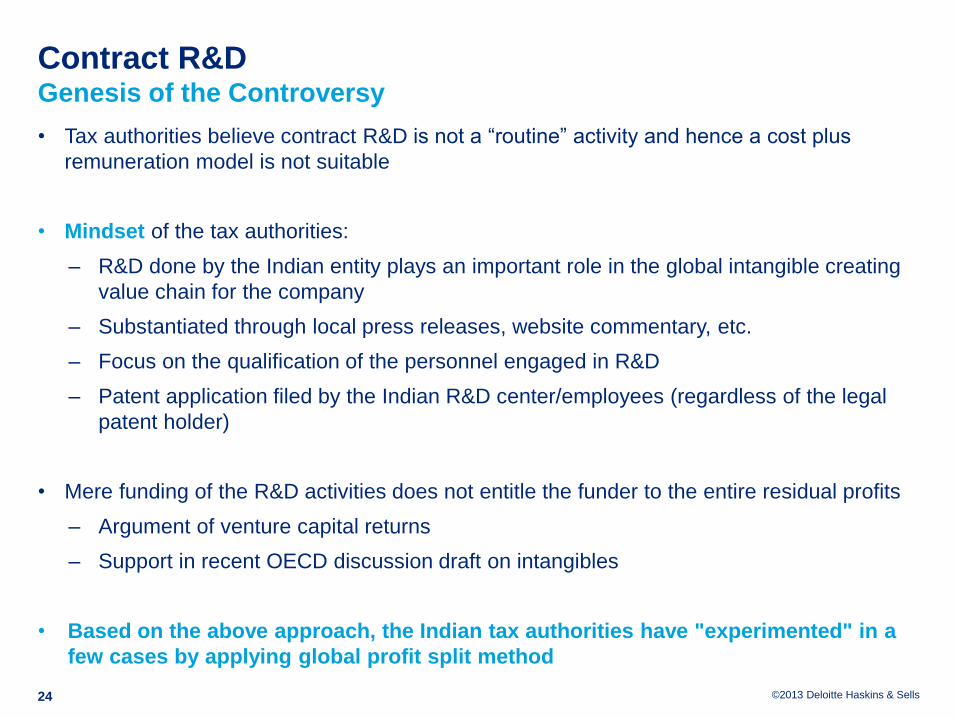

Contract R&D Genesis of the Controversy

• Tax authorities believe contract R&D is not a “routine” activity and hence a cost plus

remuneration model is not suitable

• Mindset of the tax authorities:

– R&D done by the Indian entity plays an important role in the global intangible creating

value chain for the company

– Substantiated through local press releases, website commentary, etc.

– Focus on the qualification of the personnel engaged in R&D

– Patent application filed by the Indian R&D center/employees (regardless of the legal

patent holder)

• Mere funding of the R&D activities does not entitle the funder to the entire residual profits

– Argument of venture capital returns

– Support in recent OECD discussion draft on intangibles

• Based on the above approach, the Indian tax authorities have "experimented" in a

few cases by applying global profit split method

24

©2013 Deloitte Haskins & Sells

Contract R&D Genesis of the Controversy

• India Chapter in the UN practice manual on transfer pricing highlights following views of

the Central Board of Direct Taxes (“CBDT”):

– Risk cannot be controlled remotely by the parent company when Indian subsidiary:

• is engaged in core functions

• core function require important strategic decisions by its Indian employees

• exercises control over operational and other risks

• Rangachary Committee was constituted in September 2012 to look into transfer pricing

issues of R&D centers

• Based on the recommendations from the Rangachary Committee, CBDT issued Circular 2

