Southern California Housing Outlook Kevin Gillen On Economic Trends

21

SOUTHERN CALIFORNIA HOUSING OUTLOOK Welcome To The Southern California Housing Outlook January 2015

-

Upload

meyers-research-llc -

Category

Real Estate

-

view

202 -

download

0

Transcript of Southern California Housing Outlook Kevin Gillen On Economic Trends

SOUTHERN CALIFORNIA HOUSING OUTLOOK

Welcome To The

Southern California Housing OutlookJanuary 2015

20Southern California Housing OutlookJanuary 2015

Economic SessionKevin Gillen, Ph.D, Chief Economist at Meyers Research

Southern California Housing OutlookJanuary 2015 21

Outline

• Review and discuss current housing market metrics

• Review and discuss underlying economic/demographic drivers of these metrics

• Link housing’s current inputs to its current outcomes

• Deliver the short- and long-term outlook for both U.S. and California housing market

Southern California Housing OutlookJanuary 2015 24

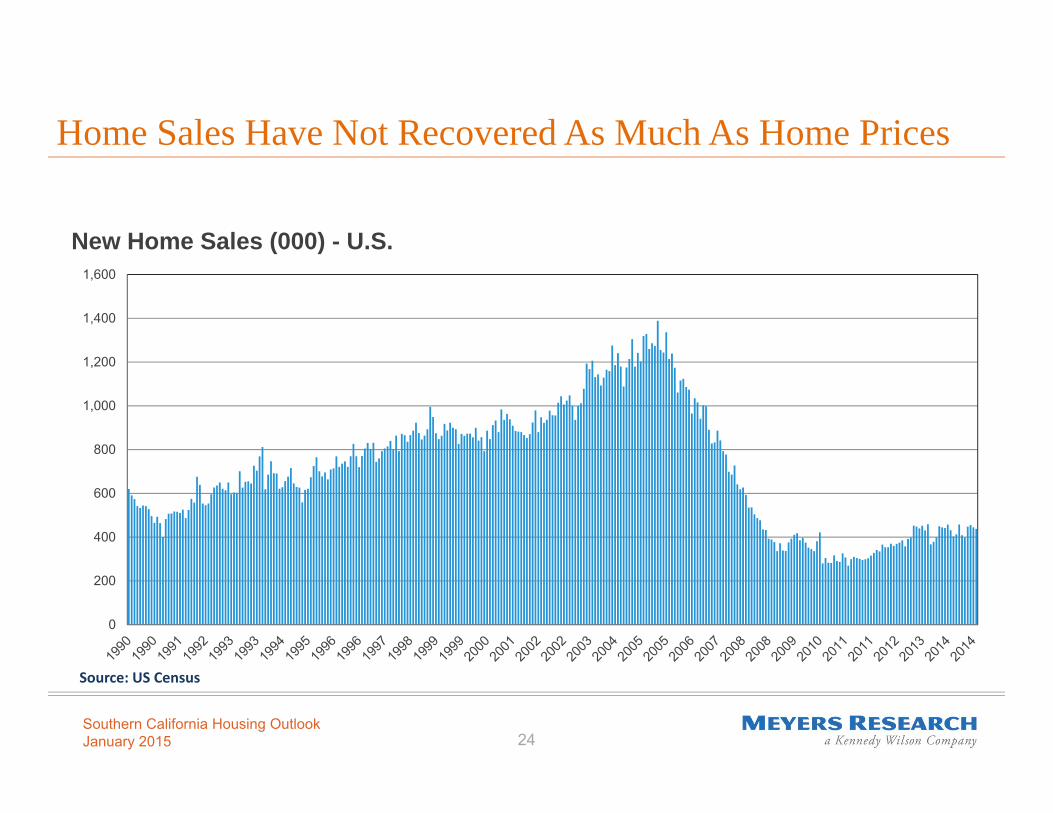

Home Sales Have Not Recovered As Much As Home Prices

0

200

400

600

800

1,000

1,200

1,400

1,600

New Home Sales (000) - U.S.

Source: US Census

Southern California Housing OutlookJanuary 2015 27

Those are the housing market’s current outcomes.

But: what are the underlying inputs that are determining those outcomes?

