Source of Earnings - Canadian Institute of Actuaries · and Other Changes xxx xxx Earnings on...

42

1 Source of Earnings Thomas Hinton, FCIA, FSA With assistance from Blake A. Hill, FCIA, FSA Practice Education Course Cours orienté vers la pratique CIA Practice Education Course Finance/Investment June 1-4, 2014 Ottawa, ON

Transcript of Source of Earnings - Canadian Institute of Actuaries · and Other Changes xxx xxx Earnings on...

1

Source of Earnings

Thomas Hinton, FCIA, FSA

With assistance from

Blake A. Hill, FCIA, FSA

Practice Education Course Cours orienté vers la pratique

CIA Practice Education Course

Finance/Investment June 1-4, 2014

Ottawa, ON

2

Background

Classic Financial Statements: • Point in Time:

– Balance Sheets • Change over Time

– Income Statements – Source of Earnings

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

3

Background

Income Statements: Revenue

– Premium – Investment Income

Less Dispositions – Expenses – Claims – Change in Reserves …

= Net Income Before Tax

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

4

Background

So what value does an SOE analysis provide over a traditional Income Statement?

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

5

Example: What happened here?

Actual Plan Premium 1,000 900 Investment Income 100 110 Claims 500 400 Surrenders 200 160 Change in Reserves 300 300 Net Income Before Tax 100 150

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

6

Background

SOE analysis should be: – Consistent with other reporting; – Easy to understand, produce, and replicate; – Well documented; – Contain all components of earnings/explain material

aspects of net income.

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

7

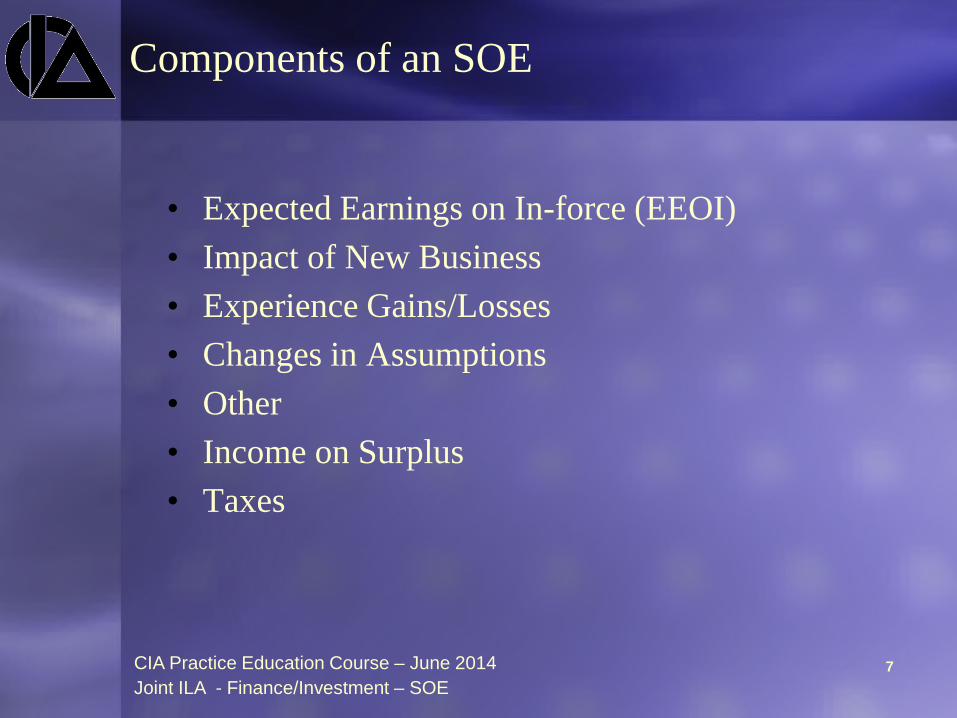

Components of an SOE

• Expected Earnings on In-force (EEOI) • Impact of New Business • Experience Gains/Losses • Changes in Assumptions • Other • Income on Surplus • Taxes

