Solvency and Licensing Update - Stewart

33

Solvency and Licensing Update Charlie Craig Senior Vice President Associate General Counsel SW States Regional Counsel

Transcript of Solvency and Licensing Update - Stewart

Solvency and

Licensing Update

Charlie Craig Senior Vice President

Associate General Counsel

SW States Regional Counsel

Why Solvency?

1. Title companies licensed in Texas have the public’s trust;

handle more than a billion dollars of other people’s money

every year and provide title insurance needed for people to

buy, sell and loan money on Texas real estate.

2. The size and growth of the Texas real estate market and the

regulated environment encouraged more and more agents to

establish companies in Texas.

3. The automation of title plants and use of subscriptions rather

than plant ownership aided more agents to get into the title

business in Texas.

4. Then the 2008-09 economic downturn hit…

• Despite audits by TDI and underwriters, some agents

(and one underwriter) failed for a variety of reasons:

- Fraud, theft, poor business practices and in some cases the

downturn(s) in the economy

- Incompetency

• To maintain the public’s (including the legislature and the

TDI’s) trust, minimum solvency standards for agents

were needed.

Why Solvency?

• United Title was a subsidiary of a Colorado agent. It grew rapidly

in Texas and was solvent on its own.

• However, the parent company ran into financial trouble and its

bank froze its funding, causing the parent to eventually file

bankruptcy.

• Even though United Title was solvent, its parent shut down United

Title on one Friday and fired all of its employees on the spot.

• Since United Title itself was NOT insolvent and its escrow

accounts were still in tact, Texas Title Insurance Guaranty

Association (TTIGA) had no authority at that time to get

involved. Greater authority for TTIGA was needed …

Why Solvency? The United Title Failure

• Broad re-write based on TDI–appointed Study Committee’s

Report to the TDI Commissioner and made important changes

to the then existing law.

• Bill was a cooperative effort by Stewart Title Guaranty

Company, the Texas Land Title Association, the Texas Title

Guaranty Association and Texas Insurance Department over

legislative sessions and changes to TDI leadership and staff.

• Among other changes, introduced the idea to require proof of

Agent Capitalization and Solvency to do business in Texas.

HB 4338

• Stewart’s Solvency Bulletin TX 2014001

• TDI Adm Rule S.1, Minimum Capitalization Standards for Title

Agents and Certification and Procedure to Determine Value of

Assets including the timetables and capitalization amounts

• Insurance Code, Sections 2651.012, 2651.158 and 2651.012.

