Sovereign Wealth Funds and Infrastructure: A Perspective … · Sovereign Wealth Funds and...

31

14 May 2010 – Bogotá Sovereign Wealth Funds and Infrastructure: A Perspective for Latin America Rolando Avendaño Javier Santiso OECD Development Centre Seminar on Infrastructure Financing in Latin America CAF-IFC-OECD

Transcript of Sovereign Wealth Funds and Infrastructure: A Perspective … · Sovereign Wealth Funds and...

14 May 2010 – Bogotá

Sovereign Wealth Funds and Infrastructure: A Perspective for Latin

America

Rolando AvendañoJavier Santiso

OECD Development Centre

Seminar on Infrastructure Financing in Latin AmericaCAF-IFC-OECD

Latin America’s Infrastructure needs in the long run 1

Sovereign Wealth Funds: New Investment Drivers2

Looking and Emerging Economies: Infrastructure and Commodities3

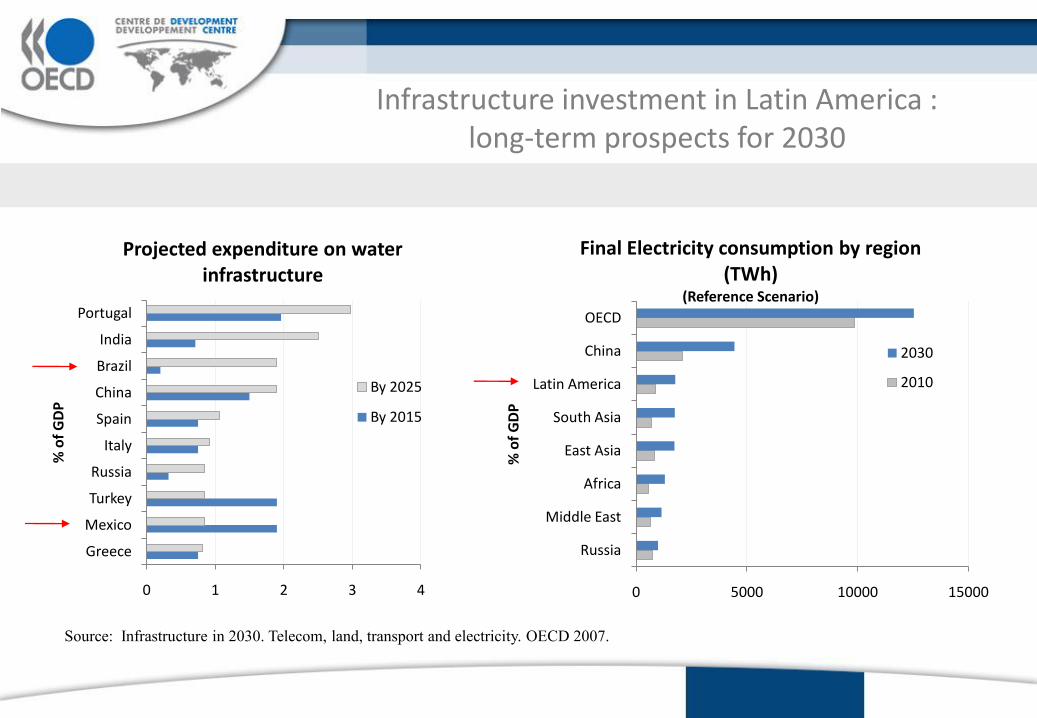

Infrastructure investment in Latin America : long-term prospects for 2030

0 1 2 3 4

Greece

Mexico

Turkey

Russia

Italy

Spain

China

Brazil

India

Portugal

% o

f G

DP

Projected expenditure on water infrastructure

By 2025

By 2015

0 5000 10000 15000

Russia

Middle East

Africa

East Asia

South Asia

Latin America

China

OECD

% o

f G

DP

Final Electricity consumption by region (TWh)

(Reference Scenario)

2030

2010

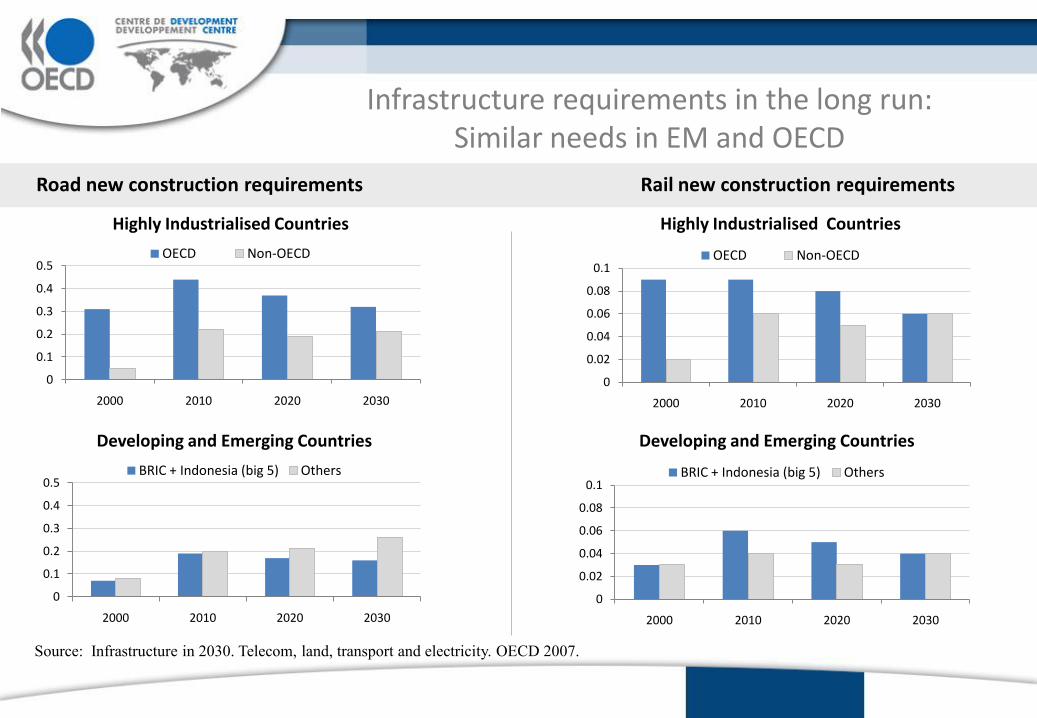

Source: Infrastructure in 2030. Telecom, land, transport and electricity. OECD 2007.

Infrastructure requirements in the long run:Similar needs in EM and OECD

0

0.1

0.2

0.3

0.4

0.5

2000 2010 2020 2030

Highly Industrialised Countries

OECD Non-OECD

0

0.1

0.2

0.3

0.4

0.5

2000 2010 2020 2030

Developing and Emerging Countries

BRIC + Indonesia (big 5) Others

0

0.02

0.04

0.06

0.08

0.1

2000 2010 2020 2030

Highly Industrialised Countries

OECD Non-OECD

0

0.02

0.04

0.06

0.08

0.1

2000 2010 2020 2030

Developing and Emerging Countries

BRIC + Indonesia (big 5) Others

Road new construction requirements Rail new construction requirements

Source: Infrastructure in 2030. Telecom, land, transport and electricity. OECD 2007.

Latin America’s Infrastructure needs in the long run 1

Sovereign Wealth Funds: New Investment Drivers2

Looking and Emerging Economies: Infrastructure and Commodities3

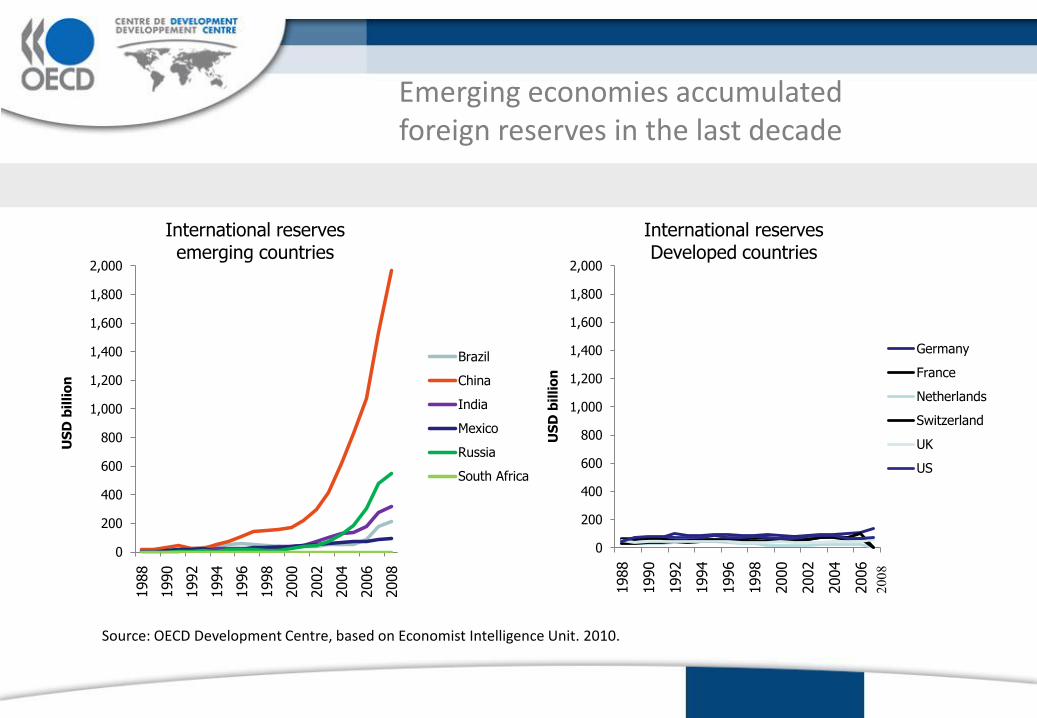

Emerging economies accumulated foreign reserves in the last decade

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

US

D b

illi

on

International reserves emerging countries

Brazil

China

India

Mexico

Russia

South Africa

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

US

D b

illi

on

International reservesDeveloped countries

Germany

France

Netherlands

Switzerland

UK

US

Source: OECD Development Centre, based on Economist Intelligence Unit. 2010.

