Softchoice Corp consolidated FS FINALm.softchoice.com/files/pdf/about/Consolidated... ·...

69

Consolidated Financial Statements (Expressed in U.S. dollars) SOFTCHOICE CORPORATION Years ended December 31, 2012 and 2011

Transcript of Softchoice Corp consolidated FS FINALm.softchoice.com/files/pdf/about/Consolidated... ·...

Consolidated Financial Statements (Expressed in U.S. dollars)

SOFTCHOICE CORPORATION

Years ended December 31, 2012 and 2011

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. KPMG Canada provides services to KPMG LLP.

KPMG Confidential

KPMG LLP Chartered Accountants Yonge Corporate Centre 4100 Yonge St. Suite 200 North York, ON M2P 2H3

Telephone (416) 228-7000 Fax (416) 228-7123 Internet www.kpmg.ca

INDEPENDANT AUDITORS' REPORT

To the Shareholders of Softchoice Corporation

We have audited the accompanying consolidated financial statements of Softchoice Corporation, which comprise the consolidated statements of financial position as at December 31, 2012 and 2011, the consolidated statements of comprehensive income, changes in equity and cash flows for the years then ended, and notes, comprising a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the consolidated financial position of Softchoice Corporation as at December 31, 2012 and 2011, and its consolidated financial performance and its consolidated cash flows for the years then ended in accordance with International Financial Reporting Standards.

Chartered Accountants, Licensed Public Accountants

February 19, 2013 Toronto, Canada

2

SOFTCHOICE CORPORATION Consolidated Statements of Comprehensive Income (In thousands of U.S. dollars, except per share information) Years ended December 31, 2012 and 2011 2012 2011 Net sales $ 1,065,620 $ 999,400 Cost of sales 858,304 810,518 Gross profit 207,316 188,882 Expenses:

Selling and marketing (note 4) 119,543 102,434 Administrative (note 4) 47,225 45,680 166,768 148,114

Income from operations 40,548 40,768 Finance costs (note 6) 528 6,169 Finance income (note 7) (1,289) (82) Other income (note 5) (232) (119) Other expense (note 5) 96 673 (897) 6,641 Income before income taxes 41,445 34,127 Income tax expense (note 8) 13,789 12,007 Net income 27,656 22,120 Other comprehensive loss:

Foreign currency translation adjustment (106) (51)

Total comprehensive income $ 27,550 $ 22,069 Net earnings per common share:

Basic (note 17) $ 1.40 $ 1.12 Diluted (note 17) 1.37 1.11

The accompanying notes are an integral part of these consolidated financial statements.

3

SOFTCHOICE CORPORATION Consolidated Statements of Changes in Equity (In thousands of U.S. dollars) Years ended December 31, 2012 and 2011 Accumulated other Total Number Capital Contributed comprehensive Retained shareholders' 2012 of shares stock surplus loss earnings equity Balance, January 1, 2012 19,837,211 $ 26,548 $ 3,274 $ (1,193) $ 111,689 $ 140,318 Total comprehensive income (loss):

Net income – – – – 27,656 27,656 Other comprehensive loss:

Foreign currency translation adjustment – – – (106) – (106)

Total comprehensive income (loss) – – – (106) 27,656 27,550

Transactions with shareholders

recorded directly in equity: Share options exercised 40,151 516 (194) – – 322 Share-based compensation – – 2,091 – – 2,091 Repurchase of common

shares (219,600) (336) (2,264) – – (2,600) Dividends declared – – – – (2,778) (2,778) (179,449) 180 (367) – (2,778) (2,965)

Balance, December 31, 2012 19,657,762 $ 26,728 $ 2,907 $ (1,299) $ 136,567 $ 164,903

Accumulated other Total Number Capital Contributed comprehensive Retained shareholders' 2011 of shares stock surplus loss earnings equity Balance, January 1, 2011 19,780,039 $ 26,016 $ 2,054 $ (1,142) $ 89,569 $ 116,497 Total comprehensive income (loss):

Net income – – – – 22,120 22,120 Other comprehensive loss:

Foreign currency translation adjustment – – – (51) – (51)

Total comprehensive income (loss) – – – (51) 22,120 22,069

Transactions with shareholders

recorded directly in equity: Share options exercised 8,599 108 (41) – – 67 Share-based compensation – – 1,722 – – 1,722 Repurchase of common

shares (4,000) (37) – – – (37) Deferred share units

exercised (note 18) 52,573 461 (461) – – – 57,172 532 1,220 – – 1,752

Balance, December 31, 2011 19,837,211 $ 26,548 $ 3,274 $ (1,193) $ 111,689 $ 140,318

The accompanying notes are an integral part of these consolidated financial statements.

4

SOFTCHOICE CORPORATION Consolidated Statements of Cash Flows (In thousands of U.S. dollars) Years ended December 31, 2012 and 2011 2012 2011 Cash provided by (used in): Operating activities:

Net income $ 27,656 $ 22,120 Adjustments for:

Amortization of intangible assets 8,663 5,989 Depreciation of property and equipment 3,124 3,018 Share-based compensation 2,091 1,722 Income tax expense 13,789 12,007 Unrealized foreign currency (gain) loss (1,086) 648 Loss on disposal of intangible assets and

property and equipment 167 16 Interest expense on financial liabilities 52 1,840 Amortization of deferred financing costs – 1,844 54,456 49,204

Change in non-cash operating working capital (note 24) 2,951 4,477 57,407 53,681 Interest paid (53) (1,832) Income taxes paid (13,252) (13,259) Cash provided by operating activities 44,102 38,590

Financing activities:

Repayment of loans and borrowings – (12,784) Proceeds from issuance of common shares 322 67 Dividends paid to shareholders (2,778) – Repurchase of common shares (2,600) (37) Cash used in financing activities (5,056) (12,754)

Investing activities: Purchase of property and equipment (2,346) (2,280) Purchase of intangible assets (2,563) (2,620) Restricted cash – 500 Acquisition of UNIS LUMIN Inc. (note 3) – (23,941) Cash used in investing activities (4,909) (28,341)

Increase (decrease) in cash 34,137 (2,505) Cash, beginning of year 32,993 35,752 Effect of exchange rate fluctuations on cash held 745 (254) Cash, end of year $ 67,875 $ 32,993

The accompanying notes are an integral part of these consolidated financial statements.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

5

1. Nature of operations

Softchoice Corporation (the "Company") was formed on May 15, 2002 pursuant to an

amalgamation with Ukraine Enterprise Corporation. The Company was incorporated under the

Canada Business Corporations Act. The Company is a North American business-to-business

direct marketer of information technology ("IT") hardware, software and services to small, medium

and large businesses and public sector institutions.

The Company's United States operations are carried on by a subsidiary ("Softchoice U.S."), a

corporation incorporated under the laws of the State of New York. On December 10, 2007, the

Company incorporated a wholly owned subsidiary, Softchoice Holdings Corporation ("Holdco").

Holdco is incorporated under the laws of the State of Delaware.

The consolidated financial statements of the Company comprise the Company and its subsidiaries

(together referred to as the "Company").

The Company's registered office is located at 173 Dufferin Street, Suite 200, Toronto, Ontario.

2. Significant accounting policies

The accounting policies set out below have been applied consistently to all periods presented in

these consolidated financial statements.

(a) Statement of compliance

These consolidated financial statements, including comparatives, have been prepared using

accounting policies in compliance with International Financial Reporting Standards (“IFRS”), as

issued by the International Accounting Standards Board ("IASB"). The policies applied in these

consolidated financial statements are based on IFRS issued and outstanding as of February

19, 2013, the date the Board of Directors approved the consolidated financial statements for

issue.

(b) Basis of presentation

The consolidated financial statements include the accounts of the Company. Intercompany

transactions and balances are eliminated on consolidation.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

6

2. Significant accounting policies (continued)

The consolidated financial statements have been prepared primarily under the historical cost

convention. The following items are carried at fair value:

(i) Financial instruments carried at fair value through profit or loss ("FVTPL").

(ii) Liabilities for cash-settled share-based payment awards.

The Company's financial year corresponds to the calendar year. The consolidated financial

statements are prepared in thousands of U.S. dollars.

Presentation of the consolidated statements of financial position differentiates between current

and non-current assets and liabilities. The consolidated statements of comprehensive income

are presented using the functional classification for expenses.

(c) Critical judgments and key sources of estimation uncertainty

The preparation of financial statements in conformity with IFRS requires management to make

judgments and estimates that affect the reported amounts of assets and liabilities and the

disclosure of contingent assets and liabilities at the date of the financial statements and the

reported amount of net sales and expenses throughout the period. Actual results could differ

from these estimates.

Management continuously evaluates the estimates and underlying assumptions based on

management’s experience and knowledge of facts and circumstances. Revisions to accounting

estimates are recognized in the period in which the estimates are revised and in any future

periods affected.