• TDI Commissioner’s Order 2806

Solvency Requirements - Where to Start

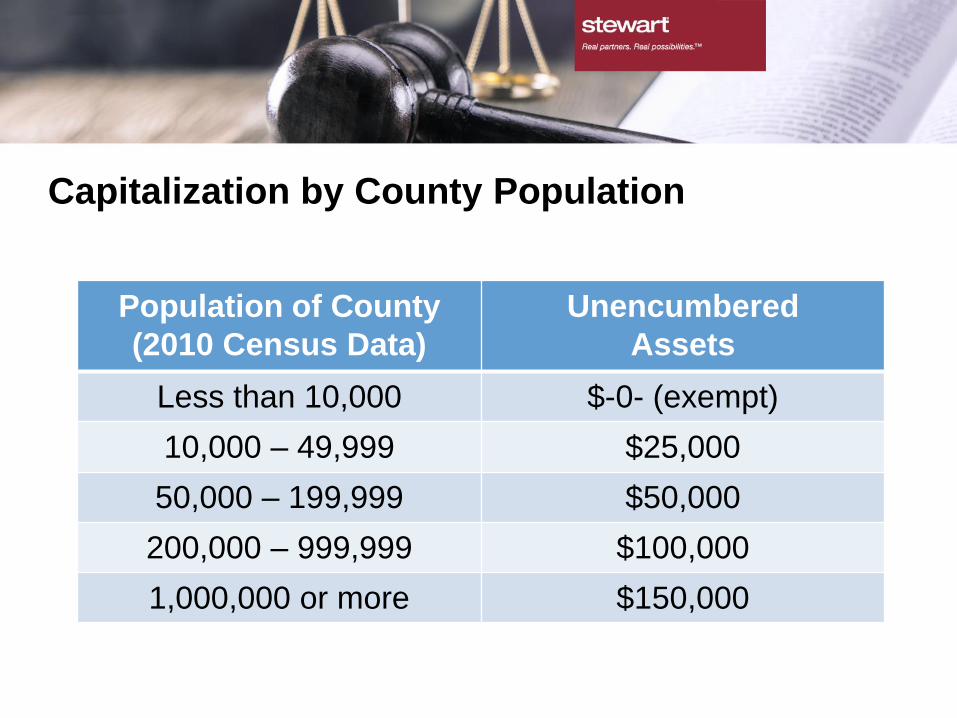

• A title agent must always maintain unencumbered assets with

a market value in excess of liabilities, exclusive of abstract

plants, as specified in Section 2651.012(c).

• Depending on the length of time an agent has been licensed

and the size of the largest county in which the agent maintains

a principal office, there are five different levels of

capitalization that range from $0 (Exempt) to $150,000

– (see chart, next slide).

• An agent that maintains a principal office in more than one

county must meet the asset standards for the largest county

for which the agent maintains a principal office.

Solvency and Capitalization

Capitalization by County Population

Population of County

(2010 Census Data)

Unencumbered

Assets

Less than 10,000 $-0- (exempt)

10,000 – 49,999 $25,000

50,000 – 199,999 $50,000

200,000 – 999,999 $100,000

1,000,000 or more $150,000

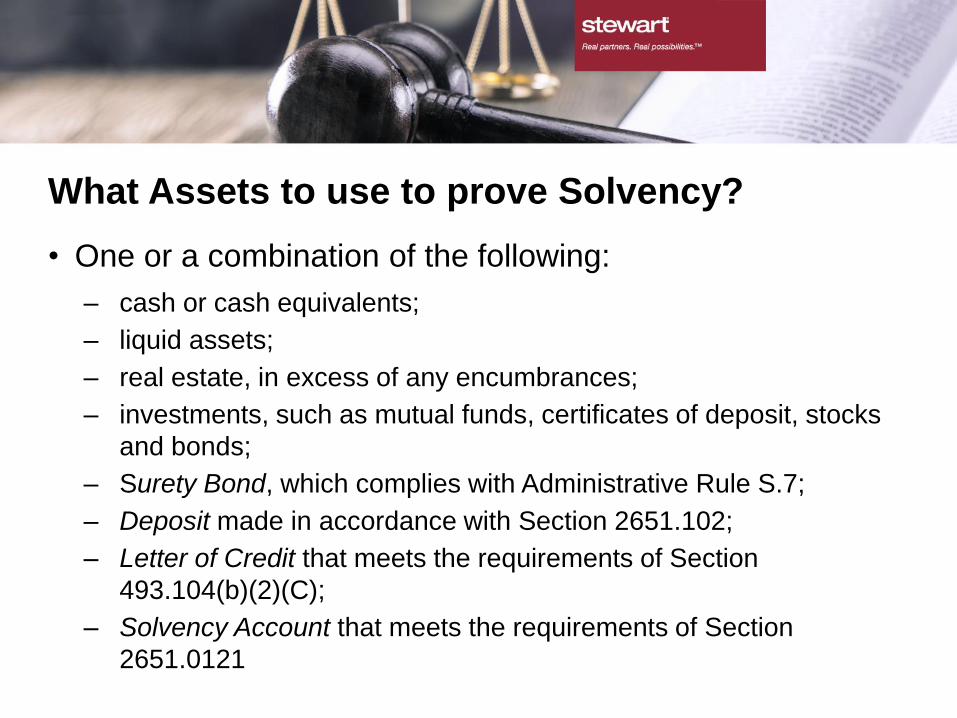

• One or a combination of the following:

– cash or cash equivalents;

– liquid assets;

– real estate, in excess of any encumbrances;

– investments, such as mutual funds, certificates of deposit, stocks

and bonds;

– Surety Bond, which complies with Administrative Rule S.7;

– Deposit made in accordance with Section 2651.102;

– Letter of Credit that meets the requirements of Section

493.104(b)(2)(C);

– Solvency Account that meets the requirements of Section

2651.0121

What Assets to use to prove Solvency?

