Solutions to Exercises

31

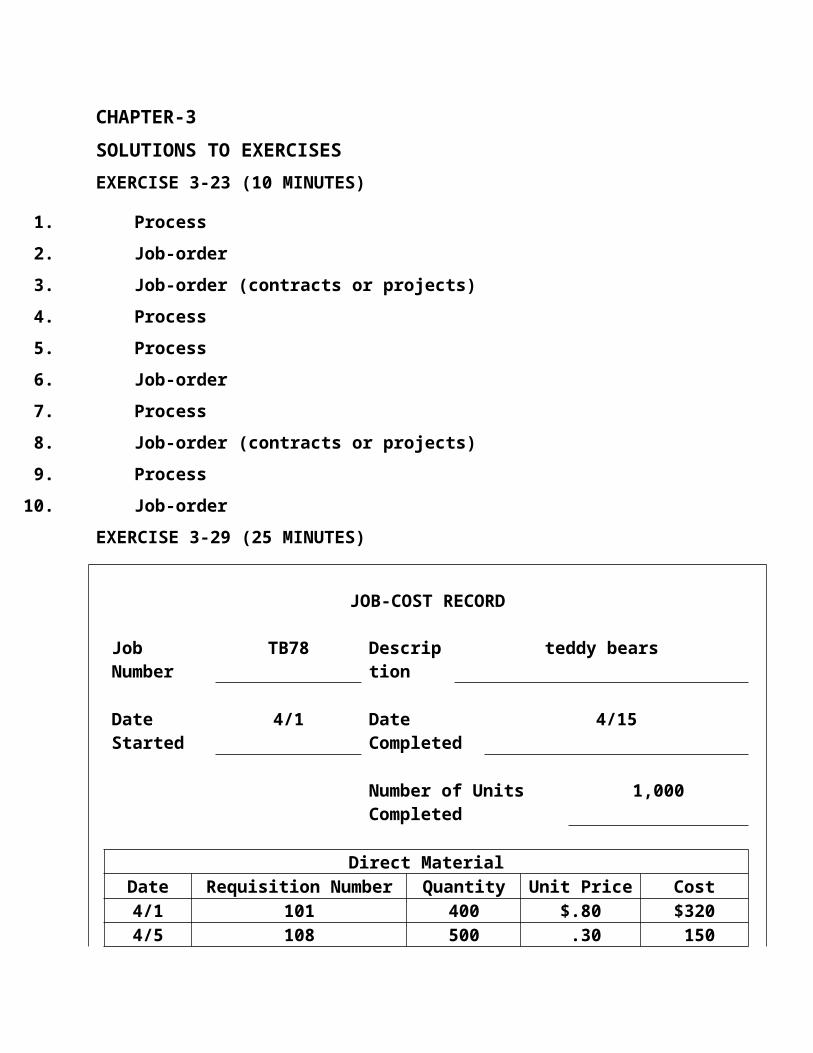

CHAPTER-3 SOLUTIONS TO EXERCISES EXERCISE 3-23 (10 MINUTES) 1. Process 2. Job-order 3. Job-order (contracts or projects) 4. Process 5. Process 6. Job-order 7. Process 8. Job-order (contracts or projects) 9. Process 10. Job-order EXERCISE 3-29 (25 MINUTES) JOB-COST RECORD Job Number TB78 Descrip tion teddy bears Date Started 4/1 Date Completed 4/15 Number of Units Completed 1,000 Direct Material Date Requisition Number Quantity Unit Price Cost 4/1 101 400 $.80 $320 4/5 108 500 .30 150

-

Upload

gauatam-tosh -

Category

Documents

-

view

271 -

download

0

Transcript of Solutions to Exercises

CHAPTER-3

SOLUTIONS TO EXERCISES

EXERCISE 3-23 (10 MINUTES)

1. Process

2. Job-order

3. Job-order (contracts or projects)

4. Process

5. Process

6. Job-order

7. Process

8. Job-order (contracts or projects)

9. Process

10. Job-order

EXERCISE 3-29 (25 MINUTES)

JOB-COST RECORD

Job Number TB78 Description teddy bears

Date Started 4/1 Date Completed 4/15

Number of Units Completed 1,000

Direct MaterialDate Requisition Number Quantity Unit Price Cost4/1 101 400 $.80 $3204/5 108 500 .30 150

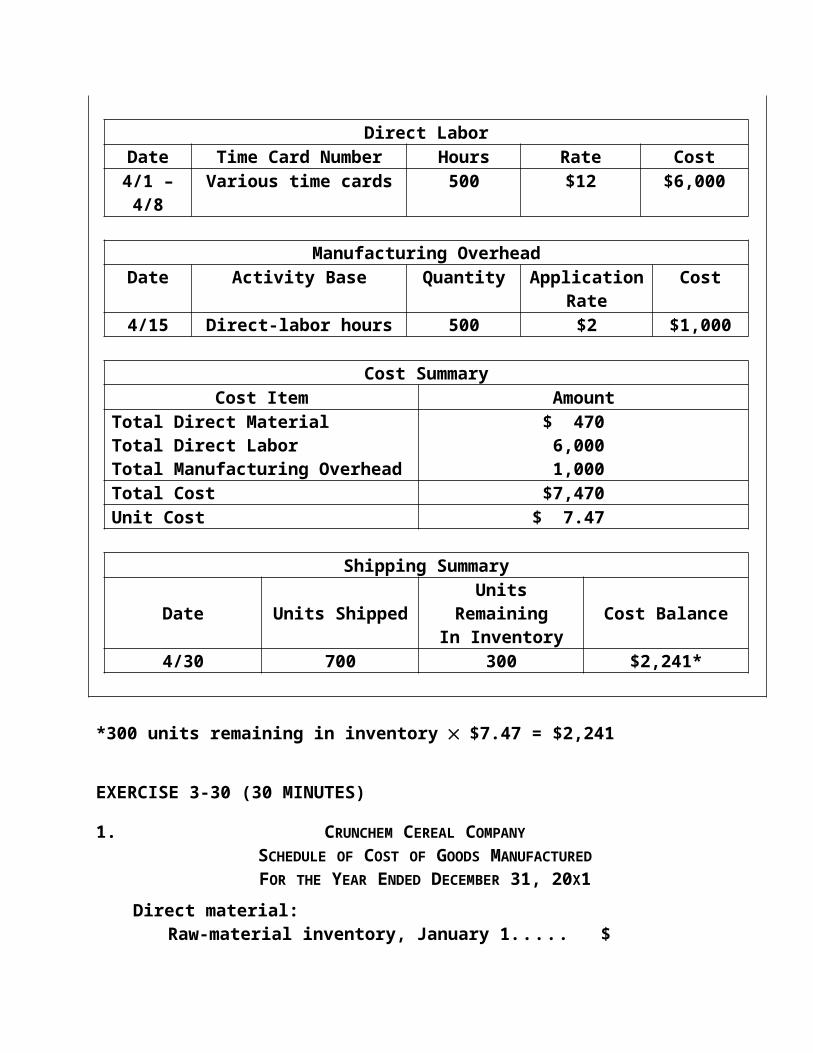

Direct LaborDate Time Card Number Hours Rate Cost

4/1 – 4/8 Various time cards 500 $12 $6,000

Manufacturing OverheadDate Activity Base Quantity Application Rate Cost4/15 Direct-labor hours 500 $2 $1,000