2008

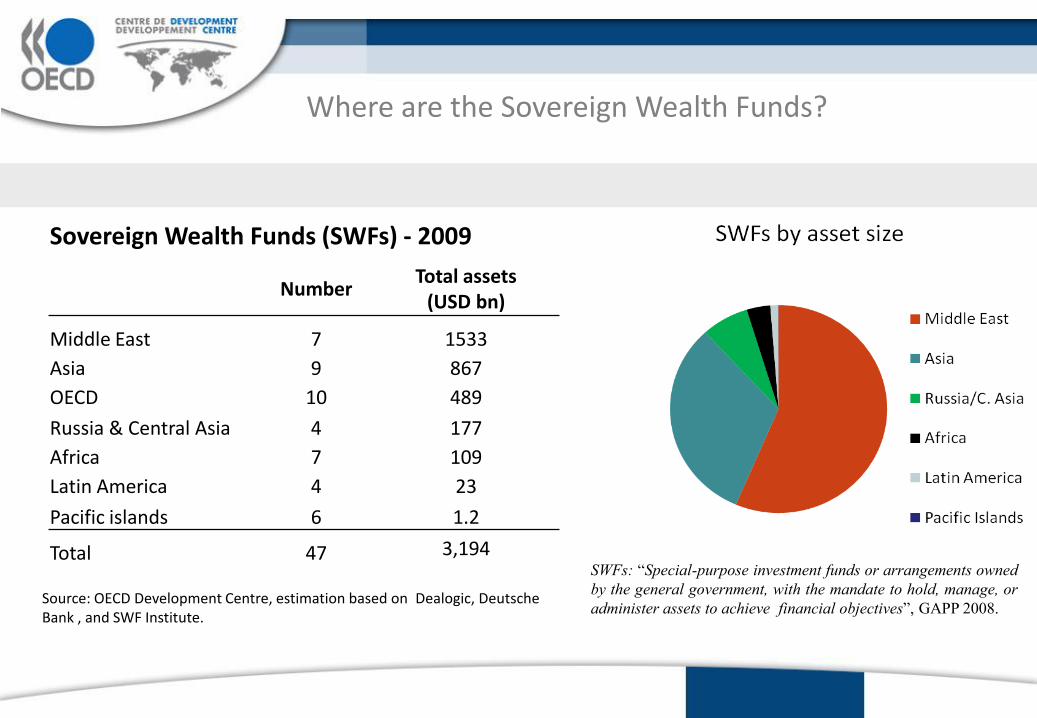

Where are the Sovereign Wealth Funds?

Sovereign Wealth Funds (SWFs) - 2009

NumberTotal assets

(USD bn)

Middle East 7 1533

Asia 9 867

OECD 10 489

Russia & Central Asia 4 177

Africa 7 109

Latin America 4 23

Pacific islands 6 1.2

Total 47 3,194

Source: OECD Development Centre, estimation based on Dealogic, Deutsche Bank , and SWF Institute.

SWFs: “Special-purpose investment funds or arrangements owned

by the general government, with the mandate to hold, manage, or

administer assets to achieve financial objectives”, GAPP 2008.

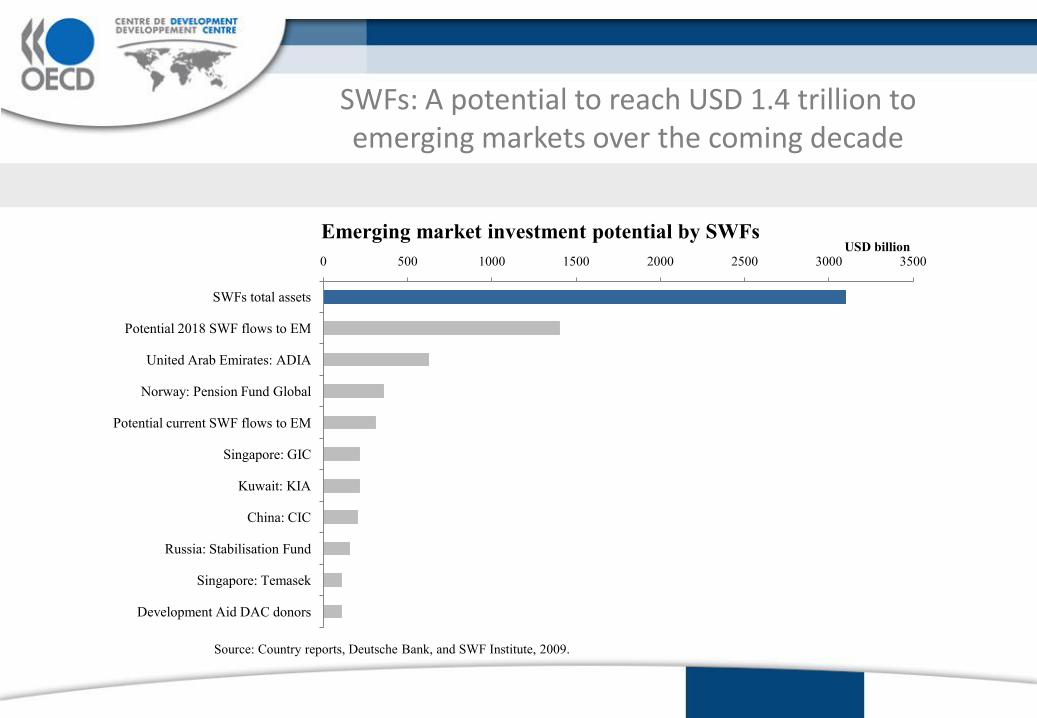

0 500 1000 1500 2000 2500 3000 3500

SWFs total assets

Potential 2018 SWF flows to EM

United Arab Emirates: ADIA

Norway: Pension Fund Global

Potential current SWF flows to EM

Singapore: GIC

Kuwait: KIA

China: CIC

Russia: Stabilisation Fund

Singapore: Temasek

Development Aid DAC donors

USD billionEmerging market investment potential by SWFs

Source: Country reports, Deutsche Bank, and SWF Institute, 2009.

SWFs: A potential to reach USD 1.4 trillion to emerging markets over the coming decade

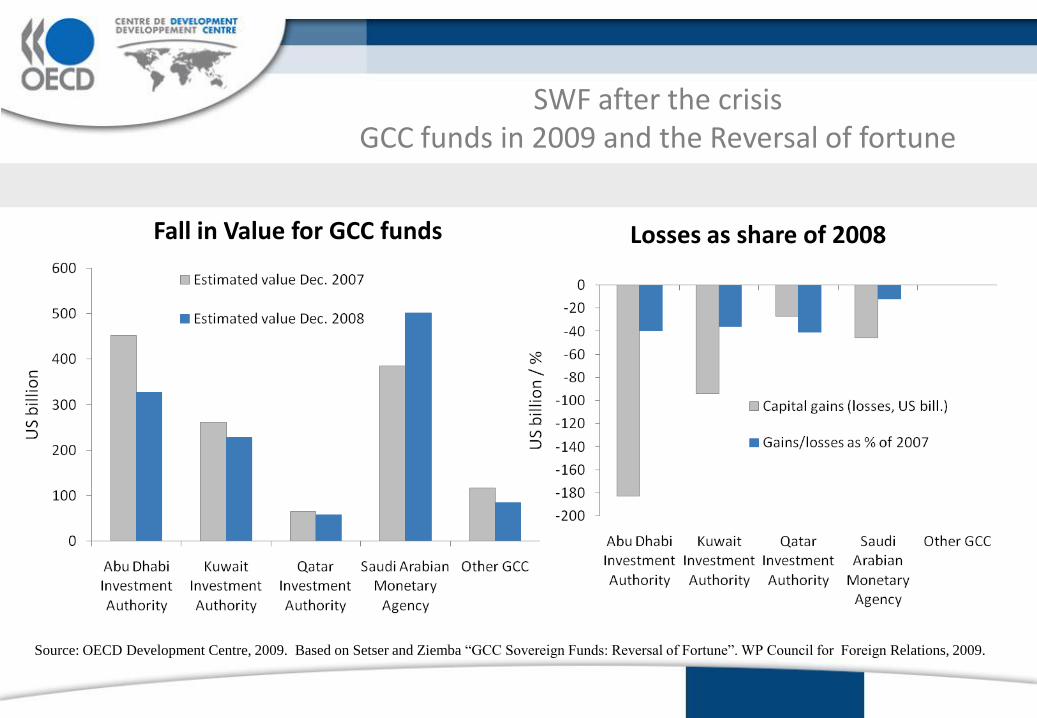

SWF after the crisis GCC funds in 2009 and the Reversal of fortune

Source: OECD Development Centre, 2009. Based on Setser and Ziemba “GCC Sovereign Funds: Reversal of Fortune”. WP Council for Foreign Relations, 2009.

