SolaBlock Investor Slides

23

SolaBlock LLC 79 River Drive, Hadley, MA 01035 www.solablock.com Tough City Solar Copyright © 2016 SolaBlock LLC

-

Upload

pjaquinlan -

Category

Business

-

view

141 -

download

0

Transcript of SolaBlock Investor Slides

SolaBlockLLC79RiverDrive,Hadley,MA01035www.solablock.com

Tough City Solar

Copyright©2016SolaBlockLLC

HighDemandforSolarPVinCi4es

Urbancommuni4eshavedesiredon-sitesolarelectricityasmuchasothercommuni4es,buthavenothadaccesstophotovoltaic(PV)productssuitedtourbancondi4ons.

• UnKlnow,urbansolarhasbeenrelaKvelynonexistent,dueto:

-Insufficientroofspace,complexsurfaces,cost,or-RiskoftheS,vandalism,orotherseveredamage.

• SolaBlockisdesignedfortheurbanlandscape,enablingurbanstructurestohaveproducKvesolargeneraKonintegratedwithbuildingfacadesandwalls.

• SolaBlockmeetsthedemandcriteriaforLEED,EnergyStar,andothergreenconstrucKoninhighdensityurbanandcampusseUngs.

SchoolsandcollegesMunicipalbuildingsHighwaysoundwallsParkinggaragesRemotebuildingsBridgesU4litybuildingsUrban“infill”buildingsPropertywalls

AnAccelera4ngMarketforBIPV“Building-integratedPV(BIPV)isoneofthefastestgrowingmarketsinthebuildingsector”*“15.4%CAGRthrough2019”**.

ü TotalcurrentBIPVmarket:$1.7billion***.ü Addressablemarket:$500million.

Solardemand—wherepeopleliveü Urbandwellersalsowantbenefitsofsolar.ü Mostvaluableclosesttobuildingloads

ü Enablingurbanzero-energyandoff-gridbuildings

ü Capableofsolarizingotherwiseimpossiblestructures(walls,bridges,etc).*NavigantResearch;**Markets&Research;***PikeResearch