Areas which require management to make significant judgment and estimates in determining

the amounts recognized in the consolidated financial statements are as follows:

(i) Gross versus net revenue presentation assessment

The determination by the Company on whether it acts as a principal in a transaction,

and recognizes revenue based on the gross amount billed to a customer, or as an

agent, and reports the sales transaction on a net basis (note 2(f)) requires significant

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

7

2. Significant accounting policies (continued)

judgment. Changes to the assumptions and judgments made by management could

materially impact the amount of net sales recognized in a particular period.

(ii) Multiple element arrangements

For revenue arrangements involving multiple elements, the Company allocates

revenue to each component of the arrangement using the relative selling price method

based on market-based inputs. The allocated portion of the arrangement which is

undelivered is then deferred. In some instances, a group of contracts or agreements

with the same customer may be so closely related that they are, in effect, part of a

single arrangement and, therefore, the Company will allocate the corresponding

revenue among the various components, as described above. Changes to the

assumptions and judgments made by management could materially impact the amount

of revenue recognized in a particular period (note 2(f)(vi)).

(iii) Revenue recognition of professional services

Revenue recognition on professional services is based on the percentage of

completion of the transaction which is assessed based on actual hours incurred and

budgeted hours required to complete the transaction. The Company estimates the

revenue and costs associated with the transaction based on historical experience (note

2(f)(v)).

(iv) Sales returns provision

The Company records an estimate of sales returns based on historical information.

The historical estimate is reviewed and recalculated throughout the year to ensure it

reflects the most relevant data available (note 2(f)(v)).

(v) Determination of cash-generating unit (“CGU”)

Significant judgment was involved in determining the smallest group of assets that

generates independent cash flow. Changes to this assessment could materially impact

the level at which goodwill is tested for impairment (note 13).

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

8

2. Significant accounting policies (continued)

(vi) Sales tax provision

The Company is subject to sales tax in numerous jurisdictions. There are many

transactions and calculations for which the ultimate tax determination is uncertain

during the ordinary course of business. The Company maintains provisions for

uncertain tax positions that it believes appropriately reflect its risk with respect to tax

matters under active discussion, audit, dispute or appeal with tax authorities, or which

are otherwise considered to involve uncertainty. These provisions are made using the

best estimate of the amount expected to be paid, based on a qualitative assessment of

all relevant factors and historical precedence.

(vii) Deferred tax assets and liabilities

The Company estimates the timing, amount and likelihood of the recognition of

deferred tax assets and liabilities based on historical experience and substantially

enacted tax rates (note 2(n)).

(viii) Fair value allocations recorded as a result of business acquisitions

The determination of fair values to the net identifiable assets acquired in business

acquisitions often requires management to make assumptions and estimates about

future events. Changes in any of the assumptions or estimates used in determining the

fair value of acquired assets and liabilities could impact the amount assigned to assets,

liabilities and goodwill in the purchase price allocation (note 3).

(ix) Recoverability of goodwill

Goodwill is tested for impairment annually or more frequently if there is an indication of

impairment. The assessment of fair values of CGUs include estimates and

assumptions of growth rates, foreign exchange rates, discount rates, future operating

performance and capital requirements. These estimates and assumptions are based

on industry and historical practices as well as future expectations (note 13). Changes

to these estimates or assumptions could impact the impairment analysis of goodwill.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

9

2. Significant accounting policies (continued)

(x) Allowance for doubtful accounts

The Company monitors the financial stability of its customers and the environment in

which they operate to make estimates regarding the likelihood that the individual

accounts receivable balance will be paid. Credit risks for outstanding accounts

receivable is regularly assessed and reviewed. The allowance for doubt accounts is

recorded based on specific customer information and experience (note 20).

(xi) Inventory provision

The Company estimates the value of inventory that will become obsolete based on

historical data and the expectations in the industry (note 11).

(xii) Useful lives of tangible and long-lived assets

Significant judgment is involved in the determination of useful lives and residual values

of tangible and long-lived assets, for the computation of depreciation and amortization.

The determination of useful lives and residual values is based on the Company’s

expectations of the asset’s future economic benefits and is reviewed annually and

adjusted if required (note 2(k) and note 2(l)).

(xiii) Stock-based compensation

For equity-settled share-based payment transactions, the fair value method of

accounting is used. Under this method, the cost of goods or services received is

recorded based on the estimated fair value at the grant date and charged to net income

over the vesting period.

For cash-settled shared-based payment transactions, the related expense is accrued at

the fair value of the liability at the grant date. Until the liability is settled, the Company

re-measures the fair value at the end of each reporting period and at the date of

settlement, with any changes in fair value recognized in net income for the period.

The fair value method of accounting for share-based compensation requires that

management make certain judgments and assumptions such as, forfeiture rate and

volatility that, if changed, could produce a significantly different result.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

10

2. Significant accounting policies (continued)

(d) Basis of consolidation

The consolidated financial statements of the Company include the accounts of all of its

subsidiaries.

(i) Subsidiaries

Subsidiaries are entities controlled by the Company. The financial statements of the

subsidiaries are included in the consolidated financial statements from the date control

commences until the date control ceases. Intercompany transactions between subsidiaries

are eliminated upon consolidation.

(ii) Business combinations

Goodwill arising from acquisitions is recognized as an asset and measured at fair value,

being the excess of the consideration transferred over the Company's interest in the net fair

value of the identifiable assets, including intangible assets, liabilities and contingent

liabilities recognized. If the Company's interest in the net fair value of the acquiree's

identifiable assets, liabilities and contingent liabilities exceeds the cost of the business

combination, the excess is recognized immediately in the consolidated statements of

comprehensive income. The interest of non-controlling shareholders in the acquiree, if any,

is initially measured at the non-controlling shareholders' proportion of the net fair value of

the assets, liabilities and contingent liabilities recognized. Transaction costs, other than

those associated with the issuance of debt and equity securities that the Company incurs in

connection with the business combination, are expensed as incurred.

(e) Foreign currency

The functional currency of the Company is the Canadian dollar. The Company's presentation

currency is the United States (“U.S.”) dollar to allow more direct comparison to peers within

North America.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

11

2. Significant accounting policies (continued)

In preparing the consolidated financial statements of the Company and its subsidiaries,

transactions in currencies other than the respective functional currencies are recorded at the

exchange rates at the dates of the transactions. At the date of each consolidated statement of

financial position, monetary assets and liabilities are translated using the period-end foreign

exchange rate. Non-monetary assets and liabilities are translated using the historical rate on

the date of the transaction. Non-monetary assets and liabilities that are stated at fair value are

translated using the historical rate on the date that the fair value was determined. Revenue

and expense items are translated at average rates of exchange for the year. Foreign currency

differences arising on translation are recognized in net income.

The assets and liabilities of Softchoice U.S. are translated into Canadian dollars at exchange

rates at the reporting date. The income and expenses of Softchoice U.S. are translated into

Canadian dollars at average exchange rates. The assets and liabilities of the Company are

translated into U.S. dollars at exchange rates at the reporting date. The income and expenses

of the Company are translated into U.S. dollars at average exchange rates for the year.

Translation adjustments resulting from this process are recognized in other comprehensive

income (loss) in the cumulative translation account.

(f) Revenue recognition

The Company generates revenue from the sale of computer hardware, software and post

contract customer support. The Company also generates revenue from providing professional

services to end-users, such as data center configuration and the design and development of IT

systems. Sales of product in which the Company acts as a principal are presented on a gross

basis. As a principal, the Company obtains and validates a customer's order, purchases the

product from the supplier at a negotiated price, arranges for shipment of the product, collects

payment from customers, and processes returns. The Company's product is shipped directly to

customers using third-party carriers. Sales of product in which the Company acts as an agent

are presented on a net basis.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

12

2. Significant accounting policies (continued)

(i) Hardware

Revenue from the sale of hardware is recorded when evidence of an arrangement exists,

the product is shipped (Freight on Board ("FOB") shipping point) or received by the

customer (FOB destination), depending upon the customer's arrangement, and collection is

reasonably assured.

(ii) Software licenses

Revenue from the sale of software licenses is recorded when evidence of an arrangement

exists, customers acquire the right to use or copy software under license, but not prior to

the commencement of the initial license term, the price is fixed and determinable and

collection is reasonably assured.

The Company sells subscription licenses and certain software assurance benefits (for

which the Company is not the primary obligor) that are recognized on a net basis. For

sales of licenses where revenue is recognized on a net basis, the Company records the

revenue at the time of sale.