& 3 / 2013 on March 26, 2013

25

©2013 Deloitte Haskins & Sells

Brief Summary of the Circulars

• Circular No. 2- provides clarification on selection of Profit Split Method (PSM) as the most

appropriate

• Circular No. 3- provides certain conditions which need to be cumulatively satisfied by a

development center in India to demonstrate that it is a contract R&D service provider

assuming insignificant risks

26

©2013 Deloitte Haskins & Sells

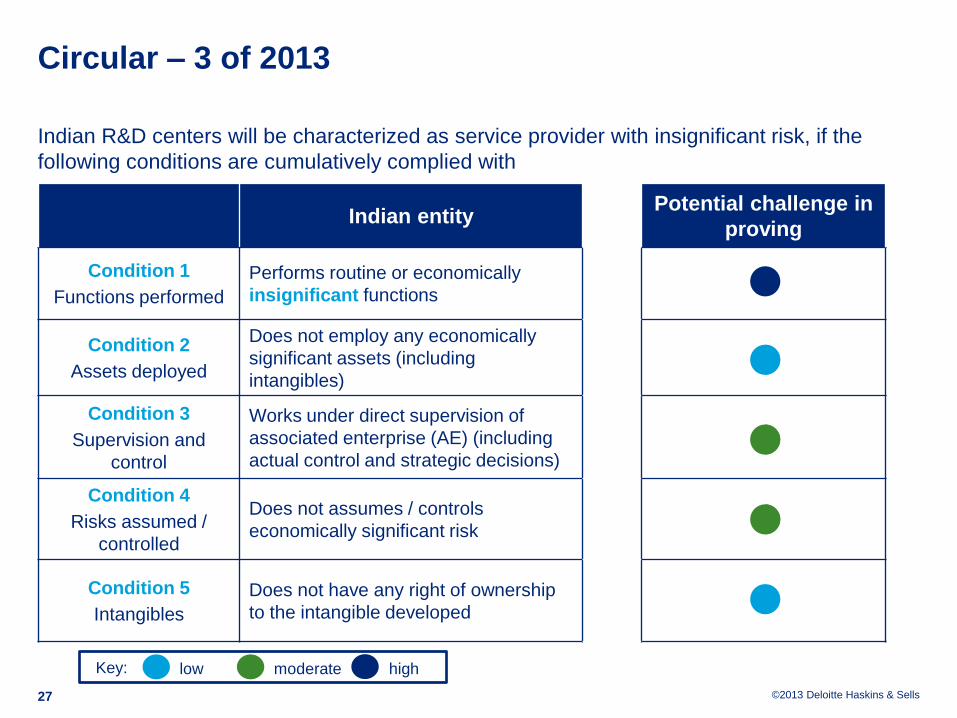

Circular – 3 of 2013

Indian R&D centers will be characterized as service provider with insignificant risk, if the

following conditions are cumulatively complied with

Indian entity Potential challenge in

proving

Condition 1

Functions performed

Performs routine or economically

insignificant functions

Condition 2

Assets deployed

Does not employ any economically

significant assets (including

intangibles)

Condition 3

Supervision and

control

Works under direct supervision of

associated enterprise (AE) (including

actual control and strategic decisions)

Condition 4

Risks assumed /

controlled

Does not assumes / controls

economically significant risk

Condition 5

Intangibles

Does not have any right of ownership

to the intangible developed

high low moderate Key:

27

©2013 Deloitte Haskins & Sells

Circular 2 of 2013

• If transfer pricing officer (TPO) is of the view that profit split method (PSM) cannot be

applied, he must record reasons

• "Due to non-availability of information and reliable data required for application of the

method"

• Discourages use of transactional net margin method (TNMM)

• Since it claims that "there is no correlation between cost incurred on R&D activities and

return on an intangible developed"

• If PSM is not applied by the taxpayer, then taxpayer should have good and sufficient

reason – For non-availability of such information

• TPO may consider TNMM or comparable uncontrolled price (CUP) method by selecting

comparable and make upward adjustment, considering – Transfer of intangible without additional remuneration

– Locational savings / location specific advantage

28

©2013 Deloitte Haskins & Sells

Implications arising from the Circulars

A harmonious reading of the above Circulars shows:

• If the cumulative conditions as prescribed in Circular 3 are not met, then the TPO would

have to necessarily apply PSM

• If for any reason, the TPO is not able to apply PSM, then he is required to

explain/document those reasons

• If TNMM or CUP are applied, then, upward adjustments are required to be made for

factors like location specific advantages and location savings

‒ The circulars do not:

• provide definition /explanation of various terms

• do not clarify situations with reference to examples

• With the reduction in tolerance band flexibility under TNMM has reduced

29

©2013 Deloitte Haskins & Sells

Way forward

The above circulars, though issued with the intent of providing guidance to tax authorities and

taxpayers, have created significant interest as well as concerns amongst MNEs having

Contract R&D Centers.