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

8

EEOI

Earnings that would be reflected if actual results matched valuation best estimate. Includes

– Expected release of PfAD – Expected Fee Income – Income from Funds on Deposit – Amortization of Balance Sheet Amounts

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

9

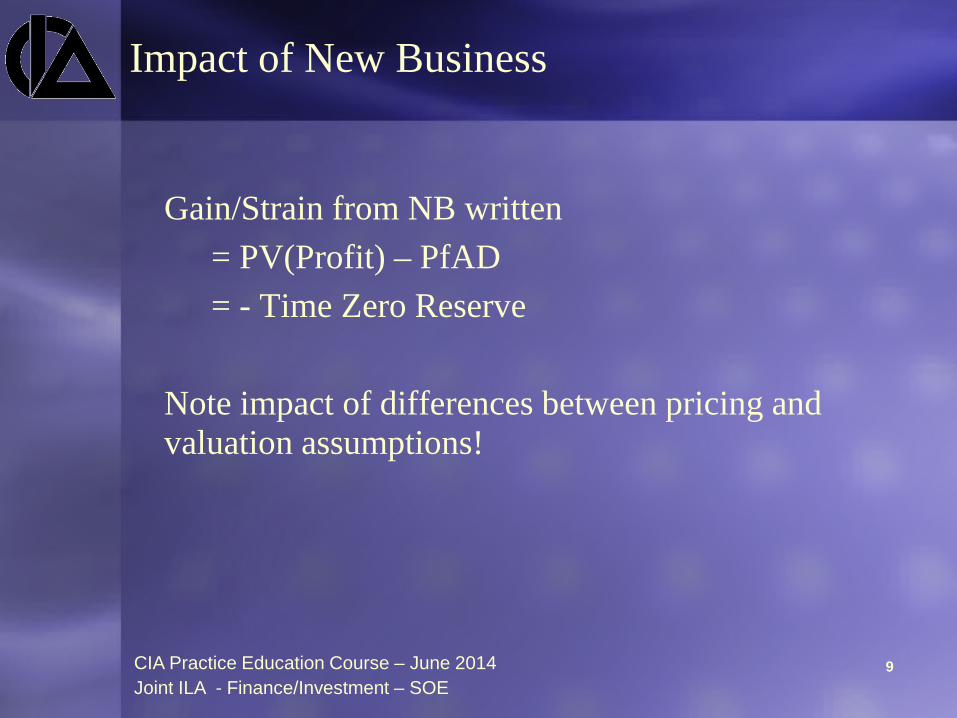

Impact of New Business

Gain/Strain from NB written = PV(Profit) – PfAD = - Time Zero Reserve Note impact of differences between pricing and valuation assumptions!

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

10

Experience G/L

Actual experience vs valuation best estimate over the reporting period.

– Mortality/Morbidity – Surrender – Investment and so on …

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

11

Experience G/L

Why can’t we just take Actual/Expected from plan or budget? Hint: what Income Statement Lines are impacted by variances in:

• New Business • Mortality Experience • Lapse • …

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

12

Changes in Assumptions and Other

– Best estimate assumptions and margins; – Changes in methodology; – Correction of errors; – Management actions.