Losses as share of 2008Fall in Value for GCC funds

-60

-50

-40

-30

-20

-10

0

Blackstone Bear StearsMorgan Stanley

Pe

rfo

rman

ce (

%)

China

-60

-50

-40

-30

-20

-10

0

10

AMD Citi Carlyle

Pe

rfo

rman

ce (

%)

Abu Dhabi

-60

-50

-40

-30

-20

-10

0

Blackstone Bear StearsMorgan Stanley

Pe

rfo

rman

ce (

%)

Dubai

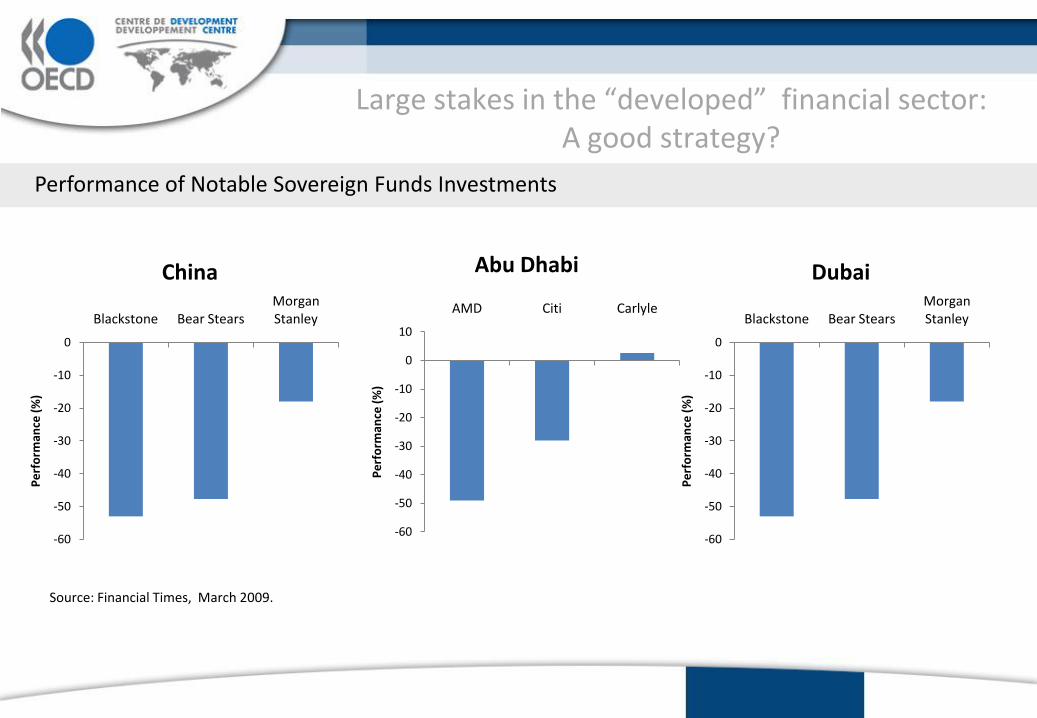

Source: Financial Times, March 2009.

Performance of Notable Sovereign Funds Investments

Large stakes in the “developed” financial sector: A good strategy?

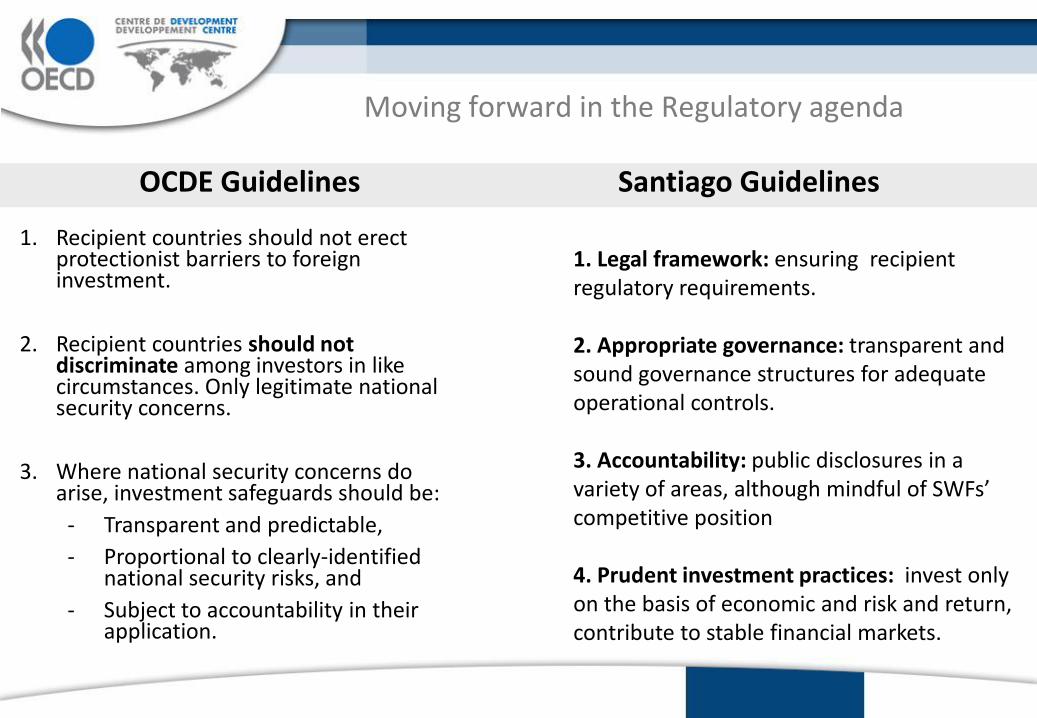

Moving forward in the Regulatory agenda

1. Legal framework: ensuring recipient regulatory requirements.

2. Appropriate governance: transparent and sound governance structures for adequateoperational controls.

3. Accountability: public disclosures in a variety of areas, although mindful of SWFs’ competitive position

4. Prudent investment practices: invest only on the basis of economic and risk and return, contribute to stable financial markets.

Santiago Guidelines

1. Recipient countries should not erect protectionist barriers to foreign investment.

2. Recipient countries should not discriminate among investors in like circumstances. Only legitimate national security concerns.

3. Where national security concerns do arise, investment safeguards should be:

- Transparent and predictable,

- Proportional to clearly-identified national security risks, and

- Subject to accountability in their application.

OCDE Guidelines

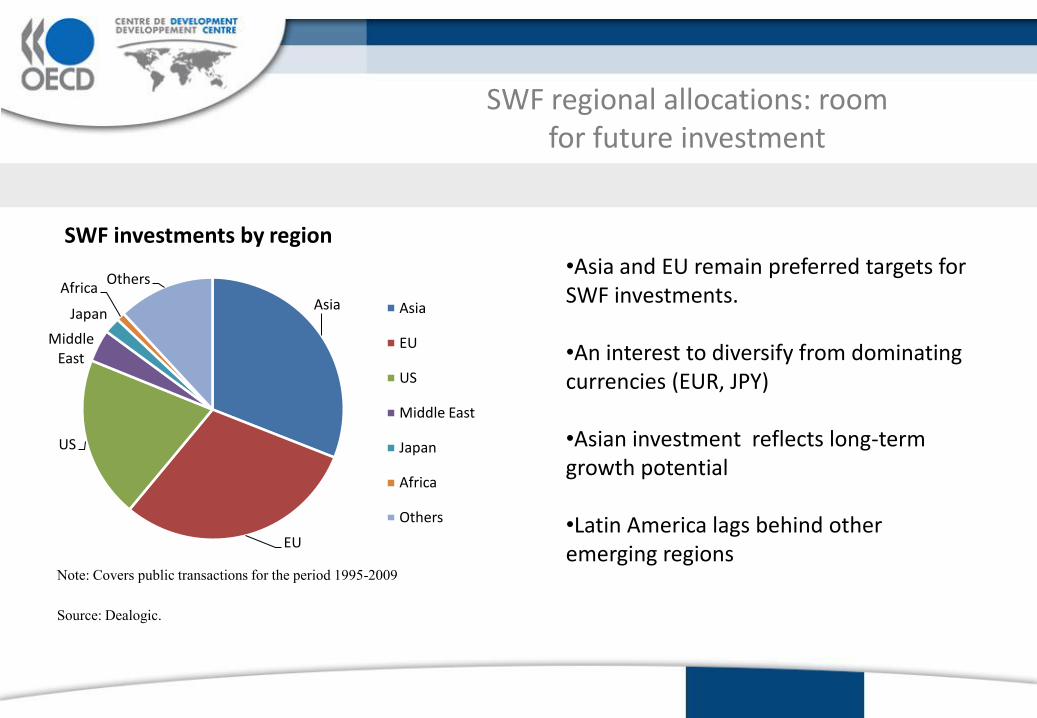

SWF regional allocations: room for future investment

Asia

EU

US

Middle East

Japan

AfricaOthers

Asia

EU

US

Middle East

Japan

Africa

Others

•Asia and EU remain preferred targets for SWF investments.