Cost SummaryCost Item Amount

Total Direct MaterialTotal Direct LaborTotal Manufacturing Overhead

$ 4706,0001,000

Total Cost $7,470Unit Cost $ 7.47

Shipping Summary

Date Units ShippedUnits Remaining

In Inventory Cost Balance4/30 700 300 $2,241*

*300 units remaining in inventory$7.47 = $2,241

EXERCISE 3-30 (30 MINUTES)

1. CRUNCHEM CEREAL COMPANY

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE YEAR ENDED DECEMBER 31, 20X1

Direct material:Raw-material inventory, January 1...........................................$ 30,000Add: Purchases of raw material................................................ 278,000Raw material available for use..................................................$308,000Deduct: Raw-material inventory, December 31....................... 33,000Raw material used...................................................................... $275,000

Direct labor.......................................................................................... 120,000

Manufacturing overhead 252,000 *Total manufacturing costs................................................................. $647,000

Add: Work-in-process inventory, January 1..................................... 39,000 Subtotal................................................................................................ $686,000

Deduct: Work-in-process inventory, December 31.......................... 42,900 Cost of goods manufactured............................................................. $643,100

*Applied manufacturing overhead is $252,000 ($120,000210%). Actual manufacturing overhead is also $252,000, so there is no overapplied or underapplied overhead.

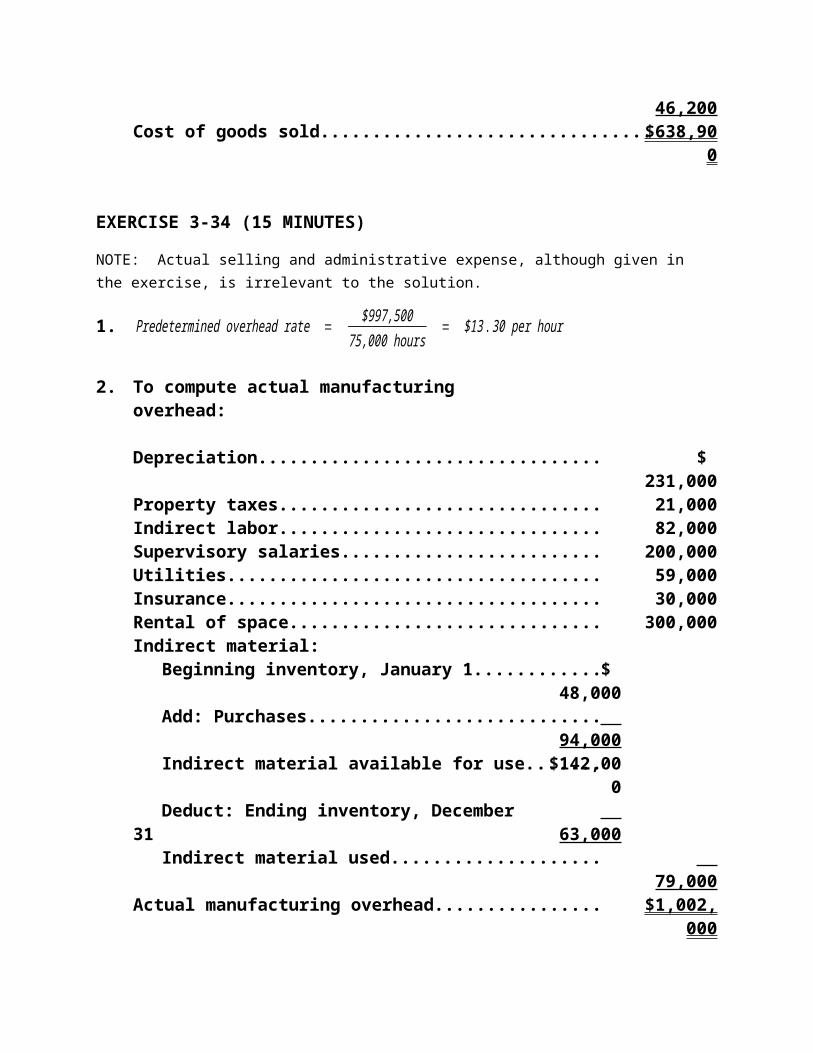

2. Finished-goods inventory, January 1..................................................................... $ 42,000Add: Cost of goods manufactured......................................................................... 643,100Cost of goods available for sale............................................................................. $685,100Deduct: Finished-goods inventory, December 31................................................. 46,200Cost of goods sold................................................................................................... $638,900

EXERCISE 3-34 (15 MINUTES)

NOTE: Actual selling and administrative expense, although given in the exercise, is irrelevant to the solution.

1. Predetermined overhead rate = $997,500

75,000 hours = $13 . 30 per hour

2. To compute actual manufacturing overhead:

Depreciation................................................................................................. $ 231,000Property taxes.............................................................................................. 21,000Indirect labor................................................................................................ 82,000Supervisory salaries.................................................................................... 200,000Utilities.......................................................................................................... 59,000Insurance...................................................................................................... 30,000Rental of space............................................................................................ 300,000Indirect material:

Beginning inventory, January 1..........................................................$ 48,000Add: Purchases.................................................................................... 94,000Indirect material available for use.......................................................$142,000Deduct: Ending inventory, December 31........................................... 63,000Indirect material used.......................................................................... 79,000

Actual manufacturing overhead................................................................. $1,002,000

actual appliedOverapplied = manufacturing – manufacturing

Overhead overhead overhead

= $1,002,000 – ($13.3080,000*) = $62,000

*Actual direct-labor hours.

3. Manufacturing Overhead............................................................. 62,000Cost of Goods Sold........................................................... 62,000

EXERCISE 3-35 (20 MINUTES)

NOTE: Budgeted sales revenue, although given in the exercise, is irrelevant to the solution.

