Sourcing Industry Briefing & BYOD Trends

18

Copyright © 2012 Information Services Group, Inc. All Rights Reserved. No part of this document may be reproduced in any form or by any electronic or mechanical means, including information storage and retrieval devices or systems, without prior written permission from ISG, Inc. Hotel, Restaurants & Leisure Industries Sourcing Industry Briefing & BYOD Trends

-

Upload

information-services-group-isg -

Category

Business

-

view

776 -

download

0

Transcript of Sourcing Industry Briefing & BYOD Trends

Copyright © 2012 Information Services Group, Inc. All Rights Reserved. No part of this document may be reproduced in any form or by any electronic or mechanical means, including information storage and retrieval devices or systems, without prior written permission from ISG, Inc.

Hotel, Restaurants & Leisure Industries Sourcing Industry Briefing & BYOD Trends

2

Busiest Year Ever in the Broader Outsourcing Market

↑ Number of Contracts

↑ EMEA – record year

↓ Americas & Asia-Pacific

↓ Mega Relationships

↑ Restructurings

→ Pace of Annualized Rev. Growth ─ Flat to 1%

→ BPO up 49%, ITO down 6%

→ Leading IT Providers Consistent across Top 20

→ Contract Durations

TCV ($B)* Trends

* Managed Services Contracts with TCV > $25M

85.0 90.0 93.5 93.1 99.4

14.8 21.1 20.2 30.6 32.4

2007 2008 2009 2010 2011

Total TCV Restructured TCV

$92.2B 5 yr avg

3

Major Developments in the U.S. Sourcing Market

Today $28

7 yrs Ago $41

1 U.S. TCV ($B) Continues Significant Downward Trend

3

2 ↓~30%

47

28

↓40%

Pool of U.S. Companies Ranked in G-100 is Down 4

7 Yrs Ago Today

U.S. Companies ranked in G-500 Contribute Less to US Awards

↓25%

7 Yrs Ago Today

$ $ 58% of TCV 33% of TCV

U.S. Market Saturation for G-100

7 Yr Ago

Today

55%

4

Changing Outsourcing Market Dynamics

1 More Transactions Include Offshore Delivery Than Ever 2 Large Companies Leveraging

Multi-sourcing More Than Ever

4 Number of Service Providers Making Up 75% Share of TCV

37

10 Yrs Ago Today

7

15 3 Continued Growth in Savings

Realized through Outsourcing

33%

69%

7 Yrs Ago

Today

2x

10 Yrs Ago Today

53% 33%

% G2000

7 Yrs Ago

Today

5

Key Long-term Trends in Sourcing Structure & Solutions

1 Shift in Enterprise Decision Maker’s Solution Requirements

3

2 Shift in ITO Enterprise Pricing Strategies

Longevity Disposability Pricing Bands Utility Pricing

$

Shift in BPO Enterprise Purpose, Spurring Activity

Industry Specific

Traditional Back-office

4 Global Service Provider Community Changing Shape

6

Service Provider Diversity Creates Price Pressure

growth In Mid-Market Space

87%

58%

1% 20%

MNCs India-heritage

Today 2000

Market Share

68%

77%

87%

2000

2005

2010

$25-199M $200-999M $1B+

% New Contracts in TCV Bands

India-heritage Provider

7

Capability

Cost / Capacity

Industry and Technology Trends Affecting the CIO Agenda

► Margin Pressure ► Efficient Use of Capital ► Responsive Capacity

► Transformation ► Social Platforms

Upending Customer Centricity

Challenges

► Data Analytics / BI ► Unified Communications ► Next-Gen Systems

► Cloud: As-A- Service Solutions

► Mobility eEnablement of back-end systems

► Multi-sourcing ► Service Integration ► Governance

► Data Privacy & Security ► Global Service Delivery ► Business Resiliency

► Shift to Standardized Solutions ► Global Service Delivery

8

Hotels, Restaurants & Leisure − Market Overview

$22 $58

$140 $155

$227

$309 $291 $319

$404

2003 2004 2005 2006 2007 2008 2009 2010 2011

US$

Mill

ions

Market Size (ACV) - Hotels, Restaurants & Leisure

69%159% 141% 11% 47% 36% -6% 9%Growth: 27%

11 12 Outsourcing Not Outsourcing

23 Public Companies In G2000

9

2011 IT Functional Areas Under Managed Service Contracts > $25M TCV

Hotels, Restaurants & Leisure companies tend to have high levels of adoption for many ITO towers, indicating a tendency to bundle ITO services