Taxpayer should carry out transfer pricing review while mapping the functions and

documentation with reference to the conditions stated in the circular, identify key risk areas

and way forward in light of current Indian environment.

Mapping each business process with respect to the functions carried out by Indian entity and its affiliates

Review existing documentation trail maintained by the Indian entity

Identify key risk / focus areas

Set of guiding principles with respect to key risk areas and operational process to mitigate transfer pricing risks

30

©2013 Deloitte Haskins & Sells

Suggested Defense Strategy

Documentation

• Map out the global R&D value chain process

• Document number of employees in India, the decision nodes, regulatory approvals needed

(and where)

• List key people in the R&D process and their location

• Document alternate R&D locations

• Emphasize the importance of other intangibles in the global business

Quantitative rebuttals

• Role of legacy technology/intangibles in Indian R&D operations

• The above to be done to prepare an effective response to the tests/factors laid out in the

Circulars

31

©2013 Deloitte Haskins & Sells

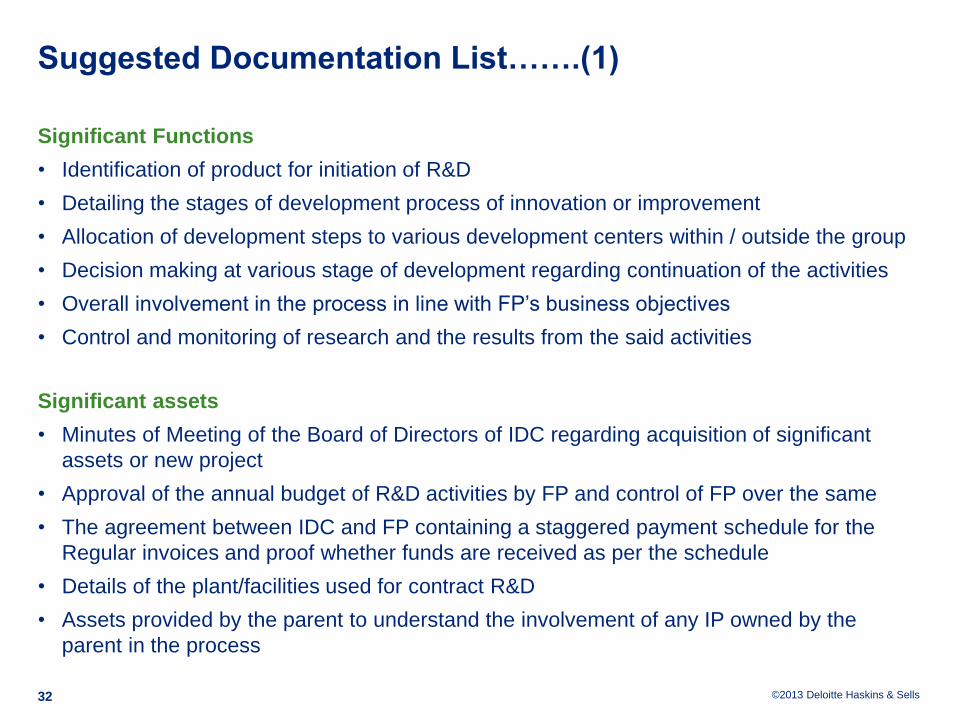

Suggested Documentation List…….(1)

Significant Functions

• Identification of product for initiation of R&D

• Detailing the stages of development process of innovation or improvement

• Allocation of development steps to various development centers within / outside the group

• Decision making at various stage of development regarding continuation of the activities

• Overall involvement in the process in line with FP’s business objectives

• Control and monitoring of research and the results from the said activities

Significant assets

• Minutes of Meeting of the Board of Directors of IDC regarding acquisition of significant

assets or new project

• Approval of the annual budget of R&D activities by FP and control of FP over the same

• The agreement between IDC and FP containing a staggered payment schedule for the

Regular invoices and proof whether funds are received as per the schedule

• Details of the plant/facilities used for contract R&D

• Assets provided by the parent to understand the involvement of any IP owned by the

parent in the process

32

©2013 Deloitte Haskins & Sells

Suggested Documentation …..(2)

Control and Supervision

• Decision to hire (or terminate the contract with) the Indian company

• Decision of the type of research that should be carried out and objectives assigned to it,

• Decision of the budget allocated to the Indian company

• Reporting process followed by the Indian company to enable the parent to assess the

outcome of the research activities.