SolaBlock–ToughCitySolar

Longservicelife

Vandalresistant

TheSresistant

Weatherresistant

VersaKle

CosteffecKve

Fundamentallylikenoothersolar

$∞

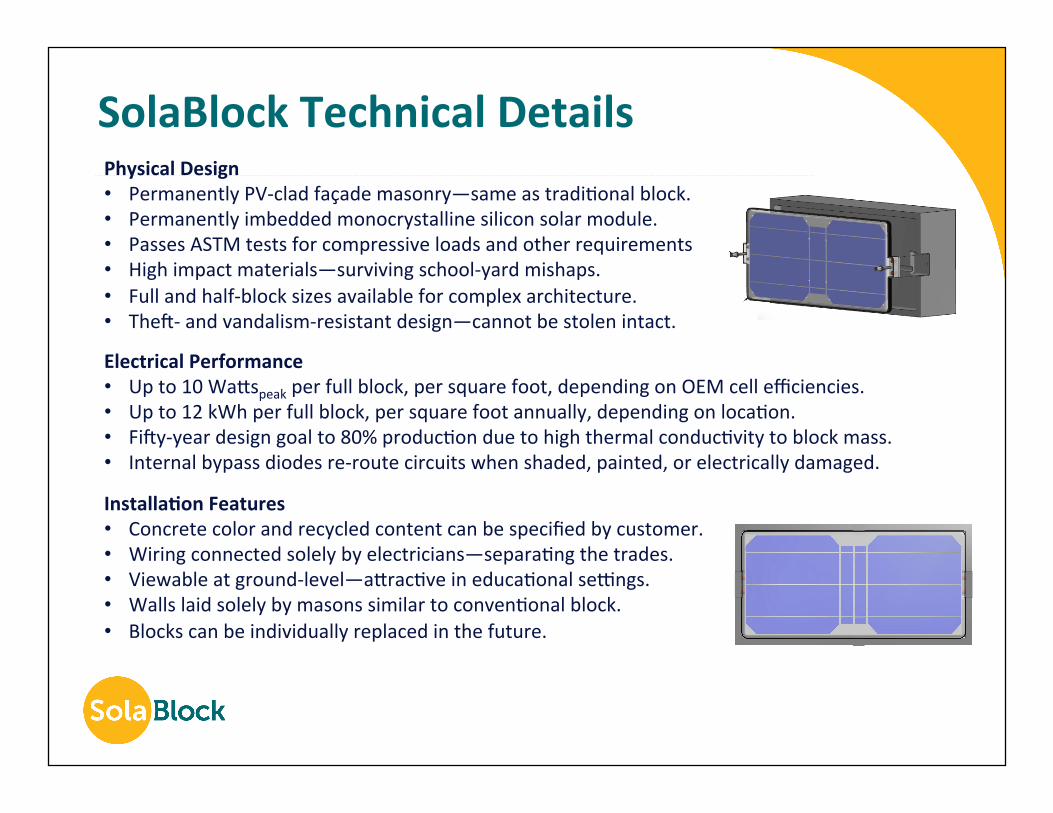

SolaBlockTechnicalDetailsPhysicalDesign• PermanentlyPV-cladfaçademasonry—sameastradiKonalblock.• Permanentlyimbeddedmonocrystallinesiliconsolarmodule.• PassesASTMtestsforcompressiveloadsandotherrequirements.• Highimpactmaterials—survivingschool-yardmishaps.• Fullandhalf-blocksizesavailableforcomplexarchitecture.• TheS-andvandalism-resistantdesign—cannotbestolenintact.

ElectricalPerformance• Upto10Waispeakperfullblock,persquarefoot,dependingonOEMcellefficiencies.• Upto12kWhperfullblock,persquarefootannually,dependingonlocaKon.• FiSy-yeardesigngoalto80%producKonduetohighthermalconducKvitytoblockmass.• Internalbypassdiodesre-routecircuitswhenshaded,painted,orelectricallydamaged.

Installa4onFeatures• Concretecolorandrecycledcontentcanbespecifiedbycustomer.• Wiringconnectedsolelybyelectricians—separaKngthetrades.• Viewableatground-level—airacKveineducaKonalseUngs.• WallslaidsolelybymasonssimilartoconvenKonalblock.• Blockscanbeindividuallyreplacedinthefuture.

Karen Lauter Utgoff Consulting

PatrickQuinlan,ChiefExecu4veOfficerNaKonalRenewableEnergyLab.,UMass,U-Wisc.SolarLab,ProfessionalEngineer,WhiteHouseandCongressionalTechnologyFellow.Patents.

JasonLaverty,ChiefOpera4ngOfficerFormerInstructor,InternaKonalMasonryInsKtute,Member—Local3BostonInternaKonalUnionofBricklayers,JobCorpInstructor,Patents.

ProvidingCustomerConfidencewithTechnologyExper4se,BusinessDepthandaCustomer-OrientedTeam

Advisors

StaffMarkStetz,ElectricalSystemsManager;RachaelYaseen—BusinessManager,2-4UMassSales&MarkeKnginternsandengineeringinterns.

Founders

CREATIVEDESIGNDRIVENBYMARKETINGSCIENCE

Team

Business Canvas Value Proposition

Key Activities

Key Partners

Customer Relationships

Channels

Revenue Streams

Cost Structure

Customer Segments

Key Resources

Provide on-site solar electricity to urban building owners. Provide on-site electricity for buildings vandalism, theft or weather has previously precluded it. Enable buildings, walls and other structures in urban areas to provide local electricity to meet sustainability or energy independence objectives. Enable building owners to visibly differentiate their buildings as sustainable.

Ultimate customers: • Public building

owners • Remote building

owners • LEED building

designers/ developers

• Homeowners. Our direct customers are the regional building product suppliers who serve these market segments as our partners. Multi-sided market: customers are our partners and the product end users.

We will reach regional concrete manufacturers through trade marketing. We will drive interest through contacts with public agencies, green groups and architectural organizations interested in green building.

We acquire our customers through identifying and soliciting region partners. We keep them through national support for the brand, margin-sharing, and end-use customer support.

• Supply-chain needs for high value PV, good quality block.

• R&D for more products • Marketing to partners • Drive demand • Develop low cost

volume manufacturing.

• Supply-chain providers • People, hires • Funding, investment • Brand building • IP support • Partner management • Testing and certification

services.

Supply-chain: • PV cell OEMS • Electric parts

OEMs. • Glass and

substrate OEMs

Distribution & Sales: • Regional block

and tile providers • Public building

contractors • Architects and

designers • Retail building

products retailers.

