Southeastern Actuaries Conference - Actuary.com€¦ · · 2008-05-30Southeastern Actuaries...

28

ING. Your future. Made easier. Southeastern Actuaries Conference Enterprise Risk Management (ERM) November 16, 2007

Transcript of Southeastern Actuaries Conference - Actuary.com€¦ · · 2008-05-30Southeastern Actuaries...

ING. Your future. Made easier.

Southeastern Actuaries Conference

Enterprise Risk Management (ERM)November 16, 2007

Insurance - Banking - Asset Management 2

Agenda

• ERM – Are you doing it?

• Definition of ERM – What is it?

• Industry Overview – What is going on?

• Primary Components of ERM – What are they?

• Rating Agency Perspective – What do they think?

• Economic Capital (EC) – What is it and what are we (ING) doing?

• Questions & Open Discussion – What can we learn from each other?

Insurance - Banking - Asset Management 3

Insurance - Banking - Asset Management 4

Are You Doing ERM?

• How much risk is your company taking (provide a value)?• Is your company taking more risk or less risk than a year ago?

How do you know?• Has your investment risk increased or decreased during the

past three months? How do you know?• How much investment risk is your company taking relative to

your underwriting risk? How do you know?• Do you have the right amount of capital to support the risk your

company is taking? How do you know?

If you do not have answers to the above questions, then more than likely you are not doing ERM!

Insurance - Banking - Asset Management 5

Definition of ERM

• In its “Overview of Enterprise Risk Management,” the Casualty Actuarial Society describes Enterprise Risk Management as:

“…the discipline by which an organization in any industry assesses, controls, exploits, finances and monitors risk from all sources for the purposes of increasing the organization’s short- and long-term value to its stakeholders.”

Similarly, COSO defines ERM as:“…a process, affected by an entity’s board of directors, management and

other personnel, applied in a strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity goals.”

Insurance - Banking - Asset Management 6

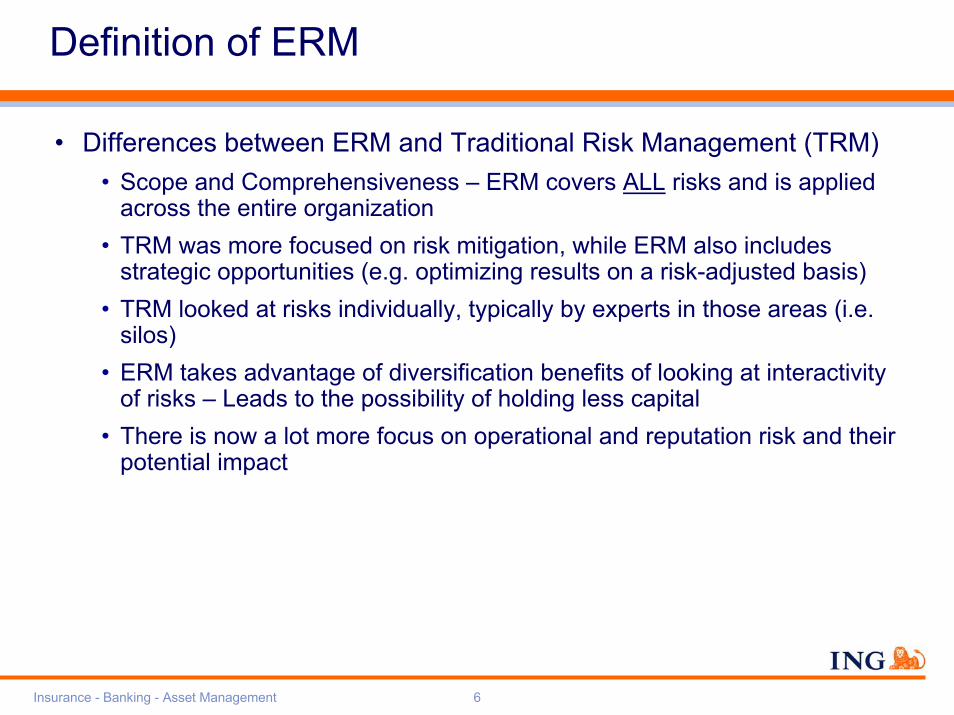

Definition of ERM

• Differences between ERM and Traditional Risk Management (TRM)• Scope and Comprehensiveness – ERM covers ALL risks and is applied

across the entire organization• TRM was more focused on risk mitigation, while ERM also includes

strategic opportunities (e.g. optimizing results on a risk-adjusted basis)• TRM looked at risks individually, typically by experts in those areas (i.e.