Significant Risks

• Overall functions / activities of the parent

• Organizational structure of the parent and the Indian company

• Key people functions test, their qualification, experience and expertise

• Timesheet record of the parent’s personnel on outsourced research and other activities

33

©2013 Deloitte Haskins & Sells

Suggested Documentation……….(3)

Ownership of assets

• Words used in the Inter-company agreement – whether the terminology used truly

represent the nature of activities carried out by the Development Center viz. Research vs.

Development

• Ownership details like patent registration, etc. of the IP developed as an outcome of R&D

activities

• Local laws relating to registration of patents

• Entire supply chain of the products developed under contract R&D activities i.e. where the

products will be manufactured and where it will be sold

• Locational savings – whether savings in cost shared between the Indian company and the

parent

34

An update on the Indian APA

scheme

©2013 Deloitte Haskins & Sells

Decision of ITAT - a statistical analysis

Rulings in favour of taxpayers

50%

Rulings in favour of tax authorities

10%

Rulings partly in favour of

taxpayers and partly in favour of

tax authorities 16%

Cases remanded back for fresh adjudication

24%

Total number of rulings analyzed - approx. 340

36

©2013 Deloitte Haskins & Sells

APA Rules in India A New Paradigm

Key Features

• Broadly similar to APA Schemes of other countries

• Agreement between taxpayer and Central Board of Direct Taxes (CBDT)

‒ To determine arm’s length price (ALP)

‒ Specify the manner in which ALP has to be determined

• Can be unilateral, bilateral, or multilateral

• Binding on taxpayer and tax authority

• Use of any method (whether specified or not) with adjustments / variations as necessary

• Application can be filed

‒ Before undertaking a proposed transaction or

‒ For continued transactions before the first day of the relevant fiscal year

(FY 13-14 would be the first year)

• Valid for the maximum period of 5 consecutive years

• Provision for renewal

• No specific provision for “rollback”

37

©2013 Deloitte Haskins & Sells

Overview of the process

Phase 1

• Pre-filing consultation

Phase 2

• Formal filing of APA application

Phase 3

• Phase 3A: Post-filing meeting and negotiations

• Phase 3B:Competent Authority (CA) negotiations (bilateral / multilateral)