•An interest to diversify from dominating currencies (EUR, JPY)

•Asian investment reflects long-term growth potential

•Latin America lags behind other emerging regions

Note: Covers public transactions for the period 1995-2009

Source: Dealogic.

SWF investments by region

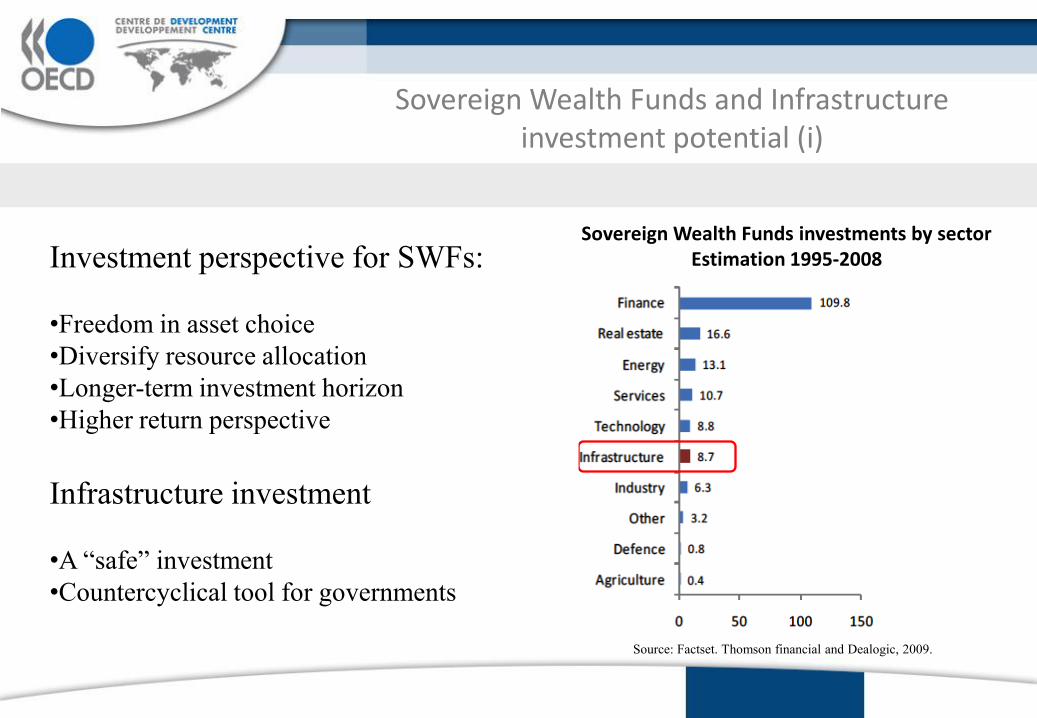

Sovereign Wealth Funds and Infrastructure investment potential (i)

Investment perspective for SWFs:

•Freedom in asset choice

•Diversify resource allocation

•Longer-term investment horizon

•Higher return perspective

Infrastructure investment

•A “safe” investment

•Countercyclical tool for governments

Source: Factset. Thomson financial and Dealogic, 2009.

Sovereign Wealth Funds investments by sectorEstimation 1995-2008

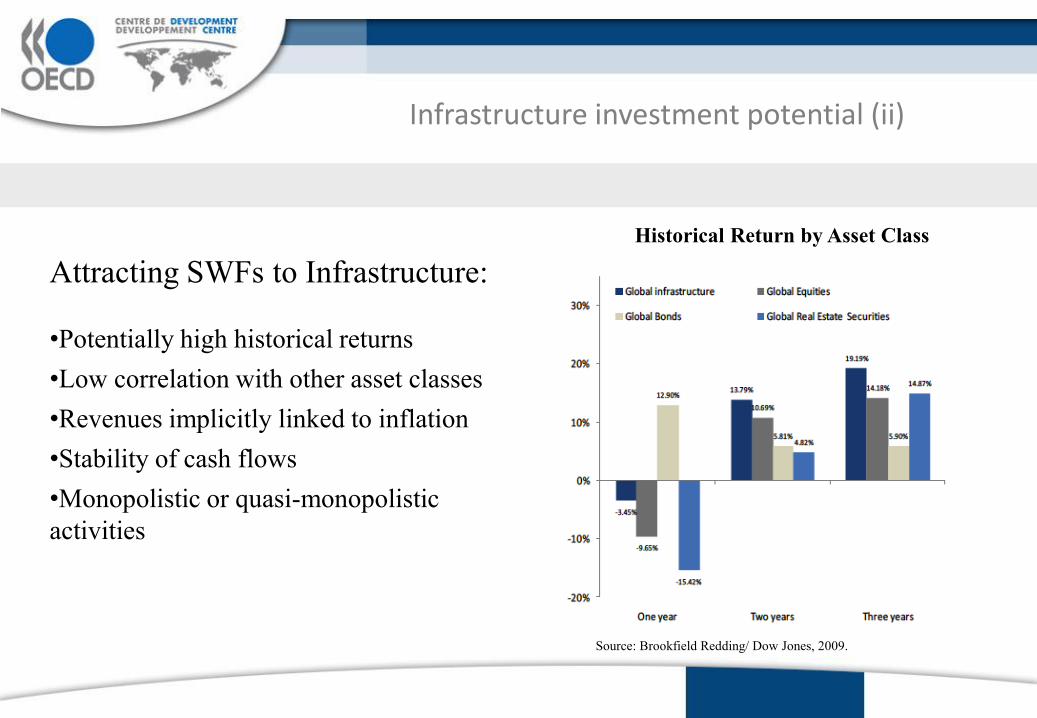

Infrastructure investment potential (ii)

Attracting SWFs to Infrastructure:

•Potentially high historical returns

•Low correlation with other asset classes

•Revenues implicitly linked to inflation

•Stability of cash flows

•Monopolistic or quasi-monopolistic

activities

Source: Brookfield Redding/ Dow Jones, 2009.

Historical Return by Asset Class

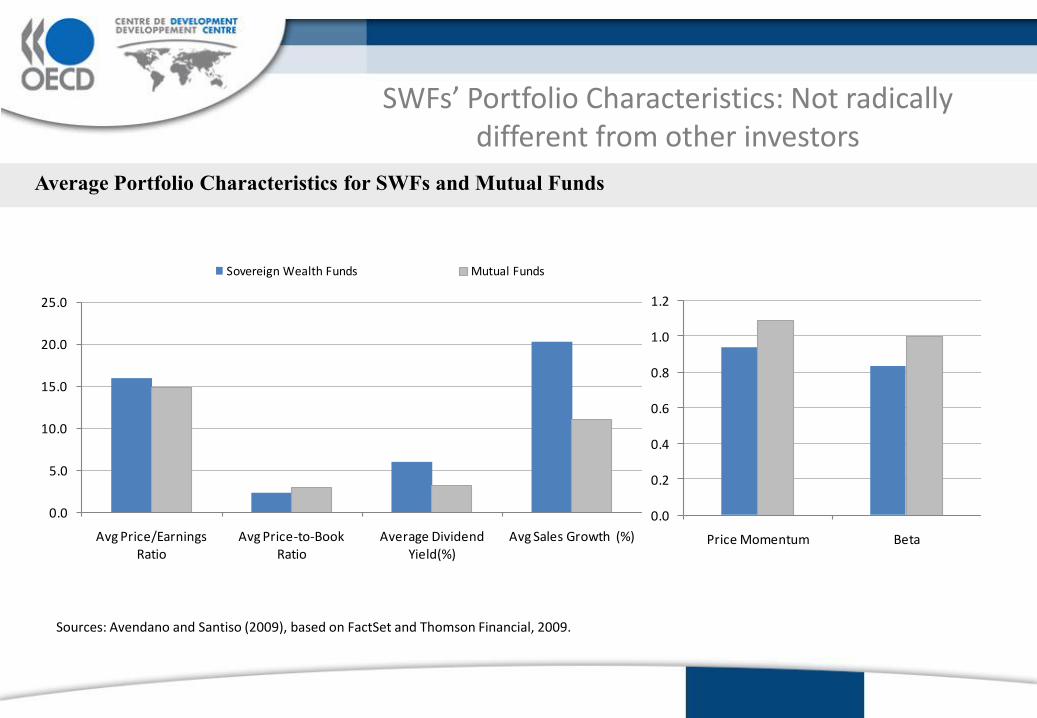

Looking at the data: SWFs and other Institutional investors

• Using data on equity holdings for a set of SWFs, we compare their investments to private mutual funds (index and actively managed).