(iii) Post contract customer support

Revenue on maintenance contracts performed by third party vendors is recognized once

the contract date is in effect. As the Company is not the primary obligor for the

maintenance contracts performed by third parties, these arrangements do not meet the

criteria for gross revenue presentation and, accordingly, are recorded on a net basis. As

the Company enters into contracts with third party service providers or vendors, the

Company evaluates whether subsequent sales of such services should be recorded as

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

13

2. Significant accounting policies (continued)

gross revenue or net revenue. The Company determines whether it acts as a principal in

the transaction and assumes the risks and rewards of ownership or if it is simply acting as

an agent or broker. Revenue on maintenance contracts performed by internal resources is

recognized on a gross basis ratably over the term of the maintenance period.

(iv) Professional services

Revenue from professional services is recognized based on the percentage of completion

of the transaction at the reporting date. The stage of completion is assessed by reference

to the actual hours incurred and the budgeted hours needed to complete the project, in

order to measure progress on each contract. Revenue and cost estimates are revised

periodically based on changes in circumstances. Any losses on contracts are recognized

in the period that such losses become known. Revenue from time and materials contracts

is recognized as time is incurred by the Company.

(v) Sales return provision

The Company estimates the level of anticipated sales returns based on historical

experience and records a provision for sales returns. The historical estimate is reviewed

throughout the year to ensure it reflects the most relevant data available.

(vi) Multiple element arrangements

The Company's revenue arrangements may contain multiple elements. These elements

may include one or more of the following: hardware, software, maintenance and/or

professional services such as installation. For arrangements involving multiple elements,

the Company allocates revenue to each component of the arrangement using the relative

selling price method based on market based inputs. The allocated portion of the

arrangement which is undelivered is then deferred. In some instances, a group of contracts

or agreements with the same customer may be so closely related that they are, in effect,

part of a single arrangement and, therefore, the Company will allocate the corresponding

revenue among various components, as described above.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

14

2. Significant accounting policies (continued)

(vii) Deferred revenue

Deferred revenue includes unearned revenue on sales of professional services and

maintenance contracts to customers where performance is not yet complete and where the

contract start date is not yet in effect.

(g) Cost of sales

Cost of sales include product costs, direct costs associated with delivering the services,

outbound and inbound freight costs and provision for inventory losses. These costs are

reduced by rebates and marketing development funds received from vendors, which are

recorded as earned based on the contractual arrangement with the vendor.

(h) Marketing development funds

The Company receives funds from vendors to support the marketing and sale of their products.

When these funds represent the reimbursement of a specific, incremental and identifiable cost,

these funds are netted against the related costs, and excess profits, if any, are recorded as a

reduction of cost of sales. When the funds are not related to specific, incremental and

identifiable costs, the amounts received are recorded as a reduction of cost of sales. Funds

are recorded when the vendor is invoiced and the terms and conditions with the vendor are

complete.

(i) Inventory

Inventory is valued at the lower of cost and net realizable value net of an inventory provision.

Cost of inventory is determined using specific identification of individual cost. The inventory

provision is determined based on historical information and professional judgment.

Inventory comprises of finished goods and work-in-progress. Finished goods comprise spare

parts, hardware purchased for resale and goods awaiting configuration for customers. Work-in-

progress represents the unbilled portion of labour and cost of purchases for services performed

but not yet billed to customers.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

15

2. Significant accounting policies (continued)

(j) Deferred costs

Deferred costs comprise of software license, software maintenance and hardware warranties

where the start date is not yet in effect.

(k) Property and equipment

Property and equipment is recorded at cost less accumulated depreciation and accumulated

impairment loss. Cost includes expenditures that are directly attributable to the acquisition of

an asset. When parts of an item of property and equipment have different useful lives, they are

accounted for as separate components of property and equipment. Gains and losses on

disposal of an item of property and equipment are determined by comparing the proceeds from

disposal with the carrying amount of the property and equipment and are recognized within

other expenses in the consolidated statements of comprehensive income.

The costs of replacing a part of an item of property and equipment is recognized in the carrying

amount of the item if it is probable that the future economic benefits embodied within the part

will flow to the Company and its costs can be measured reliably. The carrying amount of the

replaced part is written off. The costs associated with the day-to-day servicing of property and

equipment are recognized in the consolidated statements of comprehensive income as

incurred.

Depreciation is provided on a straight-line basis over the estimated useful life of property and

equipment, as this most closely reflects the pattern of consumption of the future economic

benefits embodied in the asset. Useful lives are as follows:

Office equipment 3 years Computer equipment 3 years Leasehold improvements Over term of the related lease

Depreciation methods, useful lives and residual values are reviewed at each financial year end

and adjusted if appropriate.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

16

2. Significant accounting policies (continued)

(l) Intangible assets

(i) Goodwill

For measurement of goodwill on initial recognition, see note 2(d)(ii). For subsequent

measurement, goodwill is measured at cost less accumulated impairment losses, see

2(m)(ii) for details of the annual impairment test performed.

(ii) Internally generated intangible assets

Expenditure on research is charged to the consolidated statements of comprehensive

income as incurred.

Development activities involve a plan or design for the production of new or substantially

improved products and processes. Development expenditure is capitalized only if

development costs can be measured reliably, the product or process is technically and

commercially feasible, future economic benefits are probable, and the Company intends to

and has sufficient resources to complete development and to use or sell the asset. The

costs of internally generated intangible assets includes all directly attributed costs

necessary to create, produce and prepare the intangible asset to be capable of operating in

the manner as intended by management. Directly attributable costs comprise salaries and

other employment costs incurred, on a time apportioned basis, on software development.

Capitalized development expenditure is measured at cost less accumulated amortization

and accumulated impairment losses. Internally developed, internal-use software is

included in intangible assets and is recorded at cost, which includes material and direct

labour costs. Amortization of computer software under development commences when the

software is ready for use.

(iii) Other identifiable intangible assets

Other identifiable intangible assets include computer software, customer relationships,

acquired technologies and contracts acquired by the Company and have finite useful lives.

These assets are measured at cost less accumulated amortization and accumulated

impairment losses.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

17

2. Significant accounting policies (continued)

(iv) Subsequent expenditure

Subsequent expenditure is capitalized only when it increases the future economic benefits

embodied in the specific asset to which it relates. All other expenditure, including

expenditure on brands, is recognized as an expense in the consolidated statements of

comprehensive income as incurred.

(v) Amortization

Amortization is recognized in the consolidated statements of comprehensive income on a

straight-line basis over the estimated useful lives of the intangible assets as follows:

Computer software 3 years Acquired technology 5 years Customer relationships 5 - 10 years

(m) Impairment

(i) Financial assets

Financial assets other than those carried at fair value through profit or loss are assessed at

each reporting date to determine whether there is objective evidence of an impairment. A

financial asset is impaired if objective evidence indicates that a loss event has occurred

after the initial recognition of the asset, and that the loss event had a negative effect on the

estimated future cash flows of that asset, in which the cash flows can be estimated reliably.

Objective evidence that financial assets are impaired can include default or delinquency by

a debtor, restructuring of an amount due to the Company on terms that the Company would

not consider otherwise, indications that a debtor or issuer will enter bankruptcy, or the

disappearance of an active market for a security.

The Company maintains an allowance for doubtful accounts at an amount estimated to be

sufficient to provide adequate protection against losses resulting from collecting less than

the full amount due on its accounts receivable. The Company considers evidence of

impairment for receivables at both a specific asset and collective level. All individually

significant receivables are assessed for specific impairment. Individual overdue accounts

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

18

2. Significant accounting policies (continued)

are reviewed, and allowances are recorded to present trade receivables at net realizable

value when it is known that they are not collectible in full.

In assessing collective impairment, the Company uses historical trends of the probability of

default, timing of recoveries, and the amount of loss incurred, adjusted for management's

judgement as to whether current economic and credit conditions are such that the actual

losses are likely to be greater or less than suggested by historical trends.

An impairment loss in respect of a financial asset measured at amortized cost is calculated

as the difference between its carrying amount and the present value of the estimated future

cash flows discounted at the asset's original effective interest rate. Losses are recognized

in the consolidated statements of comprehensive income and reflected in an allowance

account against receivables. Interest on the impaired asset continues to be recognized

through the unwinding of the discount.