silos)• ERM takes advantage of diversification benefits of looking at interactivity

of risks – Leads to the possibility of holding less capital• There is now a lot more focus on operational and reputation risk and their

potential impact

Insurance - Banking - Asset Management 7

Industry Overview

• The activity around ERM has increased significantly over the past year or two and can be attributed to several drivers:

• Regulation• Sarbanes-Oxley• Solvency II• SEC and NYSE requirements• Rating Agencies

• Public• Business scandals• Post 9/11

• Opportunities for Management• Achieve business goals rather than just minimize downside potential

Insurance - Banking - Asset Management 8

Industry Overview

• Education / Resources• SOA - Society of Actuaries

• Sponsors the ERM Symposium• CERA – Certified Enterprise Risk Analyst

• RIMS – Risk and Insurance Management Society• Risk Maturity Model

• An online resource that provides guidelines and best practices for developing and maintaining effective risk programs

• Allows companies to evaluate risk culture competency, identify gaps, and determine areas for improvement

• PRMIA – Professional Risk Managers International Association• PRM – Professional Risk Manager

• GARP – Global Association of Risk Professionals• FRM – Financial Risk Manager

Insurance - Banking - Asset Management 9

Industry Overview

Insurance - Banking - Asset Management 10

Primary Components of ERM

• Establishing an ERM framework and risk governance

• Risk identification

• Risk assessment

• Risk response

• Incorporation into performance measurement / management

• External risk reporting

Insurance - Banking - Asset Management 11

Rating Agency Perspective

• Rating agency’s evaluate the risks of a company and their ability to manage those risks

• Standard & Poor’s – Enterprise Risk Management (ERM) evaluation criteria

• Part of the rating process since October 2005• Evaluate ERM quality in five areas

• Risk management culture• Risk controls• Extreme risk management• Risk and economic capital models• Strategic risk management

• Classifications – Excellent, Strong, Adequate, Weak

Insurance - Banking - Asset Management 12

Economic Capital (EC)

I. What is Economic Capital? Why use it?

II. EC measurement and risk management in ING

III. Conclusions

Insurance - Banking - Asset Management 13

EC as part of the total balance sheet

Market Value Surplus= Available CapitalEconomic

Capital

Guaranteed liabilities

Excess Capital

Market Value of Assets

Market Value of

Liabilities

Risk margin

Economic Capital is the amount of assets that is needed in addition to the market value of liabilities to “guarantee” payment of all liability cash flows at a x% confidence level in a determined period of time.

Insurance - Banking - Asset Management 14

Economic Capital

Best Estimate Market Value

Surplus

99.95%

Economic Capital

Market Value Surplus in 1 year

Insurance - Banking - Asset Management 15

Why Stakeholders are Converging to EC

− Regulators demand that risks are well managed (to avoid taxpayer bail-outs)

− Depositors/policyholders expect safety of their savings and investments

− Rating agencies will only give high ratings to institutions able to measure and manage risk

Shareholders have entrusted the board with their capital

– They don’t want to lose it– They expect a decent return on it– They don’t want any surprises– They penalise volatility

ShareholdersAnalysts

RegulatorsRating AgenciesCreditors

SeniorManagement

Risk versusCapital

Risk versusReturn

Capital Adequacy Capital Efficiency

A common system is required for all users

Insurance - Banking - Asset Management 16

Discussion Points

I. What is Economic Capital? Why use it?

II. EC measurement and risk management in ING

III. Conclusions

Insurance - Banking - Asset Management 17

Capital models in ING

• Until 2002 - 150% EU Requirement• 2003-2005 - ING Capital Model (ICM) – still factor based• 2006 and onwards - Economic Capital

EconomicCapital

Market Valueof Liabilities

StatutoryReserves

150% EU Capital

Requirement

StatutoryReserves

ING CapitalModel

Requirement

Insurance - Banking - Asset Management 18

A Continual Improvement Process

Measurement

Control

Management

1999/2000 Start EC Pilots

2004: EC results used to calibrate ICM

2005:• Board & ALCO approval to further

implement EC• Input in MTP: MVaR limits• EV profit in strategic planning

process

2006:• MC Pricing targets• Full migration of EC, MVaR,• Focus on auditable, efficient risk

and value reporting processes• Risk governance• EV profit in incentive plans

Pre 1999: strong foundation in current and future assumption setting and cash flow projection experience

around Embedded Value calculations.