• Source: FactSet and Thomson Financial on portfolio holdings of institutional and private funds. Mandatory filings with national regulatory agencies (e.g. 13 filings with SEC, share register with UK), annual reports and primary sources.

• SWFs: 22 funds – 14.000 holdings

• Mutual funds: 25 largest US funds – 11.600 holdings

• Period studied: 2006-2009

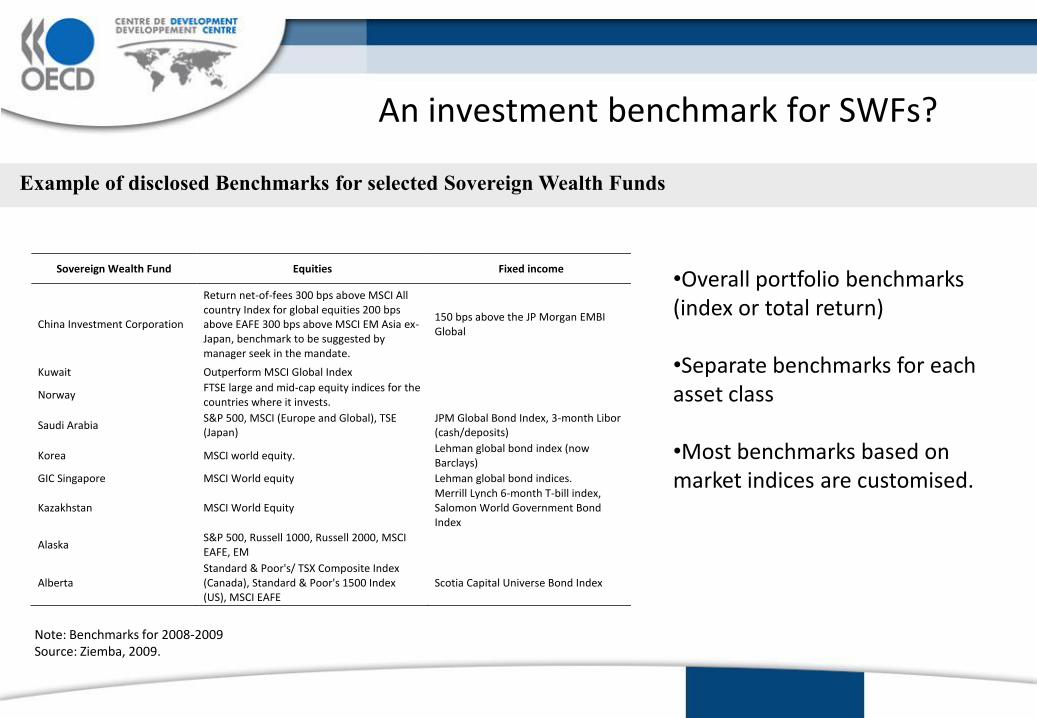

Sovereign Wealth Fund Equities Fixed income

China Investment Corporation

Return net-of-fees 300 bps above MSCI All country Index for global equities 200 bps above EAFE 300 bps above MSCI EM Asia ex-Japan, benchmark to be suggested by manager seek in the mandate.

150 bps above the JP Morgan EMBI Global

Kuwait Outperform MSCI Global Index

Norway FTSE large and mid-cap equity indices for the countries where it invests.

Saudi Arabia S&P 500, MSCI (Europe and Global), TSE (Japan)

JPM Global Bond Index, 3-month Libor (cash/deposits)

Korea MSCI world equity. Lehman global bond index (now Barclays)

GIC Singapore MSCI World equity Lehman global bond indices.

Kazakhstan MSCI World Equity Merrill Lynch 6-month T-bill index, Salomon World Government Bond Index

Alaska S&P 500, Russell 1000, Russell 2000, MSCI EAFE, EM

Alberta Standard & Poor's/ TSX Composite Index (Canada), Standard & Poor's 1500 Index (US), MSCI EAFE

Scotia Capital Universe Bond Index

Example of disclosed Benchmarks for selected Sovereign Wealth Funds

Note: Benchmarks for 2008-2009Source: Ziemba, 2009.

An investment benchmark for SWFs?

•Overall portfolio benchmarks (index or total return)

•Separate benchmarks for each asset class

•Most benchmarks based on market indices are customised.

Average Portfolio Characteristics for SWFs and Mutual Funds

Sources: Avendano and Santiso (2009), based on FactSet and Thomson Financial, 2009.

0.0

5.0

10.0

15.0

20.0

25.0

Avg Price/Earnings Ratio

Avg Price-to-Book Ratio

Average Dividend Yield(%)

Avg Sales Growth (%)

Sovereign Wealth Funds Mutual Funds

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Price Momentum Beta

SWFs’ Portfolio Characteristics: Not radically different from other investors

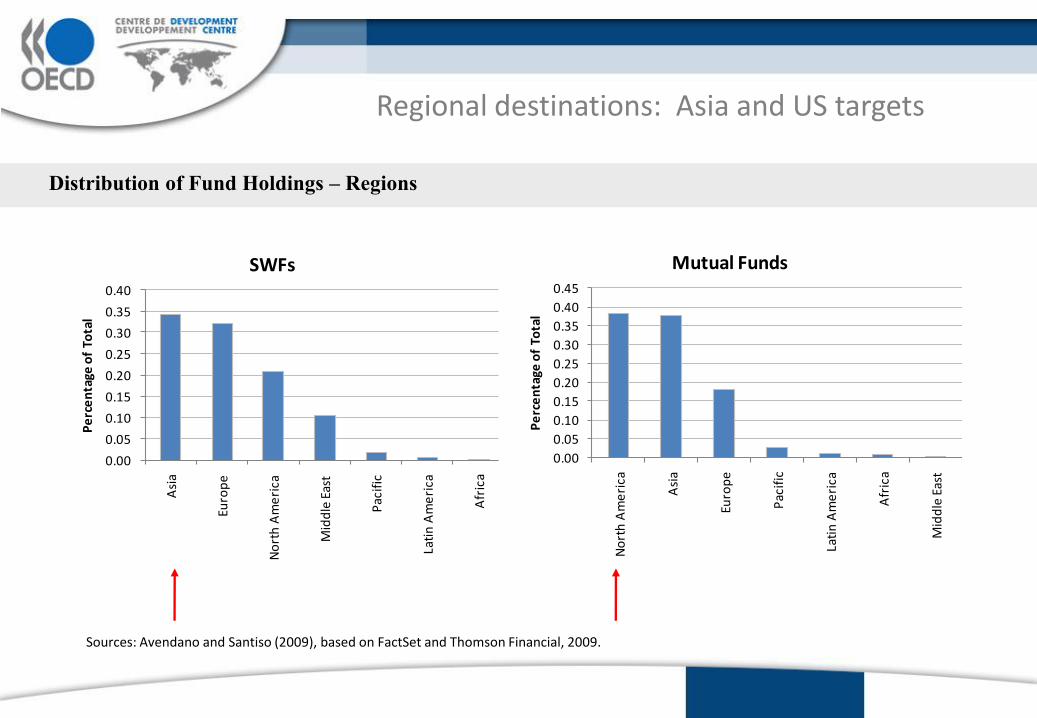

Distribution of Fund Holdings – Regions

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Asi

a

Euro

pe

No

rth

Am

eri

ca

Mid

dle

Eas

t

Pac

ific

Lati

n A

me

rica

Afr

ica

Pe

rce

nta

ge o

f To

tal

SWFs

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

No

rth

Am

eri

ca

Asi

a

Euro

pe

Pac

ific

Lati

n A

me

rica

Afr

ica

Mid

dle

Eas

t

Pe

rce

nta

ge o

f To

tal

Mutual Funds

Regional destinations: Asia and US targets

Sources: Avendano and Santiso (2009), based on FactSet and Thomson Financial, 2009.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Fin