1. Predetermined overhead rate =budgeted manufacturing overheadbudgeted level of cost driver

(a)$364,00010,000 machine hours

= $36.40 per machine hour

(b)$364,00020,000 direct-labor hours

= $18.20 per direct-labor hour

(c)$364,000$280,000*

= $1.30 per direct-labor dollar or 130%of direct-labor cost

*Budgeted direct-labor cost = 20,000$14

2. Actualmanufacturing

overhead–

appliedmanufacturing

overhead=

overapplied orunderapplied

overhead

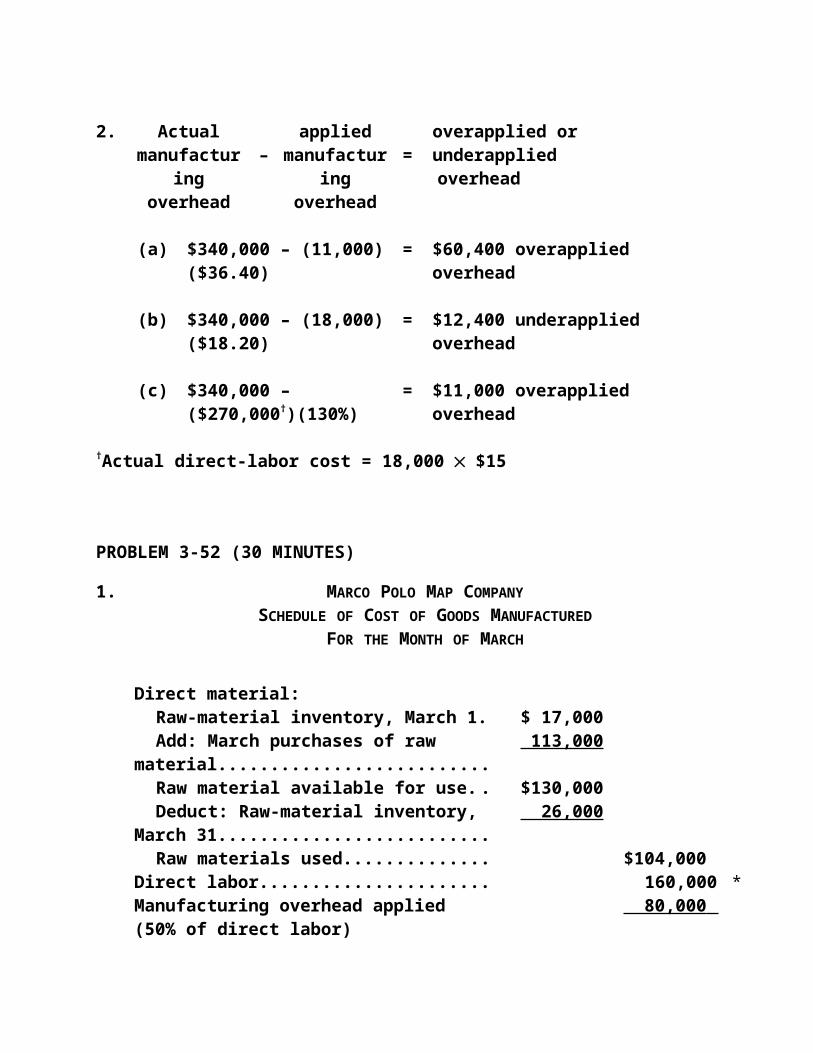

(a) $340,000 – (11,000)($36.40) = $60,400 overapplied overhead

(b) $340,000 – (18,000)($18.20) = $12,400 underapplied overhead

(c) $340,000 – ($270,000†)(130%) = $11,000 overapplied overhead

†Actual direct-labor cost = 18,000$15

PROBLEM 3-52 (30 MINUTES)

1. MARCO POLO MAP COMPANY

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE MONTH OF MARCH

Direct material:Raw-material inventory, March 1.............................. $ 17,000Add: March purchases of raw material................... 113,000Raw material available for use................................. $130,000Deduct: Raw-material inventory, March 31............. 26,000Raw materials used................................................... $104,000

Direct labor...................................................................... 160,000 *Manufacturing overhead applied (50% of direct labor) 80,000 Total manufacturing costs............................................. $344,000

Add: Work-in-process inventory, March 1.................... 40,000 Subtotal............................................................................ $384,000

Deduct: Work-in-process inventory, March 31 (90%$40,000)......................................... 36,000

Cost of goods manufactured......................................... $348,000 †

*Work upward from the bottom of the statement, using the information available. Direct labor + manufacturing overhead = total manufacturing costs – direct material cost = $344,000 – $104,000 = $240,000. Since manufacturing overhead = 50% of direct labor, then manufacturing overhead = $80,000 and direct labor = $160,000.

†Cost of goods manufactured = cost of goods sold + increase in finished-goods inventory = $345,000 + $3,000 = $348,000.

PROBLEM 3-52 (CONTINUED)

2. MARCO POLO MAP COMPANY

SCHEDULE OF PRIME COSTS

FOR THE MONTH OF MARCH

Raw material:Beginning inventory.................................................................... $ 17,000Add: Purchases............................................................................ 113,000Raw material available for use.................................................... $130,000Deduct: Ending inventory........................................................... 26,000

Raw material used................................................................................ $104,000Direct labor............................................................................................ 160,000Total prime costs.................................................................................. $264,000

3. MARCO POLO MAP COMPANY

SCHEDULE OF CONVERSION COSTS

FOR THE MONTH OF MARCH

Direct labor.............................................................................................. $160,000Manufacturing overhead applied (50% of direct labor)....................... 80,000Total conversion cost............................................................................. $240,000