(ii) Non-financial assets

The Company's non-financial assets, excluding inventories and deferred tax assets, are

reviewed for an indication of impairment at each reporting date to determine if there are

events or changes in circumstances that indicate the assets might not be recoverable. The

Company is required to estimate the recoverable amount of goodwill annually. If an

indication of impairment exists, the asset's recoverable amount is estimated at the same

date. An impairment loss is recognized when the carrying amount of an asset, or its cash-

generating unit, exceeds its recoverable amount. A cash-generating unit is the smallest

identifiable group of assets that generates cash inflows that are largely independent of the

cash inflows from other assets or groups of assets. Impairment losses are recognized in

the consolidated statements of comprehensive income for the year. Impairment losses

recognized in respect of cash-generating units are allocated first to reduce the carrying

amount of any goodwill allocated to cash generating units and then to reduce the carrying

amount of the other assets in the unit on a pro-rata basis.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

19

2. Significant accounting policies (continued)

The recoverable amount is the greater of the asset's fair value less costs to sell and value

in use. In assessing value in use, the estimated future cash flows from the asset’s eventual

use and eventual disposition are discounted to their present value using a pre-tax discount

rate that reflects current market assessments of the time value of money and the risks

specific to the asset. A terminal value calculation is included to represent the eventual

disposition of the assets. For an asset that does not generate largely independent cash

inflows, the recoverable amount is determined for the cash-generating unit to which the

asset belongs.

Impairment losses, other than those related to goodwill, are evaluated for potential

reversals when events or changes in circumstances warrant such consideration.

(n) Income taxes

Income tax expense comprises current and deferred taxes. Current taxes and deferred taxes

are recognized in the consolidated statements of comprehensive income except to the extent

that they relate to a business combination, or items recognized directly in equity or in other

comprehensive income. Current taxes are the expected tax payable or receivable on the

taxable income or loss for the year, using tax rates substantively enacted at the reporting date,

and any adjustment to tax payable in respect of previous years.

Deferred taxes are recognized in respect of temporary differences between the carrying

amounts of assets and liabilities for financial reporting purposes and the amounts used for

taxation purposes. Deferred taxes are not recognized for the following temporary differences:

(i) the initial recognition of assets or liabilities in a transaction that is not a business

combination and that affects neither accounting nor taxable income;

(ii) differences relating to investments in subsidiaries and jointly controlled entities to the extent

that it is probable that they will not reverse in the foreseeable future; and

(iii) taxable temporary differences arising on the initial recognition of goodwill.

Deferred taxes are measured at the tax rates that are expected to be applied to temporary

differences when they reverse, based on the laws that have been substantively enacted by the

reporting date.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

20

2. Significant accounting policies (continued)

Deferred tax assets and liabilities are offset if there is a legally enforceable right to offset

current tax liabilities and assets, and they relate to income taxes levied by the same tax

authority on the same taxable entity, or on different tax entities, but they intend to settle current

tax liabilities and assets on a net basis or their tax assets and liabilities will be realized

simultaneously.

A deferred tax asset is recognized for unused tax losses, tax credits and deductible temporary

differences, to the extent that it is probable that future taxable profits will be available against

which they can be utilized. Deferred tax assets are reviewed at each reporting date and are

reduced to the extent that it is no longer probable that sufficient taxable profit will be available

to allow the benefit to be realized.

(o) Net earnings per share

Basic net earnings per share are computed by dividing the net income for the period,

attributable to common shareholders of the Company, by the weighted average number of

common shares outstanding during the period, adjusted for own shares held. Diluted earnings

per share are computed using the treasury stock method whereby the weighted average

number of common shares used in the basic net earnings per share calculation is increased to

include the number of additional common shares that would have been outstanding if the

dilutive potential common shares had been issued at the beginning of the period, adjusted for

own shares held. Potential common shares represent the common shares issuable upon the

exercise of stock options. Potential common shares are excluded from the calculation if their

effect is anti-dilutive.

(p) Employee future benefits

(i) Defined contribution plan

The Company sponsors a Canadian RRSP (“RRSP”) and a U.S. 401K plan (“401K”) which

are defined contribution plans for employees of the Company. Under the RRSP, employees

may contribute up to 6% of their compensation and make additional contributions subject to

certain limits based on Canadian federal tax laws. The Company contributes 50% of the

employee’s contributions up to 3% of the employee’s compensation. Under the 401K, the

Company pays fixed contributions to a separate entity and has no legal or constructive

obligation to pay further amounts. Employees may contribute subject to certain limits

based on U.S. federal tax laws. The Company contributes 50% of the employee’s

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

21

2. Significant accounting policies (continued)

contributions up to 3% of the employee's total compensation. The Company's contributions

vest 50% after two years of enrolment in the plan but before three years, 75% after three

years of enrolment in the plan but before four years, and 100% after four years.

Contributions under these plans are recognized as an employee benefit expense in net

income in the periods during which services are rendered by employees.

(ii) Termination benefits

Termination benefits are generally payable when employment is terminated before the

normal retirement date or whenever an employee accepts voluntary redundancy in

exchange for these benefits. The Company recognizes termination benefits when it is

demonstrably committed to either terminating the employment of current employees

according to a detailed formal plan without realistic possibility of withdrawal or providing

termination benefits as a result of an offer made to encourage voluntary redundancy. If

benefits are payable more than 12 months after the reporting period, then they are

discounted to their present value.

(iii) Short-term employee benefits

Liabilities for bonuses and profit-sharing are recognized based on a formula that takes into

consideration the profit attributable to the Company's shareholders after certain

adjustments. The Company recognizes a provision when contractually obliged to do so or

where there is a past practice that has created a constructive obligation to make such

compensation payments, and the obligation can be estimated reliably.

(iv) Share-based compensation plans

1. Performance stock options (“PSO”) plan

The Company offers stock-based compensation to key employees and non-executive

directors. The Company accounts for the PSO plan, which calls for settlement by the

issuance of equity instruments using the fair value method. Under the fair value

method, compensation cost attributed to the options to employees is measured at fair

value at the grant date and amortized over the vesting period. The amount recognized

as an expense is adjusted to reflect the number of awards for which the related service

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

22

2. Significant accounting policies (continued)

and non-market vesting conditions are expected to be met, if applicable, which is based

on the number of awards that meet the related service and non-market performance

conditions at the vesting date.

2. Share appreciation rights (“SAR”) plan

Compensation cost is recognized so that each tranche in an award with graded vesting

is considered as a separate grant with a different vesting date and fair value. No

compensation cost is recognized for options that employees forfeit if they fail to satisfy

the service requirement for vesting. Share-based payment expense relating to cash-

settled awards is accrued at the fair value of the liability. Until the liability is settled, the

Company re-measures the fair value at the end of each reporting period and at the date

of settlement, with any changes in fair value recognized in the consolidated statements

of comprehensive income over the vesting period.

3. Restricted share units (“RSU”) plan

The Company accounts for restricted share units based on fair value. No compensation

cost is recognized for RSUs that employees forfeit if they fail to satisfy the service

requirement for vesting. Share-based payment expense relating to these cash-settled

awards is accrued at the fair value of the liability. Until the liability is settled, the

Company re-measures the fair value at the end of each reporting period and at the date

of settlement, with any changes in fair value recognized in the consolidated statements

of comprehensive income over the vesting period.

4. Deferred share units (“DSU”) plan

The Company accounts for deferred share units granted to its non-management

directors based on the fair value of the equity instruments. When options are

exercised, the proceeds received by the Company, together with the fair value amount

in contributed surplus, are credited to capital stock.

(q) Provisions

(i) Legal or constructive obligations

Provisions are recognized when the Company has a present legal or constructive

obligation that has arisen as a result of a past event and it is probable that a future outflow

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

23

2. Significant accounting policies (continued)

of resources will be required to settle the obligation, provided that a reliable estimate can

be made of the amount of the obligation. Provisions are measured at the present value of

the expenditures expected to be required to settle the obligation using a pre-tax rate that

reflects current market assessments of the time value of money and the risk specific to the

obligation. The increase in the provision due to the passage of time is recognized as

interest expense.

(ii) Onerous lease contracts

Onerous lease contracts include contracts in which the unavoidable costs of meeting the

obligations under the contract exceed the economic benefits expected to be received under

the contract.

(r) Leases

Leases are classified as either operating or finance, based on whether the risks and rewards of

ownership are transferred to the Company at the inception of the lease.

Operating leases

Payments made under operating leases, net of any incentives received by the lessor, are

recognized in the consolidated statements of comprehensive income on a straight-line basis

over the term of the lease. Operating leases are not recognized in the Company's statements

of financial position.

(s) Segment reporting

The Company has one reportable segment in which the assets, operations and employees are

located in Canada and the United States. The Company is a North American provider of IT

hardware, software and services to small, medium and large businesses and public sector

institutions.

(t) Finance costs

Finance costs comprise foreign exchange losses, interest expense on loans and borrowings

and amortization of deferred financing costs using the effective interest rate method. Borrowing

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

24

2. Significant accounting policies (continued)

costs that are not directly attributable to the acquisition, construction or production of a

qualifying asset are recognized in the consolidated statements of comprehensive income using

the effective interest method.

(u) Finance income

Finance income comprises foreign exchange gains, interest income on cash balances,

customer finance income, miscellaneous other revenue, and changes in the fair value of

financial assets at fair value through profit or loss. Interest income is recognized as it accrues

in the consolidated statements of comprehensive income, using the effective interest method.