Income on Surplus Taxes

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

13

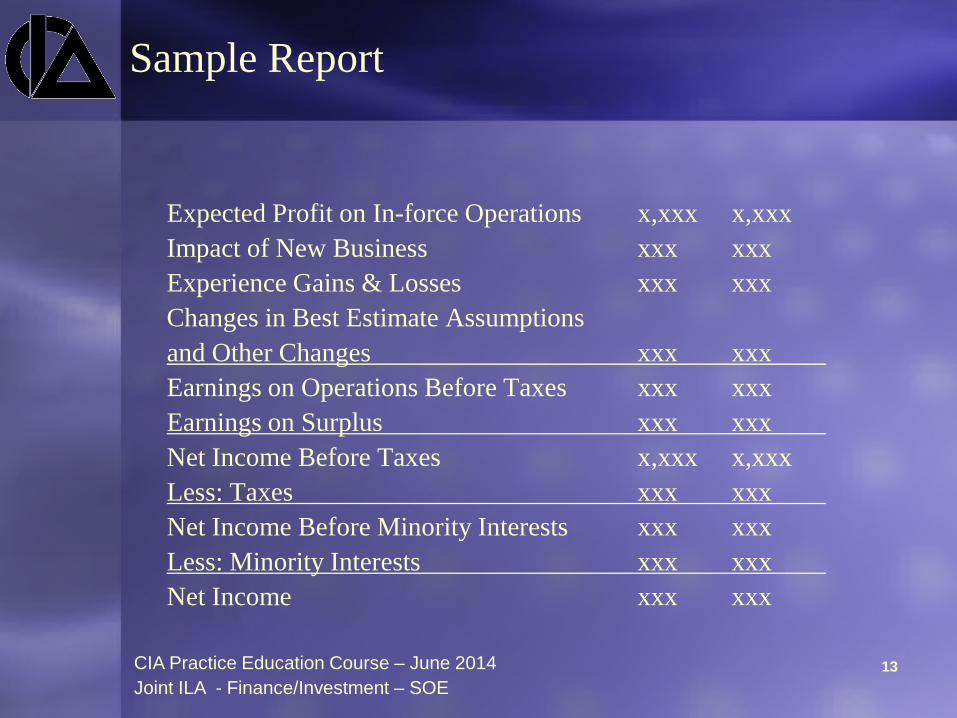

Sample Report

Expected Profit on In-force Operations x,xxx x,xxx Impact of New Business xxx xxx Experience Gains & Losses xxx xxx Changes in Best Estimate Assumptions and Other Changes xxx xxx Earnings on Operations Before Taxes xxx xxx Earnings on Surplus xxx xxx Net Income Before Taxes x,xxx x,xxx Less: Taxes xxx xxx Net Income Before Minority Interests xxx xxx Less: Minority Interests xxx xxx Net Income xxx xxx

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

14

Other Considerations

Need to be able to differentiate PfAD from best estimate reserve. Approximations may be required to determine CALM reserve associated with NB. Order may matter in calculation due to inter-relationships. Par Business

Key is to explain items that effect net income. Experience passed through dividends would not be included.

Data used would be consistent with ledger and existing processes.

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

15

Example: Question 3 from 2010 Exam

As valuation actuary at SimplyLife Co, you are responsible for preparing the financial statements for the life insurance business unit. The business unit is closed to new business and at December 31, 2009 consists of two policies, both Non-Renewable 5-Year Term Insurance. Your business unit is not responsible for surplus management.

Policy 1 Policy 2

Face Amount $100,000 $50,000

Maturity Date Dec 31, 2011 Dec 31, 2012

Premium payable BOY $1,500 $600

Date of Birth Dec 31, 1939 Dec 31, 1938

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

16

Example: Question 3

Balance Sheet: Dec 31, 2009 Assets $5,420 Policy 1 Best-Estimate $2,153 Policy 1 PfAD $500 Policy 2 Best-Estimate $2,372 Policy 2 PfAD $395 Total Liabilities $5,420

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

17

Example: Question 3

Valuation assumptions: • Mortality MfAD is 10% of best estimate • q(71) = 0.027 • q(72) = 0.028 • q(73) = 0.030 • q(74) = 0.034 • Valuation Interest Rate = 5%

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

18

Example: Question 3

Assume: • No Taxes • No Expenses Experience: • Assets Earned 7% in 2010 • Policy 1 died Dec 31, 2010

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

19

Example: Solution

Please note: the solution that follows is not the only correct answer to the question! There are many equally correct ways to solve the question and receive full marks. A less ambiguous (and much easier to grade) question would have provided PfADed and Best-Estimate Reserves rather than have candidates calculate them.