Interested parties: • Green groups • Public agencies • LEED • EnergyStar, etc.

• Leverage Costs for PV, glass, wiring, and other materials

• Labor, automation, and transportation • Shared margins with retailers • Marketing, both national and regional • IP--especially international patents

Sales to: • Our regional building products

partners • Direct sales to end-use

customers for ancillary parts

IPandMarketAdvantage

• IPDevelopment:– USuKlityanddesignpatentsawarded,EUpatentspending– IPcounsel:Fish&Richardson– Nextstep:ANSIandULcerKficaKon– DetailedinternalmanufacturingprocessesIP

• Go-to-Market:– DemonstraKonprojecttobecompletedinSpring2016– Firstlocalconcreteblockpartner:DucharmeCorp.– Seekingregionalconcrete-blockmanufacturersanddistributorpartners

SolaBlockCustomerMarketSegments

RegionalNortheastSoutheastSouthwestNorthwestInternational

ApplicationCommercial/IndustrialResidential BuildingsWall SystemsUrban StructuresSolar Projects

CustomerLEED DesignersGovernment AgenciesSchool SystemsBusiness ownersHomeowners

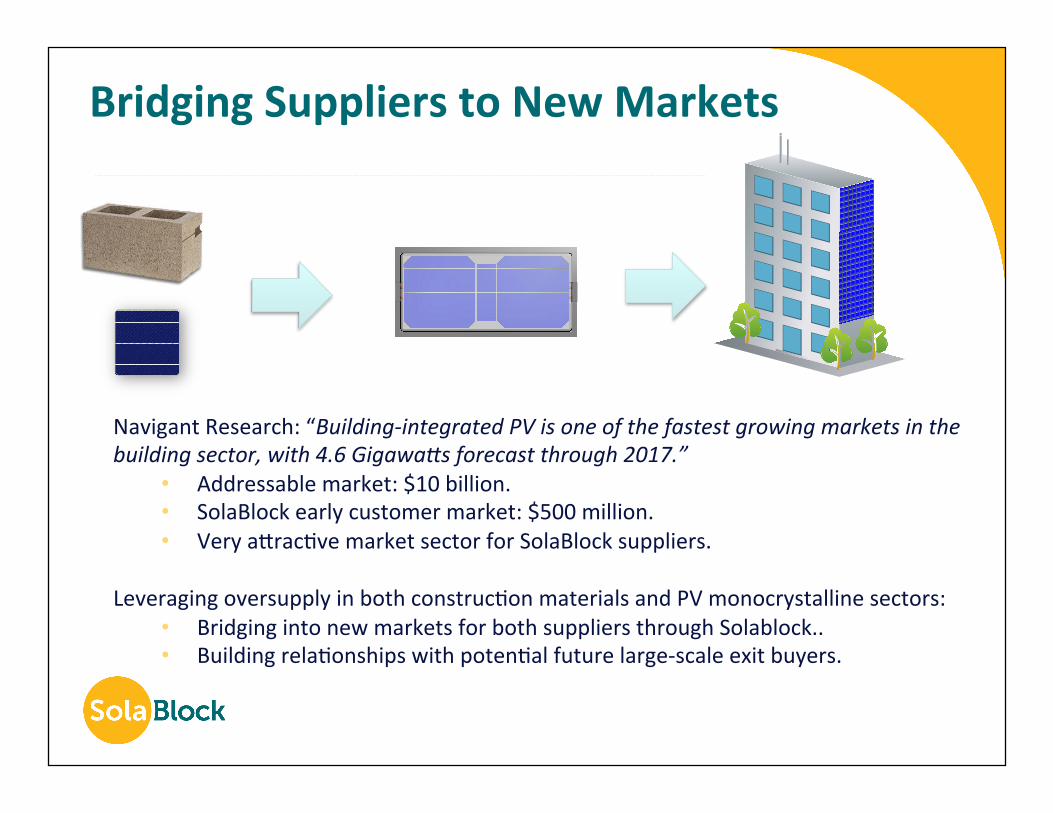

BridgingSupplierstoNewMarkets

NavigantResearch:“Building-integratedPVisoneofthefastestgrowingmarketsinthebuildingsector,with4.6GigawaMsforecastthrough2017.”