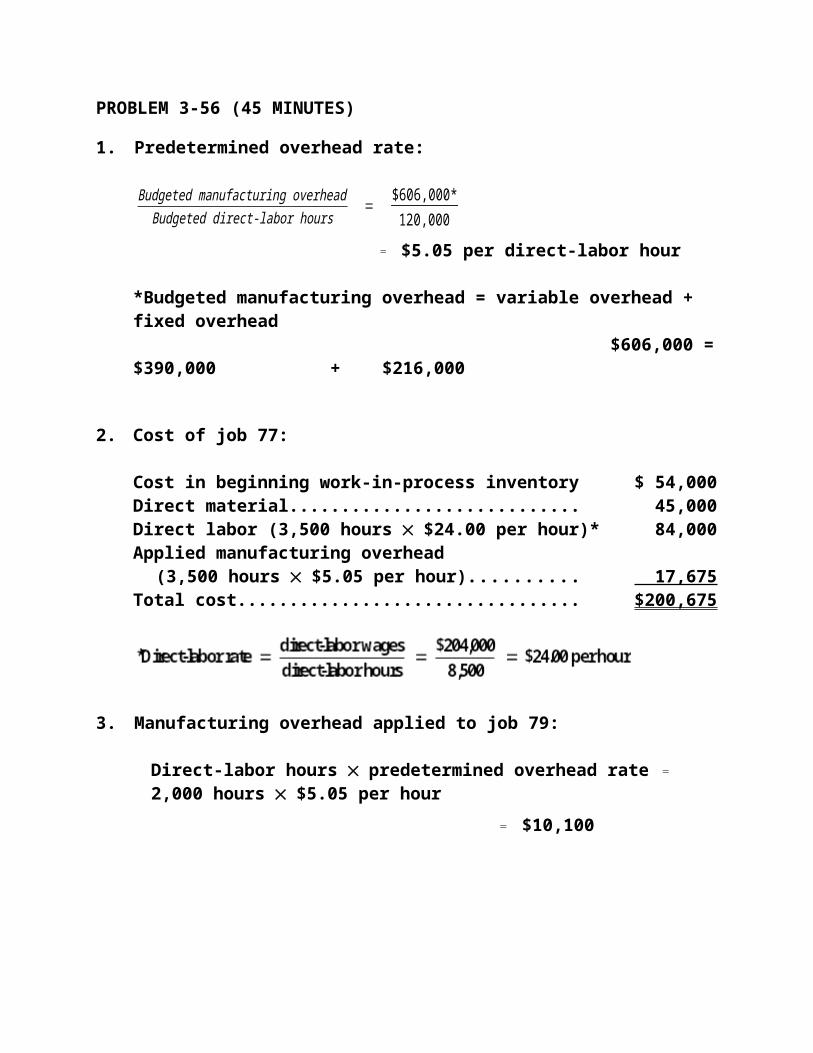

PROBLEM 3-56 (45 MINUTES)

1. Predetermined overhead rate:

Budgeted manufacturing overheadBudgeted direct-labor hours

= $606,000*

120,000 = $5.05 per direct-labor hour

*Budgeted manufacturing overhead = variable overhead + fixed overhead $606,000 = $390,000 + $216,000

2. Cost of job 77:

Cost in beginning work-in-process inventory..................................... $ 54,000Direct material......................................................................................... 45,000Direct labor (3,500 hours$24.00 per hour)*..................................... 84,000Applied manufacturing overhead

(3,500 hours$5.05 per hour)........................................................ 17,675Total cost................................................................................................. $200,675

3. Manufacturing overhead applied to job 79:

Direct-labor hourspredetermined overhead rate = 2,000 hours$5.05 per hour = $10,100

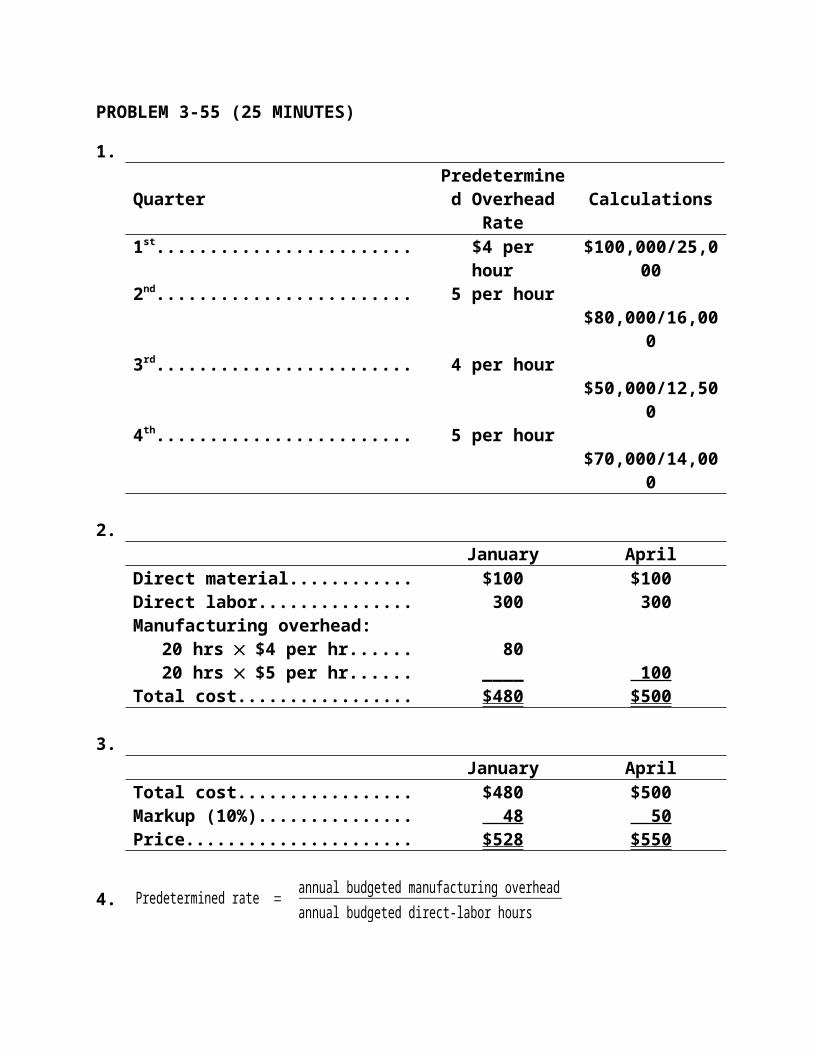

PROBLEM 3-55 (25 MINUTES)

1.

QuarterPredetermined Overhead Rate Calculations

1st................................................................... $4 per hour $100,000/25,0002nd.................................................................. 5 per hour $80,000/16,0003rd................................................................... 4 per hour $50,000/12,5004th................................................................... 5 per hour $70,000/14,000

2.January April

Direct material.............................................. $100 $100Direct labor................................................... 300 300Manufacturing overhead:

20 hrs$4 per hr................................. 8020 hrs$5 per hr................................. ____ 100

Total cost...................................................... $480 $500

3.January April

Total cost...................................................... $480 $500Markup (10%)............................................... 48 50Price.............................................................. $528 $550

4. Predetermined rate = annual budgeted manufacturing overheadannual budgeted direct-labor hours

= $300,000

67,500 = $4 . 44 per hour ( rounded )

5.January April

Direct material............................................... $100.00 $100.00Direct labor.................................................... 300.00 300.00Manufacturing overhead (20 hrs $4.44).. 88.80 88.80Total cost....................................................... $488.80 $488.80

PROBLEM 3-55 (CONTINUED)