Phase 4

• Finalizing and signing an APA

Phase 5

• Annual compliance and monitoring

Renewal of APA: process similar to original APA, no pre-filing required

38

©2013 Deloitte Haskins & Sells

Our Experience with the Indian APA till date

• More than 140 APA applications have been filed

• Maximum in anywhere in the world in the first year

• Most of the applications are unilateral

• Bilateral applications with countries other than US also filed

• Interaction with APA authorities during pre-file meetings have been positive

• Pressure on Indian APA authorities to create a successful program

39

©2013 Deloitte Haskins & Sells

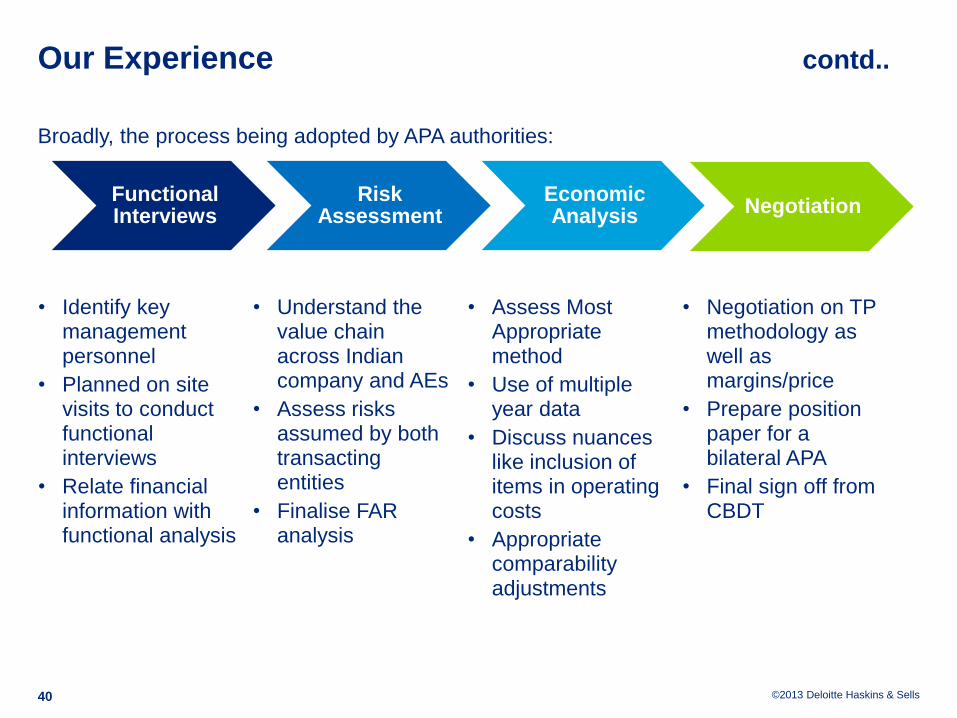

Our Experience contd..

Functional Interviews

• Identify key management personnel

• Planned on site visits to conduct functional interviews

• Relate financial information with functional analysis

Risk Assessment

• Understand the value chain across Indian company and AEs

• Assess risks assumed by both transacting entities

• Finalise FAR analysis

Economic Analysis

• Assess Most Appropriate method

• Use of multiple year data

• Discuss nuances like inclusion of items in operating costs

• Appropriate comparability adjustments

Negotiation

• Negotiation on TP methodology as well as margins/price

• Prepare position paper for a bilateral APA

• Final sign off from CBDT

Broadly, the process being adopted by APA authorities:

40

©2013 Deloitte Haskins & Sells

Suggested Strategy

• Robust Transfer Pricing documentation to be submitted along with the APA application

• Process management strategy

‒ Readiness for intense fact gathering and site visits

‒ Readiness to share information from global AEs

‒ The desired margins/prices to be supported through alternative benchmarking

methodologies

‒ Historical information to be made available

• If any gap in information, may result in delay

Transparency and Comprehensiveness to be the Key

41

Software Industries

Corporate Tax Implications

42

©2013 Deloitte Haskins & Sells

Contents

• Introduction

• Section 10A – Provisions in brief

• Section 10AA – Provisions in brief

• Recent Controversies

• Latest CBDT circular

• Provisions in Direct Tax code

43

©2013 Deloitte Haskins & Sells

Introduction

44

• The Indian Software Industry has been the beneficiary of direct tax incentives under the

provisions like Sec 10A, 10AA & 10B of the Income - tax Act, 1961 (‘Act’) in respect of

their profits derived from the export of computer software.

• These provisions prescribe incentives to “units” or “undertakings”, established under

different schemes, which are/were deriving profits from export of computer software

subject to fulfilling the prescribed conditions.

• Tax incentives have played a vital role in India’s growth story and have also proven to be a

useful tool in the government's move to fuel growth by allowing the creation of special

industrial zones such as software technology parks (STPs), entities such as export-

oriented units (EOUs) and very recently Special Economic Zones (SEZs). Sections 10A,

10AA and 10B of the Act play an important role in the scheme of tax incentives offered.

• SEZ – The scheme was announced in April 2000, and came into force in 2005. The SEZ

scheme is one step ahead of the STP scheme.

• Section 10AA was inserted in the Act in 2006 to provide a tax holiday for units operating

out of an approved Special Economic Zone. The deduction under section 10AA is

available over a period of 15 years.

• According to the latest data, exports from SEZs rose almost 30% to $88 billion in 2012-13,

from $68 billion in the previous year. Exports from SEZs accounted for 29% of total

exports in 2012-13. As of March SEZs had generated approx. 1 million jobs.