ance

Co

mm

un

icat

ion

s

Tran

spo

rtat

ion

Ene

rgy

Min

era

ls

Co

nsu

me

r D

ura

ble

s

Co

nsu

me

r N

on

-Du

rab

les

Uti

litie

s

He

alth

Te

chn

olo

gy

Ele

ctro

nic

Te

chn

olo

gy

Ind

ust

rial

Se

rvic

es

No

n-E

ne

rgy

Min

era

ls

Pro

du

cer

Man

ufa

ctu

rin

g

SWFs

0.000.050.100.150.200.250.300.350.40

Fin

ance

Ind

ust

rial

Se

rvic

es

He

alth

Te

chn

olo

gy

Ene

rgy

Min

era

ls

Co

nsu

me

r N

on

-Du

rab

les

Re

tail

Trad

e

Uti

litie

s

Co

nsu

me

r Se

rvic

es

Co

nsu

me

r D

ura

ble

s

Tech

no

logy

Se

rvic

es

Pro

du

cer

Man

ufa

ctu

rin

g

Co

mm

un

icat

ion

s

Mutual Funds

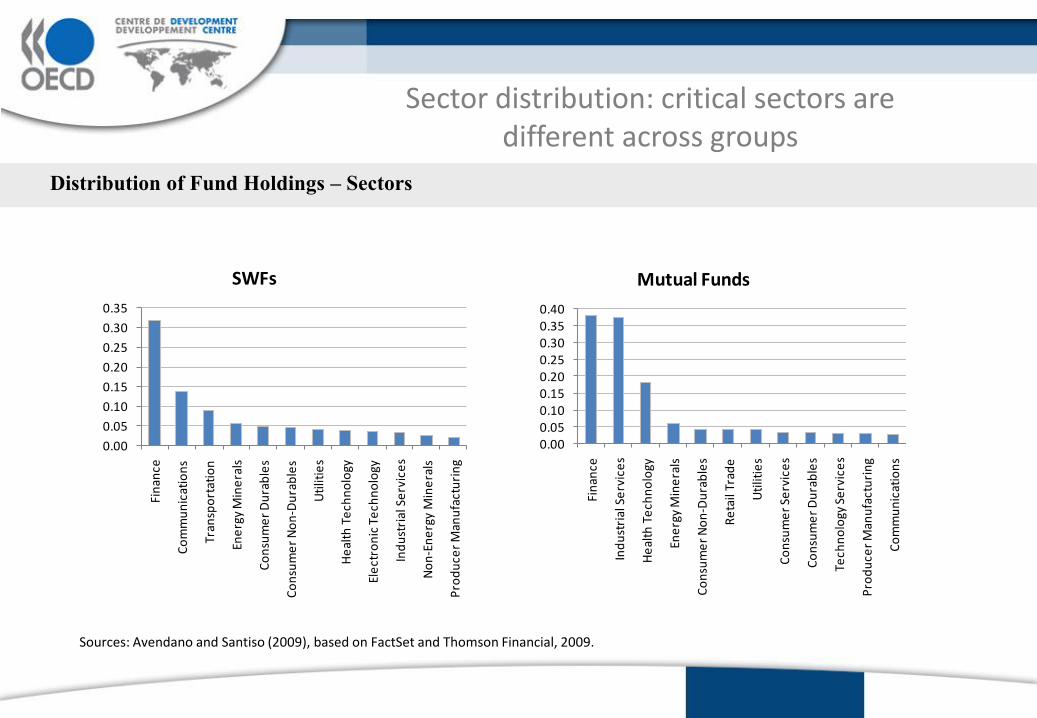

Distribution of Fund Holdings – Sectors

Sector distribution: critical sectors aredifferent across groups

Sources: Avendano and Santiso (2009), based on FactSet and Thomson Financial, 2009.

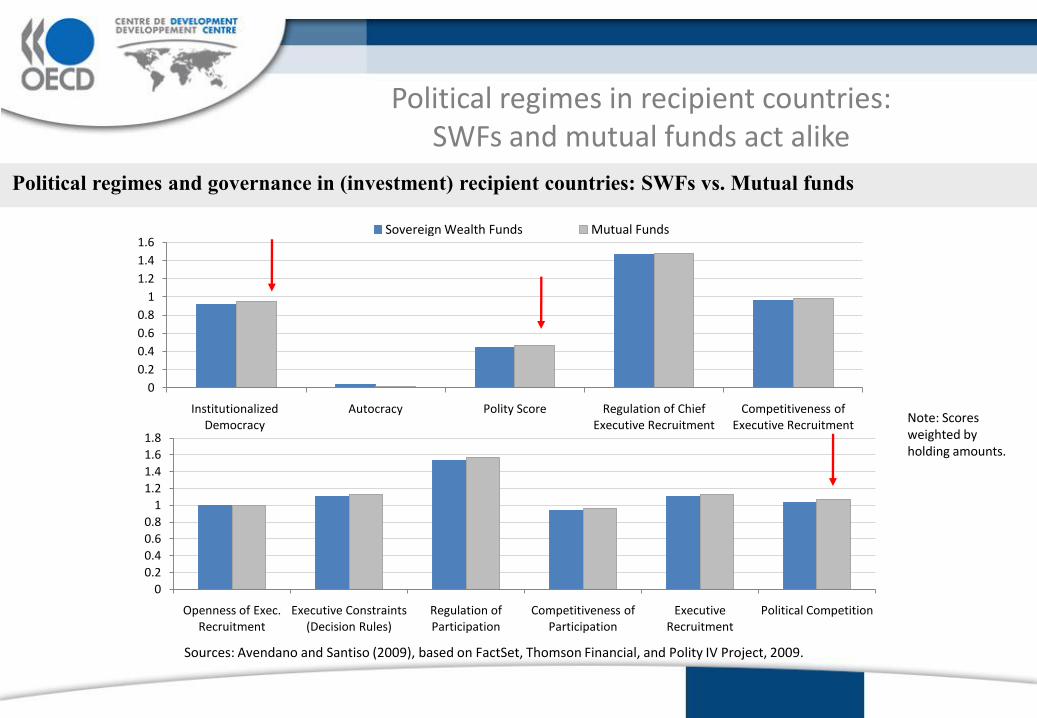

Political regimes in recipient countries:SWFs and mutual funds act alike

Sources: Avendano and Santiso (2009), based on FactSet, Thomson Financial, and Polity IV Project, 2009.

Political regimes and governance in (investment) recipient countries: SWFs vs. Mutual funds

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Institutionalized Democracy

Autocracy Polity Score Regulation of Chief Executive Recruitment

Competitiveness of Executive Recruitment

Sovereign Wealth Funds Mutual Funds

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Openness of Exec. Recruitment

Executive Constraints (Decision Rules)

Regulation of Participation

Competitiveness of Participation

Executive Recruitment

Political Competition

Note: Scores weighted by holding amounts.

Latin America’s Infrastructure needs in the long run 1

Sovereign Wealth Funds: New Investment Drivers2

Looking and Emerging Economies: Infrastructure and Commodities3

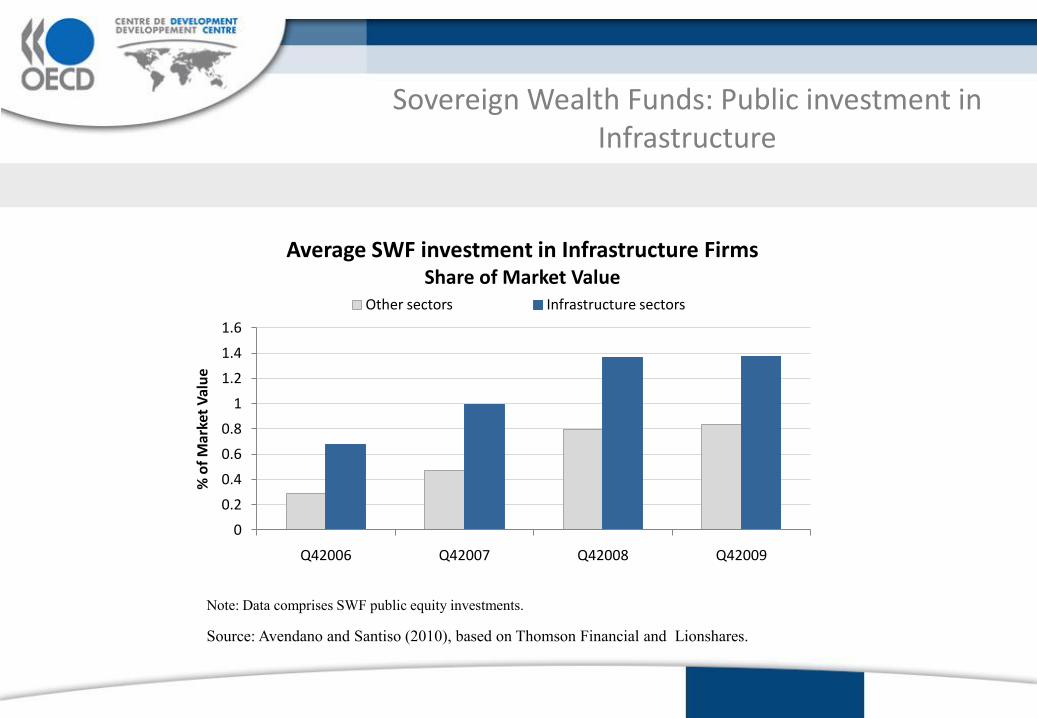

Sovereign Wealth Funds: Public investment in Infrastructure

Source: Avendano and Santiso (2010), based on Thomson Financial and Lionshares.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Q42006 Q42007 Q42008 Q42009

% o

f M

arke

t V

alu

e

Average SWF investment in Infrastructure FirmsShare of Market Value

Other sectors Infrastructure sectors

Note: Data comprises SWF public equity investments.