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

20

Example: Solution to Part A

Part A – Construct the 2010 Income statement: • Premium Income

– Both policies pay premiums at the beginning of each year: – $1,500 + $600 = $2,100

• Investment Income – Actual Assets * Actual rate of return – ($5,420 + $1,500 + $600) * 7% = $526

• Claims – Policy 1 dies: $100,000.

• Change in Reserves – Closing Reserve – Opening Reserve – = ($0 + Policy 2 PfADed Rsv @2010/12/31) – $5,420 – = $2,059 – $5,420 – = -$3,361

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

21

Example: Solution to Part A

Policy 2 was born Dec 31, 1938. On Dec 31, 2011 life turned 73 years old. Policy could have died on Dec 31, 2011 and 2012 before policy expires on Dec 31, 2012. Policy 2 PfADed Rsv @ 2010/12/31: = PV (DB) – PV (Premium) = $50,000 * ( ( q(73) * 1.1 ) / (1+i) + (1 – ( q(73) * 1.1 ) ) * ( q(74) * 1.1 ) / (1+i)^2 ) - $600 * ( 1 + (1 – ( q(73) * 1.1) ) / (1+i) ) = $3,211.60 – $1,152.57 = $2,059

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

22

Example: Solution to Part A

While we’re here, calculate the best estimate reserve and PfADs for Pol. 2: Policy 2 B/E Rsv @ 2010/12/31: = PV (DB) – PV (Premium) = $50,000 * ( q(73) / (1+i) + (1 – q(73) ) * q(74) ) / (1+i)^2 ) - $600 * ( 1 + (1 – q(73) ) / (1+i) ) = $2,924.26 – $1,154.29 = $1,770 PfADs = PfADed Rsv – B/E Rsv = $2,059 – $1,770 = $289

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

23

Example: Solution to Part A

While we’re here, calculate the PfADed and B/E Reserves for Policy 1: Policy 1 PfADed Rsv @ 2010/12/31: = $100,000 * (q(72) * 1.1 / (1+i)) - $1,500 * ( 1 ) = $2,933 – $1,500 = $1,433 Policy 1 B/E Rsv @ 2010/12/31: = $100,000 * (q(72) / (1+i)) - $1,500 * ( 1 ) = $2,667 – $1,500 = $1,167 PfADs = PfADed Rsv – B/E Rsv = $1,433 – $1,167 = $267

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

24

Example: Summary

Policy 1 Best-Est PfAD Total 2009/12/31 $2,153 $500 $2,653 2010/12/31 $1,167 $267 $1,433 Policy 2 Best-Est PfAD Total 2009/12/31 $2,372 $395 $2,767 2010/12/31 $1,770 $289 $2,059

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

25

Example: Solution to Part A

Income Statement Premium $2,100 Investment Income $526 Revenue $2,626 Benefits $100,000 Change in Reserves -$3,361 Dispositions $96,639 Net Income -$94,013

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

26

Example: Additional Question

Exercise: Construct the best estimate Income Statement: Premium Income

= $1,500 + $600 = $2,100 Investment Income

= ($5,420 + $1,500 + $600) * 5% = $376 Expected Claims = 0.027 * $100,000 + 0.028 * $50,000 = $4,100 Expected Change in Reserves

= ((0.973 * $1,433) + (0.972 * $2,059)) - $5,420 = $3,396 - $5,420 = -$2,024

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

27

Example: Additional Question

B/E Income Statement Premium $2,100 Investment Income $376 Revenue $2,476 Benefits $4,100 Change in Reserves -$2,024 Dispositions $2,076 Net Income $400

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

28

Example: Homework Questions

What does the Income Statement look like if: • Policy 1 survives but Policy 2 dies on Dec 31, 2010? • Both Policies survive? • Both Policies die on Dec 31, 2010 • How would these income statements reflect lapses?