Section 10A Provisions in brief

45

©2013 Deloitte Haskins & Sells

Background

46

• The Government of India established various free trade zones and export

processing zones for- – promotion and industrialization of the under developed regions

– rapid growth of industries.

• It was felt that a number of countries have set free trade zones to attract

investment for industrial growth by offering substantial tax concessions including

a complete tax holiday for a specified number of years.

• For encouragement of the establishment of export – oriented industries in the

free trade zone in India, the Finance Act, 1981, inserted a new section 10A in

the Income-tax Act , 1961 (the Act)

• The object of Section 10A was explained by the CBDT circular 308 dated 29th

June 1981 as under: – The section provides for a complete exemption in respect of the profits and gains

derived from an industrial undertaking;

– The government intends to keep out the profits of the export in respect of specified

undertakings from the provisions of the Act.

©2013 Deloitte Haskins & Sells

Section 10A - Special provisions in respect of the newly established

undertakings in free trade zone, etc.

47

Deduction of profits and gains derived from exports of articles or things or computer software.

Period of ten consecutive assessment years from the previous year in which undertaking

begins to manufacture or produce.

Conditions to be fulfilled

• Begun or begins to manufacture or produce articles or things or computer software

• New undertaking - Not formed by the splitting up, or the reconstruction, of a business

already in existence

• Not formed by the transfer to a new business of machinery or plant previously used for any

purpose

Exceptions: – If value of machinery previously used and transferred < 20% of total value of machinery; or

– If machinery used outside India and no depreciation claimed in India.

• Proceeds in convertible foreign exchange received in India within the stipulated time: – within a period of six months from the end of the previous year or, within such further period

– as the competent authority may allow in this behalf

• No deduction shall be allowed to any undertaking for assessment year beginning April 1,

2012 and subsequent years.

Section 10AA Provisions in brief

48

©2013 Deloitte Haskins & Sells

Section 10AA - Special provisions in respect of the newly established

undertakings in Special Economic zone

49

Deduction of profits and gains derived from exports of articles or things or provide any

services.

Period of ten consecutive assessment years from the previous year in which unit begins to

manufacture or produce.

Conditions to be fulfilled

• The assessee being an entrepreneur as defined under section 2(j) of the SEZ Act has to set

up a unit in the SEZ;

• Begun or begins to manufacture or produce articles or things or provide services on or after

the 1st day of April, 2006 in any Special Economic Zone.

• New undertaking - Not formed by the splitting up, or the reconstruction, of a business

already in existence

• Not formed by the transfer to a new business of machinery or plant previously used for any

purpose

Exceptions: – If value of machinery previously used and transferred < 20% of total value of machinery; or

– If machinery used outside India and no depreciation claimed in India.

.

©2013 Deloitte Haskins & Sells

Section 10AA - Special provisions in respect of the newly established

undertakings in Special Economic zone (contd.)

50

• Return of income should be filed in accordance with the provisions of Section 139(1) for

claiming the deduction. – Claim of tax holiday benefit to be made while filing the return of income

• The claims of tax holiday benefit has to be supported by a Chartered Accountant in a

specified form.

– Present e-filing of return does not accommodate any attachment along with the return. Hence, we

understand this should be kept ready and to be filed during the course of assessment.

Computation mechanism

Amount allowable as a deduction:

Export turnover of the unit × Profits and gains derived by the unit

Total turnover of the undertaking

(and not the turnover of the business)

Recent changes and its setback

Minimum Alternate Tax (MAT) – SEZs had got a setback as MAT was imposed on both

developers and units from FY 2011-12 (@ 20.96% for FY 2013-14).

Dividend Distribution Tax (DDT) – DDT was imposed on developers (@ 17% for FY 2013-14).

Recent Controversies

51

©2013 Deloitte Haskins & Sells

Recent Controversies

52

Splitting up and reconstruction

Formation Test

Expenses reduced from export turnover

Realization of export proceeds

Set-off of losses

• i. Set-off of non-STPI loss with STPI Income

• ii. Set-off of brought forward loss of the same undertaking

Deduction not claimed in the return

©2013 Deloitte Haskins & Sells

Recent Controversies (contd.)