• Addressablemarket:$10billion.• SolaBlockearlycustomermarket:$500million.• VeryairacKvemarketsectorforSolaBlocksuppliers.

LeveragingoversupplyinbothconstrucKonmaterialsandPVmonocrystallinesectors:• BridgingintonewmarketsforbothsuppliersthroughSolablock..• BuildingrelaKonshipswithpotenKalfuturelarge-scaleexitbuyers.

MonocrystallineCells(OEMs)

SolaBlockNa4onalMarke4ng

Customers

SolaBlockmanufacturesanddistributesPV-cladblockandKle.Tilesarecompletedonsiteandshippedtopartners.Forblocks,PV-kitsareassembledatSolaBlockandshippedtoregionalpartnersitesforfinalassemblytoblocks.

Suppliers

EndUseCustomers

HardwareSuppliers(OEMs)

Wiring,encapsulantsetc.

(OEMs)

RegionalPartners

SMUR&D SMUDesign SMUProduc4on(PV-Kits)

TileR&D TileDesign TileProduc4on RegionalPartner Customers

CustomersSMUFinalAssembly

ConcreteBlockManufacturers

Marke4ng

R&D Produc4onDesignfor

Manufacturing

RegionalPartnerLocalMarke4ng

SolaBlockValueChain

PerformanceofVer4calvs.TiltedModules

AnnualEnergyProducQon:VerQcalSouthFacingversusTiltedOrientaQon

ConKnentalUS,Japan

Canada

Europe

ReflecKvesurfaces(concrete,whitestones,snow,water,etc.)infrontofthePVcanmakeupmostofthedifference.

Ver4calPVproducesabout60%oftheoutputof4ltedsolarintheUS.InEU,70%;inCanada80%

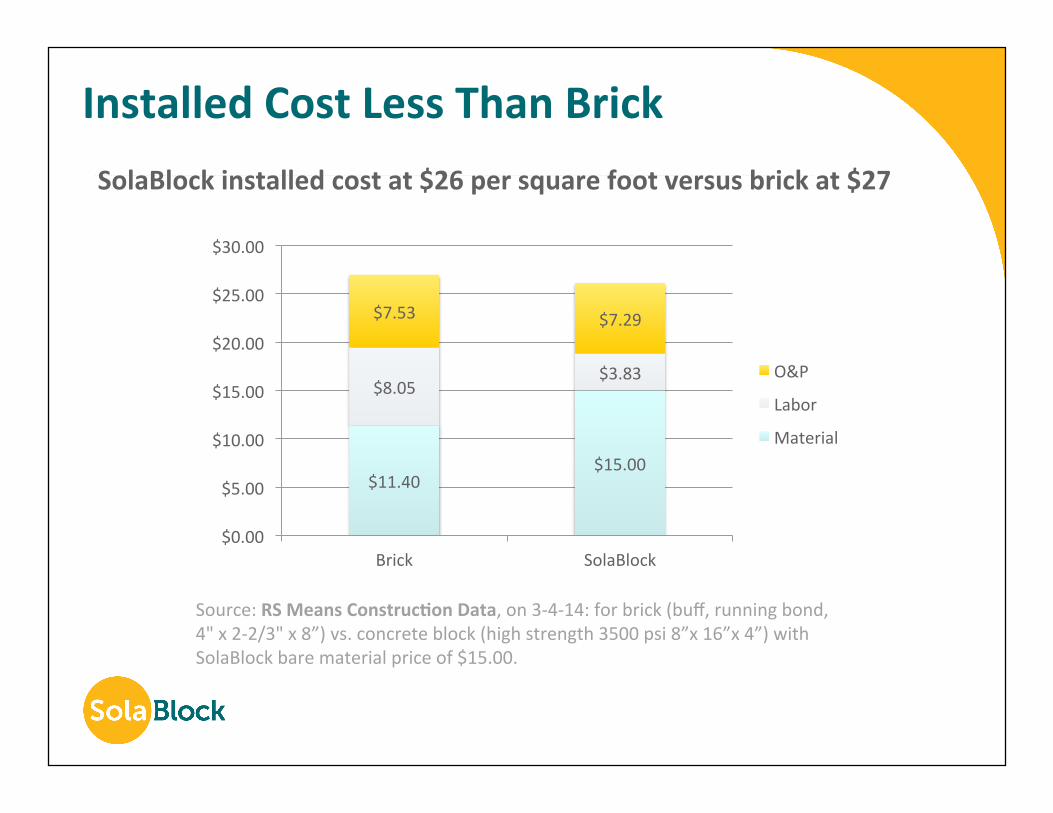

InstalledCostLessThanBrick

Source:RSMeansConstruc4onData,on3-4-14:forbrick(buff,runningbond,4"x2-2/3"x8”)vs.concreteblock(highstrength3500psi8”x16”x4”)withSolaBlockbarematerialpriceof$15.00.