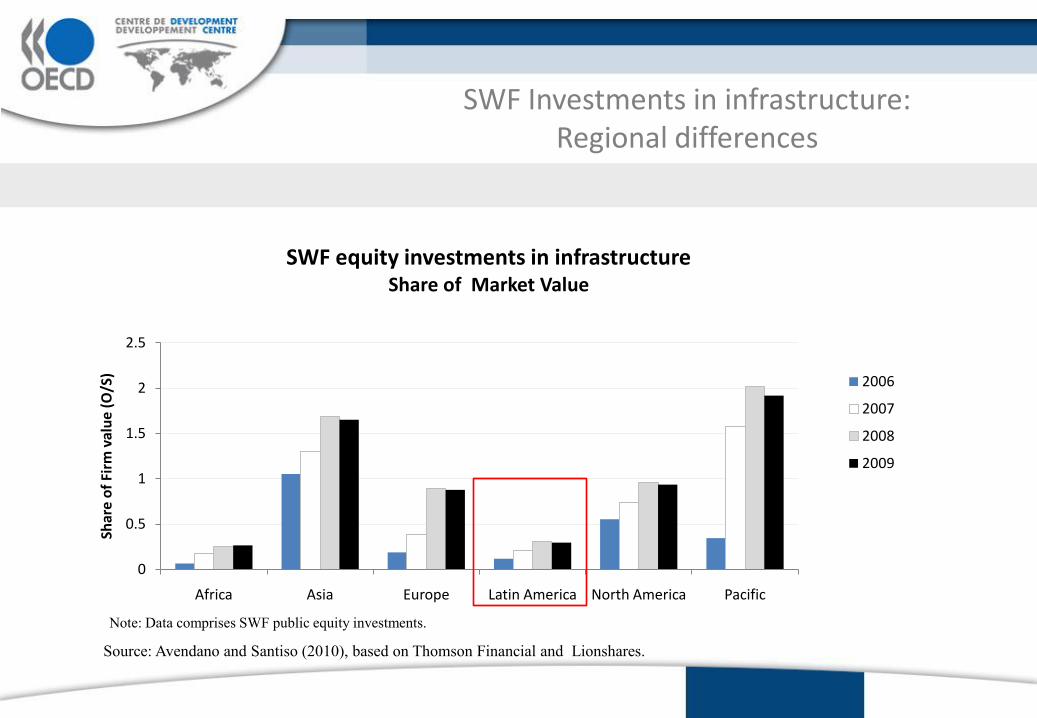

SWF Investments in infrastructure:Regional differences

0

0.5

1

1.5

2

2.5

Africa Asia Europe Latin America North America Pacific

Shar

e o

f Fi

rm v

alu

e (O

/S)

SWF equity investments in infrastructure Share of Market Value

2006

2007

2008

2009

Source: Avendano and Santiso (2010), based on Thomson Financial and Lionshares.

Note: Data comprises SWF public equity investments.

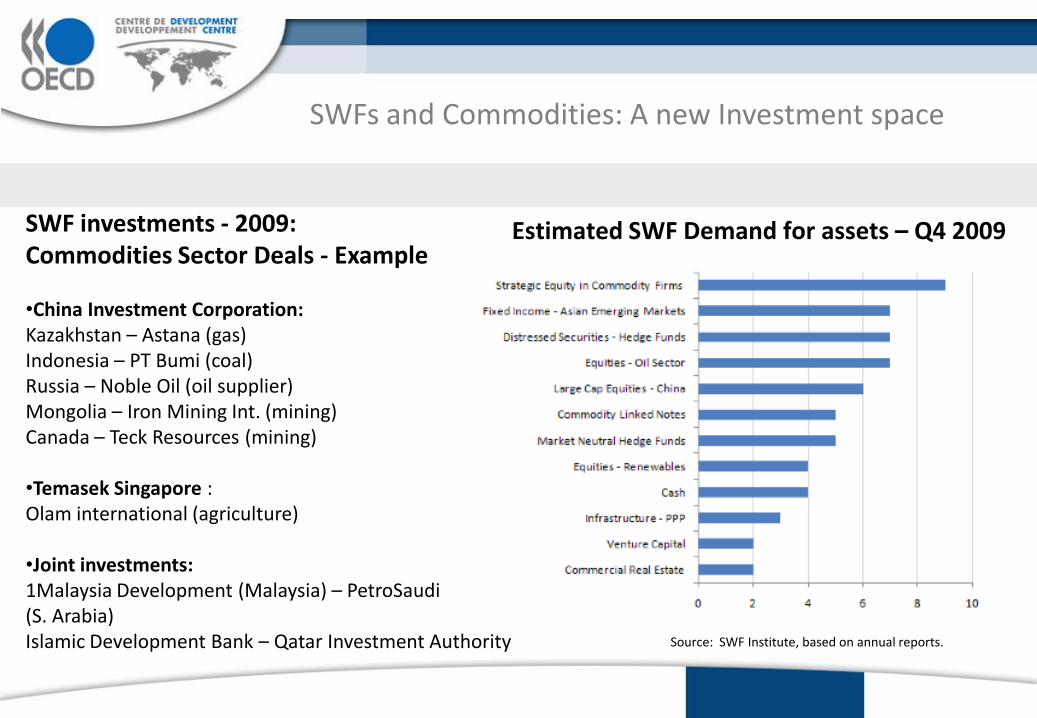

Estimated SWF Demand for assets – Q4 2009

Source: SWF Institute, based on annual reports.

SWFs and Commodities: A new Investment space

SWF investments - 2009:Commodities Sector Deals - Example

•China Investment Corporation:Kazakhstan – Astana (gas)Indonesia – PT Bumi (coal)Russia – Noble Oil (oil supplier)Mongolia – Iron Mining Int. (mining)Canada – Teck Resources (mining)

•Temasek Singapore :Olam international (agriculture)

•Joint investments:1Malaysia Development (Malaysia) – PetroSaudi(S. Arabia)Islamic Development Bank – Qatar Investment Authority

SWFs in Latin America: Brazil is dominant in Infrastructure sectors

Sector Firm Country % O/S Sector Firm Country % O/S

Brasil Telecom Participacoes Sa Ord Brazil 0.387

Brasil Telecom Sa Ord Brazil 0.083 Mercadolibre Inc Com Argentina 0.773

Communications Gvt Holding Sa Ord Brazil 0.021 Totvs Sa Ord Brazil 0.399

Tele Norte Leste Part Ord Brazil 1.006 Empresas La Polar Sa Ord Chile 1.073

Telemar Norte Leste Sa Ord Brazil 0.153 All America Latina Log Ord Brazil 0.03

Transportation Cia De Concessoes Rodoviarias Ord Brazil 0.356

Electronic Technology Embraer (Emp Brasil Aero) Ord Brazil 0.021 Gol Linhas Aereas Intel Pfd Brazil 0.193

Llx Logistica Sa Ord Brazil 0.083

Energy Minerals Petrobras Energia Sa Adr B Argentina 0 Santos Brasil Part Sa Unit 4Pfd/Ord Brazil 0

Ultrapar Participacoes Sa Pfd Brazil 0 Cia Sudamericana De Vapores Ord Chile 0.153

Lan Airlines Sa Ord Chile 0.215

Cia Siderurgica Nacional (Csn) Ord Brazil 0.33

Confab Industrial Sa Pfd Brazil 0 Aes Tiete Sa Ord Brazil 0.588

Metalurgica Gerdau Sa Ord Brazil 0.994 Cia Paranaense Ener/Copel Ord Pfd BBrazil 0

Mmx Mineracao E Metalicos Ord Brazil 0.197 Cia Saneamento Minas Gerais Ord Brazil 0.235

Non-Energy Minerals Usiminas (Minas Gerais) Pfd A Brazil 0 Cia Transmissao Energia Paulista Pfd Brazil 0

Vale Sa Adr Brazil 0 Cpfl Energia Sa Ord Brazil 0.004

Cia Acero Del Pacifico (Cap Sa) Ord Chile 0.404 Eletrobras Ord Pfd B Brazil 0

Cia De Minas Buenaventura Ord Peru 0.321 Eletropaulo Metropolitana Ord Brazil 0

Sociedad Minera Cerro Verde Ord Peru 0.017 Utilities Energetica Sao Paulo (Cesp) Ord Brazil 1.262