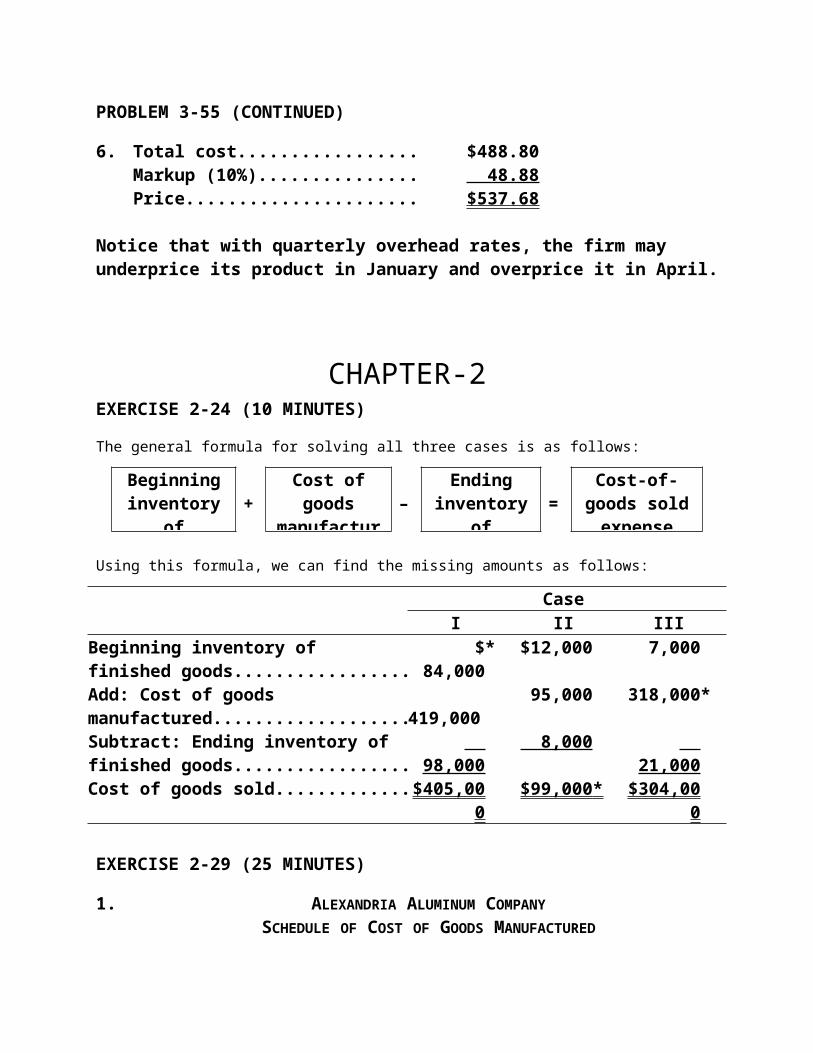

6. Total cost....................................................... $488.80Markup (10%)................................................. 48.88Price................................................................ $537.68

Notice that with quarterly overhead rates, the firm may underprice its product in January and overprice it in April.

CHAPTER-2EXERCISE 2-24 (10 MINUTES)

The general formula for solving all three cases is as follows:

Beginning inventory of

finished goods+

Cost of goods manufacturedduring period

–Ending

inventory of finished goods

= Cost-of-

goods sold expense

Using this formula, we can find the missing amounts as follows:

CaseI II III

Beginning inventory of finished goods................ $ 84,000* $12,000 7,000Add: Cost of goods manufactured....................... 419,000 95,000 318,000*Subtract: Ending inventory of finished goods.... 98,000 8,000 21,000Cost of goods sold................................................. $405,000 $99,000* $304,000

EXERCISE 2-29 (25 MINUTES)