• TDI Adm Rule S.1 set forth the original schedule for compliance

with the minimum capitalization standards and ranges from

immediate compliance for new agents and to up to 9 years

(11/1/2022) based on the number of years the agent has held a

license in the State of Texas as of 9/1/2013.

• An agent just starting up or which has not been licensed since

9/1/2013 must reach the amount for their county immediately.

• An agent licensed before 9/1/2013 had the number of years it

was licensed as of 9/1/2013, up to 9 years to comply.

• An agent that merged with an agent licensed older than it, had

the number of years the older company had.

Original Dates To Comply

Original Dates To Comply

# of Years

Texas License

Held

Deadline for Full

Compliance

(From 9/1/13)

# of Yrs. To

Reach Full

Compliance

% of Asset

Amount Needed

Each Year

Less than 3 Immediately 0 100%

>3 but <4 November 1, 2016 3 33%

>4 but <5 November 1, 2017 4 25%

>5 but <6 November 1, 2018 5 20%

>6 but <7 November 1, 2019 6 16.66%

>7 but <8 November 1, 2020 7 14.29%

>8 but <9 November 1, 2021 8 12.5%

>9 years November 1, 2022 9 11.11%

• T-S1 designates how the agency has complied with the

unencumbered asset requirement.

• T-S1 does not require proof to be submitted with the

form; but TDI may follow up with the agent to request

additional information regarding the integrity of the assets

being pledged. This information likely requested during

the regular TDI audit.

• T-S1 can be found on the TDI website at

www.tdi.texas.gov.

Form T-S1, Title Agent’s Unencumbered Assets

Certification Form

• The initial T-S1 certification must be submitted to TDI with the agent’s

first annual audit of escrow accounts (depending on the agent’s

fiscal year end).

• The subsequent annual T-S1 certification must be submitted annually

between September 1 and September 30 of each year to TDI for the

preceding calendar year (irrespective of the agent’s fiscal year end).

NOTE: late reports will subject you to TDI fines.

• TDI Adm Rule S.1 details the start dates/reports for instances of

changes in ownership, acquiring an agency through inheritance,

merger, and consolidation.

T-S1 Certification, When And How

• Determine your minimum capitalization level, schedule for immediate

compliance and the method(s)/assets you will use to meet the minimum

capitalization requirement.

• A title agent that applies for its first license and does not elect to create a

Solvency Account, it shall be required to meet 100% of the required

capitalization up front by: (1) hold unencumbered assets or (2) make a

deposit in the amount of specified under the Rule or (3) provide a bond in

the form created in S-7 as a condition precedent to the issuance of a new

license.

• The initial filing of Form T-S1 will normally accompany the annual audit of

escrow accounts submitted to TDI (the exact date depends on the agent’s

fiscal year end), unless the agent makes a deposit under Insurance Code

§2651.012(f).

• Subsequent filings of T-S1 must be submitted annually between

September 1 and September 30 (irrespective of the agent’s fiscal year end).

What New Agents Should Do

Under TDI Adm. Rule S.2, a Solvency Account can be set up using

Form T-S2 to meet the requirements. Form T-S2, is a Tripartite

Agreement that must be executed by the agent, the agent’s bank and

TDI.

• If creating a Solvency Account, the agency must deposit into the

account a portion of the agent’s portion of the premium (the greater

of 1% or $5) from each transaction. Note: Policies in excess of

$59,500 will require 1% of the premium ($59,500= $585x85%=

$550.65 *1%=$5.50 rounded to $5.00).

• Deposits must be made to the Solvency Account quarterly (within 31

days of the end of each calendar quarter). Best to do it on each

policy as issued. There is no set deadline for reaching the required

level of funds (required by Sec. 2651.012).

Rule S.2: Solvency Account as an Option

• Another one of the several approved methods of obtaining

solvency levels is a surety bond.

• TDI has to approve the bond form.

• Bond companies during the Recession didn’t want to issue.

Things have now changed to make this a real option.

See, TDI Adm. Rule S.7, Surety Bond for Title Agents to Comply

with Minimum Capitalization Standards and Texas Title Insurance

Agent’s Minimum Capitalization Bond form.