SolaBlockinstalledcostat$26persquarefootversusbrickat$27

$11.40$15.00

$8.05$3.83

$7.53 $7.29

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

Brick SolaBlock

O&P

Labor

Material

SuperiorCustomerLifecycleBenefit/Cost

Conven4onalPV*

SolaBlockPV*

LifeKme 25years 50yearsReplacements once zeroAnnualkWh/W 1.6 1.2AnnualRevenue $50 $36Cost $404 $270Benefit/Cost 3.16 3.43

RaKo==> 1.10

SolaBlockis10percentmorecost-effec4vethanconven4onalsolar

*Comparison:60-cellcSimodulevs.30SolaBlockSolarMasonryUnits(SMU)

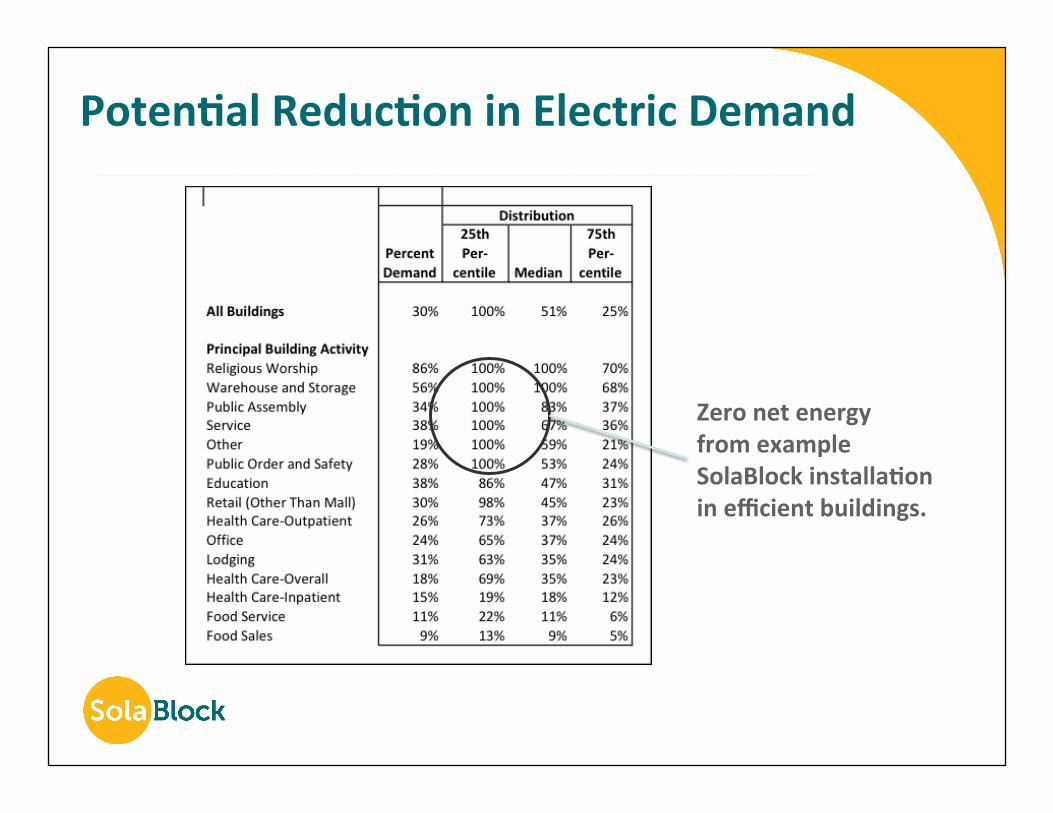

Poten4alReduc4oninElectricDemand

ZeronetenergyfromexampleSolaBlockinstalla4oninefficientbuildings.