• Macroeconomic factors

• Demand-side factors

• Supply-side factors

Housing Outcomes v. Inputs

Southern California Housing OutlookJanuary 2015 28

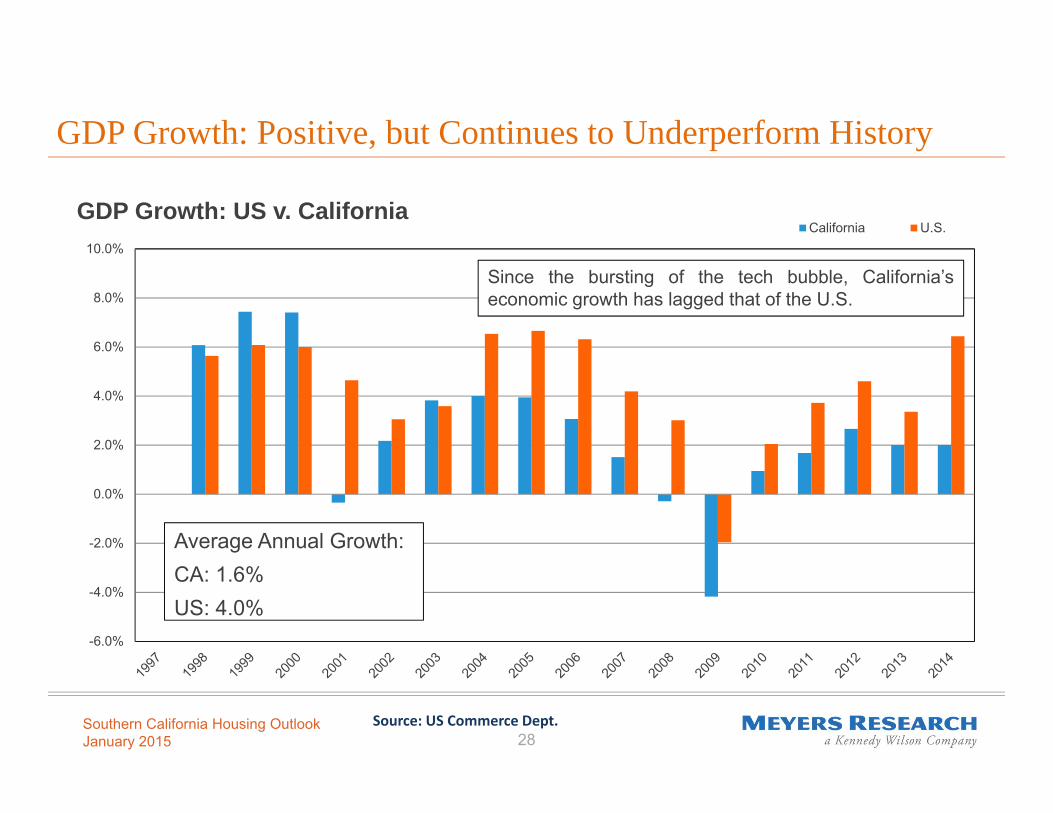

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

GDP Growth: US v. CaliforniaCalifornia U.S.

Since the bursting of the tech bubble, California’seconomic growth has lagged that of the U.S.

GDP Growth: Positive, but Continues to Underperform History

Average Annual Growth:CA: 1.6%US: 4.0%

Source: US Commerce Dept.

Southern California Housing OutlookJanuary 2015 29

Composition of California’s GDP

Real Estate is one of the largest components of California’s economy.

Makes it relatively exposed to real estate downturns.

Source: State of California

Southern California Housing OutlookJanuary 2015 30

Unemployment Declining, But Still Above Historic Average

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Unemployment Rate: US v. CaliforniaCalifornia US