Rule S.7: Surety Bond as an Option

Under TDI Adm. Rule S.3, an agent can request and obtain the release of

assets, including funds held in a solvency account thru Form T-S3. You

still have to annually prove solvency from a different source(s).

• What you should know:

– Use Form T-S3 for requests to release funds; however funds will

only be released at the discretion of TDI.

– Form T-S3 provides a checklist for the actions required to request

a release.

– No funds can be returned to an agent that has ceased operations

unless the TDI agrees to release the funds.

– Solvency Account can earn interest, collectable after agent

reaches the required level of capitalization (Rule S.2-E)

Rule S.3: Solvency Account Release Agreement

• TDI Adm. Rule S-5, Filing of Title Agent’s Certification of Quarterly

Tax Report. Good indicator of solvency…

• Quarterly (w/in 45 days thereafter), every title agent and direct

operator must submit a copy of their quarterly payroll tax report

(941) to TDI, attached to Form T-S5 and evidence that the taxes

were paid (example: cancelled check or receipt of payment).

• The remittance form must indicate whether or not the agent has

employees. If no employees, must show no material change in

financial condition on the Form T-S5.

• Can be submitted electronically and information regarding submitting

the information electronically can be found on TDI’s website.

Rule S.5: IRS Withholding Report

• Guaranty fee imposed on every title policy issued in Texas by TTIGA. (Note: TTIGA

Board set a $5 fee originally, reduced to $0 in 2014, then back to $3 in effective April 1,

2016). See, Stewart Bulletin TX 2016002.

• TDI must notify TTIGA when an agent is determined to be “impaired”.

• TTIGA must pay from guaranty fund TDI expenses to examine and audit impaired agent.

• TTIGA can advance funds to pay expenses of administering an impaired agent.

• No entity that has gone through impairment can resume business until it repays TTIGA’s

expenses.

• All owners, directors and employees of a impaired agent have a legal duty to

cooperate with TTIGA and provide access to offices, files and electronic storage.

– Failure to cooperate = sanctions by the TDI!

• TTIGA can employ or retain persons to assist it in winding up an impaired agent to:

• i. Close real estate transactions

• ii. Disburse escrow funds

• iii. Record documents

• iv. Issue final title insurance policies.

TTIGA Expansion

a. Each title insurance company shall provide annually to the department a list

of officers authorized to provide TDI with financial solvency information on

an agent. See, Rule S-4; Form T-S 4 and T-S4-A.

b. Financial solvency information on an agent provided to TDI is not considered

to be “public information”, but TDI may disclose financial information

received to a title insurance company that has appointed, or that is

considering appointing, the title agent.

c. TDI may also release financial solvency information received under this

subsection to a title agent under Section 2651.206, Insurance Code, if the

information is evidence on which an audit report or examination report relies.

d. A title insurance company that receives financial solvency information may

not release the information except under a subpoena issued by a court of

competent jurisdiction.

– TDI Rules and Forms: S.4; T-S4, Disclosure Form T-S4-A

Exchanging Agent Information

• Files kept in agent offices or in storage must be made

available to the underwriters of an agent and to TTIGA for

copying during normal business hours and for up to 60

days in case an agent fails.

• United Title failure - TDI had to send armed Marshalls to

landlords to gain access to offices for itself and the

underwriters.

File Availability

• United Title owed many agents and underwriters for premiums

due. That portion of the premium was not under state control and

could have been claimed by the parent’s bankruptcy trustee.

• Now, premiums owed for division of premium under P-24 are to

be held in trust, but doesn’t require a separate trust account.

The purpose of placing the funds into trust is to enhance the

status of the funds in case of the failure of the agent.

• If you set up a separate account for underwriter premiums, TDI

cannot audit that account other than to see the amount of funds

that were placed into the account and correlate those funds to

underwriting premiums earned.

Premiums Held In Escrow

• All title plants, new and old must have an inception date

of at least January 1, 1979.

• As per 2009 study, TDI found that a large % of Texas title

plants already went back to sovereignty or had inception

dates older than 1961.

• So the impact of requiring a 1979 inception date was

marginal, but added immediate value to the ownership,

lease/subscription of a title plant.

P-1, P-12 : Imposing a 1979 Inception Date

on Texas Title Plants

In the past, title agents were licensed only through their underwriters so each held a

separate license for each underwriter.