53

Conversion of existing DTA unit into STP /SEZ unit

Conversion of a Firm / Branch into a company

Onsite development of computer software

Body Shopping

In a significant setback to business operating in the SEZ , the Karnataka High court

has recently dismissed the Writ petition filed by SEZ Developers and Operators

challenging the constitutional validity to Levy Minimum alternate tax (MAT) and

Dividend Distribution Tax (DDT ), introduced by finance Act 2011 .

High court reiterated a settle position that there is No promissory Estoppel against

a Statute.

©2013 Deloitte Haskins & Sells

Latest CBDT Circular

54

Latest Circular No. 1/2013 [F. No. 178/84/2012-ITA.I], dated 17-1-2013] – Clarification on

issues relating to Export of Computer Software.

Salient Features of the CBDT Circular :-

• ‘On-site’ Development of computer software

• Receipts from Deployment of Technical Manpower (‘DTM’) for ‘On-site’ Software

Development

• Requirement of a separate Master Service Agreement (‘MSA’) for each Statement of Work

(‘SOW’)

• Research &Development (‘R&D’) activities pertaining to software development

• Slump sale of a Unit/ Undertaking

• Separate books of account

• Transfer of a Unit in Special Economic Zone (‘SEZ’) to another SEZ

• New Unit/ Undertaking set up in the same location

The Circular comes as a relief to the Indian Software Industry amid the various

contentious issues regarding the availability of the tax holiday for software units. The

Government could consider adapting similar approach in respect of other litigious

matters and provide a tax payer friendly regime.

Provisions in Direct tax code

55

©2013 Deloitte Haskins & Sells

Direct Tax Code (‘DTC’)

56

• Proposal for Investment based incentive for certain businesses as against profit

based incentive

• Proposal for grandfathering of tax incentives under specified sections of the

Income-tax Act

• Deduction under Section 10A and Section 10B will not be available under the

DTC

• Savings clauses under the DTC provide for the eligible business to be allowed a

deduction u/s: 10AA; 80IA; 80IB and 80IB(9);80IAB; 80IC; 80ID; 80IE; 80JJA;

80JJAA or 80LA

• The DTC provides for charging of MAT on similar lines as in the current Act,

except that the rate of 20% on book profits has been prescribed and MAT credit is

allowed to be carried forward for a period of 15 years. The DTC however does

not clarify the availability of unutilized tax credit that the taxpayer became entitled

to under the current Act.

Questions & Answers

©2013 Deloitte Haskins & Sells

Disclaimer

This publication contains general information only, and none of Deloitte Touche Tohmatsu

Limited, any of its member firms or any of the foregoing’s affiliates (collectively the “Deloitte

Network”) are, by means of this publication, rendering accounting, business, financial,

investment, legal, tax, or other professional advice or services. This publication is not a

substitute for such professional advice or services, nor should it be used as a basis for any

decision or action that may affect your finances or your business. Before making any decision

or taking any action that may affect your finances or your business, you should consult a

qualified professional adviser. No entity in the Deloitte Network shall be responsible for any

loss whatsoever sustained by any person who relies on this publication.

58

©2013 Deloitte Haskins & Sells

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company

limited by guarantee, and its network of member firms, each of which is a legally separate

and independent entity. Please see www.deloitte.com/about for a detailed description of the

legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

59

©2013 Deloitte Haskins & Sells

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member

firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal

structure of Deloitte Touche Tohmatsu Limited and its member firms.

This material and the information contained herein prepared by Deloitte Touche Tohmatsu India Private Limited (DTTIPL) is intended to provide

general information on a particular subject or subjects and is not an exhaustive treatment of such subject(s). None of DTTIPL, Deloitte Touche

Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this material, rendering

professional advice or services. The information is not intended to be relied upon as the sole basis for any decision which may affect you or your

business. Before making any decision or taking any action that might affect your personal finances or business, you should consult a qualified

professional adviser.

No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this material.

© 2013 Deloitte Touche Tohmatsu India Private Limited