Source: US Bureau of Labor Statistics

Southern California Housing OutlookJanuary 2015 31

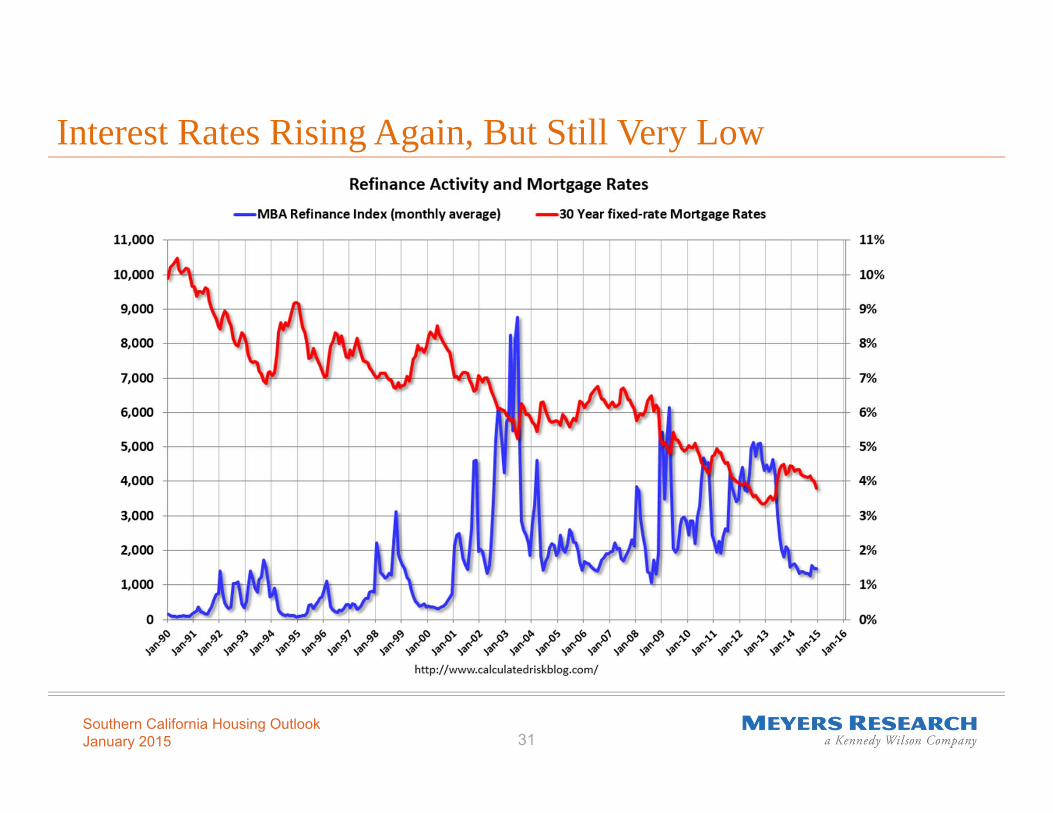

Interest Rates Rising Again, But Still Very Low

Southern California Housing OutlookJanuary 2015 32

Population Growth Positive, But Slowing

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

Population Growth: US v. CaliforniaUS California

Source: US Census

Southern California Housing OutlookJanuary 2015 33

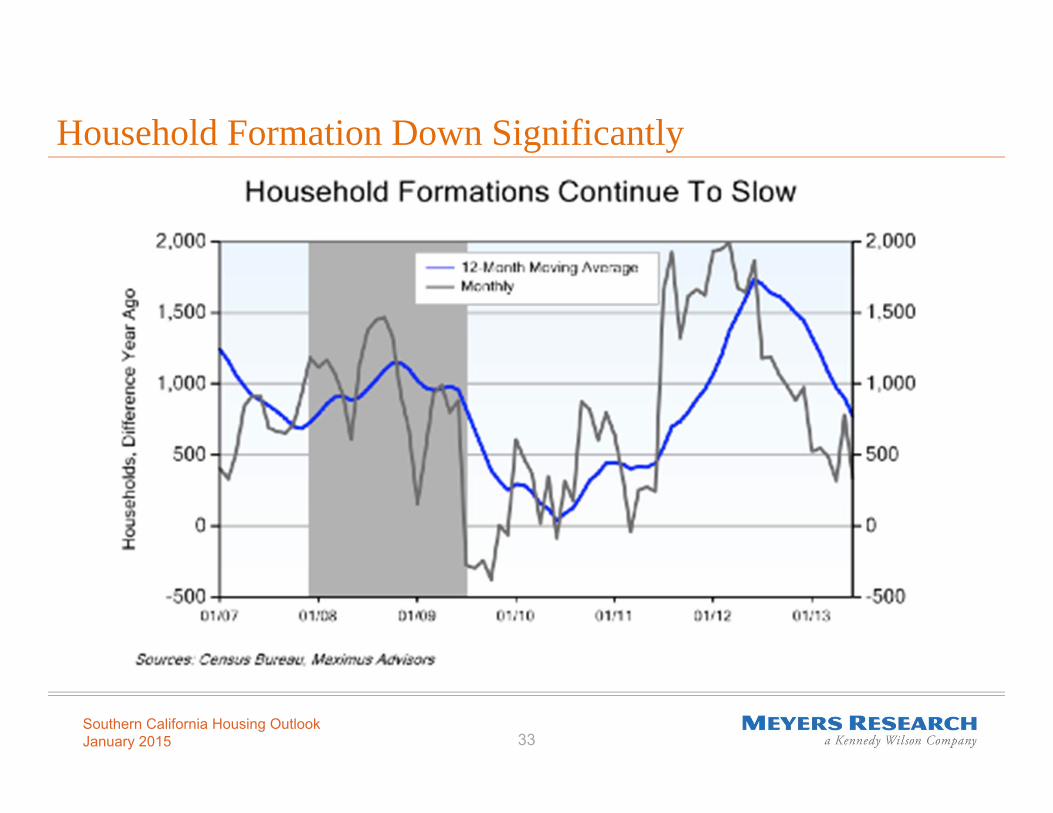

Household Formation Down Significantly

Southern California Housing OutlookJanuary 2015 34

Post-Recession Household Income Growth Stagnant

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

Median Household Income: US v. California

US California

California consistently wealthier thannational average.

Source: US Census

Southern California Housing OutlookJanuary 2015 35

New Home Construction Still Struggling to Recover

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

New Housing Starts: US v. CaliforniaUS California

Source: US Census

Southern California Housing OutlookJanuary 2015 36

Housing Inventories Back to Historic Norms

U.S. Months’ Supply ofInventory

California Months’ Supply ofInventory

Source: Calculated Risk Blog, California Association of Realtors

Southern California Housing OutlookJanuary 2015 37

To recap:• House prices rising but sales still a bit below average• Rental market doing well, but due for a correction• Economy in recovery, but underperforming• Ditto for employment• Interest rates rising, but still low• Population growth and household formation slowing• Income growth sluggish• Inventories normal, but new construction still low• California housing generally doing better than US’s, even if economy

isn’t.

These are mixed signals. So, what does it all mean?!

So: What Does It All Mean??

Southern California Housing OutlookJanuary 2015 38

Signals are mixed because it’s really a “Tale of Two Housing Markets”• Affluent and older households v. poorer and younger households• Driven by economic differences between these two households