Starting in 2014, the agents are licensed directly with TDI and the underwriters are

appointed onto the agent’s license. An agent must be appointed by at least one underwriter

to receive the initial license.

To engage in the business of title insurance in a particular county, a title agent must:

– be issued a license under Rule L-1.I. (file long form FINT143*, pay the $50 fee)

and comply with the requirements for maintaining that license in an active status,

– possess a valid, active appointment for that county from a title insurance

company's appointing official, and

– own or lease, and control an abstract plant, or participate in a bona fide joint

abstract plant operation in that county.

* Includes biographical info, business entity info/ filings, initial underwriter

appointment form, bond/deposit/letter of credit

Agent Licensing

Licenses last 2 years after date of issuance. To Renew:

• File Renewal Form FINT03, pay fee ($35)

• Must Verify:

– Form of business of the entity renewing

– Unencumbered Asset/solvency verification

– Reporting history with TDI, Audit history, past history, criminal history

– Continuing Education, Training Requirements

• Franchise Tax Account Status/ Confirm Franchise Tax Public Information

Report

Non-compliance = disciplinary action including revocation/non-renewal of agent

license, issue cease and desist order, administrative penalties, and ordering

restitution

See, Adm. Rule L-1 for Agents

Agent Licensing - Renewals

• New management personnel, including title managers,

officers, directors, shareholders who manage or administer the

day to day operations have one year to take a professional

training course for title agent management personnel if they

have not taken it before becoming an on-site manager, or did

not previously have five years’ experience as a Texas title

agency manager.

• The idea is that incoming agents to Texas need to understand

our laws and regulations and how to run a Texas company.

New Agent Initial Education

The education must be provided by the same providers

established in P-28 and must cover:

(1) the basic principles and coverages related to title insurance;

(2) recent and prospective changes in those principles and

coverages;

(3) applicable rules and laws;

(4) proper conduct of the license holder's title insurance business;

(5) accounting principles and practices and financial responsibilities

and practices relevant to title insurance; and

(6) the duties and responsibilities of a title insurance agent.

New Agent Initial Education

Agent Continuing Education

LICENSE PERIOD Total Required Hours Ethics

Less than 4 months 0 0

4 months up to and including 6 months 4 0

7 months up to and including 9 months 5 0

10 months up to and including 12 months 6 1

13 months up to and including 15 months 7 1

16 months up to and including 18 months 8 1

19 months up to and including 21 months 9 1

22 Months or more 10 1

• Title agent(s) or Direct Operation(s) appoint, bond, and apply for each

escrow officer’s license under their employment. Some escrow officers have

multiple escrow officer licenses, one for each title agency they work with.

• HB2492 passed effective Sept.1, 2015, amended Ins. Code, Section

2652.051(a), to require the individual escrow officer, rather than title

insurance agent or direct operation, to file an application for an escrow

officer's initial license with TDI (Form FINT132), while still requiring

appointment and bonding (FINT123) by the title insurance agent or direct

operation.

• Thus, the individual escrow officer will have one license that they must

maintain and then be appointed and bonded by Agent/DO.

• TDI will not enforce the provisions of HB 2491 until changes have been

made to the Texas Title Insurance Manual by rule, to be completed during

the summer of 2016. See also, Rule L-2

Change in Escrow Officer Licensing

• Escrow Officers are allowed to live in an adjoining state so long as they have

a bona fide job with a licensed Texas Agent

• Escrow Officer bond for such bi-state escrow officers is now $10,000, up

from $5,000.

• In-state escrow officer bond remains $5,000.

• If agent has more than 10 total escrow officers appointed, bond cannot be

more than $50,000 total.

Escrow Officer Licensing Bonds

• Escrow officers have similar education requirements

• All escrow officers licensed for at least 10 months must

complete 6 or more hours of continuing education, depending

on the length of time licensed. Basic Manual, P-28.A.3.

• Those hours must include at least 1 hour of ethics.

• To meet the Ethics requirements, course must be accredited

by either TDI or the State Bar of Texas.

Escrow Officer Continuing Education

Stewart Title Guaranty Company

Charlie Craig

Senior Vice President

Associate General Counsel

SW States Regional Counsel

(512) 236-0405

Be Careful Out There