82%

27%

55% 64% 64%

55%

85%

61% 47% 48%

55% 47%

0%

20%

40%

60%

80%

100%

Any ITO ADM Data Center Mid-Range Network EUC / SD

Hospitality & Leisure Market Avg

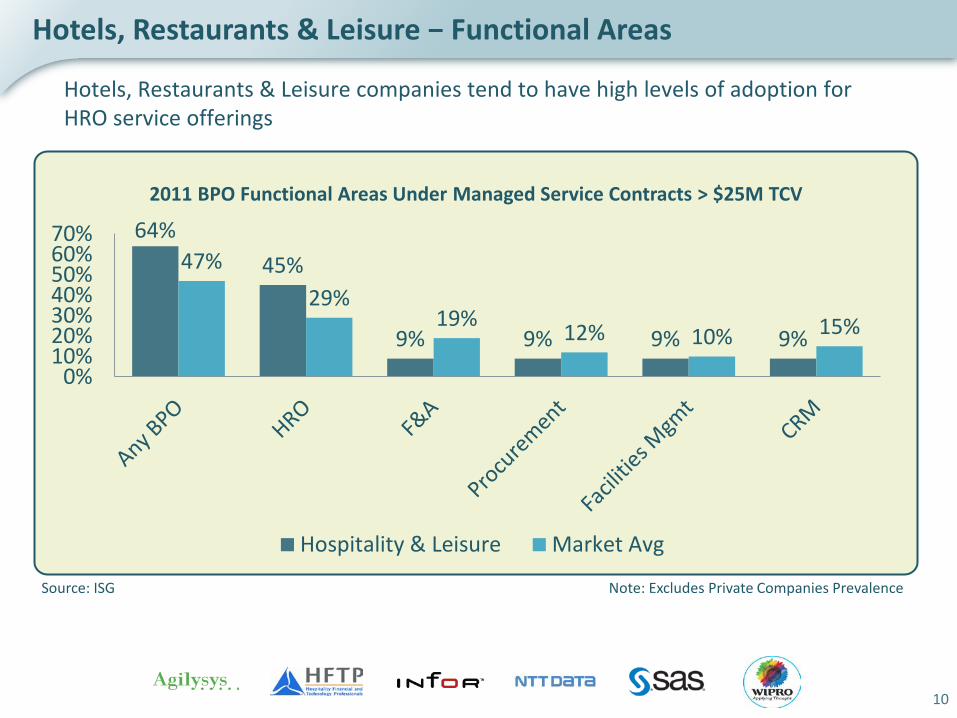

Hotels, Restaurants & Leisure − Functional Areas

Source: ISG Note: Excludes Private Companies Prevalence

10

2011 BPO Functional Areas Under Managed Service Contracts > $25M TCV

Hotels, Restaurants & Leisure companies tend to have high levels of adoption for HRO service offerings

64% 45%

9% 9% 9% 9%

47% 29%

19% 12% 10% 15%

0%10%20%30%40%50%60%70%

Hospitality & Leisure Market Avg

Hotels, Restaurants & Leisure − Functional Areas

Source: ISG Note: Excludes Private Companies Prevalence

Bring Your Own Device (BYOD)

12

“Personal” Cloud

BYOD: An IT Mega-trend Enabled by Three Trends in Technology

►Every conceivable software offering is now available via the public internet; enterprise-class technology now available to the SMB customer.

►Consumer technology is driving changing expectations in enterprise technology; employees grow accustomed to app-store like features that are often free, and updated often.