2007 Objectives• Auditable, efficient risk

and value reporting processes (ECAPS)

• Confirm usage of MCEV for internal management; consideration for valuation tool for external purposes: to be decided, considering model stability and (credit) spread recognition.

• Leverage ECAPS to change the way that actuaries view our business (risk management)

Insurance - Banking - Asset Management 19

How is Economic Capital Calculated?

• Assets, Liabilities, and Surplus at Market Value• EC = Change in Market Value Surplus under 1 in 2000 worst case

occurrences during next year • 1 in 2000 correlates to risk profile of AA rated company

• Required Capital = Sum of Individual Required Capitals based on Risk Type

• Credit and Transfer Risk • Market Risk• Business Risk • Operational Risk• Insurance (Life and Non-life) Risk

• less Diversification Effects• Total combined risk capital < sum of individual risk capitals• Diversification exists across risk types and business units

Insurance - Banking - Asset Management 20

Risk types correspond to a possible economic loss

RISK

Earnings Deviation

RISK

Earnings Deviation

Non-Life Risk

Claims Deviation

Non-Life Risk

Claims Deviation

LIFE Risk

Mortality Deviation

LIFE Risk

Mortality Deviation

OPERATIONAL RISK

Event Loss Deviation

OPERATIONAL RISK

Event Loss Deviation

BUSINESS RISK

Residual Earnings Deviation

BUSINESS RISK

Residual Earnings Deviation

MARKET RISK

Value at Risk

MARKET RISK

Value at Risk

TRANSFER RISK

Unexpected Transfer Loss

TRANSFER RISK

Unexpected Transfer Loss

CREDIT RISK

Unexpected Loss

CREDIT RISK

Unexpected Loss

Total Economic

Risk

Earnings Deviation due to variations in Credit Losses

Earnings Deviation due to inability to repatriate funds - immaterial for insuranceEarnings Deviation due to changes in the Market Price or Liquidity

Earnings Deviation due to changes in Operating Economics (e.g. Volume, Margins or Costs

Earnings Deviation due to One-off Losses unrelated to Volume, Margins and Costs

Earnings Deviation due to unexpected changes in mortality rates

Earnings Deviation due to changes in morbidity and P&C claims

Inte

r-ris

k di

vers

ifica

tion

Insurance - Banking - Asset Management 21

EC Competitive Advantages

Solvency II • Improved risk management improves view

Analyst’s View

ING’s Rating• Best Practice Risk Management will be essential part of rating

review process• Rating will influence share price and provide us with cheaper

capital

• Lobbying opportunities globally

• Capital consequences

• Analysts will recognise our pro-activeness

Pricing• Pricing on EC will better reflect risks in our products

• EC will identify unprofitable products or markets

• Exploit opportunities with EC pricing Vs. statutory

Managing our business on EC will benefit all our stakeholders

Insurance - Banking - Asset Management 22

Capital use - Managing market risks

• Measure• Objectively quantifying the market risks taken by ING Group • Measure equity, interest rate, foreign exchange, real estate, and credit spread risks

as well as credit risk- all adjusted for risk diversification

• Manage• Provide framework for optimal management of market risks in insurance (MVaR

covers 60% of total Economic Capital for ING Insurance)• Optimal allocation of scarce resources through allocation of limit space• Optimal determination of investment mix: business units to decide within limits• Making risks (i.c. risk-return) comparable throughout ING Group by creating a

‘level playing field’

GOAL: Objectively measure and actively manage market risks

Insurance - Banking - Asset Management 23

How to get it right? EC Application Software

Auditability • Clear control procedures and documentation leading to auditable EC reporting

• Large increase in automated processes • Supports auditable Risk Dashboard reporting

Timeliness • Timely quarterly reporting in line with financial calendar

Consistency • Standardised methodology and reporting format• Comparable assumptions and results across entities

Functional Improvements

• Improved methodologies, particularly on market risk calculations, diversification and aggregation of risks