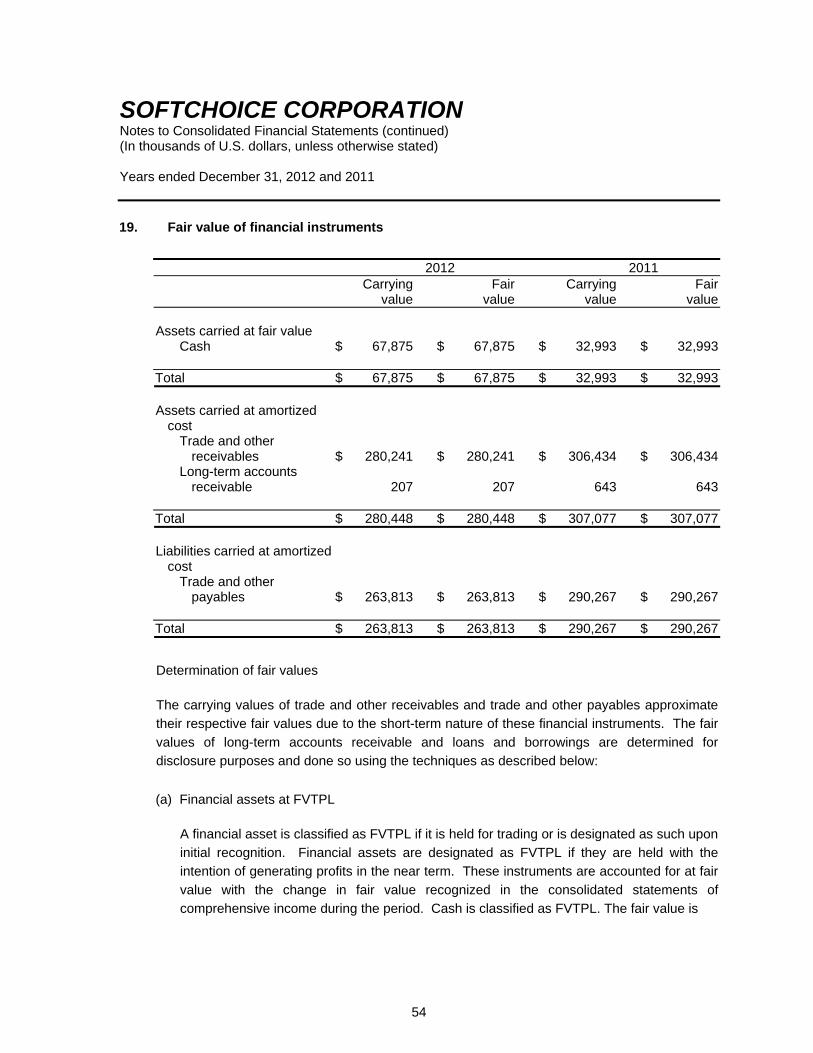

(v) Financial instruments

(i) Fair value hierarchy The fair value hierarchy establishes three levels to classify the inputs to valuation techniques used to measure fair value. Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or

liabilities.

Level 2 inputs are quoted prices in markets that are not active, quoted prices for similar assets or liabilities in active markets, inputs other than quoted prices that are observable for the asset or liability or inputs that are derived principally from or corroborated by observable market data or other means.

Level 3 inputs are unobservable (supported by little or no market activity).

The fair value hierarchy gives the highest priority to Level 1 inputs and the lowest priority to Level 3 inputs.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

25

2. Significant accounting policies (continued)

(ii) Non-derivative financial assets

The Company recognizes trade and other receivables and cash on the date that they are

originated. All other financial assets (including assets designated as fair value through

profit or loss) are recognized initially on the trade date at which the Company becomes a

party to the contractual provisions of the instrument. The Company derecognizes a

financial asset when the contractual rights to the cash flows from the asset expire, or it

transfers the rights to receive the contractual cash flows on the financial asset in a

transaction in which substantially all the risks and rewards of ownership of the financial

asset are transferred. Any interest in transferred financial assets that is created or retained

by the Company is recognized as a separate asset or liability. Financial assets and

liabilities are offset and the net amount presented in the statement of financial position

when the Company has a legal right to offset the amounts and intends either to settle on a

net basis or to realize the asset and settle the liability simultaneously. The Company has

adopted the following policies for non-derivative financial assets:

1. Fair value through profit or loss ("FVTPL")

A financial asset is classified as FVTPL if it is held for trading or is designated as

such upon initial recognition. Financial assets are designated as FVTPL if they

are held with the intention of generating profits in the near term. These

instruments are accounted for at fair value with the change in fair value

recognized in the consolidated statements of comprehensive income during the

year. Cash and restricted cash are classified as FVTPL.

2. Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or

determinable payments that are not quoted in an active market. Such assets are

initially recognized at cost less any transaction costs. Subsequent to initial

recognition, loans and receivables are measured at amortized cost using the

effective interest method, less any impairment losses. Trade and other

receivables and long-term accounts receivable are classified under this category.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

26

2. Significant accounting policies (continued)

(iii) Non-derivative financial liabilities

The Company recognizes subordinated liabilities on the date that they are originated. Such

financial liabilities are recognized initially at fair value plus any directly attributable

transaction costs. Subsequent to initial recognition, these financial liabilities are measured

at amortized cost using the effective interest method. A financial liability is derecognized

when its contractual obligation is discharged. The Company has the following non-

derivative financial liabilities: loans and borrowings and trade and other payables.

(iv) Embedded derivatives

Derivatives may be embedded in other financial and non-financial instruments (the "host

instrument"). Embedded derivatives are treated as separate derivatives when their

economic characteristics and risks are not clearly and closely related to those of the host

instrument, the terms of the embedded derivative are the same as those of a stand-alone

derivative, and the combined contract is not held for trading or designated at fair value.

These embedded derivatives are measured at fair value with subsequent changes

recognized in the statement of comprehensive income as an element of administrative

expenses.

The Company did not enter into any derivative financial instrument contracts during 2012

and 2011. In addition, there were no outstanding derivative financial instruments as at

December 31, 2012 and 2011.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

27

2. Significant accounting policies (continued)

(w) New standards and interpretations yet to be adopted

At the date of authorization of these consolidated financial statements, the IASB has issued the

following new and revised standards and amendments which are not yet effective for the

relevant reporting periods:

(i) IFRS 9, Financial Instruments ("IFRS 9")

In November 2009, the International Accounting Standards Board ("the IASB") issued IFRS

9 Financial Instruments (“IFRS 9”) as part of the first phase of its project to replace IAS 39

Financial Instruments: Recognition and Measurement. The standard released in 2009

establishes the classification and measurement of financial assets: amortized cost and fair

value. In October 2010, the IASB amended IFRS 9 for added disclosures about

investments in equity instruments measured at fair value in Other Comprehensive Income,

and included guidance on the classification and measurement of financial liabilities. In

December 2011, the IASB issued an amendment to IFRS 9 to defer the mandatory

effective date to annual periods beginning on or after January 1, 2015, with early adoption

permitted. The Company intends to adopt IFRS 9 in its financial statements for the annual

period beginning on January 1, 2015. The Company is currently assessing the impact of

adoption of IFRS 9. The extent of the impact of adoption of IFRS 9 has not yet been

determined.

(ii) IFRS 13, Fair Value Measurement (“IFRS 13”)

IFRS 13, Fair Value Measurement ("IFRS 13"), which is applicable to annual reporting

periods beginning on or after January 1, 2013, defines fair value, sets out in a single IFRS

framework for measuring fair value, and requires disclosures about fair value

measurements. The Company intends to adopt IFRS 13 prospectively in its interim

consolidated financial statements for the annual period beginning on January 1, 2013. The

application of these standards is not expected to have a material impact on the Company.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

28

2. Significant accounting policies (continued)

(iii) IAS 1, Presentation of Financial Statements: Presentation of Items of Other

Comprehensive Income (“IAS 1”)

In June 2011, the IASB published amendments to IAS 1, Presentation of Financial

Statements: Presentation of Items of Other Comprehensive Income ("IAS 1"), which are

effective for annual periods beginning on or after July 1, 2012. The amendments require

that an entity present separately the items of other comprehensive income that may be

reclassified to profit or loss in the future from those that would never be reclassified to profit

or loss. The Company intends to adopt the amendments in the interim consolidated

financial statements for the annual period beginning on January 1, 2013. As the

amendments only require changes in the presentation of items in other comprehensive

income, the Company does not expect the amendment to IAS 1 to have material impact on

the consolidated financial statements.