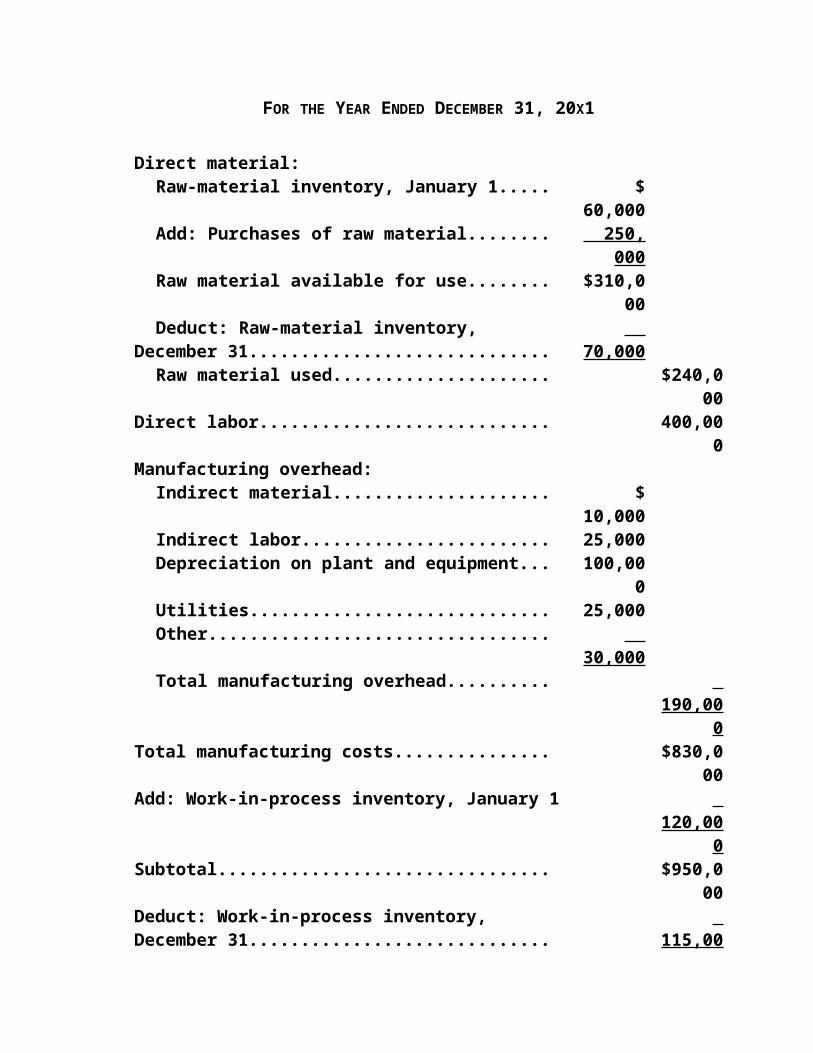

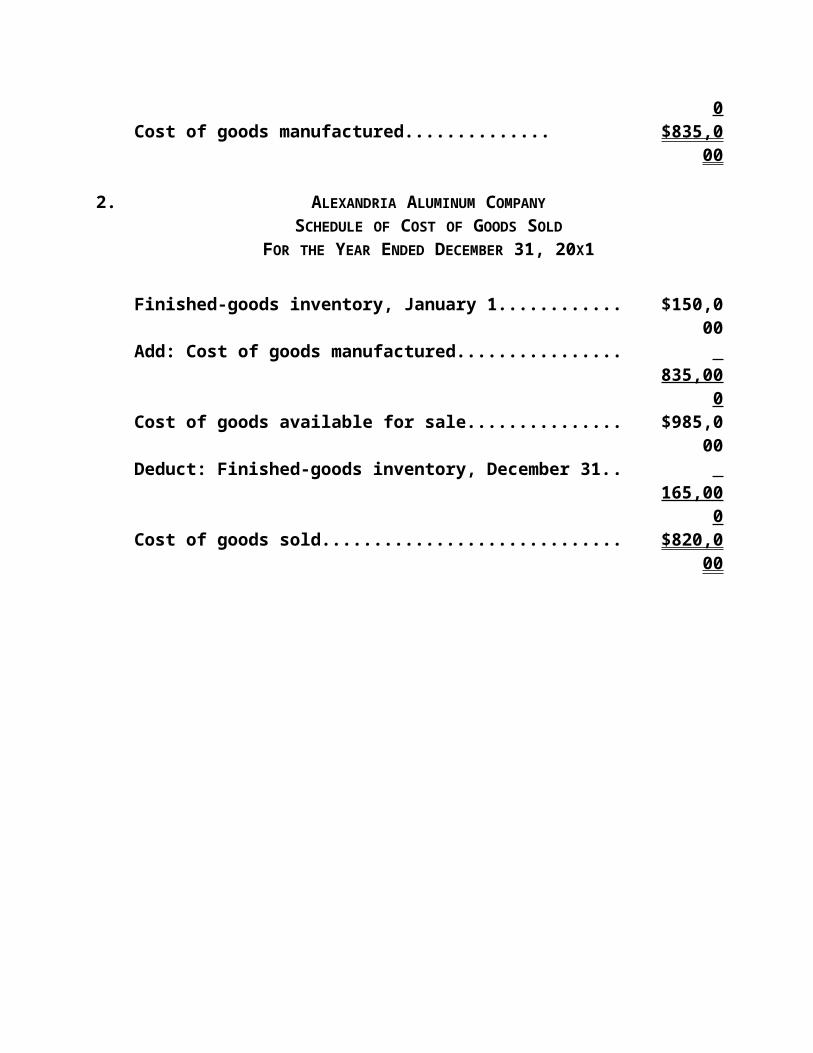

1. ALEXANDRIA ALUMINUM COMPANY

SCHEDULE OF COST OF GOODS MANUFACTURED

FOR THE YEAR ENDED DECEMBER 31, 20X1

Direct material:Raw-material inventory, January 1.......................................... $ 60,000Add: Purchases of raw material.............................................. 250,000Raw material available for use................................................. $310,000Deduct: Raw-material inventory, December 31..................... 70,000Raw material used.................................................................... $240,000

Direct labor...................................................................................... 400,000Manufacturing overhead:

Indirect material........................................................................ $ 10,000

Indirect labor............................................................................. 25,000Depreciation on plant and equipment..................................... 100,000Utilities....................................................................................... 25,000Other........................................................................................... 30,000Total manufacturing overhead................................................ 190,000

Total manufacturing costs............................................................ $830,000Add: Work-in-process inventory, January 1................................ 120,000Subtotal........................................................................................... $950,000Deduct: Work-in-process inventory, December 31..................... 115,000Cost of goods manufactured........................................................ $835,000

2. ALEXANDRIA ALUMINUM COMPANY

SCHEDULE OF COST OF GOODS SOLD

FOR THE YEAR ENDED DECEMBER 31, 20X1

Finished-goods inventory, January 1............................................................. $150,000Add: Cost of goods manufactured.................................................................. 835,000Cost of goods available for sale...................................................................... $985,000Deduct: Finished-goods inventory, December 31......................................... 165,000Cost of goods sold........................................................................................... $820,000

EXERCISE 2-29 (CONTINUED)

3. ALEXANDRIA ALUMINUM COMPANY

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 20X1

Sales revenue.................................................................................................... $1,105,000Less: Cost of goods sold................................................................................. 820,000Gross margin.................................................................................................... $ 285,000Selling and administrative expenses.............................................................. 110,000Income before taxes......................................................................................... $ 175,000Income tax expense.......................................................................................... 70,000Net income......................................................................................................... $ 105,000

PROBLEM 2-42 (25 MINUTES)

1. a. Total prime costs:

Direct material..................................................................................... $ 2,100,000Direct labor: Wages.............................................................................................. 485,000 Fringe benefits................................................................................ 95,000Total prime costs................................................................................ $ 2,680,000

PROBLEM 2-42 (CONTINUED)

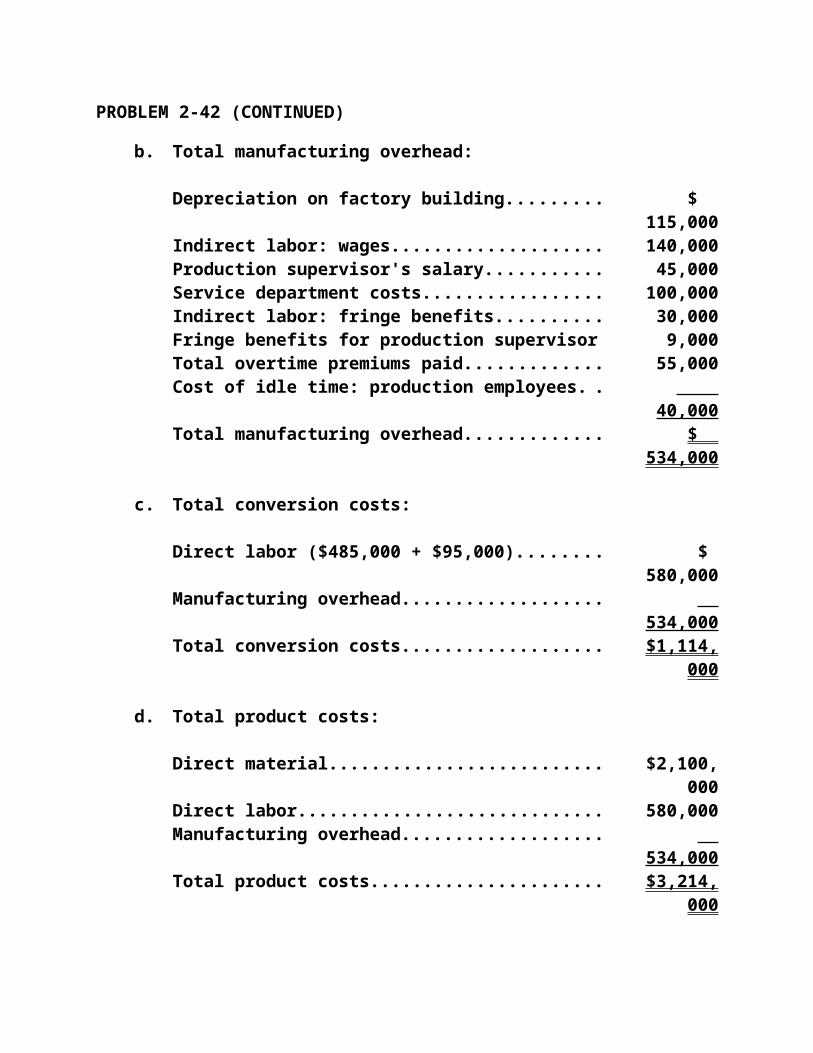

b. Total manufacturing overhead:

Depreciation on factory building...................................................... $ 115,000Indirect labor: wages......................................................................... 140,000Production supervisor's salary......................................................... 45,000Service department costs.................................................................. 100,000Indirect labor: fringe benefits............................................................ 30,000Fringe benefits for production supervisor....................................... 9,000Total overtime premiums paid.......................................................... 55,000Cost of idle time: production employees......................................... 40,000Total manufacturing overhead.......................................................... $ 534,000

c. Total conversion costs:

Direct labor ($485,000 + $95,000)...................................................... $ 580,000Manufacturing overhead.................................................................... 534,000Total conversion costs...................................................................... $1,114,000

d. Total product costs:

Direct material..................................................................................... $2,100,000Direct labor.......................................................................................... 580,000Manufacturing overhead.................................................................... 534,000Total product costs............................................................................ $3,214,000

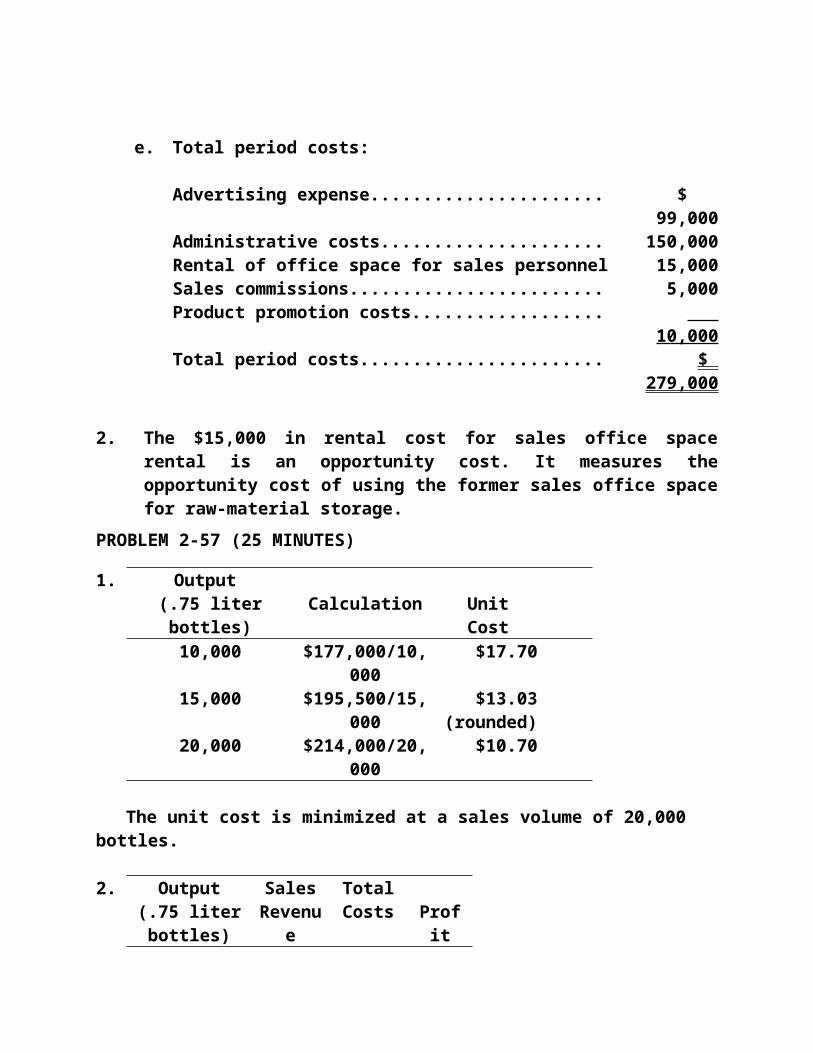

e. Total period costs:

Advertising expense.......................................................................... $ 99,000Administrative costs.......................................................................... 150,000Rental of office space for sales personnel...................................... 15,000Sales commissions............................................................................ 5,000Product promotion costs................................................................... 10,000Total period costs............................................................................... $ 279,000

2. The $15,000 in rental cost for sales office space rental is an opportunity cost. It measures the opportunity cost of using the former sales office space for raw-material storage.

PROBLEM 2-57 (25 MINUTES)

1. Output (.75 liter bottles) Calculation Unit Cost

10,000 $177,000/10,000 $17.70

15,000 $195,500/15,000 $13.03 (rounded)20,000 $214,000/20,000 $10.70

The unit cost is minimized at a sales volume of 20,000 bottles.

2. Output(.75 liter bottles)

Sales Revenue

Total Costs Profit

10,000 $180,000 $177,000 $ 3,00015,000 225,000 195,500 29,50020,000 240,000 214,000 26,000

Profit is maximized at a production level of 15,000 bottles of wine.

3. The 15,000-bottle level is best for the company, since it maximizes profit.

4. The unit cost decreases as output increases, because the fixed cost per unit declines as production and sales increase.

A lower price is required to motivate consumers to purchase a larger amount of wine.

CHAPTER-3

CHAPTER-4

SOLUTIONS TO EXERCISES

EXERCISE 4-16 (10 MINUTES)

The general formula for all three cases is the following:

Work-in-process, beginning

+ Units started during month

– Units completed during month

= Work-in-process,ending

Using this formula, the missing amounts are:

1. 12,000 units

2. 5,300 kilograms

3. 750,000 gallons

EXERCISE 4-18 (15 MINUTES)

1. 6,000 equivalent units (refer to (a) in the following table)

2. 4,400 equivalent units (refer to (b) in the following table)

CALCULATION OF EQUIVALENT UNITS: RAINBOW GLASS COMPANYWeighted-Average Method

Percentage of Equivalent Units

Physical Units

Completion with Respect to Conversion

Direct Material Conversion

Work in process, October 1.... 1,000 60%Units started during October. . 5,000Total units to account for........ 6,000

Units completed and transferred out during October........... 4,000 100% 4,000 4,000

Work in process, October 31. . 2,000 20% 2,000 400Total units accounted for........ 6,000 _____ ____Total equivalent units.............. (a) 6,000 (b) 4,400

EXERCISE 4-24 (25 MINUTES)