Compe44vePosi4on:BuildingIntegratedPhotovoltaics

SolaBlockisthebestchoiceforurbansolarapplica4ons.

VandalResistance

ThekResistance

EnergyProduc4vity

Life-cycleValue

SolaBlockSystems

ConvenKonalModules

SolarShingles

SolarWindows

SolaBlockvs.Compe4tors

FinancialModel

Costs *AssumpKons: Endofyear2017operaKons(seeP&Lforecastsfordetails). Salesof90%block10%Kle,plus10%salesinancillaryproducts.

Item CostConcreteblock $1.50

Photovoltaics(11Wp)

$6.60

Wiringanddiodes

$2.25

Coverandencapsulant

$2.85

Labor&overhead $3.30

TOTAL $15.00

Item Cost

Costperblock/Kle-set $15.00

Grossrevenueperblock/Kle-set

$19.13

Grossincomeperblock/Kle-set

$8.50

Interest,depreciaKon,taxes,etc.

$2.25

Netearnings $6.25

Grossmargin 50%

Item Cost

Grossincomeperblock/Kle-set

$8.50

Annualsales* 476,000

Annualgrosssales

$13.2M

Grossprofit $4.4M

Projectedyear-over-yearsalesgrowthto2020

100%

Revenue

Profits

GrossMargin:50%ReturnonSales:18%

FinancialPlan• 2016:$500,000SeedFunding

– IniKalsalesandpilotdemonstraKons– CerKficaKonandcompliancetesKng– Pilotcontractswithpartnerconcretemanufacturers

• 2018:$2.25MSeries-AFunding– Manufacturingscale-upandautomaKon– Businessdevelopment–mulK-regionalpartners.– Businessdevelopment–internaKonalpartners.

• 2020:$6.5MSeries-BFunding– EUmanufacturingscale-upandautomaKon

EBIDTAGrowth• Cost-of-goodssold($17)for2017basedonhighlabor-intensityandpoorbuying

powerforPVcells,fallingby1/3duetolargerpurchasing.

• RevenuegrowthcommensuratewithcompositeofBIPVmarketgrowthof15%CAGRplusannualmarketsharegrowthatnominal100%.

• Fundingneedsare$200,000in2016formanufacturing;$2,25Min2018forEUexpansioncampaign;and$6.5Min2020forworkingcapital.

20

$ 2016 2017 2018 2019 2020

COGS(perunit) 17.00 15.50 14.50 14.00 13.75

Revenue -58,000 4,138,000 12,298,000 28,618,000 61,258,000

EBIDTA 0 1,445,000 3,390,000 6,930,000 14,010,000

FundingNeeds 200,000 0 2,250,000 0 6,500,000

PlanforCompe44veAdvantage

1. SecureIntellectualProperty—oncover,encapsulant,interconnecKon,andoverallconcept.

2. NodirectcompeKtorsinthespaceatthisKme.

3. PartneringplanwithlocalpartnersensuresstrongregionalmarketposiKonsacrosstheUS.

4. RapidbrandingtoestablishoverwhelmingproductrecogniKonearlyon. SolaBlocklabelingpriortocommissioning.

GoingForward• IPsecured—USpatentssecuredandEUpatentsappliedfor• Excellentteamformed• Prototypesbuilt—IPvalidated• Commitmentfromblockmanufacturer(R.Ducharme,Inc.)• Commitmentfromblockdistributor(ChicopeeMasonSupply,Inc.)• CommitmentfromSpringfieldTechnologyPark,SpringfieldMass.• DemonstraKonstructuredesignedandreadytobuild• SeekingtesKngandvalidaKongrantsforfurthertesKng• Manufacturingplanwithregionalconcreteblockmanufacturers• DistribuKonplanwithregionalconcreteproductsdistributors

![JetBlue 2014 Investor Day_FINAL [Slides Only]](https://static.fdocuments.in/doc/165x107/55cf925a550346f57b95c20f/jetblue-2014-investor-dayfinal-slides-only.jpg)

![PM 2014 investor day 2014-06-26-LAC Region Investor Day Slides [WEBSITE FINAL]](https://static.fdocuments.in/doc/165x107/577cbc651a28aba7118da312/pm-2014-investor-day-2014-06-26-lac-region-investor-day-slides-website-final.jpg)