(iv) IFRS 10, Consolidated Financial Statements (“IFRS 10”) and amended IAS 27 (2011),

Separate Financial Statements

IFRS 10 requires an entity to consolidate an investee when it is exposed, or has rights, to

variable returns from its involvement with the investee and has the ability to affect those

returns through its power over the investee. Under existing IFRS, consolidation is required

when an entity has the power to govern the financial and operating policies of an entity so

as to obtain benefits from its activities. The Company intends to adopt this standard and

amendment in the interim consolidated financial statements for the annual period beginning

on January 1, 2013. The application of these standards will not to have a material impact

on the Company.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

29

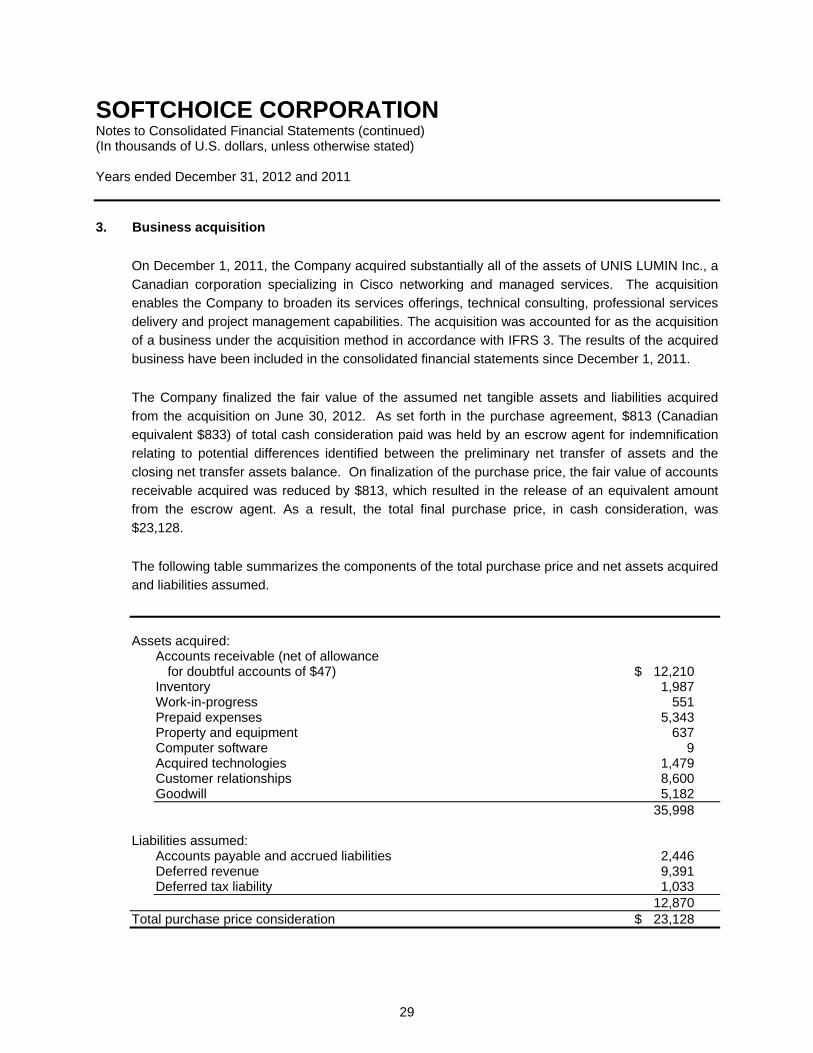

3. Business acquisition

On December 1, 2011, the Company acquired substantially all of the assets of UNIS LUMIN Inc., a

Canadian corporation specializing in Cisco networking and managed services. The acquisition

enables the Company to broaden its services offerings, technical consulting, professional services

delivery and project management capabilities. The acquisition was accounted for as the acquisition

of a business under the acquisition method in accordance with IFRS 3. The results of the acquired

business have been included in the consolidated financial statements since December 1, 2011.

The Company finalized the fair value of the assumed net tangible assets and liabilities acquired

from the acquisition on June 30, 2012. As set forth in the purchase agreement, $813 (Canadian

equivalent $833) of total cash consideration paid was held by an escrow agent for indemnification

relating to potential differences identified between the preliminary net transfer of assets and the

closing net transfer assets balance. On finalization of the purchase price, the fair value of accounts

receivable acquired was reduced by $813, which resulted in the release of an equivalent amount

from the escrow agent. As a result, the total final purchase price, in cash consideration, was

$23,128.

The following table summarizes the components of the total purchase price and net assets acquired

and liabilities assumed.

Assets acquired:

Accounts receivable (net of allowance for doubtful accounts of $47) $ 12,210

Inventory 1,987 Work-in-progress 551 Prepaid expenses 5,343 Property and equipment 637 Computer software 9 Acquired technologies 1,479 Customer relationships 8,600 Goodwill 5,182 35,998

Liabilities assumed:

Accounts payable and accrued liabilities 2,446 Deferred revenue 9,391 Deferred tax liability 1,033 12,870

Total purchase price consideration $ 23,128

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

30

3. Business acquisition (continued)

The goodwill recognized as a result of the acquisition is attributable to synergies with existing

businesses and other intangibles that do not qualify for separate recognition. The total amount of

goodwill expected to be deductible for tax purposes is $4,255.

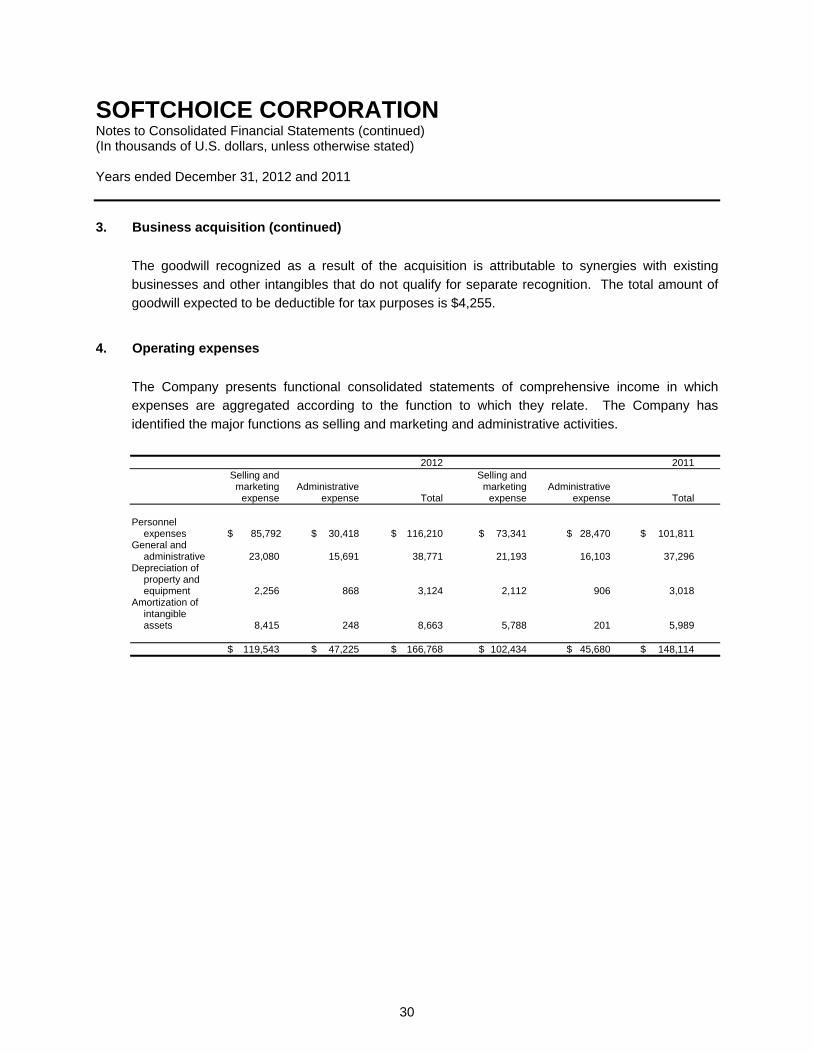

4. Operating expenses

The Company presents functional consolidated statements of comprehensive income in which

expenses are aggregated according to the function to which they relate. The Company has

identified the major functions as selling and marketing and administrative activities.