• Expandable to support MCEV performance analysis and reconciliation

• Replicating portfolio for ALM interface

Market Risk Analysis • Faster Group wide impact of analysis of specific risks• Increased analysis & communication – move from getting the

numbers to using the numbers

Insurance - Banking - Asset Management 24

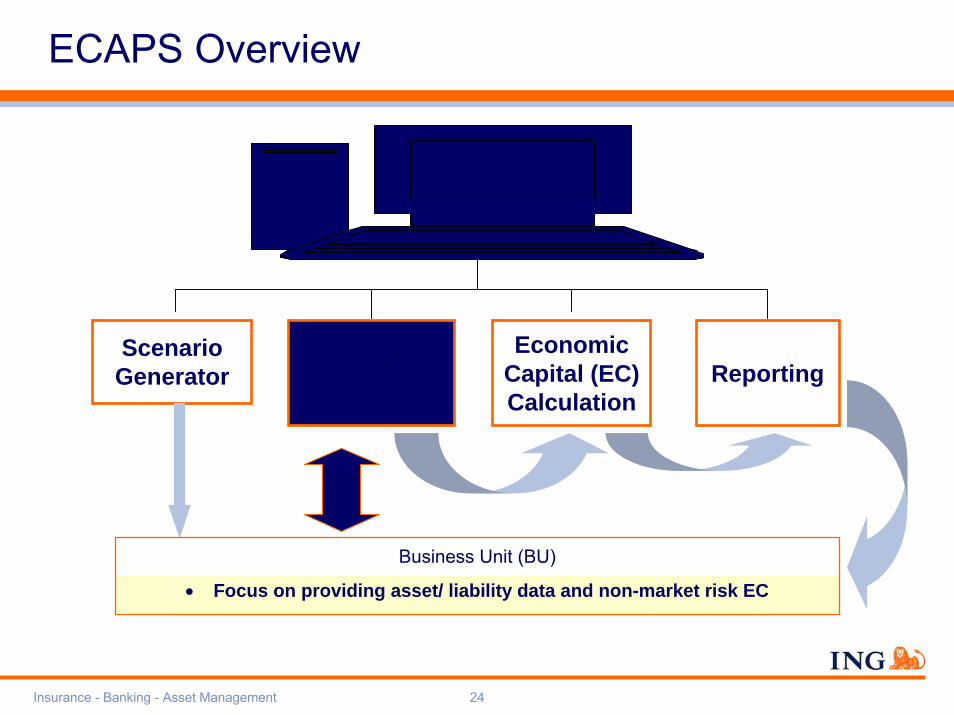

ECAPSTool

Reporting

ECAPS Overview

Replicating Portfolio

Economic Capital (EC) Calculation

Scenario Generator

Via Intranet

Business Unit (BU)

• Focus on providing asset/ liability data and non-market risk EC

Insurance - Banking - Asset Management 25

ECAPS - improvements

• Current methodology tries to measure individual liabilities veryaccurately, but makes big approximations for

• Market shocks (e.g. single factor for term structure, etc.)• Diversification / aggregation (e.g. simplified covariance matrix, Gaussian Copula)

• New methodology uses replicating portfolios to capture asset andliability risk profiles

• Much more accurate EC market shocks & diversification possible due to Monte-Carlo method

Old Method

New Method

Best PossibleCash Flow

Models

SimplifiedMarketShocks

Very SimplifiedAggregationTechniques

Best PossibleCash Flow

Models

SimplifiedPortfolio

Representation

AdvancedEC &

Aggregation

Overall Approximation

Error

Insurance - Banking - Asset Management 26

Discussion Points

I. What is Economic Capital? Why use it?

II. EC measurement and risk management in ING

III. Conclusions

Insurance - Banking - Asset Management 27

• Alignment of external, regulatory and internal move to enhanced risk measurement through EC will facilitate:

• Improved understanding of risks and therefore avoiding costly mistakes that may hurt the solvency of the insurer

• Better risk management in insurance companies• Provide more transparency for the external world• Senior executives will be able to make better informed

decisions about risk and capital, and ultimately improve the risk-adjusted business performance of the company

Summary

INCREASE TOTAL SHAREHOLDER RETURN

Insurance - Banking - Asset Management 28

Questions & Open Discussion

• Thoughts on ERM• The evolvement of ERM to-date• What are you seeing now?• Where you think this will lead to in the future?

• Challenges• Opportunities

• Questions / Comments