TULSA PAPERBOARD COMPANYWeighted-Average Method

Direct Material Conversion Total

Work in process, February 1.................... $ 5,500 $ 17,000 $ 22,500 Costs incurred during February.............. 110,000 171,600 281,600 Total costs to account for........................ $115,500 $188,600 $304,100 Equivalent units........................................ 110,000 92,000Costs per equivalent unit......................... $ 1.05 $ 2.05 $ 3.10

1. Cost of goods completed andtransferred out during February:

.......................90,000$3.10 $279,000

2. Cost remaining in February 28 workin process:

Direct material (20,000*$1.05). $ 21,000Conversion (2,000*$2.05)........ 4,100Total............................................... 25,100

Total costs accounted for................. $304,100

*Equivalent units in February 28 work in process:

DirectMaterial Conversion

Total equivalent units (weighted average)....................... 110,000 92,000

Units completed and transferred out................................ (90,000) (90,000) Equivalent units in ending work in process..................... 20,000 2,000

PROBLEM 4-36 (30 MINUTES)

1. a.Percentage

ofCompletion

with RespectTax to

Returns Conversion(physical (labor and Equivalent Units

units) overhead) Labor OverheadReturns in process, February 1...... 200 25%Returns started in February............ 825Total returns to account for............ 1,025

Returns completedduring February......................... 900 100% 900 900

Returns in process, February 28.... 125 80% 100 100 Total returns accounted for............ 1,025 ____ ____ Total equivalent units of activity.... 1,000 1,000

b.Labor Overhead Total

Returns in process, February 1................... £ 6,000 £ 2,500 £ 8,500Costs incurred during February.................. 89,000 45,000 134,000Total costs to account for............................ £95,000 £47,500 £142,500Equivalent units............................................. 1,000 1,000Costs per equivalent unit............................. £95.00 £47.50 £142.50

2. Cost of returns in process on February 28:

Labor: equivalent unitscost per equivalent unit100£95.00....................................................... £ 9,500

Overhead: equivalent unitscost per equivalent unit100£47.50....................................................... 4,750

Total cost of returns in process on February 28.......................................... £14,250

CHAPTER-5

An activity-based costing system is a two-stage process of assigning costs to products. In stage one, activity-cost pools are established. In stage two a cost driver

is identified for each activity-cost pool. Then the costs in each pool are assigned to each product line in proportion to the amount of the cost driver consumed by each product line.

A cost driver is a characteristic of an event or activity that results in the incurrence of costs by that event or activity. In activity-based costing systems, the most significant cost drivers are identified. Then a database is created that shows how these cost drivers are distributed across products. This database is used to assign costs to the various products depending on the extent to which they use each cost driver.

5-5 The four broad categories of activities identified in an activity-based costing system are as follows:

(a) Unit-level activities: Must be done for each unit of production.

(b) Batch-level activities: Must be performed for each batch of products.

(c) Product-sustaining activities: Needed to support an entire product line.

(d) Facility-level (or general-operations-level) activities: Required for the entire production process to occur.

Product-costing systems based on a single, volume-based cost driver tend to overcost high-volume products, because all overhead costs are combined into one pool and distributed across all products on the basis of only one cost driver. This simple averaging process fails to recognize the fact that a disproportionate amount of costs often is associated with low-volume or complex products. The result is that low-volume products are assigned less than their share of manufacturing costs, and high-volume products are assigned more than their share of the costs.

The pool rate is calculated by dividing the budgeted amount of an activity cost pool by the budgeted total quantity of the associated cost driver. The pool rate is the cost of a particular activity that is expected per unit of the associated cost driver.

SOLUTIONS TO EXERCISES

EXERCISE 5-21 (15 MINUTES)

1. Material-handling cost per lens:

$50,000[(25)(200) + (25)(200) ] *

× 200 = $1,000

*The total number of direct-labor hours.

An alternative calculation, since both types of product use the same amount of the cost driver, is the following:

$50,00050*

= $1,000

*The total number of units (of both types) produced.

2. Material-handling cost per mirror = $1,000. The analysis is identical to that given for requirement (1).

3. Material-handling cost per lens:

$50,000(5+15)∗¿

×5†

25=$500 ¿

*The total number of material moves.†The number of material moves for the lens product line.

4. Material-handling cost per mirror:

$50,000(5+15)

×15*

25=$1,500

*The number of material moves for the mirror product line.

EXERCISE 5-22 (15 MINUTES)

1. a. Quality-control costs assigned to the Satin Sheen line under the traditional system:

Quality-control costs = 14.5% direct-labor cost

Quality-controlcosts assigned to

Satin Sheen line = 14.5% $27,500

= $3,988 (rounded)

b. Quality-control costs assigned to the Satin Sheen line under activity-based costing:

Quantity for AssignedActivity Pool Rate Satin Sheen Cost

Incoming material inspection....... $11.50 per type..... 12 types......... $ 138In-process inspection.................... .14 per unit...... 17,500 units... 2,450Product certification...................... 77.00 per order.... 25 orders....... 1,925Total quality-control costs assigned........................................................... $4,513

2. The traditional product-costing system undercosts the Satin Sheen product line, with respect to quality-control costs, by $525 ($4,513 – $3,988).

PROBLEM 5-32 (30 MINUTES)

1. Predetermined overhead rate = budgeted overhead ÷ budgeted direct-labor hours = $800,000 ÷ 25,000* = $32 per direct labor hour

*25,000 budgeted direct-labor hours = (3,000 units of Standard)(3 hrs./unit) + (4,000 units of Enhanced)(4 hrs./unit)

Standard Enhanced

Direct material……………. $ 25 $ 40Direct labor:

3 hours x $12………… 364 hours x $12………… 48

Manufacturing overhead:3 hours x $32………… 964 hours x $32………… 128

Total cost…………………. $157 $216

2. Activity-based overhead application rates:

Activity Cost Driver Application

Activity Cost Rate

Order processing

$150,000 ÷ 500 orders processed (OP)

= $300 per OP

Machine processing

560,000 ÷ 40,000 machinehrs. (MH)

= $14 per MH

Product inspection

90,000 ÷ 10,000 inspection hrs. (IH)

= $9 per IH

A product (or service) costing system accumulates the total cost of making products and facilitates the calculation of a per-unit cost. Applications exist in:

A cost driver is any event or activity that causes costs to be incurred. Possible examples include labor hours in manual assembly work and machine hours in automated production settings.

The higher the degree of correlation between a cost-pool increase and the increase in its cost driver, the better the cost management information.

. Managerial accounting is the process of identifying, measuring, analyzing, interpreting, and communicating information in pursuit of an organization’s goals.

* Line personnel are directly involved in carrying out the mission of the organization (e.g., assembly workers in a factory, doctors in a hospital, teachers in a school).

* Staff personnel (accountants, lawyers, personnel directors, and other administrative positions) provide support for the organization’s mission.