Sovereign Risk, Debt Management and Financial...

24

Sovereign Assets and Liabilities Management Division Monetary and Capital Markets Department Sovereign Risk, Debt Management and Financial Stability Udaibir S. Das Tunis, March 30, 2010

Transcript of Sovereign Risk, Debt Management and Financial...

Sovereign Assets and Liabilities Management Division

Monetary and Capital Markets Department

Sovereign Risk, Debt Management and Financial

Stability

Udaibir S. Das

Tunis, March 30, 2010

2

Outline

Sovereign debt: A Glut?Sovereign risk: Needs to be redefined?Linkages with financial instability: Real?Debt management: Can it play a role?

Key takeaways: Sovereign risk is a key crisis legacyDebt managers have an important roleNeed an integrated framework for managing sovereign risk, debt, and financial stability

3

Evolution of the Glut

Public Debt-to-GDP ratio (in percent), Selected Countries, 1875–2008

4

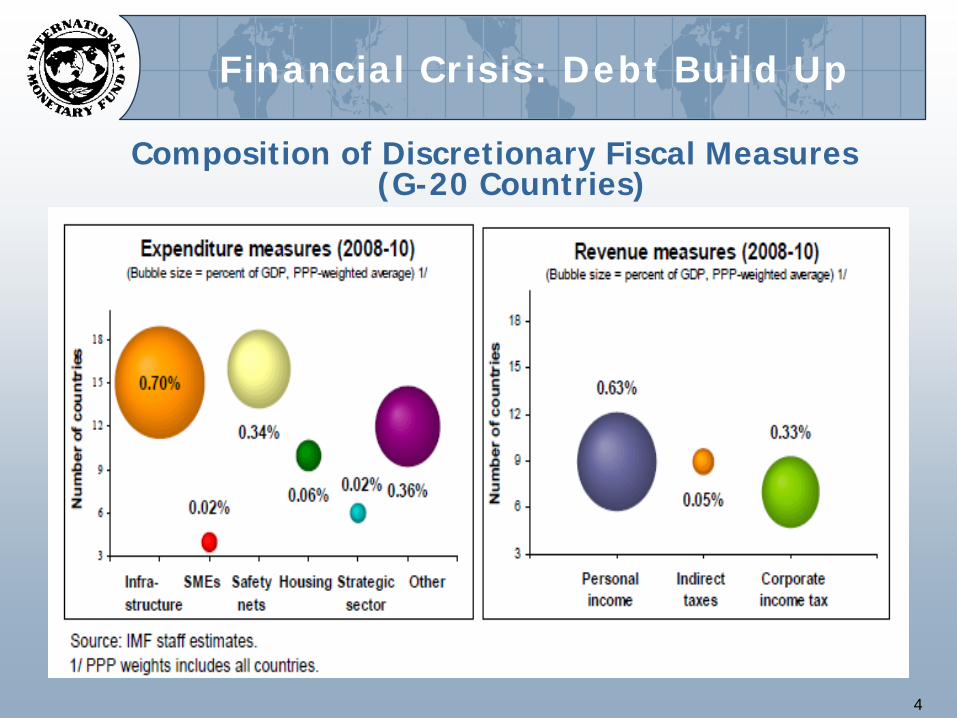

Financial Crisis: Debt Build Up

Composition of Discretionary Fiscal Measures (G-20 Countries)

5

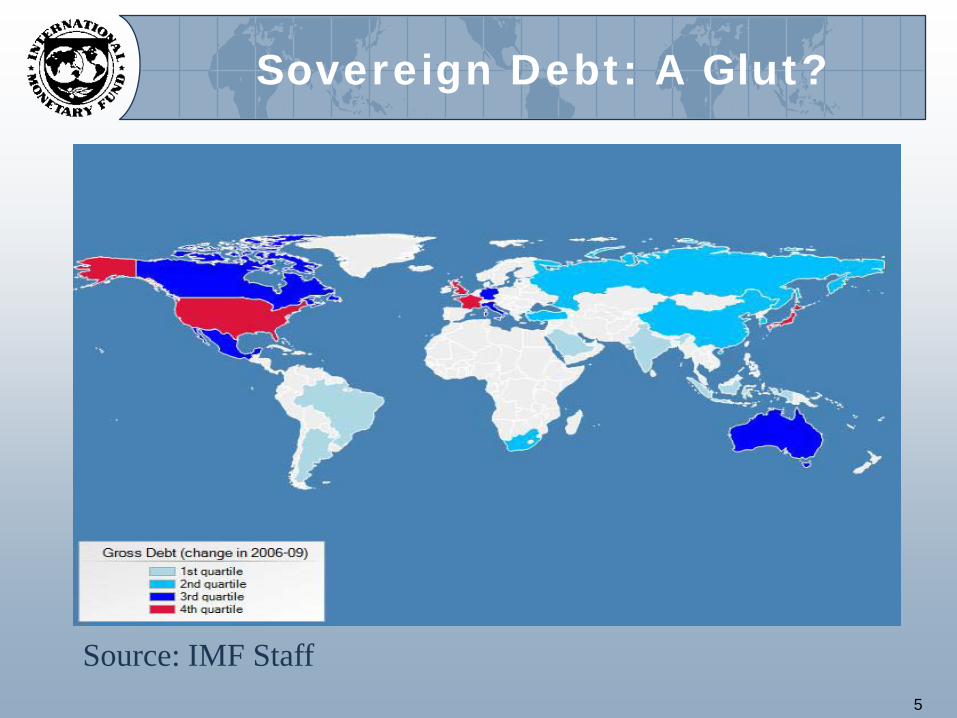

Sovereign Debt: A Glut?

Source: IMF Staff

6

Sovereign Debt: A Glut?