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

29

Example: Solution to Part B

Part B – Create an SOE Expected change in PfADs: = Rsv(0) - [ tPx * Rsv(1) ] = ($500 + $395) - ((0.973 * $267) + (0.972 * $289)) = $895 - $540 = $355 Interest on PfADs: = ($500 + $395) * 5% = $45 Expected Earnings on In-Force: = Expected PfAD Release + Interest on PfADs = $355 + $45 = $400 Question: Where have we seen this $400 before?

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

30

Example: Solution to Part B

Investment Experience Gain/Loss = Actual Investment Income – Expected Investment Income = ($5,420 + $1,500 + $600) * (0.07 – 0.05) = $150

Mortality Experience Gain/Loss = (Expected Benefits – Expected Reserve Release) – (Actual Benefits - Actual Reserve Release) Expected Benefits = (0.027 * $100,000) + (0.028 * $50,000) = $2,700 + $1,400 = $4,100 Actual Benefits = $100,000

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

31

Example: Solution to Part B

Expected Reserve Release = qx(b/e) * B/E Rsv at End of Period = (0.027 * $1,167) + (0.28 * $1,770) = $81 Actual Reserve Release = (1 * $1,167) + (0 * $1,770) = $1,167 Mortality Gain / Loss = ($4,100 – $81) – ($100,000 – $1,167) = -$94,814

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

32

Example: Solution to Part B

Gain/Loss in PfADs: = Expected PfADs - Actual PfADs = ((0.973 * $267) + (0.972 * $289)) - ((0 * $267) + (1 * $289)) = $541 - $289 = $252 Note: if we had used reserves with PfADs (and not best estimate reserves) in the

calculation of Mortality Gain/Loss there would be no outstanding G/L on PfADs.

Question: what would be the rationale for aggregating all the PfAD G/L as one item

rather than embedding them in the respective source? Question: why would some want to report G/L on PfADs separately? What is different

between PfADs and Best-Estimate Reserves?

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

33

Example: Solution to Part B

SOE Report Expected Profit on In-force Operations $400 Impact of New Business $0 Investment $150 Mortality -$94,814 PfAD $252 Experience Gains & Losses -$94,412 Unexplained $0 Net Income -$94,012

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

34

Example: Solution to Part B

SOE (CIA Sample) Expected Profit on In-force Operations $400 Impact of New Business $0 Experience Gains & Losses -$94,412 Changes in Best Estimate Assumptions and Other Changes $0 Earnings on Operations Before Taxes -$94,012 Earnings on Surplus $0 Net Income Before Taxes $0 Less: Taxes $0 Net Income Before Minority Interests -$94,012 Less: Minority Interests $0 Net Income -$94,012

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

35

Example: Additional Exercise

What would our Best-Estimate Income Statement look like if we split out Expected Earnings on In-force from Revenues and Dispositions? That is: take the Income Statement from Page 25 and morph it into a Source of Earnings Statement.

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

36

Example: Additional Exercise

Income Statement (from Page 25) Premium $2,100 Investment Income $376 Revenue $2,476 Benefits $4,100 Change in Reserves -$2,024 Dispositions $2,076 Net Income $400

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

37

Example: Additional Exercise

From page 28: Expected Earnings on In-Force: = Expected PfAD Release + Interest on PfADs = $355 + $45 = $400 Change in Reserves + Expected PfAD Release (Watch the signs!) = -$2,024 + $355 = -$1,669 Investment Income – Interest on PfADs = $376 - $45 = $331

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

38

Example: Additional Exercise

Premium $2,100 Best-Est $331 PfAD $45

Investment Income $376 Revenue $2,476 Benefits $4,100 Best-Est -$1,669 PfAD -$355