2012 2011 Selling and Selling and marketing Administrative marketing Administrative expense expense Total expense expense Total Personnel

expenses $ 85,792 $ 30,418 $ 116,210 $ 73,341 $ 28,470 $ 101,811 General and

administrative 23,080 15,691 38,771 21,193 16,103 37,296 Depreciation of

property and equipment 2,256 868 3,124 2,112 906 3,018

Amortization of intangible assets 8,415 248 8,663 5,788 201 5,989

$ 119,543 $ 47,225 $ 166,768 $ 102,434 $ 45,680 $ 148,114

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

31

4. Operating expenses (continued)

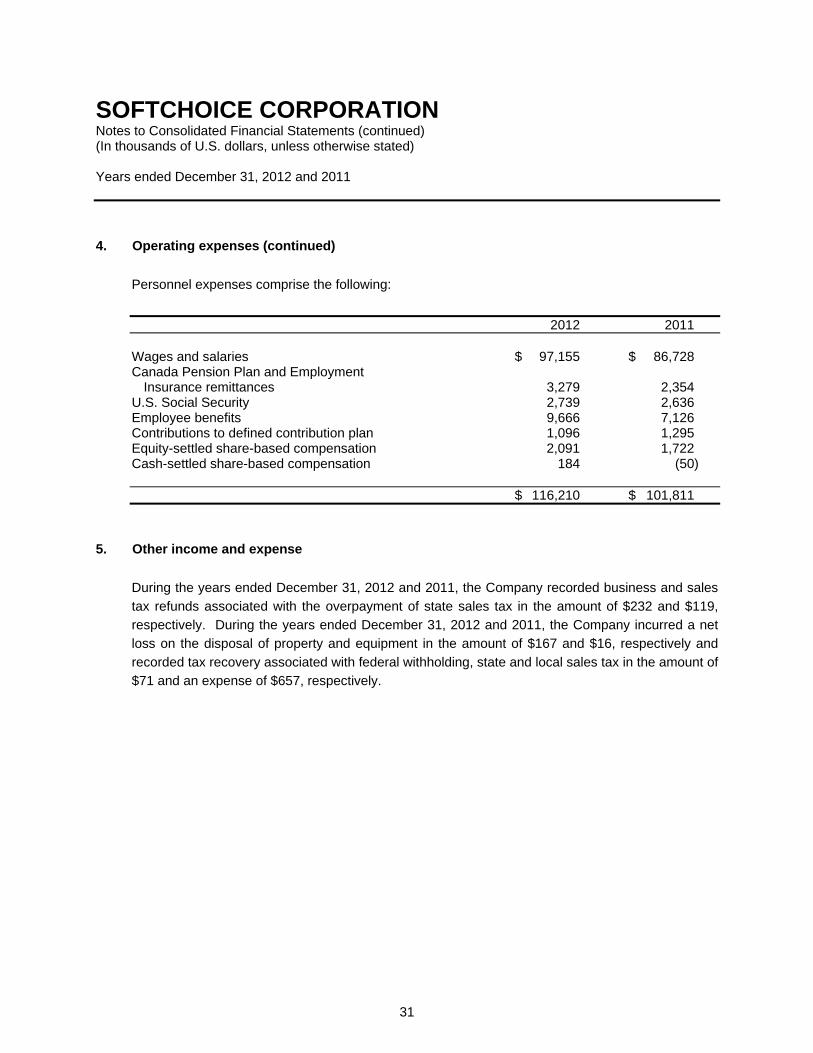

Personnel expenses comprise the following:

2012 2011 Wages and salaries $ 97,155 $ 86,728 Canada Pension Plan and Employment

Insurance remittances 3,279 2,354 U.S. Social Security 2,739 2,636 Employee benefits 9,666 7,126 Contributions to defined contribution plan 1,096 1,295 Equity-settled share-based compensation 2,091 1,722 Cash-settled share-based compensation 184 (50) $ 116,210 $ 101,811

5. Other income and expense

During the years ended December 31, 2012 and 2011, the Company recorded business and sales

tax refunds associated with the overpayment of state sales tax in the amount of $232 and $119,

respectively. During the years ended December 31, 2012 and 2011, the Company incurred a net

loss on the disposal of property and equipment in the amount of $167 and $16, respectively and

recorded tax recovery associated with federal withholding, state and local sales tax in the amount of

$71 and an expense of $657, respectively.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

32

6. Finance costs

The components of finance costs include interest expense and other financing costs as follows:

2012 2011 Interest expense on financial liabilities

measured at amortized cost: Asset-backed loan ("ABL") (note 14) $ 52 $ 110 ABL line of credit standby fees 471 615 Term debt (note 14) – 1,730 Amortization of deferred financing costs – 1,844 Interest expense on other trade payables 5 4 Net foreign exchange loss on financing activities – 1,332 Financing transaction costs – 534

$ 528 $ 6,169

7. Finance income

The components of finance income include:

2012 2011 Net foreign exchange gain on financing activities $ 1,114 $ – Interest income on loans and receivables 175 82 $ 1,289 $ 82

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

33

8. Income tax expense and deferred income taxes

(a) The components of current and deferred tax expense for 2012 and 2011 were as follows:

2012 2011 Current income tax expense (recovery):

For current reporting period $ 12,614 $ 13,254 Consequential adjustments from retroactive change in tax legislation 655 –

13,269 13,254 Deferred tax expense (recovery):

Arising from the origination and reversal of temporary differences 520 (1,247)

$ 13,789 $ 12,007

(b) Reconciliation of effective tax rate:

2012 2011 Income tax using the

Company's domestic tax rate 26.40% $ 10,943 28.07% $ 9,579

Effect of tax rates in foreign jurisdictions 5.45% 2,255 5.11% 1,744

Tax rate differential on, and consequential adjustments from, retroactive change in tax legislation 1.59% 655 – % – Permanent differences (0.16)% (64) 2.00% 684 33.28% 13,789 35.18% $ 12,007

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

34

8. Income tax expense and deferred income taxes (continued)

(c) Unrecognized deferred tax liability

At December 31, 2012 and 2011, a deferred tax liability of $3,938 and $3,458 for temporary

differences of $78,762 and $69,157, respectively, related to undistributed net income from an

investment in a subsidiary, was not recognized because the Company controls whether the

liability will be incurred and it is satisfied that it will not be incurred in the foreseeable future.

(d) Temporary differences

Temporary differences comprising the deferred tax asset and the amounts of deferred income

tax expense recognized in the consolidated statements of comprehensive income for each

temporary difference are estimated as follows:

Foreign January 1, Recognized in exchange December 31, 2012 Net income adjustments 2012 Property and equipment $ 684 $ (16) $ (1) $ 667 Goodwill 12,585 (994) 11 11,602 Intangible assets 1,977 712 9 2,698 Deferred costs 603 (278) 11 336 Unrealized foreign exchange (472) 506 (34) – Other 3,847 (450) 8 3,405 Deferred tax asset $ 19,224 $ (520) $ 4 $ 18,708

Foreign Business January 1, Recognized in exchange acquisitions December 31, 2011 Net income adjustments and other 2011 Property and equipment $ 808 $ (84) $ (40) $ – $ 684 Goodwill 13,606 (1,031) 10 – 12,585 Intangible assets 2,300 380 (48) (655) 1,977 Deferred costs 416 171 16 – 603 Unrealized foreign exchange (938) 388 78 – (472) Other 2,831 1,451 (57) (378) 3,847 Deferred tax asset $ 19,023 $ 1,275 $ (41) $ (1,033) $ 19,224

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

35

9. Cash

Cash consists of cash on hand and cash balances with major financial institutions. Bank

overdrafts are included in bank indebtedness and as of December 31, 2012 and 2011, no

amount is outstanding.

10. Trade and other receivables

Trade and other receivables comprise the following:

2012 2011 Trade receivables, net of allowance for doubtful Accounts (note 20) $ 260,617 $ 277,757 Trade receivables due from

related parties (note 21) – 227 Other receivables(i) 19,624 28,450 $ 280,241 $ 306,434 Long-term trade accounts receivable $ 207 $ 643 (i)

Other receivables include vendor rebates, marketing co-op, commissions and hardware referral receivables.