Source: Dealogic, IMF Staff

-

1

2

3

4

5

2005 2006 2007 2008 2009

Gross Issuance: Regional Distribution (USD tr)

United States Japan Eurozone Europe (non-EMU)

7

Impact on Sovereign Debt Profile

Source: Dealogic, IMF Staff. As of end-2009.

21.3

15.816.7

13.7

9.9

3

6

9

12

15

18

21

24

-

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Nu

mb

er

of

Ye

ars

USD

bn

Net Sovereign International Issuance in Emerging Markets

Issuance (lhs) Redemptions (lhs) Average Maturity (rhs)

8

Impact on Sovereign Debt Profile

Issuance load and techniques have changed risk exposure

Maturity structureCompositionInvestor base

9

Impact on Sovereign Debt Profile

Source: Dealogic, IMF Staff

6.4

8.39.0

14.8

-

3

6

9

12

15

18

21

24

2005 2006 2007 2008 2009

Gross Issuance: Average Maturity (Number of years)

USD EUR JPY GBP

10

Financial Stability: definition and linkages with sovereign risk

0.0 4.0 8.0 12.0 16.0 20.0 24.0 28.0 32.0

IrelandSwedenAustria

United KingdomPortugalGreece

BelgiumSpain

ItalyJapan

FranceUnited States

GermanyNetherlands

Share of Domestic Debt withRemaining Maturity up to 1 Year

Source: IMF Staff, BIS

Maturity structure of debt – Shorter maturities could lead to higher interest rates

11

Impact on Sovereign Debt Profile

Rise in contingent liabilities (5 elements)

Guarantees may be calledAnnounced lending facilities may be usedLoans may not be repaidAssets may not retain their valueImplicit liabilities (quasi sovereign; SOEs; sub-national)

12

Exiting will be more of an art than just economics

Unwinding while maintaining financial stability will be a key goal

Macroeconomic adjustments as well as asset liability management (ALM) operations

If an asset sale generates proceeds, an important fiscal policy question is how best to use them

Unwinding of asset facilities established to help balance sheets of financial institutions may have to be gradual

13

Sovereign Risk: Needs to be Redefined?

• “Classic” definition: Used by ratings agencies and multilateral institutions

• “Market perception driven” approach : Implied default probabilities

• “Alternative approaches”: (i) Balance Sheet Approach (BSA); (ii) Contingent Claims Analysis (CCA)

14

Sovereign Risk Needs a Renewed Focus

Re-definition of sovereign risk

More emphasis on BSA and off-balance sheet itemsShould reflect structural vulnerabilities in debt portfoliosRe-examine the measurement, monitoring and management of sovereign risk

15

Towards a New Definition of Sovereign Risk

Some factorsInvestors’ perspectives are key

Liquidity risk of outstanding debt

Larger domestic investor base Refinancing risk for the issuer

Change in credit quality reflected in rating agencies’ actions

Caution with current market measures of risk

Legal and institutional conditions

16

Towards a New Definition of Sovereign Risk

Source: IMF Staff

Reliance on foreign capital

17

Towards a New Definition of Sovereign Risk

Source: IMF Staff, Bloomberg, DataStream. Swap spreads are quoted as 10-yr bond yields minus 10 yr swap rates.

Example of market measures of risk

18

Towards a New Definition of Sovereign Risk

Contagion and risk aversion are two “exogenous” dimensions Debt managers have to cope with market conditions beyond their controlContagion a direct consequence of peer analysisOften transforms specific credit events into an asset class or a regional crisis

19

Towards a New Definition of Sovereign Risk

Sovereign Risk: A Proposed Five Pillar Framework

1. Macroeconomic underpinnings of sovereign debt sustainability (DSA)

2. Sovereign balance sheet strength (RMA/Stress test) 3. Vulnerability of sovereign debt portfolios (MTDS)4. Contagion risk (CCA)5. Global risk aversion (market price of risk)

+Inter-linkages and overlap between five pillars

20

Financial Stability: Linkages with Sovereign Risk

Impacts financial stability through liability & asset side of financial sector balance sheet

Liability side: high risk and high interest rates Asset side: high risk and intermediaries’ holding of government bonds; overall asset quality Sovereign risk from high debt level or risky structure adversely affects investment Higher risk affects composition and structure of financial sector balance sheet

21

Role of Debt Management

Macro Channels

Fiscal Channel: Lead to relatively high costs, possibly implying an unsustainable debt pathMonetary Channel: Impede monetary policy Exchange Rate Channel: Accentuate deleterious effects of exchange rate shocks

22

Role of Debt Management

Financial ChannelHelp reduce government’s exposure to interest rate risk Align profile of debt and that of the investor base Institutional ChannelsReduce market volatility Improve signaling of government policiesInvestors who are risk takers and those who hold longer term instruments

23

A Sum Up

• High sovereign indebtedness a global reality

• Greater risk of negative spillovers • Structural aspect of international markets • Strong potential to impair financial

stability

24

A Sum Up

• Where to focus?• Redefine measurement and management of

sovereign risk• Undertake integrated management of systemic

sovereign risks• Reassess overall balance sheet risk• Associate strategy for sovereign risk management as

part of national contingency framework• Reform the role and function of debt managers

• Fund staff: coming out with a study on financial stability linkages, sovereign risk heat map, and some principles for managing high public debt

![ETHIOPIA’S MEDIUM TERM DEBT MANAGEMENT STRATEGY (2013 …siteresources.worldbank.org/INTDEBTDEPT/Resources/468980... · Ethiopia’s Medium Term Debt Strategy [2013-2017] Page 1](https://static.fdocuments.in/doc/165x107/5b1c3d1c7f8b9a1b688b5d65/ethiopias-medium-term-debt-management-strategy-2013-ethiopias-medium.jpg)