Change in Reserves -$2,024 Dispositions $2,076 Net Income $400

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

39

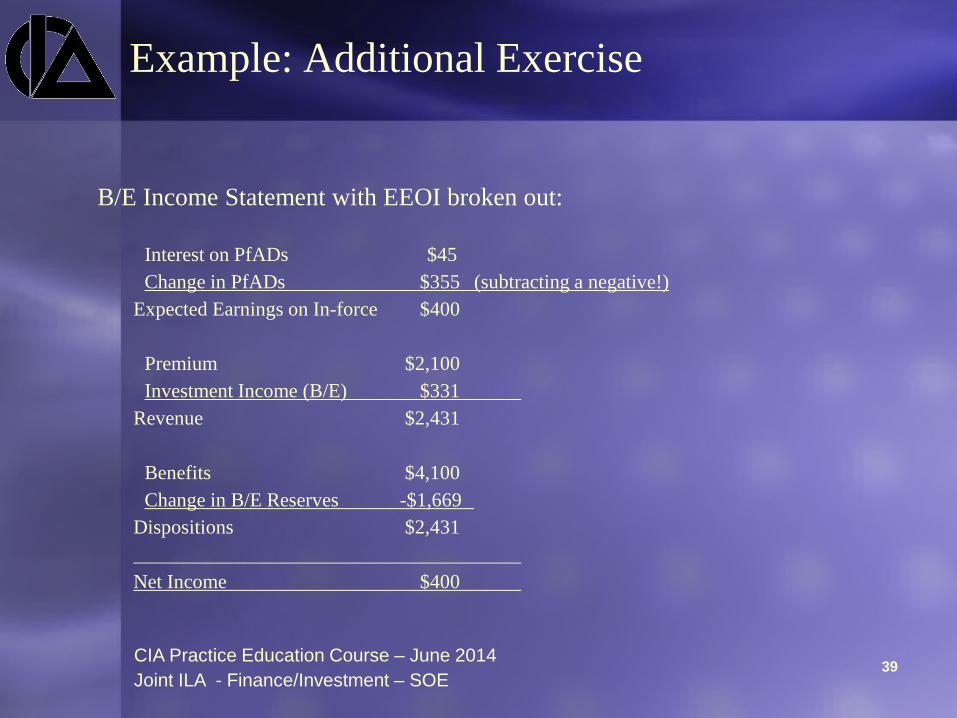

Example: Additional Exercise

B/E Income Statement with EEOI broken out: Interest on PfADs $45 Change in PfADs $355 (subtracting a negative!) Expected Earnings on In-force $400 Premium $2,100 Investment Income (B/E) $331 Revenue $2,431 Benefits $4,100 Change in B/E Reserves -$1,669 Dispositions $2,431 Net Income $400

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

40

Example: Additional Exercise

More like an SOE: Interest on PfADs $45 Change in PfADs $355 Expected Earnings on In-force $400 Premium $2,100 Investment Income (B/E) $331 Benefits -$4,100 Change in B/E Reserves $1,669 Other $0 Net Income $400

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

41

Example: a different perspective

So where did all the change in reserves go in the SOE? Income Statement Opening Closing Change PfADs $896 $289 -$607 Best Estimate $4,524 $1,770 -$2,754 Total Reserve $5,420 $2,059 -$3,341

Source of Earnings Opening Closing Change Expected Change in B/E Rsv $4,524 $2,856 -$1,669 Mortality G/L (Rsv only) - ($81 - $1,167) -$1,086 Best Estimate Rsv $4,524 $1,770 -$2,754 EEOI (PfAD Rsv only) $896 $541 -$355 PfAD G/L - -$252 -$252 PfADs $896 $289 -$607

Question: where does the “Expected Change in Reserves” appear in the SOE calculation? Hint: $1,669 + $355 = $2,024

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE

42

Example: More Homework

Build Source of Earnings for to match the Income Statements you calculated for the Homework on page 28.

CIA Practice Education Course – June 2014 Joint ILA - Finance/Investment – SOE