11. Inventories

Inventories comprise the following:

2012 2011 Finished goods, net of inventory provision $ 3,083 $ 8,407 Work-in-progress 753 465 $ 3,836 $ 8,872

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

36

11. Inventories (continued) During the year ended December 31, 2012, inventory in the amount of $222 (2011 - $72) was

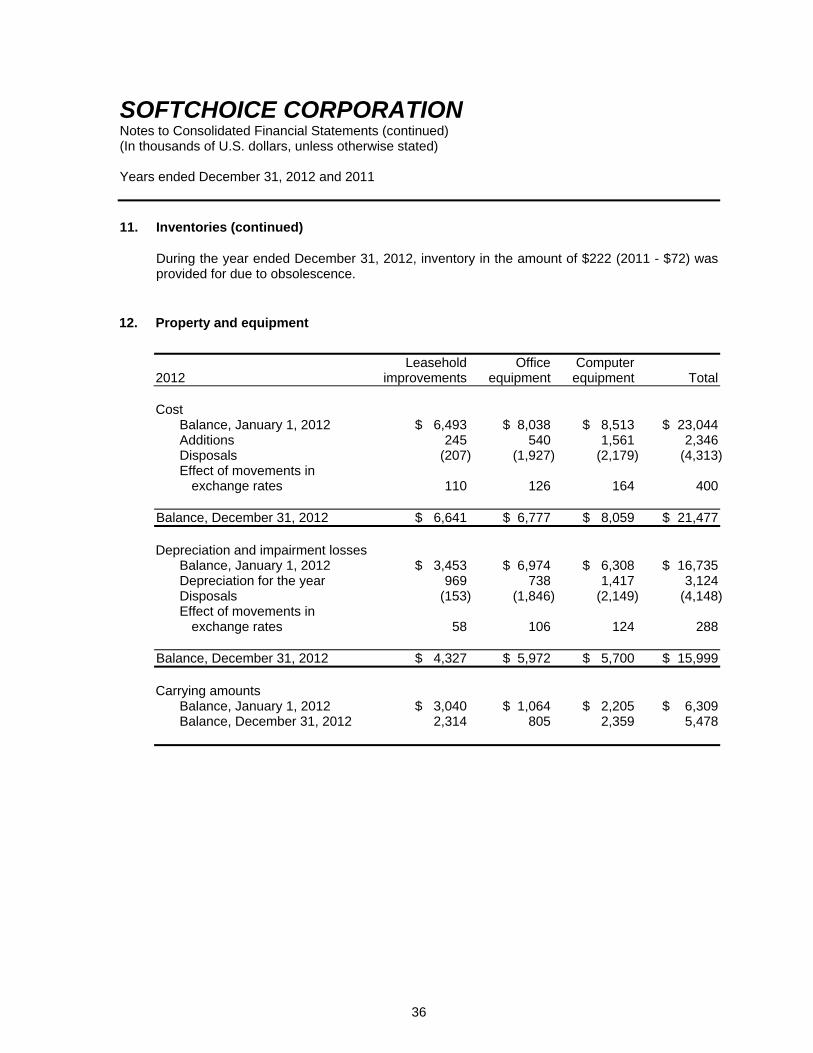

provided for due to obsolescence. 12. Property and equipment

Leasehold Office Computer 2012 improvements equipment equipment Total Cost

Balance, January 1, 2012 $ 6,493 $ 8,038 $ 8,513 $ 23,044 Additions 245 540 1,561 2,346 Disposals (207) (1,927) (2,179) (4,313) Effect of movements in

exchange rates 110 126 164 400 Balance, December 31, 2012 $ 6,641 $ 6,777 $ 8,059 $ 21,477 Depreciation and impairment losses

Balance, January 1, 2012 $ 3,453 $ 6,974 $ 6,308 $ 16,735 Depreciation for the year 969 738 1,417 3,124 Disposals (153) (1,846) (2,149) (4,148) Effect of movements in

exchange rates 58 106 124 288

Balance, December 31, 2012 $ 4,327 $ 5,972 $ 5,700 $ 15,999 Carrying amounts

Balance, January 1, 2012 $ 3,040 $ 1,064 $ 2,205 $ 6,309 Balance, December 31, 2012 2,314 805 2,359 5,478

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

37

12. Property and equipment (continued)

Leasehold Office Computer 2011 improvements equipment equipment Total Cost or deemed cost

Balance, January 1, 2011 $ 5,623 $ 7,117 $ 7,173 $ 19,913 Acquisitions through business

combinations 204 306 127 637 Additions 775 798 1,376 2,949 Disposals (4) (70) – (74) Effect of movements in

foreign exchange rates (105) (113) (163) (381) Balance, December 31, 2011 $ 6,493 $ 8,038 $ 8,513 $ 23,044 Depreciation and impairment losses

Balance, January 1, 2011 $ 2,407 $ 6,573 $ 5,185 $ 14,165 Depreciation for the year 1,206 572 1,240 3,018 Disposals (4) (70) – (74) Effect of movements in

foreign exchange rates (156) (101) (117) (374)

Balance, December 31, 2011 $ 3,453 $ 6,974 $ 6,308 $ 16,735 Carrying amounts

Balance, January 1, 2011 $ 3,216 $ 544 $ 1,988 $ 5,748 Balance, December 31, 2011 3,040 1,064 2,205 6,309

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

38

13. Goodwill and intangible assets

Computer Deferred software Customer Acquired Computer transaction under Total 2012 Goodwill contracts technologies software costs development intangibles

Cost Balance, January 1, 2012 $16,441 $ 70,469 $ 1,484 $ 9,715 $ 3,779 $ 1,930 $ 87,377 Additions – – – 224 – 2,339 2,563 Transfers – – – 1,241 – (1,241) – Disposals – (7,723) – (766) (3,817) – (12,306) Effect of movements in

foreign exchange rates 255 660 33 243 38 33 1,007

Balance, December 31, 2012 $16,696 $ 63,406 $ 1,517 $10,658 $ – $ 3,061 $ 78,641

Amortization and impairment losses Balance, January 1, 2012 $ – $ 29,743 $ 25 $ 7,627 $ 3,779 $ – $ 41,174 Amortization for the year – 7,208 302 1,153 – – 8,663 Disposals – (7,723) – (770) (3,817) – (12,310) Effect of movements in

foreign exchange rates – 330 2 173 38 – 543

Balance, December 31, 2012 $ – $ 29,558 $ 329 $ 8,183 $ – $ – $ 38,070

Carrying amounts Balance, January 1, 2012 $16,441 $ 40,726 $ 1,459 $ 2,088 $ – $ 1,930 $ 46,203 Balance, December 31, 2012 16,696 33,848 1,188 2,474 – 3,061 40,571

Computer Deferred software Customer Acquired Computer transaction under Total 2011 Goodwill contracts technologies software costs development intangibles

Cost Balance, January 1, 2011 $11,383 $ 62,284 $ – $ 8,018 $ 3,861 $ 1,262 $ 75,425 Acquisitions through

business combinations 5,182 8,600 1,479 9 – – 10,088 Additions – – – 205 – 2,415 2,620 Transfers – – – 1,705 – (1,705) – Disposals – – – – – (16) (16) Effect of movements in

foreign exchange rates (124) (415) 5 (222) (82) (26) (740)

Balance, December 31, 2011 $ 16,441 $ 70,469 $ 1,484 $ 9,715 $ 3,779 $ 1,930 $ 87,377

Amortization and impairment losses Balance, January 1, 2011 $ – $ 24,425 $ – $ 7,369 $ 2,476 $ – $ 34,270 Amortization for the year – 5,610 25 354 1,392 – 7,381 Effect of movements in

foreign exchange rates – (292) – (96) (89) – (477)

Balance, December 31, 2011 $ – $ 29,743 $ 25 $ 7,627 $ 3,779 $ – $ 41,174

Carrying amounts Balance, January 1, 2011 $11,383 $ 37,859 $ – $ 649 $ 1,385 $ 1,262 $ 41,155 Balance, December 31, 2011 16,441 40,726 1,459 2,088 – 1,930 46,203

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

39

13. Goodwill and intangible assets (continued)

(a) Impairment testing for CGUs containing goodwill:

The aggregate carrying amounts of goodwill allocated to each CGU are as follows:

2012 2011 Canada $ 11,761 $ 11,506 United States 4,935 4,935 Balance, end of year $ 16,696 $ 16,441

(b) Impairment test of goodwill

The Company has identified two CGUs, Canada and United States, which are defined as

one operating segment based on geographical location and represent the lowest level

within the Company at which goodwill is monitored for internal management purposes.

During the year ended December 31, 2011, the Company acquired the net assets of UNIS

LUMIN Inc. (note 3), which resulted in the addition of goodwill in the amount of $5,182.

This goodwill is allocated to Canada.

The Company performs its annual test for goodwill impairment in the fourth quarter of each

calendar year in accordance with its policy described in note 2(m)(ii). The recoverable

amount of a CGU is based upon value in use calculations. The recoverable amount of all

CGUs exceeded their carrying values, and as a result, no goodwill impairment was

recorded.

The valuation techniques, significant assumptions and sensitivities applied in the goodwill

impairment test are described below:

(i) Valuation techniques

The Company did not make any changes to the valuation methodology used to assess

goodwill impairment since the last annual impairment test.

SOFTCHOICE CORPORATION Notes to Consolidated Financial Statements (continued) (In thousands of U.S. dollars, unless otherwise stated) Years ended December 31, 2012 and 2011

40

13. Goodwill and intangible assets (continued)

Value in use was determined by discounting future cash flows generated from the

continuing use of the CGUs. The discounting process uses a rate of return that is

commensurate with the risk associated with the business or asset and the time value of

money. This approach requires assumptions about revenue growth rates, operating

margins and discount rates.

(ii) Significant assumptions

(a) Growth

The assumptions used were based on the Company's internal forecasts. Cash

flows were projected for a period of three years based on past experience, actual