Southern Copper Corp Com Peru 0.124 Energias Do Brasil Sa Ord Brazil 0.17

Volcan Compania Minera Sa Ord A Peru 0.063 Light Sa Ord Brazil 0.276

Mpx Energia Sa Ord Brazil 0.118

Sabesp (Saneamento Basico) Ord Brazil 0.795

Tractebel Energia Sa Ord Brazil 0.261

Transmissora Alianca (Terna) Ord Brazil 0

Colbun Sa Ord Chile 0.233

Endesa (Empresa Nac Elec) Ord Chile 0.258

Enersis Sa Ord Chile 0.245

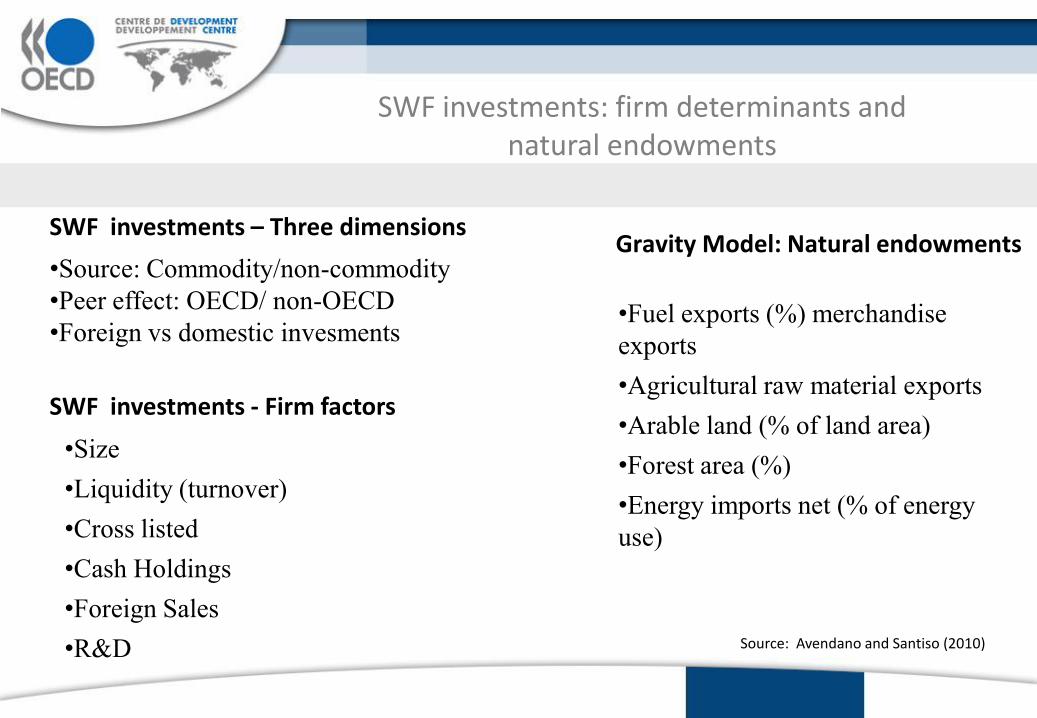

Gravity Model: Natural endowments

Source: Avendano and Santiso (2010)

SWF investments: firm determinants and natural endowments

SWF investments - Firm factors

•Fuel exports (%) merchandise

exports

•Agricultural raw material exports

•Arable land (% of land area)

•Forest area (%)

•Energy imports net (% of energy

use)

SWF investments – Three dimensions

•Size

•Liquidity (turnover)

•Cross listed

•Cash Holdings

•Foreign Sales

•R&D

•Source: Commodity/non-commodity

•Peer effect: OECD/ non-OECD

•Foreign vs domestic invesments

SWF investments: firm determinants and natural endowments

•Non-commodity funds favour firms with more foreign activity and higher

turnover, in contrast to commodity-funds.

•OECD-based funds privilege firms with lower leverage levels, whereas non-

OECD funds have a preference for profitable (i.e. high ROE) and international

(i.e. high foreign sales) firms.

•SWF foreign investments are oriented towards large and highly leveraged firms,

in contrast with their domestic (and low leveraged) investments.

•Specific sectors, such as R&D, tend to attract foreign investments.

•Natural endowments explain large shifts towards commodity-related sectors.

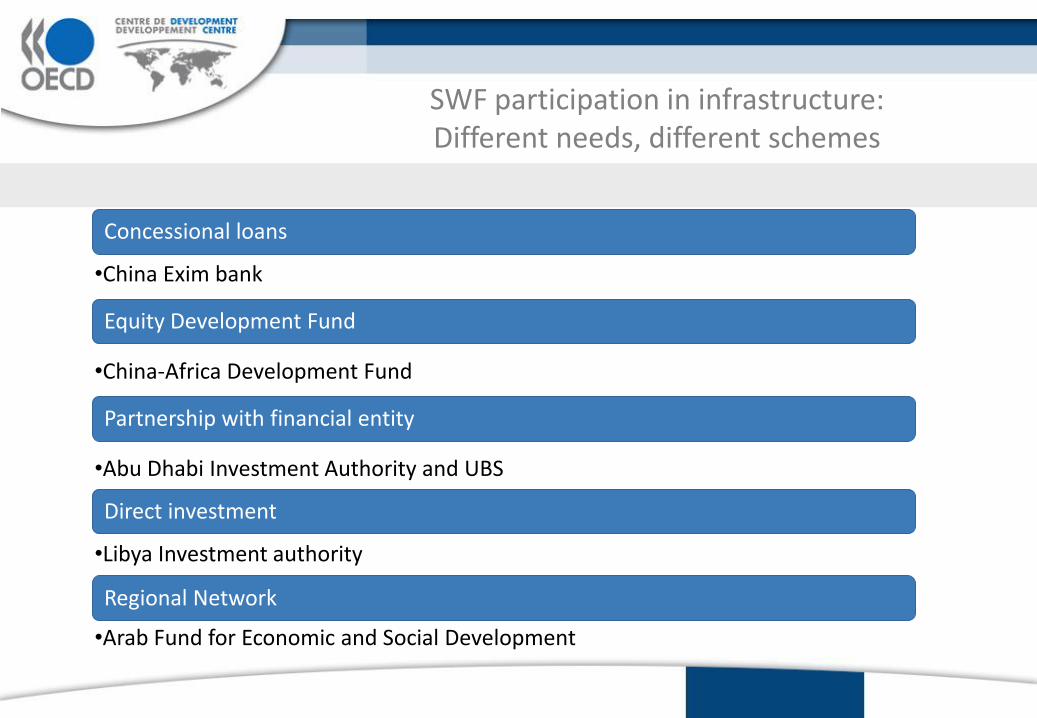

SWF participation in infrastructure: Different needs, different schemes

Concessional loans

•China Exim bank

Equity Development Fund

•China-Africa Development Fund

Partnership with financial entity

•Abu Dhabi Investment Authority and UBS

Direct investment

•Libya Investment authority

Regional Network

•Arab Fund for Economic and Social Development

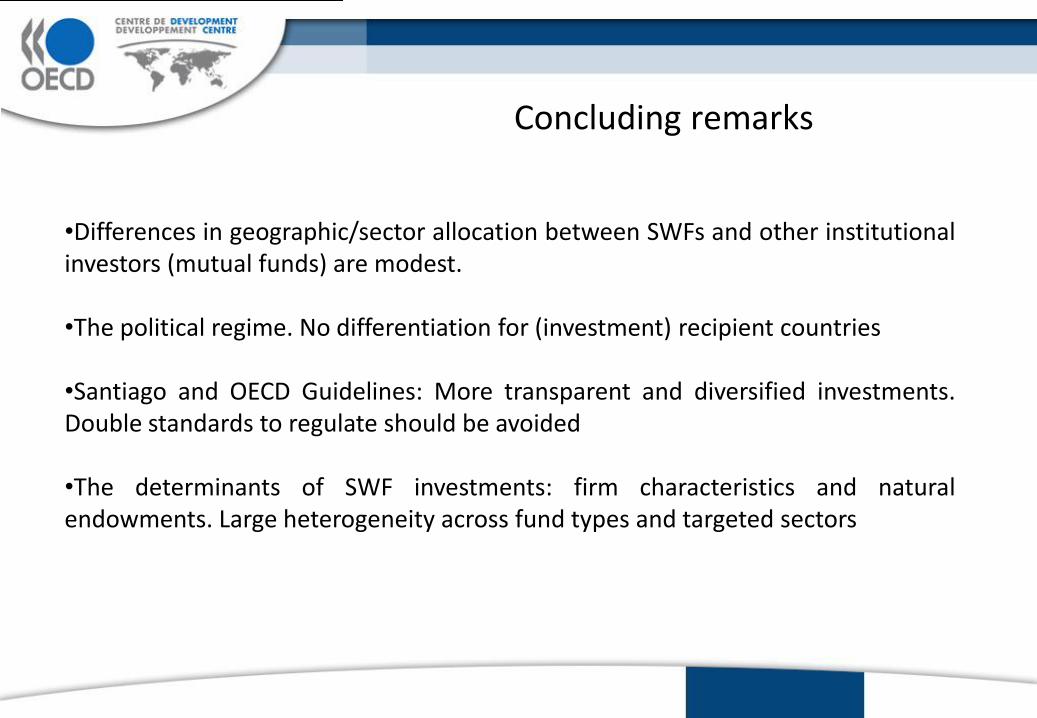

Concluding remarks

•Differences in geographic/sector allocation between SWFs and other institutionalinvestors (mutual funds) are modest.

•The political regime. No differentiation for (investment) recipient countries

•Santiago and OECD Guidelines: More transparent and diversified investments.Double standards to regulate should be avoided

•The determinants of SWF investments: firm characteristics and naturalendowments. Large heterogeneity across fund types and targeted sectors

Concluding remarks

•Financial crisis in 2008 allowed SWFs to re-consider their mandates and re-directtheir investments: “Flight to Quality” vs “Frontier Markets”

• Traditional arguments to attract investment in infrastructure remain valid forSWFs:

•Long term horizon•High returns•Diversified asset class

•SWF investments in Latin America’s infrastructure are modest, compared to otherregions. Between 2006-2009, the trend is increasing.

•SWFs, as other investors, want to reduce PPP-related risks