Enterprise Consumer

Expectations

Mobile Technology

►Mobile platforms (smartphones and tablets) are now nearly as powerful as the PC; smartphone + tablet shipments outpace PC shipments in 2010 and 2011

13

“Personal” Cloud

BYOD Taking Two Paths of Adoption

Enterprise Consumer

Expectations

Mobile Technology

IT Policy, Security &

Compliance

Unclear ROI

Legacy Apps

Results G1000:

awareness and limited recognition; very little adoption.

Midmarket &

Selected Technolgoy Firms:

recognition & adoption

14

BYOD Significant Challenges & Hurdles to Overcome

► IT Policy, Security & Compliance IT policies and processes need to be re-worked from the ground-up to accommodate Without control of assets, IT cannot guarantee security & integrity of data; CIO exposed IT builds apps for standardized platforms; BYOD is inherently non-standardized Legal implications around device ownership in a reimbursement model

► Unclear ROI Device maintenance better supported by employee vs. corporate; less expensive Reimbursement vs. procurement may actually cost more IT says it will not support; but ends up supporting a non-standardized environment Significant new unplanned technologies may be required (e.g. VDI, MDM, client-side

virtualization, etc.) Unplanned downtime for information workers (e.g., go to Apple store for new HDD)

► Legacy Applications & Connectivity Large enterprises have built client-server apps to work on specific OS builds; refactoring Limited connectivity for mobile workers means information is stored locally or VPN required Web-based, app-store like portfolio and infrastructure may needed to fully take advantage ….BUT employees still want those corporate apps on their phone!!

15

These dramatic market changes across cloud & mobile are driving employees to BYOD models, but enterprises are only slowly supporting this shift.

Results

►Creating a significant demand for BYOD approaches: 52% of all info workers use 3+ devices for work and growing PLUS ONE annually 25% of devices used for work are not PCs 71% of companies want to implement app-stores internally

►However, enterprises are not responding Less than 10% of companies are planning or have implemented BYOD programs Over 70% of employees will continue to be provided and supported by a

corporate smartphone policy Only 11% have set up internal app stores Only about a third of organizations surveyed say that usage of consumer

technologies in the workplace are key to employee retention and productivity

Sources: Forrester: Info Workers Using Mobile & Devices For Work Will Transform Markets, IDC: Top 10 2012 Predictions Symantec: State of Mobility Survey Unisys: Consumerization of IT Benchmark Study

16

To date, only a small handful of large companies have moved to BYOD, most being technology companies. However, these companies generally report:

BYOD Opportunities: Market

► Information workers are happier and may be more productive Intel reports that they gained 1.6MM hours of productivity from their BYOD shift.

► IT is freed-up to work on more important projects In theory, IT no longer needs to spend time building, testing and deploying PCs and

mobile phones, and can instead work on projects to help growth or improve productivity.

► BYOD creates a progressive image for the company Nearly all major technology magazines and blogs are looking for real-world examples

of BYOD; when they find it, it is highly publicized and is excellent case-study fodder.

Sources: Intel: Improving Security and Mobility for Personally Owned Devices

17

To date, only a small handful of large companies have moved to BYOD, most being technology companies. A few have outsourced BYOD services support:

BYOD: Outsourcing Trends

► The key additional End User Services to support a BYOD environment are: Mobile Device Management (MDM) and Mobile Applications Management (MAM)

► The two services overlap and appear to be merging into: Asset Management, Software Distribution, Security Management Current trends see a consolidation in the software vendor space and potential

integration with enterprise scale master console or management systems

► Open issues: Market alignment on pricing and SLAs; multiple class of users

Sources: Intel: Improving Security and Mobility for Personally Owned Devices

www.isg-one.com [email protected]

![Manufacturing & Sourcing: in China for China...Chambers & Partners 2016 recommends: MAARTEN ROOS R TABBERS CONTENTS OF THIS BRIEFING Manufacturing & Sourcing: in China for China [p.3]](https://static.fdocuments.in/doc/165x107/5f35044fdc46524847401b2b/manufacturing-sourcing-in-china-for-chambers-partners-2016-recommends.jpg)