(nationally) and housing supply conditions (locally)

Young Households:• Debt (esp. student debt), low skills, college degrees with little market value, less experience

• They’ve been rentingLocally, affordability is the real issue, caused by supply constraints• Land supply

• Environmental Regulations

• Zoning and permitting process

• Political Environment

So: What Does It All Mean??

Southern California Housing OutlookJanuary 2015 39

Homeownership for Young Households Near Historic Low

Source: Trulia and WSJ.com

Southern California Housing OutlookJanuary 2015 42

Implications of Supply Elasticity for Housing

y = 0.5109x + 51.871R² = 0.623

y = 0.1675x + 76.19R² = 0.9188

0

50

100

150

200

250

300

1987

1987

1988

1989

1989

1990

1991

1991

1992

1993

1993

1994

1995

1995

1996

1997

1997

1998

1999

1999

2000

2001

2001

2002

2003

2003

2004

2005

2005

2006

2007

2007

2008

2009

2009

2010

2011

2011

2012

2013

2013

2014

A Tale of Two Cities' House Price Dynamics

Los Angeles

Dallas

Linear (Los Angeles)

Linear (Dallas)

Source: Case‐Shiller

Southern California Housing OutlookJanuary 2015 45

Affordability: US v. Southern California

Source: Economy.com

Southern California Housing OutlookJanuary 2015 46

New Construction is Generally Unaffordable to Most

Source: Meyers Research

Southern California Housing OutlookJanuary 2015 47

In the Short Run:• Housing recovery will continue, both nationally and in California

• But at uneven paces across different U.S. markets

In general, 2015 is looking like a “return to normalcy”…at least at the national level• House price appreciation returning to its historic average of 4-6% per annum

• In Southern California, Affordability will remain the key constraint to a more equitable and widespread recovery

In the Long Run:• California’s supply inelasticity will be the primary governing factor in determining housing

market outcomes:

• Unaffordability

• Volatility/Cyclicality

• Risk to Statewide Economy

Where Do We Go From Here?